Vietnam Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

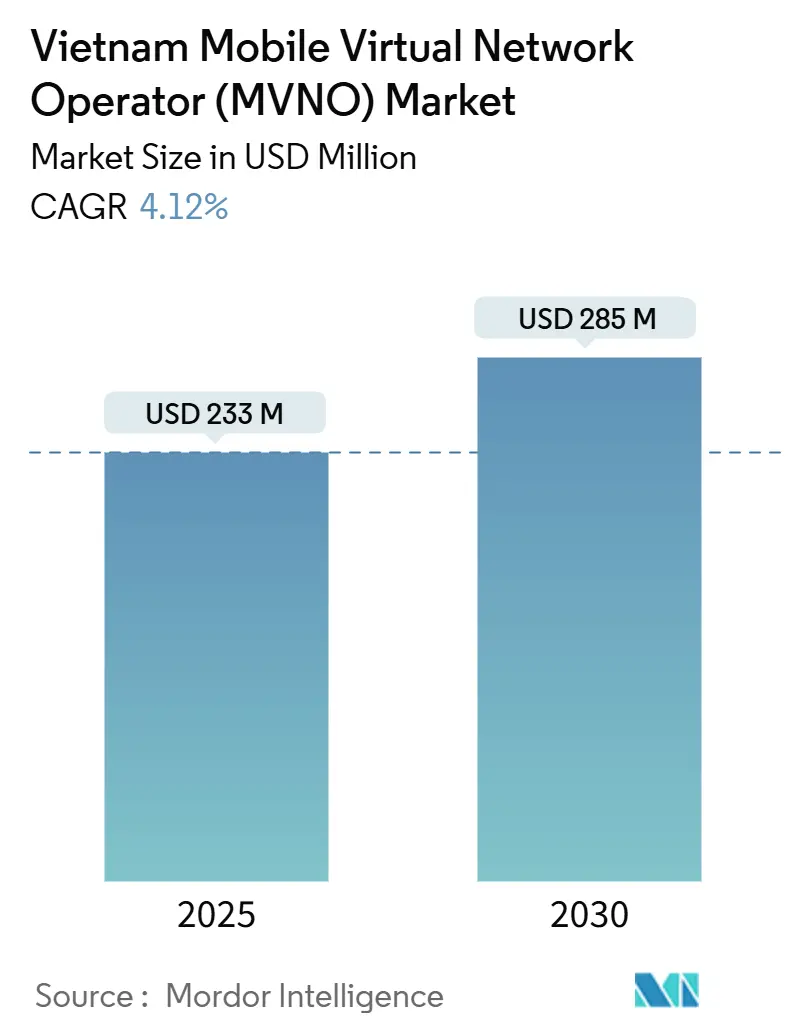

| Market Size (2025) | USD 233 Million |

| Market Size (2030) | USD 285 Million |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Vietnam Mobile Virtual Network Operator Market size is estimated at USD 233 million in 2025, and is expected to reach USD 285 million by 2030, at a CAGR of 4.12% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 3.95 million subscribers in 2025 to 4.70 million subscribers by 2030, at a CAGR of 3.56% during the forecast period (2025-2030).

This steady expansion coincides with the enforcement of the New Law on Telecommunications (LOT 2023), which compels dominant Mobile Network Operators (MNOs) to lease wholesale capacity to virtual operators and underpins a regulatory pivot toward infrastructure sharing. Rising demand for affordable data bundles, the rollout of 5G coverage beyond major cities, and an accelerating shift to embedded-SIM (eSIM) devices broaden addressable customer segments while lowering distribution costs for entrants. Mobile-number-portability (MNP) regulations effective August 2025 reduce switching friction, supporting subscriber migration to new brands and intensifying pricing competition. In parallel, digital-only banking alliances—such as VPBank-MobiFone—are enabling MVNOs to bundle financial services with connectivity, generating non-traditional revenue streams that mitigate thin voice and data margins.

Key Report Takeaways

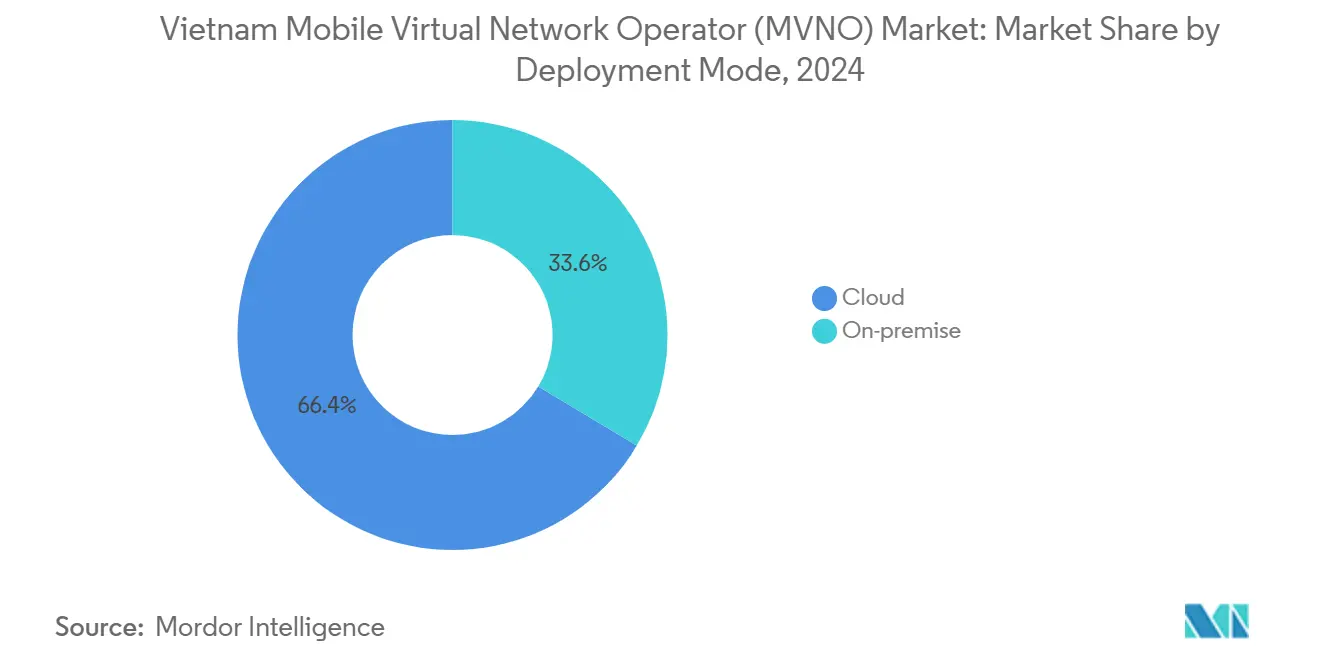

- By deployment model, cloud infrastructure captured 66.40% of the Vietnam MVNO market share in 2024; on-premise solutions are forecast to expand at a 9.54% CAGR through 2030.

- By operational mode, reseller and light MVNOs held 64.35% of the Vietnam MVNO market in 2024, while full MVNO configurations are projected to grow at 15.48% CAGR to 2030.

- By subscriber type, consumer lines accounted for 87.89% of the Vietnam MVNO market size in 2024; IoT-specific connections are advancing at a 30.26% CAGR through 2030.

- By application, discount plans led with 49.12% revenue share in 2024; cellular M2M solutions are set to climb 28.36% annually to 2030.

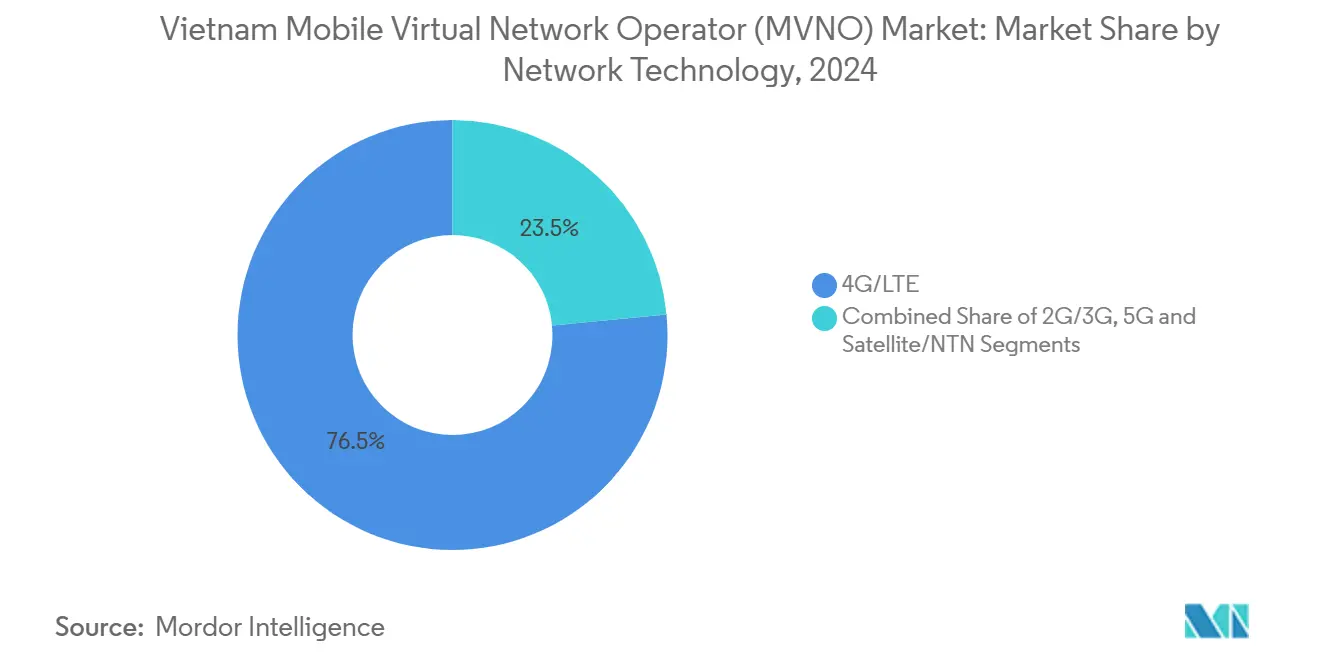

- By network technology, 4G/LTE dominated at 76.52% of the Vietnam MVNO market size in 2024, whereas 5G subscriptions exhibit a 32.50% growth outlook.

- By distribution channel, online and digital-only platforms commanded 52.64% share of the Vietnam MVNO market in 2024 and maintain a 7.95% CAGR forecast.

Vietnam Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| eSIM-ready smartphone proliferation | +1.2% | Urban clusters (Ho Chi Minh City, Hanoi) | Medium term (2-4 years) |

| Digital-only banking & fintech alliances | +0.8% | Nationwide, rural expansion focus | Long term (≥ 4 years) |

| Government target: MVNOs at 5% mobile base | +0.7% | National | Medium term (2-4 years) |

| Mobile-number-portability implementation | +0.6% | National | Short term (≤ 2 years) |

| Low-ARPU rural voice/data demand | +0.5% | Mountainous and agricultural provinces | Long term (≥ 4 years) |

| Cross-border tourist SIM demand | +0.4% | Frontier provinces, tourism hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of eSIM-ready smartphones

Embedded-SIM compatibility is pushing Vietnam MVNO market penetration by relieving operators of physical card logistics and distribution costs. Brands such as Viettel and Vinaphone now activate eSIM profiles across most flagship devices released since 2017, while tourist-focused providers enable instant data bundles that range from USD 8 to USD 40 via QR-code scanning. [1]Authentik Travel, “How to Use eSIM in Vietnam,” authentiktravel.com Reduced onboarding friction encourages short-stay visitors and domestic urban users to trial virtual brands without retail store visits, giving agile MVNOs a cost advantage over infrastructure-heavy peers.

Surge in digital-only banking and fintech partnerships

Fintech tie-ups convert MVNO subscriber bases into broader digital ecosystems. VPBank and MobiFone’s 2025 agreement established mobile point-of-sale solutions for public services and agent banking outlets in remote communes, supporting cash-light rural commerce while elevating average revenue per user.[2]VietnamPlus News Agency, “VPBank, MobiFone to Expand Digital Ecosystem,” vietnamplus.vn Regulatory extensions of the Mobile-Money pilot until December 2025 allow small-value payments over telecom accounts, opening higher-margin payment flows that offset low prepaid tariffs.

Government push to lift MVNO share to 5% by 2028

LOT 2023 obligates Viettel, VNPT, and MobiFone—designated dominant in July 2025—to publish reference offers and provide non-discriminatory wholesale terms, unlocking nationwide infrastructure for new entrants. [3]Vietnam Government Portal, “Guidelines for Mobile Number Portability Implementation,” baochinhphu.vnClear legal definitions of reseller, service, and full MVNO modes cut licensing uncertainty and encourage diversified go-to-market approaches, fostering competition beyond the traditional three-operator structure.

Mobile-number-portability regulation

MNP rules enacted in August 2025 require incumbents to finalize port-out requests within 24 hours once billing disputes are settled, enabling subscribers to retain numbers while changing providers. The policy levels the competitive field by permitting MVNOs to target users dissatisfied with network quality or tariff structures, accelerating brand switching and pressuring legacy pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wholesale rate floors imposed by MNOs | –0.9% | National | Long term (≥ 4 years) |

| Slow 5G spectrum allocation | –0.6% | Urban clusters | Medium term (2-4 years) |

| Fragmented MVNE ecosystem | –0.5% | National | Medium term (2-4 years) |

| Limited fixed-mobile convergence offers | –0.4% | Enterprise-heavy corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wholesale rate floor set by major MNOs

Despite legal obligations to lease capacity, Viettel, VNPT, and MobiFone retain bargaining power that allows premium wholesale tariffs, compressing MVNO margins and discouraging deep discount strategies. Experience in the European Union shows that explicit cost-based benchmarks may be necessary once MVNO penetration approaches 5%, yet Vietnam’s framework still relies on commercial negotiation, prolonging price rigidity.

Slow 5G spectrum allocation timeline

Only three auctions have been completed, with Viettel acquiring 700 MHz and MobiFone the 3.8 GHz band by mid-2025. Limited mid-band capacity inflates leasing fees and curtails service differentiation for MVNOs aspiring to target enterprise IoT or ultra-high-speed consumer tiers. The Ministry of Information and Communications has mandated 20,000 additional 5G base stations by end-2025, but spectrum scarcity may delay nationwide premium wholesale products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Enables Asset-Light Expansion

Cloud-hosted platforms controlled 66.40% of the Vietnam MVNO market in 2024. The architecture reduces capital intensity, accelerates service launches, and aligns with the government’s Digital Infrastructure Plan, which promotes green data centers and near-universal 5G coverage by 2030. Viettel’s ongoing USD 1 billion data-center build in Ha Noi will supply wholesale compute and storage for virtual operators, letting full MVNOs orchestrate policy control, billing, and analytics without laying fiber or towers. On-premise options hold niche appeal for government and finance clients that mandate data-residency; however, incremental security features now available in Vietnamese cloud zones are quickly narrowing that gap.

The asset-light nature of cloud deployment lowers break-even subscriber thresholds and shortens go-to-market cycles, particularly valuable in a landscape where the Vietnam MVNO market remains far below saturation. As wholesale 5G APIs become accessible, cloud-native MVNOs can slice bandwidth by latency or throughput and price micro-segments dynamically. With a forecast 9.54% CAGR through 2030, cloud will gradually raise its share, but legacy on-premise estates will still anchor mission-critical public-safety and financial messaging traffic.

By Operational Mode: Full MVNOs Capture Value Chain Control

In 2024, reseller and light configurations together represented 64.35% of active brands, yet full MVNO operations are projected to expand at 15.48% CAGR. The Vietnam MVNO market size for full-service players is still modest, but end-to-end ownership of core network elements enables bespoke pricing, network selection, and self-defined quality-of-service tiers. Regulatory clarity from LOT 2023 now details interconnection, numbering, and lawful-intercept rules, cutting red tape for ambitious entrants.

As wholesale 5G and edge-compute mature, new full MVNOs plan to wrap connectivity into SaaS portfolios for manufacturing, logistics, and tele-health. The capability to steer traffic among multiple host networks also cushions against localized outages. Still, complexity and higher initial costs mean simpler reseller models will persist in discount voice niches, leaving a bifurcated competitive field where operational sophistication matches customer value curves.

By Subscriber Type: IoT Upswings Complement Consumer Base

Consumers dominate with 87.89% of SIMs, underpinning a prepaid culture driven by competitive price-per-gigabyte bundles. Yet the Vietnam MVNO market share of IoT devices is projected to rise sharply, sustained by a 30.26% CAGR as factories adopt Industry 4.0 standards and cities deploy smart-lighting, traffic, and metering systems. Enterprises—including logistics and field services—prioritize consistent latency plus centralized fleet management dashboards, leading several MVNO hopefuls to partner with cloud hyperscalers for bundled analytics.

Regulatory encouragement of e-government services also turbocharges machine-type subscriptions for CCTV backhaul and public-asset monitoring. Although ARPU per IoT line remains below USD 1, volume scalability and churn-resilient contracts enhance predictability. Cross-selling between consumer family plans and small business IoT kits provides another growth lever as smartphone penetration nears saturation.

By Application: M2M Momentum Challenges Discount Supremacy

Discount prepaid bundles held 49.12% revenue share in 2024 due to persistent price sensitivity among students and gig-economy workers. However, cellular M2M lines—tracking everything from cold-chain containers to delivery bikes—are racing ahead with a 28.36% annual uptick, helping providers diversify away from voice dependence. Vietnam’s program to switch off 2G by September 2026 will force several million legacy devices to migrate upward, fueling fresh demand for low-data IoT plans compatible with 4G NB-IoT bearers.

Business applications in healthcare and education are also emerging, aided by 5G mini-cores hosted inside hospitals or campuses. While margins on discount SIMs face deflation, specialized M2M contracts often span three to five years, adding resilience to cash flows and supporting higher EBITDA multiples for MVNOs with vertical know-how.

By Network Technology: 5G and Satellite Complement 4G Footprint

4G/LTE still accounts for 76.52% of active lines, anchoring nationwide coverage and affordable device ecosystems. Yet the Vietnam MVNO market size for 5G is expanding at 32.50% CAGR, driven by mandated deployment of 20,000 new base stations by December 2025. Ultra-reliable low-latency services target smart-factory and AR/VR entertainment use cases, segments in which MVNOs can differentiate via quality-tiered plans.

Separately, SpaceX’s Starlink pilot, authorized for up to 600,000 Vietnamese users across five years, introduces non-terrestrial networks into mainstream connectivity and opens hybrid packages blending satellite backhaul with terrestrial roaming. Such arrangements can reach fishing fleets and mountain communes outside 4G signal, a strategic niche where early-mover MVNOs may secure loyal subscriber bases.

By Distribution Channel: Digital-First Wins Scale, Stores Retain Trust

Online activation represented 52.64% of new connections in 2024, aided by omnipresent e-commerce habits cultivated during the pandemic. The Vietnam MVNO market is especially suited to app-based onboarding as eKYC regulations allow remote identity verification via National ID chips. eSIM QR codes delivered through social-commerce channels remove the last physical hurdle, letting MVNOs operate with near-zero retail estates.

Nevertheless, rural subscribers and elders continue to value face-to-face assistance for top-ups and handset troubleshooting. Strategic partnerships with convenience chains provide cost-efficient touchpoints, while flagship sub-brand kiosks inside electronics retailers showcase devices and bundled content, harmonizing trust with digital convenience. The hybrid blueprint is expected to sustain a 7.95% CAGR for digital channels even as overall penetration rises.

Geography Analysis

Urban municipalities hold the densest traffic and premium ARPU, with Da Nang recording median mobile broadband speeds of 272.97 Mbps in April 2025, surpassing the national mean of 77.19 Mbps. Hanoi and Ho Chi Minh City together concentrate more than 45% of the nation’s 5G base stations, providing fertile ground for video-streaming and cloud-gaming-centric MVNO propositions. Suburban districts surrounding these hubs have also benefited from tower-sharing mandates, lowering expansion capex for virtual entrants.

In contrast, only 58% of Vietnam’s landmass enjoys cellular coverage even though population coverage stands at 99.8%, leaving swathes of mountainous north-central provinces underserved. The planned 2G sunset will nudge roughly 15 million rural feature-phone users toward affordable 4G bundles, a transition MVNOs can shepherd via refurbished handset campaigns and community agents. Government funding streams tied to the Universal Service Fund subsidize tower builds in border and island districts, extending wholesale footprints for voice and narrowband IoT.

Cross-border tourist flows from China, Laos, and Cambodia are rebounding, creating demand for short-term roaming solutions that avoid punitive out-of-bundle charges. MVNOs that pre-procure multi-IMSI profiles and offer Chinese-language chat support are well positioned to capture spending spikes around national holidays. Meanwhile, satellite-terrestrial hybrids present a compelling proposition for shipping lanes in the South China Sea, where connectivity blackspots have persisted despite coastal 4G buildouts. Collectively, these geographic dynamics indicate the Vietnam MVNO market will progress from a metro-centric phase to a truly nationwide footprint by the decade’s end.

Competitive Landscape

Vietnam’s mobile arena remains moderately concentrated: the top three host networks jointly served 96 million SIMs in 2024, yet the regulatory shift toward compulsory leasing is dismantling traditional entry barriers. Virtual brands currently hold below 1% of connections but are multiplying, spurred by clarified licensing tiers. Digital service diversification dominates strategy; MobiFone reported a 312% jump in cloud revenues and 1,050% surge in video-conferencing subscriptions during 2024, signalling pivot away from pure airtime.

Partnership plays are equally visible. VPBank’s co-branded SIM offers free data for mobile-banking usage, encouraging customer stickiness while enriching transactional datasets. Vinaphone cooperates with Ericsson on 5G private-network proofs-of-concept inside industrial parks, aiming to anchor export manufacturing clients to end-to-end solutions. Viettel, meanwhile, inked a USD 95 million memorandum with Korea’s KT Corp to build Vietnamese-language AI assistants, embedding telco APIs directly into local super-apps.

Regulatory compliance introduces both cost and advantage. Decree 13/2023 on personal-data protection applies equally to all network service providers; MVNOs automating consent management via cloud security partners can turn compliance into a selling point for enterprise accounts wary of reputational risk. Viewed holistically, the Vietnam MVNO market is shifting from voice reselling toward multi-service orchestration, with success hinging on ecosystem alliances, network-quality negotiation skills, and differentiated software layers rather than spectrum ownership.

Vietnam Mobile Virtual Network Operator (MVNO) Industry Leaders

Indochina Telecom

Mobicast

Asim Telecom

FPT Telecom

VNSKY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Viettel began constructing the An Khánh Data Center and a separate RandD campus valued at USD 1 billion, both slated for 2026 commercial service.

- July 2025: VPBank and MobiFone executed a broad agreement covering telecom-banking convergence, including mobiPOS rollout for rural agent banking.

- July 2025: The Ministry of Information and Communications named Viettel, VNPT, and MobiFone as dominant entities, triggering mandatory wholesale obligations.

- May 2025: Viettel secured 700 MHz spectrum for USD 75.2 million to back nationwide 5G expansion.

Vietnam Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What growth rate is forecast for the Vietnam MVNO market up to 2030?

The market is expected to expand at a 4.12% CAGR, climbing from USD 233 million in 2025 to USD 285 million by 2030.

How will the New Law on Telecommunications impact new virtual operators?

LOT 2023 obliges dominant MNOs to lease network capacity on non-discriminatory terms, lowering entry barriers and supporting diverse MVNO business models.

Why are digital-banking partnerships important for MVNOs?

Bundling mobile connectivity with payment and lending services raises ARPU and widens reach into rural areas where traditional banking infrastructure is limited.

What opportunity does the 2G shutdown create?

Around 15 million legacy users must upgrade to 4G or higher, giving MVNOs a chance to offer affordable migration bundles and gain market share.

Which technology segment is growing fastest?

5G lines are projected to grow at 32.50% annually as coverage broadens and enterprise applications such as smart manufacturing demand high-performance connectivity.

Can MVNOs target areas without terrestrial coverage?

Yes, hybrid packages that blend satellite links, such as those enabled by the Starlink pilot, can serve fishing fleets and remote mountain communities lacking cell towers.

Page last updated on: