Optical Transport Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.39 Billion |

| Market Size (2031) | USD 44.03 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

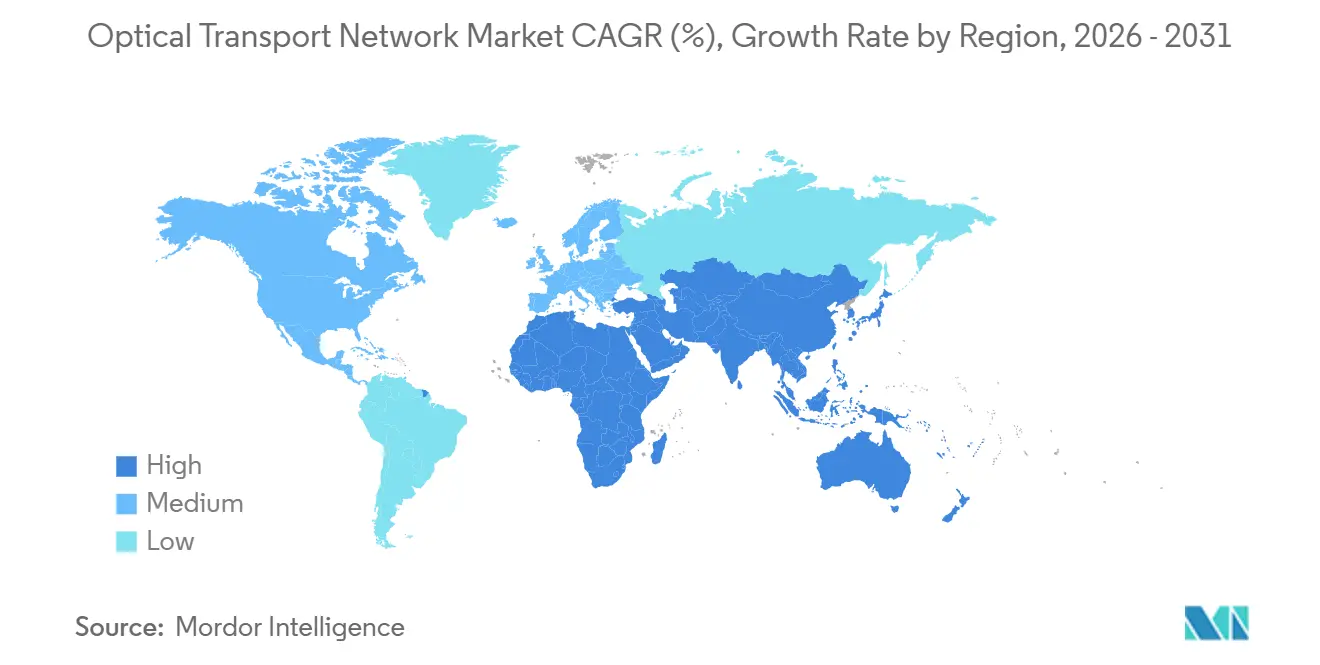

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

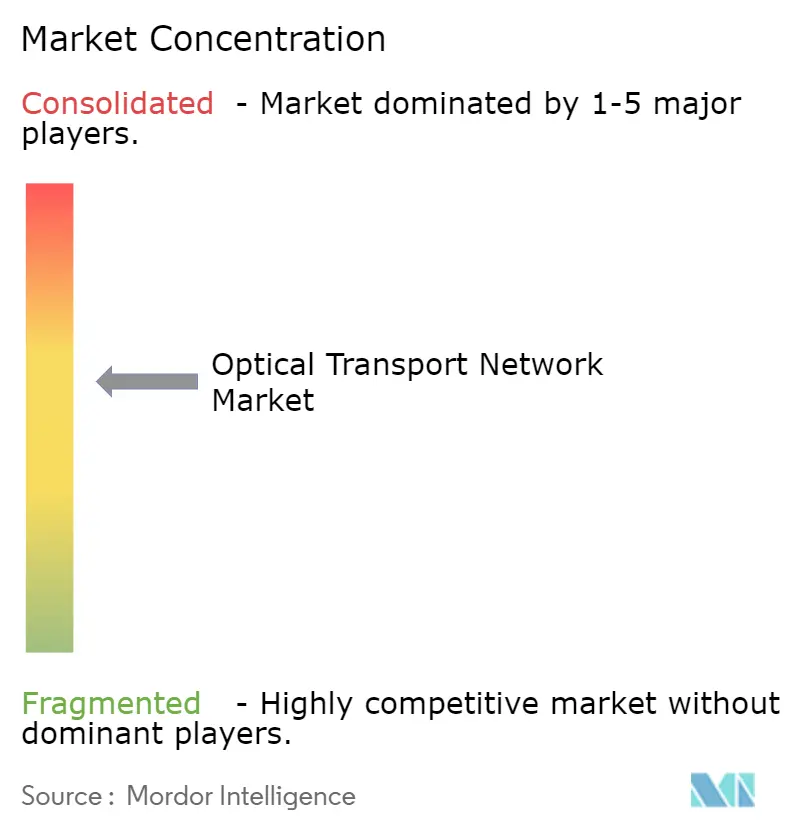

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Transport Network Market Analysis by Mordor Intelligence

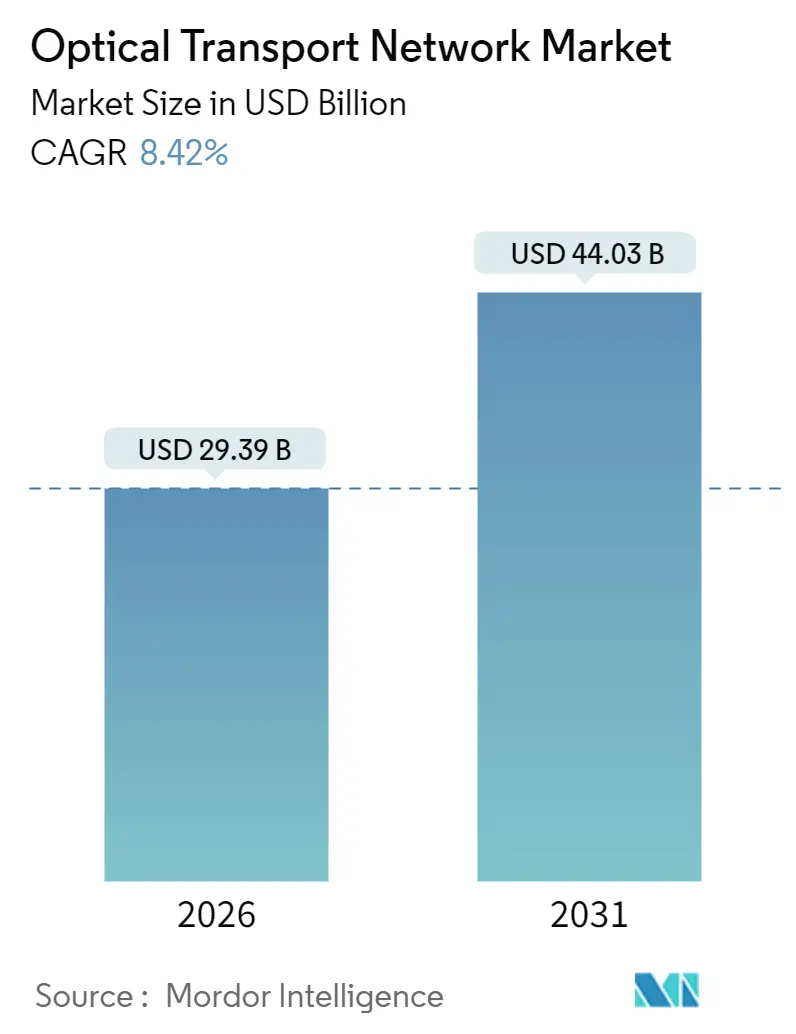

The optical transport network market size is USD 29.39 billion in 2026 and is forecast to reach USD 44.03 billion by 2031, advancing at an 8.42% CAGR. Momentum stems from hyperscale data-center interconnect (DCI) projects that now rival carrier long-haul upgrades, the mainstreaming of 400ZR/400ZR+ coherent pluggables, and multi-year government fiber stimulus in the United States and Europe. Equipment vendors benefit from dual demand streams, rural broadband buildouts, and hyperscaler AI cluster links that mitigate single-customer risk. Component commoditization is accelerating, yet service revenue is growing faster as carriers outsource design and integration for disaggregated open-line systems. Intensifying U.S.-China export controls, however, are fragmenting technology roadmaps and adding supply-chain risk.

Key Report Takeaways

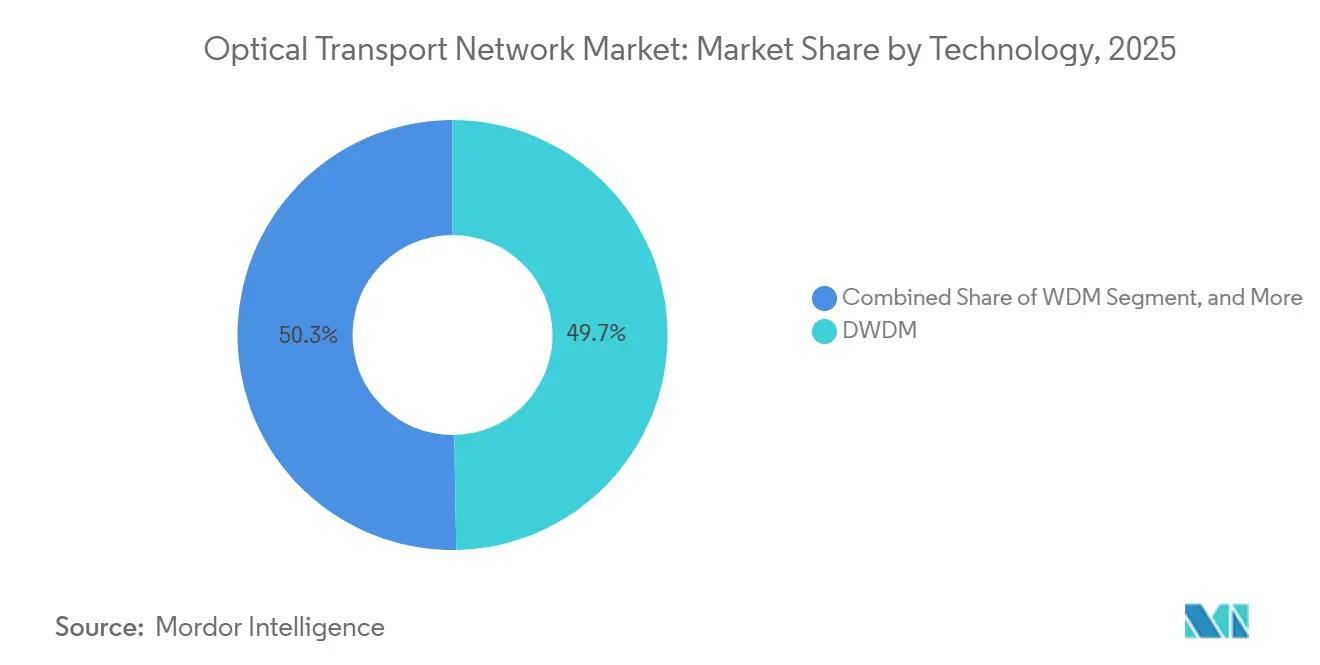

- By technology, DWDM led with 49.72% of the optical transport network market share in 2025, while WDM is projected to grow at a 9.11% CAGR through 2031.

- By offering, components accounted for 58.44% of 2025 revenue, whereas services are forecast to expand at an 8.89% CAGR over 2026-2031.

- By end-user vertical, IT and telecom operators held 43.83% of the optical transport network market share in 2025; cloud and colocation data centers are expected to log a 9.66% CAGR to 2031.

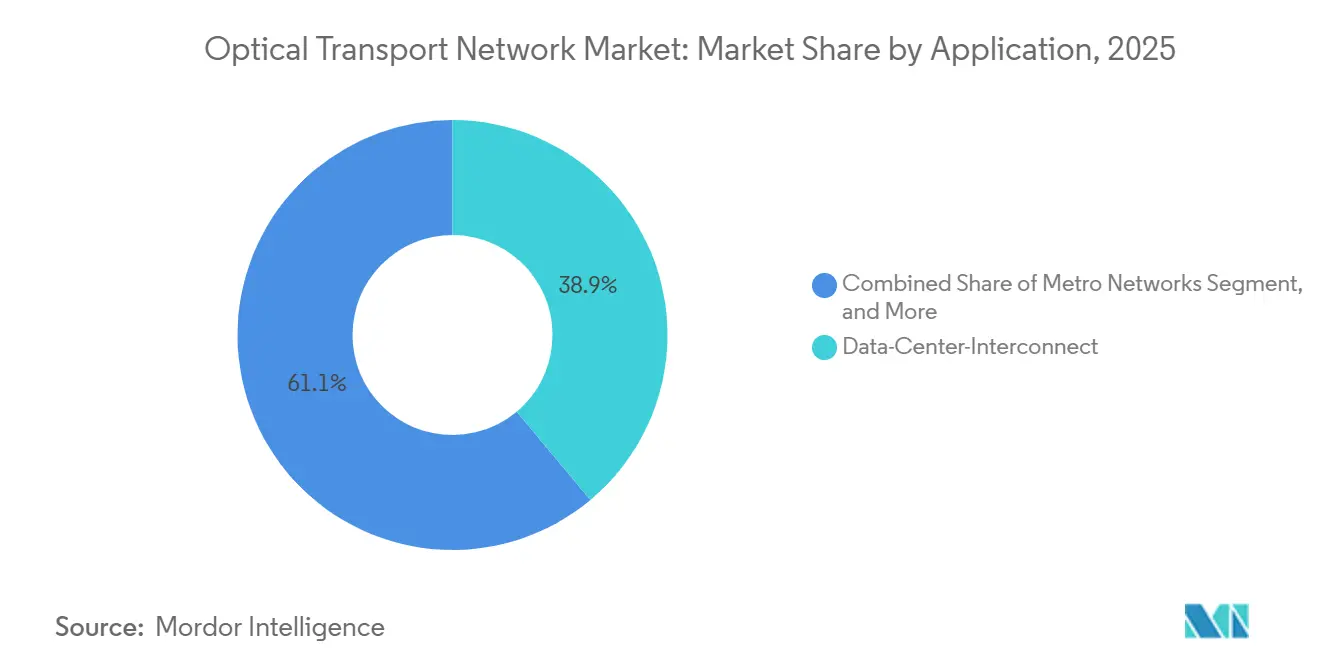

- By application, data-center interconnect captured 38.91% of 2025 revenue and is set to advance at an 8.94% CAGR through 2031.

- By data rate, wavelengths at 100-400 Gbit/s commanded 52.34% of the optical transport network market share in 2025, while beyond-800 Gbit/s systems will grow at an 8.42% CAGR.

- By geography, Asia-Pacific dominated with a 35.67% share in 2025, yet the Middle East is forecast to post the fastest CAGR of 9.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Optical Transport Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 400 ZR/ZR+ Adoption for Data Center Interconnect | +1.8% | Global, led by North America and Asia-Pacific hyperscaler hubs | Short term (≤ 2 years) |

| Hyperscaler AI-Cluster Traffic Boom | +2.1% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Government Fibre-Backhaul Stimulus | +1.3% | North America and Europe | Medium term (2-4 years) |

| Open-Line Systems Lowering Capex | +0.9% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Silicon Photonics Price Inflection | +1.0% | Global, manufacturing concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Under-Sea Green-Field Cables | +0.7% | Global, spanning four continents | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 400 ZR/ZR+ Adoption for Data Center Interconnect

Microsoft’s Azure network surpassed 50,000 deployed 400ZR modules in 2025, proving that coherent pluggables slash footprint by 40% and power by 30% compared with legacy DWDM shelves.[1]Microsoft Azure Networking Team, “Scaling Azure Networking with 400ZR Coherent Pluggables,” microsoft.com Merchant-silicon suppliers now sell modules directly to hyperscalers, bypassing traditional optical vendors and reshaping procurement models. Ciena confirmed that pluggables accounted for 22% of WaveLogic revenue in fiscal 2025, up from 11% in the prior year. As hyperscalers standardize on 400ZR/400ZR+ for metro DCI links of 80-120 km, the optical transport network market gains a durable volume catalyst that offsets telco spending cyclicality.

Hyperscaler AI-Cluster Traffic Boom

Generative-AI training demands bandwidth dense enough to interconnect clusters of 25,000 GPUs at 400 Gbit/s, driving an unprecedented wave of DCI spending. Amazon Web Services, Microsoft Azure, Google Cloud, and Meta earmarked a combined USD 400 billion of 2026 capital outlays, roughly 35% of which targets networking infrastructure.[2]Financial Times Staff, “Big Tech’s $400bn AI Spending Spree Reshapes Supply Chains,” ft.com Transceiver lead times have stretched to 52 weeks for 800 Gbit/s devices, advantaging vendors with captive photonics fabs. The shift toward IP-over-DWDM architectures allows routers with integrated coherent optics to bypass OTN switching, trimming costs but lowering service-layer revenues for carriers.

Government Fibre-Backhaul Stimulus

The NTIA’s Broadband Equity Access and Deployment program injected USD 42.45 billion into U.S. rural fiber plans in November 2024, with Buy America rules prompting Corning’s USD 500 million expansion in North Carolina.[3]National Telecommunications and Information Administration, “BEAD Program State Allocations Announced,” ntia.gov Europe’s Connecting Europe Facility 2 added EUR 2.07 billion (USD 2.2 billion) for cross-border fiber backhaul. Labor shortages, however, may delay deployments and compress equipment delivery windows, causing a bulge in orders during 2026-2027, followed by a possible trough.

Open-Line Systems Lowering Capex

Disaggregated architectures let operators source transponders, amplifiers, and ROADMs separately, slicing per-wavelength costs by up to 30%. Telefónica cut unit costs to USD 13,750 on its UNICA rollout in Spain and Brazil. While capex falls, integration complexity rises, spurring demand for professional services that lift overall vendor revenue even as hardware margins tighten.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex Freeze at Tier-2 Telcos | -1.2% | Europe, Latin America, parts of Asia-Pacific | Short term (≤ 2 years) |

| US-China Export Controls on Coherent DSPs | -0.8% | China, with regional supply-chain spillovers | Medium term (2-4 years) |

| Skilled-Labour Shortage for Fibre Installation | -0.6% | North America and Europe | Medium term (2-4 years) |

| Supply-Chain Dependency on InP Epitaxy | -0.5% | Global, concentrated in Japan and Taiwan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capex Freeze at Tier-2 Telcos (2024-2025)

Deutsche Telekom trimmed German fixed-network investment 8% year over year, while América Móvil reduced 2025 capex guidance in Brazil and Colombia by 12% in response to higher interest costs. Spending deferrals weigh on regional vendors such as ADVA, yet top suppliers partially hedge the shortfall with hyperscaler sales. Analysts expect a rebound once 5G backhaul needs and subsidy programs reignite upgrades after 2027.

US-China Export Controls on Coherent DSPs

The October 2024 Entity List action bars U.S. companies from shipping ≥600 Gbit/s coherent DSPs to China. Huawei is advancing a domestic 400 Gbit/s DSP, but performance lags Western 800 Gbit/s chips by 18 months. Dual technology roadmaps could fragment global standards and complicate multinational carrier operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DWDM Anchors Revenue, WDM Leads Growth

DWDM systems held a 49.72% share of the optical transport network market in 2025, underscoring their dominance in long-haul and submarine corridors, where spectral efficiency dictates economics. Nokia’s PSE-6s platform shows that coherent pluggables can now serve metro access links, merging DWDM performance with WDM simplicity. WDM solutions will post a 9.11% CAGR as metro operators adopt lower-cost 5G backhaul architectures. In turn, merchant-silicon vendors capture value from this convergence, reshaping competitive dynamics.

Legacy O-band technology remains niche for campus interconnects but illustrates application-specific segmentation. Ciena reported an 18% jump in WaveLogic revenue in fiscal 2025, while its traditional OTN switching revenue fell 3%, signaling internal value migration. As coherent pluggables mature, DWDM economics extend toward edge nodes, putting pressure on smaller suppliers that lack R&D heft. The optical transport network market, therefore, faces consolidation even as technology options broaden.

By Offering: Components Dominate, Services Accelerate

Components generated 58.44% of 2025 revenue, reflecting the large installed base of optical transport equipment. Yet services, projected to grow at an 8.89% CAGR, increasingly monetize the complexity of open-line systems. Cisco disclosed 68% gross margins for optical services, far above hardware margins, underscoring its strategic pivot toward recurring revenue.

The optical transport network market for services will expand as carriers outsource multi-vendor integration and capacity planning. Compact modular platforms such as Infinera’s GX G42 fuse switching and transport, reducing footprint and driving demand for lifecycle support over pure hardware refreshes. AI-driven diagnostics could erode some maintenance revenue, but vendors offset this by layering traffic optimization analytics on top of support contracts.

By End-User Vertical: Cloud Providers Outpace Telcos

IT and telecom operators still accounted for 43.83% of spending in 2025, yet hyperscale cloud and colocation customers will record a 9.66% CAGR, driven by AI clusters that demand low-latency links across multiple regions. Amazon’s commitment to deploy 100,000 coherent pluggables illustrates direct procurement at unprecedented scale, bypassing legacy distribution.

Government and defense buyers remain smaller yet high-value customers, favoring quantum-safe DWDM systems. Healthcare and banking invest in private optical links for compliance-driven disaster recovery, highlighting non-hyperscaler demand niches. Fragmented demand from energy, manufacturing, and retail often flows through channel partners, sustaining a long tail of integrators within the optical transport network industry.

By Application: DCI Surges, Long-Haul Matures

Data-center interconnect represented 38.91% of revenue in 2025 and will grow at an 8.94% CAGR as workload distribution intensifies. Microsoft’s Azure architecture employs 32-wavelength bundles delivering 12.8 Tbit/s per link, demonstrating DCI scale. In contrast, long-haul DWDM remains stable, driven mainly by submarine expansions, while metro networks face price pressure from dark-fiber overbuilders.

Enterprise networks increasingly rely on SD-WAN overlays, squeezing managed wavelength services, yet large campuses still justify private optical infrastructure. Vendors like Ciena package packet-optical transport and SD-WAN to capture this hybrid demand. The optical transport network market, therefore, tilts toward cloud-centric applications even as traditional carrier segments plateau.

By Data Rate/Wavelength: 100-400 Gbit/s Dominates, Above 800 Gbit/s Emerges

Wavelengths at 100-400 Gbit/s captured 52.34% share in 2025, reflecting both legacy 100 Gbit/s assets and the proliferation of 400ZR modules. Beyond-800 Gbit/s systems are forecast to grow at an 8.42% CAGR as silicon photonics yields improve, with Nokia demonstrating 1.6 Tbit/s over 500 km in 2025 lab trials.

Higher data rates offer 2-4× capacity at 1.5× cost, but power budgets remain challenging since 800 Gbit/s pluggables draw 22 watts. Infinera’s ICE 7 reduces this to 18 watts by monolithic integration, indicating ongoing efficiency gains. The optical transport network market size attached to 800 Gbit/s and above will rise steadily once module costs align with traffic curves after 2028.

Geography Analysis

Asia-Pacific held 35.67% of 2025 revenue, buoyed by China’s backbone upgrades and India’s BharatNet Phase III, which allocated INR 1.39 trillion (USD 16.8 billion) to rural fiber. China’s three state carriers installed 180,000 new 100 Gbit/s wavelengths during 2024-2025. U.S. export controls, however, could slow China’s transition to 800 Gbit/s gear, widening the technology gap with Western operators. Japan and South Korea continue to drive submarine innovation, with NEC securing a 24-fiber-pair Tokyo-Los Angeles cable supporting 400 Tbit/s.

The Middle East is projected to post the fastest CAGR of 9.47% through 2031. Saudi Arabia’s Public Investment Fund committed USD 6.4 billion to twelve hyperscale data centers in 2025, each requiring 400 Gbit/s redundant links. UAE-based Khazna Data Centers is deploying 1.6 Tbit/s WaveLogic 6 optics on the Dubai-Abu Dhabi corridor, underlining sovereign efforts to localize AI training workloads.

North America and Europe remain the largest absolute markets thanks to legacy DWDM estates awaiting refresh. The BEAD program’s USD 42.45 billion stimulus will drive metro DWDM and coherent-pluggable demand, while Europe’s submarine projects, such as EllaLink and 2Africa, sustain long-haul orders. Capex freezes at some tier-2 European telcos temper near-term growth, yet cross-border CEF-2 funds of EUR 2.07 billion (USD 2.2 billion) should close connectivity gaps in Poland, Romania, and Greece. Regulatory oversight by the FCC and ETSI ensures interoperability, tempering vendor lock-in but potentially lengthening approval cycles.

Mordor Intelligence provides coverage of the optical transport network market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The optical transport network market exhibits moderate concentration, with Nokia, Ciena, and Huawei together controlling about 60% of DWDM line-system sales. Merchant-silicon entrants Marvell and Broadcom now supply coherent DSPs directly to hyperscalers, eroding integrated-vendor margins. Ciena’s WaveLogic modules, at 48% gross margin, trail its 62% margin on full systems, illustrating pricing pressure.

Strategic moves reflect adaptation. Nokia acquired Infinera in January 2025 for USD 2.3 billion to pool R&D and broaden its coherent portfolio. Cisco exited the component business by divesting Acacia in September 2025, pivoting to SDN and AI routing software. White-box vendors such as Ribbon and Padtec target cost-conscious tier-2 carriers with OpenROADM-compliant gear, though integration complexity limits adoption to operators with advanced engineering talent.

Patent filings show heavy investment in probabilistic constellation shaping and digital subcarrier multiplexing to raise spectral efficiency 20-30%. Compliance with ITU-T G.698.2 and OpenROADM MSAs secures baseline interoperability while permitting proprietary performance tweaks. As coherent pluggables commoditize, software orchestration and services differentiation will decide competitive advantage rather than raw optical reach.

Optical Transport Network Industry Leaders

Nokia Corporation

Ciena Corporation

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Fujitsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The NTIA awarded USD 42.45 billion of BEAD funding across all U.S. states, triggering Corning’s USD 500 million fiber-manufacturing expansion in North Carolina.

- October 2025: Infinera launched the GX G42 compact modular platform, integrating optical transport and packet switching for metro and regional networks.

- September 2025: Cisco divested Acacia Communications for USD 1.8 billion, exiting the coherent-transceiver segment to focus on software-defined networking.

- August 2025: Juniper Networks expanded its partnership with Marvell to embed Orion coherent DSPs in PTX routers, enabling IP-over-DWDM architectures.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the optical transport network market as the global revenues generated from new wavelength-division-multiplexing (WDM and DWDM) transport platforms, optical switches, and edge reconfigurable add-drop multiplexers that carry client traffic at 100 Gbit/s and above across long-haul, metro, and data-center-interconnect routes.

Scope Exclusion: Legacy SONET/SDH gear and purely electrical packet switching equipment are not considered.

Segmentation Overview

- By Technology

- WDM

- DWDM

- O-Band and Other Technologies

- By Offering

- Services

- Network Maintenance and Support

- Network Design and Integration

- Components

- Optical Transport Equipment

- Optical Switch

- Optical Platform/Edge ROADM

- Services

- By End-User Vertical

- IT and Telecom Operators

- Cloud and Colocation Data Centres

- Government and Defence

- Healthcare

- Banking and Financial Services

- Other End-User Verticals

- By Application

- Long-Haul DWDM

- Data-Center-Interconnect

- Metro Networks

- Enterprise Networks

- By Data Rate / Wavelength

- 100-400 Gbit/s

- 400-800 Gbit/s

- Beyond 800 Gbit/s

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with optical hardware engineers at telcos, procurement heads at hyperscale data centers in North America, Europe, and Asia-Pacific, and regional fiber contractors; surveys with system integrators validated average 400ZR port budgets and expected refresh cycles. These dialogues resolved gray areas in secondary findings and guided the final assumptions we applied.

Desk Research

We began with structured scans of non-paywalled tier-1 sources such as the International Telecommunication Union datasets, TeleGeography's global bandwidth maps, the OECD Broadband Portal, Fiber Broadband Association statistics, and GSMA network economics papers; these quantify fiber route mileage, lit capacity, and service penetration trends that anchor our demand pool. Company 10-Ks, investor decks, and respected press feeds aggregated through Dow Jones Factiva and D&B Hoovers supplemented vendor shipments, ASP moves, and contract awards. Patent filings, IEEE Photonics journals, and national customs data (notably U.S. ITC and China's GACC export HS-code 851762) clarified technology adoption timing and coherent-module export flows, helping us gauge price curves. This list is illustrative rather than exhaustive.

Market-Sizing & Forecasting

A blended top-down approach converts national fiber route-kilometers and installed 100 G+ wavelengths into an addressable demand pool, which is then benchmarked with selective bottom-up checks drawn from sampled supplier shipment volumes and channel ASPs. Key variables include 400 G transceiver unit costs, lit fiber growth, long-haul DWDM capacity additions, hyperscaler capex plans, and regulatory fiber subsidy outlays. Multivariate regression links these drivers to historical revenue movements, while scenario analysis accommodates currency swings and inflation-adjusted ASP slides. Where supplier data gaps exist, region-weighted interpolation is applied before iterative model reconciliation.

Data Validation & Update Cycle

Intermediate outputs pass variance thresholds versus independent bandwidth tallies; anomalies trigger re-contact of respondents or recalibration. Senior reviewers clear each workbook. The model is refreshed annually, and any mid-cycle material event, such as a major coherent-module price shock, initiates a targeted update so clients receive the latest view.

Why Mordor's Optical Transport Network Baseline Inspires Confidence

Published estimates often diverge because firms pick differing scope boundaries, component mixes, and refresh cadences. Our team spells out inclusions and exclusions up front, so users see exactly what the number represents.

Key Gap Drivers: Some peers roll only transport equipment while omitting optical switches, others assume uniform ASP erosion or use historic averages without reconciling them to today's 400ZR pricing, and several extend five-year CAGRs linearly beyond their data horizon; Mordor publishes a six-year forecast grounded in live interviews and multi-variable testing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27 B (2025) | Mordor Intelligence | - |

| USD 24.52 B (2024) | Global Consultancy A | Switches excluded; older base-year FX rates held constant |

| USD 26.53 B (2025) | Industry Study B | Relies on flat 5% ASP decline, limited primary validation |

| USD 30.56 B (2025) | Insights Firm C | Includes certain legacy OTN gear; aggressive hyperscaler capex assumption |

Taken together, the comparison shows that Mordor's disciplined scope choices, interview-backed variables, and yearly refresh cadence deliver a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

How large is the optical transport network market in 2026?

The optical transport network market size is USD 29.39 billion in 2026.

What is the projected CAGR for optical transport equipment from 2026-2031?

Overall revenue is forecast to grow at an 8.42% CAGR through 2031.

Which technology segment will grow fastest?

WDM systems are forecast to post the highest 9.11% CAGR as metro operators adopt simpler architectures.

Why are hyperscalers influencing procurement patterns?

Cloud and colocation data centers need low-latency data-center interconnect links for AI workloads, driving direct purchases of coherent pluggables at scale.

How will U.S. BEAD funding affect vendor demand?

BEAD’s USD 42.45 billion allocation is set to create a multi-year procurement cycle for metro DWDM and coherent pluggable modules across rural broadband builds.

What challenges could limit market expansion?

Export controls, tier-2 telco capex freezes, and skilled-labor shortages for fiber installation all pose near-term headwinds.

Page last updated on: