Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

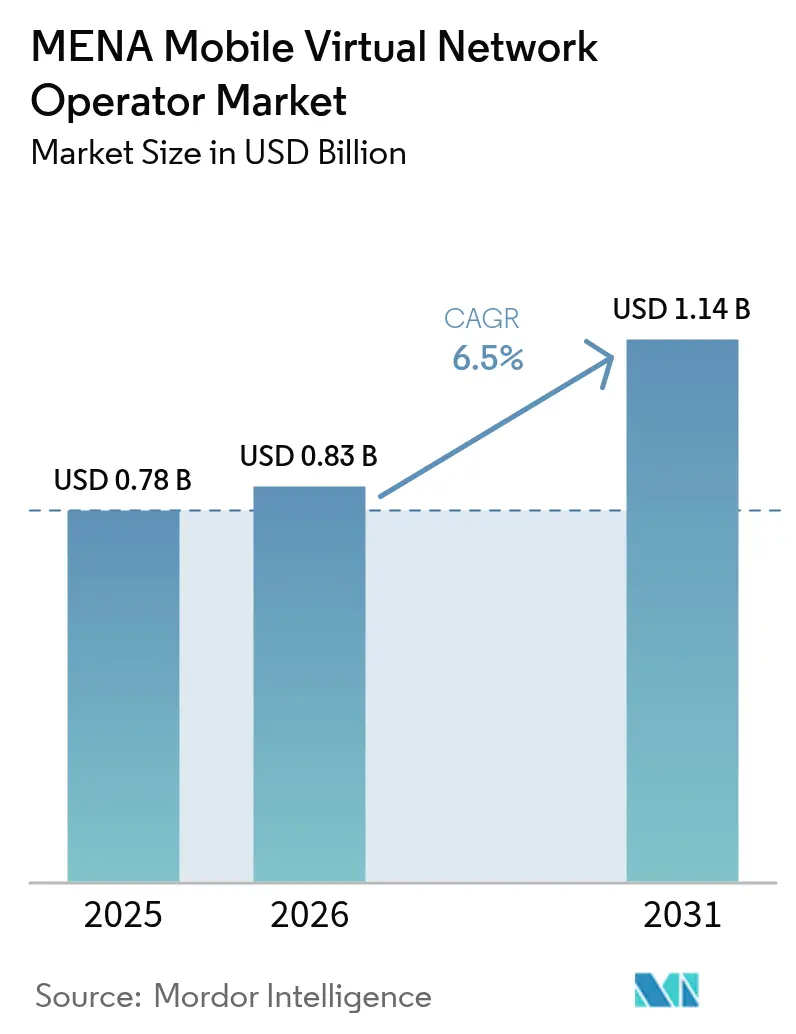

| Base Year Market Size (2025) | USD 0.78 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

MENA Mobile Virtual Network Operator Market size in 2026 is estimated at USD 0.83 billion, growing from 2025 value of USD 0.78 billion with 2031 projections showing USD 1.14 billion, growing at 6.5% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 12.5 million subscribers in 2025 to 16.64 million subscribers by 2030, at a CAGR of 5.89% during the forecast period (2025-2030). The expansion reflects accelerating digital transformation, favorable wholesale regulations, and the appeal of low-cost, app-centric mobile propositions. Cloud-native platforms, eSIM adoption, and satellite-NTN links reduce capital intensity and allow operators to reach niche segments quickly. Regulatory price caps continue to compress wholesale fees in Saudi Arabia, the UAE, and Oman, widening gross‐margin headroom for agile newcomers. Competitive focus is tilting toward IoT enablement, cross-border remittance bundling, and lifestyle-based sub-brands rather than pure price-cutting.

Key Report Takeaways

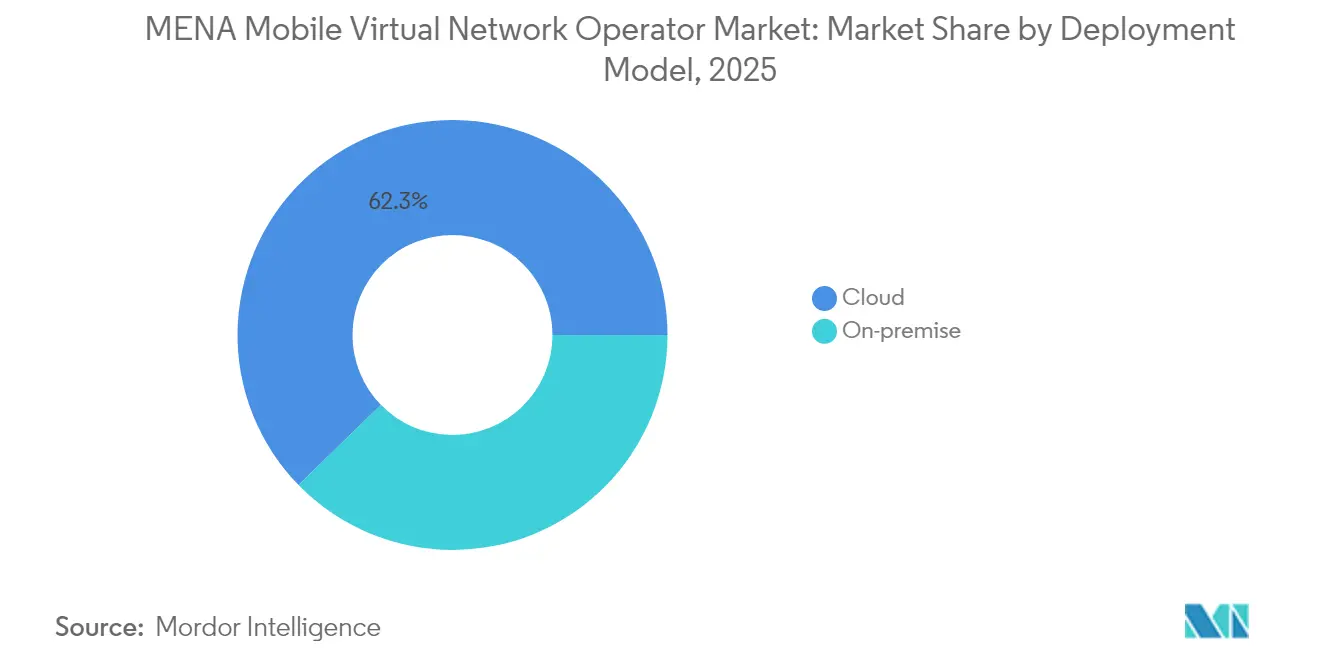

- By deployment model, cloud infrastructure captured 62.30% revenue share of the MENA MVNO market in 2025, and the segment is projected to grow at 11.45% CAGR through 2031.

- By operational mode, reseller/light/brand MVNOs held 62.85% of the MENA MVNO market share in 2025, while full MVNOs are advancing at a 23.6% CAGR to 2031.

- By subscriber type, consumer segment commanded 84.10% share of the MENA MVNO market size in 2025, whereas IoT-specific connections are forecast to expand at 24.9% CAGR between 2026-2031.

- By application, discount services led with 43.10% share in 2025, while cellular M2M connectivity is the fastest growing application at 17.75% CAGR to 2031.

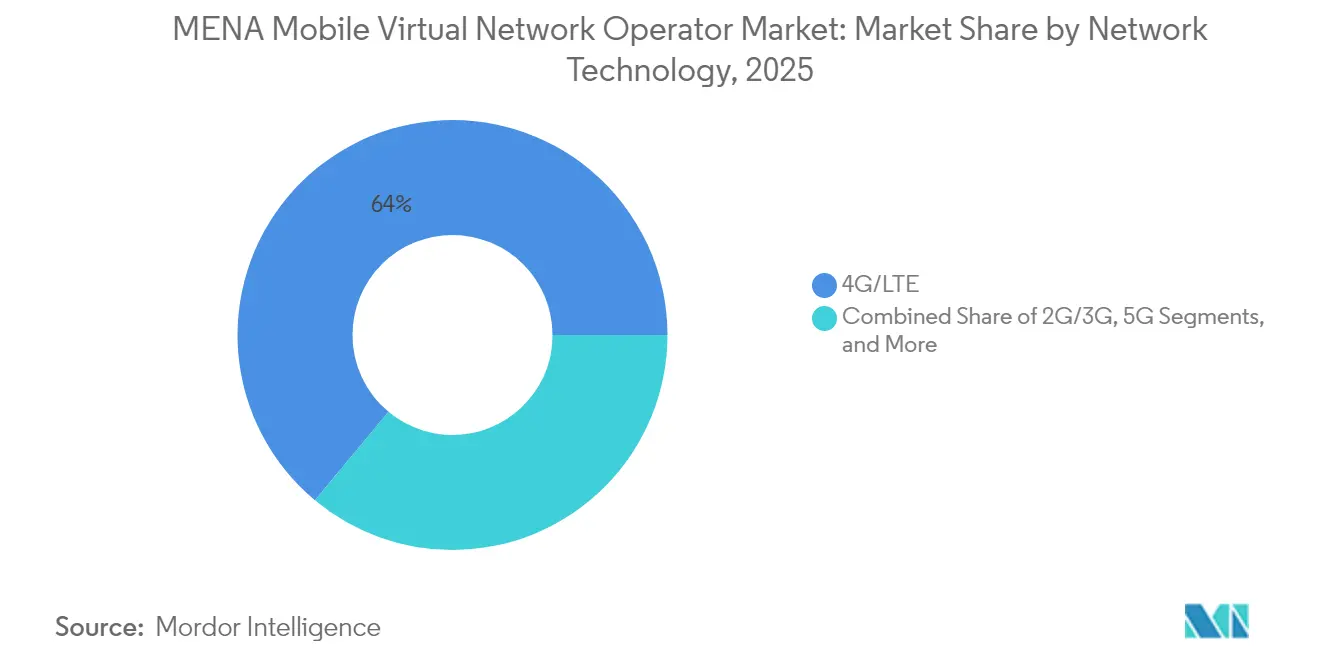

- By network technology, 4G/LTE supported 63.95% of deployments in 2025, yet satellite/NTN connections are set to climb at 124.8% CAGR through 2031.

- By distribution channel, the online/digital-only channel captured 50.05% revenue share of the MENA MVNO market in 2025, while the third-party/wholesale segment is projected to grow at 12.9% CAGR through 2031.

- By geography, the Middle East contributed 60.10% of 2025 revenue and is on course for a 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MENA Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive expatriate and youth segments fuel prepaid churn towards MVNOs | +1.8% | GCC core; spill-over to North Africa | Medium term (2-4 years) |

| 5G-enabled digital brands leverage eSIM and app-only onboarding | +1.2% | Middle East; selective North Africa | Short term (≤ 2 years) |

| Regulator-mandated network-sharing/wholesale price caps improve MVNO economics | +0.9% | Saudi Arabia, UAE, Oman; wider MENA | Long term (≥ 4 years) |

| Cross-border remittance bundling (e.g., airtime-to-cash corridors) | +0.7% | GCC–North Africa corridors | Medium term (2-4 years) |

| Satellite–NTN connectivity for remote oil and gas sites | +0.6% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Green fintech-MVNO hybrids monetize carbon-credit micro-transactions | +0.4% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Expatriate and Youth Segments Fuel Prepaid Churn

Roughly 10 million expatriates in Saudi Arabia and large youth cohorts across the GCC seek low-commitment prepaid plans, prompting steady subscriber migration toward MVNO offers that combine cheaper international minutes with flexible data allocations. Number-portability reforms and fully digital onboarding remove switching friction, accelerating churn away from incumbents. Virgin Mobile’s jump to 3.5 million regional users illustrates how simplified tariffs plus in-app servicing capture scale quickly. The resulting pressure forces host operators to renegotiate wholesale terms to retain outbound traffic, indirectly improving MVNO economics. Expat and youth-led growth, therefore, secures a stable demand base for the MENA MVNO market without heavy marketing spend.

5G-Enabled Digital Brands Leverage eSIM and App-Only Onboarding

Regional eSIM connections are tracking 20% annual growth, with projections of 135 million active profiles by 2028, allowing MVNOs to forgo physical distribution and activate users in minutes.[1]GSMA, “eSIM: State of the Consumer Market 2025,” gsma.com Platforms such as Jawwy by stc rely on cloud-native charging stacks that push real-time offers and policy controls to customer apps, lowering acquisition costs and supporting granular segmentation. The convergence of 5G network slicing with eSIM provisioning enables micro-bundles, daily gigabyte passes, or latency-optimized streams, creating monetizable use cases absent from SIM card channels. As a result, digital-only brands enhance stickiness and lift ARPU even when headline tariffs remain low, reinforcing growth prospects for the MENA MVNO market.

Regulator-Mandated Network-Sharing and Wholesale Price Caps Improve Economics

Saudi Arabia, the UAE, and Oman have enforced cost-based wholesale access that narrows the retail-minus spread and gives MVNOs predictable margin structures. Kuwait’s SMS termination rules and Morocco’s penalties on Maroc Telecom for abuse of dominance further attest to a policy shift favoring service diversity. Stable wholesale inputs shorten payback periods and unlock more aggressive go-to-market strategies for new entrants. Over the long term, these reforms contribute almost a percentage point to the projected CAGR of the MENA MVNO market as barriers to entry fall and price innovation intensifies.

Satellite-NTN Connectivity for Remote Oil and Gas Sites

New 5G-NR-based non-terrestrial networks from Space42 and Viasat promise direct-to-device links that bypass terrestrial coverage gaps in deserts, rigs, and maritime lanes. With the regional upstream energy sector requiring resilient telemetry and workforce safety feeds, satellite MVNO propositions can charge premium rates while avoiding heavy tower rollouts. Early trials in the UAE and Oman indicate download speeds sufficient for HD video inspection, a pivotal use case for field engineers. This emerging capability is set to inject incremental revenue into the MENA MVNO market and broaden its addressable footprint beyond urban cores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High mobile-data floor prices in Gulf states squeeze MVNO ARPU | -0.8% | GCC markets, particularly UAE, Kuwait, Bahrain | Short term (≤ 2 years) |

| Limited number-portability in North Africa curbs subscriber switching | -0.5% | North Africa core, Egypt, Morocco, Tunisia, Algeria | Medium term (2-4 years) |

| Rising wholesale 5G slicing fees vs. legacy 4G rates | -0.4% | Global MENA, early impact in Saudi Arabia, UAE | Short term (≤ 2 years) |

| Geopolitical spectrum-allocation delays (e.g., Libya, Yemen) | -0.3% | Libya, Yemen, selective conflict-affected areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Mobile-Data Floor Prices in Gulf States Squeeze ARPU

Wholesale data-floor regulations mean MVNOs in the UAE and Kuwait often pay per-gigabyte rates that are 15-20% above European comparables, constraining headline discounts and limiting addressable mass-market segments. While value-added features can offset some margin loss, operators struggle to undercut incumbents on data-hungry consumer plans. Competitive differentiation, therefore, shifts to lifestyle branding, loyalty perks, and fintech add-ons rather than aggressive price moves, tempering near-term upside for the MENA MVNO market.

Limited Number-Portability in North Africa Curbs Switching

Patchy port-out procedures in Egypt and Algeria prolong activation cycles and force many users to abandon long-held numbers when migrating to alternative providers, cooling churn rates, and raising acquisition costs. Regulatory focus on infrastructure investment over retail competition delays full portability mandates. For MVNOs, the friction reduces campaign efficiency and stunts word-of-mouth virality, shaving half a percentage point off expected CAGR contributions within North African sub-markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Platforms Secure Cost Leadership

Cloud implementations held 62.30% revenue in 2025 and pushed the MENA MVNO market size forward with an 11.45% CAGR. The operating model removes hefty capex items such as mobile switching nodes and allows pay-as-you-grow scaling, creating a breakeven horizon under 18 months for greenfield brands. AI-assisted fraud checks and real-time policy engines come bundled with most hyperscale offerings, reinforcing service quality.

On-premise environments persist where data-sovereignty clauses require local processing, notably in sovereign energy and defense verticals. These deployments impose longer deployment cycles yet deliver tight network integration for service-level commitments. Vendors are increasingly hybridizing solutions by anchoring mission-critical functions on private clouds while shifting mediation, analytics, and billing to multitenant regions, smoothing migration paths for legacy MVNOs.

By Operational Mode: Full MVNOs Capture Strategic Control

Reseller/light/brand formats accounted for 62.85% of the MENA MVNO market share in 2025 as quick-launch brands leveraged existing host assets. Yet full MVNO frameworks, controlling core network elements and SIM profiles, are set to record 23.6% CAGR, signaling the market’s march toward service autonomy.

Branded concepts like Red Bull Mobile experiment with perpetual Gigacoin data wallets, a structure unviable under restrictive reseller contracts. Full control allows independent roaming deals and on-demand quality tiers built atop 5G network slices. Over time, richer margins and differentiated feature sets propel full MVNO appeal, anchoring long-term competitiveness inside the MENA MVNO market.

By Subscriber Type: IoT Becomes the Next Revenue Hill

Consumer users dominated with an 84.10% share in 2025, driven by expatriate demand for low-cost international calling. Enterprise lines add predictable revenue through managed mobility contracts, but IoT links are pacing fastest with 24.9% CAGR.

In Oman, IoT SIMs grew 72% year on year to 1.1 million, covering tank monitoring, smart irrigation, and fleet tracking. Specialist MVNOs that bundle sensor modules, cloud dashboards and data analytics command ARPU multiples of pure connectivity. Consequently, the MENA MVNO market is shifting investment toward vertical-solution playbooks that couple connectivity with domain services.

By Application: M2M Connectivity Outruns Discount Voice

Discount packages retained a 43.10% share in 2025, serving price-driven churners. Yet machine-centric cellular M2M traffic is projected to compound at 17.75% CAGR through 2031, surpassing business voice in incremental revenue addition.

Global IoT aggregators such as Emnify rent capacity wholesale and resell SIMs with pooled data, multi-IMSI fallback, and policy APIs, features prized by energy and logistics customers. MVNOs piggybacking such stacks can leapfrog into industrial segments without heavy R&D, letting them diversify beyond narrow-margin prepaid voice.

By Network Technology: Satellites Extend Edge Coverage

4G/LTE underpinned 63.95% of 2025 live bases, while 5G rollouts across seven GCC nations promise bandwidth-rich propositions. Satellite/NTN is the breakout, swelling at 124.8% CAGR as field sites, maritime fleets, and desert supply chains demand always-on telemetry.

Qatar aims to shutter 3G networks by December 2025 to reclaim spectrum for 5G, forcing legacy-device migrations. MVNOs that integrate satellite payloads with terrestrial roaming offer seamless fallback, insulating industrial clients from planned sunsets and advancing the frontier of the MENA MVNO market.

By Distribution Channel: Digital-Only Portals Cut CAC

Online/digital-only channels accounted for 50.05% revenue in 2025 by stripping out SIM logistics and kiosk staffing. eSIM QR codes and instant KYC via national ID apps enable one-click activation, shrinking acquisition cost by 40-60%.

Third-party e-voucher platforms such as Paynet.red add reach in expatriate neighborhoods via grocery stores and web wallets, delivering 12.9% CAGR growth to wholesale channels. Although physical stores endure for handset bundles and enterprise demos, digital onboarding dominates incremental net adds, underscoring the importance of UX investment across the MENA MVNO market.

Geography Analysis

Middle Eastern operators commanded 60.10% revenue in 2025 and are projected to book a 7.75% CAGR through 2031. Saudi Arabia’s Vision 2030 strategy seeded regulatory incentives that accelerated MVNO licensing, while Mobily’s six-year infrastructure pact, worth over 5% of 2023 revenue, guarantees capacity for brand partners. The UAE blends high eSIM penetration with national digital-ID onboarding, giving MVNOs frictionless sign-up funnels. Oman lifted licensed entities to 24 and recorded 7.5 million active lines, lighting a path for SME-oriented virtual brands.

North Africa held a 39.90% share, yet differing portability policies and constrained device financing temper growth. Egypt’s e& Cash wallet opens airtime-to-cash corridors for 10 million migrant workers, but a lack of seamless number transfer slows churn from incumbents. Morocco’s antitrust clamp-down on Maroc Telecom benefits newcomers, while Tunisia’s three-operator 5G auction hints at future wholesale openings. Algeria’s cautious liberalization keeps MVNO proposals in limbo, though large remittance-receiving communities remain tantalizing.

Regional cross-border strategic agreements, such as those with Ooredoo, Mobily with iBASIS, create a harmonized ICT backbone, allowing MVNOs to provision unified regional plans that roam seamlessly. Satellite beams complement terrestrial gaps from Libyan desert oilfields to Yemeni highlands, extending the serviceable addressable market. Divergent 5G maturity levels imply country-specific entry tactics, yet the broader region remains on an upward adoption curve that benefits the overall MENA MVNO market.

Competitive Landscape

Competition sits at a middle point between oligopoly and fragmentation. Virgin Mobile MEA, FRiENDi, Jawwy, and Red Bull MOBILE surpass 4.5 million combined subscribers, while dozens of micro-brands exploit fintech or lifestyle adjacencies. Cloud billing, AI-driven fraud filters, and network-slice brokerage become standard differentiators.

Virgin Mobile’s single app supports KYC, eSIM download, and cross-border top-up, cutting average handling time to under five minutes. Red Bull Mobile pairs unlimited social media passes with event access, leaning on parent-brand equity to offset price rigidity. Jawwy, by integrating Celfocus's policy control with MATRIXX's rating, empowers users to exchange data for minutes in real-time, enhancing its perceived value.

Beyond ONE and TIMWETECH deliver carrier billing to 3.5 million GCC users, monetizing digital content in cash-heavy societies. Upcoming green-fintech hybrids plan to bundle carbon-credit micro-transactions with airtime, hinting at service modularity imperatives that shape future competition inside the MENA MVNO market.

MENA Mobile Virtual Network Operator Industry Leaders

Lebara Mobile KSA

FRiENDi Mobile Oman (Beyond ONE)

Renna Mobile Oman

Jawwy (Saudi Telecom Company)

Virgin Mobile Middle East and Africa (Beyond ONE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Beyond ONE joined TIMWETECH to deploy digital content billing across Virgin Mobile Saudi Arabia and FRiENDi Oman, covering 3.5 million lines.

- February 2025: Mobily deepened collaboration with iBASIS to bolster international data roaming quality for MVNO partners.

- October 2024: stc Group and Ooredoo Group signed an MoU to coordinate wholesale frameworks across key MENA markets.

- September 2024: Mobily sealed a six-year infrastructure deal with Red Bull MOBILE valued at over 5% of 2023 revenue.

- February 2024: Jawwy refreshed its digital CX with real-time policy and charging upgrades from Celfocus and MATRIXX.

MENA Mobile Virtual Network Operator Market Report Scope

Mobile virtual network operators (MVNO) are wireless communications services provider that does not have the wireless network infrastructure over which it provides services to their customers. These companies sign a business agreement with a mobile network operator, buy bulk access to network services at wholesale rates, and set retail prices independently.

The MENA Mobile Virtual Network Operator Market is segmented by Subscriber (Business and Consumer) and Country (United Arab Emirates, Saudi Arabia, Oman, Iran, and the Rest of Middle East & North Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Deployment Model

| Cloud |

| On-premise |

By Operational Mode

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

By Subscriber Type

| Consumer |

| Enterprise |

| IoT-specific |

By Application

| Discount |

| Business |

| Cellular M2M |

| Others |

By Network Technology

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

By Distribution Channel

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| North Africa | Egypt |

| Morocco | |

| Tunisia | |

| Algeria | |

| Rest of North Africa |

| By Deployment Model | Cloud | |

| On-premise | ||

| By Operational Mode | Reseller / Light / Brand MVNO | |

| Service Operator | ||

| Full MVNO | ||

| By Subscriber Type | Consumer | |

| Enterprise | ||

| IoT-specific | ||

| By Application | Discount | |

| Business | ||

| Cellular M2M | ||

| Others | ||

| By Network Technology | 2G/3G | |

| 4G/LTE | ||

| 5G | ||

| Satellite/NTN | ||

| By Distribution Channel | Online / Digital-only | |

| Traditional Retail Stores | ||

| Carrier Sub-brand Stores | ||

| Third-Party / Wholesale | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| North Africa | Egypt | |

| Morocco | ||

| Tunisia | ||

| Algeria | ||

| Rest of North Africa | ||

Key Questions Answered in the Report

What is the current value of the MENA MVNO market?

The MENA MVNO market is valued at USD 0.83 billion in 2026 and is forecast to reach USD 1.14 billion by 2031.

Which deployment model leads adoption?

Cloud platforms dominate with 62.30% revenue share because they lower capex and accelerate regional launches.

How fast is satellite–NTN connectivity growing?

Satellite and other non-terrestrial links are projected to post a 124.8% CAGR through 2031 as energy and maritime sectors demand remote coverage.

Which subscriber segment is expanding the quickest?

IoT-specific connections are forecast to grow at 24.9% CAGR, outstripping consumer and enterprise lines.

Which country contributes the largest share?

The Middle East, led by Saudi Arabia and the UAE, accounts for 60.10% of 2025 market revenue.

What keeps ARPU under pressure in Gulf markets?

Wholesale data-floor pricing prevents MVNOs from offering deep discounts, forcing differentiation through non-price features.

Page last updated on: