Fiber Optic Component Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

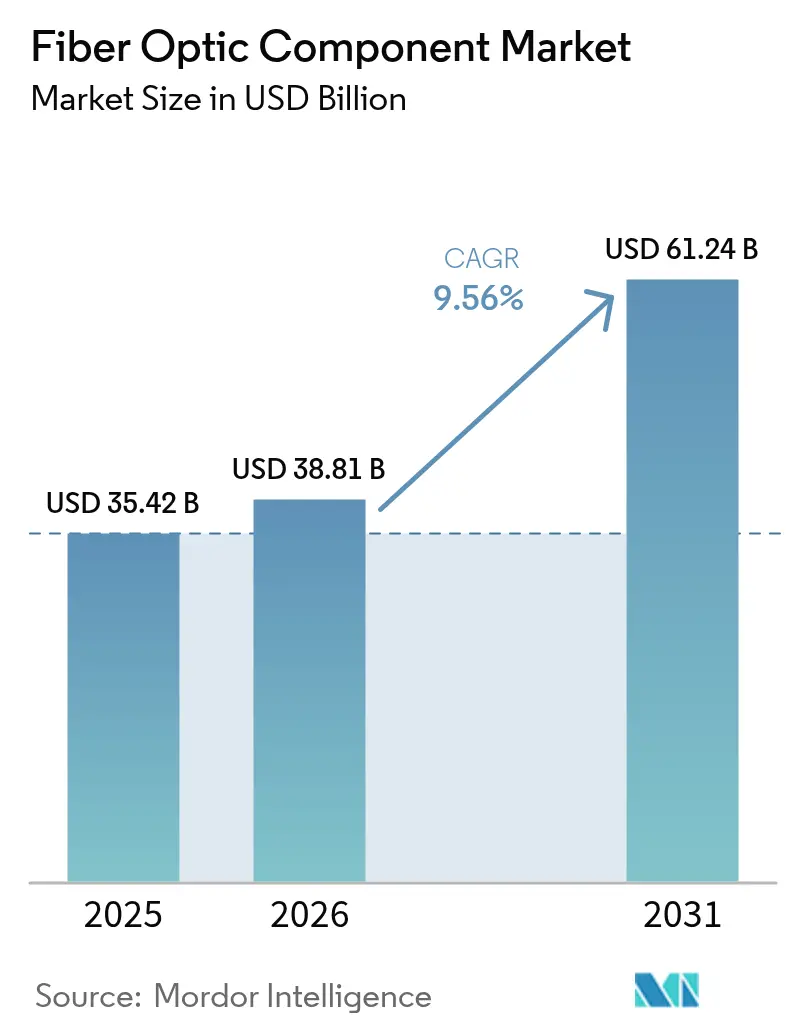

| Market Size (2026) | USD 38.81 Billion |

| Market Size (2031) | USD 61.24 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

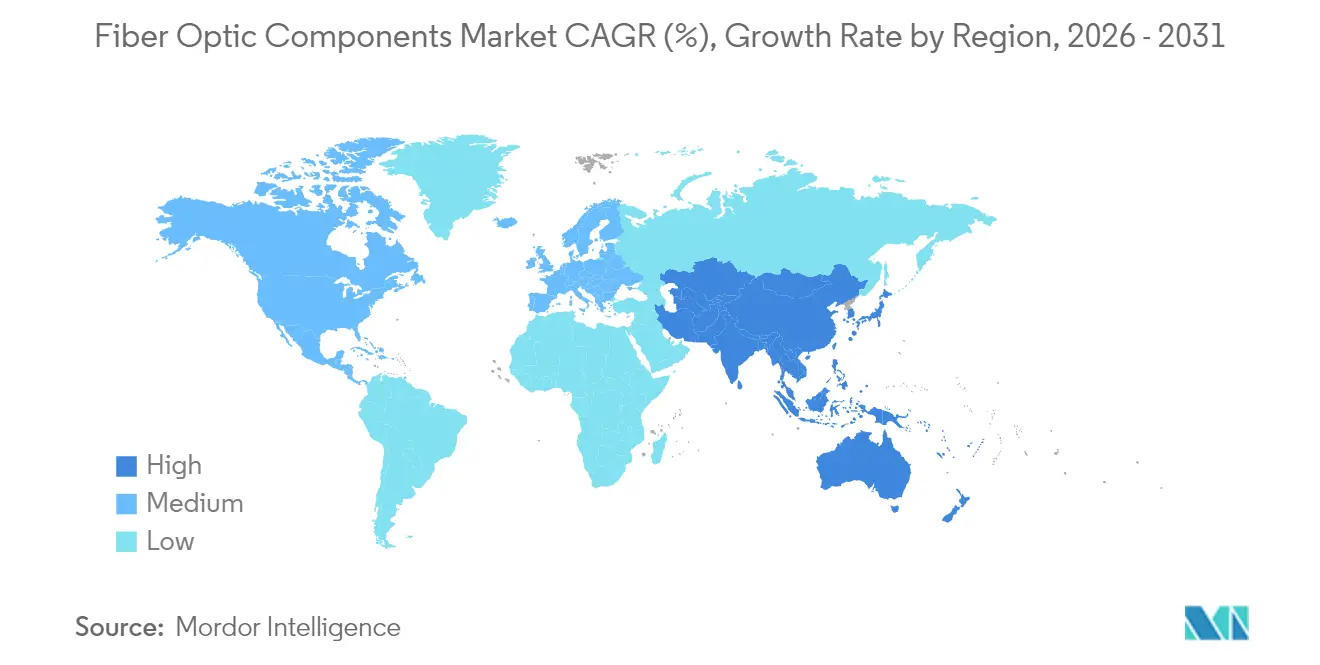

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Optic Component Market Analysis by Mordor Intelligence

Fiber Optic Component Market size in 2026 is estimated at USD 38.81 billion, growing from 2025 value of USD 35.42 billion with 2031 projections showing USD 61.24 billion, growing at 9.56% CAGR over 2026-2031.

This expansion underscores the fiber optic component market resilience as global networks pivot to artificial intelligence workloads, 5G densification, and quantum-safe communication. Supply-chain pressures on critical compound semiconductors have amplified vertical integration strategies among major vendors while motivating accelerated R&D on alternative materials. In parallel, hyperscale data-center operators reserve long-term capacity commitments that stabilize demand visibility for cable manufacturers and photonic chipmakers. Government-funded rural broadband programs in the United States, the European Union, and key Asia Pacific economies are reinforcing baseline consumption of passive optical infrastructure across both mature and developing regions.

Key Report Takeaways

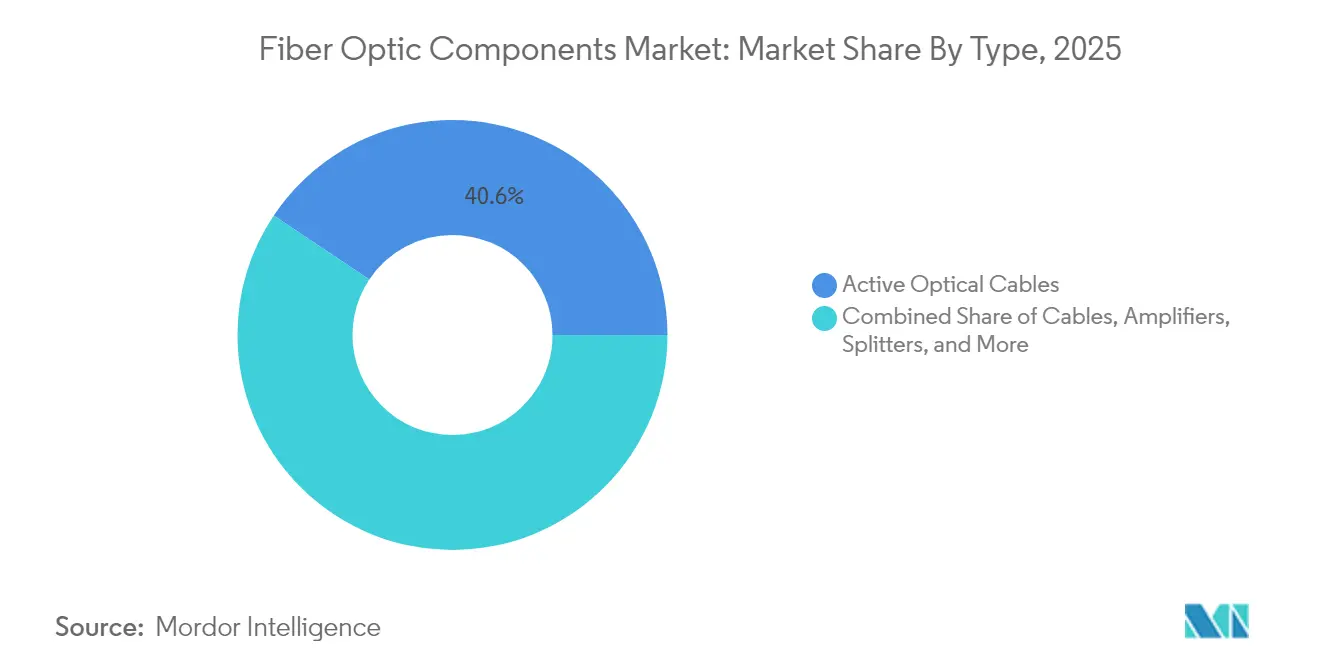

- By type, optical cables commanded 40.62% of the fiber optic component market share in 2025, while active optical cables are projected to expand at an 10.97% CAGR to 2031.

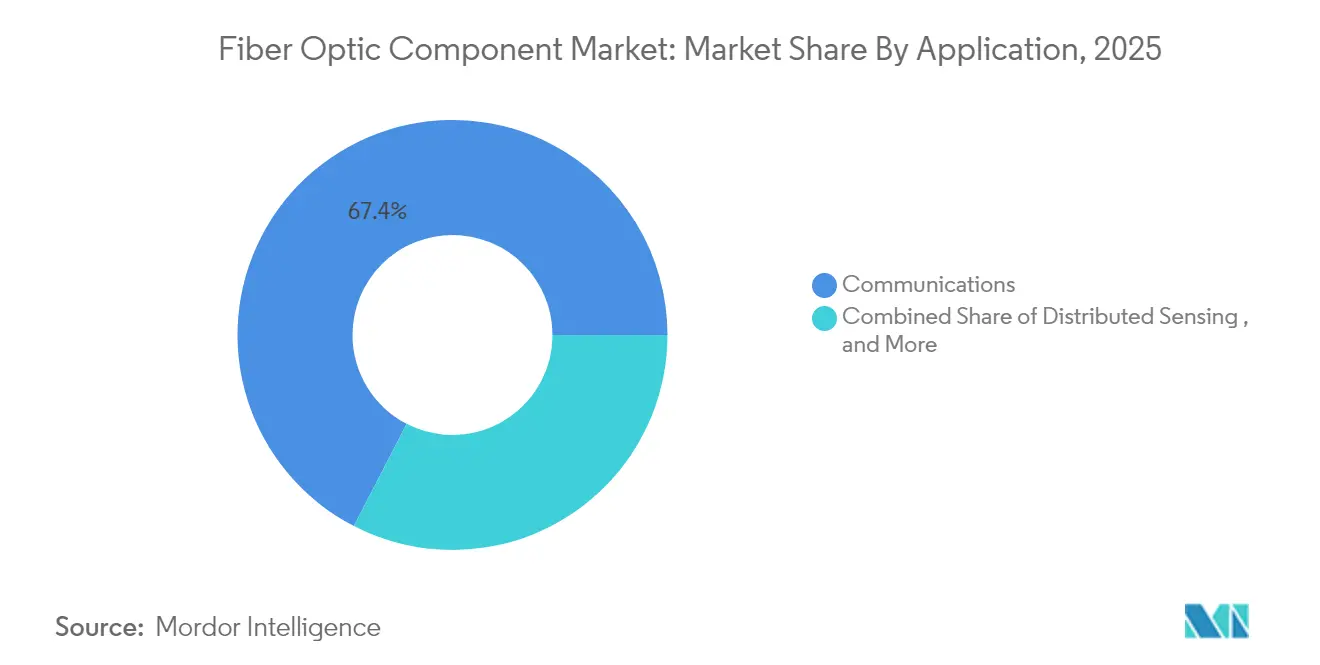

- By application, communications held 67.42% revenue share in 2025; the same segment also records the fastest 10.72% CAGR through 2031.

- By end-user, telecom operators retained 55.38% share of the fiber optic component market size in 2025, whereas hyperscale and enterprise data centers are advancing at 12.01% CAGR.

- By geography, Asia Pacific led with 38.74% share in 2025 and is projected to grow at a 10.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Fiber Optic Component Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale-data-center fiber refresh wave | +2.10% | Global, concentrated in North America and the Asia Pacific | Medium term (2–4 years) |

| 5G fronthaul/backhaul densification | +1.80% | Global, with early deployment in Asia Pacific and Europe | Short term (≤ 2 years) |

| AI/ML optics > 800 Gb accelerating PAM4/Co-Packaged Optics | +2.40% | North America and Asia Pacific, spillover to Europe | Medium term (2–4 years) |

| Rapid FTTH rollout in emerging APAC and Africa | +1.60% | Asia Pacific and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale-data-center fiber refresh wave

Surging generative-AI training clusters require far denser optical interconnects than legacy cloud nodes. Corning reported a 46% year-over-year jump in optical-communications revenue to USD 1.36 billion during Q1 2025, underpinned by a multi-year supply agreement that reserves 10% of its global fiber output for a single data-center operator[1]Wendell Weeks, “Corning Q1 2025 Results Highlight Optical Surge,” Corning Incorporated, corning.com. Optical transceiver shipments exceeded USD 3 billion in Q2 2024, marking the strongest sequential revenue performance since 2019. Equipment vendors are redesigning leaf-and-spine architectures around 800 G and 1.6 T optics, which requires higher-grade bend-insensitive fiber inside cable trays. These shifts elevate demand for low-loss fiber types and advance orders for co-packaged optics. The broad refresh cycle increases visibility for component suppliers over a multi-year horizon.

5G fronthaul and backhaul densification

Wide-scale standalone 5G rollouts multiply fiber counts from radio head to baseband unit. Thailand’s Village Broadband Internet initiative extended fiber to 24,700 remote communities by March 2025. Malaysia’s national broadband project, valued at MYR 21 billion (USD 4.4 billion), upgraded 60% of premises to fiber as of December 2024. Sumitomo Electric’s 0.07-millisecond converter improves the time-synchronization precision needed for fronthaul coordination[4]Hiroshi Nishihara, “0.07 ms Converter for Remote 3D Visuals,” Sumitomo Electric, sumitomoelectric.com. Prysmian’s latest ultra-high-density ribbon cables help operators push more fibers into constrained ducts Prysmian Group. These deployments transform network topologies toward distributed architectures, lifting demand for connectors, closures, and low-latency cables.

AI/ML optics accelerating PAM4 and co-packaged integration

Lumentum demonstrated an enhanced 800 G ZR+ transceiver fabricated on proprietary indium-phosphide technology, doubling its datacom chip order backlog by mid-2025. The company expanded backend assembly lines in Thailand to mitigate material bottlenecks and shorten lead times. Shanghai Jiao Tong University has scaled thin-film lithium-niobate photonic chip production, which could broaden ecosystem access to high-speed modulators. Suppliers shipped more than 20 million 400 G and 800 G optical modules in 2024, signalling broad acceptance of PAM4 signalling for advanced AI clusters. As model sizes rise, operators must trim power budgets, making co-packaged optics a default choice at 51.2 T switch capacity. Continuous feedback between AI system architects and photonics engineers accelerates successive design-win cycles.

Rapid FTTH expansion in emerging markets

Indonesia initiated a national optical backbone to bridge digital gaps across 4,200 islands, while the Philippines’ USD 288 million National Fiber Backbone spans 1,245 kilometers and targets 70 million new users by 2028. India committed USD 16.1 billion to rural broadband, having already connected 270,000 villages by April 2025. Australia’s Better Connectivity Plan earmarked AUD 1.1 billion (USD 740 million) for rural fiber corridors. Such projects assure long-tail demand for passive infrastructure, diversify supplier revenue beyond hyperscale clients, and set the stage for future 5G and smart-grid services.

Restraints Impact Analysis of Fiber Optic Component Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of indium-phosphide and gallium-arsenide epi-capacity | −1.4% | Global, acute impact in Asia Pacific manufacturing | Short term (≤ 2 years) |

| Geopolitical export controls on advanced photonics to China | −1.1% | Global supply chains, concentrated in Asia Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shortage of indium-phosphide and gallium-arsenide epi-capacity

China’s export restriction on gallium and germanium in 2023 lifted spot prices by 250% and 75%, respectively. The U.S. Geological Survey calculated a potential USD 3.4 billion GDP hit if bans become absolute. Coherent’s new six-inch indium-phosphide wafer line in Texas promises 60% cost reduction once fully ramped, quadrupling die output per wafer. Fraunhofer ISE’s InP-on-GaAs substrates lower wafer costs by 80% and enable eight-inch pilot runs. Even so, tooling cycles limit near-term relief, forcing contract manufacturers to prioritize high-margin transceiver customers and extend delivery windows on lower-speed parts.

Geopolitical export controls are fragmenting global supply chains

U.S. export rules targeting photonic integrated circuits complicate supply contracts that previously leveraged Asia Pacific back-end capacity. Chinese foundries are accelerating domestic photonic chip programs to reduce dependency on imported epitaxy equipment. Parallel supply chains raise costs due to duplicated R&D and compliance audits. European vendors must file dual-use license applications for every new high-speed transceiver family, lengthening time-to-market. Multiregional qualification of assembly locations spreads risk but strains working-capital budgets. While fragmentation spurs localized innovation clusters, it weighs on near-term volumes and margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fiber Optic Component Market Segment Analysis

By Type:

Active Optical Cables Outpace Traditional InfrastructureOptical cables retained a 40.62% share of the fiber optic component market in 2025, driven by entrenched deployments in metro and long-haul backbones. The fiber optic component market size for this segment reached USD 14.39 billion, reflecting the dominance of passive cable spending in large state-funded rollouts. However, active optical cables post an 10.97% CAGR to 2031 as hyperscale operators migrate to fully integrated, pluggable links inside server racks. Demand for amplifiers and splitters remains tied to point-to-point upgrades on existing routes, particularly where governments finance rural reach projects.

Adoption of co-packaged optics turns active cables into short-reach engines of bandwidth scaling. Corning introduced Gen-AI fiber assemblies with integrated power-optimized connectors aimed at 102.4 T switch enclosures. Transceiver makers bundle digital signal processors with photonic dies, shrinking footprint while lifting energy efficiency. The active segment thereby captures incremental share by substituting traditional trunks at datacom distances below 100 meters. Suppliers that couple glass-drawing expertise with module integration stand to gain follow-on design wins.

By Application:

Communications Dominance Amid DiversificationCommunications accounted for 67.42% of revenue and exhibited the highest 10.72% CAGR, reinforcing the fiber optic component market share leadership of service providers and data center interconnects. Fiber optic component industry observers note that distributed sensing and medical instrumentation have begun to command premium pricing, yet their volumes remain modest relative to broadband access. The fiber optic component market size tied to communications is set to breach USD 41.3 billion by 2031, as 800 G optics proliferate.

Healthcare deployments illustrate lateral growth. A Shenzhen hospital upgraded to an all-optical LAN and reported a 60% improvement in triage data access times. Tele-robotic surgery trials in Europe used 5G-backed fiber strands to achieve sub-35-millisecond round-trip latency. In industrial settings, distributed acoustic sensing safeguards pipelines and rail corridors. Despite diversifying use cases, communications spending anchors supplier volume forecasts, ensuring economies of scale that subsequently benefit niche applications.

By End-User:

Hyperscale Data Centers Drive Market TransformationTelecom operators locked in a 55.38% share in 2025 owing to cumulative rights-of-way and universal service mandates. Yet the hyperscale and enterprise data-center segment is advancing at 12.01% CAGR and is projected to reach USD 19.95 billion by 2031. This shift tilts R&D toward low-power VCSEL arrays and silicon photonics engines customized for AI workloads.

Corning forecasts a 30% compound sales increase in its enterprise division through 2027 as cloud providers pre-buy capacity. Defense agencies add counter-drone fiber links that demand battle-hardening, while energy majors equip methane-leak monitoring systems with fiber interferometers. Such divergence spreads revenue risk and spurs specialized connector formats, including expanded-beam and hermaphroditic assemblies. Suppliers agile enough to straddle high-volume telecom orders and lower-volume, ruggedized defense contracts secure balanced portfolios.

Geography Analysis

APAC Fiber Optic Component Market

Asia Pacific held 38.74% of the fiber optic component market in 2025 and is growing at 10.44% CAGR. China’s 50 G passive optical network rollout and 10-gigabit city program create step-function increases in optical-line-terminal capacity. Japan’s National Institute of Information and Communications Technology demonstrated 1.02 Pbit/s transmission across 1,808 kilometers, proving that existing terrestrial fiber can meet long-haul AI traffic. Government subsidies ensure that emerging economies such as India and the Philippines fund last-mile fiber, sustaining baseline demand even during macro-slowdowns.

North America Fiber Optic Component Market

North America is the second-largest regional contributor, buoyed by hyperscale campus expansions in Virginia’s data-center corridor and Oregon’s renewable-powered server farms. The U.S. Broadband Equity, Access, and Deployment (BEAD) program allocates USD 42.45 billion for unserved areas, mandating fiber where feasible. Quantum-network testbeds in Boston and Chicago validate ultra-secure key distribution over installed dark fiber, catalysing new categories of ultra-low-loss cabling.

EMEA and LATAM Fiber Optic Component Market

Europe emphasizes industrial automation and quantum-safe government links. Germany recorded quantum communications over existing Deutsche Telekom fiber spanning 76 kilometers without repeaters. The UK taskforce achieved 410-kilometer quantum-secure video transmission in April 2025. Southern European utility firms invest in fiber-based SCADA upgrades, while the Nordics leverage abundant hydropower to attract AI clusters, thereby drawing co-packaged optics demand. Latin America and the Middle East & Africa remain smaller today but log double-digit growth as undersea cable landings and data-center incentives proliferate.

Regulatory Landscape

Policy and permitting reforms are continuing to shape fiber build economics, with downstream pull into passive components used in access and metro builds. In the United States, the Federal Communications Commission (FCC) advanced actions in 2026 that target wireline deployment friction, including a June 2026 draft Notice of Proposed Rulemaking on eliminating barriers to wireline deployments (rights-of-way fees and permitting timelines) and an Order streamlining Broadband Data Collection reporting with changes taking effect July 24, 2026. Together, these steps affect how quickly operators convert funding programs into fiber route miles and component orders.

In Europe, EU-level measures are tightening the linkage between building infrastructure and full-fiber readiness. The Gigabit Infrastructure Act introduces fiber-ready requirements for certain new buildings and major renovations, standardizing in-building physical infrastructure and in-building fiber wiring needs across member states. In parallel, the European Commission adopted the Digital Networks Act proposal in January 2026 to modernize connectivity rules, including national transition planning around copper-to-fiber migration, reinforcing the regulatory tailwind for in-building and last-mile fiber component consumption.

Value Chain Analysis

The value chain spans upstream materials (silica preforms, specialty dopants, compound semiconductor wafers such as InP/GaAs, and precision ceramics), component manufacturing (fiber draw and cabling, connector/ferrule machining, PIC and laser fabrication, module packaging and test), and downstream channels (telecom operators and ISPs, hyperscale and enterprise data centers, system OEMs, and distributors/contract manufacturers). Upstream preform and epitaxy constraints remain the key choke points, with long lead times to add capacity, while downstream demand is increasingly defined by AI-oriented interconnect architectures that pull higher-density connectors, advanced packaging, and low-loss cabling into the bill of materials.

Industry responses are leaning toward multi-sourcing and tighter qualification coordination to stabilize supply and validate interoperability at scale. In 2026, US Conec, Hakusan, and Sanwa Technologies announced agreements to multi-source MMC (very small form factor) multi-fiber connectors and TMT ferrules. In March 2026, the MMC multi-source framework expanded with Corning, Fujikura, and Sumitomo Electric Lightwave to include PRIZM TMT expanded-beam technology. On the active side, partnerships such as Sivers Semiconductors with O-Net Technologies (external laser sources for co-packaged optics) and Point2 Technology with Sumitomo Electric (25G transceiver module development) show vendors distributing risk across lasers, photonics, and assembly-test to reduce time-to-qualification for data center and 5G transport deployments.

Competitive Landscape

The fiber optic component market displays moderate consolidation. Corning, Prysmian, Sumitomo Electric, and Furukawa collectively hold a commanding position in glass preform and cable volumes, whereas Broadcom, Lumentum, and Coherent dominate photonic integrated circuit design. Tier-one incumbents deepen vertical integration to secure material access following gallium and indium volatility. Corning’s new preform line in Poland shortens European lead times, while Prysmian installs ribbon-drawing towers in the United States to localize BEAD contracts.

Technology differentiation intensifies. Coherent’s six-inch indium-phosphide wafers unlock four-fold die counts, raising barriers for smaller foundries. NICT and Sumitomo Electric pushed coupled-core fiber to 1.02 Pbit/s across 1,808 kilometers, laying groundwork for hollow-core upgrades in the next decade[2]Hitoshi Kawashima, “455 Tb/s Stable Transmission Using Coupled-Core Fiber,” NTT Corporation, ntt.com. NTT’s 455 Tb/s multicore trials showed MIMO equalization viability, hinting at roadmap continuity before space-division multiplexing becomes mainstream. Patent litigation rises around co-packaged optic thermal-management designs, particularly among U.S. and Chinese startups.

Strategic partnerships proliferate. Lumen Technologies secured 10% of Corning’s global output through 2026, ensuring AI campus expansions proceed uninterrupted. Sumitomo Electric’s EUR 90 million acquisition of Südkabel expands high-voltage direct current cable offerings for subsea interconnects. Fraunhofer ISE collaborates with European photonics clusters to scale InP-on-GaAs substrates that bypass gallium supply risk. With capital intensity rising, mid-tier players pursue specialization niches such as medical endoscopy fibers, sensing interferometers, or airborne tactical links.

Fiber Optic Component Industry Leaders

Lumentum Holdings Inc.

Broadcom Inc.

Coherent Corp. (II-VI)

Sumitomo Electric Industries Ltd.

Accelink Technologies

- *Disclaimer: Major Players sorted in no particular order

Fiber Optic Component Market Companies Covered in this Report

- Lumentum Holdings Inc.

- Broadcom Inc.

- Coherent Corp. (II-VI)

- Sumitomo Electric Industries Ltd.

- Accelink Technologies

- Fujitsu Optical Components

- Source Photonics

- NeoPhotonics (Cisco)

- O-Net Technologies

- Corning Incorporated

- Prysmian Group

- Sterlite Technologies

- Hisense Broadband

- Innolight Technology

- EMCORE Corporation

- Reflex Photonics

- FiberHome Telecommunication

- Huawei Technologies

- Mwtechnologies LDA

- OptiEnz Sensors

Market Opportunities and Future Outlook

Onshoring and capacity additions across lasers, silicon photonics, transceiver assembly, and fiber/cable manufacturing are opening near-term whitespace for suppliers that can qualify to hyperscaler and carrier specifications while meeting localization requirements tied to public funding. In March 2026, Lumentum announced a new manufacturing facility in Greensboro, North Carolina, focused on InP-based optical devices for large AI data centers. In May 2026, Corning announced a multi-year partnership with NVIDIA tied to expanded US optical connectivity manufacturing, including three new facilities in North Carolina and Texas and a stated 50% increase in domestic fiber production capacity. These actions point to procurement emphasis on US-based supply for AI connectivity buildouts.

High-speed data center optics and high-density connectivity form a second opportunity area, covering 800G and 1.6T transceivers, co-packaged optics building blocks, and connector ecosystems engineered for higher fiber counts per rack. Applied Optoelectronics began expansion at its Pearland, Texas campus in July 2026 to scale 800G and 1.6T optical transceiver production, and Broadcom disclosed third-generation co-packaged optics technology with 200G per lane capability in May 2025. On the cable side, long-duration supply agreements and expansion programs are reshaping sourcing, including Prysmian and Molex signing a 10-year, EUR 5.5 billion agreement in July 2026 for data center optical cables alongside a broader capacity expansion plan. This expands the addressable space for qualified component vendors across US data center corridors and related logistics footprints.

Recent Industry Developments in Fiber Optic Component Market

- March 2026: Lumentum and NVIDIA announced a strategic partnership that included a USD 2 billion investment by NVIDIA in Lumentum via a private placement of convertible preferred stock. The partnership focuses on accelerating R&D and scaling US-based manufacturing capacity for advanced optics used in large AI data centers, reinforcing the shift toward purpose-built datacom optics supply chains.

- May 2025: Broadcom announced third-generation co-packaged optics (CPO) technology featuring 200G-per-lane capability. The update highlighted ecosystem readiness topics such as OSAT process flows, thermal design, and fiber routing, advancing the practical path from pluggable optics toward higher-density switch-adjacent optical interconnects.

- March 2024: Broadcom delivered the Bailly 51.2 Tbps co-packaged optics Ethernet switch integrating eight 6.4 Tbps optical engines with the Tomahawk 5 switch chip. This raised the performance bar for co-packaged architectures and pushed component ecosystems toward tighter integration across optical engines, interposers, and fiber attach.

Fiber Optic Component Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from fiber optic components used to transmit, route, split, amplify, and terminate optical signals across telecom networks, data centers, and enterprise and industrial links, reported in USD value terms.

Scope exclusions: We exclude installation and integration services, refurbished or resold hardware, turnkey network rollout contracts, and copper-based connectivity solutions.

Segments Covered in This Report

- By Type

- Cables

- Amplifiers

- Active Optical Cables

- Splitters

- Connectors

- Transceivers

- Others

- By Application

- Distributed Sensing

- Communications

- Analytical and Medical Equipment

- Lighting

- By End-user

- Telecom Operators

- Hyperscale and Enterprise Data Centers

- Industrial and Energy

- Healthcare and Life-Sciences

- Defense and Aerospace

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirated

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and anchor the model to observable demand signals. We reviewed public infrastructure and connectivity indicators from sources such as the International Telecommunication Union, the World Bank, the U.S. Federal Communications Commission, and national telecom regulators, followed by trade and production signals from sources such as UN Comtrade and national customs portals.

To convert those signals into market value, we also relied on company filings, investor presentations, product catalogs, and reputable standards bodies such as IEEE and the Fiber Broadband Association for terminology and technology transitions. When helpful, a paid subscription focused on company financials and news was used to corroborate revenue direction, and a patent database was checked to understand which component families were seeing faster innovation. These sources are illustrative rather than exhaustive, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary conversations were used to pressure test our assumptions on component mix, pricing movement, and shipment trends across the fiber value chain. We spoke with executives, product leaders, and commercial managers from manufacturers, distributors, and large buyers, and we ensured coverage across major consuming regions so that adoption patterns in telecom, data centers, and industrial networks were reflected. These inputs helped close gaps that desk research cannot fully answer, such as realistic ASP ranges by module class and the timing of technology refresh cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 44% |

| Mid tier: 57% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 17% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started from a top-down build where network expansion and bandwidth demand were translated into component demand pools, which were then valued using observed price bands for key parts. For fiber optic components, the model is kept practical by leaning on signals like fiber-to-the-home passings, data center build activity, 5G and long-haul capacity additions, and mix shifts toward higher-speed optics, which together explain most of the volume movement.

To make sure totals stayed realistic, we corroborated results with selective bottom-up approximations, including sampled supplier revenue roll ups, channel checks on shipment direction, and ASP times volume cross-checks for major component groups such as transceivers, connectors, splitters, and amplifiers. Where public information was patchy (for example, for smaller passive modules sold through distributors), gaps were handled using conservative penetration and replacement-rate assumptions that were reviewed with interviewees.

For forecasting, we used scenario analysis supported by simple time-series smoothing, because near-term demand is sensitive to capex cycles in telecom and data centers. Key drivers that were varied in the scenarios included capex intensity, mix upgrade speed to higher data rates, and regional rollout timing, and then the outputs were reconciled to the adoption expectations shared by industry participants.

Data Validation & Update Cycle

Validation was done through multiple checks so that a single data point could not overly influence the outcome. We compared model outputs against independent signals such as trade direction, public operator rollout plans, and reported demand commentary in earnings materials, and then investigated any large variances before the numbers were finalized.

A second analyst review was used to re-check assumptions, currency handling, and year alignment across inputs, followed by targeted re-contacts when a mismatch stayed unresolved. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp pricing moves, sudden capex resets, or major technology transitions. Before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Fiber Optic Component Market Size Measured Against Other Published Estimates

Published market values for fiber optic components can vary because each publisher may count a different set of items and may choose a different start year for the same growth story. Differences also come from how pricing is treated, because average selling prices for optics and passive parts do not move in the same direction every year.

The biggest gap drivers are usually whether fiber optic cables and active optical cables are counted fully as components, how much of installation and rollout spending is included, and whether refurbished equipment is treated as new demand. Timing matters too, because some estimates lean on older operator capex cycles, while others assume a faster switch to higher-speed modules that lifts value even when unit volumes are steady.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.81 B (2026) | |

| Industry Publisher A | USD 36.38 B (2025) | Uses a different base year and may bundle a wider set of cable-related demand and adjacent spend into the total, which makes the definition less comparable for component-only sizing. |

| Trade Journal B | USD 28.62 B (2024) | Relies more on historic revenue curves and can understate recent price and mix uplift from higher-speed optics, and then the USD value can shift further based on currency timing. |

The spread in the table is mostly explained by scope boundaries and by which year is treated as the current reference point, followed by how quickly pricing and mix are refreshed as speeds move up. When installation services, refurbished units, and turnkey rollout spending sit outside scope, and when the model is rechecked against year-specific mix shifts in transceivers and passive modules, the totals stay closer to real component demand signals, which is how the sizing is handled by Mordor Intelligence.

Key Questions Answered in the Report

How large is the fiber optic component market in 2026?

The fiber optic component market size is USD 38.81 billion in 2026 and is forecast to climb to USD 61.24 billion by 2031.

Which region leads the fiber optic component market growth?

Asia Pacific holds 38.74% revenue share and is expanding at a 10.44% CAGR, driven by national broadband rollouts and photonics manufacturing capacity.

What segment is growing fastest within the fiber optic component market?

Active optical cables show the highest growth at 10.97% CAGR, reflecting hyperscale data-center adoption of co-packaged optics.

How are supply-chain constraints affecting suppliers?

Gallium and indium export restrictions inflate material costs, prompting vertical integration and alternative substrate R&D such as InP-on-GaAs solutions.

What recent breakthrough sets the bandwidth benchmark?

NICT and Sumitomo Electric achieved 1.02 Pbit/s over 1,808 kilometers, demonstrating the future headroom for long-haul fiber systems.

Which end-user segment is fastest growing?

Hyperscale and enterprise data centers are advancing at 12.01% CAGR as AI training clusters demand ultra-high-speed optical interconnects.

Page last updated on: