Commercial P2P CDN Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

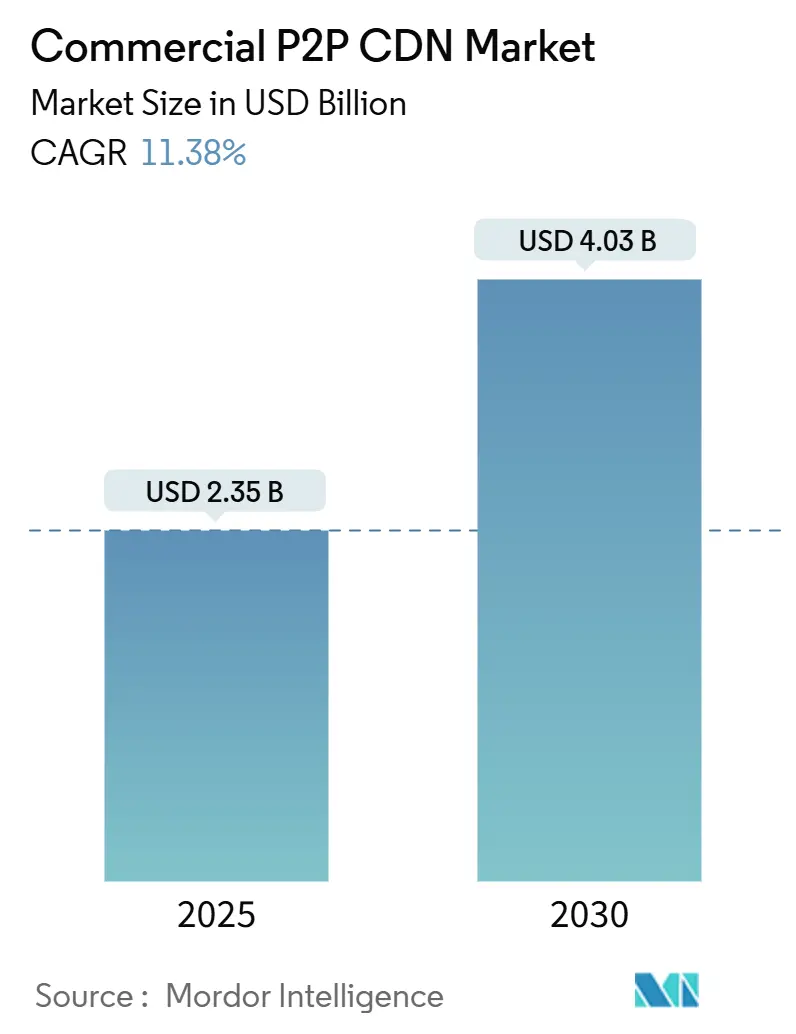

| Market Size (2025) | USD 2.35 Billion |

| Market Size (2030) | USD 4.03 Billion |

| Growth Rate (2025 - 2030) | 11.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial P2P CDN Market Analysis by Mordor Intelligence

The Commercial P2P CDN market size stood at USD 2.35 billion in 2025 and is forecast to reach USD 4.03 billion by 2030, expanding at an 11.38% CAGR over the period. Demand growth is rooted in higher-resolution video, livestream gaming, and mobile-first viewing habits that overload traditional CDNs while raising origin-bandwidth costs for publishers. Enterprises recognize that peer bandwidth sharing can trim egress fees, so hybrid architectures that mix edge nodes with browser-based P2P are moving into mainstream deployments. Browser support for WebRTC and service-worker caching has matured, allowing vendors to assure basic security and playback quality. Meanwhile, Open-Caching standards from the Streaming Video Alliance simplify interconnection with Tier-1 ISPs, letting operators keep popular assets inside metro footprints and cut backbone traffic.

Key Report Takeaways

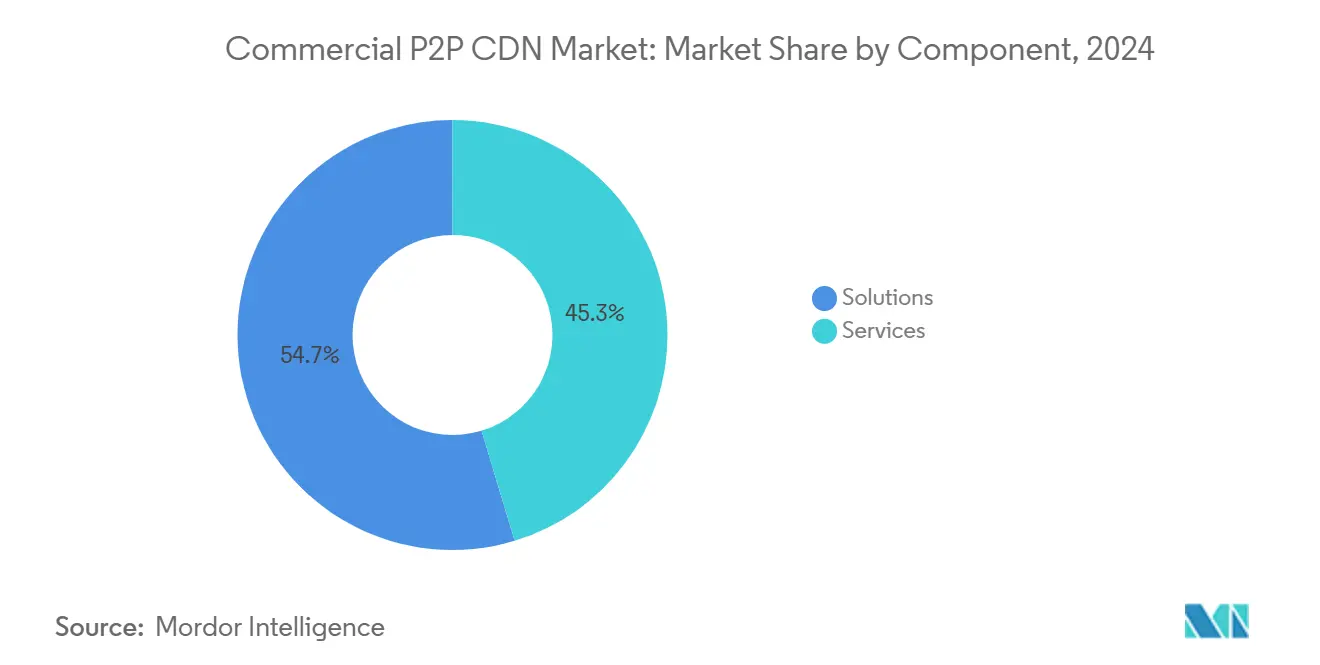

- By component, solutions led with 54.67% of Commercial P2P CDN market share in 2024, while services are projected to grow at 12.56% CAGR to 2030.

- By content type, video accounted for 67.43% of the Commercial P2P CDN market size in 2024; gaming traffic is set to advance at 15.65% CAGR through 2030.

- By vertical, media and entertainment retained 41.43% revenue share in 2024, whereas gaming shows the fastest trajectory at the same 15.65% CAGR.

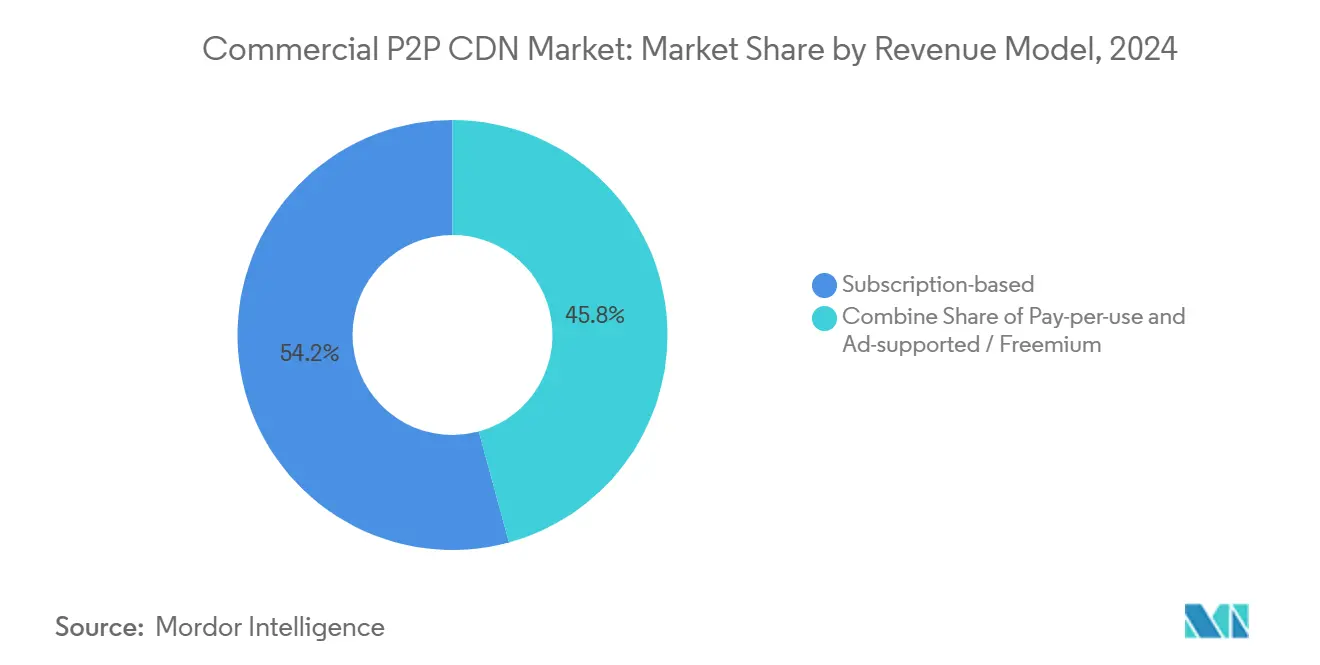

- By revenue model, subscriptions controlled 54.23% share in 2024, and pay-per-use is forecast to rise at 13.42% CAGR.

- By end-user, large enterprises held 68.34% share in 2024, yet SMEs will grow at 12.92% CAGR as self-service platforms lower entry barriers.

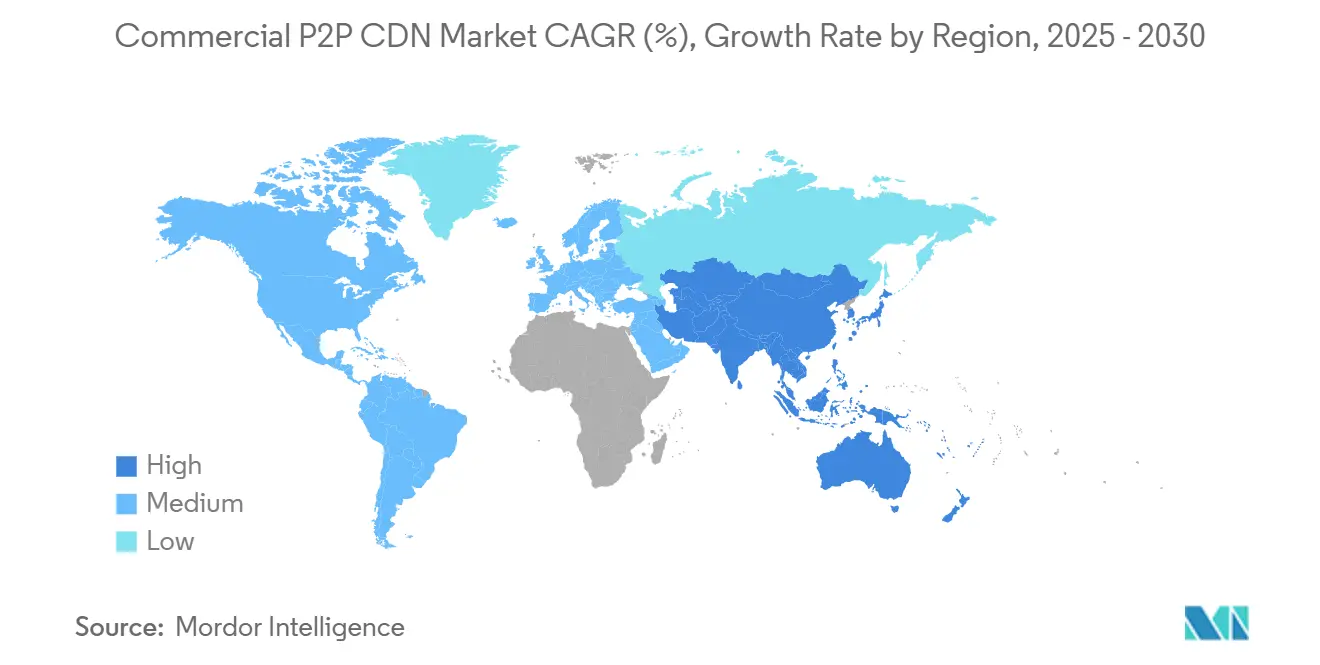

- By region, North America captured 39.68% share in 2024, but Asia-Pacific is expected to post the strongest 14.98% CAGR through 2030.

Global Commercial P2P CDN Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTT video-streaming boom | +2.8% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Online gaming and e-sports traffic surge | +2.1% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Cost-effective origin-offload via peer bandwidth | +1.9% | Global, notably Europe | Long term (≥ 4 years) |

| Open-Caching adoption by Tier-1 ISPs | +1.6% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Edge-assisted VR/AR live-event delivery | +1.4% | North America and Europe, early Japan uptake | Long term (≥ 4 years) |

| Carbon-reduction mandates favor decentralized CDNs | +1.0% | Europe first, then North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OTT Video-Streaming Boom

Global streaming traffic reached 68 exabytes in 2024, doubling since 2020. Next-generation 8K pilots, such as Ateme and Focal Point VR’s broadcast to Apple Vision Pro, confirm that bitrate requirements are rising beyond what legacy edge footprints alone can sustain. [1]Aten & Focal Point VR, “8K Live Streaming to Apple Vision Pro,” ateme.com Ad-supported plans add concurrency spikes because viewers join simultaneously at show premieres. Adaptive-bitrate ladders now exceed 15 rungs for personalized streams, so peer replication helps keep hot segments near users while alleviating mid-haul links.

Online Gaming and E-Sports Traffic Surge

E-sports audiences hit 640 million and generated USD 1.617 billion in 2024. [2]BaishanCloud, “How CDN Helps e-Sports Live Streaming,” intl.baishancloud.comTeleport Media’s Euro 2020 coverage showed 70% offload with 470,000 concurrent viewers. Sandbox Interactive trimmed distribution bills by 40% after moving patch delivery to a P2P-enabled network. Converged edge-cloud nodes process positional data closer to players, then peers disseminate spectator feeds, cutting latency for both game logic and broadcast layers.

Cost-Effective Origin-Offload via Peer Bandwidth

Enterprises wrestle with cloud egress fees that scale linearly with traffic. Tutorials on AWS cost control consistently rank peer‐assisted delivery among top mitigation levers. Novage’s Media Loader achieves up to 80% bandwidth savings for VOD libraries by letting browsers exchange segments. Microsoft Connected Cache embeds peer nodes within ISP points-of-presence to keep Windows and Xbox updates on-net, reducing transit fees and improving throughput. [3]Microsoft, “Microsoft Peering,” microsoft.com

Open-Caching Adoption by Tier-1 ISPs

Comcast’s edge platform uses Qwilt reference software to present a standardized interface for content owners. Open-Caching nodes identify asset popularity in real time, so P2P swarms form where demand is highest. Rural operators benefit as well; Capcon Networks’ Connect-IX project with DE-CIX offers direct interconnection for community ISPs, letting local peers fulfill traffic without backhaul links.. Standards from GSMA Open Ga.teway extend the model to mobile carriers across Asia-Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and security risks across peers | −1.8% | Global, sharpest in Europe | Short term (≤ 2 years) |

| QoS unpredictability on heterogeneous last-mile | −1.3% | Global, higher in emerging markets | Medium term (2-4 years) |

| Browser security rules limiting service-worker P2P | −0.9% | Global implementations | Short term (≤ 2 years) |

| Cloud egress-fee discounts narrowing P2P advantage | −0.7% | North America and Europe enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Security Risks Across Peers

Decentralized delivery surfaces the risk that malicious nodes may inject tampered segments. Studies on IPFS highlight anonymity abuse where harmful objects masquerade as legitimate files. [4]Athens University of Economics and Business, “Investigating Anonymity Abuse in IPFS,” arxiv.orgEthereum network research shows that validator IPs can be deanonymized, suggesting similar exposure patterns for P2P CDN topologies. Regulated industries demand Web Application Firewalls and tokenized URLs when adopting peer delivery, which raises deployment complexity. CableLabs warns that residential proxies could become stepping stones for botnets if node reputation is not enforced.

QoS Unpredictability on Heterogeneous Last-Mile

Peer churn and asymmetric access links disrupt smooth bitrate ladders. Academic work applying Q-learning with fuzzy logic finds that throughput can swing widely without predictive peer scoring. Edge-cloud queuing models reveal service-quality dips during VM migrations, compounding variability for multi-CDN handoffs. QUIC pacing gaps above 2 Gbps require kernel-level tuning; otherwise, stalls appear in high-rate streams. Enterprises with SLA-bound workloads, therefore, lean on hybrid setups where a fall-back to traditional edges maintains baseline performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hybrid Platforms Anchor Adoption

Solutions generated 54.67% revenue in 2024, forming the backbone of Commercial P2P CDN market deployments. These platforms bundle peer-coordinator logic, multi-CDN failover, and analytics dashboards that align with existing DevOps tooling. Large streaming services prefer unified consoles because they already manage hundreds of edge POPs worldwide. The services segment, though smaller, will outpace at 12.56% CAGR as customers seek managed onboarding, performance audits, and 24 × 7 security operations. Integrators design swarm-tuning algorithms that match peer upload capacity with content popularity curves, removing guesswork for in-house teams.

Akamai’s cloud-computing business rising 24% year over year exemplifies how CDNs reposition as full-stack providers that weave P2P modules into broader compute fabrics. That convergence accelerates contract size, and it draws SMEs that lack specialist staff. Consequently, services will keep lifting the Commercial P2P CDN market even once core software penetration plateaus.

By Content Type: Video Remains the Workhorse

Video streaming held 67.43% share in 2024 within the Commercial P2P CDN market. Viewer tolerance for buffering is low, and average bitrates rose beyond 12 Mbps for 4K content in 2025. Adaptive ladders and thumbnail scrubbing multiply segment requests, making peer caching efficient. The segment is forecast to add another 12.78% CAGR as UHD, HDR, and spatial audio spread. Non-video objects—software patches, static web assets, and IoT firmware—earn steady but narrower adoption; their workflows depend more on checksum validation and occasional spikes, such as a game launch.

Wowza’s roadmap, which prioritizes Open-Caching hooks and AI routing, shows incumbent encoders relying on peer hand-off for top profiles. Meanwhile, blockchain experiments like VidBlock illustrate attempts to combine segment attestation with decentralized seed nodes.

By Vertical: Gaming Takes the Growth Crown

Media and entertainment accounted for 41.43% of the Commercial P2P CDN market size in 2024, but gaming will scale faster at 15.65% CAGR. AAA updates often exceed 50 GB, and simultaneous release windows stress single-origin models. P2P shards distribute payloads across active gamers, ensuring regional parity. E-sports broadcasts also prize real-time sync; P2P meshes keep camera feeds in lock-step to avoid spoiler disparities. Other verticals—e-commerce, BFSI, education—adopt P2P for niche workflows such as product-asset bursts or secure document delivery, yet security evaluations slow rollouts.

Akamai’s collaboration with Riot Games on global match delivery underscores the performance stakes in professional circuits. Cost relief is persuasive too; finance houses cite egress invoices as top-three infra-line items, nudging trials for internal research portals.

By Revenue Model: Usage-Based Plans Gain Favor

Subscription bundles still dominated at 54.23% in 2024, giving finance teams stable monthly forecasting. However, pay-per-use schemes are projected to climb 13.42% CAGR because they align spend with unpredictable peaks. Event-driven streamers and seasonal e-commerce players can burst without over-provisioning. Cloudflare posted USD 479.1 million Q1 2025 revenue and attributes a quarter of new bookings to usage-metered edge functions, including peer-assist toggles.

Ad-supported tiers and freemium models address viewers unwilling to pay subscription fees. They rely on P2P to offset monetization dilution because publisher margins tighten when advertising CPMs fluctuate. Mix-and-match pricing, where core traffic sits on a flat plan while overage storms revert to usage rates, is emerging as a compromise that mitigates bill shock yet keeps budget clarity.

By End-User: Democratization Reaches SMEs

Large enterprises commanded 68.34% share in 2024, driven by multi-region OTT operators, major studios, and cloud-gaming hosts. These organizations integrate peers into CI/CD pipelines and real-time analytics suites. Yet platform simplification now unlocks SME participation, pushing a 12.92% CAGR through 2030. Self-service portals auto-generate embed scripts, and SaaS dashboards surface peer heatmaps so non-specialists can troubleshoot.

Sandbox Interactive’s 40% cost savings validate the value proposition for mid-sized game studios. Education providers follow suit; lecture videos packaged in segment playlists seed from campus labs to remote students. The Commercial P2P CDN market thereby widens its customer base beyond early adopters.

Geography Analysis

North America led the Commercial P2P CDN market with 39.68% revenue share in 2024. OTT ecosystems are mature, broadband penetration is high, and enterprises have budget for multi-layer delivery stacks. Akamai booked USD 1.015 billion Q1 2025 revenue with 52% from U.S. clients, reflecting sustained regional investment. Gaming alliances such as Akamai-Riot combine P2P logic with edge POPs to guarantee match integrity. Regulatory mood remains supportive; no federal laws restrict peer videostreaming, and state privacy bills focus more on user consent than network architecture.

Asia-Pacific is the fastest climber at 14.98% CAGR to 2030, benefiting from mobile-first demographics and state-backed cloud expansion. Regional data-center capacity reached 12,206 MW in 2024 with another 14,338 MW planned, giving suppliers local seeding hubs. AWS will invest JPY 2.26 trillion (USD 15.1 billion) in Japan by 2027, bolstering edge fabric available for hybrid P2P deployments. Japan’s video-distribution market climbed to JPY 571 billion (USD 3.8 billion) in 2024, tightening the need for bandwidth-efficient delivery PRTIMES.JP. China’s data-localization rules complicate cross-border CDN flows, so peer-assisted clusters that operate inside domestic ISPs gain favor.

Europe remains pivotal due to sustainability regulation. Operators signed a pact to run 75% renewable energy by 2025 and 100% by 2030, accelerating adoption of architectures that reduce central compute. Open-Caching tests in Germany and France show 30–50% backhaul savings, supporting ISP enthusiasm. Data-sovereignty stipulations under GDPR push vendors to add geo-fencing that keeps peer swarms inside EU borders, indirectly stimulating localized node density.

Competitive Landscape

Competition in the Commercial P2P CDN market mixes legacy CDNs embedding peer engines and specialists providing peer-only stacks. Akamai, Cloudflare, and AWS use scale advantages to bundle P2P with edge compute, WAF, and media services. Akamai acquired Noname Security for USD 450 million to tighten API defenses, addressing concerns that peer-injected segments may exploit unprotected endpoints. Cloudflare partnered with Kyndryl to package Zero-Trust consultancy with its connectivity cloud, positioning against complex enterprise migrations.

Niche vendors—Streamroot, Hive Streaming, Teleport Media—differentiate through algorithmic mesh formation and viewer-experience telemetry tuned for high-density events. Pipe Network proposes a permissionless node marketplace where small businesses host micro-POPs and earn tokens for bandwidth. Such decentralization could erode entry barriers for regional content owners.

Security and analytics remain battlegrounds. Providers race to certify SOC 2 Type II and ISO 27001 while embedding AI anomaly detection. Multi-CDN orchestration that toggles between peer, private, and public edges is now table stakes. Vendors also court ISPs: Qwilt signs revenue-share deals giving operators a slice of delivery fees; this alignment encourages cache insertion lower in the network and makes P2P overlays more stable.

Overall, mid-level fragmentation persists because top five players together command roughly 45% revenue. Integration hurdles and specialized latency requirements leave room for focused entrants.

Commercial P2P CDN Industry Leaders

Akamai Technologies Inc.

Amazon Web Services Inc.

Cloudflare Inc.

Microsoft Corp. (Peer5 Inc.)

Fastly Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ateme and Focal Point VR streamed the first live 8K feed to Apple Vision Pro, demonstrating bandwidth demands that reinforce P2P value.

- February 2025: Akamai Technologies secured a multi-year strategic agreement exceeding USD 100 million with a major technology company for managed Kubernetes clusters, expanding global delivery capacity.

- February 2025: Capcon Networks launched Connect-IX with DE-CIX to improve rural traffic exchange, making peer acceleration accessible to underserved regions.

- June 2024: Akamai partnered with Digital China to strengthen security sales channels amid fast-growing Chinese demand.

Global Commercial P2P CDN Market Report Scope

| Solutions |

| Services |

| Video |

| Non-Video |

| Media and Entertainment |

| Gaming |

| E-commerce |

| BFSI |

| Education |

| Other Vertical |

| Subscription-based |

| Pay-per-use |

| Ad-supported / Freemium |

| SMEs |

| Large Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Solutions | ||

| Services | |||

| By Content Type | Video | ||

| Non-Video | |||

| By Vertical | Media and Entertainment | ||

| Gaming | |||

| E-commerce | |||

| BFSI | |||

| Education | |||

| Other Vertical | |||

| By Revenue Model | Subscription-based | ||

| Pay-per-use | |||

| Ad-supported / Freemium | |||

| By End-User | SMEs | ||

| Large Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Commercial P2P CDN space today?

The Commercial P2P CDN market size reached USD 2.35 billion in 2025 and is on track for USD 4.03 billion by 2030, expanding at 11.38% CAGR.

Which segment is growing fastest within peer-assisted delivery?

Gaming applications post the highest 15.65% CAGR owing to large game-file updates and e-sports livestream traffic bursts.

Why are enterprises shifting from traditional CDNs to hybrid P2P models?

They aim to reduce cloud egress expenses, improve scalability for peak events, and comply with regional carbon targets without adding new data-center footprint.

Which region offers the strongest future upside?

Asia-Pacific leads with a projected 14.98% CAGR through 2030, supported by heavy data-center expansion and soaring mobile streaming demand.

What is the biggest adoption barrier for regulated industries?

Data-privacy and content-integrity concerns remain paramount because P2P exposes assets to untrusted peers, necessitating robust encryption and validation layers.

How do usage-based pricing plans influence vendor selection?

Pay-per-use models give event-driven services cost flexibility, making vendors that support granular metering attractive to both SMEs and large enterprises.

Page last updated on: