Hong Kong Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

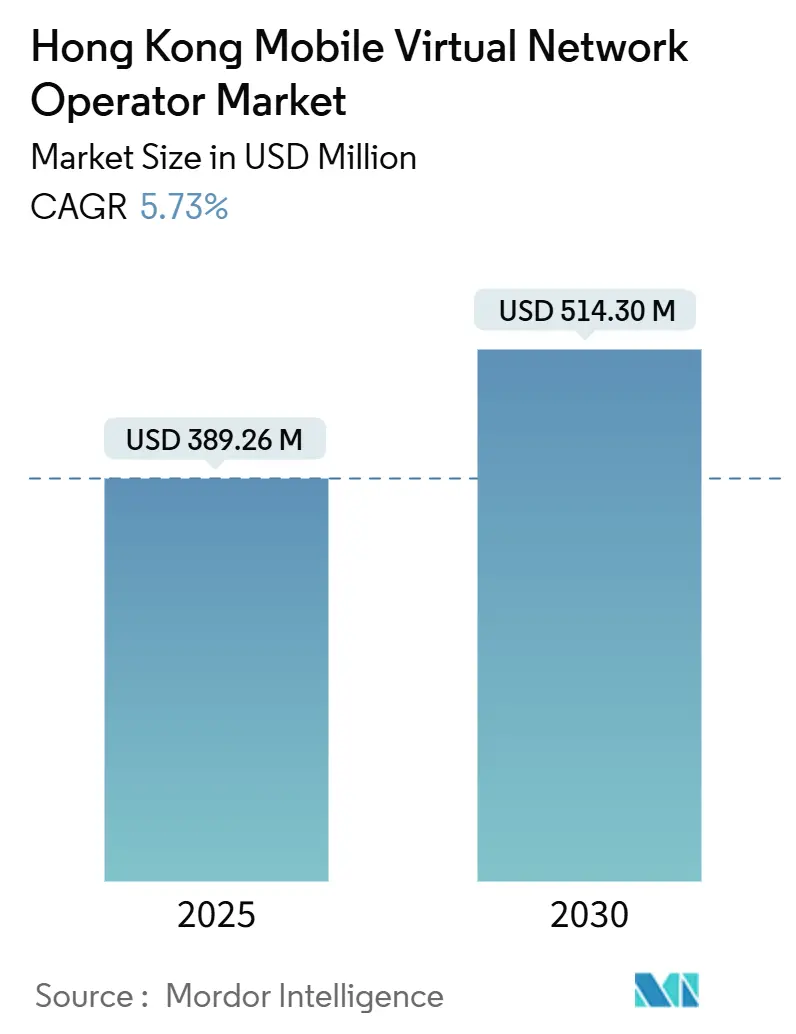

| Market Size (2025) | USD 389.26 Million |

| Market Size (2030) | USD 514.30 Million |

| Growth Rate (2025 - 2030) | 5.73% CAGR |

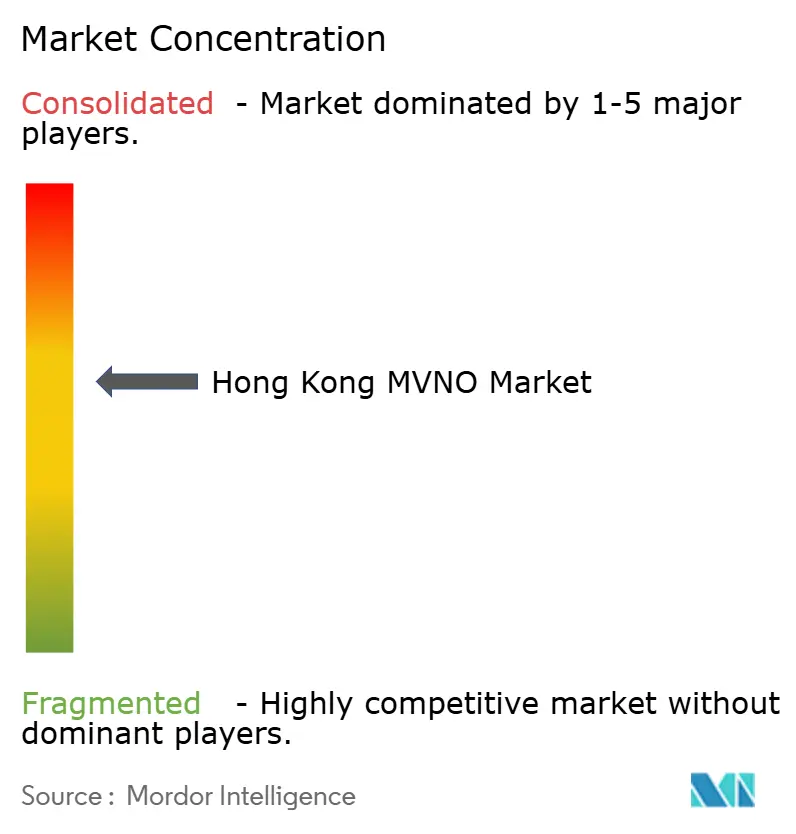

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

The Hong Kong Mobile Virtual Network Operator Market size is estimated at USD 389.26 million in 2025, and is expected to reach USD 514.30 million by 2030, at a CAGR of 5.73% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 4.32 million subscribers in 2025 to 5.38 million subscribers by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

This steady advance reflects a mature yet innovation-friendly telecoms arena where a structured 5-year SIM-VNO licensing scheme provides regulatory certainty, 5G wholesale access lowers capital outlays, and cross-border digital payment integration enlarges addressable demand. Network-technology upgrades are decisive, with direct-to-phone satellite services supplementing ubiquitous 4G/LTE and accelerating niche IoT rollouts in smart-port logistics. Competitive dynamics hinge on targeted service bundles, especially low-cost roaming for 34 million annual visitors, eSIM-based digital onboarding, and FinTech-telco tie-ups that knit Hong Kong, Macau, and nine Greater Bay Area cities into a single usage footprint. Although incumbent MNO sub-brands engage in sharp price maneuvers, MVNOs that align with cross-border needs, machine-to-machine (M2M) connectivity, and digital-only customer journeys continue to carve out defensible positions in the Hong Kong MVNO market.

Key Report Takeaways

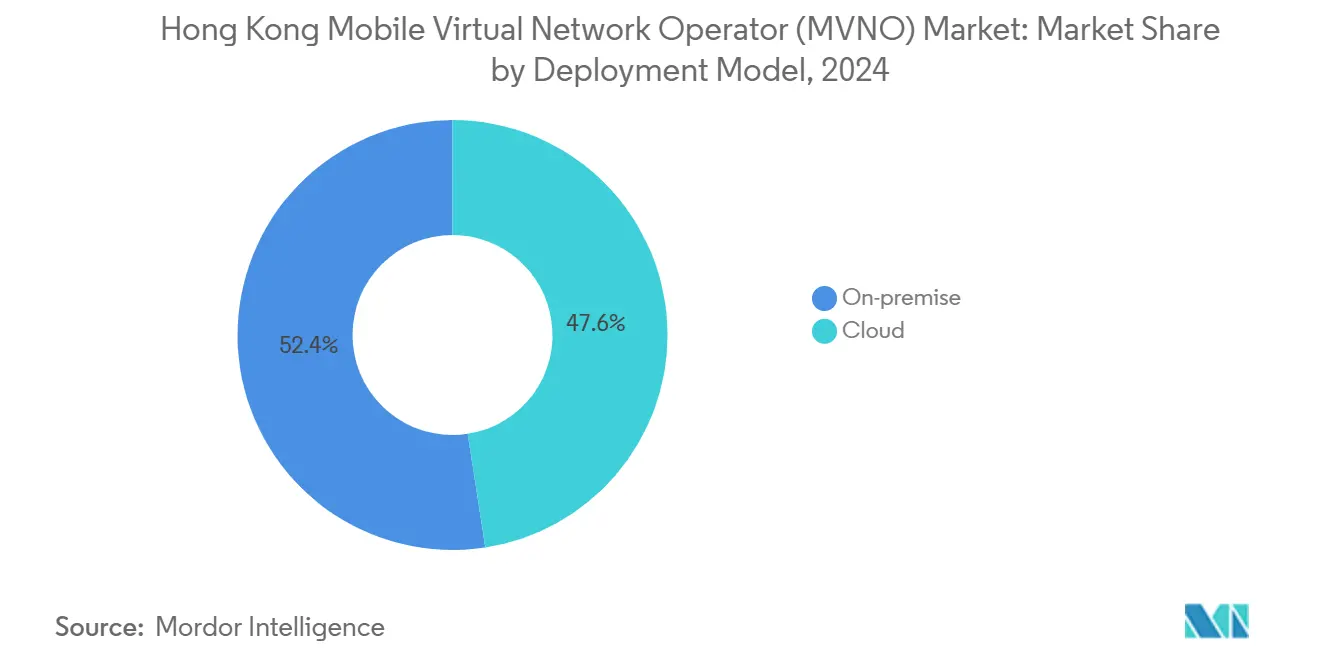

- By deployment model, on-premise solutions held 52.43% of the Hong Kong mobile virtual network operator (MVNO) market share in 2024; cloud deployments are projected to rise at a 15.30% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs led with 45.62% revenue share in 2024, while service-operator models are set for the fastest 10.60% CAGR to 2030.

- By subscriber type, consumers accounted for 65.60% of the market size in 2024, whereas IoT lines are advancing at a 14.31% CAGR over the forecast horizon.

- By application, discount services controlled 38.46% share of the Hong Kong mobile virtual network operator market size in 2024; cellular M2M connectivity is pacing ahead at 13.79% CAGR to 2030.

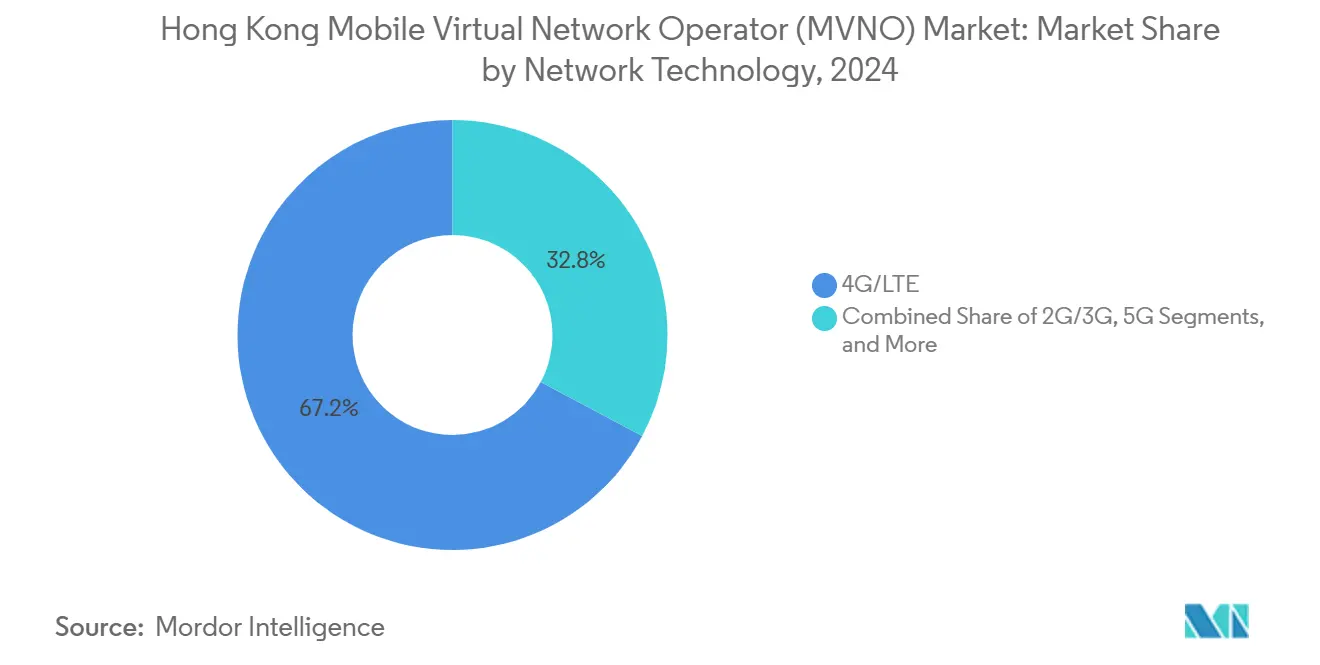

- By network technology, 4G/LTE preserved 67.21% market share in 2024; satellite/NTN lines are slated for a 45.88% CAGR through 2030.

- By distribution channel, online/digital-only sales captured a 53.52% share in 2024 and are growing at a 10.40% CAGR to 2030.

Hong Kong Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread 5G wholesale access lowering entry barriers | +1.2% | Hong Kong territory-wide | Short term (≤ 2 years) |

| Government-backed Open Network Access and 5-year “SIM-VNO” license scheme | +0.8% | Hong Kong territory-wide | Medium term (2-4 years) |

| Soaring demand for low-cost international roaming among expatriates and tourists | +1.5% | Hong Kong and cross-border | Medium term (2-4 years) |

| High smartphone eSIM adoption enabling digital-only onboarding | +0.9% | Hong Kong territory-wide | Short term (≤ 2 years) |

| Cross-border FinTech-telco bundles (e.g., wallet-with-SIM) creating new niches | +0.7% | Greater Bay Area | Long term (≥ 4 years) |

| IoT rollout in smart ports and logistics hubs driving M2M lines | +0.6% | Hong Kong and regional logistics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread 5G wholesale access lowering entry barriers

OFCA’s 2024 spectrum auctions delivered plentiful mid-band and millimeter-wave capacity at competitive wholesale prices, allowing new entrants to access advanced radio assets without heavy infrastructure spend [1]FCA, “Spectrum Auction Results 2024,” ofca.gov.hk. Dense urban topology further compresses cell-site requirements, making the Hong Kong mobile virtual network operator (MVNO) market an attractive landing pad for global brands seeking a fast regional foothold. The same wholesale rules empower IoT-specific MVNOs to run low-latency industrial applications in Hong Kong’s automated container terminals. With quick network leases and manageable capital exposure, smaller players can test differentiated value propositions around roaming packs, satellite backup, or M2M guarantees, reshaping competitive boundaries in the market.

Government-backed open-network access and 5-year SIM-VNO license scheme

Hong Kong’s SIM-VNO framework grants five-year permits, assures nondiscriminatory wholesale terms, and stipulates clear numbering allocations, an uncommon level of certainty among regional regimes. Such predictability spurs multi-country operators to align long-range capital plans with Hong Kong service launches. License clauses also earmark IoT traffic categories, supporting narrow-band requirements for logistics hubs and smart city devices. While compliance with real-name SIM rules from February 2023 imposes extra onboarding steps, uniform enforcement creates a level playing field that undergirds trust and bolsters the growth trajectory of the Hong Kong mobile virtual network operator (MVNO) market.

Low-cost international roaming demand from expatriates and tourists

The territory’s 7.4 million residents and 34 million yearly visitors fuel a constant quest for budget-friendly data when crossing between Hong Kong, Macau, and Guangdong cities. Greater Bay Area roaming alliances now allow MVNOs to negotiate pooled wholesale rates and issue unified phone numbers, slashing traveler bills [2]Qiu Quanlin, “MPay Can Be Used in Guangzhou Public Transport,” chinadaily.com.cn. Bundled QR-code payments via AlipayHK augment convenience, letting MVNO packages double as e-wallet rails. These twin advantages widen the addressable audience for specialty providers in the Hong Kong MVNO market while locking in higher lifetime value through payments-plus-connectivity offers.

High smartphone eSIM adoption enabling digital-only onboarding

Hong Kong logs 17.4 million mobile connections, an average of 2.35 per person, reflecting multi-device lifestyles perfect for eSIM’s multi-profile design. Real-time QR-activation eliminates retail overhead, letting digital-native MVNOs acquire customers remotely pre-arrival. Automated KYC integrations satisfy real-name requirements in-app, shaving onboard friction to seconds. Faster activation and zero-store costs reduce churn risk and free capital for service innovation, reinforcing the Hong Kong mobile virtual network operator market’s tilt toward agile, cloud-centric challengers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small domestic population capping total addressable subscribers | -0.9% | Hong Kong territory-wide | Long term (≥ 4 years) |

| Aggressive price cuts by MNO sub-brands squeezing MVNO margins | -1.1% | Hong Kong territory-wide | Short term (≤ 2 years) |

| High 5G wholesale bandwidth fees tied to steep volume commitments | -0.7% | Hong Kong territory-wide | Medium term (2-4 years) |

| Stricter real-name SIM registration raising onboarding friction | -0.5% | Hong Kong territory-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Small domestic population capping total subscribers

With only 7.4 million residents, Hong Kong sets a natural ceiling on mass-market lines. Incumbent MNOs already command entrenched customer bases through converged mobile-broadband bundles, constraining residual volume for newcomers. MVNOs, therefore, pivot to higher-yield niches such as IoT fleets, expatriate roaming, and premium cross-border bundles. This necessity pushes product creativity but raises customer-acquisition costs, tempering the long-run expansion pace of the Hong Kong mobile virtual network operator (MVNO) market.

Aggressive price cuts by MNO sub-brands squeezing MVNO margins

Operators like SmarTone’s Birdie and 3 Hong Kong’s SoSIM wield direct network access and integrated billing to underprice wholesale-dependent MVNOs while retaining premium flagship brands. Margin compression forces discount-oriented MVNOs toward unsustainable pricing or service withdrawal, thinning competitive variety. Sustainability thus hinges on service differentiation, FinTech tie-ups, satellite fallback, or vertical-specific IoT, not headline tariffs, adding strategic complexity to the Hong Kong MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud migration accelerates digital transformation

On-premise platforms controlled 52.43% of Hong Kong MVNO market share in 2024, mirroring the territory’s legacy switch and BSS estates. Yet the cloud cohort is scaling briskly at 15.30% CAGR, propelled by lower capex thresholds and rapid service-launch cycles that attract cross-border entrants. The market size gains for cloud deployments are tied to elastic server capacity that matches seasonal tourist swings.

Cloud-native MVNOs exploit API-based rating, real-time roaming updates, and AI help desks to shrink operating expenses and bolster net promoter scores. Joint cloud regions in Hong Kong and Shenzhen shorten latency for Greater Bay Area data sessions, enhancing user experience for travelers who straddle both sides of the boundary. Suppliers of network-as-software modules see expanding addressable revenue as more MVNOs trade hardware racks for SaaS stacks inside the Hong Kong MVNO market.

By Operational Mode: Service operators gain traction through specialization

Reseller/light brands led revenue at 45.62% in 2024, owing to simple wholesale resale. However, service-operator licenses are forecast to rise 10.60% CAGR by 2030 as MVNOs seek deeper customer-experience control. Hong Kong MVNO market size enlargement in this tier stems from embedded policy engines enabling differentiated data buckets, quality of service tiers, and FinTech add-ons.

Service-operator status also unlocks direct SIM management, critical for IoT fleets that require remote profile swaps across mainland-Hong Kong corridors. While full-MVNO ambitions remain limited by market scale, mid-tier control balances agility with manageable opex. This sweet spot encourages both foreign and local brands to upgrade license class, sharpening competitive variety within the Hong Kong mobile virtual network operator Market

By Subscriber Type: IoT segments drive future growth

Consumers dominate with 65.60% of the Hong Kong mobile virtual network operator (MVNO) market size in 2024; nonetheless, IoT SIMs are rising 14.31% CAGR as smart-port automation demands always-on container tracking. Predictable data bursts and low-latency 5G slices appeal to logistics operators managing 18 million TEU throughput annually at Kwai Tsing terminals.

Enterprise smartphone fleets remain stable yet comparatively slow-growing. MVNOs package eSIM multi-profile offers so executives can toggle mainland and Hong Kong numbers seamlessly. Consumer-segment competition thus shifts from raw GB pricing toward convenience bundles, e-wallet tie-ins, airport pick-up, and zero-touch activation, which fortify brand loyalty in the high-ARPU strata of the Hong Kong mobile virtual network operator (MVNO) market.

By Application: M2M connectivity transforms industrial operations

Discount voice-data bundles held a 38.46% share in 2024, but cellular M2M lines will post a 13.79% CAGR as cranes, AGVs, and smart-meter networks demand resilient links. Hong Kong mobile virtual network operator market share gains in M2M come from specialized SLAs, 99.95% uptime, static IP, and secure APN, which generic consumer packs cannot match.

Business-application MVNOs harness hybrid cloud BSS to serve multinationals that mandate unified roaming invoices across Asia. Other niche uses, event pop-up coverage, and disaster backup, round out the long tail. As pricing wars erode discount-segment margins, operators redirect capital toward higher-value telemetry and industrial analytics, bolstering profitability levers within the Hong Kong MVNO market.

By Network Technology: Satellite integration reshapes connectivity options

4G/LTE retained 67.21% share in 2024, underscoring handset inertia and network ubiquity. Yet satellite/NTN subscriptions are predicted to surge 45.88% CAGR as China Telecom’s Tiantong service extends signal to vessels and hilltop emergency crews. Hong Kong MVNO market size increments from satellite-derived derive from bundled plans combining urban 5G with maritime backup under a single eSIM profile.

Parallel 2G/3G sunset timetables compel late-adopter consumers to migrate, unlocking upsell opportunities. Early 5G SA trials across Kowloon Bay industrial areas also seed demand for network slicing, letting MVNOs retail guaranteed-latency slices for AR/VR logistics training. Such tech layering cements Hong Kong’s standing as one of Asia’s most advanced MVNO innovation sandboxes.

By Distribution Channel: Digital channels dominate customer acquisition

Online self-service captured 53.52% of sales in 2024, benefiting from 92% internet penetration and trilingual app interfaces that guide instant eSIM installs. Hong Kong MVNO market size from digital channels is climbing 10.40% CAGR, aided by affiliate tie-ups with OTAs and airline apps that cross-sell data packs at ticket checkout.

Traditional storefronts still cater to handset financing and elderly segments, but escalating retail rents constrain expansion. Carrier sub-brand shops leverage existing footprints to funnel walk-in traffic to budget plans, squeezing standalone MVNO kiosks. As KYC APIs mature, full remote activation compliant with real-name law trims acquisition cost per user, reinforcing the dominance of digital sales funnels in the Hong Kong mobile virtual network operator (MVNO) market.

Geography Analysis

Hong Kong’s 1,106 km² footprint enables blanket 5G coverage with far fewer macro sites than regional peers, keeping wholesale network expense low for newcomers. At 6,700 inhabitants per km², cell-edge utilization rates remain high, giving MVNOs predictable throughput economics and reinforcing the profitability ceiling of the Hong Kong mobile virtual network operator (MVNO) market.

Greater Bay Area integration magnifies the scope to 86 million people without lifting physical capex inside the SAR. Unified QR-code fare systems and e-wallet interoperability across Shenzhen, Guangzhou, and Macau extend MVNO bundles beyond customs checkpoints [3]Qiu Quanlin, “MPay Can Be Used in Guangzhou Public Transport,” chinadaily.com.cn. This regional halo effect offsets the domicile population limit, letting operators pursue scale volume on a cross-jurisdiction basis while billing in familiar Hong Kong dollars.

The city’s role as an aviation and finance nexus sustains elevated roaming and corporate data demand. Business travelers banking in the Central district expect faultless swaps between Hong Kong and mainland networks, a requirement MVNOs satisfy through multi-IMSI or eSIM dynamic switching. FinTech partnerships with Octopus Cards and PingPong open revenue beyond airtime by embedding MVNO invoices inside stored-value wallets, carving extra monetization layers within the Hong Kong MVNO market.

Competitive Landscape

The Hong Kong MVNO market features moderate concentration. Aggressive sub-brands from incumbent MNOs intensify rivalry, but regulatory guarantees of open access keep barriers manageable. Digital-only entrants exploit cloud BSS and social-media customer service to outmaneuver legacy call centers on speed and cost.

Strategic pivots cluster around cross-border differentiation. CITIC’s CTExcel leverages mainland shareholder ties to retail integrated Hong Kong-Guangdong number pairs for expatriates. Emerging providers pair satellite fallback with land-based eSIM to woo maritime and hiking enthusiasts.

Technology races shape brand strength. Players that were first to offer one-click eSIM signup in Cantonese, English, and Mandarin slashed churn. AI chatbots integrated with real-name verification APIs now resolve onboarding queries in under two minutes, positioning such operators as benchmarks for digital experience inside the Hong Kong mobile virtual network operator market. Consolidation pressure will likely grow as 5G SA slicing costs and satellite airtime fees favor scale, spurring tactical alliances or acquisitions among mid-tier brands.

Hong Kong Mobile Virtual Network Operator Industry Leaders

Sun Mobile Limited

HKBN Mobile Ltd.

CTExcel (CITIC Telecom International Limited)

Birdie Mobile Limited

Club SIM (CSL Mobile Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AlipayHK and Macau’s MPay linked to Guangzhou metro, bus, and ferry payments via Alipay+ cross-border platform, broadening FinTech-connectivity bundling prospects for MVNOs.

- April 2025: HKBN posted interim profit of HKD 108 million (USD 13.8 million) after unveiling its N mobile MVNO brand, underscoring cross-selling potency in converged service models.

- March 2025: Octopus Cards and PingPong announced a partnership for localized cross-border payment solutions, offering MVNOs pre-integrated billing rails into a 98% penetration stored-value ecosystem.

Hong Kong Mobile Virtual Network Operator Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large will Hong Kong’s MVNO market be by 2030?

Forecasts put the Hong Kong MVNO market size at USD 0.51 billion in 2030 on a 5.73% CAGR path.

Which subscriber segment is expanding the fastest?

IoT connections are growing at a 14.31% CAGR as smart-port and logistics projects deploy cellular M2M lines.

What is the main growth catalyst for MVNOs in Hong Kong?

Cross-border connectivity bundles that link Hong Kong, Macau, and mainland cities drive incremental demand from travelers and expatriates.

Which network technology shows the highest forecast growth?

Satellite/NTN subscriptions are projected to advance at a 45.88% CAGR through 2030 thanks to direct-to-phone services.

How are MVNOs differentiating against MNO sub-brands?

Successful players pair eSIM-based digital onboarding with FinTech payment integration, roaming add-ons, and niche IoT SLAs.

What regulatory framework supports MVNO entry?

OFCA’s SIM-VNO license grants 5-year operating rights and mandates nondiscriminatory wholesale access, sustaining competitive parity.

Page last updated on: