Russia Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

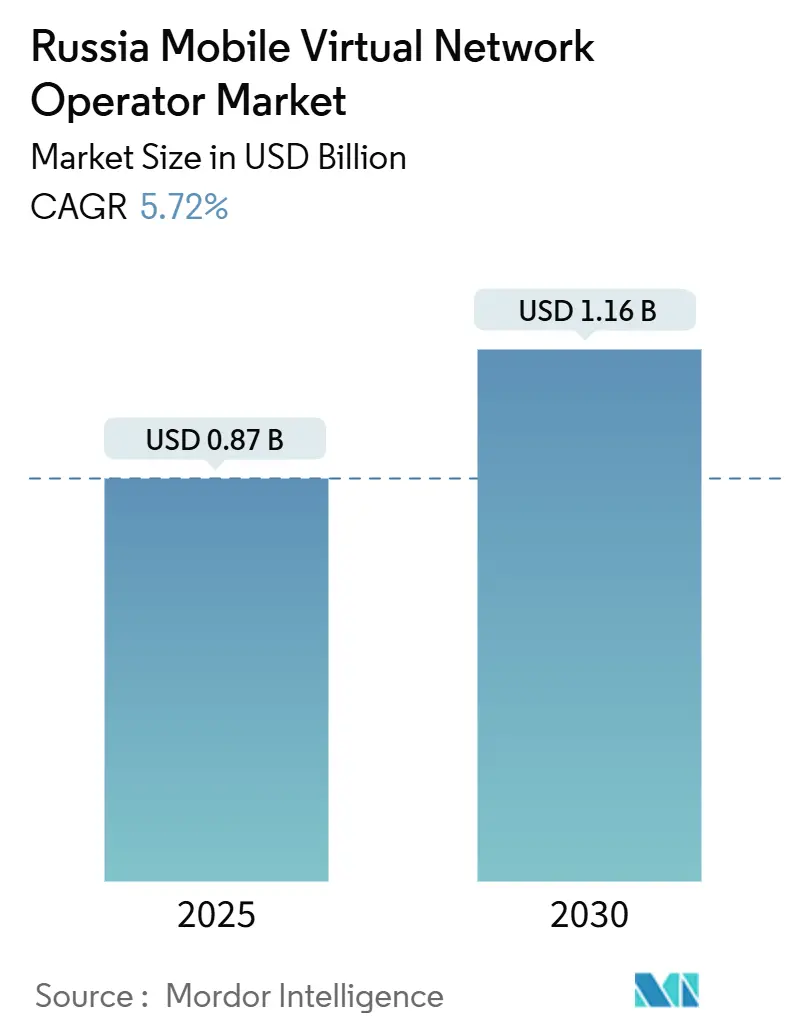

| Market Size (2025) | USD 0.87 Billion |

| Market Size (2030) | USD 1.16 Billion |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

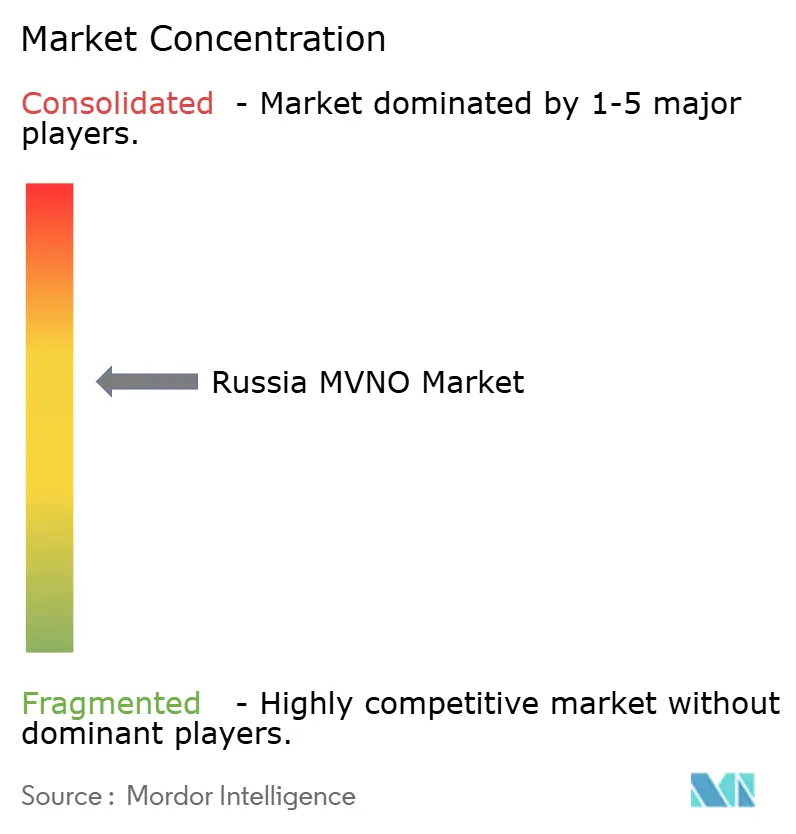

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

The Russia Mobile Virtual Network Operator Market size is estimated at USD 0.87 billion in 2025, and is expected to reach USD 1.16 billion by 2030, at a CAGR of 5.72% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 23.47 million subscribers in 2025 to 33.17 million subscribers by 2030, at a CAGR of 7.16% during the forecast period (2025-2030).

Robust subscriber additions across banking-backed brands, accelerating IoT connectivity roll-outs, and government incentives that keep corporate tax rates for IT ventures at 5% until 2030 collectively sustain near-term revenue growth. Rising 5G trials, fast-spreading eSIM activation, and expanding domestic cloud capacity further strengthen competitive positioning for both incumbent and new virtual operators. At the same time, wholesale pricing power held by the four major MNOs and lingering import-equipment restrictions temper margin expansion, signaling a gradual rather than explosive growth path for the Russian Mobile Virtual Network Operator Market. Yet, demand pockets in tier-2 and tier-3 cities, where price sensitivity remains acute, continue to attract light-asset MVNO models that rely on T2’s nationwide radio network.

Key Report Takeaways

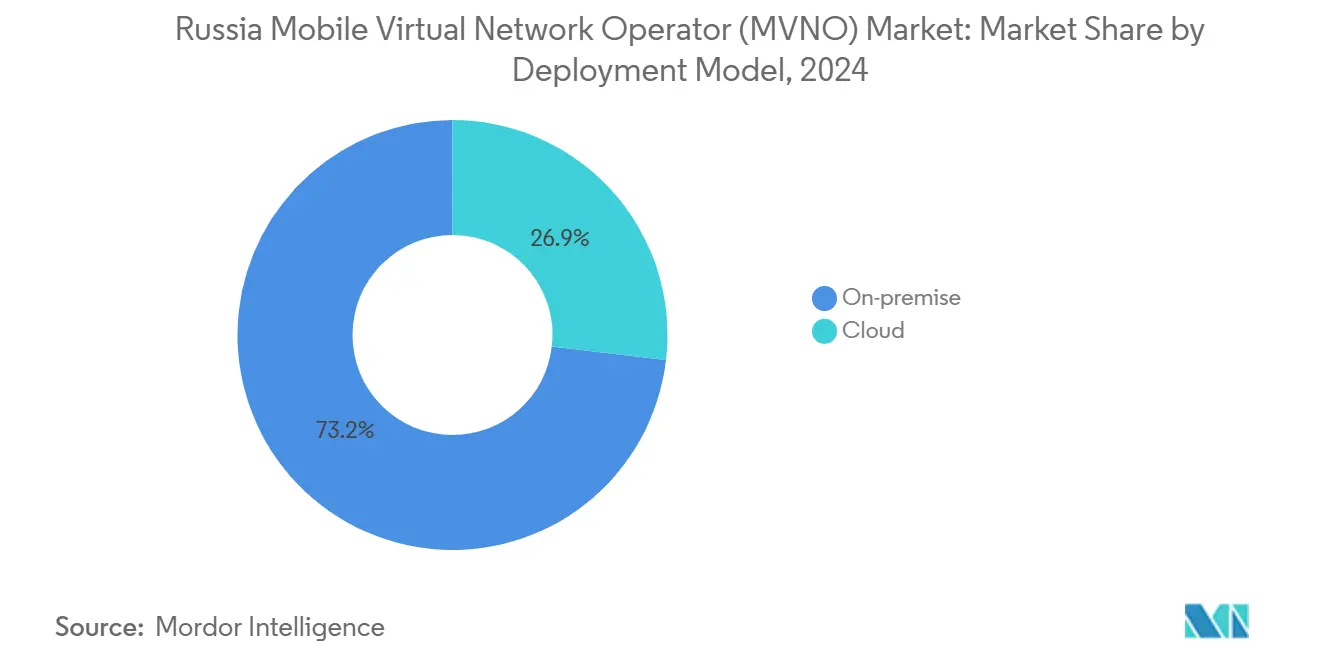

- By deployment model, on-premise platforms controlled 73.15% of the Russia MVNO market share in 2024, and cloud-based deployments are projected to post a 22.51% CAGR through 2030.

- By operational mode, reseller and light MVNOs secured 80.72% revenue in 2024, while full MVNO operations are set to record a 21.29% CAGR to 2030.

- By subscriber type, consumer lines made up 84.25% in 2024, and IoT accounts are anticipated to expand at a 23.65% CAGR to 2030.

- By application, discount plans captured 56.84% revenue in 2024, and cellular M2M connectivity is on track for a 23.33% CAGR to 2030.

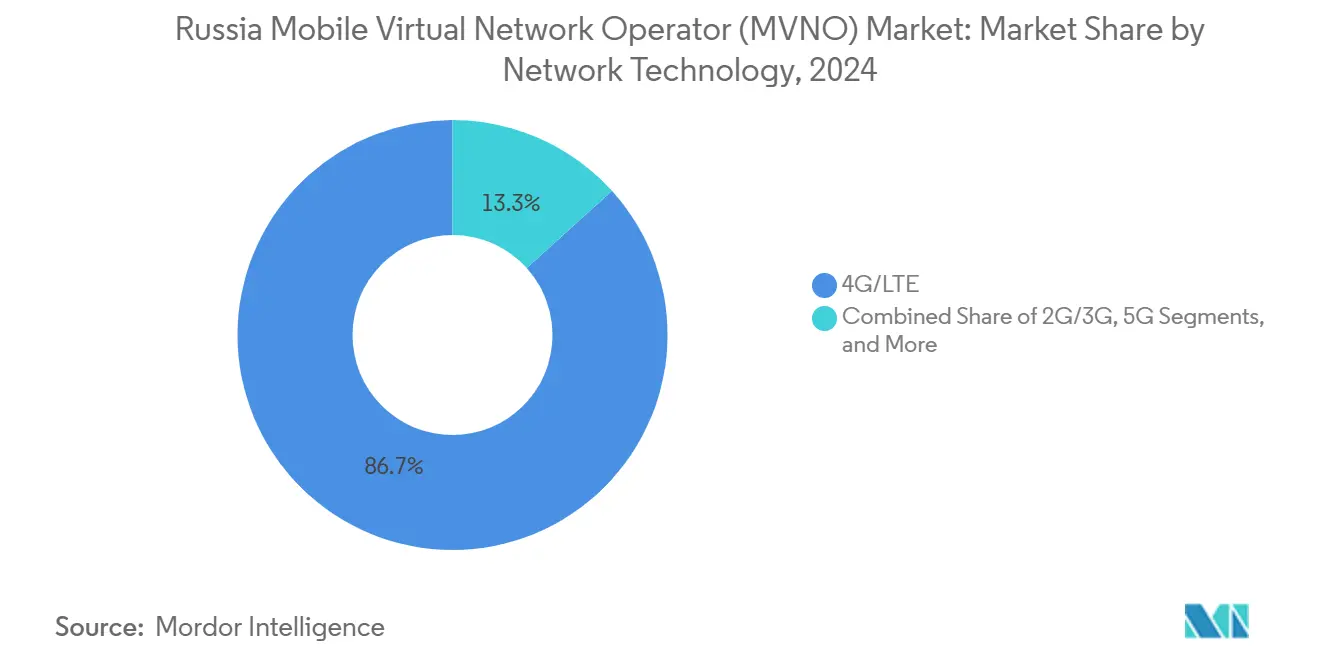

- By network technology, 4G/LTE enabled 86.71% of MVNO traffic in 2024, while 5G services are projected to surge at a 52.76% CAGR to 2030.

- By distribution channel, traditional retail retained 46.46% in 2024, and online/digital-only sign-ups are forecast to grow at a 12.93% CAGR to 2030.

Russia Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for lower-cost mobile plans | +1.2% | Tier-2 and tier-3 urban centers | Medium term (2-4 years) |

| Government MVNO-friendly licensing and wholesale rules | +0.8% | National regulatory framework | Long term (≥ 4 years) |

| Rapid expansion of IoT/M2M connectivity demand in logistics and utilities | +1.5% | Industrial clusters in Moscow-St. Petersburg corridor | Medium term (2-4 years) |

| Nation-wide eSIM adoption and full-digital onboarding | +0.7% | Major cities expanding to regional markets | Short term (≤ 2 years) |

| Network-sharing pacts enabling hyper-niche MVNO positioning (e.g., gaming, ethnic) | +0.4% | High-density metropolitan areas | Long term (≥ 4 years) |

| Industrial private 5G outsourcing to MVNOs for manufacturing and mining sites | +0.6% | Siberian mining and Urals manufacturing zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Lower-Cost Mobile Plans

Price-sensitive households increasingly shift from incumbent postpaid bundles to prepaid MVNO tariffs that undercut major carriers by 10-20% in regional markets [1]O. Borodin et al., “Efficiency of Price Competition in the Telecommunications Market,” E3S Web of Conferences, e3s-conferences.org. Banking-backed brands cross-sell connectivity with debit and credit products, lowering acquisition costs and unlocking new loyalty rewards. The 84.25% consumer share in 2024 confirms the pull of discount-first propositions aimed at younger, data-heavy subscribers. Regional income gaps also allow MVNOs to tailor micro-bundles that traditional MNOs cannot price profitably. Corporate tax relief on IT income lets virtual operators keep headline prices low while funding customer-experience upgrades.

Government MVNO-Friendly Licensing and Wholesale Rules

Policy makers align spectrum, cybersecurity, and localization directives with digital-economy targets, removing fees on 5G frequencies and streamlining registration for specialized MVNO entities [2]Ministry of Digital Development, “Order on 5G Spectrum Fee Cancellation,” mincifra.gov.ru. Wholesale tariffs are audited to ensure reasonable access, although incumbent networks still set base prices. Data-sovereignty clauses push domestic platform investment, supporting emerging MVNO-enablement ventures backed by Rostelecom and VimpelCom. Simplified approval processes shorten launch cycles for fintech, retail, and IoT-centric brands that meet security benchmarks. Collectively, these measures underpin the long-run expansion outlook for the Russia Mobile Virtual Network Operator Market.

Rapid Expansion of IoT/M2M Connectivity Demand in Logistics and Utilities

Russia’s IoT market hit RUB 181 billion in 2024, and logistics fleets, smart meter deployments, and factory automation projects now favor specialized MVNO solutions. Platforms such as Kometa manage over 100,000 industrial SIMs through partnerships with MTS and Rostelecom. Full MVNOs with their own core networks are well-positioned to bundle managed services, analytics, and edge computing. NB-IoT overlays on 4G provide scalable coverage for metering and asset tracking, while private 5G pilots promise lower latency for robotics and process control. As industrial policy prioritizes technological sovereignty, machine-to-machine subscriptions remain the fastest-expanding addressable base.

Nation-Wide eSIM Adoption and Full-Digital Onboarding

MTS forecasts that 25% of connected devices will ship with embedded SIMs by 2025, accelerating instant provisioning and app-based account activation [3]MTS PJSC, “eSIM Growth Forecast in Russia,” mts.ru . SberMobile’s eSIM launch inside the SberBank Online super-app shows how existing digital ecosystems slash onboarding friction. Online distribution is already growing at a 12.93% CAGR, enabling MVNOs to reach peripheral regions without brick-and-mortar costs. Travel eSIM packs aimed at cross-border commuters and students broaden retail appeal. The model supports regulatory demands for customer ID verification while shrinking logistics overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oligopolistic MNO wholesale pricing power | –1.8% | Nationwide wholesale market | Long term (≥ 4 years) |

| Import-equipment restrictions under international sanctions | –1.1% | National infrastructure roll-outs | Medium term (2-4 years) |

| Data-localization and storage compliance costs for small MVNOs | –0.6% | Nationwide regulatory mandate | Short term (≤ 2 years) |

| Limited multi-operator eSIM QR-code retail channels outside tier-1 cities | –0.3% | Regional markets beyond Moscow and St. Petersburg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oligopolistic MNO Wholesale Pricing Power

The four national carriers, MTS, MegaFon, Beeline, and T2, own radio networks, towers, and transport assets, allowing them to dictate wholesale voice, SMS, and data rates that squeeze MVNO margins. T2 remains the only large-scale host, serving about 3.75 million virtual operator lines and attracting 54% of banking MVNO traffic. Vertical integration gives incumbents negotiating leverage on service-level agreements, backhaul provisioning, and interconnect fees. Smaller full MVNOs that need roaming and signaling links pay higher input costs than marketing-only resellers. Without deeper regulatory carve-outs, wholesale concentration will continue to restrain long-term profitability for the Russia MVNO market [4]Roskomnadzor, “Wholesale Access and Tariff Oversight Report 2025,” rkn.gov.ru.

Import-Equipment Restrictions Under International Sanctions

US and EU export controls on advanced radio and core-network gear limit vendor choice, forcing operators to shift to domestic alternatives that may command higher prices or lag in feature sets. The departure of Nokia, Ericsson, and several chipset suppliers amplifies procurement risk for niche MVNOs that rely on third-party billing, analytics, or IoT device libraries built on Western hardware. Mandates that 40% of components be Russian-made by 2025 further raise compliance costs. Although the state subsidizes local electronics plants, supply chain transition is likely to slow next-generation service launches and depress short-term growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Digital Transformation

Cloud-hosted enablement suites accounted for 26.85% revenue in 2024, yet they are set to grow at a 22.51% CAGR through 2030 as cost, scale, and compliance pressures mount. Domestic providers such as Yandex.Cloud, MTS Cloud, and Sber Cloud let virtual operators spin up real-time charging, CRM, and analytics modules within sovereign data centers, thereby satisfying localization rules and reducing capex. Banking brands favor cloud because it integrates smoothly with existing fintech stacks and open-API banking software. Legacy on-premise deployments still held 73.15% revenue during 2024, chiefly due to early-stage MVNOs embedded directly inside host-operator data centers.

Migration to the cloud also lowers time-to-market for niche propositions such as expatriate voice packs or single-use IoT device plans. Elastic compute allows traffic surges during marketing campaigns without stranded hardware. These advantages are pushing more entrants to bypass on-premise builds, underpinning sustained cloud traction inside the Russian Mobile Virtual Network Operator Market. As domestic hyperscalers continue to add 5G-ready packet-core features, the cloud option will remain the primary launch vector for upcoming entrants.

By Operational Mode: Banking MVNOs Lead Market Consolidation

Reseller and light-brand models represented 80.72% of 2024 revenue, mainly due to bundled offers from SberMobile, Tinkoff Mobile, and Alfa-Mobile that ride on T2’s wholesale network. These lightly regulated modes rely on host-provided numbering resources and signaling, which trims capital outlay. Service operator variants add their own billing stacks, enabling targeted loyalty promotions for cross-selling credit cards, insurance, and micro-loans. Full MVNOs, although only 19.28% by revenue, will expand at a 21.29% CAGR through 2030 as they seek network-independent innovation roadmaps that include specialized IoT cores and enterprise private-network slices.

Rostelecom’s RUB 1.7 billion purchase of MVNE player TVE-Telecom clarified the pivot toward in-house enablement services that support full-control models. As enterprise clients demand tailored quality-of-service and on-premise packet cores, full MVNO frameworks will secure bigger contracts in manufacturing and logistics. This dual-track evolution ensures the Russia Mobile Virtual Network Operator Market continues to accommodate low-cost consumer propositions while nurturing higher-margin B2B verticals.

By Subscriber Type: Enterprise Digitalization Accelerates IoT Growth

Consumer SIMs retained 84.25% share in 2024, anchored by widespread discount voice-and-data bundles that undercut MNO tariffs. Enterprise mobility subscriptions, covering corporate voice lines and VPN tunneling, formed a smaller but steady segment. IoT endpoints, though only a sliver of the total base, will surge at a 23.65% CAGR through 2030, driven by automated meter reading, vehicle telematics, and industrial telemetry. Mining operators in Yakutia and metallurgical plants in the Urals are trialing private cellular and edge analytics that ride on MVNO-managed SIMs.

As machine fleet sizes balloon from thousands to millions of units, billing flexibility, custom rate plans, and embedded SIM provisioning tilt procurement toward specialized MVNOs. Consumer lines mature into ARPU optimization plays, while enterprise and IoT categories unlock multi-year contracts with stable revenue flow, reshaping the overall revenue mix inside the Russia MVNO market.

By Application: M2M Connectivity Transforms Industrial Sectors

Discount voice and data still captured 56.84% of application revenue in 2024, reflecting keen household focus on affordable tariffs. Business-grade services, including secure access point names and IP-sec tunnels, support enterprise BYOD roll-outs. Cellular M2M links, expected to clock a 23.33% CAGR through 2030, underpin smart logistics hubs, energy grid monitoring, and predictive maintenance sensors. For example, Kometa connects over 100,000 industrial devices through agreements with MTS and Rostelecom that guarantee network diversity for critical operations.

Other niche applications cater to migrant communities, gamer-centric data passes, and short-term travel packs. The Russia Mobile Virtual Network Operator Market size for M2M is set to widen as new domestic chipset vendors emerge, while tax concessions for software exports help MVNOs develop value-added analytics that raise switching barriers.

By Network Technology: 5G Deployment Overcomes Spectrum Constraints

4G/LTE powered 86.71% of MVNO traffic in 2024, owing to nearly universal coverage in populated western oblasts. Legacy 3G layers gradually refarm into LTE, yet remain vital for voice fallback in remote provinces. The 5G segment, though still embryonic, is forecast to leap at a 52.76% CAGR as zero-fee spectrum licenses and domestic base-station programs aim to deploy 7,500 sites by 2025. Ultra-low-latency slices offer compelling use cases in robotics and augmented-reality logistics.

Satellite and non-terrestrial access supplements terrestrial gaps, particularly along the Northern Sea Route, where mining and energy firms always seek on-demand telemetry. As device vendors roll out Russian-made 5G modules, MVNOs will be able to issue standalone private-network packages, broadening addressable use cases and reinforcing the Russia Mobile Virtual Network Operator Market growth runway.

By Distribution Channel: Digital Transformation Reshapes Customer Acquisition

Traditional multibrand retail retained 46.46% of sign-ups in 2024, driven by older segments who prefer face-to-face transactions. Carrier sub-brand shops and third-party wholesalers supplement coverage in malls and transport hubs. However, online purchase journeys are rising at a 12.93% CAGR to 2030 as eSIM functionality enables instant activation through QR codes. SberMobile’s one-click purchase inside the SberBank super-app increased average daily activations by 35% during 2024, validating the digital push.

Third-party e-commerce platforms enhance availability in remote cities, while social-media chatbots provide plan configuration and subscriber verification. As digital onboarding scales, MVNOs lower logistics spend, enabling sharper price positioning and freeing capital for value-added services that enrich the Russia MVNO market experience.

Geography Analysis

Subscriber density and traffic monetization remain highest along the Moscow-St. Petersburg corridor, which also hosts most 5G pilots, large-scale eSIM promotions, and banking-brand retail expansions. Western oblasts benefit from dense fiber backhaul that improves quality-of-service for video-centric bundles and fintech super-app integrations. Secondary regions such as Tatarstan, Bashkortostan, and Krasnodar Krai are emerging battlegrounds where discount propositions resonate with price-sensitive households, helping MVNOs outrun MNO legacy tariffs. Siberian industrial zones, although population-sparse, generate high ARPU IoT traffic from mining operations that employ precision-drilling systems and autonomous hauling fleets.

The Urals manufacturing belt presents growing demand for private LTE and pilot 5G deployments, creating anchor clients for full MVNOs offering edge-compute gateways. Southern agricultural districts increasingly use cellular M2M for crop monitoring and tractor telemetry, further diversifying the geographic revenue mix. Cross-border trade routes with Kazakhstan and Belarus require roaming-friendly eSIM packs, pushing select MVNOs to negotiate bilateral wholesale deals despite sanction-driven equipment constraints. This mosaic of regional needs shapes a multi-speed expansion path for the Russia Mobile Virtual Network Operator (MVNO) Market.

Competitive Landscape

T2 commands most wholesale traffic, hosting more than half of banking-backed brands, illustrating the moderate consolidation level that defines the Russia MVNO market. SberMobile, Tinkoff Mobile, and Alfa-Mobile leverage existing financial ecosystems to keep churn below 4% and boost lifetime value through bundled cashback. Meanwhile, VimpelCom’s 64% stake in MVNE outfit Voca-Tech signals its intention to monetize network assets via enablement services, widening entry points for niche MVNOs. Rostelecom’s acquisition pipeline and in-house MVNE stack underwrite industrial IoT connectivity for energy majors.

Price competition intensifies as MegaFon licenses excess 4G capacity to ethnically focused brands targeting migrant workers. Strategic moves now orbit around cloud-native billing stacks, AI-based customer support bots, and data-driven upsell engines rather than pure tariff discounts. Sanction-induced vendor exits push operators to co-develop radio gear with domestic manufacturers, embedding supply-chain resilience into strategic planning. Collectively, these actions give the Russia Mobile Virtual Network Operator Market a balanced yet increasingly innovative outlook.

Russia Mobile Virtual Network Operator Industry Leaders

Yota (Scartel LLC)

Tinkoff Mobile LLC

SberMobile (Sberbank-Telecom)

Rostelecom PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: VimpelCom increased its stake in Voca-Tech to 64%, expanding MVNO enablement capabilities and diversifying wholesale revenue streams.

- January 2025: Kazakhtelecom completed the USD 1.1 billion divestment of Mobile Telecom Service LLP to Power International Holding, setting a regional precedent for operator carve-outs.

- October 2024: Russia invested RUB 100 billion in the Bureau 1440 satellite constellation to bolster non-terrestrial connectivity options for remote MVNO deployments.

- October 2024: Alfa-Bank launched Alfa-Mobile MVNO services on Beeline infrastructure, underlining continued banking-sector interest in virtual operator models.

Russia Mobile Virtual Network Operator Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Russia MVNO market in 2025?

The market is valued at USD 0.87 billion with a projected rise to USD 1.16 billion by 2030.

What drives demand for virtual operators in regional Russian cities?

Lower-cost plans and growing eSIM adoption help MVNOs outcompete MNO tariffs, especially where disposable income is limited.

Which subscriber segment is expanding fastest?

IoT lines are set to expand at a 23.65% CAGR, fueled by logistics and industrial automation projects.

Why are banking institutions dominant MVNO players?

Established customer bases and digital-banking apps reduce acquisition costs and support bundled service uptake.

How is government policy shaping MVNO growth?

Zero-fee 5G spectrum, streamlined licensing, and 5% IT tax rates collectively create a supportive operating climate.

What limits MVNO profitability today?

Concentrated wholesale pricing controlled by the four national MNOs compresses margins for independent full MVNOs.

Page last updated on: