South Korea Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

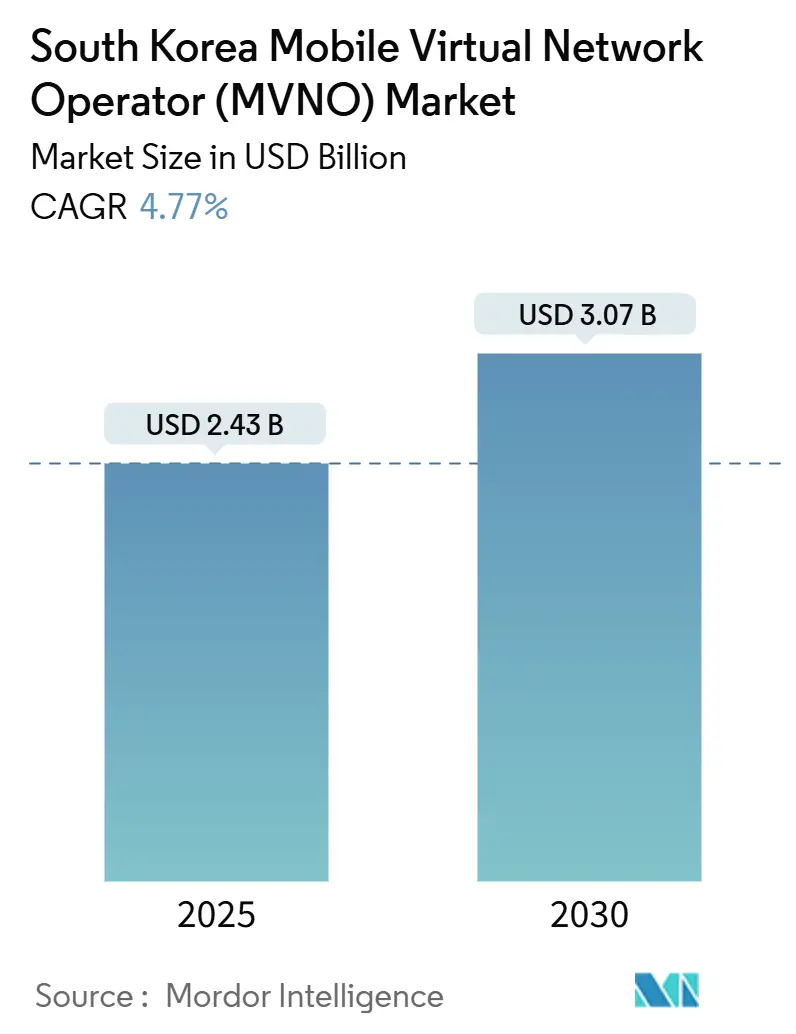

| Market Size (2025) | USD 2.43 Billion |

| Market Size (2030) | USD 3.07 Billion |

| Growth Rate (2025 - 2030) | 4.77% CAGR |

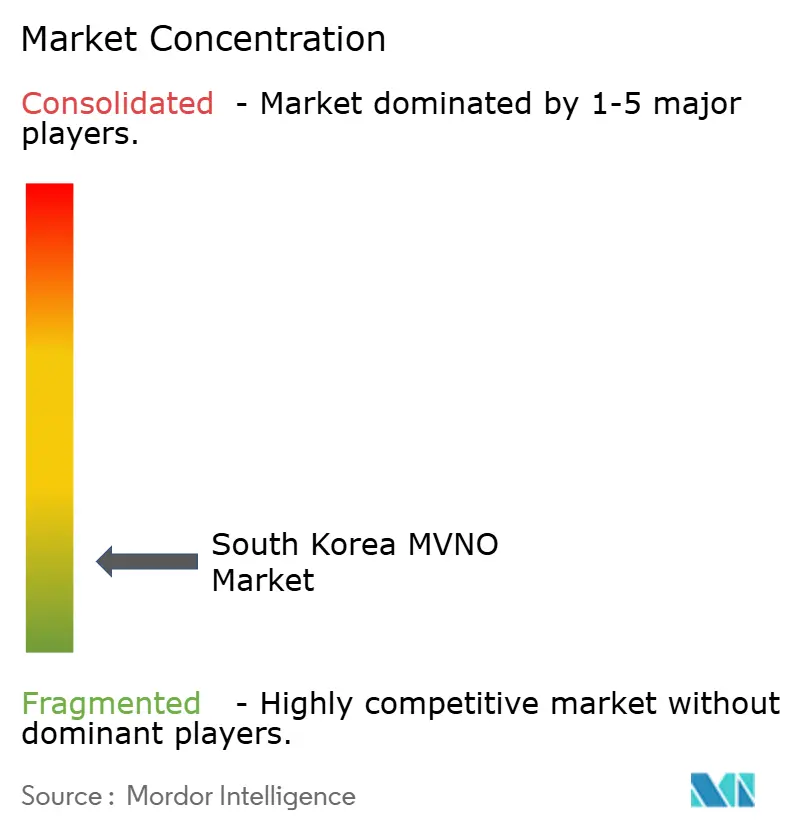

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The South Korea MVNO Market size is estimated at USD 2.43 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 4.77% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 9.55 million subscribers in 2025 to 11.63 million subscribers by 2030, at a CAGR of 4.03% during the forecast period (2025-2030). Rising wholesale price reforms, aggressive 5G plan launches in the 10,000 KRW range, and eSIM-driven digital onboarding are reshaping competitive dynamics, allowing smaller brands to secure price-sensitive customers while preserving margins. Cloud-centric deployments reduce capital outlays and speed up service launches, and device subsidy deregulation scheduled for July 2025 is expected to further stimulate subscriber churn toward value-oriented offerings. Enterprise and IoT use cases, particularly private 5G networks in industrial hubs, signal new revenue streams and underpin the sector’s gradual shift from retail voice-data reselling to connectivity-as-a-service. Finally, satellite/NTN pilots illustrate the long-term ambition to extend coverage to remote zones and unlock global roaming synergies.

Key Report Takeaways

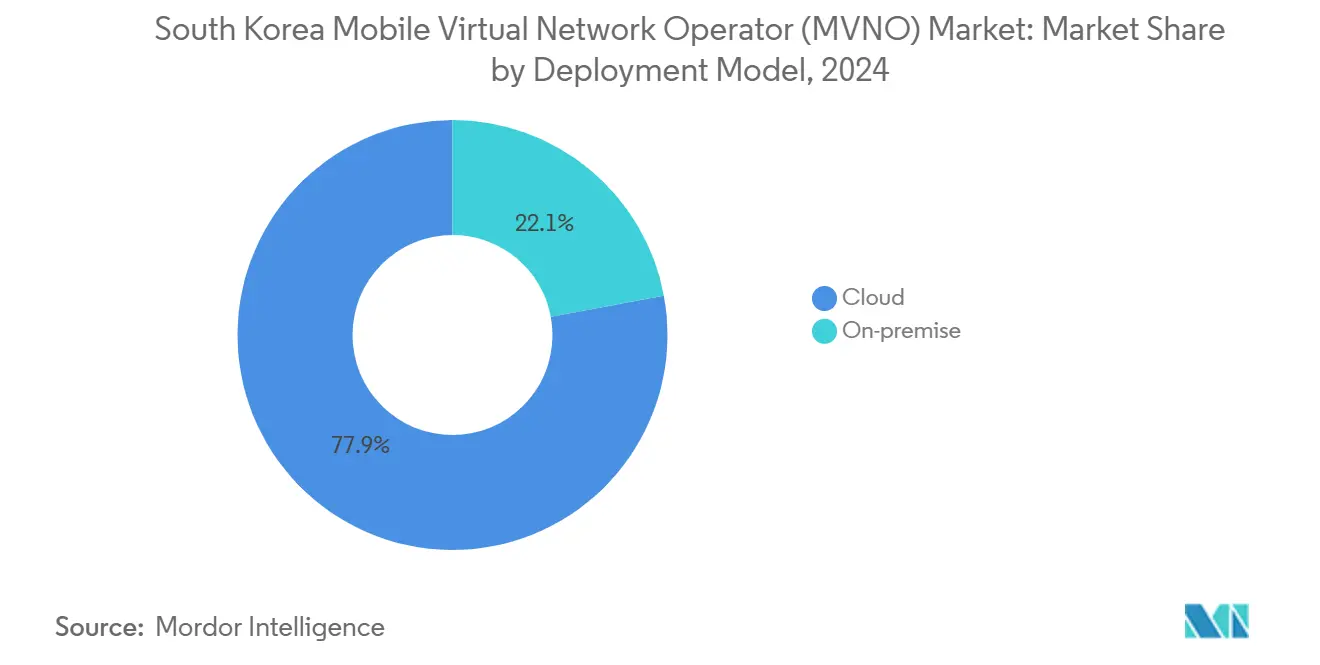

- By deployment model, cloud infrastructure commanded 77.93% of the South Korea MVNO market share in 2024; it is projected to expand at a 7.51% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs led with 57.79% revenue share in 2024, while the full MVNO tier is forecast to post a 24.59% CAGR to 2030.

- By subscriber type, consumer lines accounted for 76.04% of the South Korea MVNO market size in 2024, whereas enterprise subscriptions are advancing at a 33.62% CAGR.

- By application, the Others bucket covered 40.98% share in 2024; cellular M2M connectivity shows the fastest CAGR at 19.33% up to 2030.

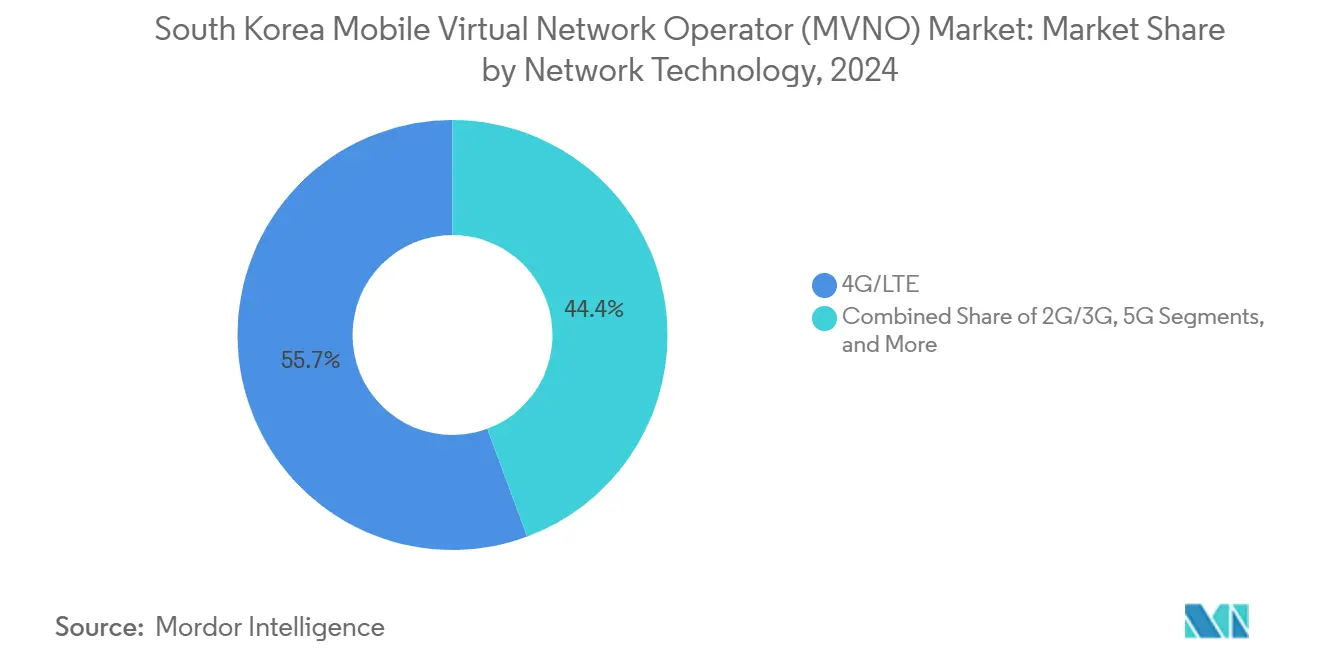

- By network technology, 4G/LTE retained a 55.65% share in 2024, and satellite/NTN plans are set to grow the quickest CAGR at 99.44% up to 2030.

- By distribution channel, online/digital-only sales captured a 62.44% share in 2024, with third-party/wholesale outlets rising at a 9.02% CAGR.

South Korea Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for MVNO competition | +1.2% | Nationwide, Seoul metro | Short term (≤ 2 years) |

| Rising demand for low-cost data plans | +0.8% | Nationwide | Medium term (2-4 years) |

| Nationwide 5G coverage unlocking MVNO offers | +1.0% | Nationwide, urban focus | Medium term (2-4 years) |

| eSIM-driven frictionless onboarding | +0.6% | Nationwide | Long term (≥ 4 years) |

| Fintech-telco bundling | +0.4% | Urban centers | Medium term (2-4 years) |

| Industrial IoT and private-network SIM uptake | +0.7% | Industrial complexes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government incentives for MVNO competition

Wholesale data rates were slashed 36.4% in 2024, dropping from KRW 1.29/MB to KRW 0.82/MB and enabling 5G plans around KRW 15,000-19,800 with 20 GB data allowances, roughly one-third the price of comparable MNO tariffs [1]대한민국 정부 규제정보포털, “Regulatory Innovation Results,” better.go.kr. Demand-driven spectrum allocation, effective H1 2025, permits operators to pre-request frequencies, and seven MVNOs now qualify for enhanced bulk-purchase discounts. These policies support the South Korean MVNO market in surpassing its current 16.7% subscription share target.

Rising demand for low-cost data plans

Daily port-ins exceed 100 lines after cut-price 5G launches, saving switchers nearly KRW 400,000 per year compared with legacy carrier bundles [2]최지연, “₩10,000-range 5G MVNO Plans,” zdnet.co.kr . Survey data show 83% of MVNO users preferring eSIM activation, reflecting the broader consumer pivot toward self-service, price-oriented connectivity.

Nationwide 5G coverage unlocking MVNO offerings

Full 5G coverage has neutralized historic network-quality gaps; SK Telecom recorded average 5G speeds of 1,064.54 Mbps, and multiple 22 GB low-cost plans surfaced on KT and LG U+ networks in early 2025. Private 5G allocations across 56 sites enable network slicing and edge-compute propositions tailored to manufacturing, healthcare, and power-grid operators.

eSIM-driven frictionless onboarding

eSIM uptake hit 83% among MVNO subscribers, cutting SIM logistics costs and letting customers activate service in minutes through purely digital flows. StageFive’s unlimited global roaming eSIM underlines the differentiation possibilities, reporting 162% revenue growth on the back of self-built billing stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wholesale pricing power of MNOs | -1.1% | Nationwide | Medium term (2-4 years) |

| Cannibalization by MNO sub-brands | -0.9% | Urban competitive zones | Short term (≤ 2 years) |

| Unclear satellite/NTN spectrum policy | -0.3% | Nationwide | Long term (≥ 4 years) |

| Limited 5G SA core-virtualization skills | -0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wholesale pricing power of MNOs

Revenue-share bands ranging 43%-62.5% keep MVNO gross margins thin, and cumulative losses at KB Liiv M reached KRW 60.5 billion for 2019-2023 [3]씨엠티정보통신 재무정보, saramin.co.kr. Smaller entrants struggle to secure favorable wholesale terms, while traffic de-prioritization risks under peak loads persist.

Cannibalization by MNO sub-brands

With subsidy caps lifted from July 2025, incumbent carriers can re-enter the device-discount game, eroding MVNO price leadership. KB Liiv M’s share slipped from 5.3% in 2022 to 4.8% in 2023 amid early promotional flanking by sub-brands [4]조승리, “Sub-Brand Subsidy Competition,” businesspost.co.kr .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure drives digital transformation

Cloud deployments captured 77.93% of the South Korean MVNO market share in 2024, reflecting operators’ appetite for scalable opex-based platforms. This configuration is forecast to widen the South Korea MVNO market size at a 7.51% CAGR as brands deploy real-time billing and AI-powered customer-care stacks over public cloud instances. On-premise systems remain relevant among banks and government agencies that demand strict data sovereignty, thus tempering a full-scale shift.

Service agility explains cloud demand. StageFive uses a cloud-native BSS to iterate roaming bundles every quarter, while 25% of private 5G sites employ a shared-core topology that merges cost benefits with latency gains. Regulatory fast-track certification for cloud workloads further accelerates market entry.

By Operational Mode: Full MVNO transition accelerates

Reseller/light/brand configurations still dominate with 57.79% share, but full MVNO entities are projected to lift the South Korea MVNO market size for that tier at a 24.59% CAGR through 2030. Full control of IMSIs and core network elements allows bespoke quality of service and pricing, critical for enterprise IoT contracts.

StageFive has flagged an infrastructure build-out to move beyond light MVNO status, citing spectrum self-allocation provisions as a catalyst. Financial hurdles remain higher, yet the margin upside from wholesale avoidance and network-slice monetization justifies the shift.

By Subscriber Type: Enterprise segment emerges as growth engine

Consumer lines held a 76.04% share in 2024, but enterprise SIMs are forecast to scale at a 33.62% CAGR, driving incremental South Korea MVNO market revenue. Private 5G deployments at POSCO, Samsung Medical Center, and Korea Electric Power Corporation illustrate use cases across autonomous locomotives, remote surgery, and grid safety.

Consumers continue to flock to 20 GB 5G bundles priced in the 10,000 KRW range, underscoring sustained cost-savings pull. Meanwhile, IoT-tailored SKUs integrating edge compute and AI video analytics signal future diversification beyond smartphones.

By Application: Cellular M2M drives innovation

The others category accounts for a 40.98% share by virtue of eclectic fintech-bundled and cross-border roaming offers. Yet, cellular M2M lines are on track for a 19.33% CAGR, mirroring Korea’s Industry 4.0 roadmap. Logistics hubs deploy AGV fleets powered by MVNO SIMs, and shipyards stream multi-4K feeds for AI safety surveillance, each reinforcing the South Korea MVNO market’s industrial relevance.

Discounts and business plans continue attracting SMEs seeking low-overhead connectivity, while device-insurance add-ons help operators lift ARPU without eroding headline price points.

By Network Technology: 5G transition accelerates

4G/LTE still contributes 55.65% of connections, but 5G uptake is surging owing to the wholesale price cut that slashed plan costs by 63.7% against incumbent MNO lists. Seven MVNOs on SK T and KT pipes now market standalone 5G handsets with 20 GB allowances, broadening addressability. Satellite/NTN trials post a headline 99.44% CAGR from a small base, buoyed by KT’s KOREASAT-6 tests and a USD 240 million government LEO program slated for 2025-2030.

By Distribution Channel: Digital-first strategy dominates

Online portals amassed a 62.44% share in 2024, fueled by 83% eSIM adoption that removes physical SIM friction. KT M Mobile recorded 180,000 activations within 30 months via entirely remote flows. Third-party chains like 7-Eleven still matter for handset-bundle buyers and are growing fastest at 9.02% CAGR.

Geography Analysis

Nationwide policy backing, including data wholesale cuts and demand-led spectrum auctions, anchors the South Korean MVNO market. Seoul metro customers illustrate the highest churn propensity and digital onboarding rates, making the capital the bellwether for plan innovation. Rural 5G coverage completion removes a past barrier and opens a unified addressable base.

Roughly 9.5 million MVNO lines translate to a 16.7% share of national mobile subscriptions. Industrial coastal clusters at Gwangyang, Pohang, and Ulsan leverage private 5G to automate heavy manufacturing, driving enterprise SIM expansion. Cross-border growth plays are surfacing: FreeTelecom’s Telus partnership shows how Korean MVNO know-how can transfer abroad, while Starlink’s impending launch promises a redundancy layer for remote maritime coverage.

Competitive Landscape

Twelve active operators create a fragmented competitive field. KB Liiv M, KT M Mobile, and U+-anchored carriers collectively keep individual shares below 5%, while fintech-backed Toss Mobile leverages a KRW 2 trillion fintech ecosystem to cut acquisition costs. Repeal of the Device Distribution Improvement Act in July 2025 is set to intensify handset-bundled promotions, and eSIM portals will lower entry hurdles for digital-native challengers.

Differentiation leans on vertical focus. StageFive’s all-you-can-use roaming bundle spans 140 nations and relies on proprietary OSS/BSS, pushing the brand to 162% revenue growth year-on-year. White-space opportunities persist in industrial IoT connectivity and satellite-backed rural coverage, encouraging specialized entrants to carve defensible niches within the broader South Korea MVNO market.

South Korea Mobile Virtual Network Operator (MVNO) Industry Leaders

SK Telink Corporation

KT M Mobile Co., Ltd.

CJ Hello Mobile (LG HelloVision Co., Ltd.)

Korea Cable Telecom Co., Ltd. (freeT)

Sejong Telecom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Roughly 20 low-cost 5G bundles launched at 10,000 KRW with 20 GB data, trimming consumer spend by 400,000 KRW annually and adding 100+ daily sign-ups.

- March 2025: MSIT shifted spectrum allocation to a demand-driven model, mandating 100% upfront payment for new mobile blocks.

- February 2025: StageFive unveiled the first unlimited global eSIM roaming product, covering 140 nations at 9,600 KRW for a 3-day Asia pass.

- January 2025: Starlink’s Korean entry neared completion, initially providing Wi-Fi via terminal devices while direct-to-cell capability remains in testing.

South Korea Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the South Korea MVNO market in 2025?

The sector is valued at USD 2.43 billion in 2025 and is set to climb to USD 3.07 billion by 2030.

What CAGR is forecast for South Korea MVNO revenue to 2030?

The market is projected to expand at a 4.77% compound annual growth rate over the period.

Which deployment model dominates operator infrastructure?

Cloud platforms represent 77.93% of deployments, favored for rapid scaling and lower capital needs.

Why are enterprise SIMs important to future growth?

Private 5G and IoT projects push enterprise lines toward a 33.62% CAGR, adding high-value contracts.

How will the July 2025 subsidy law repeal affect competition?

Removal of subsidy caps gives MNO sub-brands leeway to offer aggressive bundles, increasing churn potential toward both incumbents and agile MVNOs.

What role does eSIM technology play in subscriber acquisition?

ESIM adoption exceeds 80% among MVNO users, enabling instant digital activation and slashing distribution costs, bolstering operator margins.

Page last updated on: