Netherlands Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

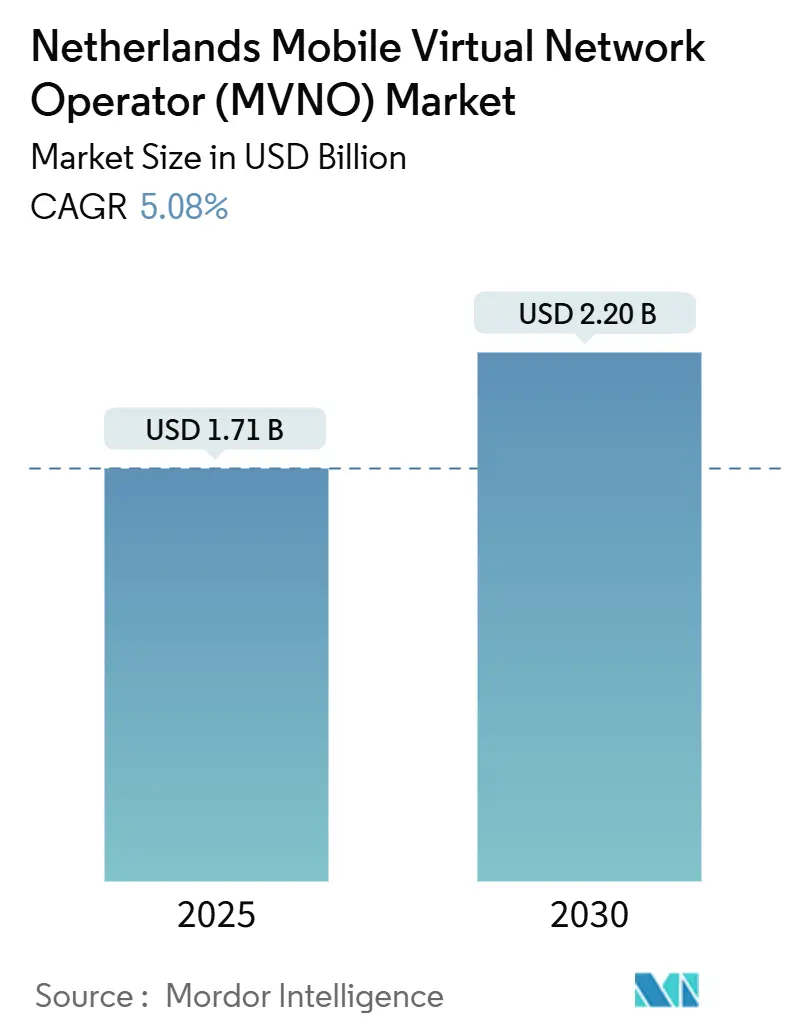

| Market Size (2025) | USD 1.71 Billion |

| Market Size (2030) | USD 2.20 Billion |

| Growth Rate (2025 - 2030) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Netherlands Mobile Virtual Network Operator Market size is estimated at USD 1.71 billion in 2025, and is expected to reach USD 2.20 billion by 2030, at a CAGR of 5.08% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 2.84 million Subscribers in 2025 to 3.33 million Subscribers by 2030, at a CAGR of 3.27% during the forecast period (2025-2030).

Robust expansion stems from favorable wholesale access regulation, accelerated 5G deployment, and mounting demand for cost-effective plans that together reinforce the Netherlands MVNO market as a testing ground for digital-first connectivity strategies. Competitive repositioning, exemplified by KPN’s 2024 acquisition of Youfone, signals a shift toward scale-driven synergies, while rising IoT and eSIM adoption open white-space segments for niche operators. At the same time, pervasive network quality expectations, lofty spectrum costs, and intensifying price competition continue to squeeze margins, compelling operators to differentiate on service quality rather than tariffs.

Key Report Takeaways

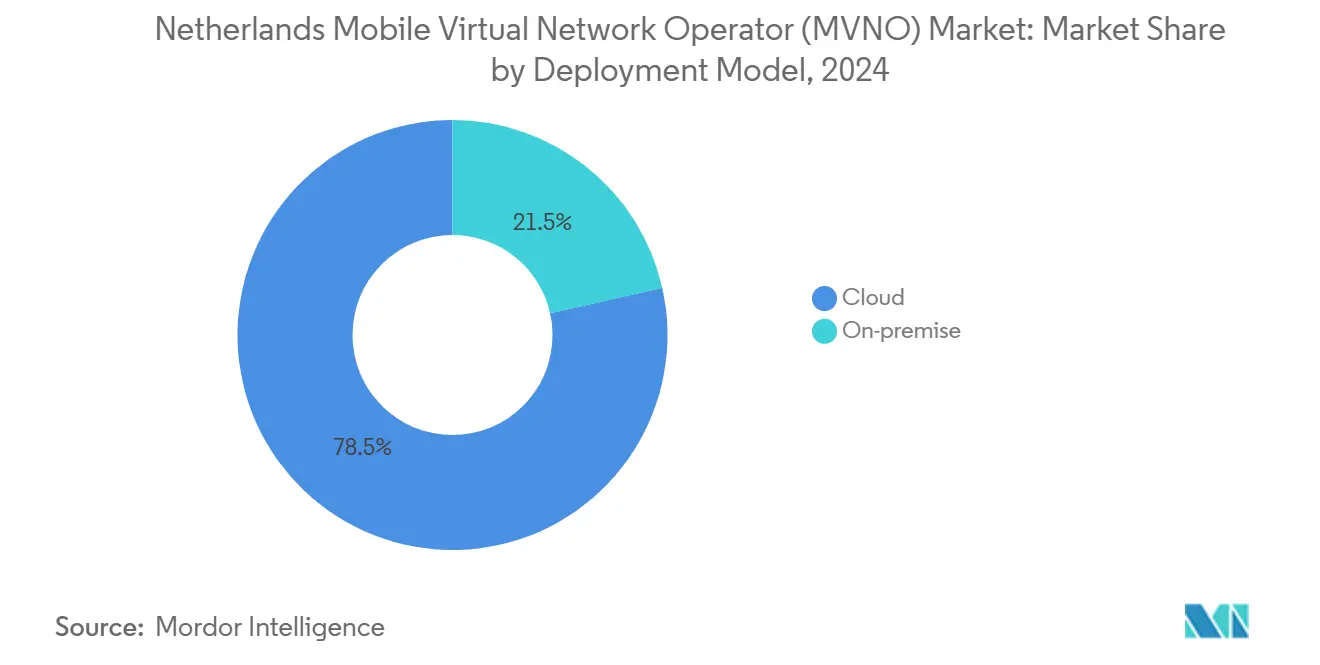

- By deployment model, cloud-based solutions commanded 78.50% of the Netherlands MVNO market share in 2024, and it is expected to drive the growth at a 7.50% CAGR to 2030.

- By operational mode, resellers/light/ brand MVNO commanded 47.29% of the Netherlands MVNO market share in 2024, while full MVNOs are projected to expand at a 12.65% CAGR through 2030.

- By subscriber type, consumer users held 76.40% of the Netherlands MVNO market size in 2024, while IoT-specific connectivity is forecast to climb at a 19.24% CAGR to 2030.

- By application, discount commanded 37.22% of the Netherlands MVNO market share in 2024, while cellular M2M is projected to expand at a 15.79% CAGR through 2030.

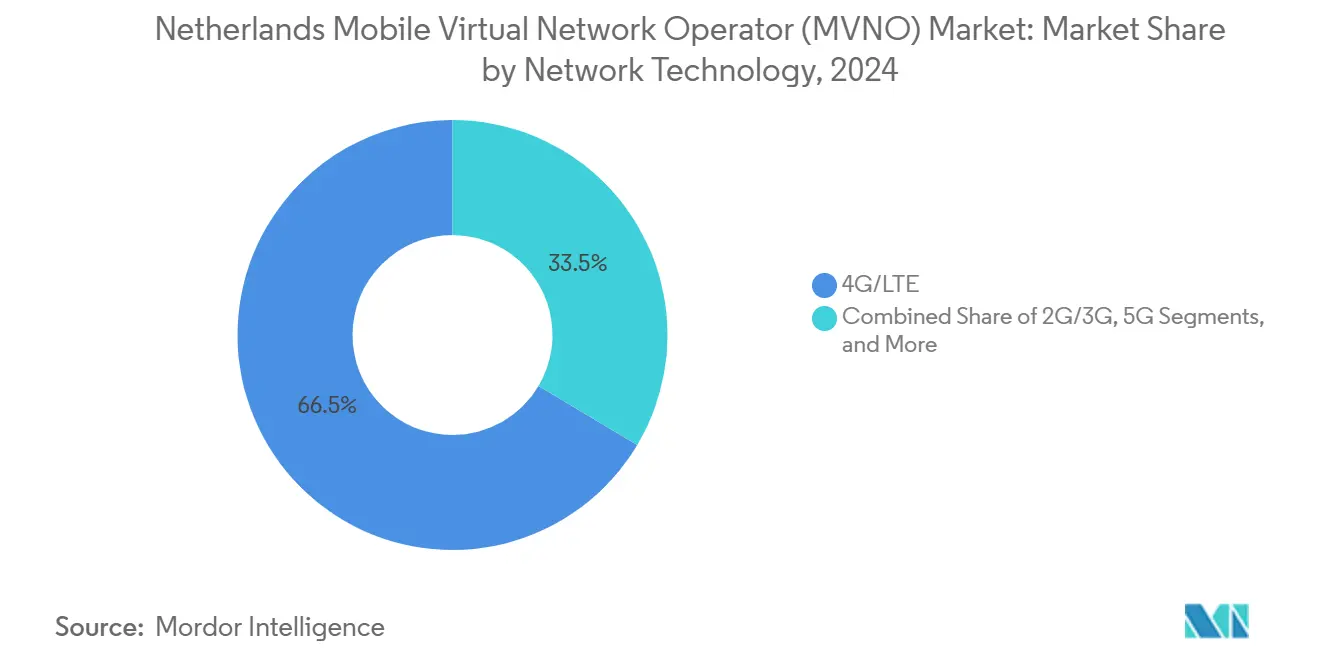

- By network technology, 4G/LTE commanded 66.46% of the Netherlands MVNO market share in 2024, and satellite/NTN solutions are poised for an 84.45% CAGR from 2025-2030.

- By distribution channel, online / digital-only commanded 58.16% of the Netherlands MVNO market share in 2024, and it is expected to drive the growth at a 8.10% CAGR to 2030.

Netherlands Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for cost-effective mobile plans | +1.2% | Urban clusters nationwide | Short term (≤ 2 years) |

| Accelerated 5G rollout and favorable wholesale terms | +0.9% | Randstad leadership | Medium term (2-4 years) |

| Rising IoT/M2M connectivity needs | +0.8% | Industrial corridors | Long term (≥ 4 years) |

| eSIM adoption catalyzing digital-only brands | +0.7% | Tech-savvy demographics | Medium term (2-4 years) |

| Corporate appetite for private mobile networks | +0.6% | Enterprise hubs | Long term (≥ 4 years) |

| Government connectivity-inclusivity programs | +0.4% | Socio-economically challenged zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G rollout and favorable wholesale terms lowering entry barriers

Completion of the 3.6 GHz auction increased 5G spectrum supply and improved wholesale pricing, allowing MVNOs to access near-1 Gbps downlink speeds and 14 ms latency on KPN’s standalone network [1]Juan Pedro Tomás, “Dutch carrier KPN tests 5G SA technology,” RCR Wireless News, rcrwireless.com. Opensignal’s 78.8 score for Odido underscores the quality that MVNOs can now commercialize, while ACM mandates force non-discriminatory access, eliminating legacy bottlenecks. Lower upfront fees for spectrum-enabled wholesale packages let challenger brands pivot from mere reselling toward enterprise-grade offerings that once required costly core deployments.

Rising IoT/M2M connectivity needs spurring specialist MVNO offerings

KPN IoT already manages 12 million M2M SIMs across 195 countries, signaling explosive machine-centric demand. Enterprises shifting from LPWAN to private LTE rely on specialist MVNOs for device lifecycle management, secure VPNs, and vertical-specific analytics. Partnerships such as Ukkoverkot and V&M Telecom’s band-42 private LTE license highlight a corporate willingness to invest in dedicated connectivity, expanding the Netherlands MVNO market beyond consumer voice-data toward industrial automation and smart-agriculture niches.

eSIM adoption enabling digital-only challenger brands to scale rapidly

Global eSIM connections are projected to hit 1 billion smartphones by 2025 and 6.9 billion by 2030 [2]Gregory Gundelfinger, “Positioning for Success in the eSIM Era,” thefastmode.com. Youfone’s April 2025 eSIM launch showed how digital onboarding slashes physical distribution cost and accelerates customer acquisition. Vodafone’s partnership with eSIM Go adds a platform approach that could spawn dozens of micro-MVNOs, intensifying fragmentation. For the Netherlands MVNO market, eSIM lowers switching friction, forcing incumbents to double-down on loyalty-driven perks and seamless app experiences.

Corporate demand for private mobile networks driving enterprise-MVNO partnerships

After KPN unveiled private 5G services tailored to factories and logistics sites, enterprises recognized that mission-critical traffic requires deterministic performance unattainable on public slices. TowerCo, KPN’s infrastructure spin-off with pension fund ABP, creates neutral-host assets that MVNOs can lease for localized coverage, enabling premium SLAs. As a result, enterprise MVNO contracts now include security, quality of service dashboards, and on-prem edge nodes, creating new revenue lines insulated from consumer price wars.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price competition squeezing ARPU | –0.8% | Nationwide consumer market | Short term (≤ 2 years) |

| High dependency on host MNO network quality | –0.6% | Varies by MNO | Medium term (2-4 years) |

| Stringent KYC/AML rules raising onboarding friction | –0.4% | Prepaid segments | Short term (≤ 2 years) |

| IPv4 scarcity and costly IPv6 migration | –0.3% | Legacy platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying price competition squeezing ARPU and margins

SIM-only offers start at EUR 4.50 per month, while inflation-related wholesale hikes continue, eroding margins. Odido’s 3.2% price increase in 2025 has not translated into proportional retail uplift due to aggressive discounting, forcing MVNOs into razor-thin profitability. Private-equity interest in Lebara underscores the financial pressure on voice-centric models now cannibalized by OTT apps.

High dependency on host MNO network quality and commercial terms

Odido’s nationwide outage in August 2025 blocked services for Simpel and Ben, underlining wholesale vulnerability. Consolidation, such as KPN’s acquisition of Youfone, narrows the pool of host networks, weakening MVNO bargaining power. New EU cost models on roaming rates add further uncertainty to long-term wholesale agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure drives digital transformation

Cloud-based deployments accounted for 78.50% of 2024 revenue, reflecting how software-defined cores let operators spin up services within weeks rather than quarters. Netherlands MVNO market size for cloud platforms is projected to expand at a 7.50% CAGR to 2030 as AI-driven billing and self-service portals grow mainstream [3]Netcracker Technology, “Supports Odido's Fixed-Wireless Access Launch,” netcracker.com. On-premise remains relevant for government contracts requiring strict data residency, yet faces capex hurdles that tilt new entrants toward pay-as-you-grow clouds.

Cloud dominance also enables multi-tenant slicing and low-touch onboarding, crucial for Netherlands MVNO market differentiation in IoT and enterprise verticals. Netcracker’s partnership with Odido on fixed-wireless access underscores how BSS delivered as SaaS accelerates time-to-revenue, allowing MVNOs to monetize 5G hotspots and edge services without owning towers.

By Operational Mode: Full MVNO model gains strategic momentum

Light-MVNOs held 47.29% share in 2024, but full-MVNOs are on track for 12.65% CAGR through 2030 as brands seek autonomy over numbering resources and IMS cores. Netherlands MVNO market share improvements stem from operators upgrading to full cores to manage eSIM activation, policy control, and convergent charging.

Migration incentives include rising wholesale voice-termination fees and the need for differentiated quality of service. ACM obliges MNOs to provide access to signaling and RAN sharing, easing technical hurdles. The result is a ladder-of-investment where successful resellers emulate Youfone’s scale play before eventual exits or acquisitions.

By Subscriber Type: IoT-specific connectivity emerges as growth engine

Consumer plans represent 76.40% of 2024 revenue, yet IoT connections are forecast for a 19.24% CAGR to 2030, making them the fastest addition to the Netherlands MVNO market size. Enterprises in logistics and agriculture demand managed SIM lifecycle tools and API-based provisioning that generalized consumer MVNOs seldom provide.

Specialist MVNOs leverage low-power modules and multi-IMSI profiles to guarantee coverage across 600+ roaming partners, addressing device uptime SLAs. Consumer growth stabilizes as penetration nears saturation; hence, operators hedge churn with machine-centric revenue that carries multi-year contracts and lower support overhead.

By Application: Cellular M2M applications drive innovation

Discount plans retained 37.22% of 2024 revenue, mirroring the price-sensitive Dutch consumer landscape. However, cellular M2M applications are cited for a 15.79% CAGR, propelled by smart-meter rollouts and industrial robotics. The Netherlands MVNO market size related to cellular M2M extends beyond SIM sales to include device management portals and embedded analytics.

Business applications ranging from POS terminals to field-force tablets provide steady ARPU and cross-sell opportunities for data security add-ons, while “other” use cases, such as AR and edge gaming, remain emergent, awaiting broader 5G SA coverage.

By Network Technology: Satellite/NTN prepares for connectivity revolution

4G/LTE delivered 66.46% of 2024 traffic, reflecting its wide footprint and cost efficiency. Yet satellite/NTN links are projected for 84.45% CAGR, riding on lower launch costs and 3GPP Release 17 convergence [4]Barbara Pareglio, “Mobile and Satellite Convergence,” satellitetoday.com . Netherlands MVNO market participants partner with LEO constellations to offer fallback coverage for maritime and logistics customers, adding resiliency against terrestrial outages.

5G adoption advances via carrier aggregation and network slicing, enabling premium plans for cloud gaming and remote surgery, while 2G/3G sunsets free spectrum for rural 5G FWA solutions.

By Distribution Channel: Digital-only models reshape customer acquisition

Online channels captured 58.16% share in 2024 and are forecast for 8.10% CAGR, benefiting from eSIM click-to-activate journeys. Netherlands MVNO market economics favor digital brands that avoid shop rents and leverage chatbots for Tier-1 support. Physical stores persist for handset-bundle buyers and senior citizens, but their share shrinks as omnichannel experiences move from bricks to clicks.

Lyca Mobile’s in-app top-ups and eKYC show how legacy ethnically-focused MVNOs refresh relevance. Carrier sub-brands experiment with pop-up kiosks, blending low-cost operations with branding consistency.

Geography Analysis

Although compact and densely networked, the Netherlands contains micro-markets shaped by socioeconomic profiles rather than physical distance. Randstad’s tech corridor commands the lion’s share of early 5G SA deployments, making it fertile ground for enterprise MVNO pilots and high-ARPU data plans. Rural provinces see growing interest in hybrid satellite-terrestrial bundles where deep-indoor or offshore coverage gaps persist.

Government proposals for EUR 16 social tariffs could open 0.4 million low-income households to entry-level services, yet they may pressure the Netherlands MVNO market pricing floors. For roaming-dependent expatriate populations, Amsterdam remains a distribution hub for travel eSIMs that auto-switch across EU operators, enhancing cross-border stickiness.

The nation’s digital backbone enables MVNOs to deploy analytics at city scale, informing hyper-local promotions. Equally, harmonized EU regulation about wholesale roaming fees facilitates Dutch MVNO expansion abroad, turning home-market operational excellence into a springboard for pan-European growth.

Competitive Landscape

The Netherlands MVNO market features moderate concentration: the top five operators hold roughly 55% combined revenue. KPN’s Youfone buyout pushed its mobile share to 34% and demonstrated valuation premiums for scale and brand equity.

Strategic differentiation pivots on eSIM support, IoT orchestration, and white-label platforms. Vodafone’s collaboration with Gigs allows near-instant MVNO launches, lowering barriers for micro-segments from student collectives to sports-fan communities. Meanwhile, dependency risks surfaced when Odido’s outage sidelined Simpel and Ben, prompting some digital-only players to negotiate multi-IMSI redundancy.

Looking forward, Liberty Global’s interest in VodafoneZiggo could spawn fresh wholesale relationships or tighten network access, while private-equity backing for Lebara signals capital chasing consolidation plays. Niche IoT MVNOs, buoyed by long-term industrial contracts, may become attractive takeover targets for infrastructure funds hungry for predictable cash flows.

Netherlands Mobile Virtual Network Operator (MVNO) Industry Leaders

Lebara B.V.

Lycamobile

Youfone Nederland B.V.

Simpel B.V.

Hollandsnieuwe (Vodafone Libertel BV)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Liberty Global opened talks to buy Vodafone’s stake in VodafoneZiggo.

- January 2025: GroenLinks-PvdA proposed compulsory low-cost internet subscriptions at EUR 16 for low-income users, targeting all major operators.

- December 2024: Odido raised mobile and fixed prices by 3.2% due to inflation adjustment.

- August 2024: Lebara partnered with Waterland Private Equity to accelerate European expansion.

- April 2024: Youfone introduced eSIM onboarding, streamlining customer acquisition.

Netherlands Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the estimated value of the Netherlands MVNO segment in 2025?

It is valued at USD 1.71 billion in 2025.

What annual growth rate is projected for the sector through 2030?

A 5.08% CAGR is forecast, taking revenue to USD 2.20 billion by 2030.

Which deployment model currently dominates revenue?

Cloud-based deployments accounted for 78.50% of 2024 revenue and continue to lead.

Which subscriber category is expanding the quickest?

IoT-specific connections are projected to rise at a 19.24% CAGR through 2030.

Why are operators shifting toward full-MVNO status?

Full MVNOs gain greater control over numbering resources, service quality, and revenue, supporting a 12.65% CAGR to 2030.

How is eSIM adoption reshaping competitive strategy?

ESIMs enable instant digital onboarding and lower distribution costs, letting challenger brands scale without physical stores.

Page last updated on: