Virtual Desktop Infrastructure (VDI) Endpoint Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.03 Billion |

| Market Size (2031) | USD 9.89 Billion |

| Growth Rate (2026 - 2031) | 14.48% CAGR |

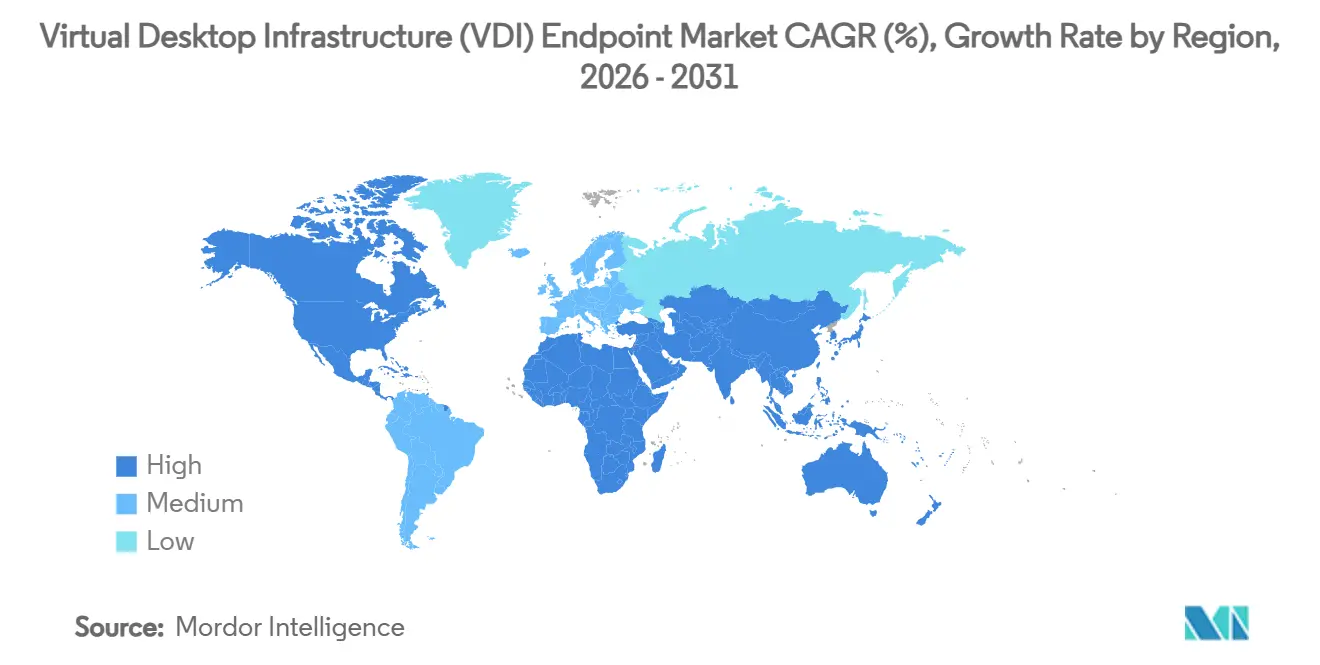

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

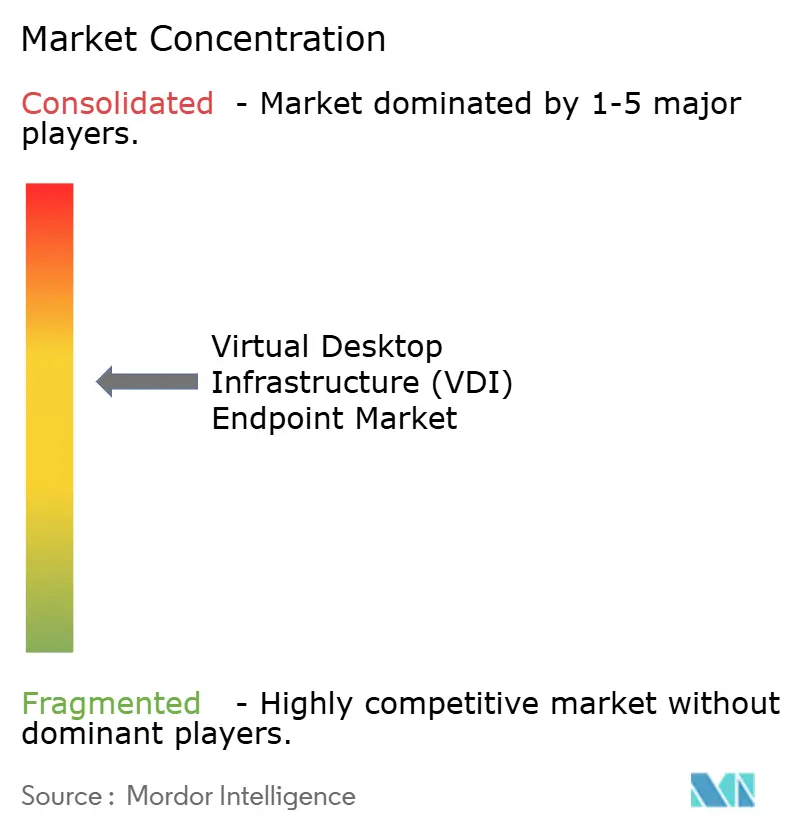

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Desktop Infrastructure (VDI) Endpoint Market Analysis by Mordor Intelligence

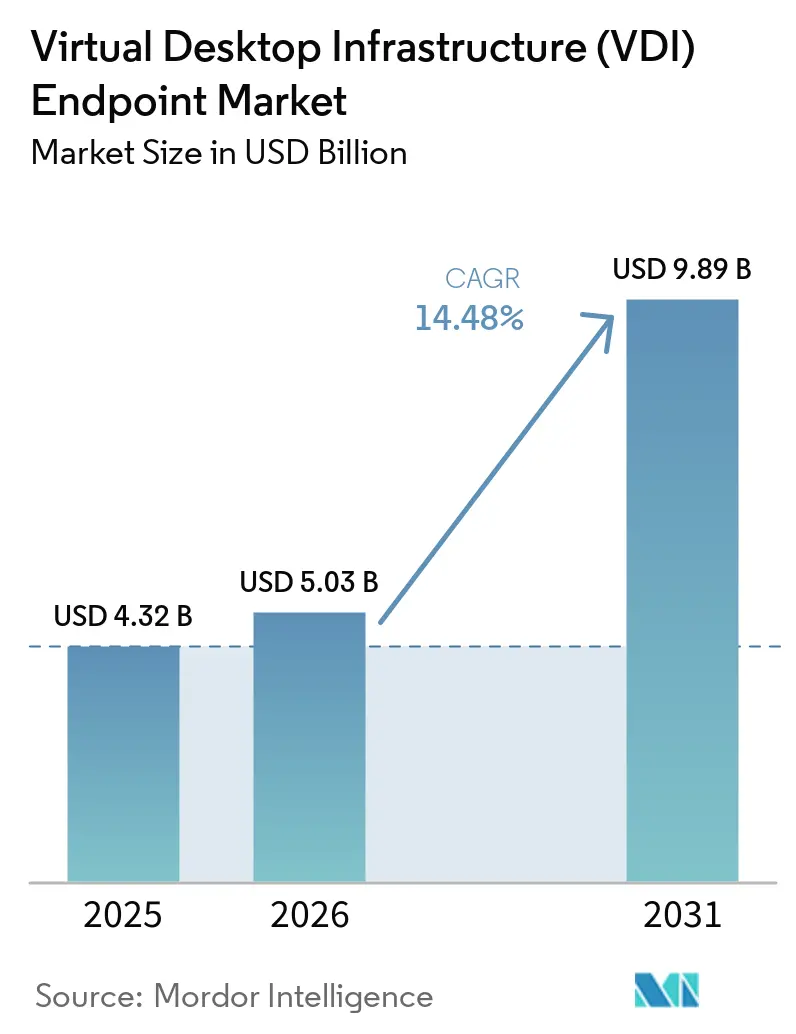

The virtual desktop infrastructure endpoint market size was valued at USD 4.32 billion in 2025 and is estimated to grow from USD 5.03 billion in 2026 to reach USD 9.89 billion by 2031, at a CAGR of 14.48% during the forecast period (2026-2031). Enterprises are standardizing on centralized desktop delivery so that remote, branch, and contract staff receive identical workspaces without shipping physical PCs. Persistent hybrid work patterns, the growing adoption of zero-trust security frameworks, and the shift from capital expenditure to subscription pricing are accelerating refresh decisions. Demand is swinging toward software-based endpoints that repurpose existing laptops, while hyperscalers bundle desktops-as-a-service with storage, artificial intelligence, and security add-ons. Regional data-localization mandates and sovereign-cloud projects are fragmenting global rollouts, prompting vendors to open new data center regions and certify endpoints for country-specific regulations. Competition spans thin-client hardware suppliers, operating system vendors, desktop broker platforms, and cloud providers, each positioning for a larger slice of the virtual desktop infrastructure endpoint market.

Key Report Takeaways

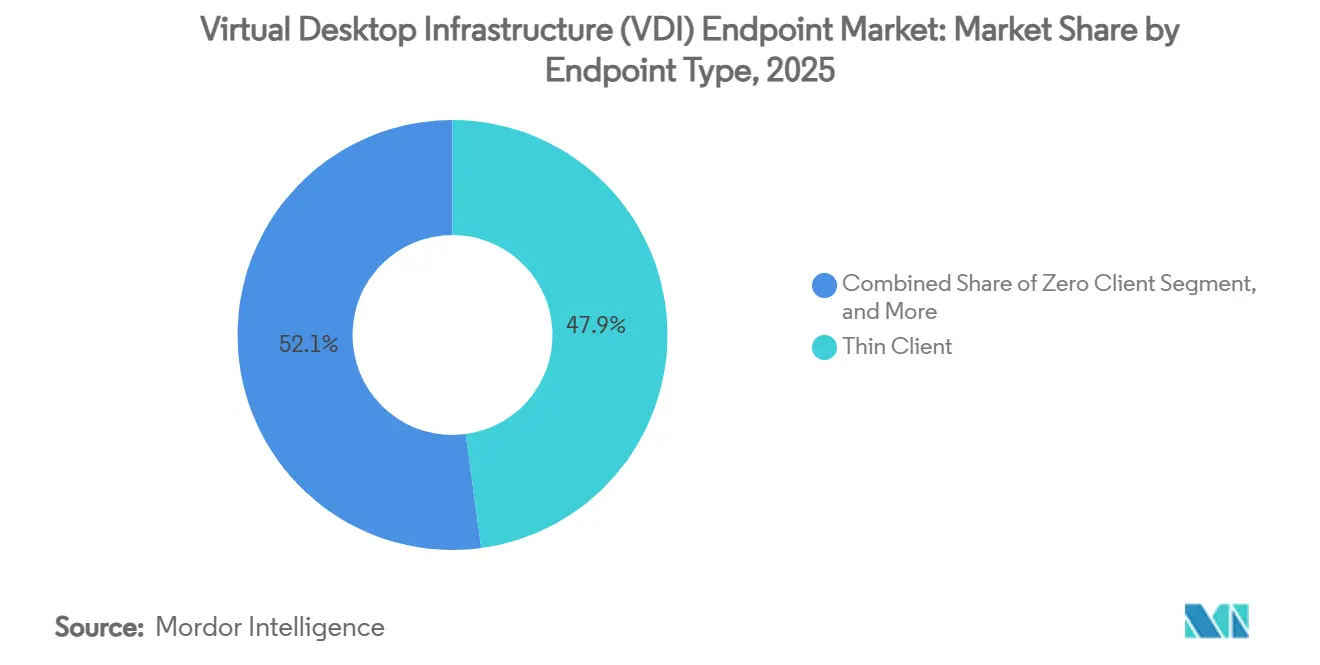

- By endpoint type, thin clients led with 47.87% of the virtual desktop infrastructure endpoint market share in 2025, while software-based endpoints are projected to grow at a 15.48% CAGR through 2031.

- By deployment mode, on-premises rollouts accounted for 58.21% of revenue in 2025, yet cloud-hosted virtual desktops are forecast to grow at a 15.08% CAGR during 2026-2031.

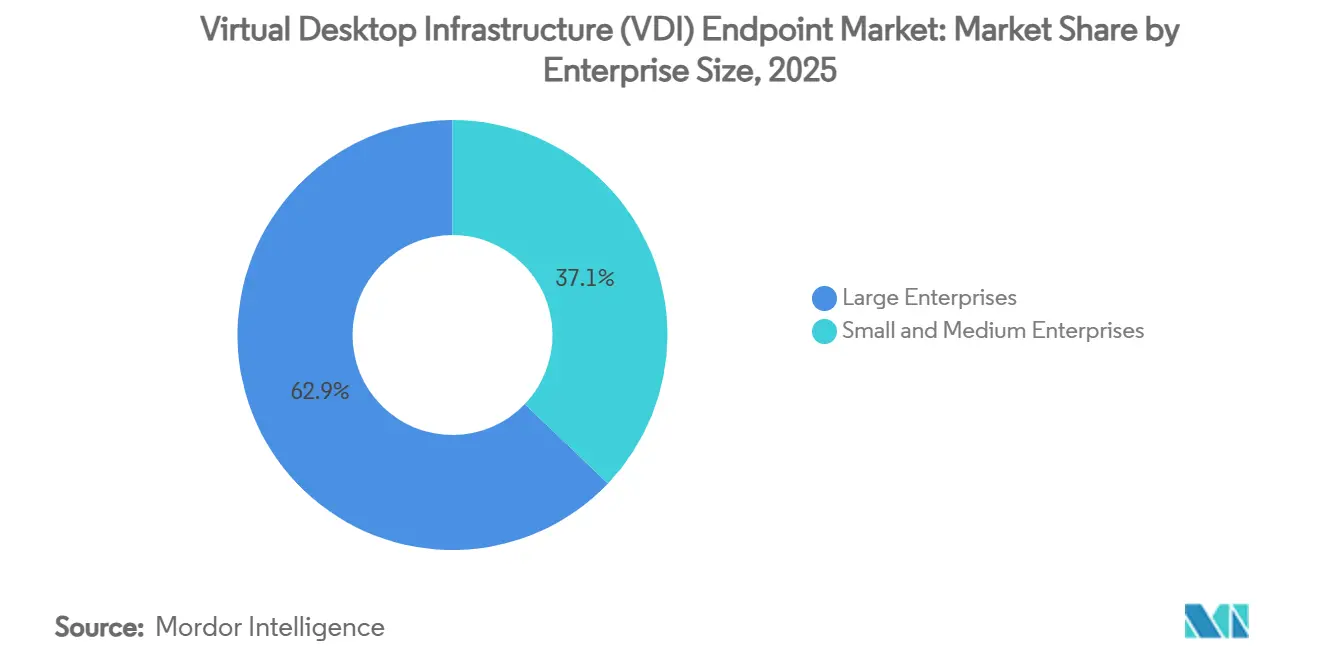

- By enterprise size, large organizations accounted for 62.87% of 2025 revenue, whereas small and medium enterprises are set to expand at a 14.88% CAGR over the same horizon.

- By industry vertical, IT and telecom generated 29.43% of 2025 demand, and healthcare is expected to post the fastest growth at a 16.08% CAGR through 2031.

- By geography, North America held 36.43% share in 2025, while Asia-Pacific is predicted to record a 15.26% CAGR, the highest among all regions during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Virtual Desktop Infrastructure (VDI) Endpoint Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Hybrid Work Environments | +2.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Demand for Secure Endpoints in Zero Trust Architectures | +2.5% | Global, led by North America, Europe and Asia-Pacific | Short term (≤ 2 years) |

| Cost Savings From Centralised Desktop Management | +2.2% | Global, strongest in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Mainstream Adoption of GPU-Enabled Virtual Desktops | +1.9% | North America, Europe and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Government Mandates on Data Localisation | +1.6% | Asia-Pacific, Middle East and Europe | Short term (≤ 2 years) |

| Rise of ARM-Based Thin Clients for Energy Efficiency | +1.3% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Hybrid Work Environments

Hybrid schedules have become an entrenched operating norm, compelling information-technology teams to deliver identical, secure desktops to employees working alternately from home, branch offices, and third-party locations. Virtual desktops eliminate the logistics and security risks of shipping PCs, as applications, data, and policies remain in the data center. Microsoft introduced ephemeral operating-system disks for Azure Virtual Desktop in October 2025, allowing session hosts to reset to a clean baseline after each logoff, reducing persistent malware risk and simplifying image management for organizations.[1]Microsoft, “Azure Virtual Desktop Documentation,” microsoft.com Platform enhancements, such as ephemeral operating-system disks, let administrators reset machines to a pristine state at log-off, reducing malware persistence and simplifying image maintenance. Collaboration performance has also improved; optimized codecs offload media to endpoints, enabling videoconferencing to function smoothly even over residential broadband. Contact centers, field service teams, and consultancies that rotate large numbers of contractors through shared pools cite faster onboarding and lower help-desk volumes as direct benefits of the hybrid-work model.

Demand for Secure Endpoints in Zero Trust Architectures

Zero-trust strategies require continuous verification of user identity and device posture, making local storage a liability. By shifting the entire desktop to a controlled environment, virtual desktop infrastructure ensures that sensitive information remains within the corporate perimeter and that every action is logged centrally. Integration between connection brokers and identity-and-access-management services now allows contextual policies that block sessions from non-compliant devices or risky networks in real time. Financial services firms and public agencies are early adopters because virtual desktops provide tamper-proof audit trails that meet stringent regulatory requirements. As regulators in healthcare, energy, and critical infrastructure specify zero-trust architectures, the virtual desktop infrastructure endpoint market gains from mandated upgrades.

Cost Savings From Centralised Desktop Management

Hosting desktops in the datacenter collapses operating-system patching, software distribution, and help-desk support into a golden-image workflow, reducing repetitive tasks across thousands of endpoints. Repurposed PCs or purpose-built thin clients extend hardware lifecycles by offloading processing to servers, reducing capital requirements and e-waste. Modern management consoles combine device discovery, policy assignment, and firmware updates in a single pane of glass that small teams can run without specialized virtualization skills. Energy consumption falls sharply as solid-state thin clients draw a fraction of the wattage of legacy towers, and datacenter consolidation generates further savings in cooling and floor space. Together, these levers form a compelling return-on-investment narrative for chief financial officers weighing virtual desktop projects.

Mainstream Adoption of GPU-Enabled Virtual Desktops

Advances in virtual graphics processing now partition a single high-end card into multiple secure slices, making it economical to virtualize workloads such as computer-aided design, generative artificial intelligence inference, and real-time video editing. Industrial manufacturers deploy virtual workstations on production floors to protect intellectual property, while media agencies spin up high-performance desktops on demand for rendering peaks. Cloud desktop-as-a-service bundles include preconfigured GPU instances, which allow mid-size studios and engineering firms to experiment without purchasing expensive cards. The expanded use cases enhance the overall value proposition of the virtual desktop infrastructure endpoint market, extending its relevance beyond traditional knowledge-worker segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Up-Front Infrastructure Costs | -1.8% | Global, acute in small and medium enterprises | Short term (≤ 2 years) |

| Bandwidth Limitations in Emerging Economies | -1.5% | Africa, South Asia and parts of South America | Medium term (2-4 years) |

| Limited Peripheral Compatibility in Zero Clients | -0.9% | Global, specialised industries | Long term (≥ 4 years) |

| Skills Gap in VDI Endpoint Management | -0.7% | Asia-Pacific, Middle East and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Up-Front Infrastructure Costs

Building an on-premises virtual desktop environment requires servers, storage arrays, networking gear, and hypervisor licenses before the first user signs in, a hurdle that weighs heavily on cost-sensitive buyers. A typical 500-seat VDI cluster requires USD 200,000 to USD 400,000 in initial hardware and software costs, plus ongoing costs for hypervisor support, storage expansion, and datacenter power and cooling.[2]Nerdio, “VDI Cost Analysis,” nerdio.com Although cloud subscriptions shift spending to operating expenditure, monthly fees can outpace amortized on-premises costs when organizations have stable, long-tenure workforces. Predicting variable compute, storage, and bandwidth consumption in public clouds remains complex, and mis-sizing often triggers unplanned bills that erode projected savings. Smaller businesses, therefore, hesitate to move past proof-of-concept pilots until service providers package virtual desktops as fixed-price bundles. Financing programs, pay-per-use data center appliances, and managed service offerings aim to smooth the capital hump, yet adoption in emerging markets still lags.

Bandwidth Limitations in Emerging Economies

User experience deteriorates when last-mile networks cannot deliver the throughput and latency required by remote display protocols. In many rural districts, peak download speeds remain below 10 Mbps, insufficient for high-definition multitasking on dual monitors. Even in metro areas, congested shared links cause jitter that leads to mouse lag, video stutter, and dropped calls. Codec optimizations, protocol adaptivity, and edge gateways mitigate these effects but cannot fully overcome poor connectivity for graphics-heavy workloads. Governments and telcos are expanding fiber backbones and 5G rollouts, yet timelines stretch over years, keeping virtual desktop infrastructure endpoint market growth below its potential in affected regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Endpoint Type: Software Conversion Surges as Enterprises Stretch Device Lifecycles

Software-based endpoints are forecast to grow at a 15.48% CAGR between 2026 and 2031, reinforcing the narrative that organizations prefer converting existing laptops and desktops rather than purchasing new hardware. In 2025, thin clients still commanded 47.87% of the virtual desktop infrastructure endpoint market share, underpinned by call centers, healthcare nursing stations, and factory kiosks that value fanless designs and extended temperature tolerance. Enterprises deploying conversion utilities extend a Windows or macOS laptop’s usable life by up to 7 years, sidestepping procurement queues and reducing electronic waste. Growing familiarity with Linux-based endpoint operating systems has lowered user-acceptance barriers, while centralized patching allays security concerns. Zero clients remain niche, favored by defense agencies that forbid local operating systems, though limited peripheral support constrains growth. Mobile thin-client laptops and rugged tablets are carving out roles for field inspectors and emergency responders who need VDI access away from fixed desks. such as 10ZiG's 7500qTAA series, address field technicians and traveling executives who require VDI access without tethering to a desk, combining portability with Trade Agreements Act compliance for United States federal procurement.[3]10ZiG Technology, “Seamless Printing for VDI and DaaS with ThinPrint & 10ZiG,” 10zig.com The virtual desktop infrastructure endpoint market size for software-converted devices is expected to double over the forecast period as organizations tighten hardware budgets and sustainability mandates take hold.

Thin-client vendors are responding with lighter footprints, improved multimedia off-load and integrated browser containers that blur the line between hardware and software solutions. Automatic printer redirection, webcam passthrough, and multi-factor authentication modules now ship as standard, reducing the functional gap between dedicated appliances and repurposed PCs.Endpoint management consoles detect, enroll,l and push updates to both categories, giving administrators a homogeneous fleet view. These advances reinforce buyer confidence that a mixed hardware-software strategy will not fracture support processes, further expanding the addressable pool for the virtual desktop infrastructure endpoint market.

By Deployment Mode: Cloud Desktops Close the Gap With On-Premises Installations

On-premises deployments accounted for 58.21% of revenue in 2025, primarily because financial services, manufacturing execution, and latency-sensitive industrial control workloads remain tied to local data centers. However, cloud-hosted desktops are projected to expand at a 15.08% CAGR through 2031, narrowing the split as consumption-based pricing appeals to businesses lacking internal virtualization talent. Hyperscalers bundle identity management, file services, and security analytics, letting small teams spin up pilots in hours. The virtual desktop infrastructure endpoint market for cloud subscriptions is growing fastest in retail chains, design studios, and professional services firms that experience seasonal or project-based peaks.

Hybrid architectures combine local clusters for baseline steady-state loads with cloud bursting for high-demand periods, optimizing both cost and compliance. Unified control planes orchestrate image lifecycle, user assignments, and telemetry across sites, masking infrastructure heterogeneity. Legal mandates requiring data to remain within national borders are steering some organizations toward multi-cloud topologies, where North American employees run virtual desktops in domestic regions while colleagues in Europe or Asia connect to sovereign instances. Such fragmentation drives demand for policy engines that abstract from provider-specific details, further fueling innovation in the virtual desktop infrastructure endpoint market.

By Enterprise Size: Managed Services Propel Small and Medium Enterprise Uptake

Large enterprises held 62.87% of revenue share in 2025, thanks to multi-thousand-seat legacy rollouts and complex desktop footprints. Yet small and medium enterprises are on track to post a 14.88% CAGR to 2031, outpacing their bigger peers. Turnkey desktop-as-a-service platforms bundle networking, security, and support into per-user subscriptions, eliminating the need for in-house hypervisor or storage specialists. These offerings resonate with startups, creative agencies, and regional manufacturers that would otherwise struggle to recruit virtualization engineers. Free or low-cost endpoint-management tools further lower barriers, enabling a single administrator to remotely monitor hundreds of devices.

Scalability on demand is another attraction; a retailer can add virtual check-out stations during holiday peaks and release capacity in January, paying only for the burst window. Conversely, large enterprises benefit from contracting leverage, volume licenses, and bespoke integrations with legacy authentication and enterprise-resource-planning systems. They also adopt virtual desktop infrastructure for mergers and acquisitions, enabling acquired employees to access corporate applications within hours. Both cohorts, therefore, remain vital to the virtual desktop infrastructure endpoint market, but growth momentum rests firmly with managed-service-driven small and medium enterprises.

By Industry Vertical: Healthcare Outpaces All Sectors on Telehealth Expansion

In 2025, IT and telecom accounted for 29.43% of spending, reflecting early adoption of network operations centers and software development environments. Looking forward, healthcare is forecast to grow at a 16.08% CAGR, the fastest among all verticals. Telehealth platforms, electronic medical record integration, and strict privacy regulations encourage hospitals to centralize desktops so that protected health information never resides on clinician laptops. Virtual desktops also simplify application updates across hundreds of nursing stations, reducing downtime for mission-critical radiology and pharmacy systems. The virtual desktop infrastructure endpoint market size for healthcare endpoints is set to surpass earlier estimates as reimbursements for remote consultations become permanent.

Banking, financial services, and insurance institutions deploy high-performance virtual workstations for options pricing, anti-money laundering analytics, and secure customer service. Government agencies leverage desktop virtualization to fulfill continuity-of-operations mandates and to support geographically dispersed workforces without compromising citizen data. Educational institutions convert aging lab PCs into thin clients, stretching public budgets and giving students the same desktop experience whether on campus or at home. Manufacturing and retail sectors roll out kiosk-mode endpoints on shop floors and in stores to protect intellectual property and payment data, underscoring that almost every industry now contributes to the expanding virtual desktop infrastructure endpoint market.

Geography Analysis

Asia-Pacific is projected to register the highest regional CAGR at 15.26% from 2026 to 2031, fueled by Digital India, China’s Cybersecurity Law, and Gulf Cooperation Council Vision 2030 initiatives that channel government budgets into sovereign clouds and zero-trust architectures.[4]Aivensoft, “Vision 2030 Digital Transformation,” aivensoft.com New local cloud regions, including Microsoft’s Saudi Arabia East facility slated for late 2026, will let enterprises run latency-sensitive workloads domestically, spurring endpoint upgrades across energy, public sector, and financial services verticals. Local thin-client assemblers and software resellers benefit from buy-local clauses embedded in public tenders, adding competitive dynamism to the virtual desktop infrastructure endpoint market.

North America, which captured 36.43% of 2025 revenue, maintains a technology leadership position thanks to dense hyperscaler footprints, mature channel partners, and early cross-industry adoption. Financial houses in New York deploy GPU-enabled virtual desktops to model market scenarios, while federal agencies mandate Trade Agreements Act-compliant endpoints for secure facilities. Adoption growth is steadier than spectacular, yet continual refresh cycles keep absolute spending high.

Europe’s General Data Protection Regulation encourages hybrid and on-premises deployments to avoid cross-border data transfers, though accelerated cloud region launches in Germany, France, and the Nordics are nudging enterprises toward hosted desktops. Meanwhile, South America and Africa face slower uptake due to under-provisioned connectivity and higher import tariffs on hardware, but targeted national broadband plans and digital government programs are planting the seeds for future expansion in the virtual desktop infrastructure endpoint market.

Competitive Landscape

Competitive intensity is moderate, with hardware, software, and cloud ecosystems overlapping. Traditional thin-client leaders are diversifying into operating-system licensing and management platforms so customers can convert existing PCs rather than buy new boxes. The 2025 acquisition that merged two leading endpoint operating system suppliers exemplifies this pivot, shifting revenue models from one-time hardware margins to recurring software subscriptions and managed services.

Hyperscale providers bundle desktop-as-a-service with storage, identity, and analytics, leveraging deep capital pools to expand into local markets and undercut smaller hosting firms. Desktop-broker software vendors counter by partnering with cloud providers, offering proprietary policy engines atop infrastructure-as-a-service foundations so enterprises can keep familiar management consoles during migration. Feature differentiation now centers on protocol efficiency, GPU scheduling, automated patch orchestration, and compliance certifications that shorten procurement cycles in regulated industries.

Niche opportunities persist in frontline retail, ruggedized manufacturing, and defense, where zero-client appliances, containerized app streaming, and air-gapped architectures solve specialized constraints. Open-source broker projects and Linux-first distributions appeal to cost-sensitive education and municipal markets, providing a low-license-fee entry point. This mosaic of strategies ensures that no single player exceeds a dominant threshold, sustaining innovation across the virtual desktop infrastructure endpoint market.

Virtual Desktop Infrastructure (VDI) Endpoint Industry Leaders

HP Inc.

Dell Technologies, Inc.

Lenovo Group Limited

IGEL Technology GmbH

NComputing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: 10ZiG Technology released 10ZiG Manager v5.5, introducing intelligent client-check-in queuing, pagination for large inventories, and reduced resource consumption to manage tens of thousands of thin clients at no license cost.

- March 2026: Microsoft confirmed its Saudi Arabia East Azure region will open in Q4 2026 with three availability zones, supporting local Azure Virtual Desktop workloads that meet data-residency rules.

- November 2025: Microsoft enabled hybrid Azure Virtual Desktop support on Azure Stack HCI, allowing on-premises session hosts managed through the Azure portal.

- October 2025: Microsoft added ephemeral operating-system disks to Azure Virtual Desktop to reset session hosts on log-off, cutting persistent-malware risk and storage spend.

Global Virtual Desktop Infrastructure (VDI) Endpoint Market Report Scope

The Virtual Desktop Infrastructure (VDI) Endpoint Market refers to the ecosystem of hardware devices and software solutions used by end users to securely access virtual desktops hosted on centralized servers or in the cloud. These endpoints act as the interface between users and virtualized computing resources, enabling remote access to applications, data, and desktop environments without requiring full local processing capabilities.

The Virtual Desktop Infrastructure Endpoint Market Report is Segmented by Endpoint Type (Thin Client, Zero Client, Smart Device/PC, Mobile Thin Client, and Software-based Endpoint), Deployment Mode (On-premises, Cloud-hosted, and Hybrid), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare, Government, Education, Manufacturing, Retail, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Thin Client |

| Zero Client |

| Smart Device/PC |

| Mobile Thin Client |

| Software-based Endpoint |

| On-premises |

| Cloud-hosted |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare |

| Government |

| Education |

| Manufacturing |

| Retail |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Endpoint Type | Thin Client | ||

| Zero Client | |||

| Smart Device/PC | |||

| Mobile Thin Client | |||

| Software-based Endpoint | |||

| By Deployment-Mode | On-premises | ||

| Cloud-hosted | |||

| Hybrid | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Industry Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Government | |||

| Education | |||

| Manufacturing | |||

| Retail | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the virtual desktop infrastructure endpoint space by 2031?

It is forecast to reach USD 9.89 billion, rising from USD 5.03 billion in 2026 at a 14.48% CAGR.

Which endpoint type is expected to grow the fastest through 2031?

Software-based endpoints are set to post the highest growth, advancing at a 15.48% CAGR.

How does zero-trust security influence desktop-virtualization decisions?

Zero-trust frameworks favor virtual desktops because data stays in the datacenter, sessions are continuously authenticated and every action is logged for compliance.

Why are small and medium enterprises increasingly choosing managed desktop services?

Managed service bundles remove the need for in-house virtualization skills, offer flat per-user pricing and allow quick scaling during business peaks.

Which region is predicted to record the strongest expansion over 2026-2031?

Asia-Pacific is projected to grow at a 15.26% CAGR, driven by sovereign-cloud projects and digital-government programs.

How do GPU-enabled virtual desktops change user workloads?

Multi-instance GPU technology lets one card serve several high-performance desktops, bringing design, simulation and generative artificial intelligence tasks into virtual environments without costly workstations.

Page last updated on: