Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

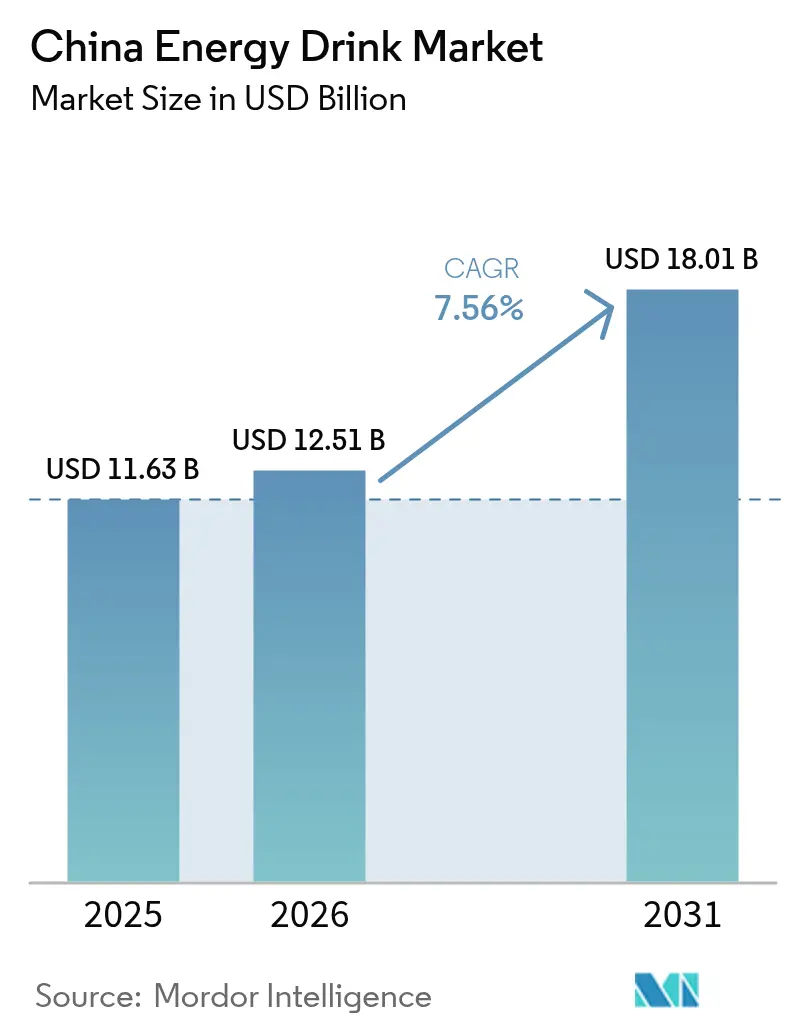

| Base Year Market Size (2025) | USD 11.63 Billion |

| Market Size (2026) | USD 12.51 Billion |

| Market Size (2031) | USD 18.01 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

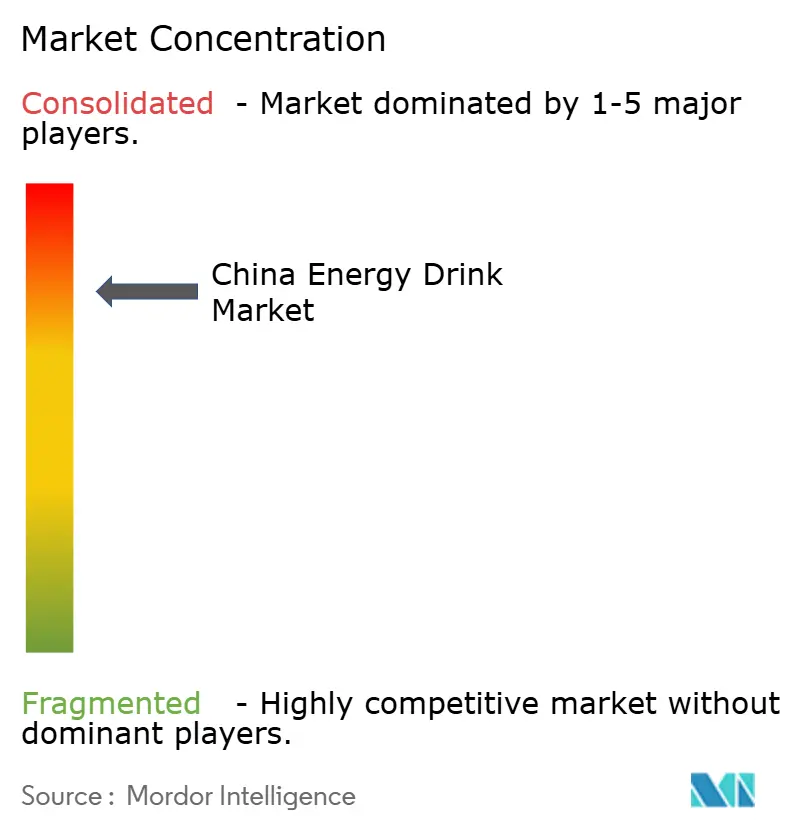

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Energy Drink Market Analysis by Mordor Intelligence

The China energy drinks market size is expected to grow from USD 11.63 billion in 2025 to USD 12.51 billion in 2026 and is forecast to reach USD 18.01 billion by 2031 at 7.56% CAGR over 2026-2031. This growth represents a CAGR of 8.10% during the forecast period. The market's expansion is driven by increasing consumer demand for functional beverages that provide instant energy and enhanced performance. Factors such as rising disposable incomes, urbanization, and a growing health-conscious population are further fueling the adoption of energy drinks across the country. Additionally, the introduction of innovative flavors and packaging by key players is expected to attract a broader consumer base, contributing to the market's robust growth trajectory. The growing prevalence of hectic lifestyles, particularly among the younger demographic and working professionals, has amplified the demand for convenient energy-boosting solutions, positioning energy drinks as a preferred choice. Furthermore, the increasing penetration of e-commerce platforms has enhanced product accessibility, enabling manufacturers to reach a wider audience. The market is also witnessing a shift toward sugar-free and natural ingredient-based energy drinks, aligning with the evolving preferences of health-conscious consumers. Key players in the market are actively investing in marketing campaigns and endorsements by celebrities and influencers to strengthen brand visibility and consumer engagement.

Key Report Takeaways

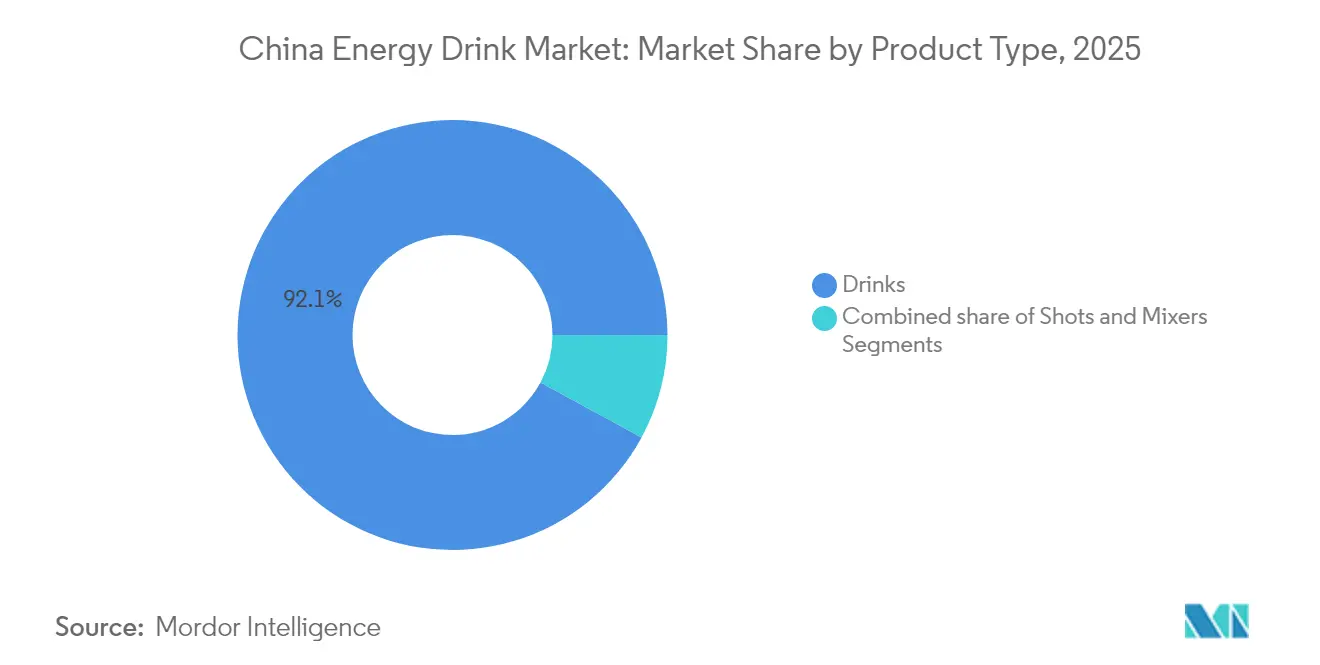

- By product type, drinks led with 92.10% revenue share in 2025, while shots are set to expand at an 8.09% CAGR to 2031.

- By packaging, cans held 76.75% of the China energy drinks market share in 2025; PET/Glass bottles are projected to grow at an 8.21% CAGR.

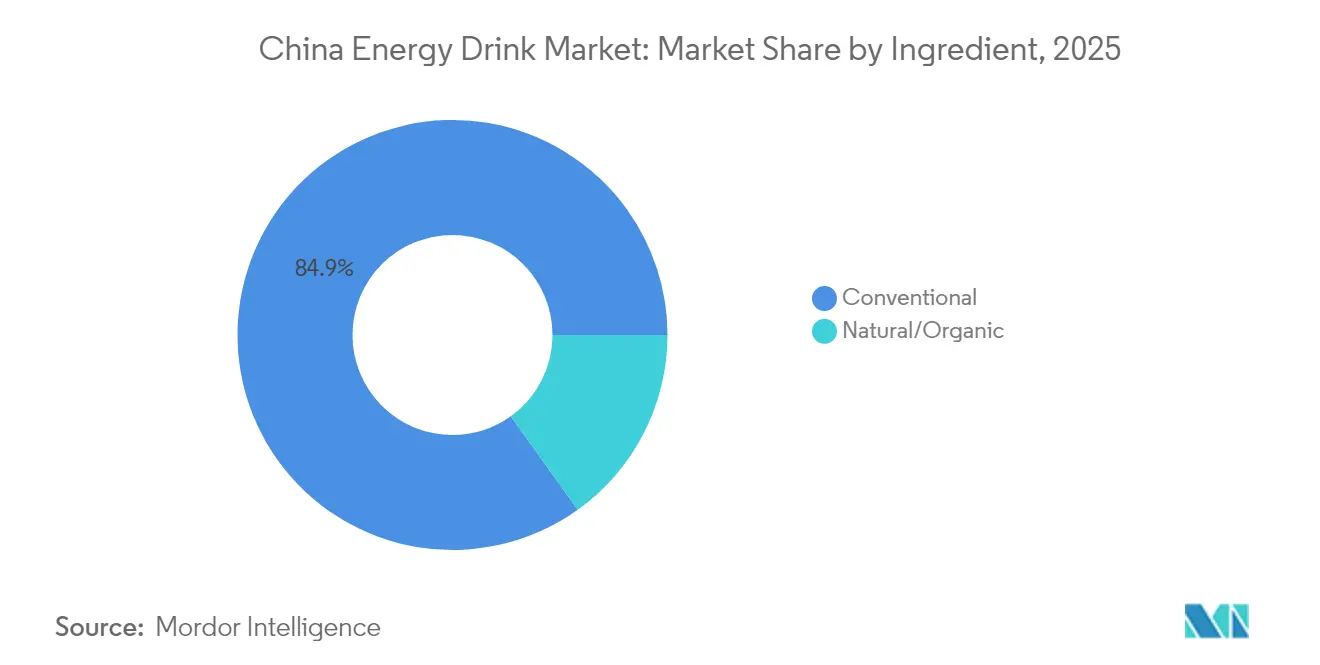

- By ingredient, conventional formulations commanded 84.90% share of the China energy drinks market size in 2025; natural/organic variants exhibit a 8.62% CAGR through 2031.

- By distribution channel, off-trade accounted for 87.25% share of the China energy drinks market in 2025, whereas on-trade is forecast to rise at an 7.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Energy Drink Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product Innovation in Terms of Flavor and Ingredients | +1.5% | National, with early gains in Tier-1 cities | Medium term (2-4 years) |

| Rising Influence of Endorsements and Social Media Marketing | +1.8% | National, concentrated in urban markets | Short term (≤ 2 years) |

| Strong Demand From Fitness-Conscious Consumers | +1.2% | Tier-1 and Tier-2 cities primarily | Medium term (2-4 years) |

| Growing Demand For On-The-Go Healthy Beverages | +1.1% | Urban centers with high mobility | Short term (≤ 2 years) |

| Rapid Urbanization Driving the Market Growth | +0.9% | Tier-2 and Tier-3 cities expansion | Long term (≥ 4 years) |

| Increasing Youth Population | +0.6% | National demographic shift | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Innovation in Terms of Flavor and Ingredients

In the China energy drink market, product innovation in terms of flavor and ingredients serves as a significant market driver. Manufacturers are increasingly focusing on introducing unique and localized flavors to cater to the diverse taste preferences of Chinese consumers. For instance, flavors inspired by traditional Chinese ingredients, such as goji berries, ginseng, and chrysanthemum, are gaining popularity. Additionally, there is a growing emphasis on incorporating functional ingredients, such as vitamins, minerals, amino acids, and natural extracts, to align with the rising demand for health-conscious and performance-enhancing beverages. These functional ingredients not only provide energy but also offer additional health benefits, such as improved focus, hydration, and recovery, which resonate well with the evolving consumer preferences. Furthermore, the trend of clean-label products is influencing the market, with consumers increasingly seeking beverages free from artificial additives, preservatives, and excessive sugar content. This has prompted manufacturers to explore natural sweeteners, such as stevia and monk fruit, as well as organic and plant-based ingredients to enhance the appeal of their products.

Strong Demand From Fitness-Conscious Consumers

The growing awareness of health and fitness among consumers in China is significantly driving the demand for energy drinks. With an increasing number of individuals adopting active lifestyles and prioritizing physical well-being, energy drinks have become a popular choice to support their fitness goals. These beverages are often marketed as products that enhance energy levels, improve performance, and aid in recovery, making them highly appealing to fitness-conscious consumers. Additionally, the rise in gym memberships, participation in sports, and other physical activities has further fueled the consumption of energy drinks in the country. The increasing prevalence of fitness trends, such as yoga, aerobics, and high-intensity interval training (HIIT), has also contributed to the growing demand for energy drinks, as these beverages are perceived to provide the necessary stamina and hydration required for such activities. Furthermore, the influence of social media and fitness influencers has played a crucial role in promoting energy drinks as an essential part of a healthy and active lifestyle.

Rapid Urbanization Driving the Market Growth

Rapid urbanization in China is significantly driving the growth of the energy drink market. According to World Bank data, the urban population of China accounted for 66% in 2024, highlighting the substantial shift of the population from rural to urban areas [1]Source: World Bank, "Urban population (% of total population)- China", data.worldbank.org. As urban areas expand and populations concentrate in cities, there is an increasing demand for convenient and functional beverages like energy drinks. The fast-paced lifestyle in urban regions has led to a growing need for quick energy boosts, making energy drinks a preferred choice among consumers. Additionally, the rise in disposable income and changing consumer preferences in urban areas are further contributing to the market's growth. The increasing number of working professionals and students in cities, who often seek energy drinks to enhance focus and productivity, is also playing a crucial role in driving demand. Furthermore, urbanization has facilitated the expansion of modern retail channels, such as supermarkets, hypermarkets, and convenience stores, making energy drinks more accessible to a broader consumer base. This trend is expected to continue, further propelling the growth of the energy drink market in China during the forecast period.

Increasing Youth Population

The increasing youth population is driving the market growth positively. With a growing number of young individuals, there is a rising demand for energy drinks, as these products are often marketed as lifestyle beverages that cater to the active and dynamic preferences of this demographic. The youth segment, characterized by a higher inclination toward fitness, sports, and on-the-go consumption, is contributing to the expanding consumer base for energy drinks. Additionally, the younger generation's openness to experimenting with new flavors and brands further fuels market growth. This demographic shift is expected to play a pivotal role in shaping the energy drink market in China during the forecast period. According to the Economic and Social Commission for Asia and the Pacific, the percentage of the male and female population aged 15-35 years in China was observed to be 53.7% and 47.3%, respectively, in 2023 [2]Source: Economic and Social Commission for Asia and the Pacific, “China-Key population indicators, 2023”, population-trends-asiapacific.org. This substantial proportion of the youth population highlights the immense potential for energy drink manufacturers to target this age group effectively. The youth population in China is also increasingly influenced by global trends, including the adoption of energy drinks as a means to enhance physical performance, improve focus, and combat fatigue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Over Chemical Ingredients | -0.8% | National, intensified in educated urban markets | Medium term (2-4 years) |

| Consumer Inclination Towards Fresh Juice Products | -0.5% | Tier-1 cities with premium positioning | Short term (≤ 2 years) |

| Intense Market Competition | -0.4% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Rising Awareness Against Sugar | -0.3% | Urban areas with health-conscious consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concers Over Chemical Ingredients

Health concerns regarding the chemical ingredients used in energy drinks are acting as a significant restraint in the China energy drink market. Consumers are increasingly becoming aware of the potential adverse effects associated with the consumption of synthetic additives, artificial sweeteners, and high caffeine content commonly found in energy drinks. This growing awareness is leading to a shift in consumer preferences toward healthier and more natural alternatives. Additionally, regulatory bodies are imposing stricter guidelines and monitoring the use of chemical ingredients in energy drinks, further impacting the market. Manufacturers are facing challenges in reformulating their products to meet these evolving consumer demands and regulatory standards, which is hindering the market's growth potential. Furthermore, the increasing prevalence of health issues such as obesity, diabetes, and cardiovascular diseases, which are often linked to the excessive consumption of energy drinks, is amplifying these concerns.

Rising Awareness Against Sugar

In the China Energy Drink Market, rising awareness about the adverse health effects of excessive sugar consumption acts as a significant market restraint. Consumers are becoming increasingly conscious of the link between high sugar intake and health issues such as obesity, diabetes, and cardiovascular diseases. According to the National Institute of Health, diabetes prevalence in Chinese adults aged 20–79 years is projected to increase from 8.2% to 9.7% during 2020–2030 [3]Source: National Institute of Health, “Projected rapid growth in diabetes disease burden and economic burden in China: a spatio-temporal study from 2020 to 2030”, pmc.ncbi.nlm.nih.gov. This alarming trend has further heightened consumer awareness and shifted preferences toward healthier alternatives or sugar-free energy drink options. Additionally, government regulations and campaigns aimed at reducing sugar consumption further impact the market. These initiatives include imposing taxes on sugary beverages and mandating clear labeling of sugar content, which influences purchasing decisions. As a result, manufacturers in the energy drink market face challenges in balancing taste, functionality, and health-conscious demands, which could potentially hinder market growth during the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drinks Dominate Through Distribution Scale

In the China energy drink market, traditional energy drinks dominate with a substantial 92.10% market share in 2025. This dominance highlights the segment's robust distribution infrastructure and the strong consumer preference for conventional energy drink formats. These drinks benefit from widespread availability across various retail channels, including supermarkets, convenience stores, and online platforms, ensuring easy access for consumers. Their established brand presence, coupled with extensive marketing campaigns, has solidified their position as a go-to energy solution for a diverse consumer base. Traditional energy drinks cater to a wide demographic, including athletes, students, and working professionals, who rely on these beverages for a quick and reliable energy boost.

Conversely, the shots segment is emerging as the fastest-growing category in the market, with an impressive 8.09% CAGR projected through 2031. This growth is driven by increasing consumer demand for compact and concentrated energy solutions that offer convenience and precise dosing. Energy shots are particularly appealing to urban consumers with fast-paced lifestyles, as they provide the same energy benefits as traditional drinks but in smaller, portable volumes. These products are often marketed as premium offerings, with innovative formulations that include natural ingredients, added nutrients, or functional benefits, such as improved focus or endurance. The willingness of consumers to pay higher per-unit prices for these attributes reflects a growing trend toward functional and on-the-go energy products in China.

By Packaging Type: Cans Lead Despite Sustainability Pressures

In 2025, cans dominate the China energy drink market, holding a significant 76.75% market share. This dominance is attributed to their superior shelf stability, which ensures longer product life and consistent quality. Additionally, cans offer excellent brand visibility, making them a preferred choice for manufacturers aiming to capture consumer attention on retail shelves. Global brands like Red Bull and Monster have played a pivotal role in associating cans with premium energy drink experiences, further solidifying their position in the market. The lightweight and recyclable nature of cans also contribute to their widespread adoption, aligning with the growing focus on convenience and environmental considerations.

Conversely, PET and glass bottles are emerging as the fastest-growing segment in the China energy drink market, with a robust CAGR of 8.21% projected through 2031. This growth is primarily driven by increasing consumer awareness of sustainability and the environmental impact of packaging materials. PET and glass bottles are perceived as more eco-friendly options, particularly when paired with advancements in recycling technologies. Furthermore, their resealable design supports multiple consumption occasions, catering to the evolving lifestyles of consumers who prefer on-the-go and portion-controlled drinking. These factors, combined with the rising demand for premium and customizable packaging, are propelling the adoption of PET and glass bottles in the market.

By Ingredient: Natural/Organic Gains Momentum Despite Conventional Dominance

In 2025, conventional ingredients dominate the China energy drink market, holding an 84.90% share. This dominance is attributed to their cost-effectiveness and the presence of robust, well-established supply chains that ensure widespread availability. These ingredients enable manufacturers to produce energy drinks at scale while maintaining consistent product quality, which appeals to a broad consumer base. Additionally, the familiarity and reliability associated with conventional ingredients make them a preferred choice for many consumers, particularly those who prioritize affordability and accessibility over ingredient innovation.

Natural and organic ingredients, on the other hand, represent the fastest-growing segment in the China energy drink market, with a projected CAGR of 8.62% through 2031. This growth is driven by an increasing number of health-conscious consumers who demand greater transparency in ingredient sourcing and formulation. These consumers are actively seeking energy drink options that align with their wellness-focused lifestyles, emphasizing natural and organic components. The rising awareness of the potential health benefits associated with such ingredients, coupled with a growing preference for sustainable and clean-label products, is further propelling the adoption of natural and organic energy drinks in the market.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Recovery

In 2025, off-trade channels dominate the China energy drink market with an 87.25% market share, highlighting their critical role in ensuring widespread consumer accessibility. Convenience stores, supermarkets, and online retail platforms are the primary drivers of this dominance, offering consumers easy access to energy drinks at competitive prices. The growing penetration of e-commerce platforms, coupled with the increasing preference for home delivery services, has further strengthened the position of off-trade channels. Additionally, the convenience of purchasing energy drinks alongside other daily essentials in supermarkets and convenience stores continues to attract a broad consumer base, particularly in urban areas.

On the other hand, on-trade channels in China are expected to exhibit significant growth potential, with a projected CAGR of 7.98% through 2031. This growth is primarily driven by the recovery of the foodservice sector and the rising trend of premiumization in energy drink consumption. Restaurants, bars, and entertainment venues are increasingly incorporating energy drinks into their offerings, catering to a growing consumer demand for premium and innovative beverage options. The shift in consumer preferences towards social and experiential consumption, particularly among younger demographics, is further boosting the relevance of on-trade channels.

Geography Analysis

China's energy drinks market showcases regional consumption patterns shaped by varying levels of economic development, urbanization, and cultural nuances. In Tier-1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen, residents spend the most on energy drinks. This trend is fueled by fast-paced lifestyles, higher disposable incomes, and a heightened awareness of international brands and wellness trends. These major cities act as testing grounds for innovations, where premium formulations and new products gain traction before reaching wider markets. The concentration of affluent consumers and advanced retail infrastructure in these cities further supports the introduction of high-end products and experimental offerings.

Meanwhile, Tier-2 and Tier-3 cities emerge as the main frontiers for energy drink growth. These areas, witnessing swift urbanization and infrastructure advancements, boast a rising middle class with increased purchasing power. This evolution not only opens up new consumption opportunities but also enhances retail accessibility. Consumers in these burgeoning markets lean towards value-driven products and trusted brands with established safety records. This presents a golden opportunity for market leaders to broaden their distribution networks while still holding a premium stance in the more affluent Tier-1 cities. Additionally, the growing penetration of modern trade channels and e-commerce platforms in these regions is further facilitating market expansion.

As brands navigate this landscape, their geographic distribution strategy becomes pivotal for gaining a competitive edge. Success hinges on tailoring approaches to cater to the unique demands of each region, all while upholding a unified brand identity and consistent product quality. Regional tastes dictate preferences in flavor profiles, packaging styles, and pricing. This not only paves the way for localized product innovations but also poses a challenge for manufacturers striving for economies of scale amidst diverse market demands. Companies must balance the need for customization with operational efficiency to effectively capture market share across these varied geographic segments.

Regulatory Landscape

Energy drinks marketed as ordinary beverages in China must comply with the national food safety framework for beverages, including GB 7101-2022, which governs core safety and compositional requirements for beverage products. Where brands pursue functional or health-related claims, additional compliance pathways apply under the State Administration for Market Regulation (SAMR) health food registration/filing system, which creates a practical split between standard beverage compliance and health-food-style substantiation for stronger functional positioning.

For imports, the General Administration of Customs (GACC) updated its overseas food manufacturer registration regime with Decree No. 280, effective June 1, 2026, replacing the prior Decree 248 framework and reinforcing risk-based registration management for facilities exporting foods to China. Alongside mandatory national standards, voluntary industry standards such as T/CIET 408-2024 and T/CEAC 023-2024 provide additional technical specifications for energy drink quality, and they can affect procurement, QA, and retailer acceptance requirements even when they are not legally binding.

Competitive Landscape

The China energy drink market operates within a highly consolidated competitive landscape, highlighting the oligopolistic nature of the market, where a few key players dominate the industry. These established companies benefit from significant market power, allowing them to influence pricing, product offerings, and overall market trends. Their dominance is further reinforced by their ability to invest heavily in marketing, research, and product innovation, creating substantial barriers for new entrants and smaller competitors. The high concentration also reflects the ability of these players to adapt to changing consumer preferences and regulatory requirements, further solidifying their position.

One of the primary factors contributing to the dominance of these players is their extensive distribution networks. These networks enable them to ensure widespread availability of their products across urban and rural areas, catering to a diverse consumer base. Additionally, their strong relationships with retailers and distributors provide them with a competitive edge in securing prime shelf space and maintaining consistent product visibility. This strategic advantage allows them to effectively reach their target audience and sustain their market position. Furthermore, the ability to leverage e-commerce platforms has expanded their reach, particularly among younger, tech-savvy consumers, who form a significant portion of the energy drink market's target demographic.

Brand recognition also plays a crucial role in maintaining the market dominance of these key players. Over the years, these companies have invested significantly in building strong brand identities through advertising campaigns, sponsorships, and endorsements, particularly in sports and entertainment sectors. This has resulted in high consumer loyalty and trust, making it challenging for new entrants to compete. Additionally, these brands often introduce limited-edition products and flavors to maintain consumer interest and drive repeat purchases.

China Energy Drink Industry Leaders

-

Monster Beverage Corporation

-

The Coca-Cola Company

-

PepsiCo,Inc.

-

Eastroc Beverage Group Co., Ltd.

-

Red Bull GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrating around reformulation and portfolio segmentation that align functional benefits with tighter compliance and consumer scrutiny on sugar and ingredients. With conventional formulations still dominating (84.90% share in 2025), while natural/organic variants expand from a smaller base, brands can scale sugar-free and clean-label energy propositions using recognizable ingredient themes (for example, ginseng or goji-inspired flavoring cues) while remaining within beverage standard requirements such as GB 7101-2022. The fast-growing shots sub-segment also creates room for premium, precise-dosing formats for urban, on-the-go use cases, with distribution support through off-trade and online channels.

Execution and operational capability are also shaping competitive outcomes. Monster Beverage highlighted using The Coca-Cola Company distribution network to deepen reach in China, including targeted channel strategies such as university-focused penetration, which supports broader availability and faster new-SKU rollout. Domestic leaders are concurrently funding multi-base capacity and supply-chain upgrades, exemplified by Eastroc Beverage raising capital in Hong Kong in January 2026 to expand production capacity and upgrade its supply chain. This keeps manufacturing footprint, traceability, and channel coverage central to shelf access and pricing power in a highly consolidated market.

Recent Industry Developments

- June 2026: Monster Beverage stated it is leveraging The Coca-Cola Company distribution system to expand its energy drink presence in China, including a push through university-related channels. This strengthens route-to-market reach and supports faster rollout capability in high-traffic urban consumption occasions, increasing competitive pressure on shelf space and promotional intensity.

- January 2026: Eastroc Beverage launched its Hong Kong listing and raised HKD 10.14 billion, positioning the proceeds toward production capacity expansion and supply-chain upgrades. This financing supports faster scale-up of manufacturing and logistics, reinforcing the advantage of large domestic players in a highly consolidated market.

- November 2024: TCP Group announced a growth roadmap that included launching a third manufacturing facility in Guangxi by early 2025. The planned capacity expansion is intended to underpin localized supply and broaden distribution coverage, supporting competitive positioning as brands add SKUs and packaging options for different city tiers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of energy drinks sold in China that are positioned for mental or physical stimulation, typically using caffeine and similar functional ingredients. It includes both carbonated and non-carbonated formats across retail and foodservice, measured on a sales value basis.

Scope exclusions: We exclude broader soft drinks that do not make an energy or stimulation claim, and we do not count DIY mixes that are not sold as finished energy drinks.

Segmentation Overview

-

By Product Type

- Drinks

- Shots

- Mixers

-

By Packaging Type

- PET/Glass Bottles

- Cans

- Other Packaging Types

-

By Ingredient

- Conventional

- Natural/Organic

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Convenience Stores/Grocery Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Others Distribution Channel

Data Sources, Market Sizing, and Validation

Desk Research

We start by building a fact base around demand drivers and the selling environment in China, then convert those signals into sizing inputs. Public sources such as China Customs trade statistics, National Bureau of Statistics releases, State Administration for Market Regulation notices, and China National Food Safety Standard documentation help us understand category definitions, labeling rules, and broader consumption direction.

To shape the model, we also review company annual reports and investor presentations, reputable press coverage, and association websites for beverage and retail organizations. We include peer-reviewed nutrition and ingredient literature to track functional claims and formulation shifts. Where needed, we use paid subscriptions that compile company financials and separate paid subscriptions that track shipment-level import and export records to sanity check scale and pricing movements. These desk sources are illustrative only, and additional references were also used for data collection, cross-checks, and clarifying open questions.

Primary Interviews and Surveys

Primary interviews are used to test what we saw in desk research, especially around channel mix, price ladders, and what is actually selling through across different city tiers. We spoke with a mix of brand-side managers, distributors, retailers, and participants from ingredients and packaging, then rechecked assumptions across major consumption regions in China so the final market model does not rely on a single viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | |

| Mid tier: 46% | Functional/Unit leaders: 35% | |

| Smaller Players: 15% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the China demand pool is reconstructed by mapping energy drink consumption through on-trade and off-trade, then translating it into value using observed price bands by pack type and channel. Once that structure is stable, we run selective bottom-up checks, such as rolling up a sample of supplier and brand revenues where disclosures exist, and validating implied volumes using sampled ASP multiplied by estimated units sold.

Key inputs that move the model include retail shelf pricing and promotion intensity, the online share of beverage purchases, the mix of cans versus PET or glass, ingredient positioning shifts (conventional versus natural), and the pace of sugar-free or low-calorie adoption. Because seasonality is visible in this category, we also factor in peak-period uplift patterns described by channel respondents, and then adjust for unusual years with one-off demand spikes.

For forecasting, we use scenario analysis so the base case reflects expected price and volume movement while still allowing both a more conservative and a more aggressive path. Assumptions are anchored to expert feedback on premiumization, channel growth (especially online), and realistic capacity and distribution expansion. Where bottom-up disclosure is missing for smaller brands, gaps are handled by applying observed channel assortment counts and typical price ladders, and then rechecking the implied totals against independent demand signals.

Data Validation & Update Cycle

Outputs are checked in more than one way before they are finalized, and the first check is whether the model behaves like the real category, including sensible channel shares, pack mix, and price progression. After that, we run variance checks against independent indicators such as trade flows, major retail activity signals, and publicly visible pricing patterns, and we review any outliers until the driver is understood.

A second analyst reviews the key assumptions and calculation logic, and follow-up calls are triggered when a metric shifts materially or when a respondent describes a different channel reality than expected. The report is refreshed annually, with interim updates when there are material events that can move prices or demand. Before delivery, a final pass is completed so the client receives the most current view available at that time.

Mordor Intelligence's China Energy Drink Market Size Compared With Other Published Estimates

Published market sizes for China energy drinks often vary because different studies do not count the same product set, and they also apply different price and channel assumptions. Timing matters as well, since the same year can look larger or smaller depending on currency conversion dates and how quickly new information is incorporated.

The main gap comes from whether energy shots and energy mixers are included, and from how fast average selling prices are allowed to rise across online and offline channels. In Mordor Intelligence's approach, these adjacent formats are explicitly included in the product scope, and ASPs are validated using channel-level price ladders before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.51 B (2026) | |

| Industry Publisher A | USD 6.50 B (2024) | Uses an earlier base year and appears to anchor pricing and distribution on a narrower mainstream energy drink definition, which can undercount newer formats and the recent shift in channel mix. |

| Syndicated Summary B | USD 9.65 B (2024) | Works off a different base year and forecast window, and the higher trajectory can be driven by more aggressive ASP progression and looser validation of on-trade versus off-trade splits across China. |

Taken together, the spread is mostly explained by scope alignment and how price and channel shares are treated in the model. When product formats, channel weights, and ASP logic are stated clearly and checked against observable signals, the resulting market size is easier to replicate and update with new developments.

Key Questions Answered in the Report

What is the current size of the China energy drink market?

The market is worth USD 12.51 billion in 2026 and is forecast to reach USD 18.01 billion by 2031.

How fast is the China energy drinks market expected to grow?

It is projected to expand at an 7.56% CAGR during 2026-2031, driven by product innovation and rising health-oriented demand.

Which product segment is growing the quickest?

Energy shots are expanding at an 8.09% CAGR through 2031, reflecting consumer appetite for concentrated, portable formats.

Why are natural and organic ingredients important?

Health-conscious consumers increasingly prefer clean-label drinks, giving natural or organic formulations a 8.62% CAGR advantage.

Page last updated on: