Vietnam Energy Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

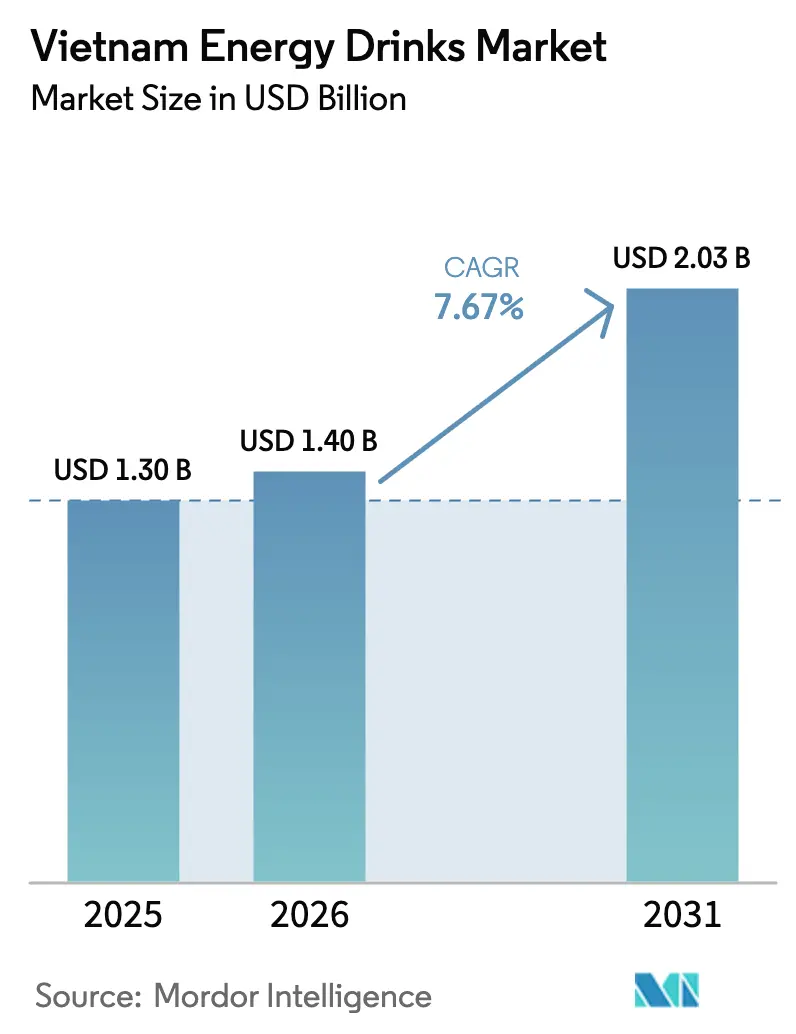

| Base Year Market Size (2025) | USD 1.3 Billion |

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

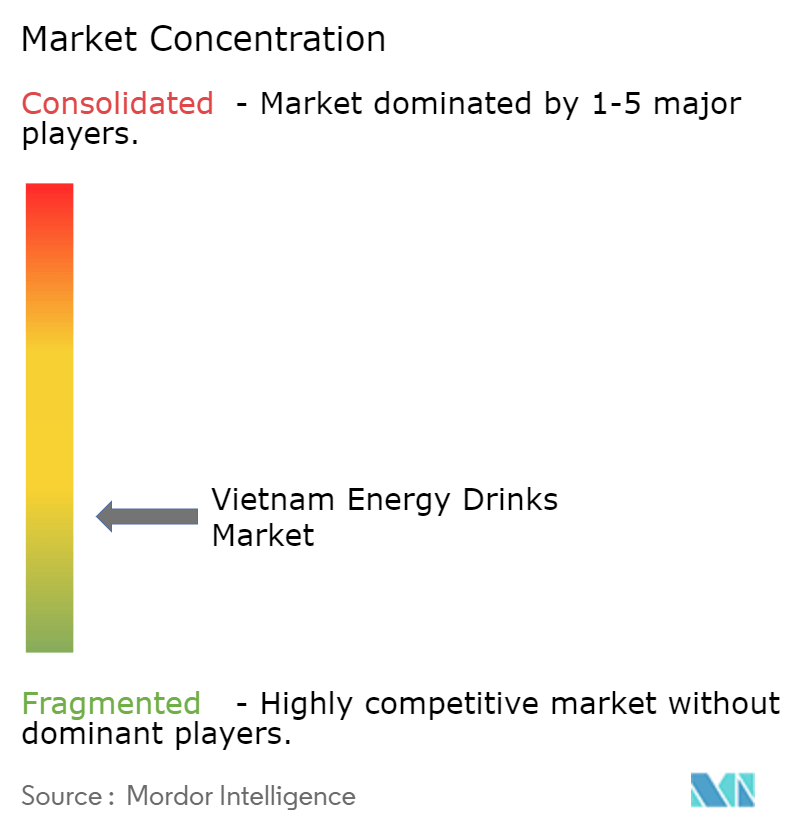

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Energy Drinks Market Analysis by Mordor Intelligence

Vietnam energy drinks market size in 2026 is estimated at USD 1.4 billion, growing from 2025 value of USD 1.3 billion with 2031 projections showing USD 2.03 billion, growing at 7.67% CAGR over 2026-2031. Urbanization, rising disposable incomes, and an active fitness culture are converging to lift everyday demand well beyond traditional impulse occasions, while favorable demographics keep the core consumer base youthful and expanding. Regulatory intervention, notably the special-consumption tax on sugary beverages that begins in 2027, is unintentionally accelerating low- and no-sugar innovation as major producers recalibrate formulations and pricing models to protect volume and margin. At the same time, the spread of e-sports and round-the-clock digital entertainment is lengthening usage windows and stimulating incremental sales during late-evening and overnight periods. Distribution modernization—in particular the rapid build-out of convenience stores and the widening reach of e-commerce—continues to narrow supply-chain inefficiencies and put premium functional beverages within easy reach of consumers in both tier-1 cities and fast-growing secondary hubs.

Key Report Takeaways

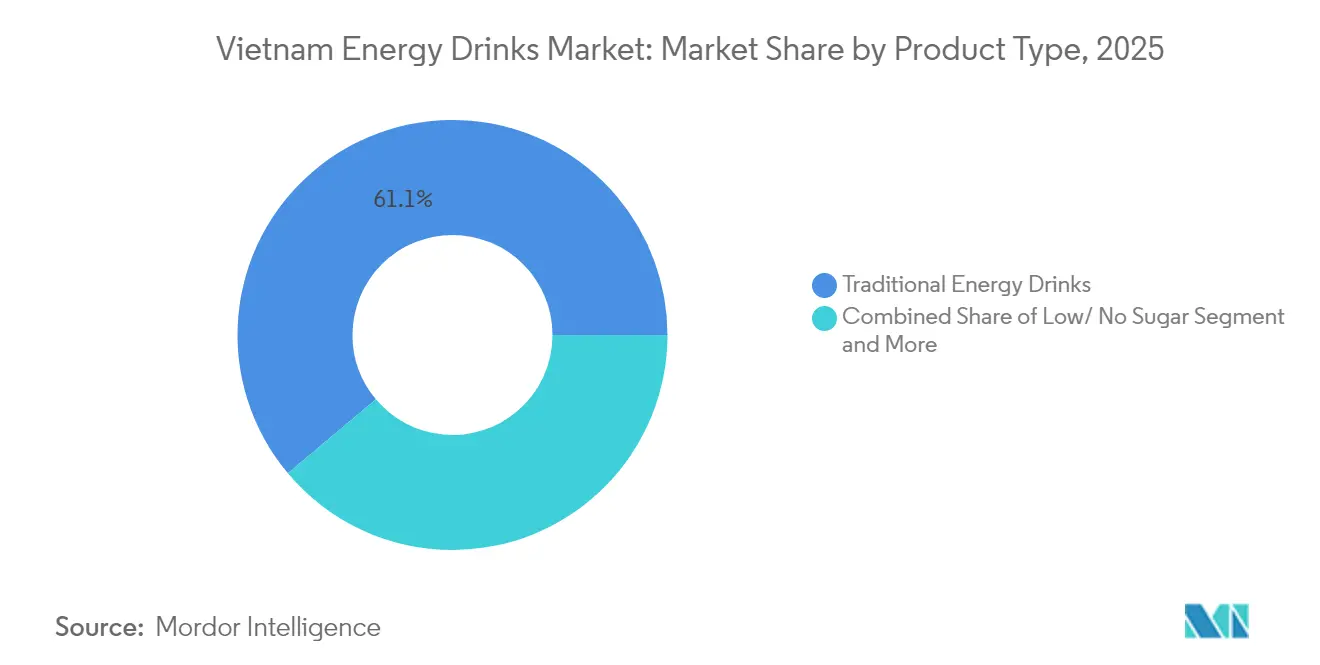

- By product type, Traditional Energy Drinks captured 61.12% of the Vietnam energy drinks market share in 2025, while the Low/No-Sugar segment is forecast to expand at a 10.38% CAGR to 2031.

- By packaging, metal cans led with 50.92% revenue share in 2025; PET bottles are advancing at an 8.55% CAGR through 2031.

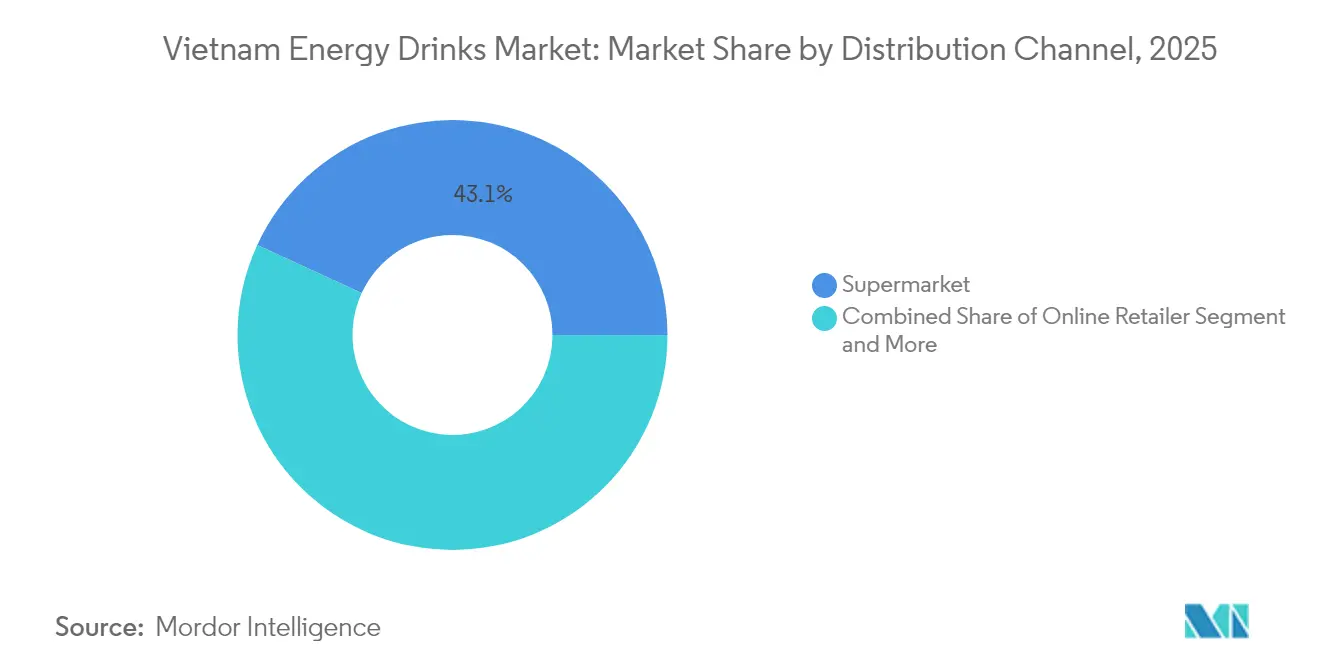

- By distribution channel, supermarkets held 43.12% in 2025, whereas online retailers are projected to grow at a 11.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fitness-oriented demand | +1.8% | Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Endorsements, sponsorships & social-media marketing | +1.5% | National urban millennials & Gen Z | Short term (≤ 2 years) |

| Rising disposable income & urban lifestyle shifts | +2.1% | Major metros and tier-2 cities | Long term (≥ 4 years) |

| Expansion of convenience-store chains | +1.2% | Urban & peri-urban | Medium term (2-4 years) |

| E-sports & late-night gaming culture | +0.9% | Urban youth gaming hubs | Short term (≤ 2 years) |

| Impending sugar tax spurring low/no-sugar launches | +0.8% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Fitness-Oriented Consumers

The country’s fitness boom is reshaping beverage repertoires as gym-goers, recreational athletes, and time-pressed professionals embrace functional caffeine, B-vitamins, and botanical adaptogens in pursuit of performance gains. Premium energy drinks enriched with natural ingredients now sit alongside sports nutrition staples in health clubs, driving trial among consumers who value quick absorption and minimal preparation. This same cohort is willing to pay price premiums when claims around reduced sugar, herbal extracts, and cognitive support align with personal wellness goals. Brands that broadcast transparent labeling and verifiable nutrient content—requirements codified in Ministry of Health directive Công văn 2310/BYT-ATTP—secure shelf space and consumer trust simultaneously.

Growing Influence of Endorsements, Sponsorships & Social-Media Marketing

High-visibility tie-ins with elite sports franchises are redefining how Vietnamese consumers perceive energy drinks. Masan Consumer’s Wake-Up 247 collaboration with Manchester City unleashed limited-edition packaging that features star players and galvanized social chatter among football fans nationwide. When amplified across TikTok, Facebook, and local streaming platforms, such partnerships create powerful lifestyle cues that extend beyond functional benefit narratives. Micro-influencer seeding and user-generated content promote authenticity and allow real-time feedback loops that refine message tone, imagery, and placement. The outcome is a surge in brand affinity among urban Gen Z audiences who prize relatability and digital engagement over conventional TV advertising.

Rising Disposable Income and Urban Lifestyle Shifts

Vietnam’s steady GDP per-capita climb is driving a decisive pivot from price-centric to quality-driven purchasing. Dual-income households juggling demanding schedules treat premium energy drinks as a value-added convenience, favoring products that combine refreshing taste with on-the-go functionality. The trend is visible in the migration from single-serve sachets toward multi-pack metal cans and PET bottles that promise both status signaling and perceived better quality. In modern trade aisles, premium tiers frequently secure eye-level placement, reflecting margin-rich rotations that retailers willingly support. Over the long term, this premiumization arc helps underpin the 7.76% CAGR anchoring the broader Vietnam energy drinks market.

Expansion of Convenience-Store Chains

More than 6,000 modern convenience outlets now populate urban and peri-urban corridors, operating 24/7 and offering chilled energy drinks at arm’s length to shift workers, students, and ride-hailing drivers. Planograms optimized for impulse stimulation—end-cap displays, grab-and-go coolers, and meal-deal bundles—intensify category visibility. Partnerships between brands and chain operators unlock exclusive flavor launches and loyalty‐program tie-ins that generate incremental footfall. As chains expand into tier-2 municipalities, they democratize access for consumers previously reliant on wet markets or small family stores, reinforcing category penetration and raising baseline sales even in off-peak months.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitute products (RTD coffee, functional shots) | -1.4% | Urban markets with diverse beverage options | Short term (≤ 2 years) |

| Mounting health concerns over sugar & caffeine intake | -2.2% | Health-conscious urban demographics nationwide | Medium term (2-4 years) |

| Proposed excise duty on sweetened beverages | -1.8% | National regulatory compliance affecting all sugar-containing products | Medium term (2-4 years) |

| PET-recycling quota raising packaging compliance costs | -0.9% | Manufacturing hubs with PET packaging operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitute Products (RTD Coffee, Functional Shots)

Vietnam’s rich coffee heritage gifts RTD brews an authenticity edge that energy drinks struggle to match. Artisanal cold brews boasting traceable bean origins promise a smoother flavor profile and a “natural” caffeine kick, siphoning share from synthetic-perceived energy beverages, especially among professionals seeking a premium afternoon boost. Compact functional shots add another layer of competition by delivering concentrated energy in 60-90 ml formats that minimize calorie intake and container waste. As these alternatives adopt sports sponsorships and influencer marketing once unique to energy drinks, brand differentiation narrows, posing a near-term drag on category growth potential.

Mounting Health Concerns over Sugar & Caffeine Intake

Heightened public discourse linking sugary drinks to obesity and diabetes is prompting Vietnamese consumers to scrutinize labels and moderate consumption. Guidance from health authorities and physicians now openly warns against frequent high-caffeine beverage intake, particularly for adolescents and individuals with cardiovascular conditions. Viral social-media stories highlighting adverse reactions to excessive energy drink use amplify these warnings and can spark temporary pullbacks in sales. Although manufacturers are aggressively promoting reduced-sugar portfolios, such messages often coexist with lingering skepticism about artificial sweeteners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Dominance Faces Health Revolution

Traditional Energy Drinks accounted for a commanding 61.12% of Vietnam energy drinks market share in 2025, reflecting long-entrenched consumption habits among manual laborers, drivers, and shift workers who prize reliable stimulation over nuanced flavor or health claims. Multi-pack metal cans sold through supermarkets and mom-and-pop outlets maintain strong velocity, particularly during festive seasons when gifting spurs bulk purchases. The incoming sugar tax, combined with expanding fitness participation, is nudging core users to split their baskets between classic and reduced-sugar SKUs, positioning reformulated lines as a bridge rather than a total replacement. Brands leveraging natural sweeteners and added electrolytes find ready traction at both brick-and-mortar and online checkouts, suggesting future revenue resilience even if regulatory thresholds tighten further.

The Vietnam energy drinks market size attached to Low/No-Sugar formulations is expected to widen materially as product pipelines fill with stevia- and monk-fruit-based recipes that replicate sweetness while trimming calories. Retailers allocate incremental shelf facings to these SKUs to pre-empt consumer migration toward imported diet-positioned beverages. Marketing narratives emphasize metabolic efficiency and sustained cognitive function without the crash traditionally associated with sucrose-laden drinks. Over time, portfolio balancing toward diversified sugar profiles may enable leading players to cushion potential revenue dips from health-related backlash while keeping engagement high among traditionalist cohorts.

By Packaging Type: Metal Cans Dominate Despite Sustainability Pressures

Metal cans retained 50.92% share of the Vietnam energy drinks market in 2025 owing to superior carbonation retention, tactile chill, and iconic category aesthetics that resonate with long-time consumers. Limited-edition graphics tied to sports events and music festivals regularly spark collector behavior, pushing short-run sales spikes that strengthen brand equity. Still, aluminum’s embodied energy cost is drawing scrutiny as environmental education improves. Extended Producer Responsibility rules mandating 22% recycling for rigid PET from 2024 have, somewhat paradoxically, boosted PET bottle investment because improved collection infrastructure narrows the sustainability gap.

PET bottles are forecast to post an 8.55% CAGR thanks to their lighter weight, resealability, and compatibility with larger serving sizes that appeal to consumers seeking better value per milliliter. Clear PET also showcases liquid color, enabling brands to underscore natural ingredient cues visually. For modern trade operators, shelf stacking is simpler and breakage risk minimal, reinforcing retailer preference in high-traffic aisles. While glass remains niche due to handling cost, next-generation PET incorporating recycled content could narrow perception gaps on eco-credentials, further challenging can dominance over the medium term within the Vietnam energy drinks market.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Supermarkets commanded 43.12% of 2025 value sales, aided by broad assortments, loyalty programs, and cross-aisle promotions that bundle snacks with energy drinks for impulse upsell. Located mainly in urban cores, these stores consistently launch exclusive flavors and multi-pack deals timed to sporting events, driving pantry loading among middle-income families. Yet operating-hour limits and the need for physical travel leave white space for digital channels to capture incremental occasions such as late-night gaming sessions.

Online retailers are predicted to deliver a 11.98% CAGR through 2031, leapfrogging infrastructure constraints by offering nationwide coverage via express delivery. Sophisticated search and recommendation engines surface niche SKUs, including imported premium brands and specialized low-caffeine options, giving consumers breadth impossible to stock in most physical outlets. Direct-to-consumer storefronts from leading brands further compress the value chain, freeing margin for subscription discounts and personalized bundle offerings. With Vietnam’s e-commerce penetration still climbing, the Vietnam energy drinks market has significant headroom for digital share gains, especially as mobile-wallet adoption normalizes cashless transactions in second-tier provinces.

Geography Analysis

Vietnam’s key metropolitan areas—Ho Chi Minh City, Hanoi, and Da Nang—dominate energy drink consumption, driven by dense populations, extended working hours, and modern retail availability. Low-sugar energy drink SKUs in these cities are already outperforming national averages, indicating a trend likely to expand to smaller cities. The 10.92% revenue growth in the 2024 food-and-beverage sector further supports this momentum, benefiting both mainstream and premium segments. In tier-2 cities like Can Tho and Hai Phong, rapid convenience-store rollouts, rising disposable incomes, and youth migration to industrial parks are fueling volume growth, particularly for PET multi-serves that combine affordability with modern appeal. Meanwhile, smartphone shopping is helping brands penetrate underdeveloped rural areas through cost-effective, targeted social media campaigns.

Cross-border imports from Thailand and South Korea are introducing new flavors and upscale positioning, intensifying competition in the upper-mid price segment. Simultaneously, domestic players like Masan Consumer are expanding internationally, achieving 73.2% international revenue growth in 2025 by leveraging manufacturing scale across ASEAN markets. These two-way trade dynamics are raising domestic quality standards and compelling regional players to innovate continuously to maintain their market share.

Competitive Landscape

Vietnam's energy drinks market is dominated by key players such as Tan Hiep Phat, Suntory PepsiCo, Red Bull Vietnam, Coca-Cola Vietnam, and Masan Consumer, who collectively control most of the market value. These companies benefit from economies of scale in sourcing, bottling, and nationwide merchandising, enabling them to better manage raw material fluctuations and regulatory costs compared to smaller competitors. Their diverse product portfolios, including classic, sugar-reduced, and flavor-extended variants, cater to evolving health and taste preferences, further strengthening their market position. Strategic investments, such as Coca-Cola Vietnam's USD 136 million LEED Gold facility in Tay Ninh and Tan Hiep Phat's capacity expansion at its Number One Hậu Giang site, highlight their confidence in the market's long-term resilience. Additionally, Masan Consumer's partnership with Manchester City enhances brand visibility and supports experiential marketing initiatives that smaller players struggle to match.

While opportunities exist for niche players focusing on organic certifications, vegan attributes, or regionally inspired botanicals, scaling beyond urban markets requires significant investments in cold-chain logistics and point-of-sale infrastructure. This creates a challenging competitive environment, with leading companies expected to defend their market share through continuous product innovation, active digital engagement, and sustainable packaging initiatives that align with shifting consumer values.

Vietnam Energy Drinks Industry Leaders

PepsiCo, Inc.

Tan Hiep Phat

Red Bull Vietnam

Coca-Cola Vietnam

Masan Consumer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Number 1 Energy Drink unveiled an exclusive program in Vietnam, offering consumers a chance to win billions of VND. Titled “Rip Now for Instant Wins—Number 1” and “Energize—Break Through to Become Number 1,” the initiative offers over 250,000 valuable cash prizes to consumers nationwide. Such marketing strategies significantly boost the demand for energy drinks.

- June 2024: According to sources from the Vietnamese government, PepsiCo Inc. is set to invest nearly USD 400 million in Vietnam. This investment will fund the establishment of two new plants: one dedicated to beverages and the other to food products, both utilizing renewable energy. The beverage plant, costing over USD 300 million, will be situated in the southern Long An province. Notably, operations will be managed by the existing joint venture, Suntory PepsiCo Vietnam Beverage. This announcement coincided with a three-day visit to Vietnam by delegations from over 60 U.S. companies, including Suntory PepsiCo Vietnam Beverage.

- January 2024: Vietnam's Masan Group introduced EnerZ, a new energy drink to the market. The beverage's formulation includes choline, vitamin B6, and caffeine as its primary active ingredients. EnerZ is available in two flavor variants: melon and mango & passion fruit, providing consumers with a palatable energy drink option containing real fruit juice. The product utilizes Ace-K and sucralose as sweetening agents.

Vietnam Energy Drinks Market Report Scope

Energy drinks contain stimulant compounds, usually caffeine, that provide energy and enhance the consumer's physical performance and mental alertness. It may or may not be carbonated and contains sugar, other sweeteners, herbal extracts, vitamins, minerals, and amino acids.

The Vietnam Energy Drinks Market is segmented into packaging type and distribution channels. By packaging type, the market is segmented into bottles, and cans. In terms of distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Energy Shots |

| Natural/ Organic Energy Drinks |

| Sugar-free or low-calorie Energy Drinks |

| Traditional Energy Drinks |

| Others |

| PET Bottles |

| Metal Cans |

| Glass Bottles |

| Supermarkets/ hypermarkets |

| Convenience Stores |

| Speciality Stores |

| Online Retailers |

| Others |

| By Product Type | Energy Shots |

| Natural/ Organic Energy Drinks | |

| Sugar-free or low-calorie Energy Drinks | |

| Traditional Energy Drinks | |

| Others | |

| By Packaging Type | PET Bottles |

| Metal Cans | |

| Glass Bottles | |

| By Distribution Channel | Supermarkets/ hypermarkets |

| Convenience Stores | |

| Speciality Stores | |

| Online Retailers | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the Vietnam energy drinks market by 2031?

The market is projected to reach USD 2.03 billion by 2031, advancing at a 7.67% CAGR.

Which product category is expanding the fastest in Vietnam’s energy drink space?

Low/No-Sugar energy drinks are projected to post a 10.38% CAGR through 2031 as health consciousness rises.

How will the 2027 sugar tax affect energy drink formulations?

The 8% levy incentivizes manufacturers to accelerate low- and no-sugar launches to mitigate price increases.

How will the 2027 sugar tax affect energy drink formulations?

The 8% levy incentivizes manufacturers to accelerate low- and no-sugar launches to mitigate price increases.

Page last updated on: