Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

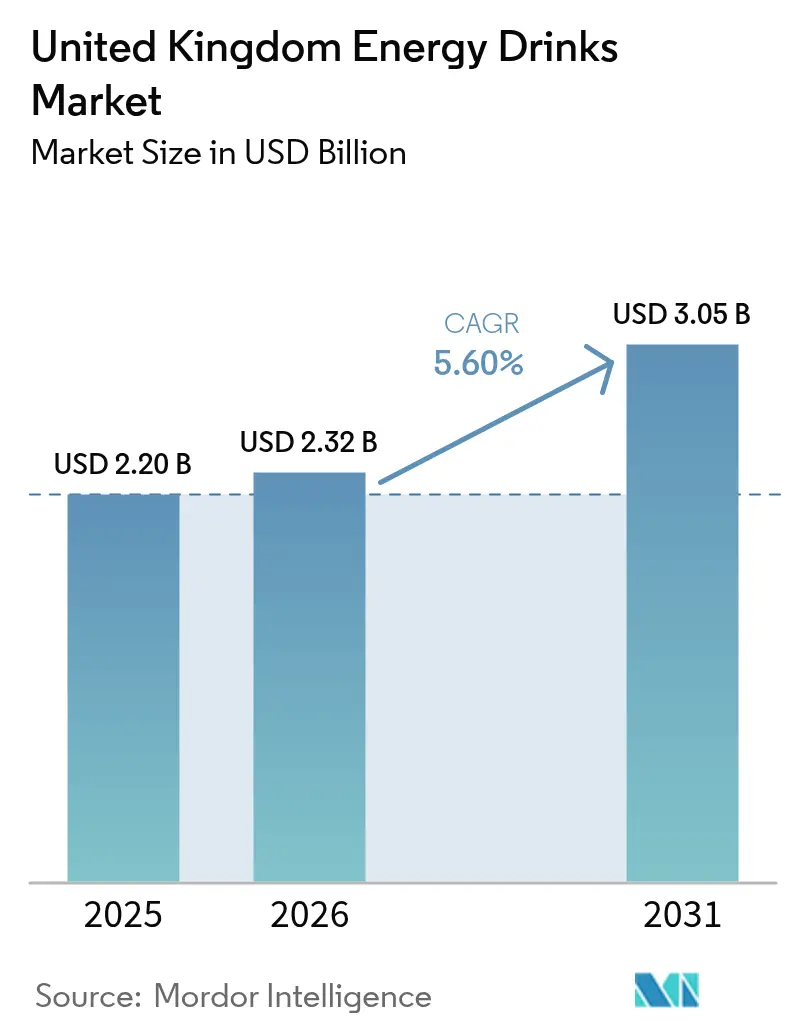

| Base Year Market Size (2025) | USD 2.20 Billion |

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Energy Drinks Market Analysis by Mordor Intelligence

The United Kingdom energy drinks market size is expected to grow from USD 2.20 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 3.05 billion by 2031 at 5.6% CAGR over 2026-2031. Despite tightening sugar-tax thresholds, with limits dropping from 5 g to 4 g sugar per 100 ml, consumption continues to rise, pushing leading brands to rapidly reformulate. Proposed measures, including a nationwide sales ban for those under 16 and the October 2025 HFSS advertising watershed, challenge marketing budgets. However, they also hasten the industry's pivot towards low-sugar, functional beverages. Innovations like natural caffeine sources, zero-sugar recipes, and sports-centric formulations are broadening the consumer appeal. In response to surging aluminum prices, manufacturers are channeling investments into high-speed canning lines and distribution hubs to safeguard their margins. Retailers, recognizing the trend, are amplifying shelf space for energy drinks, which are increasingly seen as impulse buys by busy urban shoppers.

Key Report Takeaways

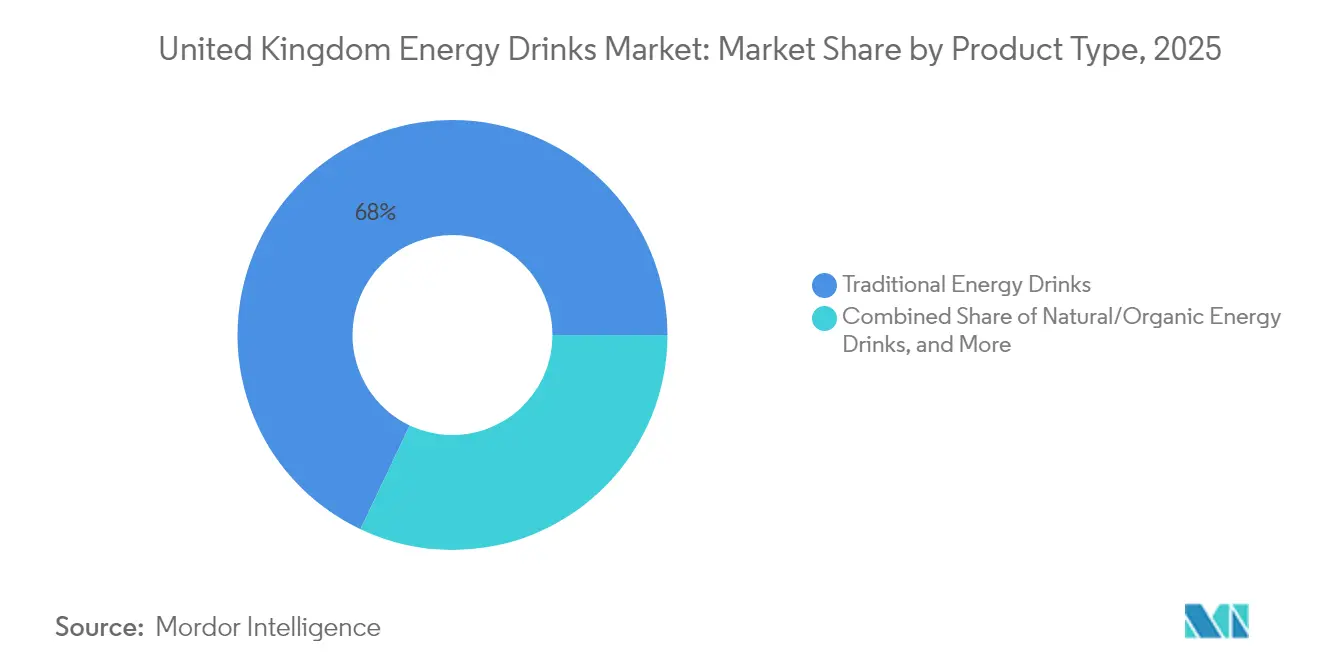

- By product type, traditional energy drinks led with 67.96% of the United Kingdom energy drinks market share in 2025, whereas natural and organic variants are projected to expand at a 7.61% CAGR through 2031.

- By packaging type, cans accounted for a 77.88% share of the United Kingdom energy drinks market size in 2025, while PET bottles are project to advance at a 7.15% CAGR between 2026 and 2031.

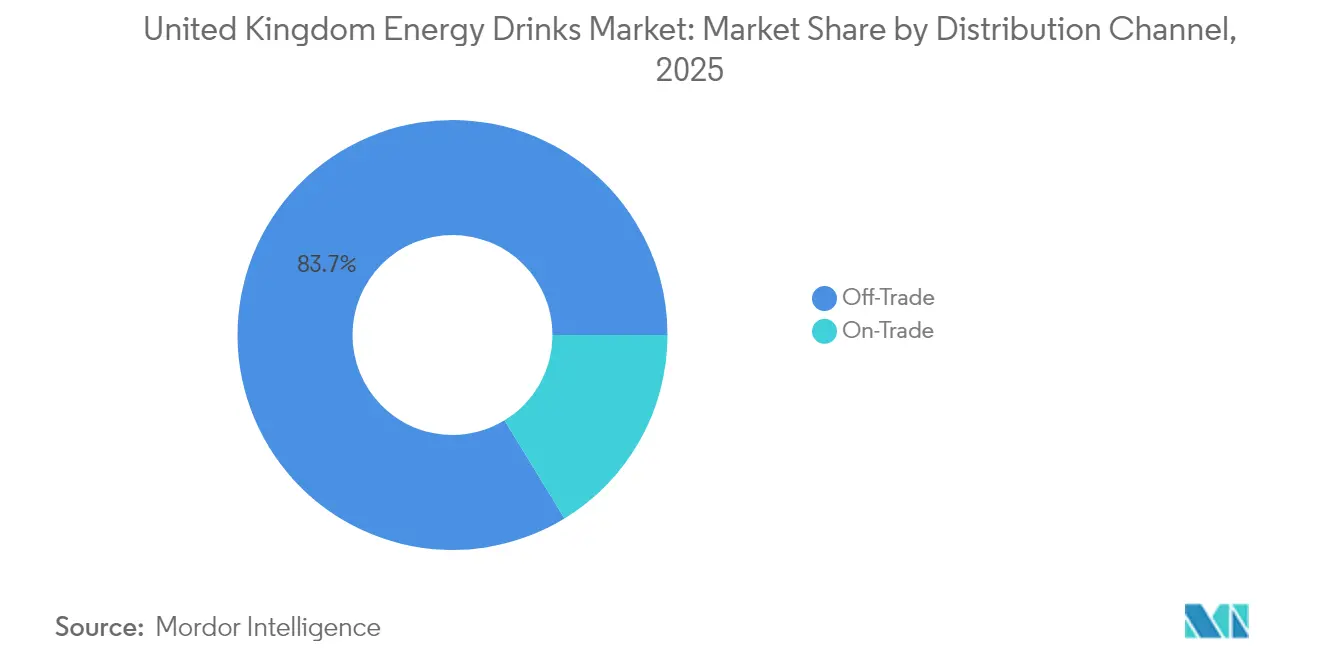

- By distribution channel, off-trade held 83.72% of sales in 2025, but on-trade is forecast to record the highest 6.34% CAGR through 2031.

- By geography, England captured 85.02% of the market value in 2025, and Northern Ireland is expected to post a 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban lifestyle and convenience demand | +1.2% | England core, spill-over to Scotland and Wales | Medium term (2-4 years) |

| Advancements in production technology | +0.8% | National, early gains in Rugby, Sunderland, Peterborough | Long term (≥ 4 years) |

| Premiumization and demand for healthier ingredients | +1.5% | England and Scotland primary, Wales emerging | Medium term (2-4 years) |

| Aggressive advertising and events sponsorship | +0.9% | National, major urban centers | Short term (≤ 2 years) |

| Sugar-free SKUs targeting diabetic population | +1.1% | National, stronger in England and Scotland | Medium term (2-4 years) |

| Rising demand among active and sports enthusiasts | +1.3% | National, higher penetration in England | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Lifestyle and Convenience Demand

As urban professionals juggle demanding schedules, they're turning to energy drinks for a quick boost. Convenience stores, noting this trend, plan to expand their energy drink shelf space by 21% in 2024, as reported by Convenience Store News. This surge is especially pronounced in metropolitan areas, where young adults aged 18-24 are consuming these functional beverages at rates significantly higher than the national average. Reflecting this convenience-driven trend, half of the shoppers now favor 250ml cans over the traditional 500ml formats. Retailers, keenly aware of the impulse-driven nature of these purchases, are strategically placing energy drinks in high-traffic areas. This urban trend is particularly advantageous for brands that offer a range of functional ingredients, moving beyond just caffeine, as consumers increasingly seek holistic wellness solutions amidst their busy lives.

Advancements in Production Technology

Key players in the manufacturing sector are investing heavily in production capabilities to enhance efficiency and differentiate their products. For example, Britvic has committed to operational improvements with a GBP 25 million upgrade to its distribution center and a GBP 13 million new canning line in Rugby. These technological advancements enable manufacturers to quickly adapt to regulatory changes, such as evolving sugar tax thresholds, while supporting premiumization trends. Modern production systems now seamlessly incorporate functional ingredients, including adaptogens and nootropics, to enhance overall well-being. Britvic’s London Essence Freshly Infused range exemplifies innovation, using micro-dosing technology to reduce packaging waste while delivering customizable flavor profiles.

Premiumization and Demand for Healthier Ingredients

Consumers are increasingly willing to pay a premium for functional wellness drinks, signaling a lucrative opportunity in the market. The zero-sugar segment is witnessing a surge, fueled by health-conscious individuals who desire energy solutions that align with their dietary goals. Brands like Tenzing are tapping into this trend, introducing products boasting 200mg of natural caffeine sourced from premium ingredients like green tea and guayusa extract. However, this premiumization isn't limited to just the ingredients. Brands are also integrating functional benefits, such as cordyceps mushrooms, magnesium, and vitamin complexes, to validate their elevated price points. This trend underscores a pivotal shift: moving from merely providing energy to offering holistic wellness support. As a result, brands are not only enjoying fatter margins but are also fostering consumer loyalty through these perceived health advantages.

Aggressive Advertising and Events Sponsorship

Strategic marketing investments bolster brand awareness and fuel category growth. However, impending HFSS restrictions, set to take effect in October 2025, are poised to fundamentally alter promotional strategies. As per the Department of Health and Social Care, the 9pm watershed for television advertising, coupled with a blanket online advertising ban for high-sugar products, is nudging brands towards alternative engagement channels[1]Source: Department of Health and Social Care, “Restricting Advertising of Less Healthy Food or Drink,” gov.uk. Red Bull's Summer Edition campaigns underscore the potency of limited-time offerings, with NIQ data revealing that flavored variants account for nearly one-third of the functional energy market's growth. As brands navigate these regulatory waters, sports sponsorship and experiential marketing have surged in prominence, serving as compliant touchpoints with target audiences. Furthermore, the industry's pivot towards influencer partnerships and brand collaborations highlights a strategic adaptation to advertising constraints, ensuring continued consumer engagement through genuine endorsements and seamless lifestyle integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high caffeine and sugar | -1.8% | National, stronger impact in England and Scotland | Short term (≤ 2 years) |

| Sugar tax and government sugar reduction initiatives | -1.2% | National, uniform impact across all regions | Medium term (2-4 years) |

| Rising aluminum can costs affecting packaging prices | -0.7% | National, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| HFSS advertising restrictions | -1.1% | National, with stronger impact in major media markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over High Caffeine and Sugar

Public health advocates ramp up pressure on energy drink consumption, especially among the youth, as studies link these beverages to heightened anxiety and declining academic performance. Responding to this mounting evidence, the UK government, backed by 57 studies involving over a million children, moves to ban sales to those under 16, as reported by BBC News. The Committee on Toxicity of Chemicals in Food notes that while energy drinks account for just 5.2% of total caffeine consumption, they significantly shape caffeine intake patterns[2]Source: Committee on Toxicity, “Energy Drinks Statement,” cot.food.gov.uk. Recognizing these health concerns, major supermarkets impose voluntary age restrictions, a move supported by over 90% of respondents in consultations advocating for sales bans to minors. In light of this scrutiny, manufacturers pivot towards reformulating their products, prioritizing natural ingredients and functional benefits without compromising on energy delivery. The evolving regulatory landscape increasingly rewards brands that showcase a commitment to health responsibility, evident through their product innovations and restrained marketing approaches.

Sugar Tax and Government Sugar Reduction Initiatives

Manufacturers grapple with heightened cost pressures and the imperative to reformulate due to the proposed strengthening of the Soft Drinks Industry Levy. As per HM Revenue & Customs, a consultation is underway to reduce the minimum sugar threshold from 5g to 4g per 100ml, impacting product formulations industry-wide[3]Source: HM Revenue & Customs, “Strengthening the Soft Drinks Industry Levy,” gov.uk. Since its inception, the levy has successfully driven a 46% reduction in sugar content in the targeted drinks, underscoring its efficacy in instigating behavioral shifts within the industry, as highlighted by the British Dental Journal[4]Source: Rachel Marshman, “The ‘sugar tax’ seven years on,” British Dental Journal, nature.com. The Guardian notes that the tax's triumph in slashing children's sugar intake from soft drinks not only justifies government intervention but also bestows competitive edges to brands that have swiftly adopted low-sugar formulations. Manufacturers are in a constant tug-of-war, striving to align taste preferences with tax benefits, a challenge that demands advanced sweetening techniques and a well-informed consumer base. Furthermore, the potential for the levy to extend its reach to other high-sugar categories casts a shadow of uncertainty over long-term product development strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Dominance Faces Natural Disruption

In 2025, traditional energy drinks commanded a dominant 67.96% market share. However, it's the natural and organic variants that are surging ahead, boasting an impressive 7.61% CAGR growth rate projected through 2031. This trend underscores a growing divide in consumer preferences: a steadfast loyalty to established brands juxtaposed with a rising health consciousness. Responding to heightened health concerns and regulatory mandates, manufacturers are pivoting towards sugar-free and low-calorie offerings, with zero-sugar variants leading the charge. While energy shots carve out a niche for those prioritizing convenience, the broader category of energy drinks is diversifying, introducing innovative formats such as powdered variants and functional blends.

The swift ascent of the natural and organic segment underscores a consumer readiness to invest in premium products for perceived health advantages. A testament to this trend's lucrative potential is Tenzing's debut of its "world's strongest natural energy drink," boasting 200mg of caffeine sourced entirely from nature. Meanwhile, traditional energy formulations grapple with mounting pressures from health advocates and regulatory bodies, pushing legacy brands to reconsider and reformulate their offerings. This segment's transformation is emblematic of a larger consumer shift towards transparency, clean labeling, and functional nutrition. Brands that adeptly communicate their natural positioning while ensuring energy efficacy stand poised to capitalize on these evolving consumer sentiments.

By Packaging Type: Cans Dominate While Sustainability Drives Innovation

In 2025, aluminum cans dominated with a 77.88% market share, underscoring consumer preferences for portability, brand visibility, and a sense of freshness. Yet, it's PET bottles that chart the most robust growth, boasting a 7.15% CAGR through 2031, fueled by convenience and sustainability drives. As environmental awareness reshapes consumer choices and regulatory landscapes, the packaging industry stands at a crossroads. Glass bottles, despite their premium pricing and logistical hurdles, carve out a niche, resonating with eco-conscious consumers.

With sustainability at the forefront, the impending Deposit Return Scheme set for October 2027 presents a dual-edged sword of challenges and opportunities, as highlighted by the Department for Environment, Food & Rural Affairs. Leading the charge in environmental stewardship, Britvic pledges to achieve 99.6% recyclable packaging and incorporate 50% recycled PET by 2025. Companies like Purity Soft Drinks are pioneering cap innovations that not only curb litter but also boost recyclability. As the packaging realm evolves, it deftly navigates the tightrope of functionality, sustainability, and cost, all while aligning with consumer demands for environmental accountability.

By Distribution Channel: Off-Trade Leadership With On-Trade Recovery

In 2025, off-trade channels, including supermarkets, convenience stores, and online platforms, account for an 83.72% market share. This stronghold highlights the impulse-buy nature of energy drinks and a consumer preference for convenience. While on-trade channels hold a smaller slice of the market, they boast the fastest growth rate and are expected to expand at a 6.34% CAGR through 2031. This surge signals a rebound for hospitality venues post-pandemic and a trend towards premium offerings. Supermarkets and hypermarkets, with their vast reach and promotional prowess, command the largest share among individual channels.

Convenience stores are stepping up as pivotal growth engines. Retailers are responding to the category's robust performance by allocating more shelf space to energy drinks. Meanwhile, online retail is experiencing a surge, particularly among younger consumers who are drawn to its variety and convenience. This channel's upswing mirrors the broader e-commerce boom and the rise of subscription models. Other channels, such as vending machines and workplace retail, capitalize on the on-the-go consumption trend. As distribution channels evolve, the emphasis on omnichannel strategies grows. Brands are keen to enhance their presence across varied consumer touchpoints, all while navigating shifting shopping habits and regulatory challenges in promotions.

Geography Analysis

In 2025, England commanded a dominant 85.02% market share, a testament to its demographic heft and bustling economic activity. However, mounting regulatory pressures loom over the region, potentially stifling its growth. A proposed ban on energy drink sales to those under 16 could hit English retailers hard, given their concentrated market presence. Meanwhile, restrictions on HFSS advertising, set to kick in from October 2025, will curtail vital promotional avenues, as highlighted by the Department of Health and Social Care. Urban hubs like London, Manchester, and Birmingham, with their convenience-driven lifestyles, see a notable consumption surge, especially among young adults aged 18-24 who frequently indulge in functional beverages. England's manufacturing landscape is bustling, with notable investments like Britvic's GBP 25 million upgrade to its distribution center and enhancements to its Rugby production facility. The region's growth trajectory, extending to 2030, hinges on adeptly maneuvering through these regulatory challenges while keeping consumers engaged through savvy, compliant marketing.

Scotland, despite its smaller market share, showcases distinct dynamics. The cultural significance of Irn Bru underscores unique consumer preferences, and the Scottish government's choice to forgo energy drink sales restrictions further highlights this. While Scotland is warming up to functional beverages, its traditional loyalty to local brands poses hurdles for international energy drink players. Wales, though the smallest regional market, is witnessing steady growth, buoyed by expanding distribution networks and heightened consumer awareness. The Welsh government's alignment with UK-wide initiatives, particularly the Food (Promotion and Presentation) Regulations 2025 targeting HFSS product promotions, underscores a move towards uniform regulatory frameworks across regions, as noted by the Welsh Government.

Northern Ireland stands out with a robust 5.96% CAGR growth rate projected through 2031, riding the wave of cross-border trade and urbanization. Its smaller market size allows for nimble brand positioning and focused marketing. Moreover, its closeness to the Republic of Ireland opens doors to unique distribution avenues. As per the Department for Environment, Food & Rural Affairs, the forthcoming Deposit Return Scheme will see uniform implementation across both England and Northern Ireland, signaling a need for synchronized infrastructure and compliance strategies. The regional growth trends mirror broader economic patterns, with energy drink consumption closely tied to urban density and disposable income. This geographic landscape offers brands a chance to craft tailored regional strategies, all while upholding national brand integrity and adhering to regulatory mandates across the UK.

Competitive Landscape

In the United Kingdom energy drinks market, established players dominate, but niche disruptors are carving out their space. Red Bull GmbH tops the chart with annual sales of GBP 492 million. Following closely are Monster Beverage Corp. and Suntory Holdings' Lucozade brand, each ranking in GBP 322 million. The landscape is shifting, highlighted by Keurig Dr Pepper's bold USD 990 million acquisition of Ghost Energy and Carlsberg's GBP 3.3 billion chase of Britvic[5]Source: Keurig Dr Pepper, “Acquisition of GHOST,” kdp.com. These moves underscore the tightening race for market share, all while navigating regulatory hurdles.

Brands are ramping up their competitive edge, emphasizing functional ingredients, sustainability, and savvy marketing. There's a growing appetite for natural and organic offerings, gaming-centric formulations, and unique regional flavors. While newcomers challenge the status quo, established brands are doubling down on innovation and forging strategic alliances. Take Celsius, for instance: after a swift ascent in the US, they're eyeing the UK market, thanks to Suntory's distribution. Companies are harnessing technology not just for production and sustainability, but also to engage consumers. Many are bolstering their manufacturing prowess and diving into digital marketing, especially to sidestep HFSS advertising constraints.

Brands that prioritize health and environmental concerns are reaping the rewards in today's competitive arena. This shift is largely driven by regulatory bodies, which now favor products with reduced sugar and eco-friendly packaging. Companies are also keenly aware of the value of intellectual property, especially in areas like functional ingredient blends and innovative packaging. While the market hints at further consolidation, there's still room for specialized brands catering to niche consumer segments and regional tastes.

United Kingdom Energy Drinks Industry Leaders

The Coca-Cola Company

Red Bull GmbH

PepsiCo, Inc. (Rockstar Energy)

Suntory Holdings Limited

Monster Energy Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Red Bull launched its White Peach Summer Edition, replacing the previous Curuba Elderflower variant and contributing nearly one-third of functional energy flavored growth according to NIQ data, demonstrating the strategic importance of limited-time offerings in driving category expansion.

- February 2025: Celsius energy drinks officially launched in the UK through an exclusive distribution partnership with Suntory Beverage & Food, bringing the USD 2.7 billion US brand to major retailers, including Tesco and WHSmith, with zero-sugar formulations targeting health-conscious consumers.

- November 2024: Monster Energy unveiled its biggest product launch in 20 years with a zero-sugar variant of Monster Original, reflecting industry-wide recognition of health-conscious consumer trends and regulatory pressures toward sugar reduction.

- October 2024: Keurig Dr Pepper announced the acquisition of Ghost Lifestyle and Ghost Beverages for approximately USD 990 million, initially purchasing a 60% stake with plans to acquire the remaining 40% in 2028, strengthening its energy drink portfolio in the rapidly growing lifestyle segment.

United Kingdom Energy Drinks Market Report Scope

An energy drink is a mixture of stimulating compounds, usually caffeine, marketed as providing mental and physical stimulation. The United Kingdom's energy drink market is segmented by packaging type, product type, and distribution channels. Based on packaging type, the market is segmented into cans and pet bottles. Based on product type, the market is segmented into drinks, shots, and mixers. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. The report offers market size and forecast value (USD million) for all the above segments.

By Product Type

| Energy Shots |

| Natural/Organic Energy Drinks |

| Sugar-free or Low-calories Energy Drinks |

| Traditional Energy Drinks |

| Other Energy Drinks |

By Packaging Type

| Cans |

| PET Bottles |

| Glass Bottles |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience / Grocery Stores | |

| Online Retail | |

| Other Distribution Channel |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Type | Energy Shots | |

| Natural/Organic Energy Drinks | ||

| Sugar-free or Low-calories Energy Drinks | ||

| Traditional Energy Drinks | ||

| Other Energy Drinks | ||

| By Packaging Type | Cans | |

| PET Bottles | ||

| Glass Bottles | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience / Grocery Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| By Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the United Kingdom energy drinks market?

The market is worth USD 2.32 billion in 2026 and is projected to grow steadily through 2031.

How fast is the category expected to grow?

A 5.60% CAGR is forecast between 2026 and 2031, driven by healthier formulations and expanding distribution.

Which segment is expanding the quickest?

Natural and organic energy drinks are advancing at a 7.61% CAGR, reflecting rising wellness priorities.

Why are manufacturers reformulating recipes?

A lower sugar-tax threshold and a planned sales ban to minors require reduced sugar and clearer caffeine labeling.

What regions hold the most upside?

Northern Ireland shows the highest growth outlook at 5.96% CAGR, while England remains the largest market by value.

Page last updated on: