Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

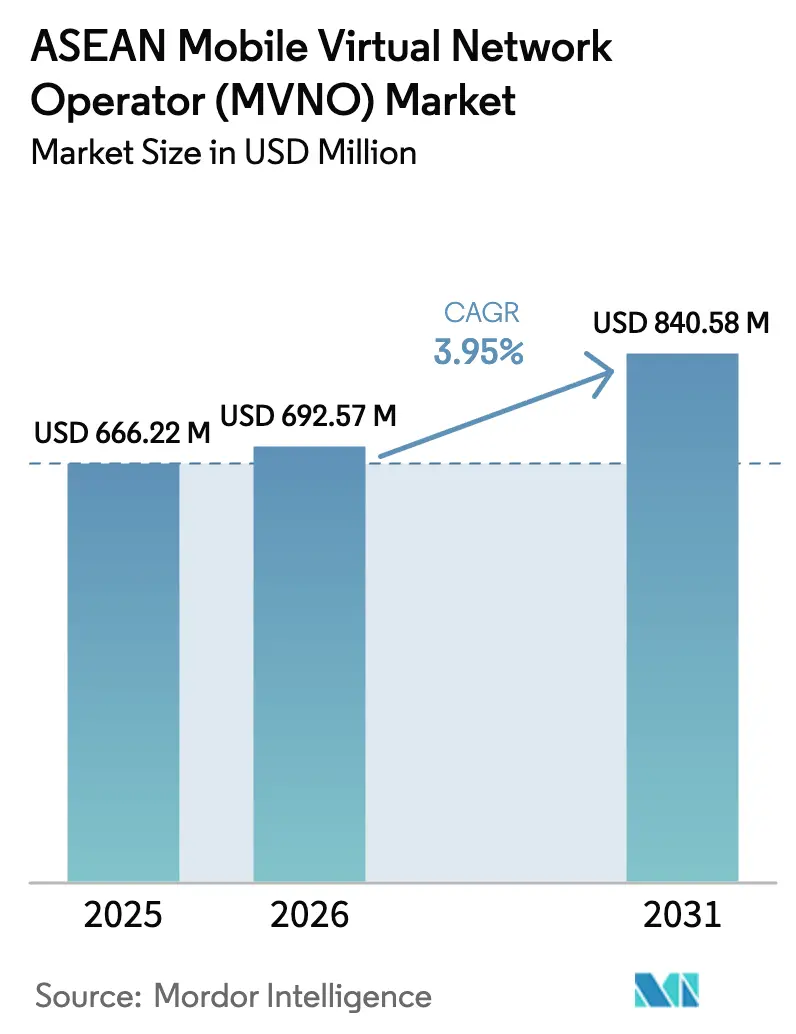

| Base Year Market Size (2025) | USD 666.22 Million |

| Market Size (2026) | USD 692.57 Million |

| Market Size (2031) | USD 840.58 Million |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The ASEAN MVNO market size is expected to grow from USD 666.22 million in 2025 to USD 692.57 million in 2026 and is forecast to reach USD 840.58 million by 2031 at 3.95% CAGR over 2026-2031. Wholesale-access mandates in Thailand, Vietnam, and Malaysia are unlocking unused 5G capacity, while bank-branded virtual operators are entering with bundled financial and connectivity services. Cloud-native BSS and OSS platforms shorten launch cycles, enabling new entrants to reach market in under 100 days. Competitive pressure from MNO sub-brands keeps retail prices low, shifting MVNO differentiation toward vertical solutions such as IoT fleet management and migrant-worker roaming bundles. Satellite-to-cell partnerships promise future reach into remote archipelagos, though current bandwidth costs limit adoption to low-data-use cases.

Key Report Takeaways

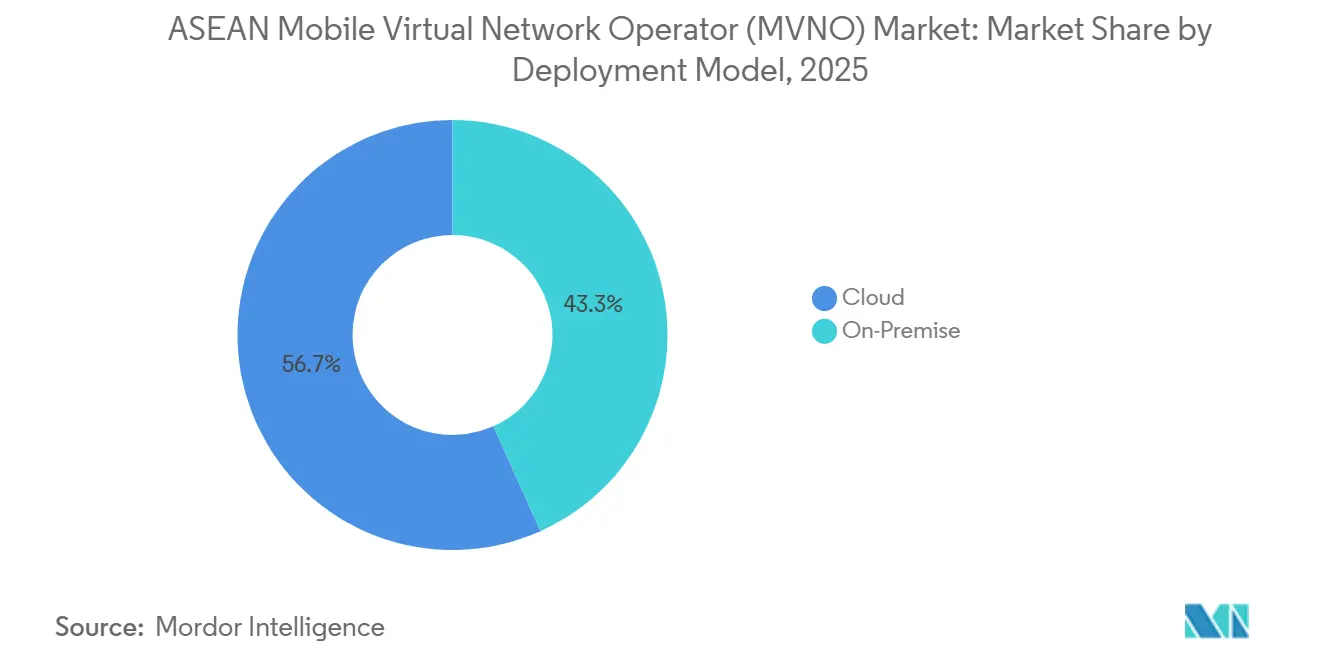

- By deployment model, cloud platforms held 56.71% of the ASEAN MVNO market share in 2025, while the segment is projected to expand at a 4.58% CAGR through 2031.

- By operational mode, reseller configurations led with a 38.57% share in 2025, whereas full MVNO setups are the fastest-growing at a 4.91% CAGR over 2026-2031.

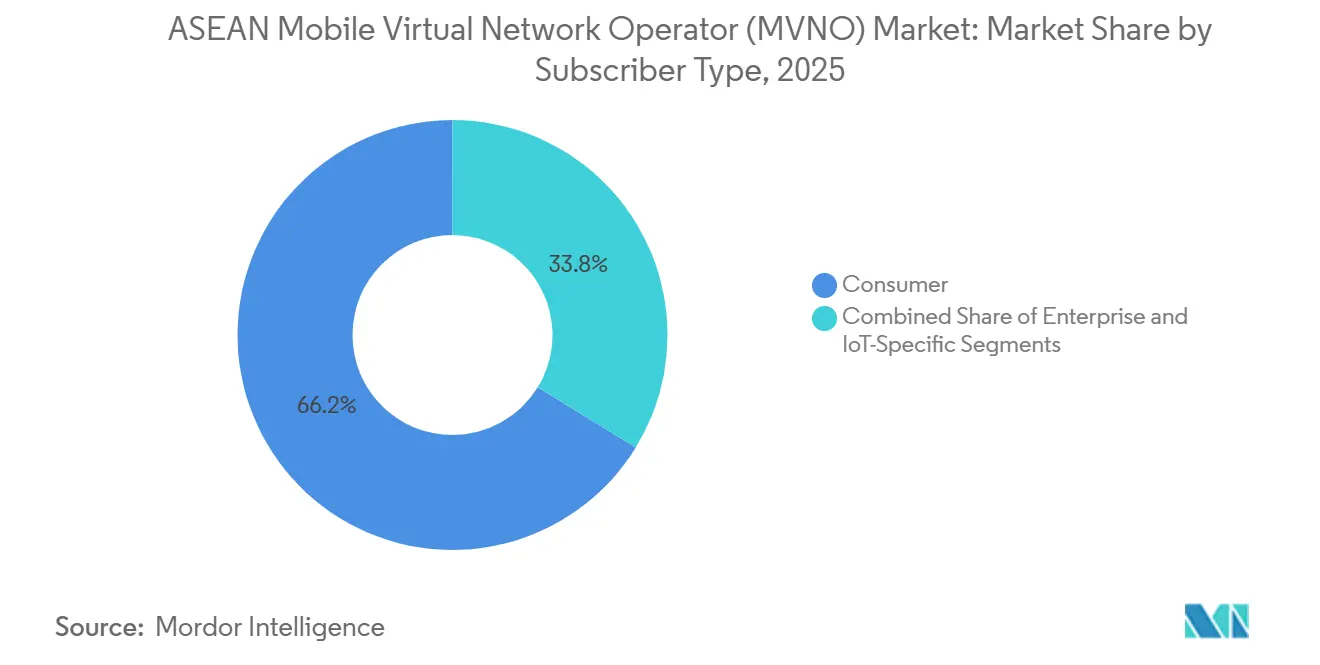

- By subscriber type, consumer lines accounted for a 66.23% share in 2025, and IoT-specific plans are expected to rise at a 4.22% CAGR to 2031.

- By application, discount offerings commanded a 28.71% share in 2025, yet cellular M2M connections are on track for the highest CAGR of 4.53%.

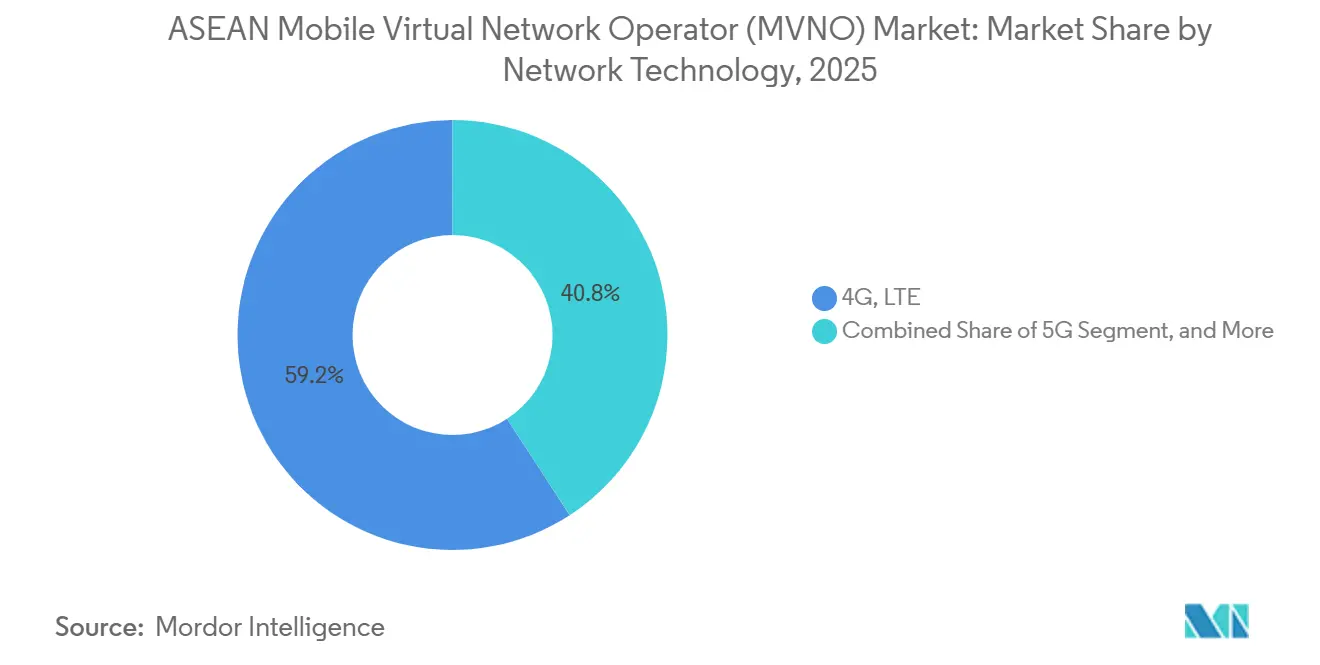

- By network technology, 4G and LTE services represented a 59.18% share in 2025, while 5G subscriptions are forecast to expand at a 5.01% CAGR.

- By distribution channel, online and digital-only sales accounted for 44.06% of sales in 2025, with this route projected to grow at a 5.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mobile-Subscriber Base and Smartphone Penetration | +1.20% | ASEAN-wide, strongest in Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Demand for Low-Cost Voice and Data Plans | +0.90% | ASEAN-wide, concentrated in Thailand, Indonesia, Philippines | Short term (≤ 2 years) |

| Expansion of IoT, M2M Connections | +1.00% | Singapore, Malaysia, Thailand urban corridors; spillover to Indonesia logistics hubs | Medium term (2-4 years) |

| Regulatory Push for Open Wholesale Access and eSIM-Enabled Entry | +0.80% | Thailand, Vietnam, Malaysia | Short term (≤ 2 years) |

| Fintech and Telco Convergence Spawning Bank-Branded MVNOs | +0.50% | Malaysia, Singapore, Thailand | Medium term (2-4 years) |

| Satellite-to-Cell Partnerships Enabling Global MVNO Coverage | +0.30% | Indonesia, Philippines archipelagos; rural Thailand, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile-Subscriber Base and Smartphone Penetration

ASEAN counted more than 450 million mobile broadband lines in 2025, led by Vietnam with 104.7 million subscriptions under three dominant networks that control over 90% of capacity.[1]GSMA Intelligence, “Mobile Economy Asia Pacific 2024,” gsma.com Urban smartphone penetration already tops 80 percent in Singapore, Malaysia, and Thailand, but lower-income and rural zones across Indonesia and the Philippines still rely on prepaid data packs, creating headroom for value-driven MVNOs. Youthful demographics median age below 30 across key markets propel data usage that outpaces voice traffic, so virtual operators design plans centered on large data buckets and minimal voice minutes. Historical data show every 1-percentage-point uptick in smartphone penetration adds roughly 1.5 points to MVNO subscriber growth, reinforcing the positive feedback loop. As standalone 5G rolls out, MVNOs can launch differentiated low-latency services, yet adoption lags in areas where 4G coverage remains incomplete, preserving the near-term role of LTE networks.

Demand for Low-Cost Voice and Data Plans

Average monthly ARPU ranges between USD 5 and USD 8 in Indonesia and the Philippines, compared with USD 15-20 in Singapore, so price competition is acute. Discount MVNOs captured 28.71% of applications in 2025 by marketing prepaid SIMs with 100-300 GB for the local equivalent of USD 5-15, undercutting MNO sub-brands. Migrant workers about 10 million region-wide favour unlimited international calls and regional roaming, niches that global brands exploit with bundled remittance services. Thailand’s 20% wholesale-fee reduction scheduled for 2026 will widen retail price headroom, but sustained undercutting lengthens subscriber payback periods to 18-24 months, stretching cash flow. Operators therefore bundle data rollover or loyalty rewards to lift effective ARPU without headline price hikes.

Expansion of IoT and M2M Connections

Cellular IoT links exceeded 50 million devices in 2025, with NB-IoT live in Indonesia, Malaysia, Singapore, and Vietnam.[2]5G Americas, “Cellular IoT in Asia Pacific,” 5gamericas.org Tata Communications reported fleet SIM growth above 40% year-over-year as trucking firms demand cross-border roaming across Thailand-Malaysia-Singapore corridors.[3] Automotive brands embedding eSIMs negotiate wholesale terms directly, bypassing resellers and unlocking a fresh MVNO revenue pool. Utilities in Singapore and Malaysia deploy NB-IoT meters, though fragmented spectrum plans complicate multi-country rollouts. Forthcoming 5G RedCap modules will support higher-bandwidth industrial sensors, broadening the addressable slice of the ASEAN MVNO market.

Regulatory Push for Open Wholesale Access and eSIM-Enabled Entry

Thailand’s “One Region, One MVNO” program obliges each facilities-based operator to host at least one regional MVNO per zone and cuts wholesale fees by 20 percent, lowering entry barriers. Vietnam’s Telecommunications Law 2023 eases licensing by requiring only financial fitness and signed network agreements, rather than full facilities build. Malaysia’s biennial Mandatory Standard on Access Pricing gives virtual operators cost predictability during contract negotiations. Singapore relies on market forces, yet competition from a fourth network prompted incumbents to open wholesale channels voluntarily, resulting in more than 10 active MVNOs by 2025. Divergent eSIM rules digital onboarding allowed in Singapore but still physical in Indonesia create short-term complexity, but pioneers who master local compliance gain first-mover advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Squeeze from Intense Price Competition | -0.70% | ASEAN-wide, acute in Singapore, Malaysia | Short term (≤ 2 years) |

| Dependence on Host MNOs for Network Quality and Wholesale Fees | -0.50% | ASEAN-wide, critical in Thailand, Vietnam | Medium term (2-4 years) |

| Device-OEM Control of eSIM Ownership Bypassing MVNO Model | -0.30% | Singapore, Malaysia; emerging in Thailand | Medium term (2-4 years) |

| Private-Spectrum Sharing Lets Enterprises Self-Provision Service | -0.20% | Singapore, Malaysia industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Squeeze from Intense Price Competition

MNO digital brands such as GOMO and Giga price 100-300 GB plans at SGD 10-18, matching independent MVNO offers while enjoying network cost advantages. Wholesale fees absorb up to 60% of MVNO retail revenue, leaving slender 15-20% gross margins after marketing and support. Singapore saw multiple shutdowns between 2023 and 2025 because acquisition costs of SGD 40-60 per user demanded two-year payback periods that cash-strapped entrants could not sustain. Malaysia’s dual 5G network introduces official price oversight, yet disclosed contracts show host operators still retain rate-setting leverage. Minimum-guarantee clauses penalize under-utilization, prompting virtual operators to pivot toward higher-value enterprise and IoT niches where volume commitments align with predictable demand.

Dependence on Host MNOs for Network Quality and Wholesale Fees

MVNO traffic often receives lower priority than host-network retail traffic, so speeds can drop during congestion, driving customer churn. OpenSignal tests found download-speed gaps between StarHub retail users and its hosted MVNOs, confirming the risk. Thailand’s fee-cut mandate does not ensure service-level parity, leaving virtual operators exposed to throttling during upgrades. Contract renegotiations add operational risk; Lycamobile’s 2025 U.S. network switch triggered 15-20% subscriber losses during SIM swaps. Full MVNO models that deploy their own core allow better QoS control yet require USD 5-10 million in capital and specialized talent that smaller entrants may not raise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Platforms Compress Launch Cycles

Cloud-hosted solutions captured 56.71% of the ASEAN MVNO market share in 2025, and the ASEAN MVNO market size for cloud deployments is forecast to expand at a 4.58% CAGR through 2031. Reduced capital outlay shift from USD 3-5 million upfront to pay-as-you-grow operating expense has convinced many start-ups to adopt AWS, Azure, or Google Cloud for BSS and OSS. MyRepublic launched in just 90 days after migrating to Tata Communications’ cloud stack, whereas on-premises builds require up to 18 months. Single-tenant cloud instances also simplify multi-country expansion because localization modules plug in quickly, which is critical for pan-ASEAN growth strategies. On-premises systems still hold 56.71% share because full MVNOs and regulated verticals prefer local data custody and ultra-low latency. Circles.Life trimmed per-subscriber costs by almost 40% after shifting to a cloud-native core in 2024, an efficiency that is hard for legacy deployments to replicate. Regulatory nuances matter: Indonesia’s data-sovereignty rules oblige certain data classes to reside domestically, so hybrid clouds that keep billing in-country while running CRM in public cloud will dominate the transition period. Looking ahead, over 70% of new ASEAN MVNO market launches are expected to be cloud-first by 2028, reflecting a strategic pivot from hardware ownership to service orchestration.

The competitive payoff is speed and flexibility. Cloud APIs support rapid integration of value-added apps mobile payments, content streaming, or IoT dashboards allowing virtual operators to refresh offers weekly rather than quarterly. However, vendor lock-in is emerging as a concern since migrating between clouds could cost 20-30% of annual IT spend, offsetting some agility gains. Operators are experimenting with multi-cloud for redundancy, though added complexity may outweigh benefits for smaller teams. Overall, cloud adoption is redefining cost structures and lowering entry barriers, intensifying rivalry within the ASEAN MVNO market.

By Operational Mode: Full MVNOs Gain Margin Control

Reseller models led with 38.57% share in 2025, yet the ASEAN MVNO market size for full MVNO configurations is projected to grow at a 4.91% CAGR to 2031. Resellers thrive on simplicity, purchasing bulk minutes and data, then rebranding, which keeps initial investment under USD 1 million. Still, they surrender control over routing, quality of service, and wholesale costs. As price competition intensifies, virtual operators are upgrading to full MVNO status, installing HLRs, packet gateways, and policy engines to reclaim margin and service differentiation. Circles.Life and StarHub’s giga illustrate the shift, each adding core-network elements to manage QoS and launch value-added features like private APN for enterprises. Service Operator and Light/Brand MVNOs provide a middle path, balancing cost with limited differentiation, but growth rates lag the full MVNO frontier.

Capital remains the hurdle: basic core deployments need USD 5-10 million and skilled engineers, so many entrants partner with managed-service providers who amortize infrastructure across multiple clients. Regulatory changes help; Thailand and Vietnam mandate open wholesale access, giving would-be full MVNOs better bargaining power to justify investment. Profitability evidence is building early movers report gross margins rising from 20 percent as resellers to near 35 percent after full migration. Consequently, the share of full MVNOs in the ASEAN MVNO market is expected to overtake resellers after 2029, pushing the industry toward deeper vertical integration.

By Subscriber Type: IoT Plans Unlock B2B Revenue

Consumer lines accounted for 66.23% share in 2025, yet the ASEAN MVNO market size attached to IoT-specific plans is on course for a 4.22% CAGR through 2031. Price-driven consumer segments show high churn 25-30% annually in Singapore because plan switching costs are minimal. Enterprise subscriptions, although lower in count, command double the average revenue per user by bundling device management, VPN, and SLA backing. IoT plans, even at USD 1-3 per SIM, reach profitability via sheer scale; a logistics fleet may activate tens of thousands of trackers under a single contract. Tata Communications’ MOVE platform recorded more than 40% annual growth in ASEAN fleet SIMs during 2025, demonstrating strong latent demand.

Telematics and smart-meter deployments illustrate use-case breadth: BYD vehicles shipping into Thailand embed eSIMs for over-the-air updates, while utilities in Singapore meter water consumption every 15 minutes over NB-IoT. Consumer ARPU stagnates because discount MVNOs continually undercut each other, so operators diversify into enterprise and IoT to stabilize earnings. Regulatory compliance adds complexity data localization, cybersecurity audits but also raises switching barriers, locking in corporate accounts. As 5G RedCap modules mature, video telematics and industrial sensors will need higher throughput, expanding the revenue ceiling for IoT-focused virtual operators across the ASEAN MVNO market.

By Application: M2M Monetizes Vertical Use Cases

Discount offerings captured 28.71% of the ASEAN MVNO market share in 2025, yet the ASEAN MVNO market size attributable to cellular M2M is projected to expand at a 4.53% CAGR through 2031. Logistics operators in Thailand, Malaysia, and Singapore already connect more than 2 million trailers and delivery vans via pooled-data SIMs that cut roaming costs by 15-20% compared with MNO retail plans. Utilities embrace NB-IoT meters that transmit hourly readings, while industrial players pilot LTE-M sensors for asset tracking inside factories. Discount consumer plans remain relevant during economic slowdowns, but MNO sub-brands now match headline pricing, leaving razor-thin margins. Roaming bundles aimed at cross-border travellers face disruption from eSIM marketplaces that sell instant activation at 30-50% lower rates, forcing MVNOs to wrap travel insurance or streaming add-ons to protect revenue streams. The upshot is a clear pivot: virtual operators are building sector-specific M2M platforms complete with cloud dashboards and API hooks because they deliver sticky multi-year contracts instead of promotional churn.

Cellular M2M’s momentum also stems from regulatory push: Singapore mandates advanced electricity metering by 2028, while Malaysia’s Energy Commission requires smart gas meters for new industrial sites by 2027, guaranteeing device-volume growth. Automotive telematics expands as Chinese and Korean OEMs localize assembly plants across ASEAN, embedding eSIMs for diagnostics and over-the-air updates. Airlines and maritime operators test satellite-hybrid SIMs that roam seamlessly between terrestrial 5G and LEO constellations, a use case that single-network resellers cannot match. These vertical integrations illustrate how the ASEAN MVNO market is evolving from generic consumer discounts toward specialized connectivity platforms that monetize data flows inside industry ecosystems.

By Network Technology: 5G Unlocks Service Innovation

4G and LTE dominated with 59.18% share in 2025, but the ASEAN MVNO market size for 5G subscriptions is forecast to rise at a 5.01% CAGR to 2031. Circles. Life launched 5G standalone plans with latency below 10 milliseconds for cloud gaming and AR during February 2025, proving that MVNOs can differentiate on quality rather than price alone. Malaysia’s U Mobile and Eastel agreement grants virtual access to nationwide 5G, positioning Eastel to sell network-slicing SLAs to fintech and media firms. Legacy 2G/3G networks will shut down across Singapore, Malaysia, and Thailand by 2028, freeing spectrum for LTE refarming and pushing low-data IoT devices to NB-IoT bands. Satellite-to-cell services bring a parallel path: Starlink’s beta allows smartphones to connect directly in remote Indonesian islands, expanding nominal coverage but at bandwidth costs 5-10× terrestrial wholesale prices, so early deployments stay limited to emergency messaging.

For MVNOs, 5G economics remain challenging; wholesale 5G capacity costs roughly 25% more than LTE, squeezing margins unless enterprises pay premiums for guaranteed throughput. Yet standalone cores enable network slicing, letting a virtual operator carve a private lane for a factory at fixed megabit rates and charge a service markup. As 5G RedCap chipsets enter mass production in 2027, mid-tier industrial sensors will migrate from LTE, raising total addressable SIM volume. Consequently, MVNOs that lock in early slice agreements with host networks can secure multi-year revenues insulated from consumer price wars, cementing 5G’s role as a profit lever inside the ASEAN MVNO market.

By Distribution Channel: Digital Acquisition Scales Efficiently

Online and digital-only distribution accounted for a 44.06% share in 2025 and is projected to post the fastest 5.28% CAGR through 2031. Instant eSIM provisioning within branded mobile apps compresses activation time from days to under 5 minutes while halving customer-acquisition costs compared to physical retail. giga! Singapore reported an average onboarding cost of SGD 35 after shifting fully to app-based KYC, roughly 40% below store-channel averages. Traditional retail persists for older users, migrant workers who favour cash top-ups, and countries where regulators still mandate in-person ID checks; it thus retains a 55.94% share but shows limited growth. Carrier sub-brand stores extend host networks’ brick-and-mortar presence to sell captive MVNO plans, but the model mainly defends incumbents rather than expanding the third-party universe.

eSIM fragmentation tempers the digital boom: Singapore and Malaysia allow remote provisioning, yet Indonesia and the Philippines still require physical verification, slowing adoption. Device compatibility also matters; entry-level Android phones that dominate rural markets often lack eSIM hardware. Even so, omnichannel strategies are converging virtual operators use QR-based eSIMs for tech-savvy customers and mail out triple-cut plastic SIMs for everyone else, supported by AI chatbots that resolve 70% of queries without human agents. As regulators harmonize KYC rules and budget devices gain eSIM chips, digital-only channels will surpass half of new subscriber adds before 2029, cementing acquisition efficiency as a core competitive weapon across the ASEAN MVNO market.

Geography Analysis

Singapore and Malaysia together represented just over half of ASEAN MVNO revenue in 2025, underpinned by wholesale-friendly regulation, near-universal 4G coverage, and urban consumers who switch freely between no-contract plans. Singapore housed more than 10 MVNOs across four host networks, yet no operator topped 15% share, which forced differentiation toward roaming bonuses, data rollover, or loyalty cashbacks. Pricing clustered around SGD 15 for 100-300 GB, illustrating commoditization. Malaysia’s dual wholesale 5G model deepened capacity and capped prices, enabling Eastel to sign the country’s first 5G MVNO deal in October 2025. China Mobile International’s CMLink launch via Maxis the following August targeted the sizable Chinese expatriate base with dual-number features that link Malaysian and PRC lines, hinting at how cultural communities can form profitable niches.

Thailand and Vietnam entered a regulatory opening phase between 2024 and 2025. Thailand’s “One Region, One MVNO” rule compels every infrastructure provider to host at least one rural-focused virtual operator per region and cuts wholesale prices by 20%, but financing and service-level negotiations slowed rollouts, so nationwide commercial launches now aim for late-2026. Vietnam’s Telecommunications Law 2023 reduced licensing friction, yet by early-2026 major MVNO launches remained pending because host MNOs fear cannibalization. Vietnam still offers latent potential: three facilities-based networks hold more than 90% of 104 million mobile lines, implying spare capacity once wholesale terms settle.

Indonesia and the Philippines show vast population pools yet tougher economics. Both archipelagic geographies require expensive backhaul to thousands of islands; tower fiberization in outer zones can exceed USD 10,000 per site, so MNOs are reluctant to discount wholesale capacity far from urban cores. Non-terrestrial networks promise relief: low-earth-orbit satellite tests already connect remote Philippine villages, although present data rates serve only emergency and IoT messaging. Migrant-worker flows and tourism foster roaming-centric MVNOs such as ZYM Mobile, which bundles 600 GB Malaysian data perks into Singapore plans, leveraging cross-border demand for seamless roaming. Overall, a two-speed pattern persists: Singapore and Malaysia epitomize mature, margin-tight competition, whereas Thailand, Vietnam, Indonesia, and the Philippines offer frontier upside contingent on regulatory follow-through and infrastructure upgrades.

Competitive Landscape

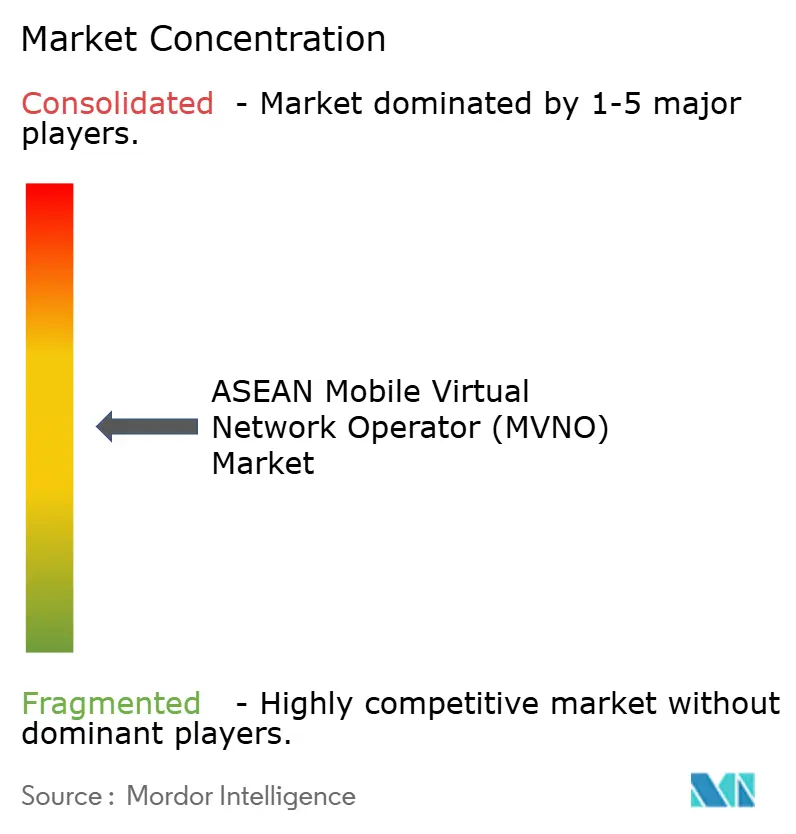

The ASEAN MVNO sector is moderately fragmented, with roughly two dozen active brands but no pan-regional leader commanding more than 15% share. Host networks hedge by launching their own digital sub-brands GOMO (Singtel), Giga (StarHub), and K-go (M1) that match independent pricing while retaining network cost advantages, compressing the wholesale pool. Independent MVNOs therefore split into two playbooks. First, discount-centric players chase scale via app-based sign-ups, accepting thin 15-20% gross margins and 25-30% annual churn; sustainability hinges on low operating costs driven by cloud BSS and AI chatbots. Second, enterprise and IoT specialists pursue sticky B2B revenue, bundling private APN, device management, and multi-network failover that elevate ARPU to USD 20-30 and cut churn below 15%.

Strategic partnerships signal the shifting ground. Circles.Life’s February 2025 deal with M1 introduced ASEAN’s first 5G standalone MVNO slice that supports sub-10-millisecond latency for cloud gaming, while Eastel’s five-year wholesale contract with U Mobile unlocks a route to sell customizable services from 2026 onward. CMLink’s August 2025 Malaysian entry, leveraging Maxis coverage and China Mobile’s global roaming backbone, exemplifies cross-border synergies that could replicate elsewhere. Technology adoption differentiates winners: operators deploying AI-based churn models and dynamic pricing report operating-expense cuts of up to 30% relative to manual processes. On the horizon, eSIM marketplaces such as Airalo threaten the profitable traveller segment by aggregating capacity at global scale and selling instant plans at a 30-50% discount, while satellite-to-cell services may one day commoditize rural coverage.

Mergers and exits underline margin strain. Singapore lost at least three MVNOs Gorilla Mobile, Grid Mobile, and Zero Mobile between 2023 and 2025 as acquisition costs outpaced lifetime value. MyRepublic is raising SGD 100 million in Series C to fund expansion after turning EBITDA-positive in broadband but still loss-making in mobile, showing that even seasoned ISPs need fresh capital to compete. Private-equity interest remains limited because minimum-guarantee wholesale contracts hamper downside protection. Consequently, market consolidation is likely over the next three years, and survivors will either own differentiated platform IP or align closely with sector ecosystems such as fintech, logistics, or automotive telematics.

ASEAN Mobile Virtual Network Operator (MVNO) Industry Leaders

Circles.Life (Liberty Wireless Pte Ltd.)

GOMO (Singtel Mobile Singapore Pte Ltd.)

redONE Network Sdn Bhd

Tune Talk Sdn Bhd

Celcom Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Industrial Technology Research Institute completed multi-orbit 5G NTN trials with MediaTek, Eutelsat, and Chunghwa Telecom, demonstrating 2 bps/Hz over GEO satellites and validating hybrid terrestrial-satellite MVNO architectures.

- January 2025: Vietnam implemented Decree 163/2024 under its new Telecommunications Law, reclassifying M2M traffic as basic telecom service and setting streamlined notification rules for offshore cloud cores.

- December 2024: ESA and Telesat linked a moving LEO satellite to a terrestrial 5G NTN, proving stable connectivity through horizon-to-38° elevation transitions with Amarisoft 5G software.

ASEAN Mobile Virtual Network Operator (MVNO) Market Report Scope

The ASEAN Mobile Virtual Network Operator (MVNO) Market Report is Segmented by Deployment Model (Cloud, On-Premise), Operational Mode (Reseller, Service Operator, Full MVNO, Light/Brand MVNO), Subscriber Type (Consumer, Enterprise, IoT-Specific), Application (Discount, Business, Cellular M2M, Media and Entertainment, Retail, Roaming, Migrant, Telecom Wholesale), Network Technology (2G/3G, 4G/LTE, 5G, Satellite/NTN), Distribution Channel (Online/Digital-Only, Traditional Retail Stores, Carrier Sub-Brand Stores, Third-Party/Wholesale), and Geography (ASEAN). Market Forecasts are Provided in Terms of Value (USD).

By Deployment Model

| Cloud |

| On-Premise |

By Operational Mode

| Reseller |

| Service Operator |

| Full MVNO |

| Light, Brand MVNO |

By Subscriber Type

| Consumer |

| Enterprise |

| IoT-Specific |

By Application

| Discount |

| Business |

| Cellular M2M |

| Media and Entertainment |

| Retail |

| Roaming |

| Migrant |

| Telecom Wholesale |

By Network Technology

| 2G, 3G |

| 4G, LTE |

| 5G |

| Satellite, NTN |

By Distribution Channel

| Online, Digital-Only |

| Traditional Retail Stores |

| Carrier Sub-Brand Stores |

| Third-Party, Wholesale |

| By Deployment Model | Cloud |

| On-Premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light, Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-Specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Media and Entertainment | |

| Retail | |

| Roaming | |

| Migrant | |

| Telecom Wholesale | |

| By Network Technology | 2G, 3G |

| 4G, LTE | |

| 5G | |

| Satellite, NTN | |

| By Distribution Channel | Online, Digital-Only |

| Traditional Retail Stores | |

| Carrier Sub-Brand Stores | |

| Third-Party, Wholesale |

Key Questions Answered in the Report

How fast is the ASEAN MVNO market expected to grow between 2026 and 2031?

The market is projected to expand from USD 692.57 million in 2026 to USD 840.58 million by 2031, reflecting a 3.95% CAGR.

Which deployment model is gaining traction among new MVNO launches?

Cloud-based BSS and OSS platforms are becoming the default choice because they cut launch time to under 100 days and reduce upfront capital.

Why are full MVNO configurations drawing interest despite higher capex?

Full MVNOs control routing and quality of service, lifting gross margins toward 35% and enabling differentiated enterprise solutions.

What role will 5G play for MVNOs over the next five years?

Standalone 5G cores permit network slicing, letting MVNOs sell low-latency or SLA-backed plans to enterprises, although wholesale 5G still costs about 25% more than LTE.

How does regulation affect MVNO profitability in ASEAN?

Policies such as Thailand's 20% wholesale-fee cut and Malaysia's biennial access-price reviews lower input costs and open capacity, yet quality-of-service guarantees remain limited.

Are satellite-to-cell services a near-term threat to terrestrial MVNOs?

Not immediately, because per-gigabyte satellite capacity is 5-10 times costlier; early use cases stay confined to emergency messaging and low-data IoT in remote islands.

Page last updated on: