Europe Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

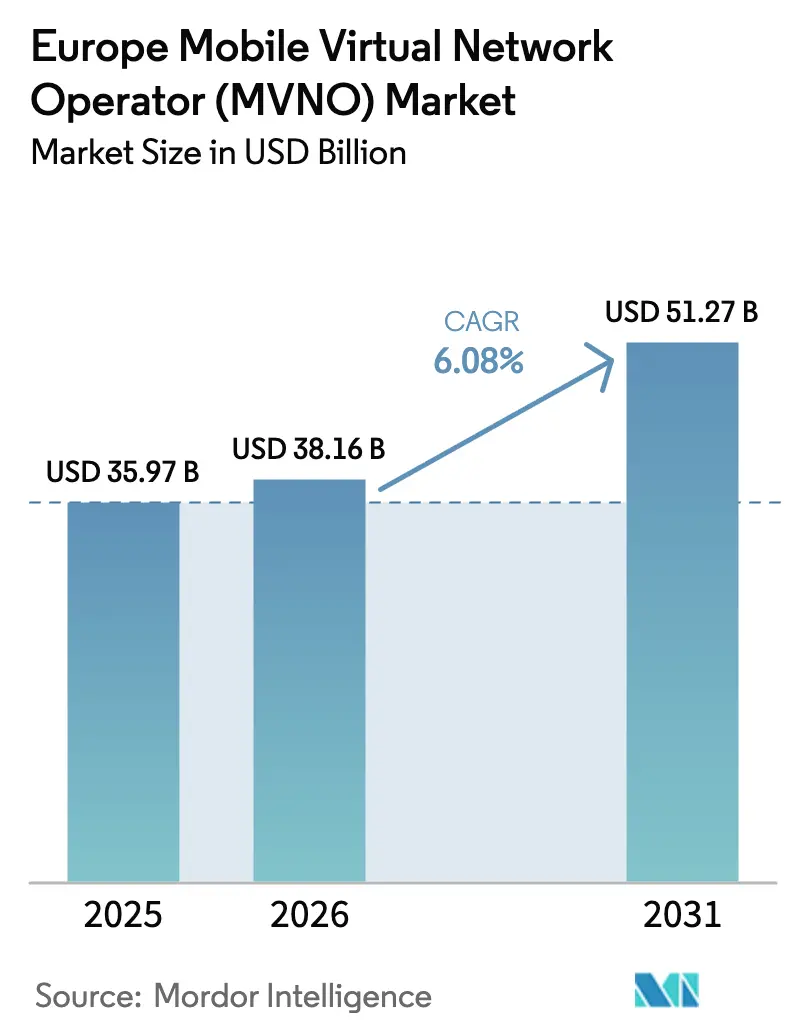

| Base Year Market Size (2025) | USD 35.97 Billion |

| Market Size (2026) | USD 38.16 Billion |

| Market Size (2031) | USD 51.27 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

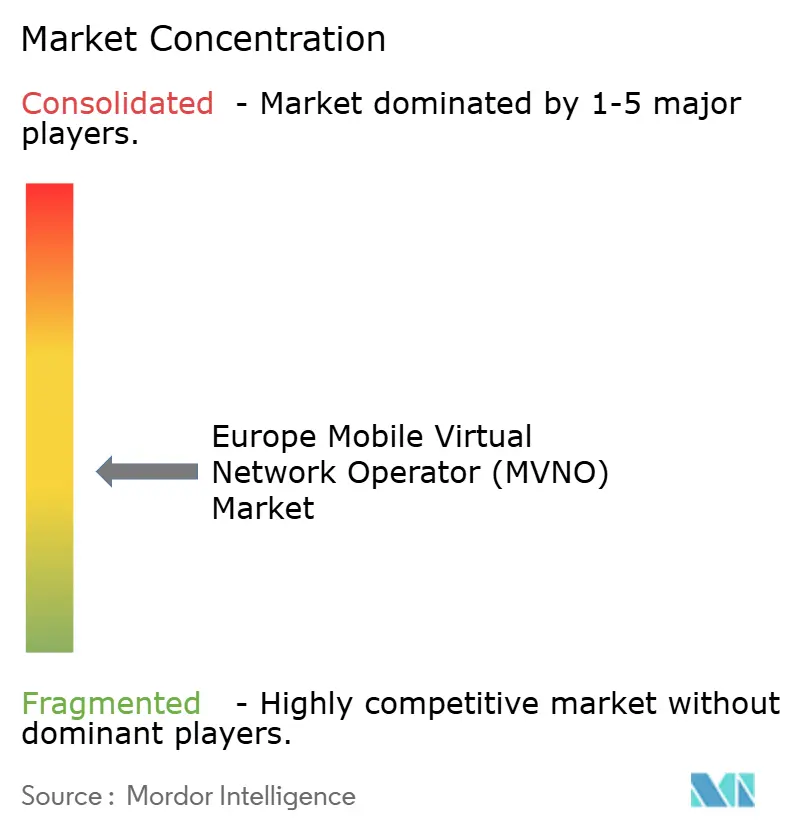

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Europe Mobile Virtual Network Operator (MVNO) market size is expected to grow from USD 35.97 billion in 2025 to USD 38.16 billion in 2026 and is forecast to reach USD 51.27 billion by 2031 at 6.08% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 57.36 million subscribers in 2025 to 76.19 million subscribers by 2030, at a CAGR of 5.84% during the forecast period (2025-2030). Rising demand for infrastructure-light operations, tightening household budgets that favor SIM-only plans, and EU-wide wholesale-access mandates continue to attract new virtual entrants and sustain churn-driven volume growth. The segment benefits from digital-first activation models, improving eSIM uptake, and enterprise appetite for managed private networks that monetize 5G standalone (SA) capabilities. Full MVNOs capture additional value through network control and multi-IMSI routing, while discount brands leverage aggressive pricing to defend share. Strategic partnerships around satellite–terrestrial roaming and open-RAN cores further enhance service differentiation and geographic reach.

Key Report Takeaways

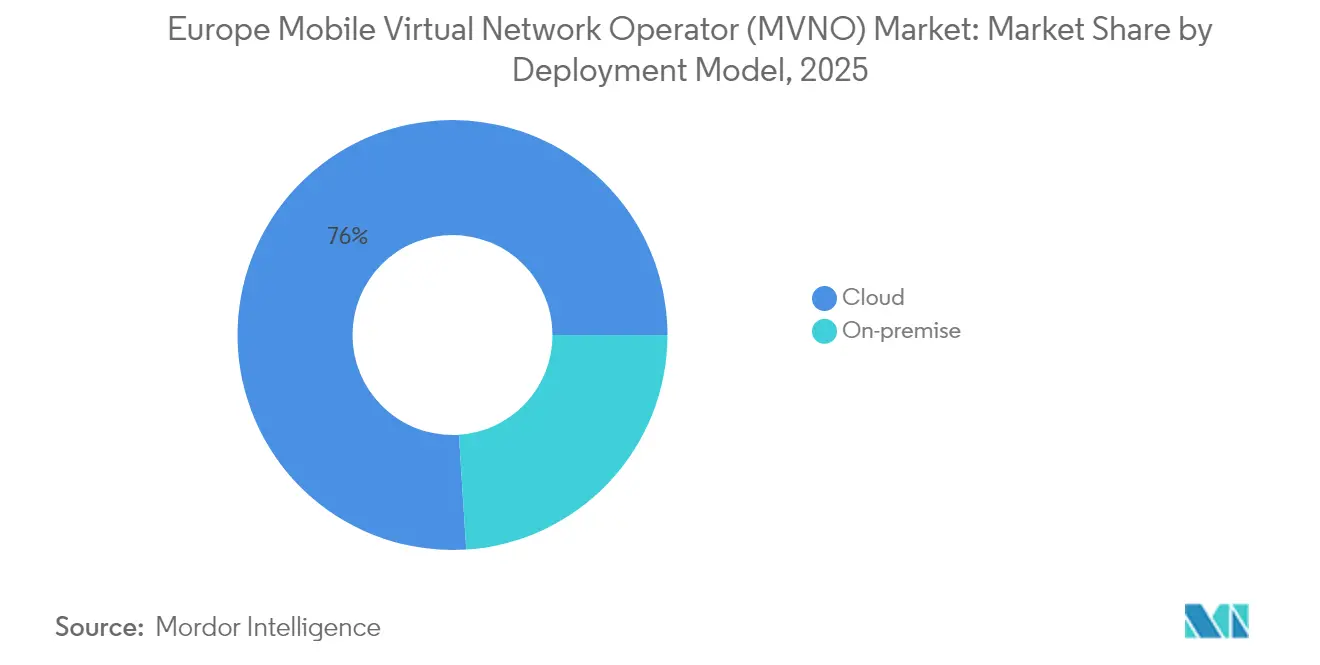

- By deployment model, cloud solutions held 76.02% of the Europe MVNO market share in 2025; the cloud segment is advancing at a 9.32% CAGR through 2031.

- By operational mode, reseller/light/brand MVNOs led with 48.10% revenue share in 2025, while full MVNOs are forecast to grow at a 14.55% CAGR during 2026-2031.

- By subscriber type, consumer accounts for 77.45% of the Europe MVNO market size in 2025, and IoT-specific connections are rising at a 13.62% CAGR.

- By application, discount services commanded 37.60% of the Europe MVNO market size in 2025, and cellular M2M is progressing at a 12.35% CAGR.

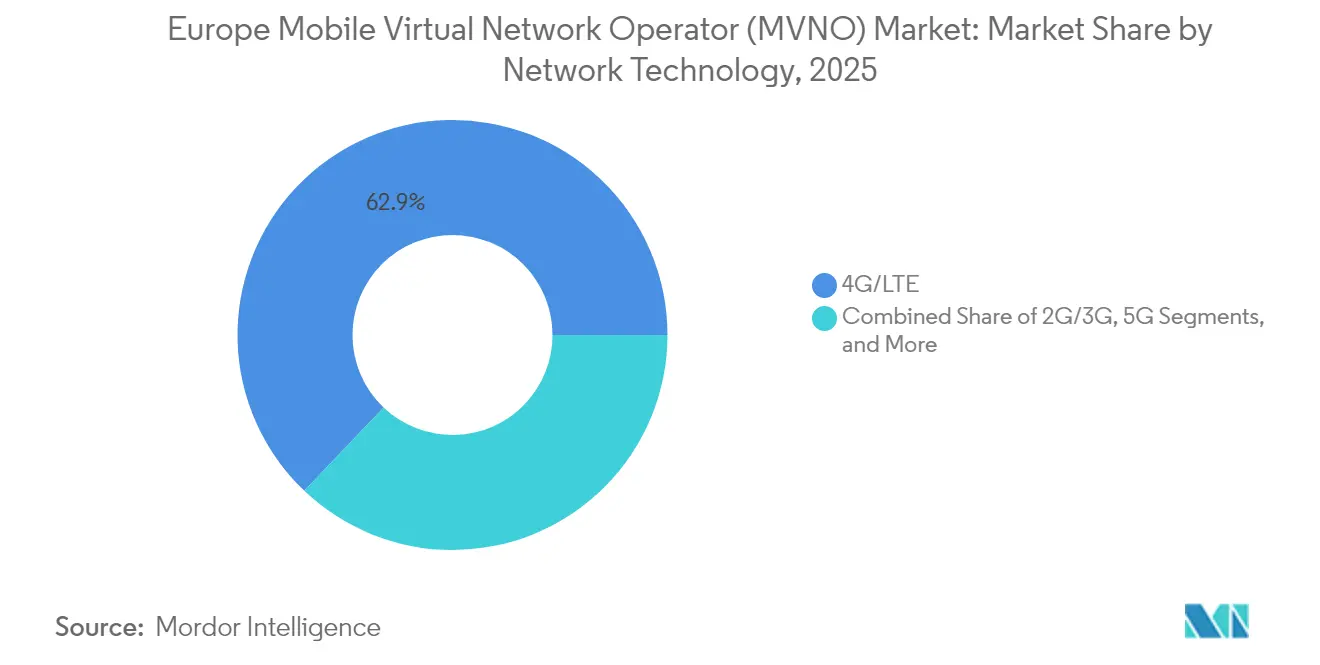

- By network technology, 4G/LTE retained 62.90% share of the Europe MVNO market size in 2025, whereas satellite/NTN is scaling at a 127.4% CAGR.

- By distribution channel, the online/digital-only channel held 62.80% of the Europe MVNO market share in 2025; it is advancing at a 8.74% CAGR through 2031.

- By country, Germany captured 21.85% Europe MVNO market share in 2025; the Rest of Europe region is predicted to climb at a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pro-competition wholesale-access regulations | +1.2% | EU-wide, strongest in Germany, UK, France | Medium term (2-4 years) |

| Cost-of-living push toward discount SIM-only brands | +0.8% | Global, concentrated in Southern and Eastern Europe | Short term (≤ 2 years) |

| 5G SA and network-slicing unlock enterprise/IoT plays | +1.5% | Western Europe core, expanding to Central/Eastern Europe | Long term (≥ 4 years) |

| Exploding demand for managed private-network services | +0.9% | Germany, UK, France, Nordic countries | Medium term (2-4 years) |

| Open-RAN cores enable MVNO transition to infra-light MNO | +0.7% | UK, Germany, Netherlands, pilot markets | Long term (≥ 4 years) |

| Rise of digital-only eSIM travel brands | +0.6% | Global, hub markets in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pro-competition wholesale-access regulations

EU competition law continues to enforce non-discriminatory wholesale terms that lower entry barriers and encourage network switching [1]European Commission, “Broadband: Basic Business Models,” digital-strategy.ec.europa.eu. Germany’s regulator allowed Lyca Mobile to migrate from Vodafone to O2 Telefonica without service disruption, showcasing how fair-dealing rules increase bargaining power for smaller providers. Similar frameworks now cover 5G SA roaming, ensuring MVNOs can offer sliced enterprise services instead of basic resale. The MVNO Europe association keeps lobbying for symmetric access pricing to prevent margin squeeze. Collectively, these measures widen supplier choice, accelerate product launches, and stabilize cost structures that underpin the Europe MVNO market.

5G SA and network slicing unlock enterprise/IoT plays

Live 5G SA slices trialed by Vodafone UK prove that virtual operators can guarantee latency and throughput for industrial robotics, cloud gaming, and campus networks [2]Vodafone Group, “5G Standalone Network Slicing Trials,” vodafone.com. A1 Bulgaria’s roaming slice with Vodafone Germany validated cross-border quality assurance, enabling pan-regional enterprise contracts. The resulting ability to sell differentiated SLAs supports premium pricing and cushions consumer ARPU erosion. Orange Business and Sunrise tested similar offers, indicating momentum beyond early adopters. With cellular M2M traffic expanding, MVNOs that control their core networks are positioned to win IoT budgets over systems integrators.

Exploding demand for managed private-network services

Enterprises are outsourcing campus-wide 5G or LTE private networks to specialists that can integrate security, edge analytics, and device life-cycle support. Deutsche Telekom’s NB-IoT satellite extension with Skylo demonstrates combined terrestrial-NTN coverage for logistics corridors [3]Deutsche Telekom, “Skylo NB-IoT Non-Terrestrial Network Program,” telekom.com. O2 Telefónica’s Business Match tariff bills only actual data usage, mirroring cloud consumption models to relieve cap-ex [4]Telefónica Deutschland, “Innovatives Tarifmodell Business Match,” telefonica.de . Full MVNOs with OSS/BSS autonomy can white-label such offers for multinational subsidiaries, stimulating double-digit revenue growth. This shift reallocates spending from legacy Wi-Fi to licensed-spectrum solutions, deepening addressable value beyond connectivity.

Rise of digital-only eSIM travel brands

App-based eSIM onboarding avoids physical distribution costs and taps impulse buyers at airports. eSIM Go opened an early-access program so emerging UK MVNOs can provision profiles instantly. Honest Mobile’s Smart SIM auto-switches across EE, O2, and Three networks when the signal weakens, raising retention without infrastructure ownership. Travel marketers pitch sustainability gains, 46% lower CO₂ emissions than plastic SIMs, to environmentally minded tourists. As roaming regulation caps retail surcharges, digital brands exploit convenience and multi-network continuity to command modest premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-competition compressing ARPU and marketing ROI | -1.1% | Global, most severe in mature markets (UK, Germany, France) | Short term (≤ 2 years) |

| Delayed/restrictive 5G wholesale agreements | -0.7% | EU-wide, varying by national regulatory approach | Medium term (2-4 years) |

| Wholesale-rate inflation post-MNO consolidation | -0.9% | UK, Netherlands, Austria (post-merger markets) | Medium term (2-4 years) |

| eSIM security and provisioning bottlenecks | -0.4% | Global, technical implementation challenges | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyper-competition compressing ARPU and marketing ROI

Low-cost brands such as Happy SIM and Naked Mobile advertise sub-EUR 5 monthly plans, eroding price floors and diminishing acquisition payback periods. Promotions like SMARTY’s 4× data offers encourage serial churners chasing temporary bargains. Lyca Mobile’s tax disputes highlight how thin margins amplify operational risk. Discount MVNOs without proprietary technology struggle to upsell services, leaving them exposed to price wars that drag down average revenue and jeopardize marketing efficiency at scale.

Wholesale-rate inflation post-MNO consolidation

National markets trending toward three-operator structures gain pricing power over wholesale lines. Assembly Research warned that the Vodafone-Three UK merger could raise virtual access costs, while Analysys Mason modeling shows similar patterns in the Netherlands and Austria. Even with mandated access, incumbents can adjust ancillary fees or delay 5G onboarding, inflating input costs for MVNOs and pressuring service profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure accelerates service agility

Cloud-hosted cores controlled 76.02% revenue in 2025, and the segment is on track for a 9.32% CAGR as operators pivot to pay-as-you-grow opex models. The Europe MVNO market leverages hyperscale data centers to automate onboarding, rate-plan creation, and eSIM profile downloads. Telness Tech ported its European platform onto the U.S. T-Mobile network within months, illustrating cross-border replicability. Cloud orchestration also simplifies AI-driven usage forecasting that cuts working capital needs. On-premise deployments remain relevant for governments or finance clients demanding strict data residency. Mobilezone packages hybrid solutions that meet such compliance while avoiding forklift upgrades. Greater elasticity allows smaller entrants to scale during seasonal peaks without stranded cap-ex, supporting high launch velocity and experimentation unseen in legacy models.

Second-order benefits amplify adoption. Multi-tenant architectures let white-label brands share billing stacks yet customize user interfaces. Real-time analytics track roaming costs, enabling instant retail price adjustments that protect margin as wholesale tariffs fluctuate. Cloud APIs integrate fintech add-ons such as Revolut Pay, evidenced by Lyca Mobile’s 2025 rollout, to monetize payment traffic alongside voice and data. With GSMA’s eSIM Remote SIM Provisioning standard maturing, cloud MVNOs can embed profile swaps that extend device life cycles, providing a green narrative that resonates with regulators and enterprise ESG mandates. Consequently, the cloud path reinforces competitive positioning of the Europe MVNO market across consumer and IoT segments.

By Operational Mode: Full MVNOs capture margin and control

Reseller/light MVNOs retained a 48.10% share in 2025, reflecting ease of entry for retail brands and supermarkets. Yet full MVNOs will post a 14.55% CAGR to 2031 as they internalize core functions like HLR/HSS, policy control, and SIM OTA. Owning the core unlocks vertical productization, private 5G, multi-IMSI roaming, and VPN overlay, which defends yield. 1GLOBAL operates across 190+ countries via KPN Netherlands and other hosts, underscoring the scale attainable when routing autonomy is secured. Service operator models bridge the gap, adding customer care and billing while outsourcing radio access, but lack deep packet inspection to guarantee enterprise SLAs.

Full control boosts negotiating power during wholesale renegotiations because traffic can be redirected with minimal user impact. Access to signaling also enables advanced fraud detection, curbing roaming abuse and protecting EBITDA. Investment requirements decline owing to virtualized cores and cloud licensing, lowering historical barriers. Over time, successful discount resellers migrate up the value chain, mirroring Freenet’s gradual shift in Germany. The Europe MVNO market, therefore, shows a maturation pattern where operational sophistication correlates with growth and resilience.

By Subscriber Type: IoT momentum outpaces consumer saturation

Consumers accounted for 77.45% subscriptions in 2025, but the Europe MVNO market now courts connected-device verticals. IoT-specific lines are forecast to grow 13.62% annually as factories, utilities, and logistics firms embed sensors into critical workflows. OQ Technology’s NB-IoT satellite test with O2 Telefonica proves extended reach for asset tracking beyond terrestrial footprints. Enterprises embrace usage-based billing to align costs with dynamic telemetry volumes. Meanwhile, field-service teams adopt rugged devices on MVNO plans that bundle zero-rating for proprietary apps, easing digital-transformation ROI calculations.

Consumer volume still matters; rising prepaid churn feeds gross-add pipelines. Yet price competition tightens unit margins, pushing operators to diversify. Enterprise managed-mobility bundles include MDM licenses, cybersecurity, and API access, fetching higher ARPU. Hybrid models mixing consumer mass with IoT niches offer portfolio resilience. As device counts per enterprise climb, the Europe MVNO market gains stickier revenue with lower churn than voice-centric retail segments.

By Application: Cellular M2M anchors industrial use cases

Discount voice and data formed a 37.60% value in 2025 as inflation nudged households toward low-cost plans. Still, cellular M2M connections will expand 12.35% per year, propelled by smart-meter rollouts, predictive maintenance, and municipal IoT. Deutsche Telekom’s Skylo agreement layers NTN on NB-IoT to serve remote sensors in maritime or mining operations, broadening the addressable scope. Business categories covering unified communications and SD-WAN preserve stable growth from SME digitization. Other applications, emergency responder networks, e-health monitoring, stay niche but strategic due to high SLA demands that justify premium pricing.

M2M growth dovetails with 5G SA’s ultra-reliable low-latency promise. Edge compute nodes hosted in cloudlets let MVNOs process data locally, reducing backhaul costs and meeting compliance for critical infrastructure. Bundle deals often combine connectivity with hardware leasing and analytics dashboards, increasing share-of-wallet. As a result, the Europe MVNO market moves beyond commodity bandwidth into solution-oriented sales.

By Network Technology: Satellite/NTN redefines coverage

4G/LTE contributed 62.90% revenue in 2025 and will remain the workhorse during the 5G rollout. However, satellite/non-terrestrial networks (NTN) show a 127.4% CAGR, signaling a paradigm shift. Vodafone’s partnership with AST SpaceMobile demonstrated a direct-to-device call from space, hinting at seamless rural coverage and disaster resilience. Spectrum harmonization efforts at CEPT facilitate hybrid SIMs that roam between terrestrial bands and L-band satellite, maintaining session persistence. MVNOs integrate such capabilities to sell uninterrupted logistics tracking, maritime crew services, and outdoor recreation data packs.

Early adopters are full MVNOs that can insert satellite IMSI ranges into their steering logic. Once 3G sunsets, freed low-band spectrum may host NR-RedCap or satellite link budgeting, letting MVNOs serve low-power devices under a single SKU. This technological diversification differentiates providers beyond price and builds moats around ubiquitous coverage.

By Distribution Channel: Digital-first funnels cut acquisition cost

Online portals delivered 62.80% activations in 2025, underpinned by app-driven eSIM provisioning. Ymobile became Britain’s first data-centric eSIM MVNO with frictionless sign-up in under five minutes, setting expectations for instant gratification. Chatbots and AI-powered KYC automate identity checks and SIM registration, lowering manual workload. Physical retail still handles SIM swaps, elderly support, and brand display, but trends toward inventory-light pop-ups. Carrier sub-brands use store presence to upsell devices while cannibalizing premium lines only selectively.

Digital Republic in Switzerland offers plan switches at month-end via dashboard controls, embodying self-service empowerment. Referral codes and social-media micro-influencers replace costly billboard campaigns. Third-party resellers bundle connectivity with electronics, spreading fixed costs across SKUs. Consequently, distribution digitization sustains the scalable economics that propel the Europe MVNO market growth trajectory.

Geography Analysis

Germany led with 21.85% revenue in 2025, owing to regulator-backed wholesale competition that enables frequent network switches and stimulates promotional churn. Lyca Mobile’s migration to O2 Telefónica showcased smooth portability under these rules, while Tchibo Mobil’s fixed-wireless homespot illustrates product expansion beyond mobile. Naked Mobile’s usage-only tariff caters to cost-conscious users, mirroring broader market value focus. Enterprise demand grows as O2’s Business Match usage-billing aligns with Industry 4.0 budgets. These dynamics keep the Germany-anchored portion of the Europe MVNO market vibrant despite price pressures.

The United Kingdom remains a pivotal arena where Ofcom’s looming Vodafone-Three merger review raises uncertainty over future wholesale pricing. Honest Mobile’s multi-network Smart SIM differentiates on resilience across EE, O2, and Three, leveraging eSIM to avoid SIM swaps. SMARTY’s data-boost campaigns intensify discount competition, while the Gigs–Vodafone UK platform accelerates new entrant onboarding. High eSIM adoption and subscription culture favor digital-only brands. Brexit, however, introduces compliance divergence that pan-European MVNOs must navigate when transporting customer data or issuing cross-border invoices.

France maintains steady expansion aided by Bouygues Telecom’s acquisition of La Poste Telecom, which consolidated wholesale bargaining yet kept MVNO brands active. Orange Wholesale’s forthcoming 5G Core-as-a-Service in 2025 will allow smaller operators to launch SA slices without capital intensity, supporting IoT and private-network verticals. Italy and Spain remain fertile through CoopVoce’s 5G debut and Digi’s evolution from MVNO to MNO. Eastern Europe contributes outsized growth to the Rest of Europe cluster at a 9.18% CAGR as liberalization and smartphone penetration rise. Collectively, regional diversity enables the Europe MVNO market to balance mature-market margin tightness with emerging-market volume uplift.

Competitive Landscape

The Europe MVNO market exhibits moderate fragmentation with sustained entrant flow and selective consolidation. Top players, Lyca Mobile, Lebara, Tesco Mobile, retain scale advantages through ethnic-calling niches and supermarket ecosystems. Waterland’s 2024 acquisition of Lebara signaled private-equity confidence in recurring cash-flow profiles despite wholesale cost inflation. Technology now outweighs brand alone; 1GLOBAL leverages full-core autonomy to deliver global multi-IMSI roaming, while Ymobile focuses on data-only youth segments with eSIM exclusivity. Providers differentiate via payment integration, as shown by Lyca Mobile’s Revolut Pay tie-up, or via sustainability pledges around plastic-free eSIMs.

Convergence between satellite and cellular blurs competitive boundaries. Vodafone-AST and OQ Technology collaborations allow MVNOs without spectrum licenses to promise near-ubiquitous reach, challenging incumbent roaming arguments. AI-driven analytics from cloud vendors optimize campaign targeting and fraud detection, lifting EBIT margins for tech-savvy operators. At the same time, hyper-competition pushes some brands toward mergers; for instance, Freenet explores platform sharing with MediaMarkt Saturn to consolidate marketing spend. Overall, innovation pace and regulatory vigilance prevent dominance by any single entity, yet scale remains critical for procurement leverage.

Europe Mobile Virtual Network Operator (MVNO) Industry Leaders

Lycamobile Europe Limited

Lebara Mobile Limited

Tesco Mobile Limited

Giffgaff Limited

iD Mobile Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: eSIM Go launched an early-access program granting UK MVNOs turnkey eSIM provisioning services.

- March 2025: Digital Republic debuted Flat Mobile Plus at CHF 25/month, bundling unlimited Swiss data and 12 GB EU roaming with monthly plan switches.

- March 2025: Honest Mobile introduced Smart SIM, a multi-network eSIM offering unlimited app data and global roaming across 180+ countries.

- January 2025: Lyca Mobile integrated Revolut Pay, achieving 100% authorization and 80% auto top-up adoption inside one month.

- December 2024: 1GLOBAL partnered with KPN Netherlands to extend 5G access within its 190-country footprint.

Europe Mobile Virtual Network Operator (MVNO) Market Report Scope

Mobile virtual network operators (MVNOs) are mainly the wireless service providers that operate without owning the wireless network infrastructure. Instead, they buy network capacity from existing MNOs to deliver services to their users.

The European mobile virtual network operator (MVNO) market is segmented by type (consumer (youth, rural, and urban) and enterprise (business)) and country (the United Kingdom, France, Germany, Denmark, Italy, Spain, and the Rest of Europe). Operational models, such as resellers, service operators, full MVNOs, and other modes, are considered under the scope. The study includes country-level analysis for key markets such as the United Kingdom, France, Germany, and Spain. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe MVNO market?

The segment is valued at USD 38.16 billion in 2026.

How fast will the Europe MVNO market expand through 2031?

Total revenue is projected to reach USD 51.27 billion by 2031, reflecting a 6.08% CAGR over the forecast window.

Which deployment model generates the most revenue today?

Cloud-based MVNO platforms account for 76.02% of 2025 revenue thanks to lower cap-ex and rapid service rollout.

What subscriber segment is fueling incremental growth?

IoT-specific lines are rising at a 13.62% CAGR, outpacing consumer additions as enterprises embed connectivity in devices and sensors.

Which network technology shows the strongest growth trend?

Satellite/non-terrestrial networks post a 127.4% CAGR, driven by partnerships that extend coverage beyond terrestrial footprints.

How concentrated is competition among European MVNOs?

The combined share of the five largest players sits well below 50%, earning a moderate concentration score of 4 on a 10-point scale.

Page last updated on: