Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Virtualized Evolved Packet Core Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Application (IoT and M2M, Mobile Private Networks (MPN) and MVNO, Broadband Wireless Access (BWA), LTE/VoLTE/VoWiFi, 5G Non-Standalone (NSA) Core, and More), End-User (Telecom Operators, Enterprises and Industrial Verticals, Government and Public Safety, Cloud Service Providers, and MVNE/MVNOs), and Geography.

Market Overview

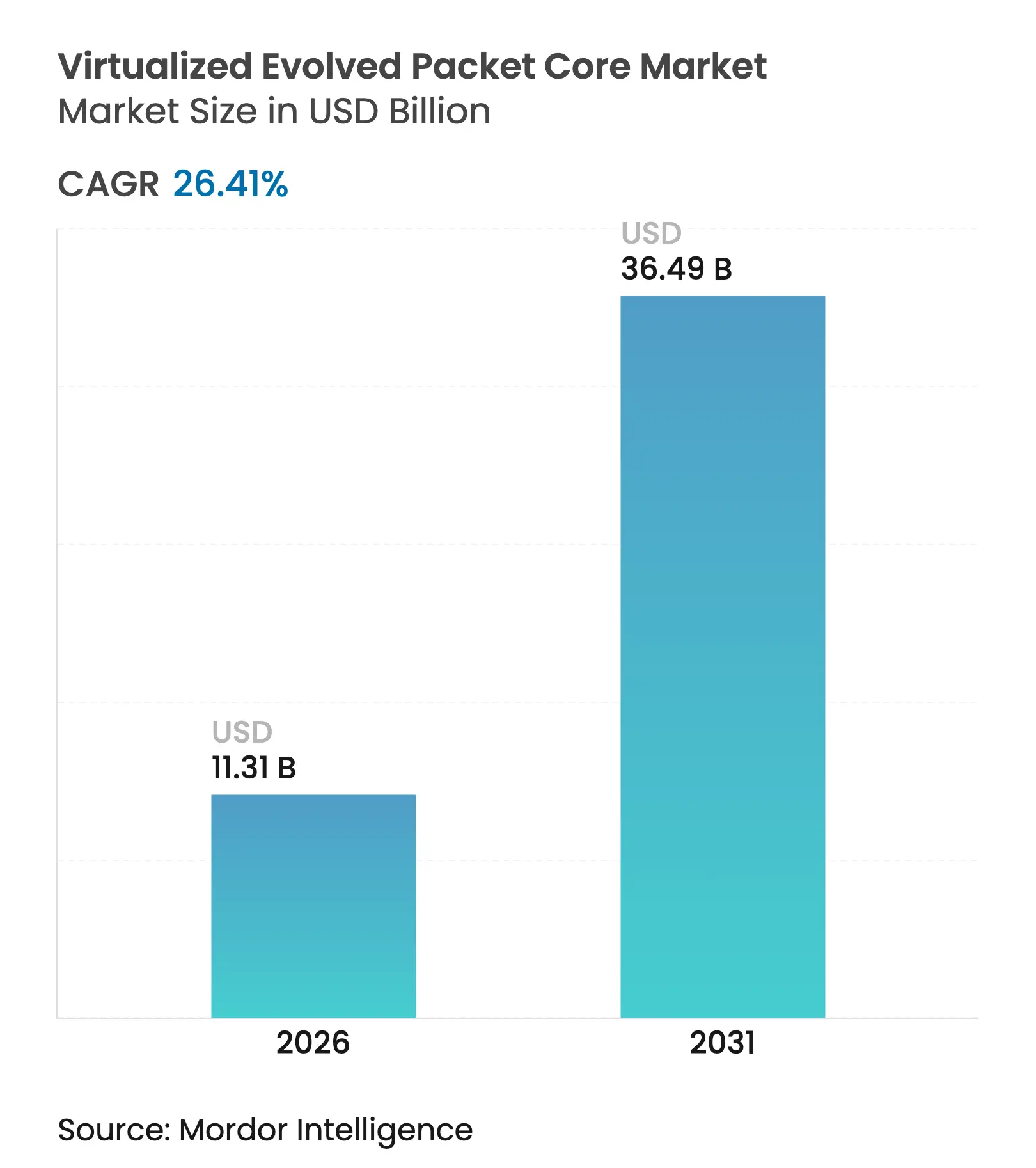

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.31 Billion |

| Market Size (2031) | USD 36.49 Billion |

| Growth Rate (2026 - 2031) | 26.41 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Growth stems from 5G standalone rollouts, rising enterprise demand for private mobile networks, and operator sustainability mandates that favor energy-efficient virtualized cores. Telcos accelerate software-defined network functions to slash capital and operating outlays, while hyperscale public-cloud partnerships allow rapid service launches and global coverage. Asia Pacific drives adoption on the back of government-backed digital programs, whereas North America pushes differentiation through network slicing and edge-cloud synergies. Meanwhile, Europe emphasizes compliance and energy efficiency, a stance that shapes technical requirements and vendor selection.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerated 5G rollouts demanding cloud-native cores Accelerated 5G rollouts demanding cloud-native cores | +8.70% | Global (North America, APAC) | Short term (≤ 2 years) | Impact on CAGR Forecast (~%):+8.70% | Geographic Relevance:Global (North America, APAC) | Impact Timeline:Short term (≤ 2 years) |

CapEx / OpEx savings from network-function virtualization CapEx / OpEx savings from network-function virtualization | +6.10% | Global | Medium term (2–4 years) | |||

Private LTE/5G networks for Industry 4.0 & campus connectivity Private LTE/5G networks for Industry 4.0 & campus connectivity | +5.30% | North America, EU → APAC | Long term (≥ 4 years) | |||

Telco sustainability mandates for energy-efficient core networks Telco sustainability mandates for energy-efficient core networks | +2.40% | EU → North America, APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerated 5G Rollouts Demanding Cloud-Native Cores

Cloud-native service-based architectures are mandatory for true 5G standalone networks, making vEPC a non-negotiable investment for operators pursuing network slicing and premium-tier services. Ericsson secured more than 120 commercial 5G core contracts by late 2024, powering 37 live 5G SA networks worldwide, providing tangible proof of commercial readiness[1]Ericsson, “Ericsson powers 37 live 5G Standalone networks,” ericsson.com. Early movers such as T-Mobile leveraged nationwide 5G SA to introduce network-slice-enabled video calling, which positions them for differentiated pricing models. Competitive pressure compels lagging carriers to accelerate modernization or risk churn. Cloud-native cores also give smaller mobile virtual network operators fast-track entry into enterprise IoT niches. Consequently, the Virtualized Evolved Packet Core market experiences a compounding adoption cycle in the short term.

CapEx/OpEx Savings from Network-Function Virtualization

Operators record sizeable cost reductions as vEPC setups shift workloads to commodity hardware and shared cloud resources. Studies show 68% lower capital outlays and 67% savings on operating expense versus monolithic hardware cores. Digital Nasional Berhad achieved 99.8% network uptime and cut customer-complaint resolution time by 90% after moving to intent-based automated operations on a virtualized core. Energy savings add a further 22% efficiency, meeting both budget and sustainability goals. Faster service launches shorten time-to-revenue from over a year to less than six months. These economics shift vEPC from optional to essential in board-level investment plans. Vendors now embed AI-powered orchestration to shrink operational workloads even further.

Private LTE/5G Networks for Industry 4.0 and Campus Connectivity

Enterprises have begun deploying dedicated cellular solutions that deliver latency, reliability, and security beyond Wi-Fi limitations. BMW’s Spartanburg plant and Toyota Material Handling’s U.S. facilities transitioned to private 5G, improving automated-guided-vehicle coordination and predictive maintenance analytics. China already hosts more than 5,325 private 5G networks that span 40 industrial sectors and enable over 20,000 production use cases[2]Dan Jones, “China’s 5G private-network tally tops 5,000,” lightreading.com. This scale demonstrates the technology’s broad viability and fuels the enterprise segment’s 29% CAGR. The Virtualized Evolved Packet Core market benefits because each private network requires a flexible, software-defined core to manage slice isolation and QoS. Vendors respond with tailored packaging, including SaaS consumption models that appeal to mid-size manufacturers.

Telco Sustainability Mandates for Energy-Efficient Core Networks

Regulators and investors evaluate carrier decarbonization trajectories, making energy efficiency a procurement criterion. Nokia’s “extreme deep sleep” power-saving mode cuts consumption by up to eight times during off-peak hours. VMware estimates that virtualization technologies have already avoided 1.2 billion metric tons of CO2 since deployment inception. Operators facing volatile power prices recognize direct OPEX risk and pivot to vEPC to minimize footprint. The European Union’s draft Green Deal telecom guidelines will raise the bar further, rewarding early adopters. As a result, energy-efficient designs become a core competitive differentiator within the Virtualized Evolved Packet Core market.

Restraints Impact Analysis

| Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Operator inertia toward legacy physical EPCs Operator inertia toward legacy physical EPCs | –3.8% | Global (mature markets) | Short term (≤ 2 years) | Impact on CAGR Forecast (~%):–3.8% | Geographic Relevance:Global (mature markets) | Impact Timeline:Short term (≤ 2 years) |

Security & compliance concerns on multi-tenant cloud Security & compliance concerns on multi-tenant cloud | –2.9% | North America, EU → Global | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Operator Inertia Toward Legacy Physical EPCs

Sunk investments and mission-critical risk aversion slow virtualization plans. Three UK replaced Nokia’s end-of-life CloudBand only when forced to modernize, underscoring reluctance to disrupt stable traffic flows. Verizon’s protracted 5G SA launch shows that even innovation leaders grapple with migration complexity. Mature markets face elevated regulatory oversight and stringent service-level expectations, making change management even more difficult. As a result, physical cores persist for longer than their economic utility justifies, dampening short-term momentum in the Virtualized Evolved Packet Core market.

Security and Compliance Concerns on Multi-Tenant Cloud

The UK Telecoms Security Act mandates roughly 258 controls, revealing how traditional frameworks strain to cover cloud-native functions. Operators must harden workloads, segment networks, and manage secrets with zero-trust rigor, tasks that inflate initial deployment effort. Google Cloud, AWS, and Microsoft introduce telecom-specific compliance blueprints, yet data sovereignty questions linger, particularly in Europe. Some carriers elect to keep packet-core control planes on-premises, adopting hybrid models that slow full-scale public-cloud adoption. These concerns temper otherwise compelling economics for virtualization.

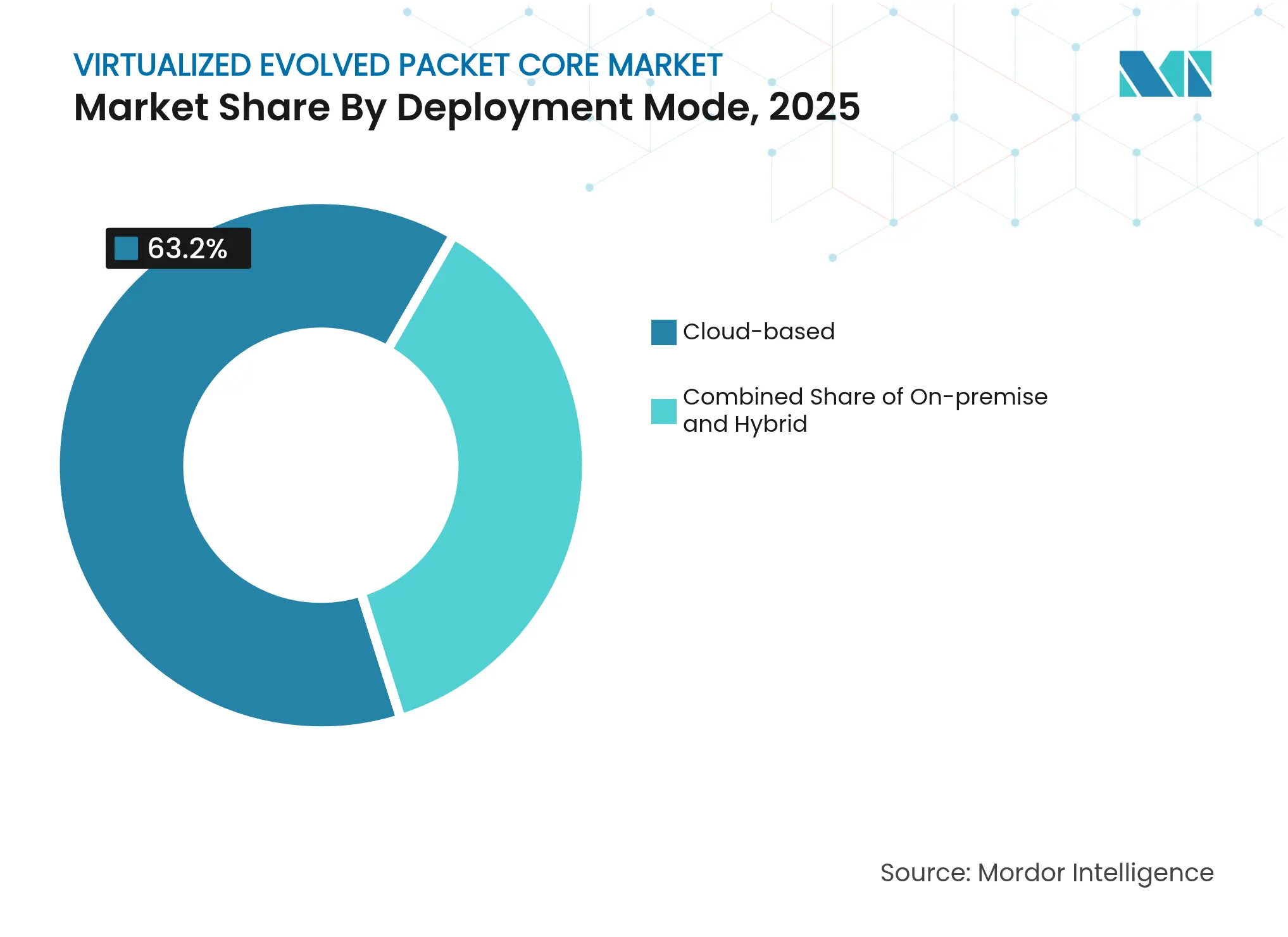

By Deployment Mode: Cloud Dominance Accelerates

Cloud implementations represented 63.20% of the Virtualized Evolved Packet Core market share in 2025, reflecting carriers’ preference for elastic scaling and rapid service iteration. The cloud cohort is forecast to grow at 31.5% CAGR, outpacing on-premises and hybrid alternatives as hyperscalers strengthen telecom feature sets. Samsung, TELUS, and AWS created North America’s first virtual roaming gateway, which proves that cross-border service innovations flourish when control-plane elements run natively on the public cloud. These examples underpin a broad shift where infrastructure ownership yields to agility.

Operators that retain data on-site embrace transitional hybrid models to satisfy sovereignty rules without forfeiting cloud economics. Ericsson’s Compact Packet Core reduces deployment complexity by 80% and cuts energy use by 30%, making cloud‐ready bundles attractive to tier-2 carriers. As more contracts stipulate outcome-based pricing, the Virtualized Evolved Packet Core market embeds managed-service add-ons such as AI-assisted operations. Small regional telcos and MVNOs leverage SaaS delivery to launch new offers in weeks rather than quarters, broadening the customer base.

Note: Segment shares of all individual segments available upon report purchase

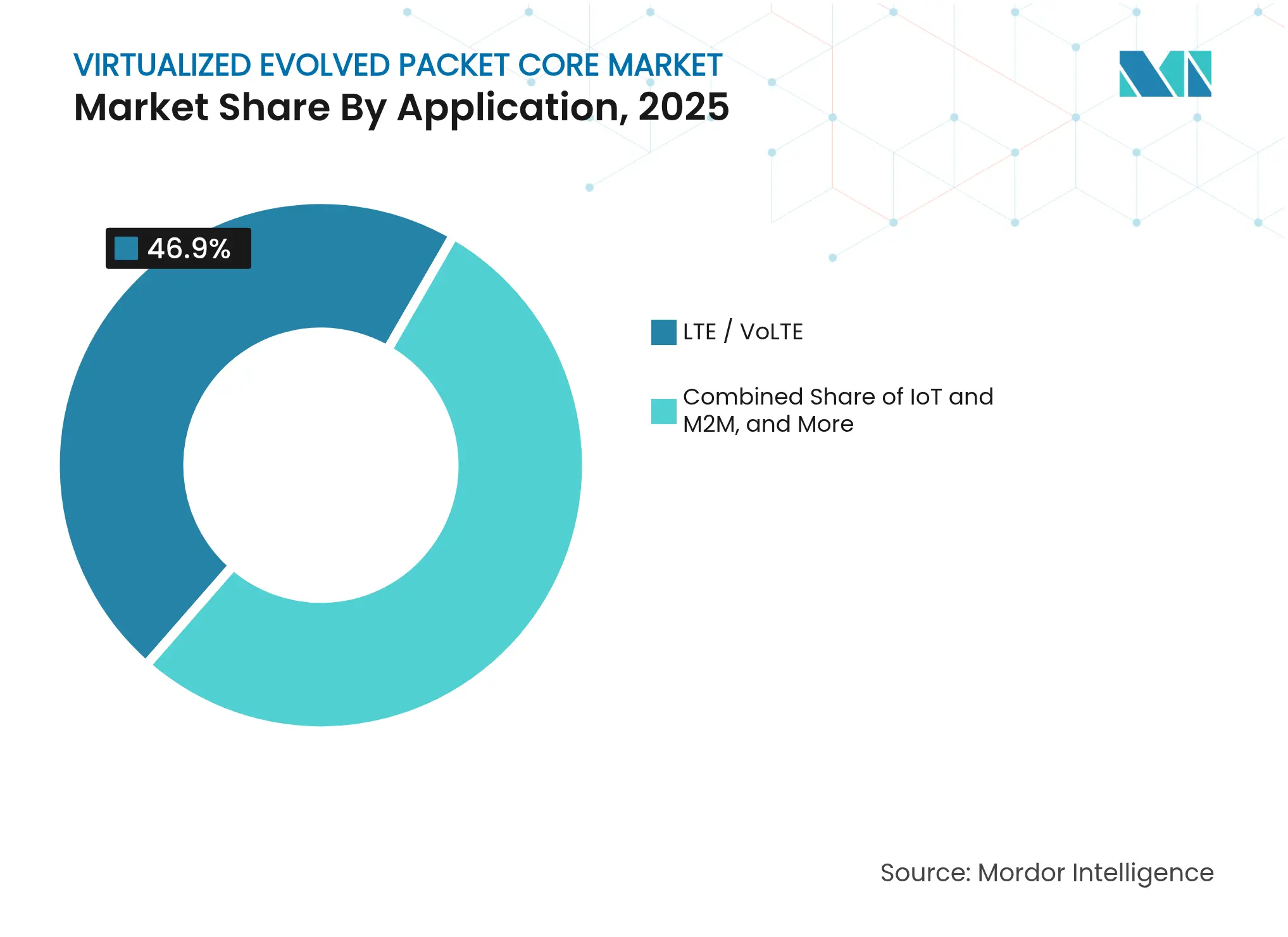

By Application: 5G SA Core Disrupts LTE Dominance

LTE/VoLTE still commanded 46.90% of the Virtualized Evolved Packet Core market size in 2025 because most mobile subscribers reside on 4G networks. However, 5G SA cores exhibit a 34.55% CAGR, indicating a structural transition toward service-based architectures that unlock network API monetization. Bharti Airtel picked Ericsson to deliver standalone signaling and charging, illustrating the commercial link between SA and revenue diversification.

Broadband Wireless Access capitalizes on SA capacity to compete with fiber, while IoT gains deterministic latency for industrial robotics. Operators introduce subscription tiers tied to slice attributes, converting technical differentiation into ARPU uplift. Consequently, future volume may remain LTE-heavy, yet value creation migrates to SA-enabled offerings. The Virtualized Evolved Packet Core industry thus aligns product roadmaps with low-latency, uRLLC, and massive-IoT profiles that only standalone cores support.

Note: Segment shares of all individual segments available upon report purchase

By End User: Enterprise Acceleration Reshapes Market

Telecom carriers retained 71.10% revenue share in 2025, yet enterprise demand expands at a 28.35% CAGR, driving portfolio recasting toward private network bundles rcrwireless.com. Manufacturers like Toyota Material Handling replaced plant-wide Wi-Fi with Ericsson private 5G, confirming that deterministic performance justifies investment at factory scale rcrwireless.com. MVNOs adopt cloud-native cores to address vertical niches, while cloud providers enter the arena with vEPC-as-a-Service for mid-tier operators.

Public-sector agencies apply dedicated slices for mission-critical communications during emergencies, further diversifying use cases. NTT and LyondellBasell’s multi-site private 5G deployment signals how global enterprises treat cellular connectivity as strategic infrastructure ntt.com. As enterprise sophistication rises, vendors ship pre-integrated application stacks that bundle MEC, analytics, and cybersecurity, raising overall deal sizes. These dynamics enlarge addressable revenue and set new functional baselines for the Virtualized Evolved Packet Core market.

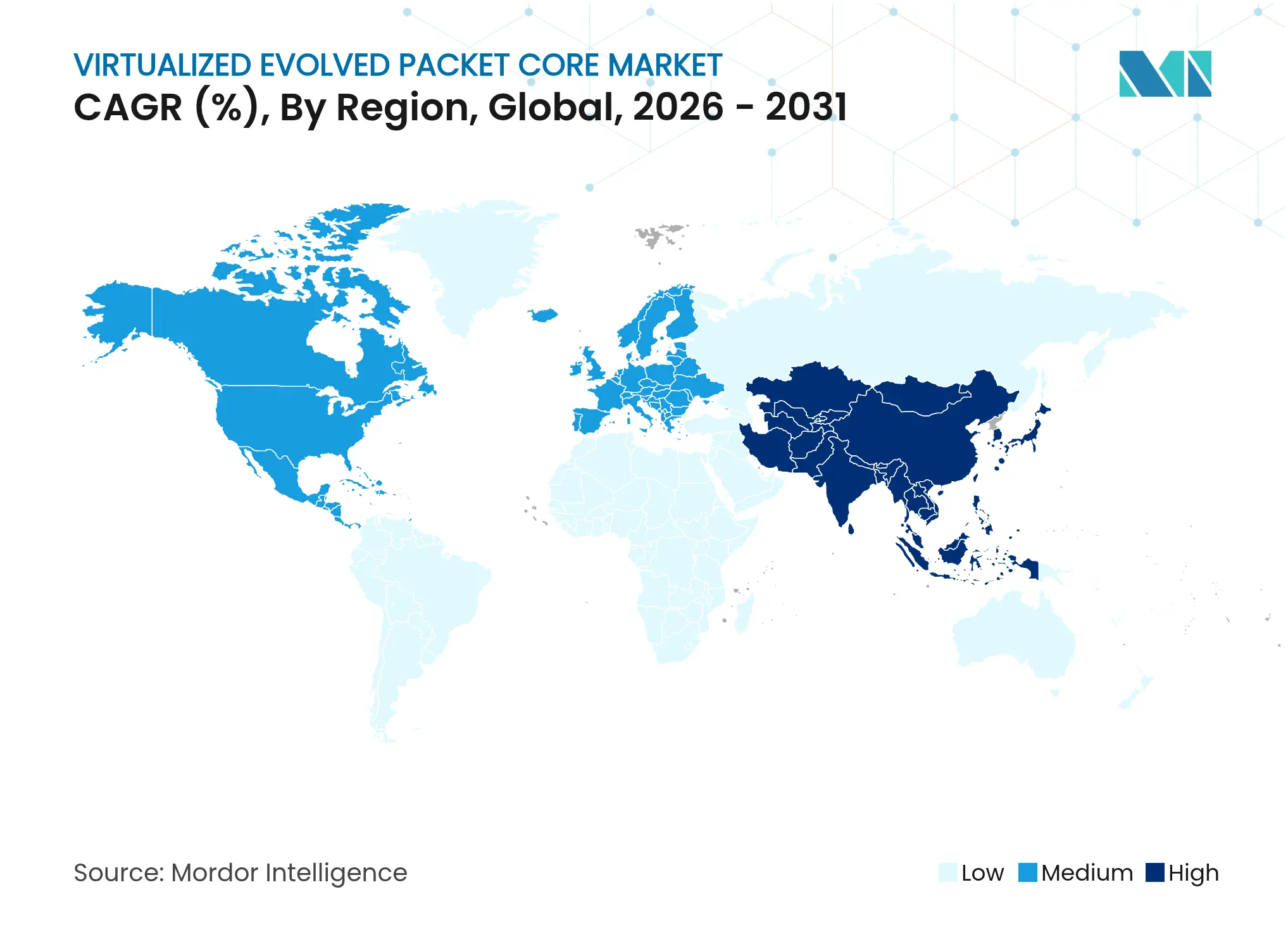

Asia Pacific generated 37.75% of the 2025 Virtualized Evolved Packet Core market size, supported by China’s 5,325 live private 5G networks that include more than 20,000 industrial use cases. Government incentives and spectrum policies accelerate manufacturing adoption, with Beijing investing USD 3 billion in 5G-Advanced coverage across 300 cities in 2025. India’s 52% 5G SA coverage, well ahead of Europe’s 2%, illustrates how emerging economies leapfrog legacy architectures via cloud-first rollouts. These programs supply scale that compels vendors to localize R&D and production, reinforcing Asia Pacific’s leadership in the Virtualized Evolved Packet Core market.

North America emphasizes premium service tiers through network slicing and O-RAN integration. Verizon deployed more than 130,000 O-RAN-capable radios and launched slice-based video calling to capture high-value subscribers. Enterprise alliances produce headline case studies: BMW’s Spartanburg plant realized uptime gains after adopting private 5G, and Samsung, TELUS, and AWS demonstrated roaming innovation via fully virtualized cores. Regulatory clarity around spectrum leasing further supports campus deployments, bolstering regional contribution to the Virtualized Evolved Packet Core market.

Europe shows mixed momentum. Three UK awarded Ericsson a 9 Tbps cloud-native core contract, and O2 Telefónica surpassed 1 million users on its AWS-hosted core within six months. Yet overall 5G SA availability stands at 2%, restrained by strict security rules such as the UK Telecoms Security Act and by a risk-averse culture that favors stability over aggressive modernization. Operators focus on energy efficiency and open-RAN experimentation, evidenced by Deutsche Telekom’s O-RAN Town initiative. These priorities temper immediate spending but create long-term demand for highly interoperable, low-power vEPC solutions within the Virtualized Evolved Packet Core market.

Market Concentration

Vendor consolidation reshapes competition as legacy infrastructure giants absorb complementary assets. Nokia’s USD 2.3 billion bid for Infinera bolsters optical transport, while HPE’s USD 14 billion move on Juniper Networks injects AI-driven automation into its telco cloud stack. Ericsson remains the contract volume leader with more than 120 commercial 5G cores and collaborates with Google Cloud to deliver cognitive operations that reach 98% anomaly-detection accuracy. Huawei unveiled AI-centric 5.5G that aligns autonomous operations and new monetization metrics, intensifying feature competition.

Technology differentiation concentrates on closed-loop automation and energy savings. Qualcomm’s Edgewise Suite supports intent-based optimization via natural-language inputs, while Ericsson’s Compact Packet Core slashes configuration times by 80%. White-space entrants such as Working Group Two supply multi-tenant, cloud-native cores that let MVNOs issue programmable SIMs quickly, broadening customer choice. Standardization under 3GPP Release 18 introduces defined APIs for edge-computing interaction, pushing vendors to balance interoperability with proprietary enhancements.

Energy credentials become a bidding requirement, and vendors tout deep-sleep modes or ARM-based acceleration to win eco-conscious tenders. Strategic alliances, exemplified by Ericsson and Dell jointly marketing Cloud RAN on PowerEdge servers, underscore the value of pre-integrated solutions that compress deployment cycles. Altogether, the Virtualized Evolved Packet Core market features moderate concentration yet active innovation, as players race to blend core, RAN, and edge capabilities into end-to-end platforms.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the virtualized evolved packet core (vEPC) market as the revenues generated from software-based implementations of the Mobility Management Entity, Serving/Packet Data Network Gateways, Policy & Charging Rules Function, and related control-plane nodes that are deployed on commercial off-the-shelf servers or public clouds to support 4G LTE, 5G NSA, and 5G SA traffic. These deployments include network slices for private LTE/5G, fixed-wireless access, and IoT connectivity. According to Mordor Intelligence, the addressable market will be worth USD 8.95 billion in 2025 and is projected to reach USD 29.51 billion by 2030.

(Exclusion) Physical, appliance-based EPCs and purely packet-core orchestration tool revenues are outside this scope.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed network planners at tier-1 operators in North America, Europe, and APAC, along with system integrators and industrial-campus IT heads that run private LTE/5G. These conversations validated license fee brackets, cloud hosting mark-ups, and realistic penetration rates for enterprise networks, helping us close data gaps left by public sources.

Desk Research

We build the initial data foundation from tier-1, non-paywalled sources such as the GSMA Mobile Economy series, Ericsson Mobility Report, ITU mobile subscription datasets, national telecom regulator filings, and 3GPP standards releases that signal new feature freezes. Company 10-Ks, investor day decks, and Telco Cloud Forum presentations supply vendor shipment anecdotes and operator rollout timelines. Where deeper financials are required, we pull curated extracts from D&B Hoovers and news flow from Dow Jones Factiva. These materials frame historical demand, pricing ranges, and virtual-core adoption benchmarks across regions. The list above is illustrative; many additional documents were consulted to cross-verify figures and assumptions.

Market-Sizing & Forecasting

A top-down model converts mobile data traffic forecasts and live 4G/5G subscriber counts into required core throughput, which is then priced using region-specific annual software license and support rates. Selective bottom-up roll-ups from vendor shipment disclosures and sampled average selling prices provide a cross-check before totals are finalized. Key variables include 5G base-station rollout counts, operator CapEx on network function virtualization, enterprise private-network contracts, average monthly data per user, and public-cloud price indices. Multivariate regression links these drivers to historical vEPC spending and projects them through 2030. Scenario analysis is run for divergent 5G adoption curves. Where bottom-up evidence is patchy, the model applies ratio benchmarks derived from primary interviews to keep totals consistent.

Data Validation & Update Cycle

Outputs pass three-layer checks: automated variance scans versus prior editions, analyst peer review, and senior-analyst sign-off. Anomalies trigger re-contacts with key respondents. The dataset refreshes annually, with interim updates if a large MNO switches on nationwide 5G SA or if macro indicators move materially. A final sense-check is performed just before release to ensure clients receive the most current baseline.

Why Our Virtualized Evolved Packet Core (vEPC) Baseline Earns Industry Trust

Benchmark comparison

Published estimates differ because firms choose distinct functional boundaries, pricing ladders, and refresh cadences. Some count only control-plane software, others fold in orchestration stacks or hardware, and exchange-rate choices further widen gaps.

Key gap drivers include: (1) Mordor reports the full vEPC function set while certain consultancies exclude policy or charging modules; (2) we quote actual 2025 spend whereas others anchor on 2023 or 2024, missing the 5G SA ramp; (3) our model re-prices licenses annually to reflect falling cloud instance costs, while others keep flat tickets; (4) our yearly refresh captures new private-network deals that slower cycles overlook.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 8.95 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 8.4 B (2023) | Global Consultancy A | excludes policy function, older base year | ||

USD 6.48 B (2024) | Industry Analysis B | relies on static license prices, limited private-network coverage |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.