Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

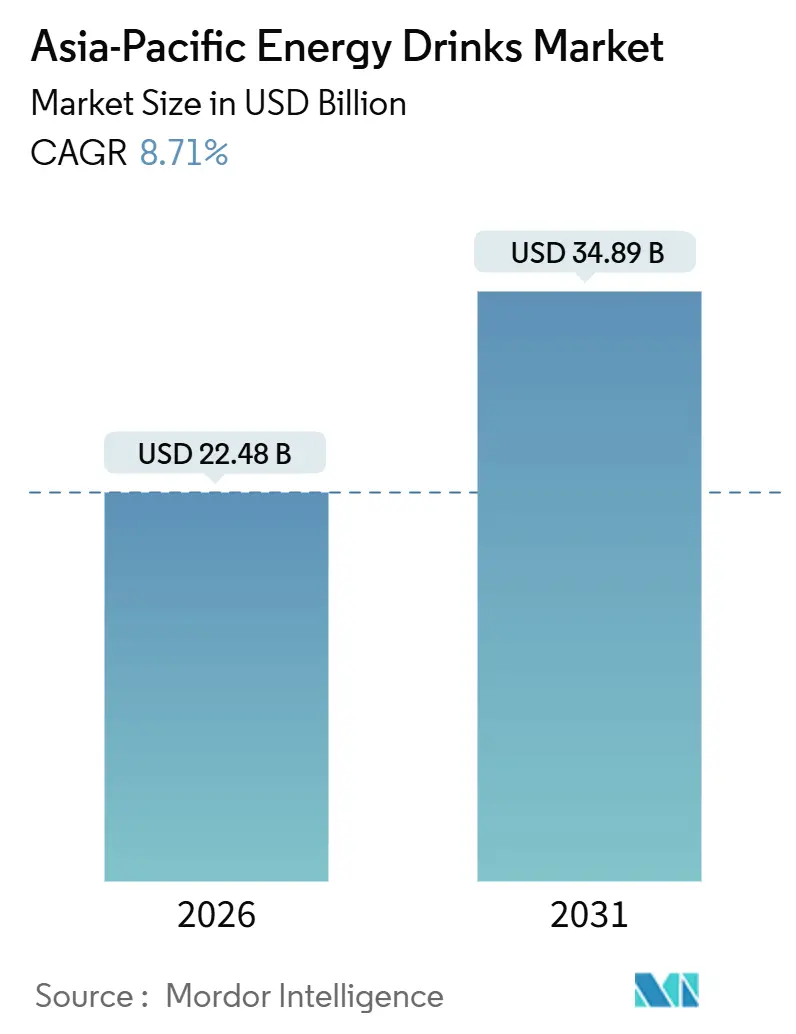

| Market Size (2026) | USD 22.48 Billion |

| Market Size (2031) | USD 34.89 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

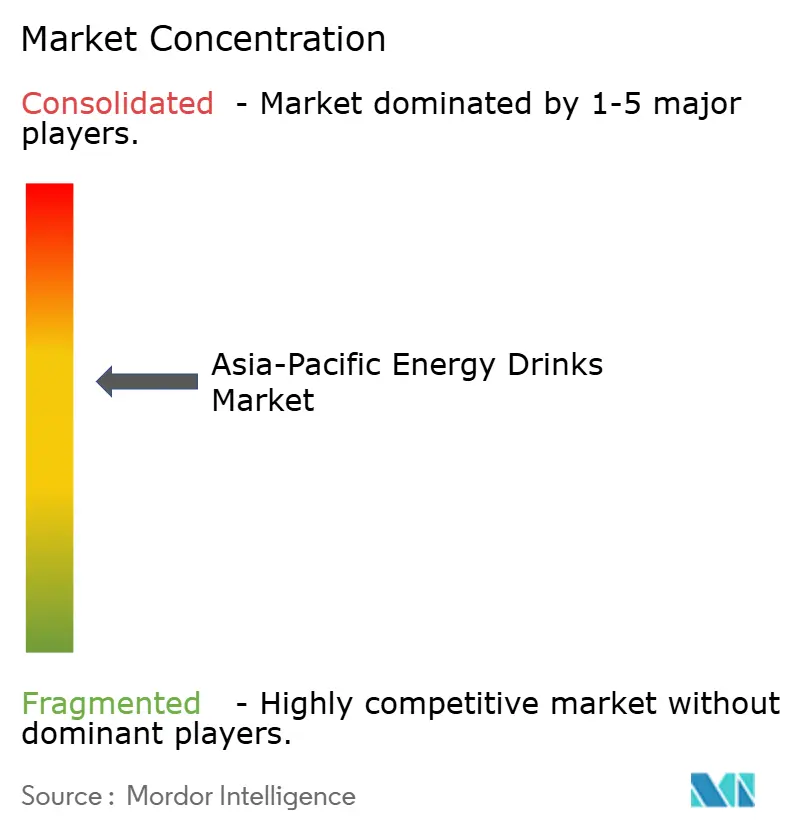

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Energy Drinks Market Analysis by Mordor Intelligence

The Asia-Pacific energy drinks market was valued at USD 22.48 billion in 2026 and is projected to reach USD 34.89 billion by 2031, growing at an 8.71% CAGR. The current market size and forecasted growth confirm that demand for convenient stimulation products is rising, even as per-capita intake remains well below North American levels. Rapid urbanization, a growing under-35 demographic, and the expansion of gym and esports cultures are compressing mealtimes and lengthening active hours, tilting beverage choices toward single-serve cans that offer instant alertness without preparation. Regulatory ceilings on caffeine are steering formulations toward botanical or synthetic sources, while sustainability mandates are pushing packaging toward high-recycled-content aluminum. Competitive intensity is moderate because multinational scale meets entrenched local champions that offer comparable functionality at lower prices, creating a balanced field where innovation rather than price alone determines share gains. Input cost inflation, particularly for taurine and robusta coffee, is accelerating reformulation cycles but also rewarding vertically integrated firms that control both R&D and raw material procurement.

Key Report Takeaways

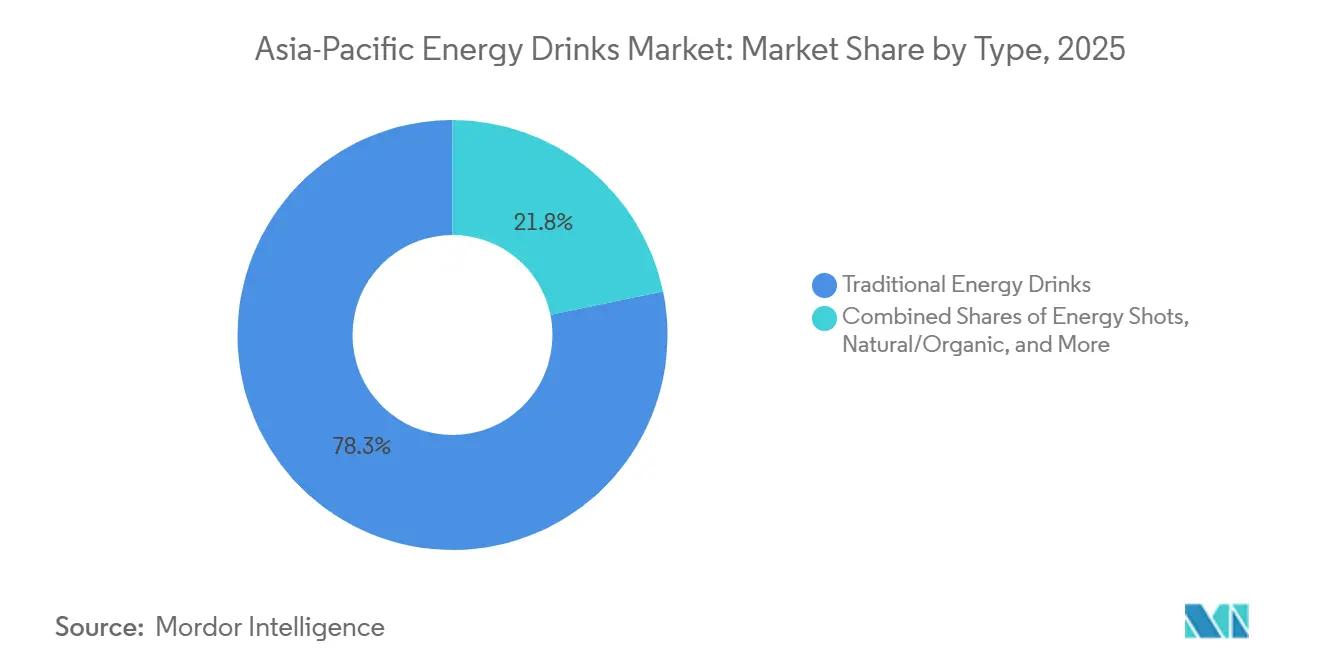

- By product type, traditional energy drinks led with 78.25% Asia-Pacific energy drinks market share in 2025, while natural and organic variants are expanding at a 9.57% CAGR to 2031.

- By packaging, PET bottles accounted for 41.24% of the Asia-Pacific energy drinks market size in 2025 and metal cans are advancing at a 10.02% CAGR through 2031.

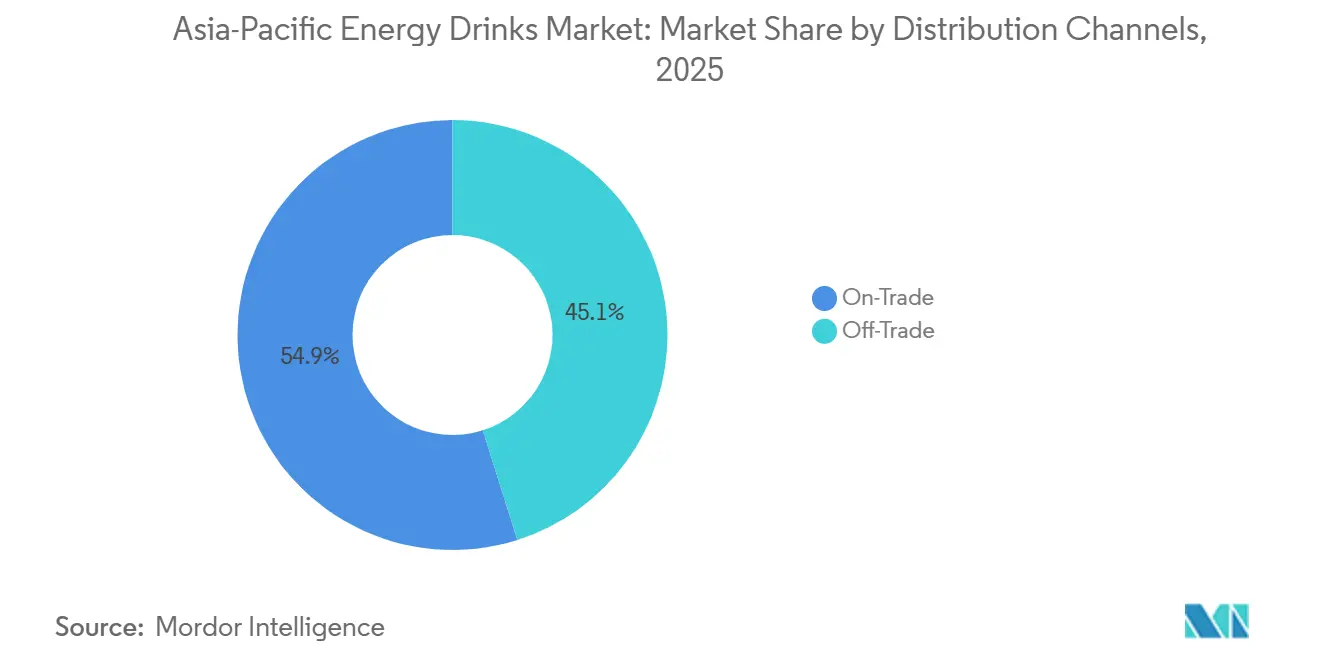

- By distribution channel, off-trade held 45.12% of the Asia-Pacific energy drinks market share in 2025, while on-trade is expected to post a 9.82% CAGR to 2031.

- By geography, China contributed 41.18% of revenue in 2025 and India is set to post the fastest 10.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization and Busy Lifestyles | +1.8% | China, India, Indonesia, Vietnam; metro corridors in ASEAN | Medium term (2–4 years) |

| Large Young Population with High Fitness and Gaming Activities | +1.5% | India, Philippines, Indonesia; South Korea gaming hubs | Short term (≤2 years) |

| Shift to Healthier Variants like Low-Sugar, Natural, and Organic Options | +1.2% | Australia, Japan, urban China; spillover to Singapore, Hong Kong | Long term (≥4 years) |

| E-Commerce and Modern Retail Expansion | +1.0% | India, China, Southeast Asia; quick-commerce in tier-2 cities | Short term (≤2 years) |

| Product Innovation in Flavors, Functional Benefits, and Packaging | +0.9% | Global; early adoption in Japan, Australia, South Korea | Medium term (2–4 years) |

| Rising Disposable Incomes Enable Premium and Functional Drink Purchases | +0.8% | China, India, ASEAN middle class; urban centers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Busy Lifestyles

Urbanization in the Asia-Pacific region is reshaping daily routines, driving a preference for grab-and-go energy formats. By 2024, over 65% of China's population lived in urban areas, while India's metropolitan regions saw an annual increase of 10 million residents, according to the United Nations-Habitat[1]Source: United Nations-Habitat, “Asia-Pacific Urbanization Trends 2024,” un.org. These trends have extended average commutes and reduced time for sit-down meals. Consequently, demand for single-serve cans and bottles offering quick caffeine boosts has surged, providing a significant advantage over traditional brewed coffee or tea. Eastroc's distribution strategy highlights this shift: the company placed 250ml cans in 3.6 million convenience stores and kiosks, capturing impulse purchases from factory workers, delivery riders, and office commuters who often lack access to espresso machines. This trend also benefits on-premise channels. Gaming cafés in South Korea and 24-hour gyms in Singapore now stock energy drinks as standard hydration options, integrating them into extended activity sessions. However, urbanization has also led to income volatility. Gig workers and shift laborers, affected by these fluctuations, are opting for affordable energy products over premium coffee. This has sustained demand for sub-USD 1 price points, a segment where many multinational brands face profitability challenges.

Large Young Population with High Fitness and Gaming Activities

In the Asia-Pacific region, a youthful demographic, particularly those under 35, is increasingly embracing fitness culture and esports, driving a surge in energy drink consumption. In India, the trend is equally pronounced: post-2020, gym memberships saw a twofold increase, and fitness influencers on Instagram have made pre-workout energy drinks a staple, especially among the aspirational middle class. PepsiCo's Sting brand smartly tapped into this youthful enthusiasm, pricing its 250ml cans at a wallet-friendly INR 20 (USD 0.24). By strategically placing these cans in college canteens and sports retailers, Sting achieved a remarkable 110 million cases sold in 2023. Meanwhile, in China, the connection between gaming and energy drinks is undeniable. Eastroc, a prominent player, not only sponsors esports tournaments but also strategically places branded coolers in internet cafés, turning casual viewers into loyal customers. Yet, this booming market faces increasing regulatory scrutiny. South Korea took a stand in 2013, banning energy drink ads during prime children's TV hours (5–7 pm). Now, India is contemplating similar restrictions, casting a shadow over marketing strategies aimed at the youth.

Shift to Healthier Variants Like Low-Sugar, Natural, and Organic Options

Australia's Shine+ brand, introduced in 2024, highlights this trend. Its 500ml Charged variant features 160mg of natural caffeine derived from green coffee beans and green tea. It also includes nootropics such as L-theanine, ginkgo biloba, and turmeric, while being entirely sugar-free. This product caters to consumers who perceive traditional energy drinks as "chemical cocktails." In early 2025, Red Bull launched its Zero variant globally, followed by Monster's Lando Norris Zero Sugar in the summer of 2025. These developments reflect the industry's recognition that sugar-free options are now essential in health-conscious markets like Japan and Australia. The focus on functional ingredients is also growing: Kirin's LC-Plasma beverages, containing the Lactococcus lactis strain Plasma, promote immune support through plasmacytoid dendritic cell activation. With sales reaching JPY 20 billion (USD 133 million) in 2023, these beverages are now expanding into Vietnam. However, the authenticity of such claims faces increasing scrutiny. Brands must balance "natural" claims with shelf stability and cost considerations. Additionally, regulatory bodies like Thailand's FDA are imposing stricter requirements. Under Notification No. 477, effective July 2024, they now demand evidence to support functional health claims[2]Source: Thai Food and Drug Administration. "Thai FDA Issues Notification to Support Health Claims for Functional Foods." en.fda.moph.go.

E-commerce and Modern Retail Expansion

Quick-commerce platforms and modern retail chains are reducing distribution barriers, enabling challenger brands in India to bypass traditional wholesaler networks. Since 2020, energy drink e-commerce in India has grown rapidly, with platforms such as Blinkit and Zepto delivering chilled cans within 10 minutes, transforming spontaneous cravings into instant sales. PepsiCo's Sting brand took advantage of this trend, expanding into tier-2 and tier-3 cities with limited physical retail presence, which significantly contributed to its 175% volume growth in late 2024. In China, modern retail channels—such as hypermarkets, convenience chains, and vending machines—now dominate, accounting for over 60% of energy drink sales. Eastroc's partnership with Alibaba's Hema supermarkets enabled real-time inventory management and targeted promotions. This shift also benefits premium SKUs, as online consumers are more willing to pay for functional or organic variants. For example, Shine+'s 12-pack priced at AUD 59 (USD 39) is well-received online, a scenario less likely in traditional convenience stores. However, last-mile logistics costs remain a challenge in archipelagic nations like Indonesia and the Philippines, where rural areas trail urban centers by 3–5 years in market penetration.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Over High Sugar, Caffeine, and Artificial Additives | -1.2% | Australia, Japan, urban China; spillover to India | Short term (≤2 years) |

| Stringent Government Rules on Sugar Content, Labeling, and Youth Marketing | -0.9% | Australia (FSANZ), India (FSSAI), South Korea (MFDS), Thailand | Medium term (2–4 years) |

| Supply Chain Issues for Ingredients and Rising Raw Material Costs | -0.7% | Global; acute in China (taurine), Vietnam (coffee) | Short term (≤2 years) |

| Consumer Shift to Natural Beverages | -0.5% | Japan, Australia, Singapore; emerging in China tier-1 cities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over High Sugar, Caffeine, and Artificial Additives

Public health advocacy and media scrutiny are diminishing consumer trust in traditional high-sugar, high-caffeine formulations, particularly among parents and health-conscious millennials. Australia's Nutri-Grade labeling system, which assigns letter grades to beverages based on sugar and saturated fat content, has relegated energy drinks to lower tiers, discouraging purchases by calorie-conscious shoppers. Japan's aging population—over 29% aged 65 and older—is shifting toward functional isotonic drinks like Otsuka's Pocari Sweat instead of energy drinks, perceiving the latter as youth-focused and potentially harmful. Legal liability concerns are also increasing; lawsuits in the United States over caffeine-related adverse events (including fatalities associated with Panera's Charged Lemonade) have prompted companies to exercise caution and reformulate products to reduce caffeine levels. This has led to brand fragmentation: as established players reformulate to minimize risks, they lose shelf space to niche "clean label" competitors that market themselves as safer alternatives, reducing market share and complicating portfolio management.

Stringent Government Rules on Sugar Content, Labeling, and Youth Marketing

Regulatory tightening is increasing compliance costs and restricting marketing reach, particularly for youth-focused campaigns. In Australia, Food Standards Australia New Zealand (FSANZ) enforces a caffeine limit of 320mg per liter, requiring reformulation of imported SKUs that exceed this cap[3]Source: Food Standards Australia New Zealand, “Caffeine Limits and Labelling,” fsanz.gov.au. India's Food Safety and Standards Authority (FSSAI) implemented a 300mg/L limit in December 2016 and mandates clear labeling with warnings about caffeine content and consumption limits, reducing impulse purchases among less informed consumers. In 2025, South Korea's Ministry of Food and Drug Safety (MFDS) required larger font sizes for caffeine warnings on labels and prohibited advertising during children's programming, hindering brand engagement with adolescents. Thailand's FDA Notification No. 477, effective July 2024, requires evidence to support functional health claims, raising the standards for assertions related to immunity, cognition, and energy boosts. These regulations disproportionately impact smaller brands without in-house regulatory teams, consolidating market share among multinationals with established compliance infrastructures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Variants Gain Despite Traditional Dominance

Traditional drinks generated 78.25% of value in 2025, reflecting longstanding price leadership and widespread vending presence. Natural and organic lines, though smaller, are on a 9.57% CAGR trajectory, well above the 8.71% overall Asia-Pacific energy drinks market pace. Red Bull Zero and Monster’s zero-sugar launches confirm that even incumbents see clean labels as baseline expectations. Energy shots remain niche but appeal to Japanese commuters who favor compact 60 ml bottles that fit vending machines. The Asia-Pacific energy drinks market size for natural and organic variants is projected to expand fast enough to reach mid-teens share by 2031 if current growth persists.

Premium hybrids such as Kirin’s immune-support LC-Plasma and Asahi’s SOLO Energy illustrate how functional benefits can support price points 30% higher than mainstream cans. However, Thailand’s stricter health-claim rules raise R&D and substantiation costs, slowing copycat entries. Balance is crucial: traditional formulations will still dominate unit volumes, but margin growth clearly pivots to cleaner, functional niches within the Asia-Pacific energy drinks industry.

By Packaging Type: Metal Cans Surge On Sustainability And Premiumization

PET bottles held 41.24% of 2025 revenues, valued by price-sensitive consumers for resealability. Metal cans, however, are rising at a 10.02% CAGR, supported by retailer demand for recyclable formats and by consumers associating aluminum with premium quality. Visy’s 83% recycled-content can cut embodied carbon by 59%, giving chain retailers a tangible ESG talking point. The Asia-Pacific energy drinks market size generated by metal cans is forecast to exceed PET by 2030 if trends continue.

Glass remains under 5% due to logistics costs, while label-less PET and pouch experiments target online shoppers who judge sustainability through packaging cues. UACJ’s pursuit of 75% recycled aluminum content raises the bar for can suppliers and may accelerate the format shift. The Asia-Pacific energy drinks market share held by cans could climb another 5–7 percentage points once Indian can-making capacity, led by Ball and domestic operators, scales through 2028.

By Distribution Channel: On-Trade Rebounds As Off-Trade Dominates

In 2025, off-trade sales accounted for 45.12% of the market, driven by the widespread presence of supermarkets, hypermarkets, and the rapidly growing convenience chains in Japan and South Korea. In India, quick-commerce apps are now delivering chilled energy drinks in mere minutes, catering to impulse buyers and seamlessly integrating smaller brands into consumer baskets—bypassing the need for costly national distributors. Despite a recovery in other sales channels, off-trade sales in the Asia-Pacific energy drinks market are projected to remain above the 40% mark.

Meanwhile, the on-trade sector, which includes bars, gyms, and gaming cafés, is witnessing a robust rebound, growing at a CAGR of 9.82%. Venues like PC-bangs in Seoul, 24-hour gyms in Singapore, and esports arenas throughout ASEAN are capitalizing on their extended dwell times, selling energy drinks at a premium of 20–30%. While multinationals are forging partnerships with venue owners for branded refrigerators, local players are tapping into their neighborhood connections to secure placements in street-level eateries. This division in sales channels suggests that while off-trade will dominate in volume, on-trade will play a crucial role in introducing and establishing premium product extensions in the Asia-Pacific energy drinks landscape.

Geography Analysis

In 2025, China accounted for 41.18% of the regional turnover, driven by Eastroc's commanding 43.02% share and its expansive network of 3.6 million outlets, spanning from tier-1 metros to rural kiosks. Eastroc's confidence in sustained demand, even amidst rising taurine costs, is evident with its Zhongshan site targeting a CNY 2.16 billion output. Meanwhile, TCP Group is establishing new plants in Sichuan and Guangxi to localize Red Bull's production, aiming for tariff relief and quicker replenishment cycles. Despite facing ingredient inflation challenges, the company finds solace in economies of scale, bolstering its margin protection.

India, projected to grow at a robust 10.11% CAGR through 2031, is heavily influenced by PepsiCo's Sting. With capacity expansions in four states and the rise of quick-commerce, energy drinks are making their way into tier-3 towns. While FSSAI's caffeine cap lends legitimacy to the category, the mandated front-panel warnings might deter casual trials. In Japan, an aging population drives a preference for functional beverages. Kirin's LC-Plasma line, raking in JPY 20 billion in 2023, capitalizes on a vast 180,000-unit vending network. Though consumption growth is tepid, premium functional lines fetch higher unit prices, ensuring healthy margins.

Australia, despite its modest volume, serves as a crucible for innovation. FSANZ's caffeine cap of 320 mg/L and Nutri-Grade scores nudge brands towards low-sugar formulations. Local productions, like Asahi's SOLO Energy and Visy's recycled cans, resonate with the nation's stringent health and environmental standards. Given the high logistics costs, domestic filling takes precedence over imports, centralizing value within Australia's supply chain. South Korea boasts one of the highest per-capita energy drink consumptions globally, largely fueled by its vibrant esports culture. New regulations mandate larger caffeine warnings on labels, and advertisements during children's programming are prohibited. Yet, brands continue to bolster their visibility through sponsorships of esports championships. Trends birthed in Seoul frequently ripple across ASEAN, positioning South Korea as a pivotal trendsetter in youth marketing within the expansive Asia-Pacific energy drinks arena.

Competitive Landscape

The Asia-Pacific energy drinks market demonstrates a balanced structure where global giants benefit from scale advantages but coexist with agile local players. In 2024, Red Bull sold 12.67 billion cans globally, while Monster reported USD 211.4 million in Asia-Pacific revenue for Q3. However, local brands like Eastroc and Osotspa hold over 40% market share in their respective home markets by leveraging strategies such as vernacular branding, factory-gate pricing, and strong distributor relationships—approaches that multinationals find difficult to replicate. PepsiCo, on the other hand, drives significant growth in India through its hybrid model, which combines global bottling efficiencies with a sub-USD 0.25 price point for its Sting brand.

Opportunities remain in functional and female-focused niches. For example, Kirin's LC-Plasma, positioned for immune support, has achieved sales three times higher than its predecessor. Similarly, Monster's Flrt, set to launch in 2026, features softer aesthetics and collagen, targeting women aged 25–40 who are moving away from high-sugar "extreme" beverages. Technology also provides a competitive advantage: Kirin's AI-powered vending network reduces stockouts and optimizes planograms, directly increasing sales per machine.

Regulatory expertise is emerging as a critical differentiator. Thailand's new regulation requiring clinically proven claims will challenge underfunded entrants, creating opportunities for established players capable of financing studies and managing compliance across multiple markets. Overall, the competitive dynamics balance buyer power with supplier innovation, resulting in a moderate concentration score.

Asia-Pacific Energy Drinks Industry Leaders

-

Eastroc Beverage(Group) Co., Ltd.

-

Fujian Dali Food Group Co., Ltd.

-

Monster Beverage Corporation

-

Red Bull GmbH

-

T.C. Pharmaceutical Industries Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: 28 BLACK, a premium energy drink brand, launched its energy drinks in India. Initial flavors for India include best-seller Açai (fruity berry taste) and Gummibär, tailored to local preferences.

- September 2025: Hell Energy Drink, a rapidly expanding global brand from Hungary, has introduced its premium Black Cherry flavor in India, featuring an intense black cherry taste with the original energy formula enriched by multiple B-vitamins and no added preservatives.

- April 2024: PepsiCo India has introduced Sting Blue Current, a limited-edition flavor addition to its Sting Energy lineup, designed to deliver an electrifying energy boost with a refreshing new taste.

Asia-Pacific Energy Drinks Market Report Scope

Energy Shots, Natural/Organic Energy Drinks, Sugar-free or Low-calories Energy Drinks, Traditional Energy Drinks are covered as segments by Soft Drink Type. Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam are covered as segments by Country.

By Product Type

| Energy Shots |

| Natural / Organic Energy Drinks |

| Sugar-Free / Low-Calorie Energy Drinks |

| Traditional Energy Drinks |

| Other Energy Drinks |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

By Grography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Energy Shots | |

| Natural / Organic Energy Drinks | ||

| Sugar-Free / Low-Calorie Energy Drinks | ||

| Traditional Energy Drinks | ||

| Other Energy Drinks | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Grography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms