Media Buying Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

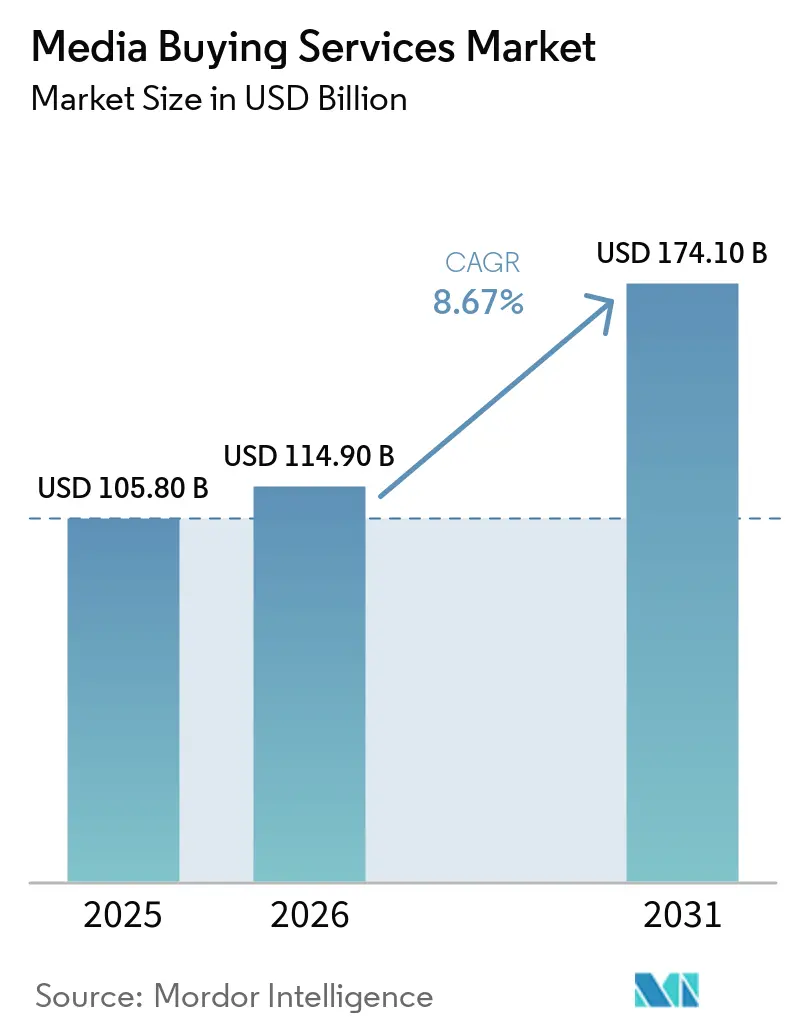

| Market Size (2026) | USD 114.90 Billion |

| Market Size (2031) | USD 174.10 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

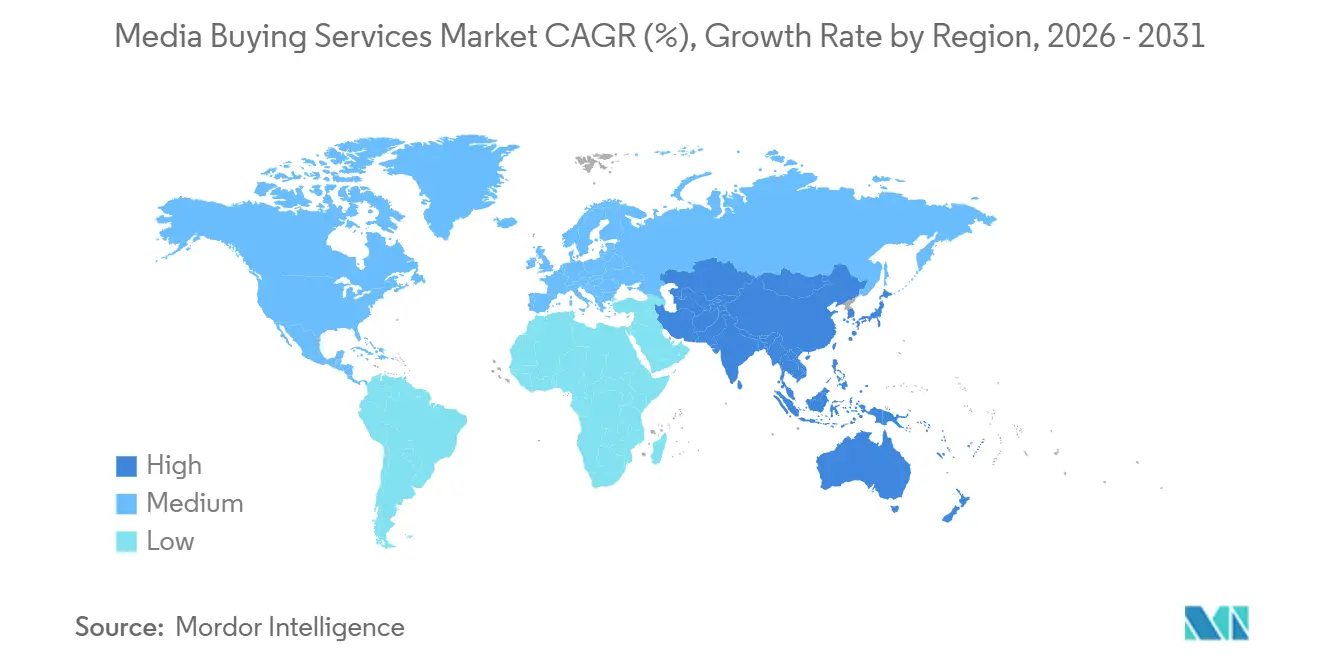

| Fastest Growing Market | Middle East |

| Largest Market | North America |

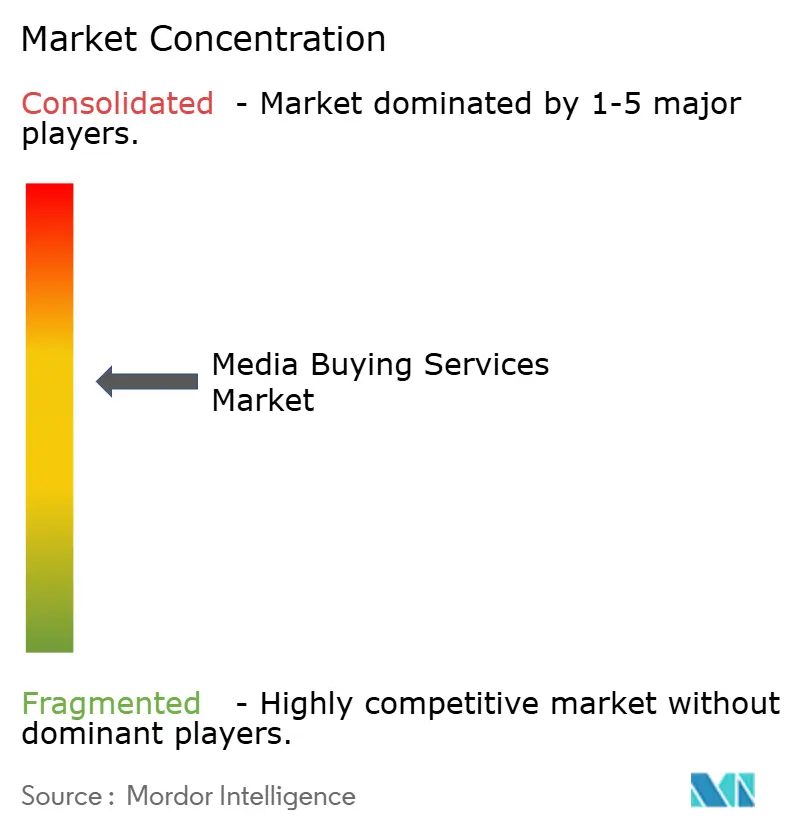

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Media Buying Services Market Analysis by Mordor Intelligence

The media buying services market size is projected to expand from USD 105.8 billion in 2025 and USD 114.9 billion in 2026 to USD 174.1 billion by 2031, registering a CAGR of 8.67% between 2026 to 2031. The media buying services market is growing because brands are shifting paid media budgets away from isolated campaign buying and toward ongoing, data-led management across multiple channels. The media buying services market also benefits from the fact that automated buying is no longer a niche function, which raises the value of partners that can manage activation, optimization, and measurement in the same workflow. Growth in the media buying services market is also supported by rising demand for connected TV, digital video, and retail media, where buying complexity is higher and direct outcome measurement matters more. Regional demand is no longer moving at the same pace, because North America still holds the largest base of advertiser spending, while Asia-Pacific is adding more of the incremental growth. Competitive conditions in the media buying services market are changing as holding companies, independent specialists, and consultancy-owned teams compete on data access, privacy-safe planning, and AI-enabled execution instead of scale alone.

Key Report Takeaways

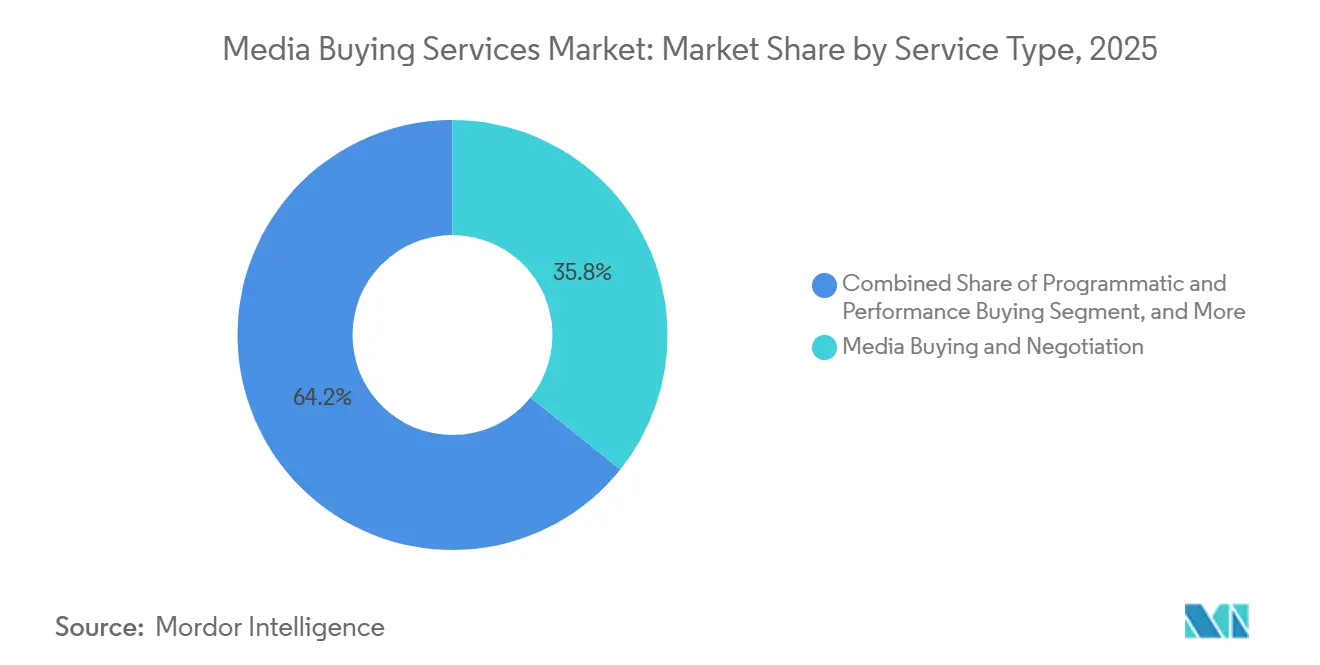

- By service type, media buying and negotiation held 35.76% of revenue in 2025, while programmatic and performance buying is projected to expand at a 9.46% CAGR through 2031.

- By media channel, search advertising accounted for 31.44% of the media buying services market size in 2025, while connected TV and OTT video is projected to advance at a 10.14% CAGR through 2031.

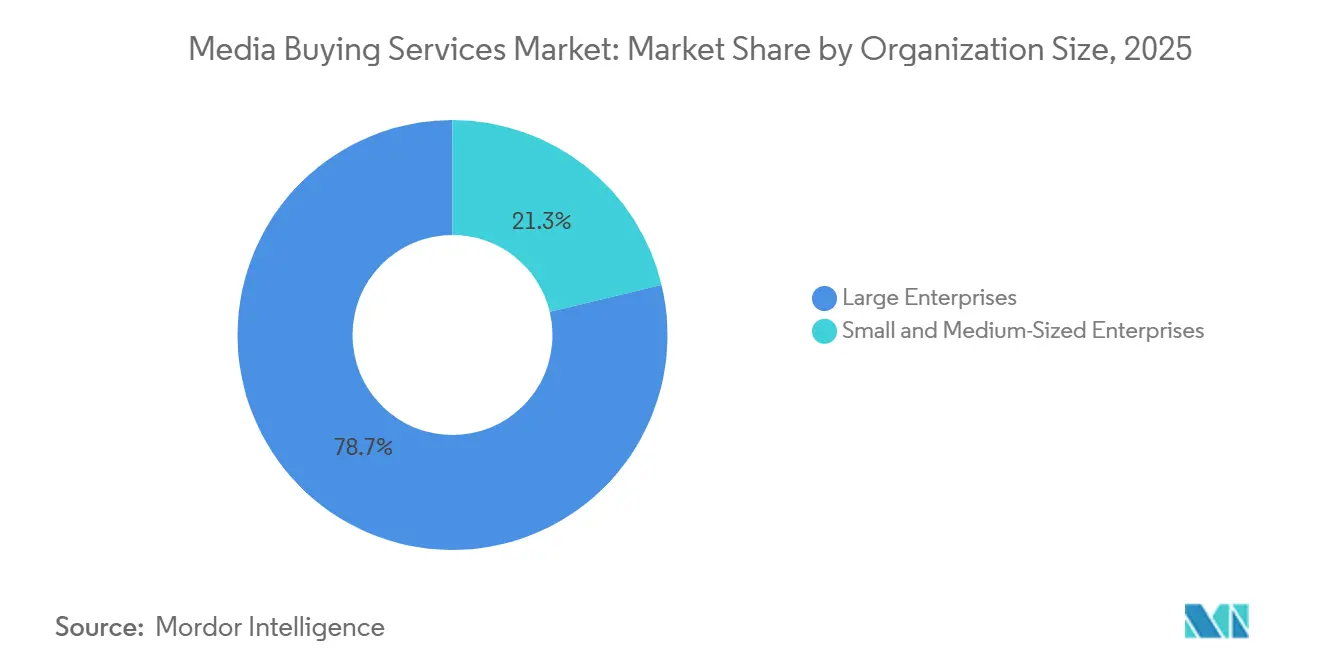

- By organization size, large enterprises held 78.73% of the media buying services market share in 2025, while SMEs recorded the highest projected CAGR at 10.07% through 2031.

- By end-user industry, retail and e-commerce accounted for 24.68% of the media buying services market in 2025, while healthcare is projected to expand at a 9.61% CAGR through 2031.

- By geography, North America accounted for 41.48% of the media buying services market in 2025, while the Middle East is projected to expand at a 8.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Media Buying Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Programmatic And AI-Driven Buying Becomes Core Agency Workflow | +2.5% | Global, with North America and APAC leading adoption | Short term (≤ 2 years) |

| Budget Migration Toward Connected TV, Retail Media, And Digital Video | +1.8% | North America leading, Europe and APAC following | Medium term (2-4 years) |

| Demand For Omnichannel Measurement And ROAS Accountability | +1.3% | Global | Medium term (2-4 years) |

| First-Party Data Activation And Privacy-Safe Audience Planning | +1.0% | EU core, spill-over to North America and APAC | Medium term (2-4 years) |

| Curated Marketplaces And Supply Path Optimization Favor Specialist Buying Partners | +0.8% | North America, with early gains in Western Europe | Short term (≤ 2 years) |

| Agentic AI Expands Outsourced Buying Among Mid-Market Brands | +0.7% | North America, expanding to Europe and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Programmatic And AI-Driven Buying Becomes Core Agency Workflow

Programmatic advertising has moved from a specialist capability to a default execution layer across digital media. In Germany, BVDW projected that programmatic buying would account for 80% of the country’s online display and video market in 2026, reaching EUR 6.5 billion, which equals USD 7.0 billion at the 2025 IRS average exchange rate.[1]Bundesverband Digitale Wirtschaft, “OVK-Prognose: Digitaler Werbemarkt wächst auf über acht Milliarden Euro,” BVDW, bvdw.org That shift changes agency selection criteria, because inventory access matters less when most buyers can reach the same pipes, and optimization logic matters more. The media buying services market is therefore placing more value on identity infrastructure, data models, and workflow automation than on manual execution alone. Agencies that cannot show a differentiated AI layer on top of standard platform access are facing stronger pressure on pricing and retention.

Budget Migration Toward Connected TV, Retail Media, And Digital Video

Connected TV and retail media are taking a larger share of new ad budgets, and that is changing where agencies create value. Dentsu projected global connected TV growth of 11.5% in 2026 and global retail media growth of 12.3% in the same year, which confirms that both channels are attracting outsized investment compared with the wider ad market. Retail media is gaining traction because it turns purchase intent data into an addressable and privacy-safe input for campaign planning. Agencies that can combine retail media signals with connected TV activation are building a tighter loop between exposure and purchase. That convergence is already shaping infrastructure choices, as shown by Stagwell’s April 2026 integration with FreeWheel to create a unified connected TV activation layer.

Demand For Omnichannel Measurement And ROAS Accountability

ROAS accountability is now a standard buying requirement across performance-led categories such as retail, healthcare, and BFSI. Advertisers still struggle to unify measurement across large closed platforms and open-web programmatic environments, and that gap keeps specialist partners relevant. In the media buying services market, agencies that can connect reporting across these environments are better placed to defend fees and expand scope. This is also why clean rooms, contextual overlays, and unified reporting dashboards are becoming part of the service mix rather than optional add-ons. IAB Tech Lab’s Clean Room Standards gained traction in 2025 and 2026, which supported the rise of a new measurement and activation layer inside the media buying services market.[2]IAB Tech Lab, “Clean Room Services Standards,” IAB Tech Lab, iabtechlab.com

First-Party Data Activation And Privacy-Safe Audience Planning

First-party data activation is no longer just a privacy response, and it is now part of competitive positioning in campaign planning. Consent-heavy rules in Europe and tighter data controls in the United States have increased the value of durable audience infrastructure. Agencies are responding by investing in identity resolution, clean-room connections, loyalty data onboarding, and publisher data partnerships. The media buying services market is therefore moving toward service models that depend less on third-party signal abundance and more on controlled data access. That shift gives outsourced partners a stronger role when they can combine audience planning, compliance handling, and media execution inside one operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Regulation And Signal Loss Reduce Targeting Precision | -1.2% | EU core, spill-over to North America and APAC | Medium term (2-4 years) |

| Ad Fraud, Brand Safety, And Viewability Risks Persist | -0.9% | Global | Short term (≤ 2 years) |

| Walled-Garden Measurement Gaps Limit Cross-Platform Optimization | -0.7% | Global, most acute in North America | Long term (≥ 4 years) |

| Margin Compression From In-Housing And Platform Automation | -0.5% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy Regulation And Signal Loss Reduce Targeting Precision

Privacy regulation has become a structural limit on addressable media rather than a narrow compliance issue. Cookie deprecation in major browsers and Apple’s App Tracking Transparency framework have reduced the volume of deterministic identifiers available for planning and optimization. That loss of signal has made audience reach planning less efficient across the open web and more fragmented across identity systems. In the media buying services market, the burden falls harder on smaller agencies that do not have legal, data, and engineering support built into their operating model. The result is a tougher planning environment where campaign precision depends more on first-party assets and publisher relationships than it did a few years ago.

Ad Fraud, Brand Safety, And Viewability Risks Persist

Media quality remains a meaningful drag on campaign efficiency and client confidence. Fraudlogix reported a global invalid traffic rate of 20.64% across 105.7 billion impressions collected in 2025, which shows how much spending is still exposed to fraudulent or non-human activity. This is not only a detection issue, because parts of the supply chain still benefit from impression volume even when quality is poor. AI-generated content adjacency is adding another layer of uncertainty for advertisers who need stronger control over context and brand suitability. The media buying services market, therefore, carries a persistent friction cost, especially for agencies that lack access to independent verification tools and stronger media quality workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Media Buying And Negotiation Anchors, Programmatic Disrupts

Media buying and negotiation retained 35.76% of service revenue in 2025, which kept this function at the center of the media buying services market size. That position remained durable because premium inventory in connected TV, sports, live news, and other high-value environments still relies heavily on direct deal structures. Buyers continue to value negotiated access, pricing discipline, and adjacency control in these environments. Those conditions keep human broker relationships relevant even as more execution shifts into software. This part of the media buying services market stayed resilient because clients still need certainty around premium placements and commercial terms.

Programmatic and performance buying is projected to record a 9.46% CAGR from 2026 to 2031, which makes it the fastest-growing service category in the media buying services market. Growth is tied to budget movement into open-web programmatic, private marketplaces, curated deals, and real-time optimization models. PubMatic said its AgenticOS platform had executed more than 30 fully autonomous end-to-end campaigns by Q1 2026, which showed how quickly workflow automation is moving into live buying operations. As transactional buying becomes more automated, agencies are placing more emphasis on strategy, analytics, and commerce activation as the fee-bearing layers of the media buying services market.

By Media Channel: Search Dominates As CTV Redraws Buying Priorities

Search advertising held 31.44% of channel revenue in 2025, which preserved its lead within the media buying services market. Search keeps that position because it captures clear lower-funnel intent and supports direct brand-to-outcome attribution across many verticals. Advertisers still rely on search to anchor performance budgets, especially when return visibility matters more than broad awareness. That stability creates consistent demand for agencies that can manage bidding, keywords, budget pacing, and cross-channel allocation. The media buying services market still leans on search because it combines spend discipline with measurable outcomes.

Connected TV and OTT video are projected to expand at a 10.14% CAGR through 2031, which makes it the fastest-growing media channel in the media buying services market. Growth is being pushed by ad-supported streaming, changing viewing habits, and the addition of commerce data into video planning. In Japan, internet advertising media expenditure grew 11.8% in 2025, driven mainly by SNS vertical video, which aligned with the broader move toward video-led discovery and activation. Display, digital video, digital audio, digital out-of-home, and retail media networks remain important, but the sharpest change is happening where video inventory, audience data, and quality controls now meet.

By Organization Size: Enterprise Concentration Obscures SME Growth Signal

Large enterprises held 78.73% of the media buying services market share in 2025, which reflected their larger budgets, wider geographic scope, and stronger need for coordinated execution. Agency groups still structure staffing, pricing, and delivery models around these accounts. Large advertisers also require more support in measurement, privacy-safe audience planning, and multi-channel activation. That keeps enterprise demand central to the media buying services market even as the client base starts to broaden.

SMEs are projected to grow at a 10.07% CAGR from 2026 to 2031, which makes them the fastest-rising buyer cohort in the media buying services market. AI-assisted buying tools are lowering the expertise and minimum-spend barriers that once kept smaller advertisers out of advanced programmatic workflows. More self-serve and agency-assisted models are opening access to campaign automation, audience planning, and optimization for brands with lower budgets. This opportunity is not a smaller version of enterprise buying, because it requires faster support, simpler reporting, and fees tied more closely to outcomes. Agencies that adapt to those needs are likely to capture the next layer of expansion in the media buying services market.

By End-User Industry: Healthcare Spend Surges As Retail Retains Scale

Retail and e-commerce accounted for 24.68% of demand in 2025, which kept the segment as the largest end-user base in the media buying services market. This lead reflects the sector’s heavy dependence on paid media for customer acquisition, promotion, and repeat purchase activity. Retail media networks have also changed the structure of demand because major retailers now act as both major buyers and major inventory owners. That makes neutrality, data access, and channel planning more complex for agencies serving the sector. The media buying services market therefore remains anchored by retail budgets even as the inventory landscape becomes more layered.

Healthcare is projected to expand at a 9.61% CAGR through 2031, making it the fastest-growing end-user group within the media buying services market size. Growth is tied to stronger direct-to-consumer prescription advertising, telehealth and digital therapeutics demand, and higher patient acquisition pressure after pandemic-era disruption. Regulatory complexity remains central, because digital and social promotion in healthcare requires tighter control over audience selection, claims handling, and platform choice. BFSI, IT and telecom, travel and hospitality, and media and entertainment remain important spending groups, but healthcare offers one of the clearest openings for specialized compliance-led buying.

Geography Analysis

North America remained the largest regional base in the media buying services market in 2025, accounting for approximately 41.48% of global market revenue. The United States drives most regional revenue because it combines concentrated advertiser spending with mature programmatic infrastructure. The region also hosts many of the largest holding company networks and buying technology partners, which keeps scale advantages high. Canada remains a solid secondary market with strong digital adoption, while Mexico is still earlier in maturity but is moving forward through mobile-first buying patterns. This concentration keeps the media buying services market highly competitive in North America, even as data use, conduct, and platform dependence draw more attention.

Europe represented the second-largest geography in the media buying services market. Germany’s online display and video advertising market is forecast to reach EUR 8.2 billion, which equals USD 8.9 billion in 2026, and programmatic is expected to account for 80% of transactions. France’s advertising market reached EUR 19.8 billion, which equals USD 21.4 billion in 2025. Digital grew 11% in that year, and digital is forecast to grow another 7.5% in 2026.[3]SRI / Irep / France Pub, “BUMP 2025: Un marché publicitaire sous tension, porté par le digital,” SRI France, sri-france.org Consent-driven data rules and a stronger premium publisher base continue to push European buyers toward programmatic guaranteed and curated private marketplace deals over open-auction buying. Asia-Pacific is the fastest-growing large regional cluster in the media buying services market. Japan’s total advertising spend crossed JPY 8,062.3 billion, which equals USD 53.4 billion in 2025, and internet advertising surpassed 50% of total ad investment for the first time. Hakuhodo DY ONE began programmatic TV buying through NTV’s AdRM-Exchange in July 2025 and added a unique-reach maximization bidding function in October 2025, demonstrating how broadcast inventory is being integrated into programmatic workflows across the region.

South America remains smaller than North America and Europe, but its digital buying base is still expanding through mobile-led advertising activity. The Middle East and Africa also remain smaller in absolute scale; however, the Middle East is projected to be the fastest-growing regional segment during 2026-2031, registering a CAGR of 8.86%. Growth is being supported by increasing digital advertising investments, rapid connected TV adoption, expanding retail media ecosystems, and government-backed digital transformation initiatives in countries such as Saudi Arabia and the United Arab Emirates. The media buying services market is widening fastest where local execution expertise can connect global tools with country-specific media systems.

Competitive Landscape

The media buying services market remained moderately concentrated in 2026. The 5 major holding company networks still controlled a disproportionate share of global managed billings, which kept the top tier influential in multinational reviews. At the same time, the broader media buying services market below that tier was more fragmented, with consultancy-owned units, performance independents, and platform-enabled specialists competing for different types of mandates. This split means scale still matters for global accounts, while specialization matters more in performance buying, retail media, healthcare compliance, and SME service models. Competitive pressure is therefore rising inside the top tier and outside it at the same time.

Strategic moves in 2026 showed that AI-enabled execution has become a clear battleground in the media buying services market. Stagwell became the first global marketing network to adopt The Trade Desk’s Koa Agents in April 2026, which signaled a direct move into agent-to-agent buying workflows. Later that month, Stagwell and FreeWheel launched a unified AI-powered connected TV platform to improve activation across premium video supply. PubMatic’s January 2026 launch of AgenticOS added more pressure on agencies and tech partners to rethink planning, curation, and fee transparency around autonomous buying.

The media buying services market is also shifting from planning expertise alone toward control of data layers, orchestration systems, and privacy-safe audience infrastructure. Agencies that lack a differentiated data spine face more price pressure because automation is reducing the value of manual execution alone. That creates room for specialists that can solve cross-border retail media activation, mid-market performance buying, or compliance-heavy vertical work better than broad network models. The result is a competitive field where the largest groups still lead on scale, but some of the fastest strategic repositioning is happening among firms building AI-led operating models and narrower domain expertise.

Media Buying Services Industry Leaders

WPP plc

Publicis Groupe S.A.

Omnicom Group Inc.

Dentsu Group Inc.

Havas N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Stagwell and FreeWheel announced on April 27, 2026 the launch of a unified AI-powered connected TV advertising platform. Integrating FreeWheel's Curation Hub and Buyer Cloud into Stagwell's media acquisition layer, the initiative enables Stagwell Curate, a centralized deal marketplace consolidating preferred CTV supply relationships, to offer direct, transparent access to premium video inventory at scale.

- April 2026: Stagwell became the first global marketing network to adopt The Trade Desk's Koa Agents, an agentic AI framework built on the Open Agentic Kit protocol, integrating it with Stagwell Media Platform to automate audience planning, inventory activation, and campaign optimization across the open internet. The partnership, announced on April 21, 2026, is structured as a global multi-stage rollout, with closed-beta client access expected later in 2026.

- May 2026: DoubleVerify extended global media quality measurement to LinkedIn Audience Network on May 21, 2026, delivering fraud, brand safety, viewability, and geography verification for B2B advertisers across LinkedIn's programmatic network, an expansion that reflects the growing priority of quality verification in professional-context media buying.

- March 2026: PubMatic and Amnet launched France's first agentic advertising campaign on March 31, 2026, using Claude LLM through PubMatic's AgenticOS. The campaign for client INTERBEV demonstrated a full natural-language planning-to-activation workflow, compressing what Amnet's traders reported as a 2-hour setup task to approximately 20 minutes, an early quantification of agentic productivity gains in a European media context.

Global Media Buying Services Market Report Scope

The Media Buying Services Market refers to the market for agencies and service providers that plan, negotiate, purchase, and optimize advertising space or time across digital and traditional media channels. The market is driven by brands’ need for better audience targeting, campaign performance, and cost-effective ad placements.

The Media Buying Services Report is Segmented by Service Type (Media Strategy and Planning, Media Buying and Negotiation, Programmatic and Performance Buying, Campaign Management and Optimization, and Measurement and Analytics), Media Channel (Search Advertising, Social Media Advertising, Display Advertising, Digital Video, and Connected TV and Over-the-Top Video), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Retail and E-commerce, Media and Entertainment, BFSI, IT and Telecom, Travel and Hospitality, and Healthcare), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Media Strategy and Planning |

| Media Buying and Negotiation |

| Programmatic and Performance Buying |

| Campaign Management and Optimization |

| Measurement and Analytics |

| Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support) |

| Search Advertising |

| Social Media Advertising |

| Display Advertising |

| Digital Video |

| Connected TV and Over-the-Top Video |

| Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH) |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Retail and E-commerce |

| Media and Entertainment |

| BFSI |

| IT and Telecom |

| Travel and Hospitality |

| Healthcare |

| Others (Automotive, Education, and Public sector) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Media Strategy and Planning | |

| Media Buying and Negotiation | ||

| Programmatic and Performance Buying | ||

| Campaign Management and Optimization | ||

| Measurement and Analytics | ||

| Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support) | ||

| By Media Channel | Search Advertising | |

| Social Media Advertising | ||

| Display Advertising | ||

| Digital Video | ||

| Connected TV and Over-the-Top Video | ||

| Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH) | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Retail and E-commerce | |

| Media and Entertainment | ||

| BFSI | ||

| IT and Telecom | ||

| Travel and Hospitality | ||

| Healthcare | ||

| Others (Automotive, Education, and Public sector) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the media buying services market?

The media buying services market was valued at USD 105.8 billion in 2025, is projected at USD 114.9 billion in 2026, and is expected to reach USD 174.1 billion by 2031 at an 8.67% CAGR.

Which service category leads revenue and which one grows the fastest?

Media buying and negotiation led with 35.76% of revenue in 2025, while programmatic and performance buying is projected to grow the fastest at a 9.46% CAGR through 2031.

Why is connected TV becoming more important for agencies?

Connected TV and OTT video is projected to grow at a 10.14% CAGR through 2031, and agencies are gaining from the higher planning, data, and activation complexity tied to video and retail media convergence.

Which client group is driving the next wave of growth?

Large enterprises still dominate demand with 78.73% share in 2025, but SMEs are the fastest-growing cohort at a 10.07% CAGR as AI-assisted buying lowers entry barriers.

Which end-user vertical matters most right now?

Retail and e-commerce remained the largest end-user segment with 24.68% share in 2025, while healthcare is the fastest-growing at a 9.61% CAGR because of stronger patient acquisition and compliance-led media demand.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing regional cluster, while North America remains the largest base and Europe stays important because of its strong premium publisher ecosystem and stricter consent environment.

Page last updated on: