China Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

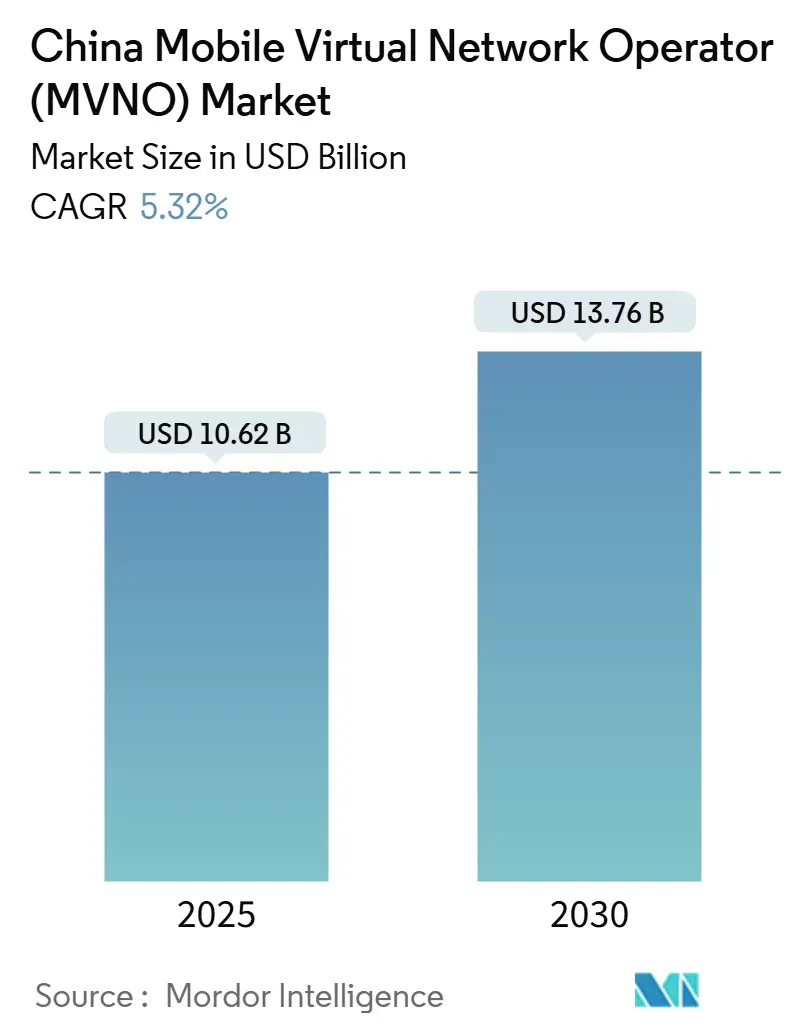

| Market Size (2025) | USD 10.62 Billion |

| Market Size (2030) | USD 13.76 Billion |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

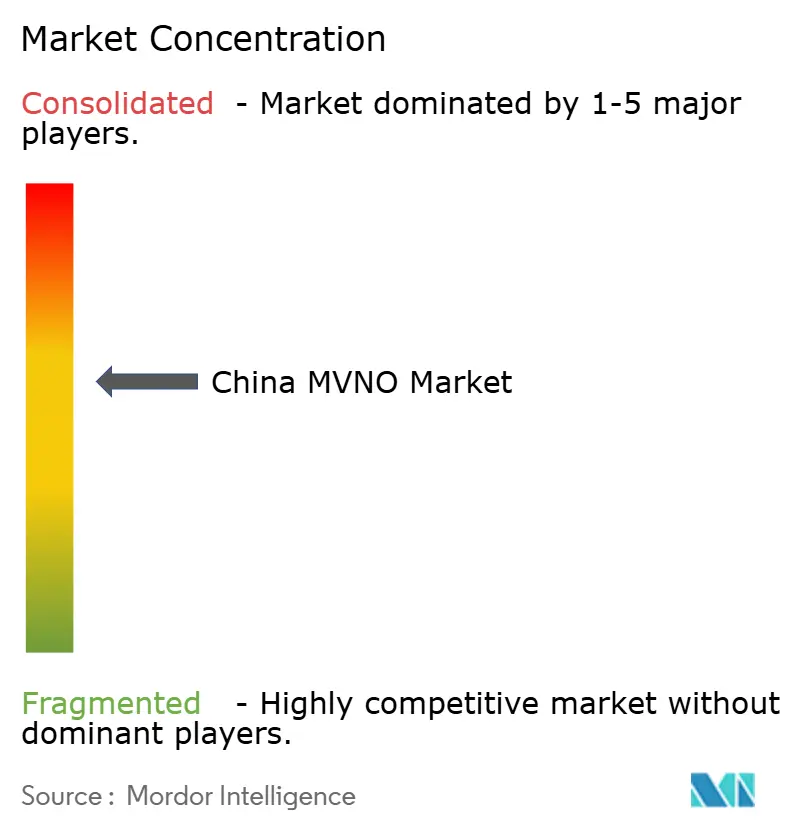

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

The China Mobile Virtual Network Operator Market size is estimated at USD 10.62 billion in 2025, and is expected to reach USD 13.76 billion by 2030, at a CAGR of 5.32% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 82.34 million subscribers in 2025 to 100.99 million subscribers by 2030, at a CAGR of 4.17% during the forecast period (2025-2030). Steady wholesale-rate discounts from the three nationwide MNOs, faster 5G rollout in Tier 1-2 cities, and the first commercial pilots of e-CNY-enabled SIM wallets are raising service innovation and average revenue per user. Enterprise outsourcing of private 5G networks to specialist virtual operators is unlocking long-term contracts, while rural revitalization funds are subsidizing coverage in underserved western and northern provinces. Digital-only licensing, real-time e-KYC verification, and network-slice marketplaces together lower barriers for cloud-native entrants seeking to differentiate beyond price.

Key Report Takeaways

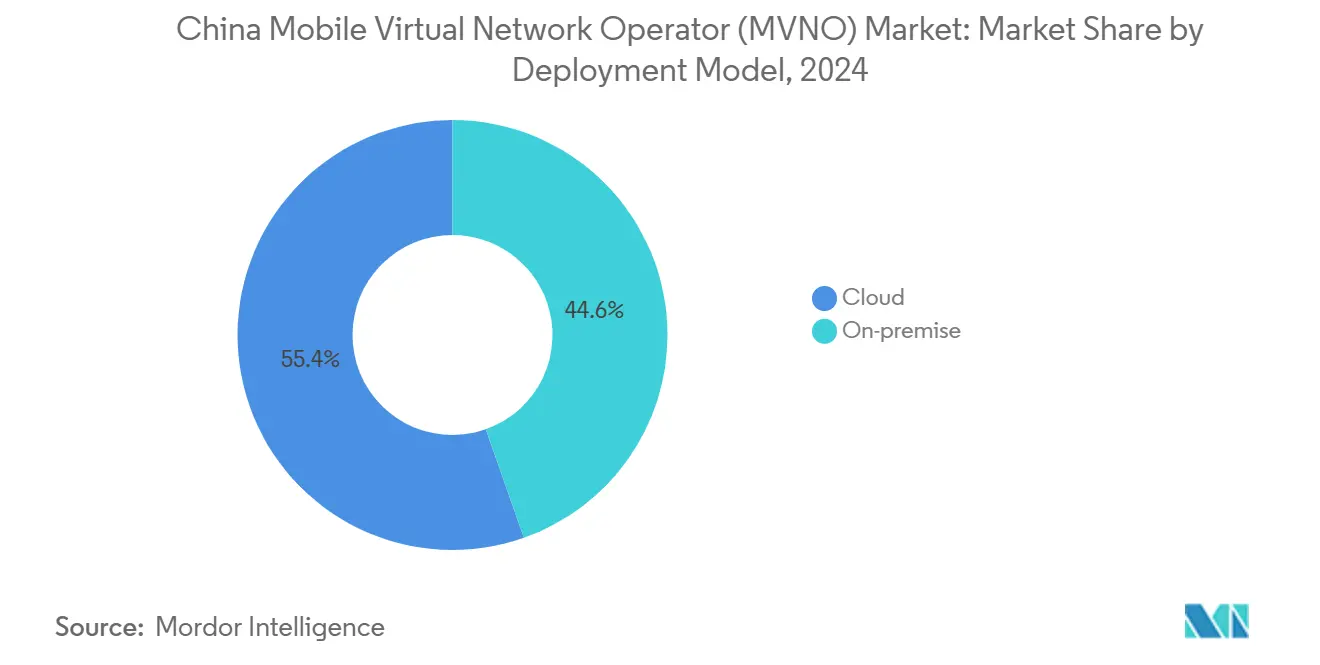

- By deployment model, cloud platforms held 55.40% of the China Mobile Virtual Network Operator Market share in 2024 and are expanding at a 9.77% CAGR to 2030.

- By operational mode, reseller/light/brand MVNOs led with 38.83% revenue share in 2024, while full MVNOs are projected to post the fastest 11.48% CAGR to 2030.

- By subscriber type, consumer accounts for 69.81% of the China Mobile Virtual Network Operator Market size in 2024, whereas enterprise subscriptions are accelerating at a 13.05% CAGR to 2030.

- By application, discount services retained a 31.09% share of the China Mobile Virtual Network Operator Market size in 2024; business services are advancing at a 9.00% CAGR to 2030.

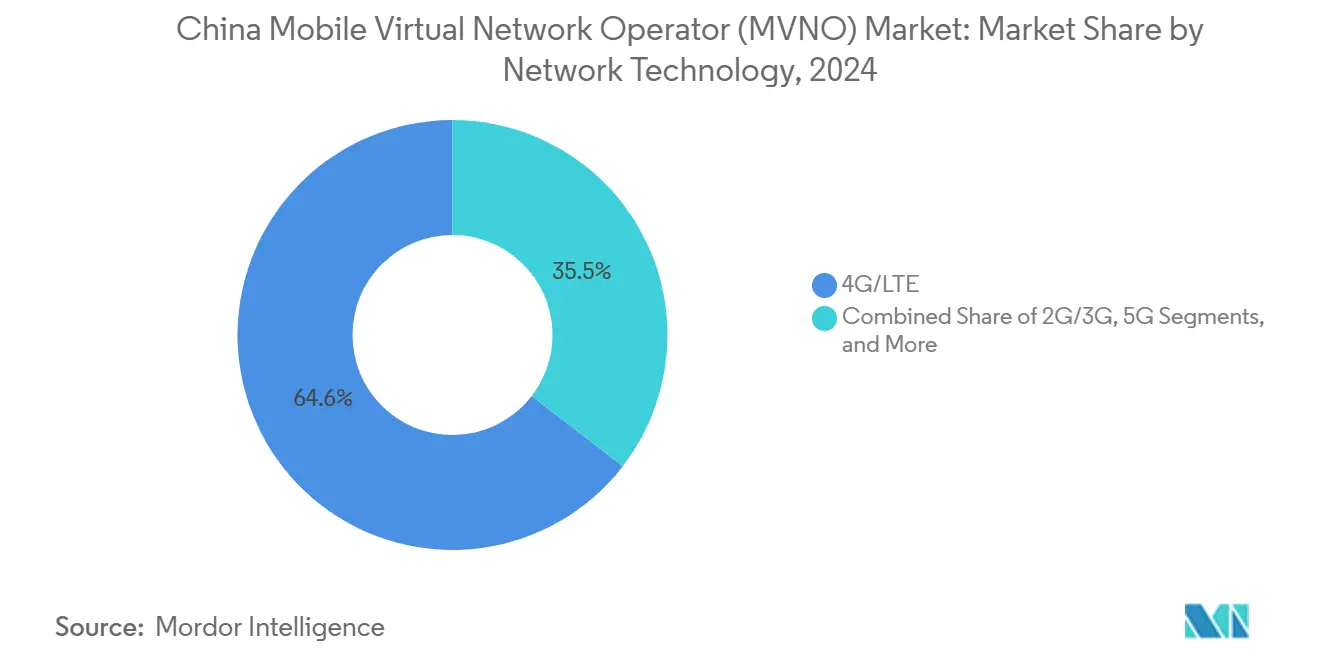

- By network technology, 4G/LTE commanded a 64.55% share in 2024, yet 5G subscriptions are soaring at a 23.72% CAGR to 2030.

- By distribution channel, online and digital-only sales captured a 44.79% share in 2024 and are predicted to grow at a 7.51% CAGR to 2030.

China Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened 5G wholesale-rate discounts from MNOs | +1.2% | Tier 1-2 urban clusters | Medium term (2-4 years) |

| Digital-only onboarding mandates for MVNO licenses | +0.8% | Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Industrial IoT private-network outsourcing boom | +1.5% | Manufacturing belts in Guangdong, Jiangsu, Zhejiang | Long term (≥ 4 years) |

| e-CNY (digital-yuan) integration with SIM/eSIM wallets | +0.7% | Pilot zones in major metro areas | Medium term (2-4 years) |

| Telco cloud-API marketplaces opening to third parties | +0.9% | National innovation zones | Medium term (2-4 years) |

| Rural revitalization subsidies for virtual operators | +0.4% | Inner Mongolia, Xinjiang, Tibet | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened 5G wholesale-rate discounts from MNOs

China’s three host networks now rebate 30-40% off standard wholesale tariffs for virtual operators bundling 5G slices with data plans, a policy that monetizes the USD 180 billion 5G footprint while sustaining traffic growth.[1]China Mobile Limited, “2024 Annual Report,” China Mobile, chinamobileltd.com Telcos secure scale economics and MVNOs gain price headroom to position premium plans. About 9,000 enterprise network slices were active by late 2024, creating fresh use cases that lift virtual operator ARPU.

Digital-only onboarding mandates for MVNO licenses

The Ministry of Industry and Information Technology requires e-KYC, facial biometrics, and electronic SIM provisioning for all new MVNOs, slashing onboarding costs by close to 65% and compressing activation to minutes.[2]Ministry of Industry and Information Technology, “Digital Transformation Guidelines for Telecommunications Industry,” MIIT, miit.gov.cn Operators integrating the APIs directly into cloud CRMs now convert online leads into paying subscribers at higher rates and with fewer fraud cases.

Industrial IoT private-network outsourcing boom

Factory owners in the coastal manufacturing corridor increasingly delegate 5G campus networks to full MVNOs that bundle slice management, edge security, and device analytics. Industrial IoT contracts touched USD 6.4 billion by 2026, accounting for 40% of China’s private 5G spend. Multi-year deals improve revenue visibility for virtual operators and deepen technical collaboration with cloud providers.

e-CNY integration with SIM/eSIM wallets

The People’s Bank of China cleared technical standards for storing digital-yuan credentials on secure SIM elements, enabling offline proximity payments that bypass apps.[3]People’s Bank of China, “Digital Yuan Integration Technical Standards,” PBoC, pbc.gov.cn MVNOs collect 0.1-0.3% per transaction plus wallet service fees, positioning connectivity providers as key rails for the national digital-currency rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising national-roaming settlement floor-prices | -0.6% | Nationwide | Short term (≤ 2 years) |

| Stricter real-name / facial-ID verification costs | -0.4% | Nationwide | Short term (≤ 2 years) |

| Edge-cloud interconnect bottlenecks for MVNO slices | -0.3% | Dense urban cores | Medium term (2-4 years) |

| Convergence of MNO sub-brands cannibalizing niches | -0.5% | Price-sensitive consumer tiers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising national-roaming settlement floor prices

New rules set a nationwide minimum for inter-provincial roaming wholesale, inflating MVNO variable costs by roughly 18% and prompting budget brands to either tighten regional targeting or absorb margin erosion. In China, rising national-roaming settlement floor prices are squeezing the operating margins of MVNOs. Elevated wholesale access fees curtail pricing flexibility, hinder the acquisition of low-ARPU customers, and diminish competitiveness against operators with their own facilities. Given the importance of roaming for comprehensive nationwide coverage, these escalating costs are not only denting profitability but also hindering the expansion of MVNOs, particularly in budget and IoT-centric segments.

Stricter real-name verification costs

Every new SIM now triggers a biometric and document-authentication check, costing USD 0.17 in 2024 and trending to USD 0.15 by 2029, adding fixed onboarding overhead that weighs more heavily on small brands. Chinese MVNOs face rising compliance and onboarding costs due to tightened real-name verification requirements. Enhanced identity-proofing, biometric validation, and state database integration not only elevate operational overheads but also delay SIM activation cycles. For MVNOs catering to low-margin prepaid users, these added verification expenses diminish acquisition efficiency and impede swift scaling, especially in digital-only and budget-friendly models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure drives scalability

Cloud platforms account for 55.40% of the China Mobile Virtual Network Operator Market share in 2024 and are advancing at a 9.77% CAGR, underscoring their role in rapid service rollout and OPEX flexibility. The China Mobile Virtual Network Operator Market size attached to cloud deployments is projected to widen as operators spin up virtualized core functions, tap automated orchestration, and align with pay-as-you-grow business strategies.

The shift lets MVNOs launch differentiated 5G slices and edge compute services without spending on physical switches and data centers. Cloud partners such as Alibaba Cloud provide API templates that cut development cycles, enabling real-time rating, e-CNY billing, and AI-based churn prediction. Vendors now pre-integrate compliance modules for digital identity and lawful intercept, reducing regulatory friction and accelerating time-to-revenue.

By Operational Mode: Full MVNOs emerge as growth leaders

Reseller and light MVNOs held 38.83% revenue share in 2024, reflecting earlier regulatory caution. However, full MVNOs are set to expand at 11.48% CAGR, supported by simplified interconnect tests and spectrum-sharing pilots that deepen control over core signaling planes. China Mobile Virtual Network Operator Market participants adopting full control gain freedom to implement quality of service policies and low-latency IoT profiles unavailable under resale contracts.

Service operators occupy a bridge position, leasing core elements yet managing product design. Their moderate growth indicates market appetite for partial autonomy without heavy capital ties. Full MVNOs, often technology firms or cloud providers, pursue service differentiation through network APIs, edge security, and data analytics, all of which strengthen customer stickiness and improve margins.

By Subscriber Type: Enterprise acceleration reshapes dynamics

Consumer lines still command 69.81% of the China Mobile Virtual Network Operator Market size as of 2024, but enterprise subscriptions are expanding at a 13.05% CAGR. Industrial IoT gateways, connected robotics, and smart-logistics trackers demand SLA-backed connectivity and edge intelligence that MVNOs tailor via 5G slices. Enterprise ARPU runs multiple times higher than consumer prepaid accounts, improving operator gross margin and lifetime value.

IoT-specific lines illustrate the evolution toward device-centric billing and lifecycle management. MVNOs package provisioning portals, secure device credentials, and lifecycle analytics to position themselves as single-pane orchestration partners for manufacturers. The mix shift elevates quality-of-service expectations and drives deeper collaboration with cloud hyperscalers and edge platform vendors.

By Application: Business services drive premium positioning

Discount plans maintain a 31.09% share, anchored by students and migrant workers seeking low-cost voice-data bundles. Business services, however, record the fastest 9.00% CAGR as enterprises embed cellular connectivity into production lines, point-of-sale devices, and remote asset monitors. The China Mobile Virtual Network Operator Market continues to migrate from pure price competition to value-added bundles featuring analytics dashboards, device management suites, and integrated payment rails.

Cellular M2M applications serve energy metering, smart parking, and telematics, highlighting multi-year contracts with predictable volumes. Beyond M2M, MVNOs now explore network-slice as a service for cloud gaming, immersive training, and high-definition video surveillance. These premium services rely on 5G’s low latency and ISO-layer slicing, cementing MVNO relevance within broader digital transformation roadmaps.

By Network Technology: 5G transformation accelerates

4G/LTE still provides 64.55% of active lines, but 5G subscriptions leap at 23.72% CAGR as consumers upgrade handsets and enterprises demand ultra-reliable low-latency links. The China Mobile Virtual Network Operator Market leverages nationwide 5G coverage of more than 3.6 million base stations to craft differentiated product tiers and QoS-backed enterprise offers.

Legacy 2G/3G sunsets free spectrum for 5G expansion, while Satellite/NTN trials target agriculture, mining, and border-security use cases. MVNOs integrate satellite backhaul into multi-bearer SIMs to provide fallback coverage in sparsely populated western regions. As 5G Advanced gains momentum after 2027, virtual operators plan to exploit integrated sensing and AI networking to further distinguish premium products.

By Distribution Channel: Digital-first strategy dominates

Online and app-based sales captured a 44.79% share and are set to grow 7.51% CAGR, driven by e-commerce deep links, embedded e-KYC widgets, and instant eSIM activation. The China Mobile Virtual Network Operator Market benefits from customer expectations shaped by super-apps, where purchasing a data plan is as seamless as ordering food.

Traditional retail retains relevance for high-touch device bundling and elderly support but suffers from higher fixed costs. Carrier sub-brand stores blend physical support with digital upgrades, while wholesale channels feed affinity groups such as ride-hailing drivers or delivery couriers. Digital distribution enables real-time plan personalization, AI-assisted upselling, and lower churn, amplifying scale advantages for cloud-native entrants.

Geography Analysis

Tier 1 and Tier 2 metropolitan areas anchor revenue because of early 5G handsets, dense enterprise campuses, and higher disposable income. Beijing, Shanghai, and Shenzhen host pilot programs for e-CNY wallets and network-slice marketplaces, making them test beds for premium MVNO services. Coastal manufacturing provinces, Guangdong, Jiangsu, and Zhejiang, order private 5G slices for smart factories, propelling industrial IoT subscriptions and supporting long-term service contracts.

Eastern regions enjoy mature fiber backhaul and urban density that lower per-site costs. Yet market saturation drives MVNOs to cultivate Tier 3-4 cities where mobile penetration remains below national averages, and local brands compete on localized content and customer service. The China Mobile Virtual Network Operator Market leverages provincial e-government portals to cross-sell digital IDs and pension apps, integrating connectivity with daily life services.

Rural revitalization initiatives allocate subsidies to Inner Mongolia, Xinjiang, and Tibet. Virtual operators partnering with China Unicom connect digital village kiosks and drone-based logistics corridors, unlocking new demand clusters. Satellite backhaul combined with low-band 5G macro sites extends coverage to border checkpoints and mining zones, creating incremental revenue with minimal competition. The western build-out also diversifies revenue away from crowded eastern corridors, balancing network loads.

Competitive Landscape

Alibaba Mobile bundles connectivity with Taobao loyalty points and Ant Group wallets, funneling e-commerce traffic into prepaid packages and boosting stickiness. JD Mobile pairs same-day SIM delivery with JD Logistics’ network, turning device upgrades into immediate connectivity sales. Both brands exploit data lakes and AI models to refine offer targeting, reducing marketing spend per acquisition.

Pure-play MVNOs differentiate through enterprise-grade service catalogs, SLA dashboards, and domain-specific solutions such as smart-factory network management. Cloud-native newcomers integrate telco platform APIs, including real-time charging, location services, and slice orchestration, into DevOps pipelines to push weekly feature releases. These capabilities matter as MNO sub-brands like China Mobile’s Pengyou intensify price competition. Consolidation is probable as biometric compliance, roaming floor prices, and technology investment together raise scale thresholds.

China Mobile Virtual Network Operator Industry Leaders

Snail Mobile Century Snail Communications Technology Co., Ltd.

Guangzhou 263 Mobile Communications Co., Ltd.

Guangdong Lenovo Dongde Communication Co., Ltd.

Suning Mobile (Suning Co., Ltd.)

JD Mobile (JD.com, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: China Mobile announced strategic partnerships with over 500 companies through its investment ecosystem, committing RMB 190 billion to support MVNO infrastructure development and cloud-native service platforms.

- April 2025: Lenovo introduced the Xiaoxin 5G CPE mobile router, offering consumers compact, high-speed 5G connectivity.

- January 2024: China Unicom launched comprehensive digital village projects across Inner Mongolia, providing government-subsidized connectivity services through MVNO partnerships.

China Mobile Virtual Network Operator Market Report Scope

The China Mobile Virtual Network Operator Market Report is Segmented by Deployment Model (Cloud, On-premise), Operational Mode (Reseller, Service Operator, Full MVNO, Light/Brand MVNO), Subscriber Type (Consumer, Enterprise, IoT-specific), Application (Discount, Business, Cellular M2M, Others), Network Technology (2G/3G, 4G/LTE, 5G, Satellite/NTN), and Distribution Channel (Online/Digital-only, Traditional Retail Stores, Carrier Sub-brand Stores, Third-Party/Wholesale). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How fast are enterprise lines growing in the China Mobile Virtual Network Operator Market?

Enterprise subscriptions are rising 13.05% CAGR between 2025 and 2030 on the back of Industrial IoT outsourcing.

Which deployment model offers the biggest opportunity?

Cloud platforms already hold 55.40% share and grow 9.77% CAGR thanks to scalable, API-driven service rollouts.

What role does e-CNY play in MVNO offerings?

Integrated SIM-based e-CNY wallets generate 0.1-0.3% per transaction fees and position virtual operators within national digital-currency infrastructure.

Why are full MVNOs attracting attention now?

Regulatory easing lets full MVNOs own core functions and deliver differentiated 5G slices, driving the highest 11.48% CAGR within operational modes.

Which regions are next for expansion?

Subsidy-supported rural provinces such as Inner Mongolia and Xinjiang present growth as digital village projects scale.

Page last updated on: