Vietnam IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

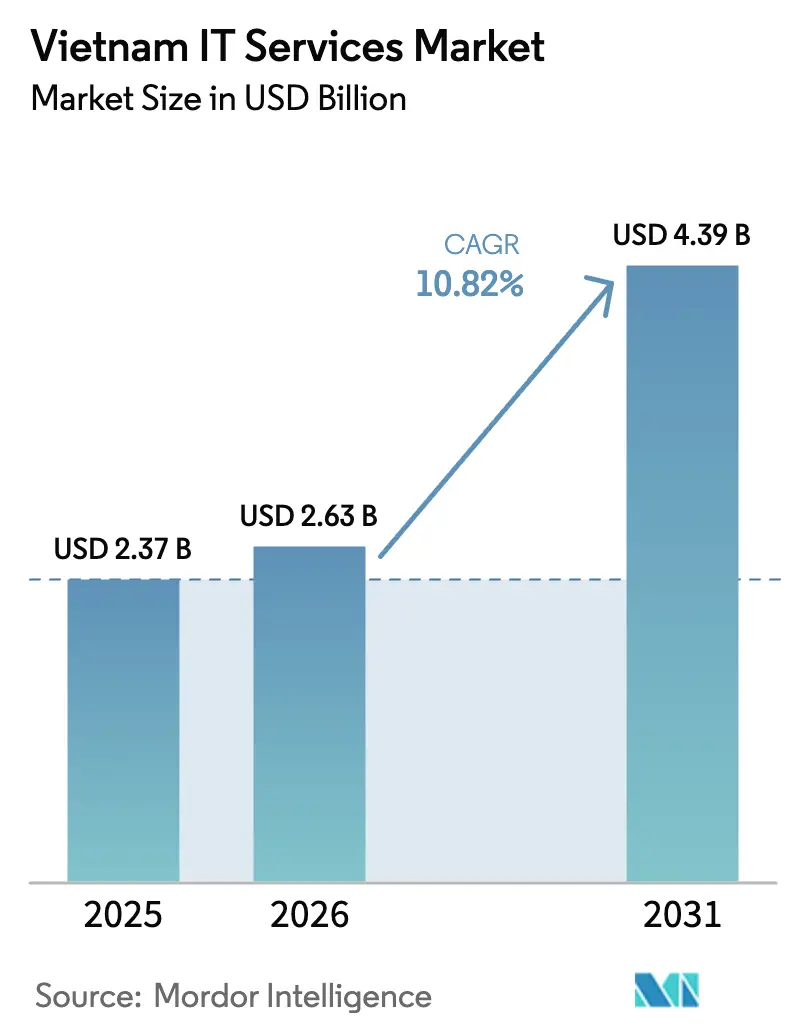

| Base Year Market Size (2025) | USD 2.37 Billion |

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam IT Services Market Analysis by Mordor Intelligence

The Vietnam IT services market size in 2026 is estimated at USD 2.63 billion, growing from 2025 value of USD 2.37 billion with 2031 projections showing USD 4.39 billion, growing at 10.82% CAGR over 2026-2031. Robust digital-government spending, near-shore outsourcing inflows from Japan and the United States, and accelerated cloud adoption form the backbone of this expansion. Enterprise demand is shifting from cost-centric outsourcing toward value-added digital transformation, pushing providers into higher-margin consulting, platform, and managed security work. Domestic champions continue to scale internationally while foreign multinationals open delivery centers in Ho Chi Minh City and Hanoi, adding further depth to the Vietnam IT services market. Talent shortages, fragmented data-privacy rules, and occasional submarine-cable outages temper the growth outlook but do not alter the upward trajectory.

Key Report Takeaways

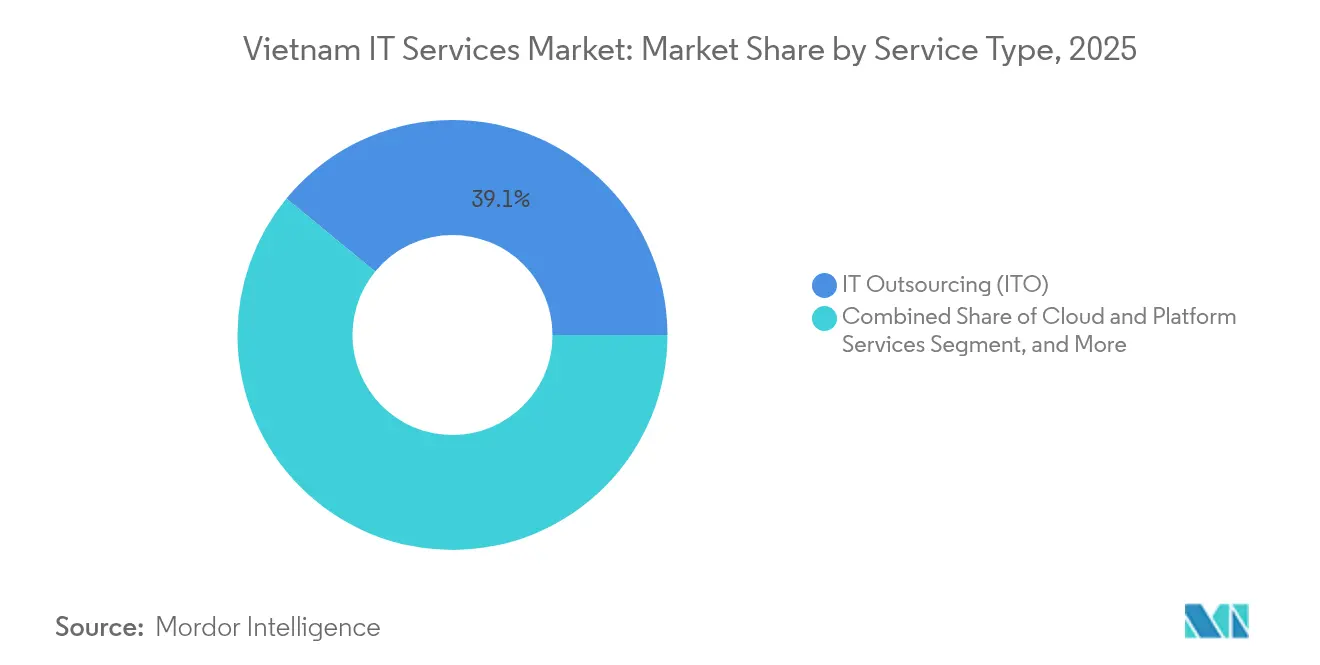

- By service type, IT Outsourcing led with 39.05% of the Vietnam IT services market share in 2025; Cloud and Platform Services are forecast to expand at a 11.86% CAGR through 2031.

- By end-user enterprise size, Large Enterprises accounted for 67.72% of the Vietnam IT services market in 2025, while Small and Medium Enterprises are advancing at a 12.74% CAGR to 2031.

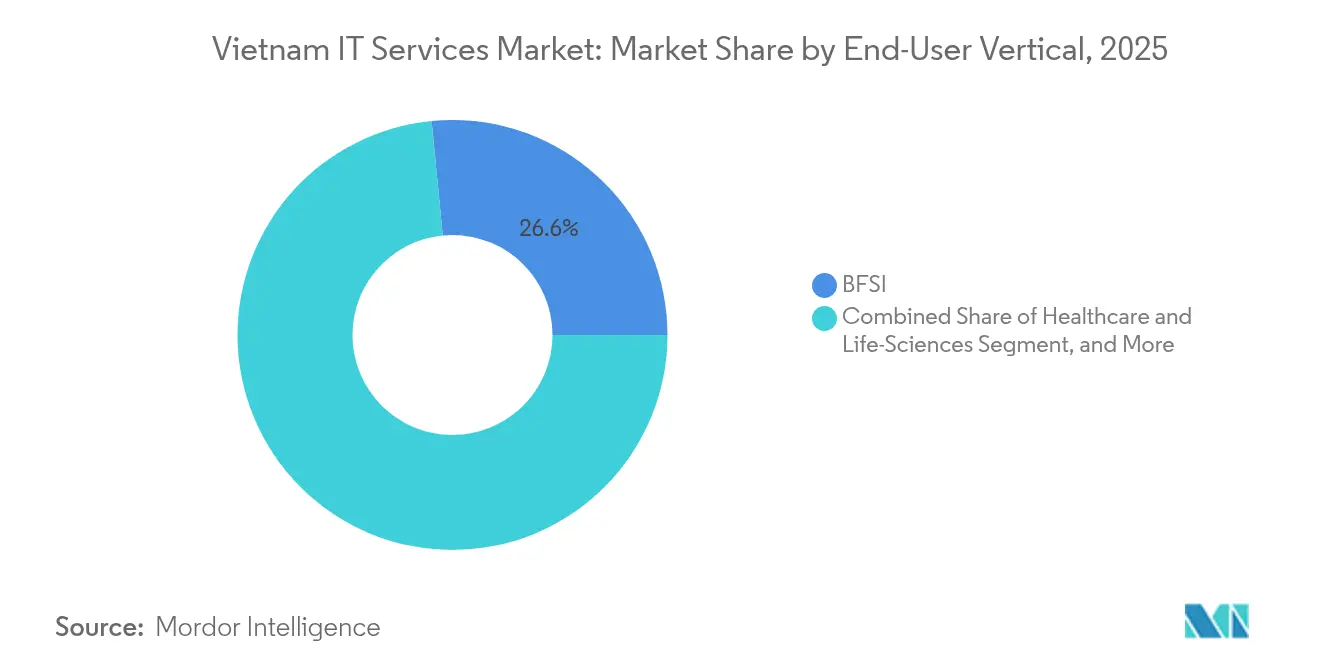

- By end-user vertical, BFSI captured 26.55% revenue share of the Vietnam IT services market in 2025, and Healthcare and Life Sciences are projected to report a 12.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Roadmap 2025 | +2.8% | National, highest in Hanoi and Ho Chi Minh City | Medium term (2-4 years) |

| Near-shore demand from Japan and the US | +2.1% | Global, affecting APAC and North America ties | Long term (≥ 4 years) |

| Domestic cloud adoption surge | +1.9% | National, initial traction in tier-1 cities | Short term (≤ 2 years) |

| Data-center localization mandates | +1.4% | National, centered in industrial zones | Medium term (2-4 years) |

| SME Tech-Loan Fund | +1.2% | National, focused on tech clusters | Short term (≤ 2 years) |

| AI regulatory sandboxes in BFSI | +0.8% | National, pilots in major financial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Roadmap 2025

The government’s roadmap stipulates concrete digitization milestones for all ministries and provincial agencies, creating a multi-year pipeline of e-government, cyber-security, and citizen-service contracts. Budget allocations for system renewal and process automation prioritize domestic providers conversant with local procurement, boosting predictable revenue flows. Private enterprises are compelled to modernize interfaces to comply with new government APIs, further broadening demand. Resolution 57-NQ/TW’s push for AI, blockchain, and IoT widens service scope, while updated procurement rules shorten award cycles. Together, these elements fortify the Vietnam IT services market. [1]FPT Information System, “Vietnam E-Government Procurement System Wins ASOCIO Award,” fptis.com

Rising Near-shore Demand from Japan and the US

Vietnam’s labor-cost advantage—engineers earn roughly one-tenth of global averages—combined with time-zone overlap and cultural affinity, makes the country a preferred near-shore hub. Providers such as FPT secured USD 1.3 billion in new contracts in 2024, underlining sustained appetite. Multinationals set up captive centers, reflecting long-term strategy rather than opportunistic cost cuts. Supply-chain diversification away from single-country dependencies accelerates this inflow, lifting the Vietnam IT services market well above regional averages. [2]FPT Software, “FPT’s Global IT Services Signed Revenue Surpassed USD 1.3B,” fptsoftware.com

Accelerated Domestic Cloud Adoption

Post-pandemic continuity planning pushed enterprises toward cloud-first architectures. Decree 53/2022/ND-CP requires select data classes to stay onshore for 24 months, giving local providers a structural advantage and stimulating the build-out of national cloud zones. Healthcare digitization and digital banking further stretch demand for migration and hybrid-cloud management. Only 6% of hospitals run electronic medical records today, leaving ample headroom for growth.

Data-Center Localization Mandates

Localization rules drive investments in industrial-zone data centers. Domestic carriers deploy hyperscale facilities, creating an indigenous cloud backbone. Providers gain new revenue from consulting on in-country workload placement, compliance, and managed hosting. The mandates also deter overseas competitors lacking Vietnamese footprints, insulating the Vietnam IT services market from pure-play global hyperscalers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortages and wage inflation | -1.8% | National, most acute in Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Fragmented data-privacy rules | -1.2% | National, complicating cross-border work | Medium term (2-4 years) |

| Undersea-cable downtime risks | -0.9% | National, hampers international delivery | Short term (≤ 2 years) |

| Lengthy SOE procurement amid anti-graft | -0.7% | National, slows public-sector contract conversion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortages and Wage Inflation

Vietnam produced 530,000 programmers by 2024, yet demand continues to outstrip supply, especially for senior architects and emerging-tech specialists. Salaries rise 15–20% annually, compressing provider margins and eroding the headline cost advantage that anchors the Vietnam IT services market. Employers channel resources into training and retention, but poaching remains rampant, creating talent circulation rather than net capacity growth. Government semiconductor-talent programs offer limited near-term relief.

Fragmented Data-Privacy Rules

The interim Personal Data Protection Decree obliges firms to follow strict—but still evolving—safeguard protocols. Sector-specific rules for finance, healthcare, and telecom pile extra layers of oversight. Providers incur higher compliance costs for audits, documentation, and localized infrastructure, a hurdle for smaller vendors courting global enterprises. [3]United Nations Development Programme, “Development and Experimentation and Transfer of an AI-Powered Digital Tool,” undp.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: ITO Dominance Drives Market Foundation

IT Outsourcing contributed 39.05% to the Vietnam IT services market size in 2025, underscoring its role as the market’s cornerstone. The segment leverages large pools of mid-level developers to deliver application maintenance and product engineering for Japanese, U.S., and Korean clients. Wage inflation nudges providers toward productivity tools, agile methodologies, and domain specialization to sustain margins. Digital transformation deals are increasingly bundled with legacy-support extensions, allowing incumbents to upsell newer services.

Cloud and Platform Services, though smaller, are the fastest risers with a 11.86% CAGR to 2031. Data-center localization fuels domestic IaaS demand, while multi-cloud orchestration and containerization create advanced consulting opportunities. Managed Security Services follows close behind, boosted by a 65% jump in cyber-incidents during 2023 and mandatory local threat-monitoring for sensitive sectors. IT Consulting and Implementation, once ancillary, now commands premium rates as enterprises seek roadmap expertise, while Business Process Outsourcing remains a niche focused on finance-and-accounting tasks for English-speaking clients. Altogether, shifting service-mix dynamics make higher-value work the next growth frontier for the Vietnam IT services market.

By End-User Enterprise Size: SME Acceleration Reshapes Demand

Large enterprises controlled 67.72% of the Vietnam IT services market size in 2025, reflecting their deeper IT budgets and complex hybrid infrastructure needs. Multinationals and leading Vietnamese conglomerates award multi-year master-service agreements, anchoring provider revenue predictability. These clients segment projects by specialty, encouraging best-of-breed supplier ecosystems.

Small and medium enterprises, backed by the 2024 SME Tech-Loan Fund, display a 12.74% CAGR outlook through 2031. Affordable financing compresses payback periods on ERP, e-commerce, and IoT investments, while packaged SaaS models suit SMEs’ lean staffing. Providers run dedicated support desks in tech parks, reducing service-delivery costs and improving churn economics. The result is a structural broadening of the Vietnam IT services market, diversifying revenue away from the traditional large-enterprise core.

By End-User Vertical: BFSI Leadership Meets Healthcare Innovation

BFSI contributed 26.55% of the Vietnam IT services market share in 2025, anchored by core-bank modernization and digital-banking rollouts under the State Bank’s sandbox. Implementation of AI-driven risk scoring, open-API gateways, and real-time fraud analytics secure steady consulting and platform work for service vendors.

Healthcare and life sciences, expanding at a 12.15% CAGR, represent the green-field prize. With only 6% of hospitals running electronic medical records, providers face sizable volumes in telemedicine platforms, imaging data lakes, and clinical-decision support. Government subsidies for digital health accelerate procurement, ensuring that healthcare overtakes manufacturing as the next demand hotspot within the Vietnam IT services market.

Manufacturing retains high spend due to Industry 4.0 ambitions, embedding IoT, SCADA upgrades, and supply-chain analytics into export-oriented factories. Retail/consumer goods ramp omnichannel stacks, while government remains a reliable adopter through e-service mandates. Telecom, energy, and logistics segment spending rounds out a diversified vertical mix that stabilizes overall growth.

Geography Analysis

Ho Chi Minh City and Hanoi combined generated roughly three-quarters of the Vietnam IT services market in 2025, a testament to their mature tech ecosystems, skilled labor pools, and access to foreign enterprises. Ho Chi Minh City retains the commercial lion’s share, with 38% of provider headcount and many Japanese client liaison offices. Hanoi capitalizes on proximity to central ministries, catalyzing public-sector digitization and housing national champions such as Viettel Solutions.

Da Nang rises as a cost-efficient secondary hub, hosting delivery centers for mid-tier firms that tap graduates from local universities. Industrial provinces like Binh Duong and Dong Nai nurture manufacturing-centric IT opportunities, enabling on-site smart-factory integration within sprawling industrial parks. Northern border provinces leverage China-linked supply-chain flows, demanding logistics and customs-automation platforms, while coastal Hai Phong and Can Tho pioneer maritime-logistics and agri-tech applications, respectively.

International connectivity underpins geographic service delivery. Five subsea cables tie Vietnam to global internet routes, but recurrent outages emphasize redundancy gaps. Planned Viettel-backed links to Singapore and Japan aim to mitigate latency and uptime risk, enhancing confidence among overseas clients of the Vietnam IT services market. Growing data-center clusters in Ho Chi Minh City’s Thu Duc City and Hanoi’s Hoa Lac Hi-Tech Park further solidify these metros as cloud inlet points, though distributed micro-data centers in provincial zones are gaining traction to cut edge-processing latency.

Competitive Landscape

The top five vendors captured around 40% of total revenue in 2024, classifying the Vietnam IT services market as moderately concentrated yet still open for specialist entrants. FPT Corporation, Viettel Solutions, and CMC Global lead on breadth, each scaling global footprints: FPT targets USD 5 billion in software exports by 2030, while Viettel earned USD 3 billion from overseas telco and defense IT in 2023. [4]FPT Software, “FPT and NVIDIA to Build the First AI Factory in Vietnam,” fptsoftware.com Their international success funnels R&D funds back home, escalating the technology baseline domestically.

Strategic differentiation pivots on AI capability, domain knowledge, and regional presence. FPT’s joint build-out of an NVIDIA-powered AI factory promises a 25% net-profit lift from AI services in 2025, setting a high bar for competitors. Viettel leverages telco roots to deploy 5G-native edge platforms, whereas CMC’s USD 1 billion co-developed data center with Samsung positions it as a localization-compliant cloud landlord. Mid-tier firms such as Rikkeisoft and Tinhvan punch above their weight through partnerships with Sumitomo Corporation and Magic Software Japan, respectively, gaining channel access and specialized tooling.

Niche opportunities flourish in healthcare IT, SME packaged solutions, and industrial IoT, areas underserved by large vendors chasing scale. Smaller specialists exploit agility to deliver verticalized SaaS and consulting, winning high-margin pockets. Pricing pressure persists in commodity web-development outsourcing, prompting widespread migration up the value chain. Joint ventures with foreign system integrators, co-innovation labs, and university pipelines for talent form integral elements of competitive playbooks across the Vietnam IT services market.

Vietnam IT Services Industry Leaders

FPT Corporation

CMC Global Co., Ltd.

Viettel Solutions Corporation

VNPT Technology

NashTech Vietnam Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The fintech regulatory sandbox under Decree 94/2025/ND-CP became effective, opening controlled pilots for AI credit scoring and open banking APIs.

- January 2025: UNDP Vietnam initiated procurement of AI-driven tools to enhance inclusive public-service access.

- January 2025: FPT Corporation reported 2024 revenue of VND 62.849 trillion (USD 2.47 billion) and pre-tax profit of VND 11.071 trillion (USD 435 million), up 19.4% and 20.3% respectively, alongside 48 contracts above USD 5 million each.

- January 2025: Viettel Group logged pre-tax profit of VND 51 trillion (USD 2.01 billion) on revenue of VND 190 trillion (USD 7.47 billion) and launched a submarine cable linking Vietnam to regional peers.

- December 2024: CMC Global sealed a USD 1 billion data-center deal with Samsung C&T, creating one of Southeast Asia’s largest facilities and strengthening localization compliance positioning.

Vietnam IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

How large is the Vietnam IT services market in 2026?

The sector is valued at USD 2.63 billion in 2026, with a forecast of USD 4.39 billion by 2031.

What CAGR is expected for Vietnam’s IT service spending to 2031?

Spending is projected to rise at a 10.82% CAGR over 2026-2031.

Which service line grows fastest through 2031?

Cloud and Platform Services carries the fastest trajectory at a 11.86% CAGR.

Why are SMEs critical to future growth?

Preferential loans below 5% spur SMEs to digitize, driving a 12.74% CAGR in their IT spend.

Which end-user vertical shows the highest 2026-2031 growth?

Healthcare and life sciences leads with a 12.15% CAGR, propelled by telemedicine and EHR projects.

What is the biggest challenge facing providers?

Acute talent shortages trigger wage inflation of 15–20% annually, pressuring margins and capacity.

Page last updated on: