Virtual PBX Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

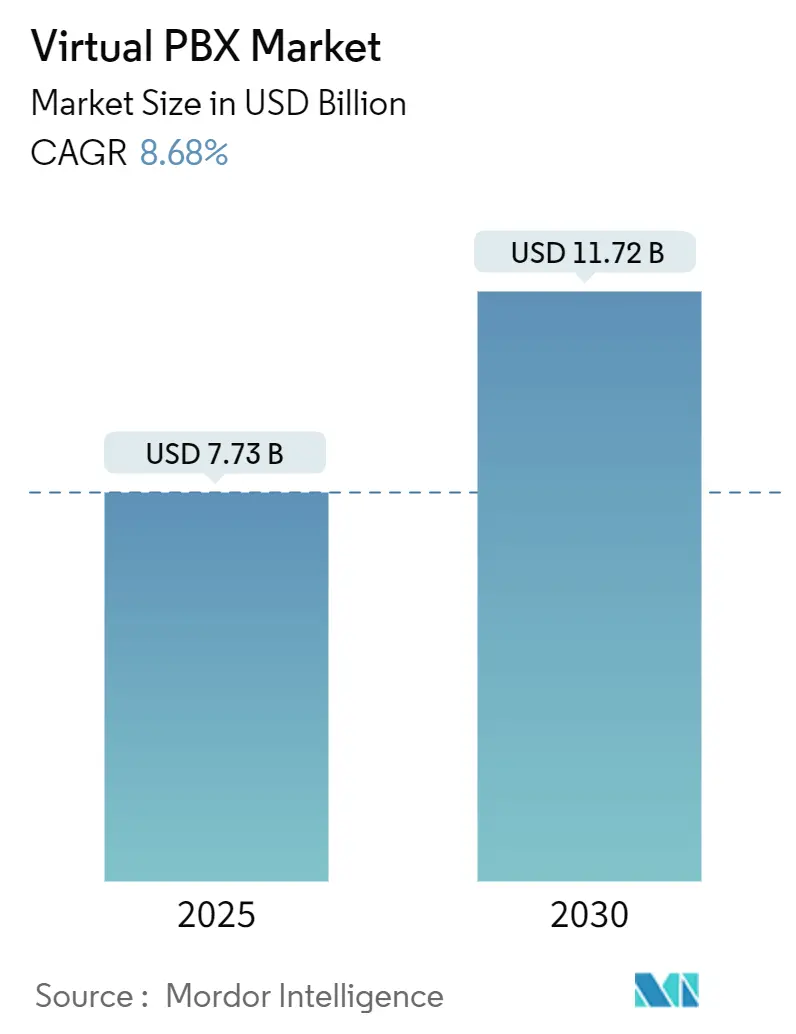

| Market Size (2025) | USD 7.73 Billion |

| Market Size (2030) | USD 11.72 Billion |

| Growth Rate (2025 - 2030) | 8.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual PBX Market Analysis by Mordor Intelligence

The virtual PBX market size stands at USD 7.73 billion in 2025 and is projected to reach USD 11.72 billion by 2030, reflecting an 8.68% CAGR. As businesses transition from traditional telephony to cloud-native unified communications, the virtual PBX market experiences robust growth. This momentum is further fueled by the expansion of 5G coverage and the swift adoption of AI-driven call management features. Major enterprises are entering into multi-year contracts, integrating UCaaS, CCaaS, and CPaaS modules. In contrast, small and midsize businesses are opting for subscription models, sidestepping hefty hardware investments. Providers are channeling investments into geo-redundant data centers and edge nodes, enhancing service reliability to rival or even exceed that of traditional on-premises PBX systems. Meanwhile, merger activities are not only reshaping the competitive landscape but also pushing for a unified standard across voice, video, and messaging platforms. Although cross-border deployments pose challenges, vendors are proactively addressing these with region-specific compliance zones and sovereign-cloud solutions, in line with the growing emphasis on data residency mandates.

Key Report Takeaways

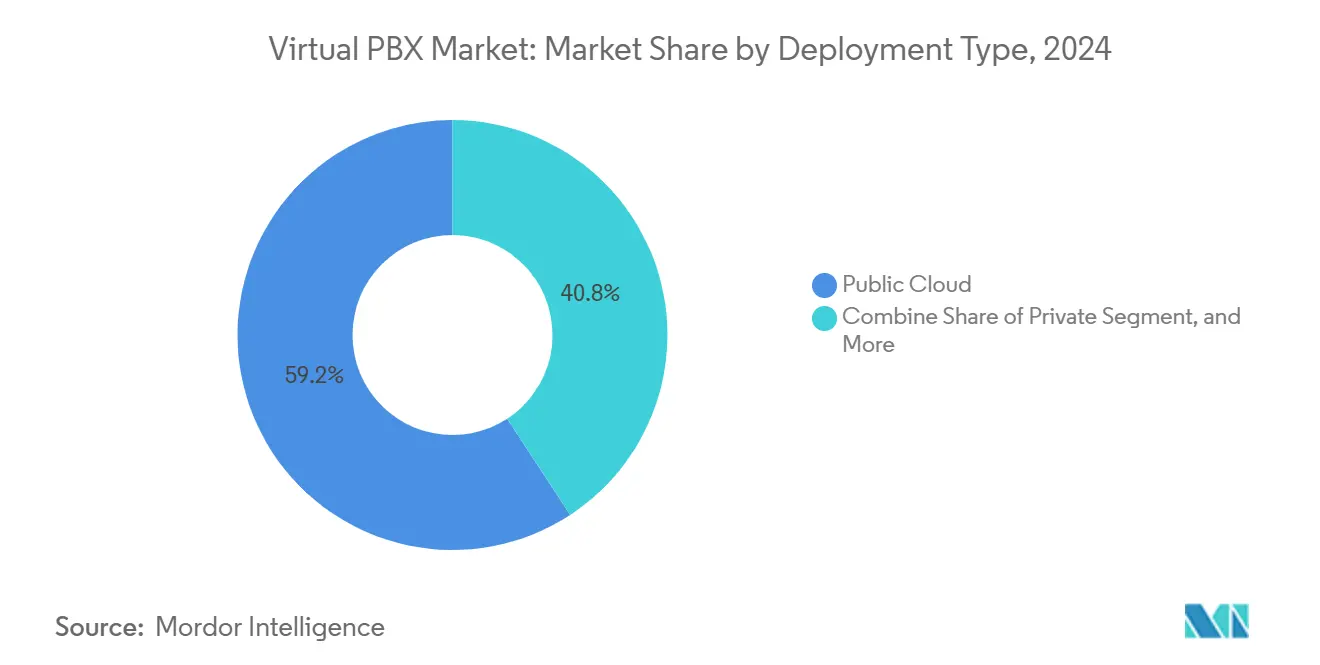

- By deployment model, public cloud led with 59.22% revenue share in 2024; hybrid cloud is forecast to advance at a 9.26% CAGR through 2030.

- By organization size, small and medium organizations held 55.67% of the 2024 virtual PBX market share, while large enterprises are expanding at an 8.79% CAGR through 2030.

- By component, solution accounted for 71.45% of the 2024 virtual PBX market size; services are projected to grow at 7.47% CAGR to 2030.

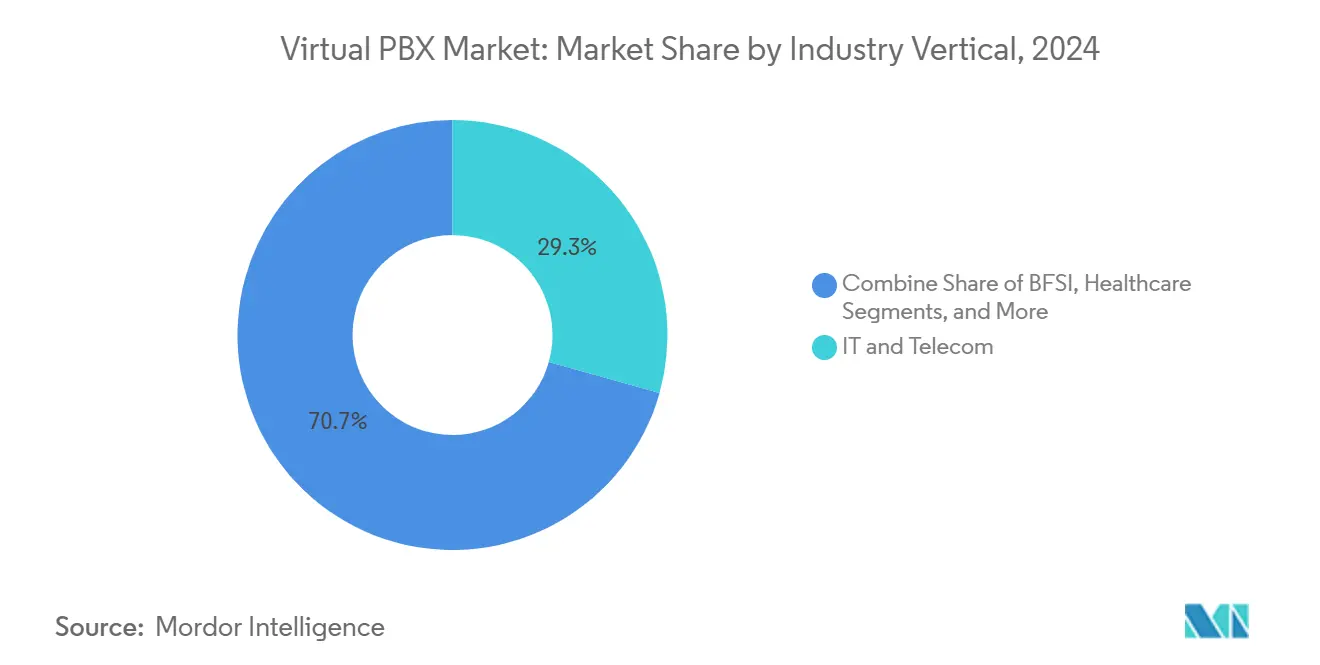

- By industry vertical, IT and telecom captured 29.34% share of the virtual PBX market size in 2024, whereas healthcare is advancing at a 10.14% CAGR through 2030.

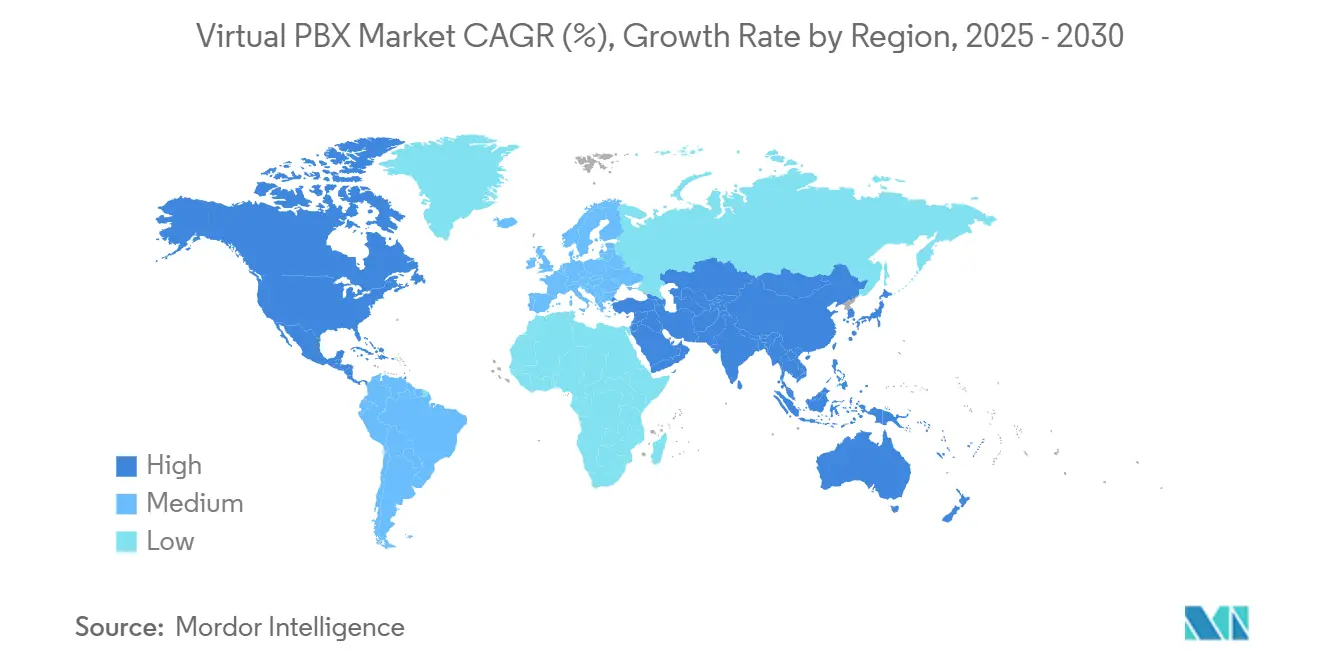

- By geography, North America commanded 35.12% of 2024 revenue, and Asia Pacific is forecast to register the fastest 9.32% CAGR through 2030.

Global Virtual PBX Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of cloud-native UCaaS | +2.1% | Global with focus in North America and Europe | Medium term (2-4 years) |

| AI-enhanced call-routing and sentiment analytics | +1.8% | Global led by North America and Asia Pacific | Short term (≤2 years) |

| Expansion of 5G standalone networks supporting QoS SLAs | +1.5% | Asia Pacific core with spill-over to North America and Europe | Long term (≥4 years) |

| Rapid cloud infrastructure maturity and reliability | +1.3% | Global | Medium term (2-4 years) |

| Technological advancements in cloud and VoIP solutions | +1.2% | Global | Short term (≤2 years) |

| Rising adoption among SMEs and startups | +0.9% | Global with emphasis on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Cloud-Native UCaaS

Enterprise exit from hardware-bound PBX systems continues to accelerate. Microsoft Teams Phone now serves more than 20 million users, and leading vendors report up to 76% operating-cost savings when clients decommission on-premises switches.[1]Fusion Connect, “It’s Time to Replace Your On-premises PBX,” fusionconnect.com84% of surveyed firms view integrated UCaaS and CCaaS deployments as the clearest path toward communication consolidation.Despite the momentum, fewer than 40% of businesses have completed migration, leaving ample headroom for the virtual PBX market. Platform roadmaps emphasize self-service provisioning workflows that simplify onboarding for non-technical staff and shorten implementation cycles from months to weeks. The virtual PBX market benefits directly as cost advantages and scalability perceptions outweigh integration concerns.

AI-Enhanced Call-Routing and Sentiment Analytics

Artificial intelligence has advanced from basic keyword spotting to real-time sentiment recognition that guides agent coaching during live conversations. RingCentral recorded more than USD 50 million in annual recurring revenue from AI-augmented offerings, signaling early but substantial willingness to pay for premium automation. 8x8 logged a substantial rise in AI interactions, an indicator that feature penetration is moving quickly from pilots to production across verticals Enterprises report 10% to 20% sales uplifts attributable to predictive routing and voice-of-customer analysis, outcomes that justify higher license fees. The virtual PBX market therefore positions AI modules not as optional add-ons but as core value drivers that heighten differentiation among providers.

Expansion of 5G Standalone Networks Supporting QoS SLAs

Network slicing under 5G standalone architecture allows carriers to commit bandwidth and latency parameters that previously were unattainable for cloud voice.[2]Ericsson, “How Network Slicing Will Benefit Society,” ericsson.comAsia Pacific operators launch private 5G zones in manufacturing parks, creating fertile ground for QoS-defined voice links that feed directly into cloud call controllers. Enterprises view these guaranteed links as insurance against jitter when replacing time-division multiplexing trunks. Implementation challenges remain for interconnect signaling and pricing models, yet proof-of-concept deployments confirm technical feasibility. As these reference sites multiply, the virtual PBX market gains a new performance narrative that counters reliability concerns surrounding public internet links.

Rapid Cloud Infrastructure Maturity and Reliability

Tier-one UCaaS suppliers now consider uptime commitments as standard practice. Cisco, along with other global providers, utilizes a network of interconnected data centers, ensuring calls are routed through the nearest point of presence to reduce latency. By placing edge computing nodes closer to end users, these providers boost failover capabilities and ensure call clarity, even during network congestion. Adopting a multicloud architecture mitigates vendor lock-in risks, allowing for a distribution of telephony workloads across major hyperscale platforms. Given that tolerance for outages is crucial for mission-critical communications, this heightened reliability is attracting traditionally risk-averse sectors like healthcare and finance, thereby strengthening the virtual PBX market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration challenges with legacy infrastructure | -1.4% | Global with concentration in North America and Europe | Medium term (2-4 years) |

| High compliance costs for data sovereignty across borders | -0.8% | Global with emphasis on EU, UK, and regulated industries | Long term (≥4 years) |

| Persistent security and privacy concerns | -0.7% | Global | Short term (≤2 years) |

| Shortage of skilled IT professionals | -0.5% | Global with acute gaps in developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Compliance Costs for Data Sovereignty Across Borders

The surge in regional data-protection laws forces providers to stand up country-specific instances or secure local carrier partnerships. Financial and healthcare customers add an extra layer of controls by requesting encrypted call recording with tamper-proof audit trails. Operating multiple sovereign-cloud environments inflates cost structures that eventually appear as higher subscription fees, limiting adoption among budget-sensitive segments. The virtual PBX market must therefore balance compliance assurance with price competitiveness to sustain growth momentum.

Integration Challenges with Legacy Infrastructure

Large enterprises often maintain analog devices, proprietary PBX trunks, and custom call-flow scripts that complicate cut-over to cloud architectures. Dual-run phases where on-premises switches operate in tandem with cloud instances inflate cost and project complexity. Hardware refreshes become unavoidable once compatibility gaps surface, and emergency-calling compliance demands additional testing. These realities slow rollout velocity and dilute the headline savings that the virtual PBX market promotes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Solutions Bridge Legacy Gap

Organizations hesitant to fully abandon their on-premises PBX investments find a balanced solution in hybrid clouds. While the public cloud secured a dominant 59.22% share of 2024 revenues, underscoring a preference for fully managed environments, the hybrid deployments' 9.26% CAGR signals a rising demand for models that accommodate both analog devices and specialized gateways. In the virtual PBX market, hybrid rollouts frequently arise from compliance needs or bandwidth constraints, hindering a swift shift to purely public instances. Vendors are responding by introducing connector kits that seamlessly integrate legacy dial-plans with cloud call flows. Looking ahead, hybrid architectures are poised to be the preferred choice for widely distributed enterprises, ensuring the virtual PBX market remains accessible to customers at various stages of transformation.

Public cloud platforms, with their rapid provisioning and instant feature access, continue to dominate. Yet, sectors like healthcare and finance, sensitive to SLAs, are pushing for call-path redundancy across both private and public links, driving investments in hybrid solutions. The evolution of SD-WAN and 5G further empowers enterprises, allowing them to gradually phase out on-premises trunks without disrupting business. Thus, hybrid frameworks emerge not merely as transitional solutions but as strategic avenues, broadening the virtual PBX market's potential.

By Organization Size: Enterprise Acceleration Drives Premium Growth

Small and midsize enterprises account for 55.67% of 2024 revenues, validating the technology’s democratizing effect by lowering entry barriers. Even micro-businesses deploy carrier-grade auto-attendants that rival large-enterprise systems. Yet large organizations register the highest 8.79% CAGR because their multi-country installations generate sizeable contract value that inflates the virtual PBX market size. Complex deployments that span thousands of extensions necessitate advanced routing logic, AI-assisted agent tools, and granular compliance features. Providers extract higher average revenue per user from this cohort, and cross-sell potential across CCaaS and CPaaS further accelerates wallet-share gains.

Large enterprises also act as early technology validators. RingCentral witnessing a rise in enterprise deal sizes, while Zoom closed a single 20,000-seat contact-center migration. These proof points influence midmarket buyers, producing a downstream effect that preserves growth across all tiers. As global macro conditions drive sustained hybrid-work policies, the virtual PBX market is positioned to capture incremental enterprise workloads that arise from branch network expansions and consolidation initiatives.

By Industry Vertical: Healthcare Leads Digital Transformation

IT and telecom held the largest 29.34% slice of the virtual PBX market share in 2024, reflecting early adopter status among tech-savvy firms. Healthcare, however, races ahead with a 10.14% CAGR as telemedicine and secure patient communications demand HIPAA-aligned voice and messaging solutions. Clinics and hospitals adopt cloud PBX suites that integrate with electronic health records and enable fail-safe paging, replacing disparate legacy systems. Case studies such as PM Pediatrics’ multi-site rollout illustrate how cloud voice supports flexible triage workflows while safeguarding protected health information.[3]RingCentral Press, “PM Pediatrics Uses RingCentral Cloud Communications,” ringcentral.com

Banking, retail, and education continue to migrate at steady rates, converting branch offices into connected experience centers that rely on unified voice and video. Regulations in finance spur encryption uptake, while retail brands deploy virtual PBX lines to coordinate omnichannel fulfillment. Government agencies look to cloud telephony to reduce budget outlays tied to Centrex fees, further extending the virtual PBX market across public-sector domains.

By Component: Services Growth Reflects Implementation Complexity

Solution form 71.45% of the 2024 virtual PBX market size because the core call-control engine remains indispensable. Yet managed services, integration consulting, and training offerings advance at an 7.47% CAGR, mirroring customer reliance on specialized expertise to execute large-scale migrations. Each enterprise instance demands unique dial-plan mapping, CRM connector configuration, and security assessment, tasks that stretch in-house IT bandwidth. This growing dependence raises attach rates for professional services, lifting provider margins and increasing total contract value.

Service growth also signals a maturing buyer mindset that views communications transformation as an ongoing journey rather than a one-time license purchase. Post-deployment managed services deliver analytics, feature tuning, and regulatory updates that keep systems current and compliant. Vendors who bundle advisory programs alongside license renewals secure longer customer lifecycles, which fortifies the virtual PBX market against commoditization risks.

Geography Analysis

North America leads the virtual PBX market with 35.12% share in 2024, bolstered by widespread fiber connectivity and employer embrace of hybrid work policies. Enterprise contracts increasingly stipulate AI-enabled analytics layers that improve customer interaction quality, a trend that fuels upsell revenue for providers. Government modernization programs, such as the federal transition from Centrex to IP voice, reinforce cloud acceptance across mission-critical environments. Skill shortages in specialized networking roles remain a headwind, yet vendor-managed deployments partly offset that gap.

Asia Pacific records the highest 9.32% CAGR. Rapid fiber build-outs, mobile-data price declines, and a growing base of digital-native SMEs drive large-scale adoption. Providers deploy multilingual support interfaces and in-country data gateways to comply with diverse regulatory frameworks, which reduces procurement friction and accelerates onboarding. Increasing 5G standalone coverage allows businesses to bypass copper loops entirely, an advantage that streams new workloads into the virtual PBX market.

Europe’s adoption pace holds steady as enterprises balance GDPR compliance with cost advantages of cloud telephony. Providers respond by establishing regional data silos and transparent audit controls. Although implementation cycles take longer, long-term contract values remain robust because organizations mandate comprehensive compliance feature sets. Initial adoption phases in South America, the Middle East, and Africa focus on contact-center functions where the revenue impact is immediately measurable. Incremental network upgrades and cloud-on-ramp programs are expected to unlock broader use cases over the forecast horizon, expanding the virtual PBX market footprint.

Competitive Landscape

Top vendors differentiate on AI breadth, reliability metrics, and ecosystem breadth rather than on raw calling features. RingCentral reports over USD 50 million annual recurring revenue from AI modules. 8x8 secures leadership positioning on both UCaaS and CCaaS quadrants by pairing customer-engagement analytics with its core telephony stack.

Tier-one cloud providers invest in carrier partnerships to bolster geographic reach. AT&T bundles Teams Phone Mobile into its wireless offering, allowing number portability between SIM and softphone clients. Cisco and Zoom focus on embedded collaboration tools that integrate natively with productivity suites, securing stickiness in enterprise workflows. Niche entrants pursue vertical specialization, such as HIPAA-focused platforms or logistics-ready dispatch tools, offering differentiated value to sectors underserviced by one-size-fits-all suites. Competitive intensity therefore spans a spectrum from price-driven SME packages to high-margin enterprise bundles, an environment that sustains innovation while preventing dominance by any single actor.

Virtual PBX Industry Leaders

RingCentral, Inc.

8x8, Inc.

Cisco Systems, Inc.

Microsoft Corporation

Vonage Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: With two significant announcements, Communications has bolstered its foothold in India: it has expanded its cloud-based Zoom Phone service to more telecom circles and officially launched its Zoom Contact Center in the nation. Zoom Phone, now licensed by India's Department of Telecommunications (DoT), has made its debut in four new telecom circles: Mumbai, Delhi NCR, Karnataka (Bengaluru), and Andhra Pradesh and Telangana (Hyderabad). This expansion complements its existing presence in Maharashtra and Tamil Nadu, totaling six pivotal regions that are home to India's major business and technology hubs. Designed to support distributed and hybrid workforces, Zoom Phone facilitates inbound and outbound calling over the Public Switched Telephone Network (PSTN). This capability aids organizations in moving from traditional PBX systems to a cohesive communications platform. Offered as an add-on for paid Zoom accounts, the service allows for native phone number acquisition via a self-service portal, even in regions where direct service hasn't yet launched. Enhancing the platform are AI-driven features like post-call summaries, voicemail prioritization, and task extraction — all complimentary for qualifying accounts. Zoom's newly introduced Contact Center in India promises to deliver sophisticated customer engagement tools, seamlessly integrated with the company's collaboration suite, underscoring Zoom's dedication to meeting the dynamic demands of Indian businesses.

- January 2025: NUWAVE Communications, Inc. has introduced Teleport, an innovative feature within its globally recognized iPILOT multi-UC service management platform. Officially launched on January 22, 2025, Teleport is designed to revolutionize enterprise transitions to modern UC platforms such as Microsoft Teams, Cisco Webex, and Zoom. By leveraging a fully automated and intelligent migration process, Teleport eliminates complexities and accelerates the adoption of next-generation communication systems. Built on NUWAVE's robust iPILOT platform, Teleport integrates advanced technology and extensive UC expertise to deliver a streamlined, secure, and efficient migration pathway, enabling organizations to achieve modernization objectives with reduced risk and enhanced efficiency.

- October 2024: VirtualPBX has unveiled its latest innovation: the Web Phone. This state-of-the-art tool enables businesses to manage communications seamlessly through a web browser, eliminating the need for any physical hardware. Tailored for businesses of all sizes, especially those with remote and mobile teams, the revamped VirtualPBX Web Phone interface empowers users to make and receive calls, access voicemails, and oversee communications from virtually anywhere, at any time.

Global Virtual PBX Market Report Scope

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Small and Medium Organizations |

| Large Organizations |

| IT and Telecom |

| BFSI |

| Healthcare |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Other Industry Verticals (includes Manufacturing, Hospitality , Logistics) |

| Solution |

| Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Organization Size | Small and Medium Organizations | |

| Large Organizations | ||

| By Industry Vertical | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Retail and E-commerce | ||

| Education | ||

| Government and Public Sector | ||

| Other Industry Verticals (includes Manufacturing, Hospitality , Logistics) | ||

| By Component | Solution | |

| Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value for global virtual PBX solutions by 2030?

The virtual PBX market is expected to reach USD 11.72 billion by 2030.

Which region is growing fastest in adopting PBX services?

Asia Pacific is set to expand at a 9.32% CAGR through 2030, the quickest among all regions.

Which enterprise segment drives the highest contract value?

Large organizations show the greatest growth momentum at an 8.79% CAGR because their deployments bundle advanced AI and contact center functions.

Why is healthcare adopting cloud telephony so rapidly?

Telemedicine expansion and strict patient-data regulations drive hospitals and clinics toward secure, HIPAA-aligned virtual PBX platforms.

What deployment approach allows phased migration from legacy PBX?

Hybrid cloud models let firms keep critical on-premises systems while adding cloud scalability, growing at 9.26% CAGR.

Which technology trend most strengthens service reliability?

5G standalone network slicing provides dedicated bandwidth for voice, improving quality of service commitments for virtual PBX users.

Page last updated on: