France Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

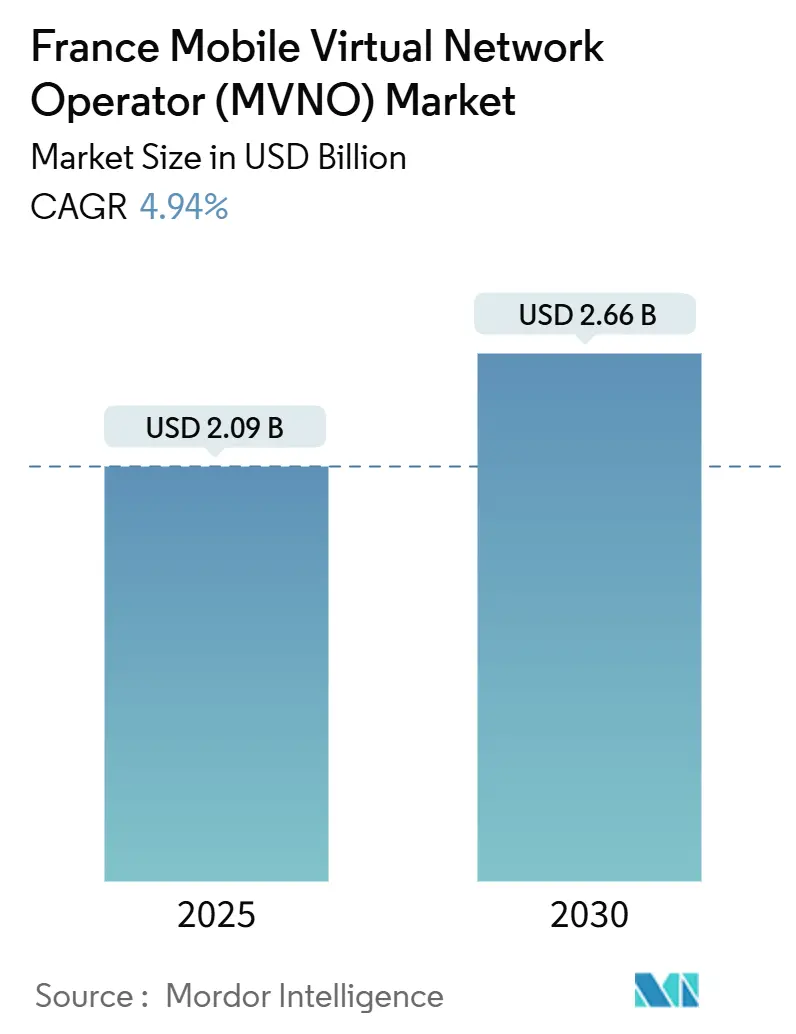

| Market Size (2025) | USD 2.09 Billion |

| Market Size (2030) | USD 2.66 Billion |

| Growth Rate (2025 - 2030) | 4.94% CAGR |

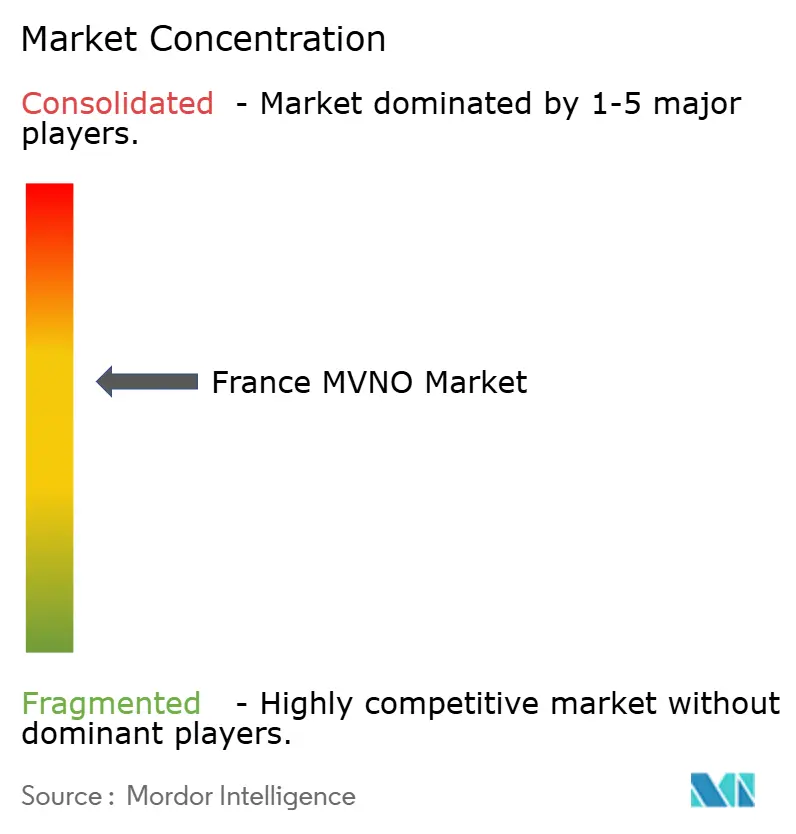

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The France Mobile Virtual Network Operator Market size is estimated at USD 2.09 billion in 2025, and is expected to reach USD 2.66 billion by 2030, at a CAGR of 4.94% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 8.47 million Subscribers in 2025 to 10.57 million Subscribers by 2030, at a CAGR of 4.53% during the forecast period (2025-2030).

Solid wholesale-access protections, nationwide 5G coverage, and rising demand for specialized IoT connectivity position the France MVNO market for durable growth [1]Autorité de régulation des communications électroniques et des postes, “Mobile Network Sharing,” ARCEP.fr . Operators are shifting from pure price disruption toward value-added service bundles that exploit advanced cloud cores, network slicing, and digital-only distribution. Cloud deployment signaling that asset-light entrants can scale quickly, while the full-MVNO model shows a clear preference for ownership of billing and customer experience functions. Consumer services still dominate volumes, yet cellular M2M and connected-vehicle use cases are the fastest-growing slices of the France MVNO market as industrial digitalization accelerates. Simultaneously, strategic acquisitions such as Bouygues Telecom’s purchase of La Poste Mobile illustrate how host networks use consolidation to internalize successful virtual brands and reinforce market positioning.

Key Report Takeaways

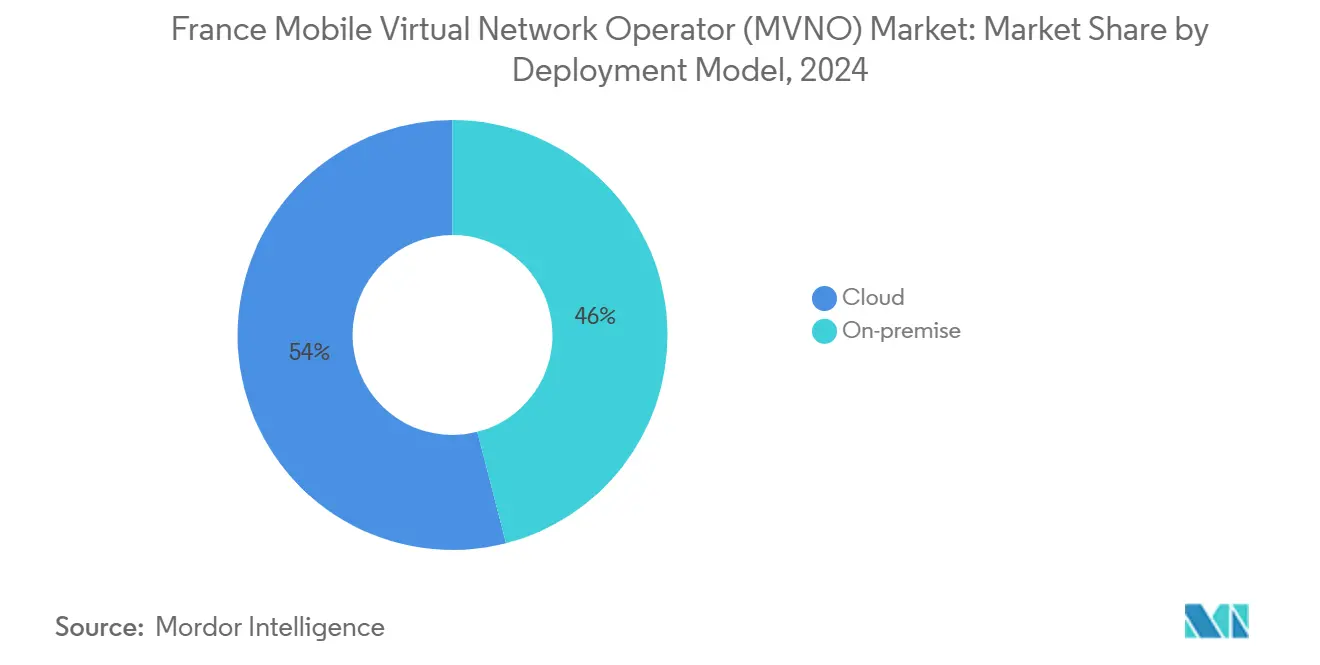

- By deployment model, cloud infrastructures captured 54% of France MVNO market share in 2024 and are expanding at an 11.53% CAGR through 2030.

- By operational mode, the full-MVNO segment held 50% of the France MVNO market size in 2024 and is advancing at an 8.70% CAGR through 2030.

- By subscriber type, IoT-specific lines are rising at a 16.88% CAGR, though consumers retained 75% share of the France MVNO market size in 2024.

- By application, Cellular M2M is rising at a 15.64% CAGR, though discount application retained 36% share of the France MVNO market size in 2024.

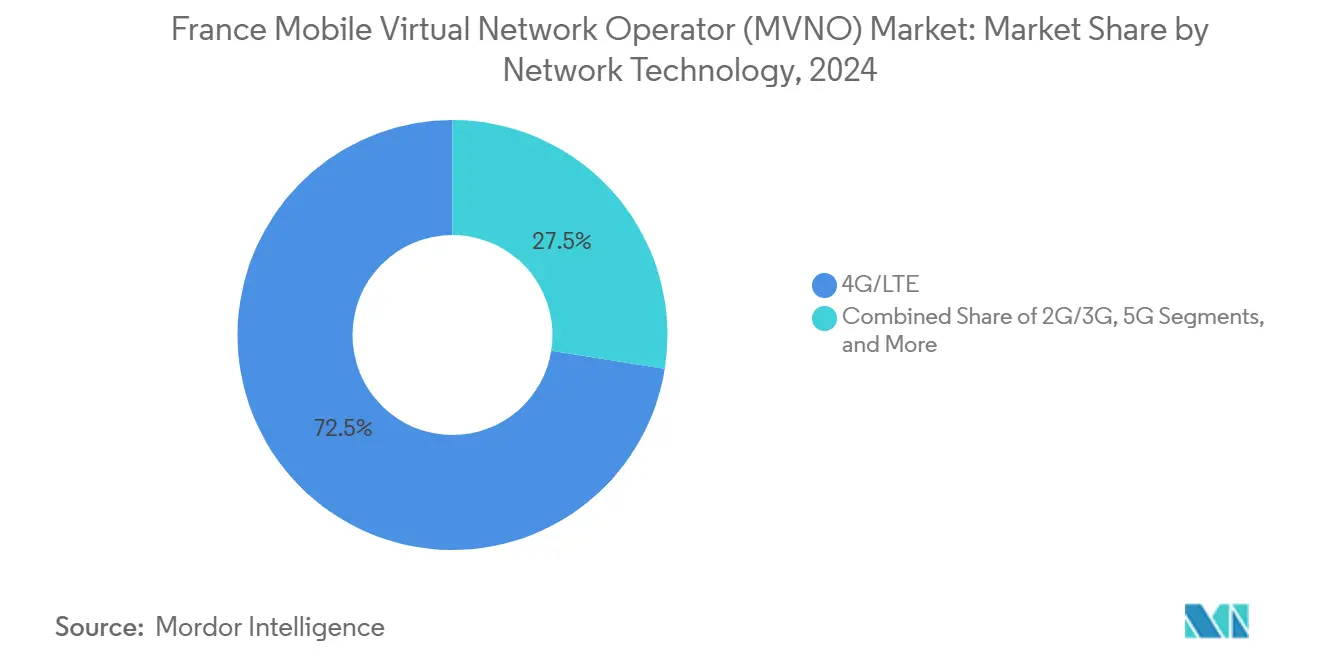

- By network technology, 5G connections are forecast to grow at a 26.57% CAGR to 2030, while 4G/LTE still commanded 72.5% of France MVNO market share in 2024.

- By distribution channel, the online/digital-only channel captured 44% of France MVNO market share in 2024 and are expanding at an 12.51% CAGR through 2030.

France Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong wholesale-access regulation (ARCEP "Loi Chatel", roaming caps) | +1.2% | National, with enhanced enforcement in metropolitan areas | Long term (≥ 4 years) |

| Price-sensitive consumer base accelerating discount SIM demand | +0.8% | National, with higher penetration in suburban and rural areas | Medium term (2-4 years) |

| Nation-wide 5G rollout enabling premium MVNO tiers | +1.5% | National, with early gains in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Digital-only distribution lowers OPEX and churn | +0.9% | National, with stronger adoption in urban demographics | Short term (≤ 2 years) |

| Connected-vehicle and IoT MVNO niches in automotive/industrial clusters | +0.6% | Regional, concentrated in automotive hubs and industrial zones | Long term (≥ 4 years) |

| "Green-MVNO" propositions aligned to France's carbon-reporting mandates | +0.4% | National, with premium uptake in environmentally conscious segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Wholesale-Access Regulation Drives Market Entry

ARCEP’s “Loi Chatel” obligations guarantee non-discriminatory network access and transparent wholesale tariffs, enabling small brands to secure nationwide footprints without punitive roaming fees. Free Mobile’s long-running national roaming arrangement with Orange, now extended to 2028, underscores how regulatory stability lowers entry barriers for the France MVNO market. Predictable costs let virtual operators direct capital toward customer acquisition rather than spectrum or tower spending. The framework, therefore, underpins the sustained participation of more than two dozen active MVNOs and supports continuous service innovation across both consumer and enterprise segments.

Nationwide 5G Rollout Enables Premium Service Tiers

By April 2025, Free Mobile covered 95% of the population with 20,000+ 5G sites and became the first French carrier to activate standalone 5G nationwide[2]Telecoms.com Editorial Staff, “France’s Free Makes Bold 5G Standalone Claims,” Telecoms.com. Orange followed with a 5G Plus enterprise offer priced at EUR 79 per month, demonstrating clear monetization paths for ultra-low-latency slices[3]Light Reading Staff, “Orange Dishes Up Slices of 5G Standalone to Biz Users,” LightReading.com. These upgrades let MVNOs introduce priority-data tiers, guaranteed bandwidth, and industrial IoT services that command higher ARPU than legacy discount voice bundles. The result is a pivot from price competition toward differentiated quality-of-service commitments inside the France MVNO market.

Digital-Only Distribution Transforms Customer Acquisition

MVNOs such as Prixtel operate exclusively online, eliminating store rent and handset inventory while providing real-time plan changes that automatically align billing with usage [4]Selectra Telecom Team, “Les Forfaits Mobile de Prixtel en Juin 2025,” Selectra.info. Lower fixed costs allow these brands to maintain price advantages even after wholesale fees, and friction-free onboarding drives lower churn among younger, urban users. Digital-first strategies, therefore, yield a dual benefit of higher margin and superior customer experience.

Connected-Vehicle and IoT Applications Create Specialized Niches

NB-IoT and LTE-M overlays on existing 4G and 5G grids enable nationwide coverage for low-power devices. Specialist enablers such as Transatel have capitalized by signing double-digit MVNO contracts that bundle SIM management, remote provisioning, and embedded-connectivity APIs for automotive OEMs. Focused expertise allows such operators to command premium pricing and cultivate long-run contracts insulated from typical prepaid churn prevalent in the France MVNO market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fixed-mobile bundles by MNOs locking customers and eroding MVNO ARPU | -1.1% | National, with stronger impact in suburban family households | Medium term (2-4 years) |

| Margin squeeze from market consolidation (e.g., Bouygues-La Poste deal) | -0.7% | National, with concentrated effects in competitive metropolitan areas | Short term (≤ 2 years) |

| Rising energy-consumption surcharges under 2024 "Numérique Soutenable" rules | -0.3% | National, with proportionally higher impact on smaller operators | Long term (≥ 4 years) |

| Lag in wholesale 5G-SA APIs delaying service innovation | -0.5% | National, with delayed premium service launches in enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fixed-Mobile Bundle Strategies Constrain MVNO Growth

Orange’s convergent offer, which lifted its bundled ARPU to EUR 77.8 in Q1 2025, locks households into multi-service packages that MVNOs struggle to replicate without fixed networks. Convenience-oriented families, therefore, remain inside incumbent ecosystems even when stand-alone mobile tariffs are cheaper elsewhere. The France MVNO market must counter with value-added mobile-only features, such as energy-tracking dashboards or carbon reporting, to erode bundle loyalty.

Market Consolidation Intensifies Competitive Pressure

Bouygues Telecom’s EUR 950 million purchase of La Poste Mobile removed a fast-growing discount brand from independent competition and delivered Bouygues an extra 2.4 million subscribers. Similar moves reduce wholesale revenue sources for remaining MVNOs and may trigger tougher contract renegotiations. Smaller players, therefore, face a build-or-be-bought dilemma, pushing them to scale IoT and B2B niches rapidly or risk absorption by host networks eager to consolidate the France MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud-hosted cores controlled 54% of the France MVNO market in 2024 and are forecast to grow at a 11.53% CAGR through 2030. This leadership underscores how asset-light architecture lets entrants shift capex into marketing, cut launch lead times, and access AI-driven analytics natively. The France MVNO market size for cloud deployments is projected to reach USD 1.62 billion by 2030, reflecting outsized uptake among new digital-only brands. On-premise cores still serve financial-services MVNOs and defense contracts, but their relative share will recede due to higher maintenance overhead.

Cloud agility enables rapid feature rollout. In 2025, Free Mobile embedded a Mistral AI assistant across 15.5 million SIMs, signaling how SaaS models accelerate differentiation and deepen engagement. Such innovations help preserve pricing power while enhancing stickiness, key advantages as the France MVNO market becomes more experience-centric.

By Operational Mode: Full-MVNO Model Enables Service Control

Full-MVNOs represented 50% of total lines in 2024, posting an 8.70% CAGR outlook to 2030 as brands seek end-to-end control. With ownership of IMS cores and billing systems, full operators can tailor bundles, generate granular usage insights, and negotiate wholesale fees from a stronger position. Their share of the France MVNO market size is anticipated to exceed USD 1.33 billion in 2030.

The model also supports portfolio brands. Euro Information Telecom manages NRJ Mobile, Auchan Telecom, and Crédit Mutuel Mobile over a unified stack, proving how economies of scope offset the higher upfront integration effort. Such versatility will matter as the France MVNO market diversifies into green, youth, senior, and expatriate niches.

By Subscriber Type: IoT Applications Drive Fastest Growth

Consumer accounts still delivered 75% of 2024 connections, yet IoT lines are climbing at 16.88% CAGR. NB-IoT is forecast to secure 45% of France’s cellular IoT links by 2030, while LTE-M will capture 6%. This trajectory implies that the France MVNO market share for IoT-specific offerings could double before decade-end. Enterprises appreciate virtual operators’ API exposure, usage-based billing, and neutrality across host networks.

Emerging regulations on carbon reporting and supply-chain traceability augment the business case for sensor rollouts, bolstering demand for SIM management platforms that are core to the France MVNO market.

By Application: Cellular M2M Leads Innovation Segments

Discount voice and data plans still commanded 36% of 2024 revenue, but cellular M2M services are the fastest mover at 15.64% CAGR. Factory automation, smart metering, and vehicle telematics need high-availability links rather than human-facing apps, aligning well with MVNOs’ agile provisioning. Consequently, the France MVNO market size aligned to M2M is expected to top USD 460 million by 2030.

As spectrum refarming reduces 2G support, MVNOs are upgrading embedded SIM fleets to LTE-M and 5G RedCap, earning uplift from extended device lifetimes and enhanced security features. This pivot underscores the strategic importance of application-specific expertise within the France MVNO market.

By Network Technology: 5G Transition Accelerates Premium Services

While 4G/LTE held 72.5% of active SIMs in 2024, 5G subscriptions are expanding at a 26.57% CAGR, reflecting devices’ rapid refresh cycle and enthusiasm for cloud-gaming, AR, and industrial automation. The France MVNO market size tied to 5G could top USD 830 million by 2030. Satellite/NTN remains niche, yet offers lifeline connectivity in overseas territories and maritime routes.

The competitive edge rests on time-to-market. ARCEP counted 47,046 authorized 5G sites by July 2024, with Free Mobile operating the largest share at 19,632. Early access to standalone cores and edge zones allows MVNOs to commercialize guaranteed-latency slices for factories and media production, reshaping revenue mix within the France MVNO market.

By Distribution Channel: Digital Transformation Reshapes Customer Acquisition

Online portals and app-based onboarding generated 44% of 2024 activations and are on a 12.51% CAGR pathway. The France MVNO market size attributable to digital sales could cross USD 1.25 billion by 2030, powered by frictionless KYC, eSIM download, and automated billing. Brick-and-mortar remains valuable for older demographics and handset upgrades but lacks cost competitiveness.

Prixtel’s tiered plans, ranging from EUR 1.99 to EUR 13.99, adjusted monthly to actual usage, illustrate the personalization possible only in a fully digital stack. This level of flexibility will be decisive as the France MVNO market races toward experience-based differentiation.

Geography Analysis

France’s metropolitan core remains the principal geography, underpinned by 5G population coverage of 95% and near-universal fiber backhaul. Paris, Lyon, and Marseille reflect the highest ARPU tiers as enterprises adopt premium slices and consumers embrace unlimited-data offers. With 20,000+ 5G sites, Free Mobile extended blanket coverage that MVNO partners can resell nationwide without service disparity.

Suburban departments drive volume through discount SIM uptake amid inflationary pressure. Price-sensitive households prefer plans below EUR 10, reinforcing the importance of competitive wholesale pricing to sustain margins inside the France MVNO market. Rural zones benefit from ARCEP’s obligation of coverage parity, narrowing historical gaps in service quality.

Overseas territories, such as Martinique, Guadeloupe, and Réunion, form a smaller but strategic extension. New frequency auctions in the 700 MHz and 3.5 GHz bands admitted four qualified operators, creating fresh wholesale hosts and therefore avenues for MVNO expansion. Though backhaul costs are higher, niche tourism and maritime IoT applications present profitable adjacencies for agile brands within the France MVNO market.

Competitive Landscape

Roughly 25 active brands hold 10-15% of national SIMs, making the France MVNO market semi-consolidated. Host networks still dominate, yet independent virtual operators survive by occupying defined niches, youth plans, expatriate roaming, ethical or green-focused services, and industrial IoT connectivity. Bouygues Telecom’s 2024 acquisition of La Poste Mobile highlighted how successful discount players often become targets once they approach 2-3 million customers.

Technology partnerships are equally strategic. Nokia renewed a multi-year supply deal with Iliad to modernize radio and core functions, ensuring performance parity with tier-1 operators. At the software layer, Free Mobile’s Mistral AI integration exemplifies how MVNOs differentiate via value-added digital services rather than spectrum ownership.

Competitive advantage increasingly rests on customer-lifecycle economics. Digital-only players post acquisition costs 35-40% lower than store-based rivals, enabling them to undercut tariffs without sacrificing EBITDA. Meanwhile, industrial MVNOs lock in 5-10-year contracts with OEMs, smoothing revenue volatility. These diverse tactics contribute to a robust but dynamic France MVNO market.

France Mobile Virtual Network Operator (MVNO) Industry Leaders

La Poste Telecom SAS (Bouygues Telecom)

Syma Mobile

Lebara France

NRJ Mobile

Prixtel SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Nokia extended its infrastructure partnership with Iliad Group to reinforce radio and core upgrades across France.

- November 2024: La Poste Groupe finalized the EUR 950 million sale of La Poste Telecom to Bouygues Telecom, adding 2.4 million subscribers to Bouygues’ base.

- October 2024: Bouygues Telecom launched the B.iG family-focused brand to defend share in a price-squeezed consumer segment.

- June 2024: ielo secured EUR 208 million in new financing to accelerate fiber-backhaul and wholesale-enablement services for MVNOs.

France Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the current value of the France MVNO market?

The France MVNO market size was USD 2.09 billion in 2025.

How fast is the France MVNO market projected to grow?

The market is forecast to expand at a 4.94% CAGR, reaching USD 2.66 billion by 2030.

Which deployment model holds the largest share among French MVNOs?

Cloud-hosted cores led with 54% share in 2024 and show an 11.53% CAGR outlook.

Why are MVNOs adopting 5G services?

Nationwide standalone 5G lets MVNOs sell premium low-latency or slice-based packages that lift ARPU.

Which subscriber segment is expanding fastest?

IoT-specific lines are growing at 16.88% CAGR as industrial and automotive applications scale.

How is consolidation affecting independent MVNOs?

Acquisitions like Bouygues-La Poste illustrate pressure on mid-size brands to scale niche expertise quickly or risk buyout.

Page last updated on: