Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

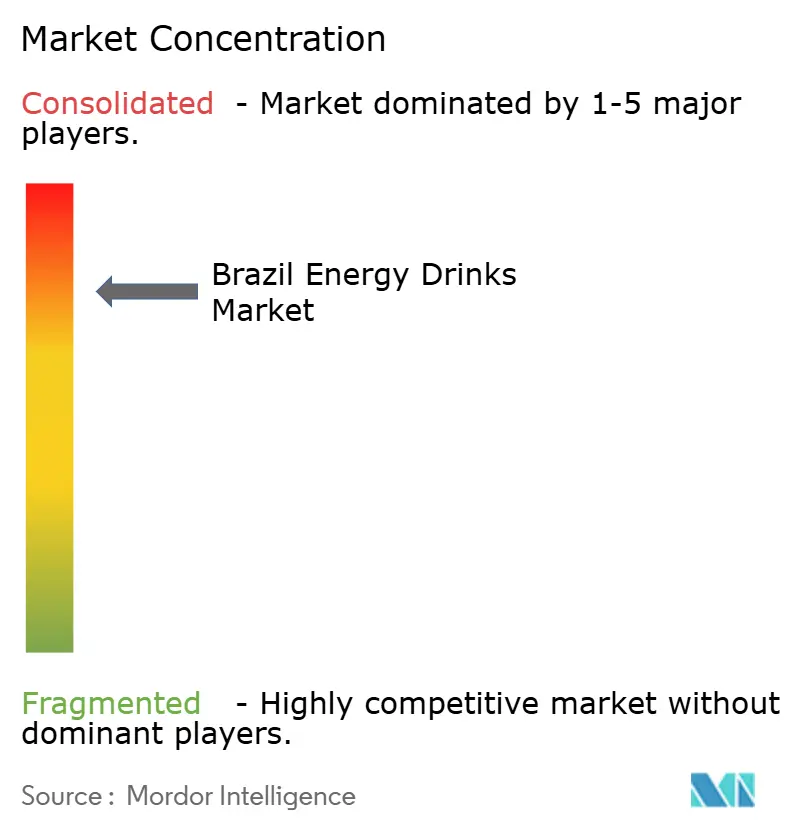

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Energy Drinks Market Analysis by Mordor Intelligence

The Brazil energy drinks market size was valued at USD 1.95 billion in 2025 and estimated to grow from USD 2.15 billion in 2026 to reach USD 3.21 billion by 2031 at a compound annual growth rate (CAGR) of 8.40 percent. The energy drinks market in Brazil is experiencing growth, driven by lifestyle changes, demographic shifts, and evolving retail trends. A large, young urban population with demanding schedules increasingly opts for convenient beverages that enhance alertness and stamina for activities such as work, studying, nightlife, and sports. The rising participation in gyms and the growing amateur fitness culture are fueling the use of energy drinks as pre-workout performance enhancers. According to the 2024 Latin America Fitness Consumer Survey by the Health & Fitness Association, 78.4% of physically active urban Brazilians are members of health and fitness organizations[1]Source: Health & Fitness Association, "2024 Latin America Fitness Consumer Survey," healthandfitness.org. Additionally, the increasing popularity of e-sports and gaming is driving demand for functional stimulation. Manufacturers are focusing on strong brand marketing tied to music festivals and extreme sports, while also introducing sugar-free and natural-ingredient options to appeal to health-conscious consumers. Moreover, expanded availability through supermarkets, convenience stores, and delivery apps has improved accessibility, encouraging impulse purchases and supporting steady market growth.

Key Report Takeaways

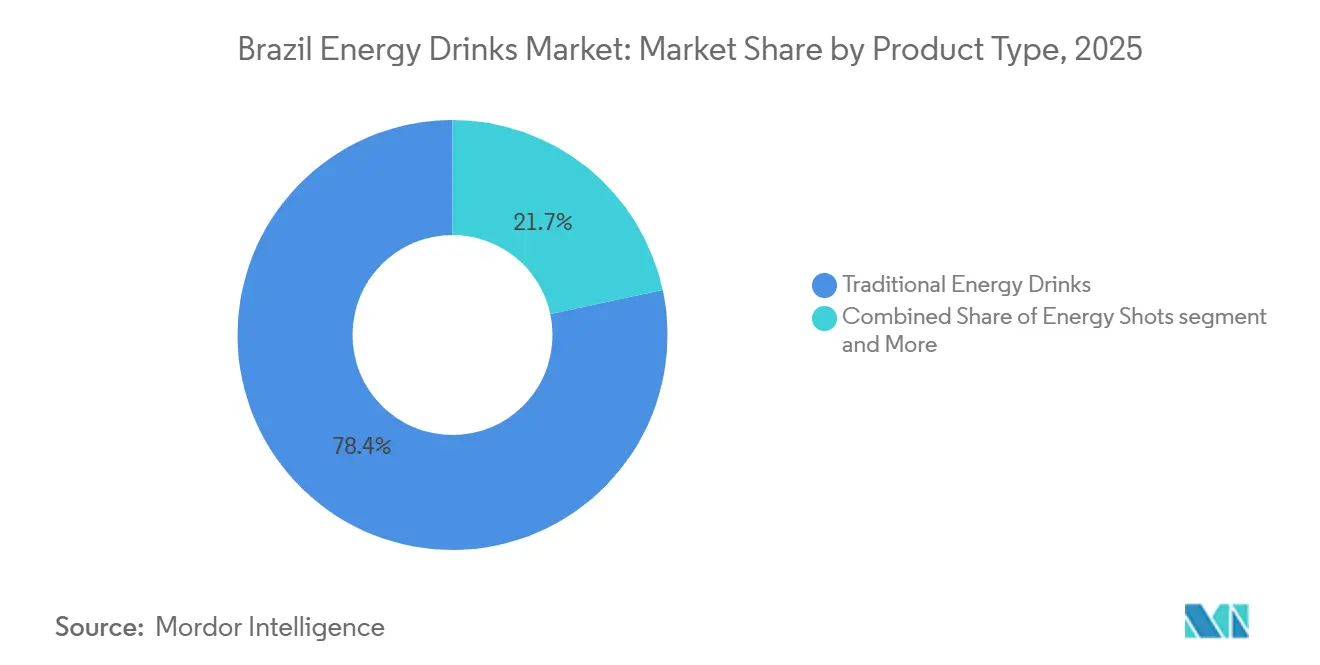

- By product type, traditional energy drinks led with 78.35% of Brazil's energy drinks market share in 2025, whereas energy shots are projected to expand at a 10.64% CAGR through 2031.

- By packaging, metal cans captured 71.32% of the Brazil energy drinks market size in 2025; Tetra Pak and pouches record the fastest 10.80% CAGR over 2026-2031.

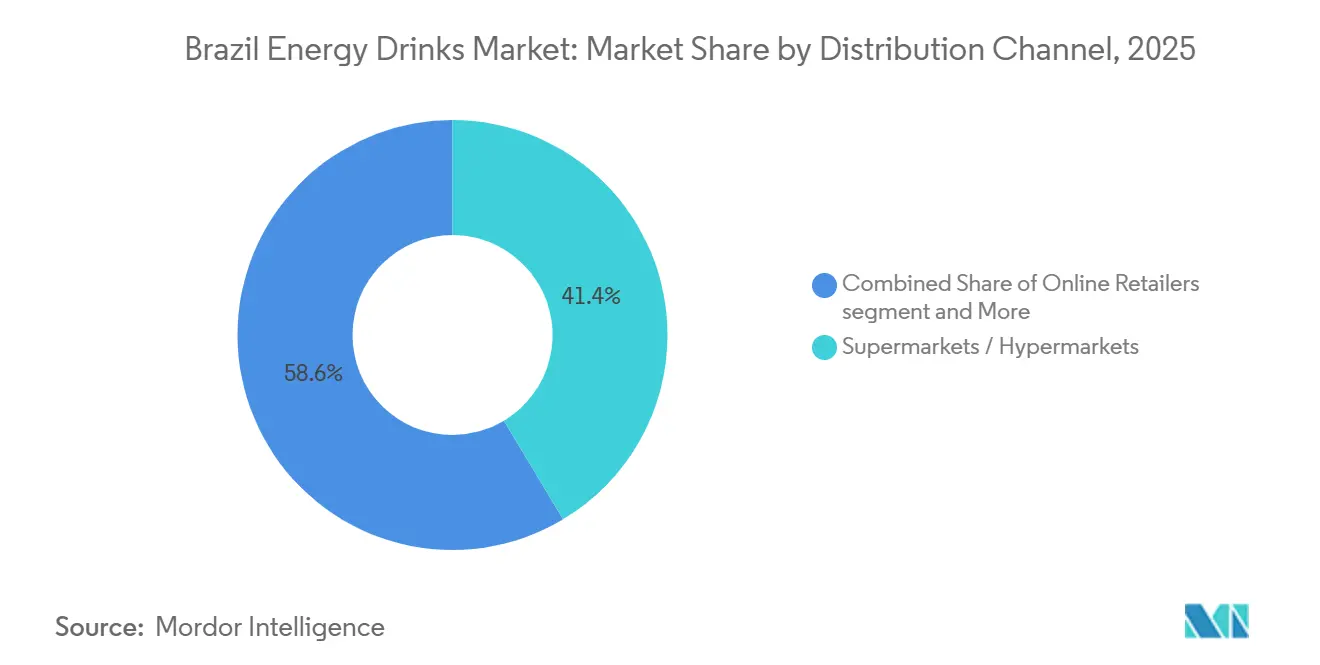

- By distribution channel, supermarkets and hypermarkets held a 41.40% of Brazil's energy drinks market share in 2025, while online retailers are advancing at an 11.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for reduced-sugar formulations | +1.2% | National, strongest in São Paulo, Rio de Janeiro, and Southern states | Medium term (2-4 years) |

| Expanding adoption of gym and fitness lifestyles | +1.0% | Urban centers (São Paulo, Rio de Janeiro, Brasília), spreading to secondary cities | Long term (≥ 4 years) |

| Rapid growth of direct-to-consumer online sales channels | +1.5% | National, with highest penetration in Southeast (62% of retail revenues) | Short term (≤ 2 years) |

| Brand visibility through gaming and e-sports sponsorships | +0.8% | National, concentrated in youth demographics (16-34 years, 62% of esports audience) | Medium term (2-4 years) |

| Product innovation centered on guarana-based functionality | +1.3% | National, leveraging Bahia production hub and Amazon heritage | Long term (≥ 4 years) |

| Rising demand for functional beverages and clean-label products | +1.0% | National, premium segments in Southeast and South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing preference for reduced-sugar formulations

Concerns over sugar consumption and lifestyle-related health issues, such as obesity and diabetes, are prompting Brazilian consumers to choose energy drinks with reduced or zero sugar content. Data from Agência Brasil indicates that 62.6% of Brazil's population was overweight in 2024, compared to 42.6% in 2006[2]Source: Agência Brasil, "Over 60% of Brazilians are overweight," agenciabrasil.ebc.com.br. Consumers are increasingly scrutinizing nutrition labels and preferring beverages that offer caffeine and functional benefits without high-calorie content. This trend is particularly prominent among gym-goers, young professionals, and regular energy drink consumers. In response, brands are reformulating their products by using low-calorie sweeteners, plant-based extracts, and simplified ingredient lists while preserving taste and performance. This strategy allows consumers to incorporate energy drinks into their daily routines without compromising health goals, broadening usage occasions from nightlife to daytime activities like productivity and fitness. As a result, reduced-sugar variants are gaining traction among health-conscious consumers, driving repeat purchases and emerging as a key growth factor in the Brazilian energy drinks market.

Expanding adoption of gym and fitness lifestyles

The increasing adoption of gym memberships, recreational sports, and fitness-oriented lifestyles in Brazil is driving a notable rise in demand for energy drinks as functional performance beverages. Consumers are increasingly using these drinks as pre-workout supplements or endurance enhancers to improve focus, stamina, and training intensity during activities such as weightlifting, running, cycling, and group fitness classes. Fitness influencers and trainers often promote caffeinated and performance-enhancing beverages as part of workout routines, strengthening their association with active lifestyles rather than solely nightlife consumption. In response, brands are positioning their products to emphasize benefits such as hydration, mental alertness, and physical performance, highlighting ingredients like caffeine, taurine, B-vitamins, and electrolytes. As regular exercise becomes a more integral part of daily routines for many Brazilians, energy drinks are increasingly incorporated into fitness preparation and recovery practices, contributing to higher purchase frequency and sustained market growth.

Rapid growth of direct-to-consumer online sales channels

The growth of direct-to-consumer (D2C) online channels is driving energy drink sales in Brazil by simplifying product discovery and repurchasing processes, reducing reliance on physical retail. E-commerce platforms, brand websites, and quick-commerce delivery apps enable consumers to purchase multipacks, subscription bundles, and limited editions with ease, promoting higher consumption frequency and fostering brand loyalty. These online channels also allow companies to target specific consumer groups, such as gamers, fitness enthusiasts, and students, through personalized promotions, influencer partnerships, and social media campaigns. Furthermore, digital storefronts offer detailed information on ingredients, sugar content, and functional benefits, aiding newer or premium brands in building consumer trust. With the continued expansion of smartphone usage and instant delivery services in urban areas, online D2C distribution is emerging as a significant growth driver by enhancing accessibility, encouraging repeat purchases, and improving consumer engagement in the Brazilian energy drinks market.

Product innovation centered on guarana-based functionality

Guarana-based functionality is a key growth driver in Brazil's energy drinks market due to the ingredient's strong cultural relevance and its association with natural energy among local consumers. Native to the Amazon region, guarana is widely recognized as a traditional stimulant, making products that feature it appear more authentic and less artificial compared to synthetic caffeine formulations. Manufacturers are integrating guarana extracts with vitamins, botanicals, and natural flavors to position these beverages as functional options aligned with natural wellness solutions. This approach appeals to health-conscious consumers seeking sustained energy, improved mental focus, and reduced side effects like jitters, while also preserving regional identity. By combining modern beverage formats with a locally trusted ingredient, companies enhance consumer trust, encourage product trials, and foster a premium perception, contributing to the steady growth of Brazil's energy drinks market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potential nationwide caffeine restrictions and mandatory warning labels | -0.8% | National, enforced by ANVISA across all states | Medium term (2-4 years) |

| Fluctuating costs of imported aluminum cans | -0.7% | National, with acute impact on manufacturers in Southeast and South | Short term (≤ 2 years) |

| Presence of counterfeit products | -0.6% | National, concentrated in online and informal retail channels | Short term (≤ 2 years) |

| Excise taxes on sugary drinks | -0.9% | National, phased implementation 2029-2033 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Potential nationwide caffeine restrictions and mandatory warning labels

Potential nationwide caffeine limits and stricter warning-label requirements are restraining Brazil's energy drinks market by increasing regulatory pressure on high-stimulant formulations and marketing practices. Authorities are expressing growing concern over excessive caffeine consumption, particularly among adolescents and frequent consumers. This concern could result in caps on allowable caffeine content, sales restrictions in specific environments, or stricter advertising regulations. Additionally, Brazil's nutrition labeling regulation, RDC 429/2020, mandates front-of-pack warning symbols when added sugar exceeds 7.5 grams per 100 milliliters[3]Source: United States Department of Agriculture, "RDC 429/2020," fas.usda.gov. This requirement is prompting brands to reformulate their products to avoid negative consumer perceptions at the point of purchase. These policies may reduce impulse purchases, limit product differentiation based on strong stimulation claims, and increase compliance and reformulation costs for manufacturers. Collectively, these regulatory challenges could slow new product launches, compress profit margins, and moderate overall market growth.

Fluctuating costs of imported aluminum cans

Fluctuating prices of imported aluminum cans constrain Brazil's energy drinks market, as packaging constitutes a significant portion of production costs. The market heavily depends on sleek, single-serve cans, leaving manufacturers vulnerable to currency fluctuations, global aluminum price variations, and logistics costs associated with imported materials. Rising input costs force brands to either raise retail prices or absorb reduced margins, both of which can diminish competitiveness against other ready-to-drink beverages. Smaller and emerging companies face greater challenges due to limited negotiating power with suppliers and distributors. Frequent price changes also disrupt promotional strategies and deter bulk purchasing, ultimately reducing profitability and hindering market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shots and Sugar-Free Variants Reshape Portfolio Mix

Traditional energy drinks accounted for 78.35% of the market share in 2025, driven by their integration into everyday consumption scenarios such as long work hours, commuting fatigue, studying, and nightlife activities. Their affordability, availability in larger pack sizes, and widespread distribution through supermarkets, convenience stores, and bars make them a popular choice among a broad consumer base. Brand promotions linked to football, music events, and youth culture further strengthen brand recognition and loyalty. Additionally, the availability of various flavors appeals to regular consumers. The combination of accessibility, familiar taste profiles, and social consumption habits supports the continued dominance of traditional energy drinks across diverse demographic groups.

Energy shots are projected to grow at a rate of 10.64% through 2031, driven by the demand for quick and portable energy solutions among urban consumers seeking immediate alertness without consuming a full-sized beverage. This compact format is favored by students, drivers, gamers, and professionals due to its convenience, ease of transport, and perceived functionality. Additionally, the low volume appeals to calorie-conscious consumers who prefer caffeine intake without excessive liquid or sugar. Pharmacies, gyms, and checkout counters further promote impulse purchases. As productivity-focused lifestyles become more prevalent, the convenience and concentrated energy benefits of energy shots continue to drive their adoption in niche but rapidly expanding usage scenarios.

By Packaging Type: Sustainability and Logistics Favor Flexible Formats

Metal cans dominated with a 71.32% market share in 2025. Energy drinks packaged in metal cans lead sales in Brazil due to their strong association with premium branding, carbonation retention, and rapid cooling convenience. Consumers view cans as providing a fresher, colder, and more intense drinking experience, particularly in hot climates and social settings such as parties, bars, and sporting events. Their durability facilitates transport and outdoor consumption, while slim designs improve shelf visibility and encourage impulse purchases in convenience stores. Additionally, cans align with the category's youthful image and are highly compatible with vending machines and quick-commerce delivery, supporting frequent purchases.

Tetra Pak and pouches are projected to grow at a rate of 10.80% through 2031. Energy drinks packaged in Tetra Pak cartons and pouches are gaining popularity due to their affordability and practicality for everyday use. These packaging formats are lightweight and often less expensive to produce, enabling brands to cater to price-sensitive consumers and smaller retail outlets, such as those in residential areas and schools. They can be stored without refrigeration before opening and are safer for on-the-go consumption, particularly for younger consumers and daytime use. Additionally, their resealable and spill-resistant design makes them convenient for travel or work, allowing brands to extend the category beyond nightlife into routine hydration and casual refreshment occasions.

By Distribution Channel: Digital Platforms Accelerate Share Gains

Supermarkets/hypermarkets accounted for 41.40% of the distribution share in 2025, supported by high product visibility, diverse flavor options, and price promotions that encourage bulk purchases. Consumers frequently include multipacks in their regular grocery shopping, making this channel significant for repeat purchases and family-level stocking. Large shelf displays, in-store discounts, and cross-merchandising near snacks or alcoholic beverages drive impulse purchases, while chilled sections enable immediate consumption after checkout. Additionally, the ability to compare brands and pack sizes in a single location fosters trust and promotes widespread adoption across different income groups.

Online retailers are projected to grow at a CAGR of 11.46% through 2031, driven by the convenience of e-commerce and targeted digital engagement. These platforms enable consumers to order energy drinks at any time and receive them quickly through delivery services. Features such as subscription packs, bundle pricing, and exclusive online flavors promote higher purchase frequency and foster brand loyalty, particularly among gamers, students, and fitness enthusiasts. Additionally, digital platforms offer detailed ingredient information and user reviews, enhancing the credibility of premium and functional products. With the expansion of mobile commerce and rapid delivery services in urban areas, online channels are increasingly facilitating habitual replenishment rather than occasional purchases.

Geography Analysis

Brazil's energy drink market is predominantly concentrated in the Southeast, driven by large metropolitan areas with dense populations, higher purchasing power, and strong participation in fitness activities, which collectively support the highest consumption levels. Major beverage companies consider Brazil a key growth market in Latin America, with premium products and continuous innovation performing particularly well in major cities. Simultaneously, manufacturers are increasing investments in production and distribution capacity to strengthen their presence in the North and Northeast. These regions offer significant long-term growth potential due to their large population base. The South also remains strategically important, supported by relatively strong consumer spending and cross-border trade dynamics, with facility upgrades in the region underscoring ongoing operational commitments.

Local sourcing advantages further influence regional market dynamics. Areas known for guarana cultivation provide opportunities for branding tied to natural ingredients and sustainability narratives. However, economic constraints in less affluent regions can limit short-term demand, despite these areas representing the largest untapped consumer base. Additionally, differences in state taxation rules create compliance challenges, which larger national companies are better equipped to manage compared to smaller regional players. The Central-West region is gradually emerging as a secondary growth area, supported by increasing white-collar employment and growing fitness adoption.

Competitive Landscape

Brazil's energy drink market is highly consolidated, dominated by global players such as Monster Beverage, Red Bull, and Coca-Cola, which leverage their extensive scale and distribution networks. Leading companies are expanding production capacity to meet growing demand while introducing localized flavors and formulations inspired by ingredients like guarana. Additionally, clean-label positioning is being adopted to enhance relevance among domestic consumers. Major beverage groups are also investing in digital ordering platforms and retailer connectivity tools to strengthen relationships with small outlets and reduce reliance on traditional intermediaries.

Despite the dominance of multinational brands, smaller companies are finding opportunities in niche formats such as compact energy shots and shelf-stable packaging. These formats require less infrastructure compared to carbonated canned products and enable targeted marketing toward youth communities, including partnerships within the esports sector. Technology adoption is reshaping competition as large players enhance manufacturing efficiency and accelerate the launch of new product variants. Digital distribution platforms are also expanding market access for emerging brands. However, stricter regulatory requirements for product notification and registration create higher entry barriers, favoring companies with established compliance capabilities.

Natural-ingredient brands that emphasize local sourcing and transparent labeling are beginning to gain attention, although their scale remains limited compared to multinational competitors. Additionally, concerns about counterfeit products in online channels are prompting leading firms to invest in traceability systems and direct-to-consumer engagement. These efforts reinforce their advantages in resources, consumer trust, and supply chain control over smaller challengers.

Brazil Energy Drinks Industry Leaders

-

Red Bull GmbH

-

Monster Beverage Corp.

-

Anheuser-Busch InBev

-

Grupo Petrópolis

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ball Corporation, a global provider of sustainable aluminum packaging solutions, partnered with the Brazilian natural energy drink brand Açaí Motion® to launch a beverage can certified by the Aluminium Stewardship Initiative (ASI). This collaboration emphasizes a mutual commitment to product traceability, quality assurance, and circular economy principles, strengthening sustainability-focused innovation in the beverage industry.

- September 2024: Flying Horse, one of Brazil's earliest energy drink brands, introduced a brand refresh to modernize its image and expand its market presence. Supported by a marketing campaign, updated visuals, and the tagline "Free All Your Versions," the Britvic-owned brand aims to attract new consumers while maintaining loyalty among its existing customer base. The repositioning emphasizes individuality and self-expression, featuring vibrant designs, motivational messaging, and revamped packaging intended to appeal to a diverse age demographic.

- February 2024: MMA icons Minotauro and Minotouro have partnered with Minalba Brasil in a licensing agreement for the Minotauro Energy Drink brand. Under this agreement, Minalba Brasil will manage the production and distribution of the product throughout Brazil's Northeast region.

Brazil Energy Drinks Market Report Scope

Energy drink refers to a soft drink with high sugar content, caffeine, or another stimulant generally consumed during or after intense exercise or to overcome fatigue. The Brazil energy drink is segmented by product type into drinks, shots, and mixers; and by distribution channel into supermarkets/ hypermarkets, convenience stores, specialist stores, and others. The report offers market size and forecasts in value terms in USD million for all the above segments.

By Product Type

| Energy Shots |

| Natural/Organic Energy Drinks |

| Sugar-free or Low-calories Energy Drinks |

| Traditional Energy Drinks |

| Other Energy Drinks |

By Packaging Type

| Metal Cans |

| PET Bottles |

| Glass Bottles |

| Tetra Pak / Pouches |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialist Stores |

| Online Retailers |

| Others |

| By Product Type | Energy Shots |

| Natural/Organic Energy Drinks | |

| Sugar-free or Low-calories Energy Drinks | |

| Traditional Energy Drinks | |

| Other Energy Drinks | |

| By Packaging Type | Metal Cans |

| PET Bottles | |

| Glass Bottles | |

| Tetra Pak / Pouches | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialist Stores | |

| Online Retailers | |

| Others |

Key Questions Answered in the Report

How fast is the Brazil energy drinks market expected to grow to 2031?

The category is forecast to rise at an 8.4% CAGR from 2026 to 2031, taking retail value to USD 3.21 billion.

Which product sub-segment is expanding the quickest?

Energy shots lead with a 10.64% CAGR because consumers favor convenient, portion-controlled formats.

Why are Tetra Pak and pouch packages gaining share?

Tetra Pak and pouch packages avoid aluminum price swings, reduce logistics weight, and align with sustainability goals, underpinning a 10.80% CAGR.

Which channel will contribute most incremental sales by 2031?

Online retailers are forecast to expand at 11.46% CAGR, adding the largest new revenue pool.

Page last updated on: