Craft Vodka Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.57 Billion |

| Market Size (2031) | USD 8.55 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

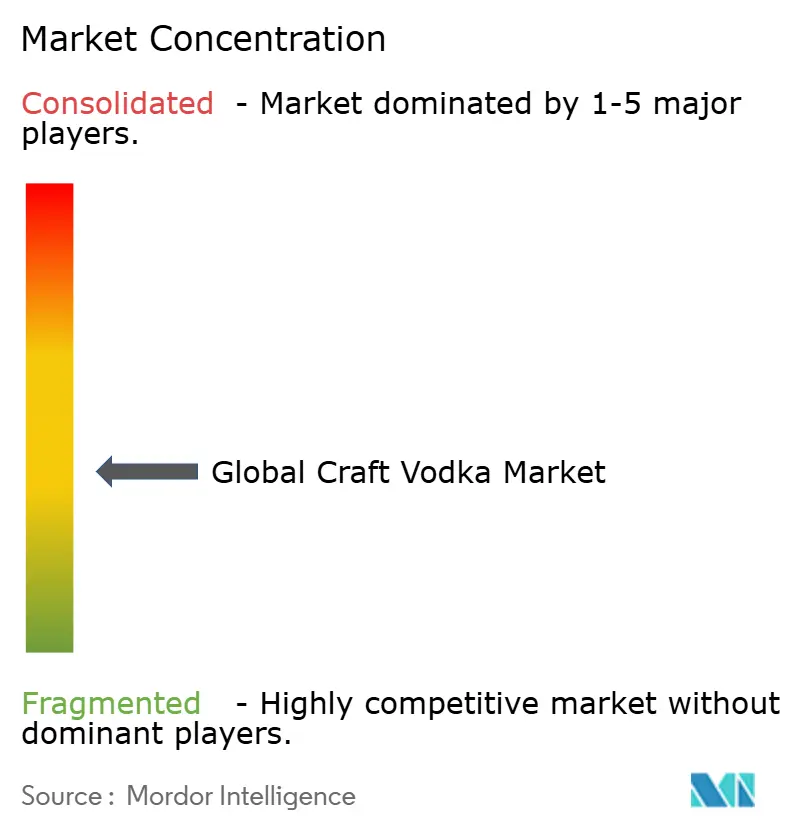

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Craft Vodka Market Analysis by Mordor Intelligence

The craft vodka market size is expected to grow from USD 6.23 billion in 2025 to USD 6.57 billion in 2026 and is forecast to reach USD 8.55 billion by 2031 at 5.42% CAGR over 2026-2031. Rising disposable incomes, a global premiumization trend in beverage alcohol, and stronger direct-to-consumer legislation are steering consumers toward small-batch labels that emphasize provenance, transparency, and sensory complexity. North America remains the largest regional base, benefiting from a mature distribution infrastructure. Europe is the fastest-growing territory as the craft vodka market converts cocktail culture, tourism, and sustainability priorities into shelf gains. Flavor innovation, alternative raw materials, and digital engagement help younger, independent distillers capture occasions historically dominated by mass-market brands. Supply-side momentum is reinforced by small producer tax relief in the United Kingdom and expanded tasting-room privileges in California, bolstering cash-flow resilience.

Key Report Takeaways

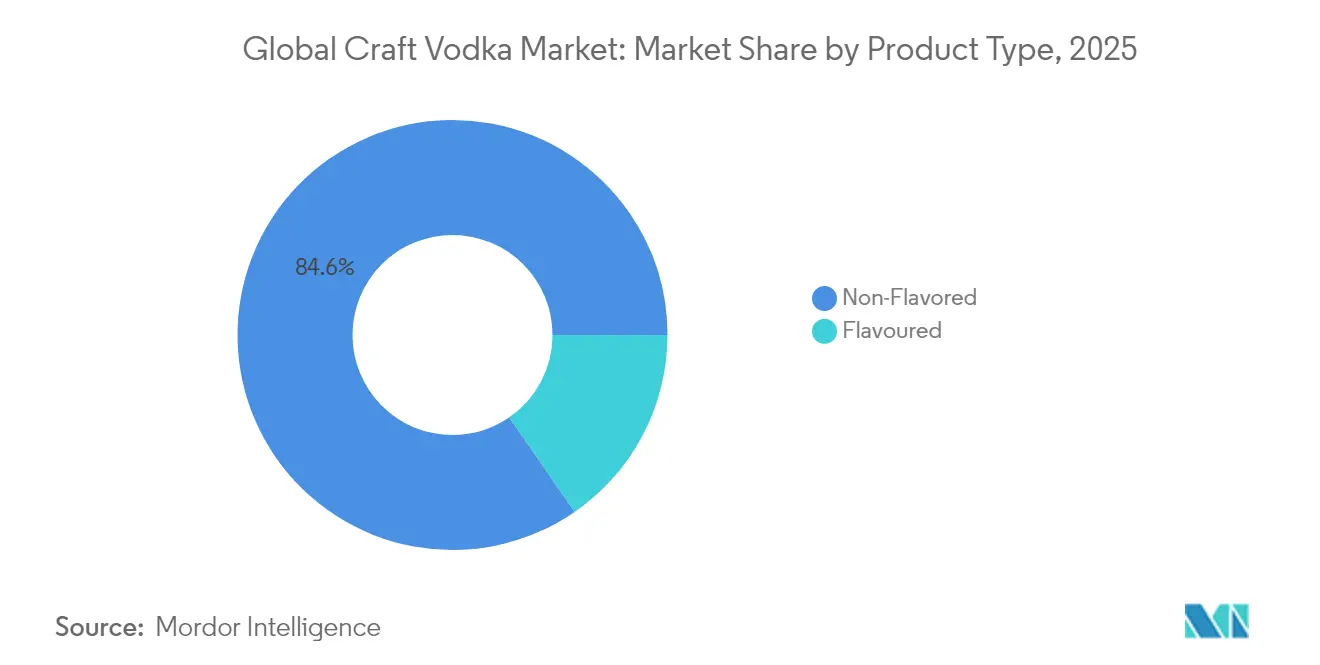

- By product type, non-flavored spirits held 84.62% of the craft vodka market share in 2025, while flavored variants are forecast to grow at a 5.85% CAGR through 2031.

- By raw material, grain-based output accounted for 68.92% of the craft vodka market size in 2025; alternative substrates are projected to climb 6.21% annually to 2031.

- By end user, men represented 68.96% of consumption in 2025, yet women are set to rise at a 6.52% CAGR, the segment’s fastest pace.

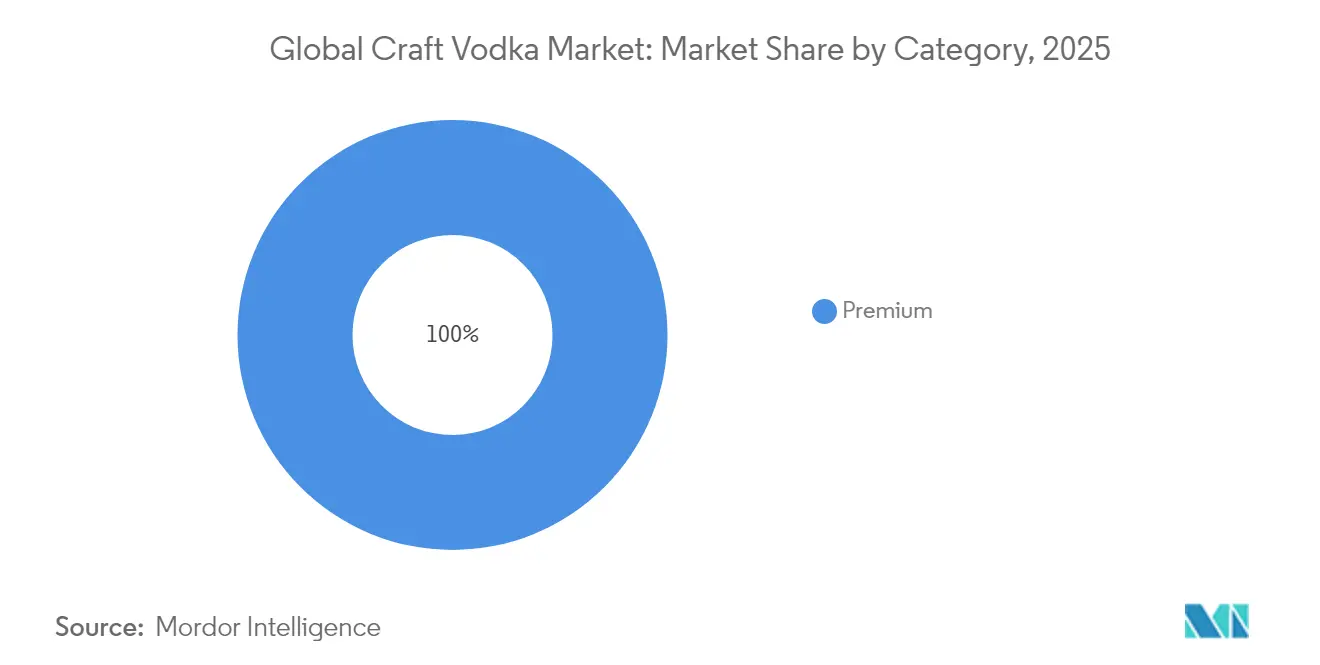

- By category, mass-market labels captured 58.05% revenue in 2025, whereas premium offerings are poised to accelerate at a 7.11% CAGR to 2031.

- By distribution channel, off-trade commanded 85.73% revenue in 2025; on-trade is recovering at a 5.66% CAGR to 2031 as hospitality volumes rebound.

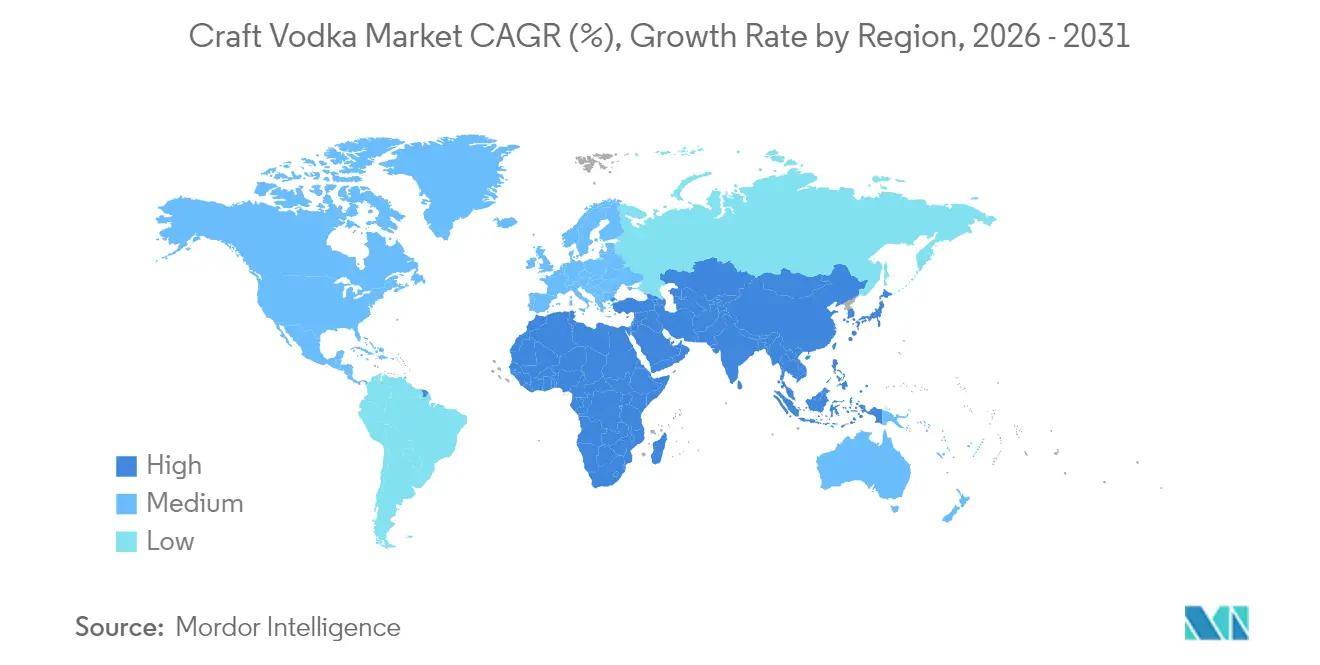

- By geography, North America led with 38.12% of craft vodka market share in 2025, while Europe will advance at a 7.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Craft Vodka Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing number of microbreweries propelling the demand for craft spirits | +1.2% | North America and Europe | Medium term (2-4 years) |

| Technological advancement in terms of production | +0.8% | Global | Long term (≥4 years) |

| Innovation in flavor and ingredients | +0.9% | Global, early gains in North America | Short term (≤2 years) |

| Growing tourism and hospitality sector | +0.7% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Sustainability and ethical sourcing | +0.6% | Europe and North America | Long term (≥4 years) |

| Strategic expansion by pub and bar chains | +0.5% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing number of microbreweries propelling the demand for craft spirits

In the United States, the extensive presence of microbreweries is shaping the business landscape for emerging vodka brands. The integration of overlapping supply chains, community-driven storytelling, and engaging tasting-room experiences, key features of the microbrewery ecosystem, is now streamlining market entry for new vodka producers. For small-scale distillers targeting regional growth, shared distributor networks and retail shelf arrangements originally tailored for craft beer have significantly reduced entry barriers. States with a high concentration of breweries, such as Kentucky, highlight the strategic benefits of clustering. These regions provide access to skilled labor pools, established adjunct ingredient contracts, and robust tourism circuits, all of which enhance the visibility and marketability of local spirits. Furthermore, consumers accustomed to seeking limited-edition products are finding similar value in single-estate vodkas, enabling producers to position their offerings at premium price points. Additionally, brand narratives emphasizing grain-to-glass authenticity align seamlessly with the marketing strategies of microbrewery trails, driving consumer engagement, encouraging product trials, and fostering repeat purchases.

Technological advancements in terms of production

Craft vodka producers are leveraging advanced stills with superior temperature and pressure control to enhance the distillation process, delivering cleaner and smoother spirits. Automated systems ensure consistent quality across batches while maintaining the integrity of small-batch production. Modern, scalable distillation units enable producers to increase output without compromising their artisanal appeal. By adopting innovative technologies, they are reducing energy consumption and waste, lowering production costs, and strengthening eco-conscious branding. Continuous distillation systems with patented stills produce higher proof neutral spirits while preserving congeners essential for mouthfeel, aligning artisanal craftsmanship with consistency demands. Sensor-enabled process controls streamline compliance with neutral-spirit purity regulations by adjusting reflux ratios in real-time, ensuring adherence to legal standards set by HM Revenue and Customs. These operational efficiencies help offset the disadvantages of smaller-scale production and accelerate breakeven timelines for emerging distilleries.

Innovation in flavor and ingredients

Premium craft vodka brands are differentiating themselves in the market by embracing innovative flavor experimentation. This includes the use of botanical infusions, cold-distilled fruits, and grains influenced by terroir, which add unique characteristics to their offerings. The Alcohol and Tobacco Tax and Trade Bureau (TTB) has recently introduced regulations permitting the limited use of sugar or citric acid treatments. This regulatory change provides brands with enhanced creative flexibility while ensuring vodka retains its neutral profile, a hallmark of the category. Furthermore, advancements in analytical technologies, such as near-infrared spectroscopy developed by the Scotch Whisky Research Institute, are enabling brands to optimize ingredient selection processes. These technologies also help reduce costs associated with traditional sensory panels, improving operational efficiency. Additionally, partnerships between the USDA and TTB have established clear pathways for organic certification. This allows brands to integrate sustainability claims into their labeling, complementing their unique flavor profiles and appealing to the growing segment of health-conscious consumers.

Growing tourism and hospitality sector

With the resurgence of leisure travel, destination distilleries are strategically capitalizing on increased foot traffic to drive high-margin bottle sales and foster long-term brand advocacy. According to data from India's Ministry of Tourism, Leisure, Holiday and Recreation accounted for 46.2% of Foreign Tourist Arrivals (FTAs) in 2023, reaffirming India's position as a premier global vacation destination[1]Source: Ministry of Tourism, "India Tourism Data Compendium 2024", www.tourism.gov.inIn Europe, the synergy between heritage tourism and exclusive offerings, such as on-site cask programs and limited tasting-room editions, enhances the appeal of distilleries as experiential destinations. Similarly, in the Asia-Pacific region, resorts are innovating by introducing premium "farm-to-shaker" vodka menus, effectively targeting the growing demand for high-end cocktail experiences. Additionally, ongoing staffing shortages in bars have prompted operators to prioritize spirits that come with comprehensive support systems. In response, distillers are proactively offering bartender-training modules and digital recipe libraries, which not only address operational challenges but also strengthen brand loyalty among hospitality professionals.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent government regulations | -0.9% | Global | Long term (≥4 years) |

| Consumers' inclination toward healthy beverages | -0.7% | North America and Europe | Medium term (2-4 years) |

| Health issues over excessive consumption | -0.6% | Global | Medium term (2-4 years) |

| Growing demand for low-alcohol products | -0.5% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations

Regulatory complexities pose significant barriers for craft vodka producers. The Alcohol and Tobacco Tax and Trade Bureau's proposed allergen and nutritional labeling requirements, with a compliance deadline set five years after the final rule's publication, increase administrative challenges for smaller producers. Additionally, variations in state-level regulations add to compliance difficulties. For instance, Mississippi's Senate Bill 2869 establishes craft spirit definitions and permitting requirements that differ from federal standards. Furthermore, state laws favoring local producers create legal uncertainties under the Commerce Clause, as demonstrated in cases like Granholm v. Heald, which addressed discrimination against out-of-state manufacturers. These regulatory pressures disproportionately impact smaller producers with limited compliance resources, potentially restricting their market entry and growth opportunities.

Consumers’ inclination toward healthy beverages

Canadian guidelines, which categorize alcohol consumption into risk zones ranging from 'no alcohol' (no risk) to '7+ drinks weekly' (high risk), highlight a significant shift toward health-conscious consumption patterns[2]Source: Statistics Canada, "Alcohol consumption levels in Canada", www.statcan.gc.ca. This shift is increasingly challenging the dominance of traditional alcohol categories in the market. The World Health Organization's Global Status Report on Alcohol and Health emphasizes the importance of implementing policy interventions to address alcohol-related harm. These interventions have heightened regulatory pressures, compelling the industry to adopt messaging that promotes reduced alcohol consumption. Consequently, the demand for lower-alcohol alternatives is on the rise, presenting both opportunities and challenges for market players. While traditional spirits categories face hurdles in adapting to these evolving consumer preferences, craft vodka producers are leveraging this trend by adopting premium positioning strategies. By emphasizing superior quality and aligning with the growing preference for moderation, these producers are effectively catering to the changing consumption patterns in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Flavored Innovation Drives Premium Positioning

Non-flavored expressions retained 84.62% of 2025 revenues, anchoring the craft vodka market as the workhorse for classic martinis and high-ball serves. Flavored lines, however, will lift revenues at a 5.85% CAGR through 2031 as distillers roll out natural botanicals and single-fruit macerations that sidestep artificial additives. In retail data sets, lemon-verbena and cucumber-mint SKUs reorder faster than legacy vanilla or cherry extensions, validating a pivot toward nuanced profiles. Demand for season-limited drops stimulates tasting-room traffic and supports higher bottle prices that fortify brand margins.

Growth momentum aligns with Alcohol and Tobacco Tax and Trade Bureau(TTB) revisions that permit minimal sweetening while retaining vodka’s neutral standard, giving producers latitude to layer subtle sweetness and acidity without drifting into liqueur classification. The strategy responds to wellness cues, focusing on real-fruit extracts and clean-label callouts instead of heavy-syrup flavors.

By Raw Material: Grain Dominance Faces Alternative Innovation

Grain remains the backbone at 68.92% of production in 2025, leveraging cost efficiencies and consumer familiarity with wheat and corn distillates. Regional grain procurement underpins sustainability messaging and fosters farmer-distiller partnerships that secure traceable supply at negotiated forward contracts. Yet alternative bases such as quinoa, rice, and even milk permeate launch calendars, fuelling a 6.21% CAGR for the “others” segment.

The adoption of these unconventional substrates addresses growing consumer concerns about allergens and introduces unique flavor profiles that cater to the preferences of adventurous and experimental drinkers. Additionally, technical expertise provided by the Scotch Whisky Research Institute on optimizing novel starches is expediting the development of innovative recipes. This shift toward a broader range of raw materials not only diversifies the segment but also creates significant opportunities for regional specialization and the establishment of robust agricultural partnerships.

By End User: Women Drive Consumption Growth

Male consumers account for 68.96% of craft vodka consumption in 2025, reflecting traditional spirits consumption patterns, while women represent the fastest-growing demographic with a 6.52% CAGR through 2031. This gender dynamic mirrors broader alcohol consumption trends. The female segment's growth correlates with craft cocktail culture expansion and women's increasing presence in hospitality industry leadership roles.

Female consumers prioritize quality over quantity, aligning with the premium positioning and artisanal production methods of craft vodka. Canadian data highlights gender-based consumption differences, with 20% of men consuming 7 or more drinks weekly compared to 11% of women, indicating a preference among women for moderate, high-quality drinking occasions. This demographic shift presents an opportunity for craft producers to develop marketing strategies that emphasize craftsmanship, sustainability, and responsible consumption. The move toward gender-inclusive marketing and product development reflects broader societal changes, benefiting premium spirits categories that focus on quality and authenticity rather than traditional masculine branding.

By Category: Premium Segment Accelerates Growth

Mass market for vodka holds 58.05% share in 2025, reflecting price-sensitive consumer segments and established distribution relationships, while premium categories drive growth at 7.11% CAGR through 2031. The premium segment's expansion aligns with broader spirits industry trends, with American whiskey's High End Premium and Super-Premium brands. Premium craft vodka benefits from the overall premiumization trend affecting all spirits categories, where consumers increasingly prioritize quality, provenance, and production methods over price considerations.

The mass market's dominance is attributed to vodka's widespread use as a mixing spirit in high-volume applications, while the premium segment's growth is fueled by neat consumption and craft cocktail usage, where quality differences are more evident. MGP Ingredients' premium plus portfolio, which is outperforming category growth, highlights the success of premium positioning strategies, even as branded spirits sales face challenges from elevated inventory levels. The market's trajectory indicates a growing polarization, with value-driven mass market products on one side and premium craft offerings on the other, putting increased pressure on middle-tier brands from both ends of the spectrum.

By Distribution Channel: Off-Trade Dominance Contrasts On-Trade Recovery

Off-trade channels command 85.73% market share in 2025, reflecting consumer purchasing patterns and retail accessibility, while on-trade venues show 5.66% growth through 2031 as hospitality sectors recover from pandemic impacts. The off-trade dominance stems from convenience, pricing advantages, and expanded retail presence of craft spirits in specialty liquor stores and premium grocery channels. Specialty liquor stores within the off-trade segment provide crucial brand education and premium positioning opportunities for craft vodka producers seeking to differentiate from mass-market alternatives.

The on-trade's resurgence underscores the hospitality sector's tenacity. UK venues, bolstered by government initiatives like energy relief and reduced business rates, strive to uphold their operations. In California, craft distillers benefit from an extension of direct-to-consumer rights, unlocking distribution avenues that sidestep the conventional three-tier system. This shift not only promises enhanced profit margins but also fosters direct ties with customers. As consumer preferences lean towards purchasing flexibility and multi-touchpoint brand engagement, the industry's evolution towards omnichannel strategies becomes evident.

Geography Analysis

North America anchors the craft vodka market with a 38.12% revenue share in 2025. The region's competitive position is strengthened by mature distribution networks, celebrity-backed product launches, and a stable supply of corn and wheat. States such as California and Texas leverage direct-to-consumer privileges, reducing reliance on national wholesalers and enabling profitable tasting-room business models.

Europe is projected to achieve a 7.49% annual growth rate through 2031, driven by the rise of experiential tourism and the growing influence of eco-conscious consumers. Sustainability-focused travelers are increasingly engaging in distillery tours and purchasing bottles, contributing to market growth. Additionally, Spirits Europe's consistent messaging on responsible drinking supports premium brands that emphasize moderation and craftsmanship over high-volume sales.

Asia-Pacific offers significant growth potential, fueled by the expansion of high-income consumer segments. The region's evolving cocktail culture is creating opportunities for premium vodka brands. In Thailand and Vietnam, where tourism thrives, locally crafted rice-based vodka is emerging as a popular gift, rivaling imported brands. Though current sales volumes are modest, the region's growth outpaces global averages, underscoring its significance in the coming years. Factors like a surge in tourist arrivals, urbanization, and a burgeoning middle class are shaping trends in the Middle East and Africa, and South America. Additionally, social media's sway in these areas is amplifying consumers' eagerness to explore novel flavors and varieties.

Competitive Landscape

The market for craft vodka is moderately fragmented, owing to the presence of large regional and domestic players in different countries. Emphasis is given on the merger, expansion, acquisition, and partnership of the companies, along with new product development, as strategic approaches adopted by the leading companies to boost their brand presence among consumers. The major players operating in the market includes Diageo Plc, Pernod Ricard SA, William Grant and Sons Ltd, Suntory Global Spirits Inc, and Heaven Hill Brands.

Distillers are prioritizing authenticity over scale by focusing on regional grains and renewable energy initiatives. The adoption of technologies such as automated stripping stills and blockchain-enabled ingredient tracing ensures batch consistency while maintaining an artisanal brand image. MGP Ingredients, a key supplier of neutral spirits to numerous craft labels, is simultaneously expanding its premium portfolio, highlighting its strategic influence in the market.

Small-batch producers are leveraging crowdfunding and local bond issuances to secure financing for barrel warehouses and visitor centers, thereby diversifying their revenue streams. Sustainability initiatives, including carbon-neutral goals and closed-loop water systems, are transitioning from competitive differentiators to baseline industry standards.

Craft Vodka Industry Leaders

-

Diageo Plc

-

Pernod Ricard SA

-

William Grant and Sons Ltd

-

Suntory Global Spirits Inc

-

Heaven Hill Brands.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Blisswater Industries has introduced its premium grain vodka, Salty Nerd, to the UAE market and is planning to expand its presence to Goa and Karnataka. The product is meticulously crafted in small batches, prioritizing high-quality ingredients and competitive pricing.

- March 2025: Spaceman Spirits Lab (Spaceman), a leading innovator in the craft spirits industry, has introduced AMARA Artisanal Pink Vodka. Produced using high-quality grapes and rice grains, AMARA is refined through an advanced five-fold distillation process.

- January 2025: Diageo has strategically relocated the production of its Chase brand gin and vodka to Scotland, integrating the operations into its Cameronbridge distillery located in Fife. This move aligns with Diageo's efforts to optimize its production capabilities and streamline operations within its existing infrastructure.

- October 2024: Pernod Ricard India has initiated the construction of Asia's largest malt distillery and maturation facility in Nagpur, Maharashtra, with a planned investment of up to INR 1,785 crore (USD 214 million) over the next 10 years. The facility is projected to produce up to 13 million liters of malt spirit annually, reflecting the company's strategic focus on strengthening its presence in the Asian market and commitment to sustainable production practices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the craft vodka market as all bottled vodka distilled in small-to-medium batches where annual output stays below 394,000 nine-liter cases, uses identifiable premium or locally sourced feedstocks, and is marketed around provenance and artisanal processes. This sizing captures flavored and unflavored SKUs sold through on-trade and off-trade retail across every major region during 2020-2030.

Scope exclusion: home-distilled products and mass-manufactured vodka lines above the craft output ceiling are omitted.

Segmentation Overview

-

By Product Type

- Flavored

- Non-Flavored

-

By Raw Material

- Grain-based

- Potato-based

- Others

-

By End User

- Men

- Women

-

By Category

- Mass

- Premium

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Egypt

- Morocco

- Nigeria

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations with master distillers, craft guild officers, liquor distributors, and specialty-bar managers across North America, Europe, and Asia-Pacific helped us validate typical batch sizes, flavor innovation adoption, and realistic off-trade price corridors. Short online surveys of adult drinkers further gauged willingness to pay for organic or gluten-free variants, filling gaps observed in public data.

Desk Research

Our analysts first assembled a foundational fact base from open sources such as the American Craft Spirits Association, Distilled Spirits Council, UN Comtrade shipment data, USDA grain statistics, and peer-reviewed journals tracking ethanol yields. Company 10-Ks, state liquor authority sales bulletins, trademark filings, and reputable trade press then supplied brand launch counts, average selling prices, and channel splits. Select proprietary databases, D&B Hoovers for company revenues and Dow Jones Factiva for deal news, added depth. This list is illustrative; many other references supported data verification and clarification.

A second pass reconciled regional duty-paid volumes, export flows, and ingredient cost curves to trace how supply, taxation, and consumer premiumization influence value growth.

Market-Sizing & Forecasting

We applied a top-down demand-pool build, reconstructing retail value from regional spirit consumption, craft share penetration, and channel mark-ups, which are then corroborated through selective bottom-up supplier roll-ups and average selling price × volume checks. Key variables modeled include: 1) active licensed craft distilleries, 2) nine-liter-case throughput per plant, 3) average retail-minus-tax price by bottle size, 4) flavored-sku mix shift, 5) grain-based input cost index, and 6) legal changes enabling direct-to-consumer sales. A multivariate regression with scenario analysis projects these drivers through 2030, while missing batch data for micro-producers is bridged using regional medians gathered from interviews.

Data Validation & Update Cycle

Outputs undergo variance checks versus import-export records, excise collections, and consumer panel scans. Senior Mordor reviewers sign off only after anomalies are resolved. Reports refresh every twelve months, with interim revisions triggered by policy changes or major M&A; a fresh analyst pass precedes each client delivery.

Why Mordor's Craft Vodka Baseline Commands Reliability

Published estimates often diverge because firms pick differing service scopes, currency treatments, and update cadences.

Key gap drivers include whether flavored micro-runs are valued at producer or retail prices, how growth from new distillery permits is embedded, and the frequency of field-level validation. Mordor's model reports full-retail value for batches under the craft threshold, factors live permit issuances quarterly, and validates price ladders with bar managers; steps some peers omit.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.23 B (2025) | Mordor Intelligence | - |

| USD 10.02 B (2024) | Global Consultancy A | Includes large "premium" brands outside craft ceiling and uses producer-level pricing |

| USD 5.12 B (2025) | Industry Association B | Excludes flavored releases and employs 2023 permit counts without annual updates |

These contrasts show that when scope, pricing tier, and refresh cadence are harmonized, Mordor's disciplined blend of public data, expert insight, and annually renewed assumptions delivers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the craft vodka market?

The craft vodka market is valued at USD 6.57 billion in 2026 and is projected to reach USD 8.55 billion by 2031.

Which region leads global sales?

North America holds the largest share at 38.12% of 2025 revenue, supported by mature distribution and strong direct-to-consumer laws.

Which segment is growing fastest?

Flavored vodka is forecast to post a 5.85% CAGR to 2031, outpacing non-flavored expressions as consumers seek natural botanical infusions.

How are regulations affecting craft producers?

Proposed U.S. rules on allergen and nutrition labeling raise compliance costs, while the United Kingdom’s strength-based duty increases tax on spirits above 22% ABV.

Page last updated on: