Retail Media Network (RMN) Technology Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 9.74 Billion |

| Growth Rate (2026 - 2031) | 20.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail Media Network (RMN) Technology Platform Market Analysis by Mordor Intelligence

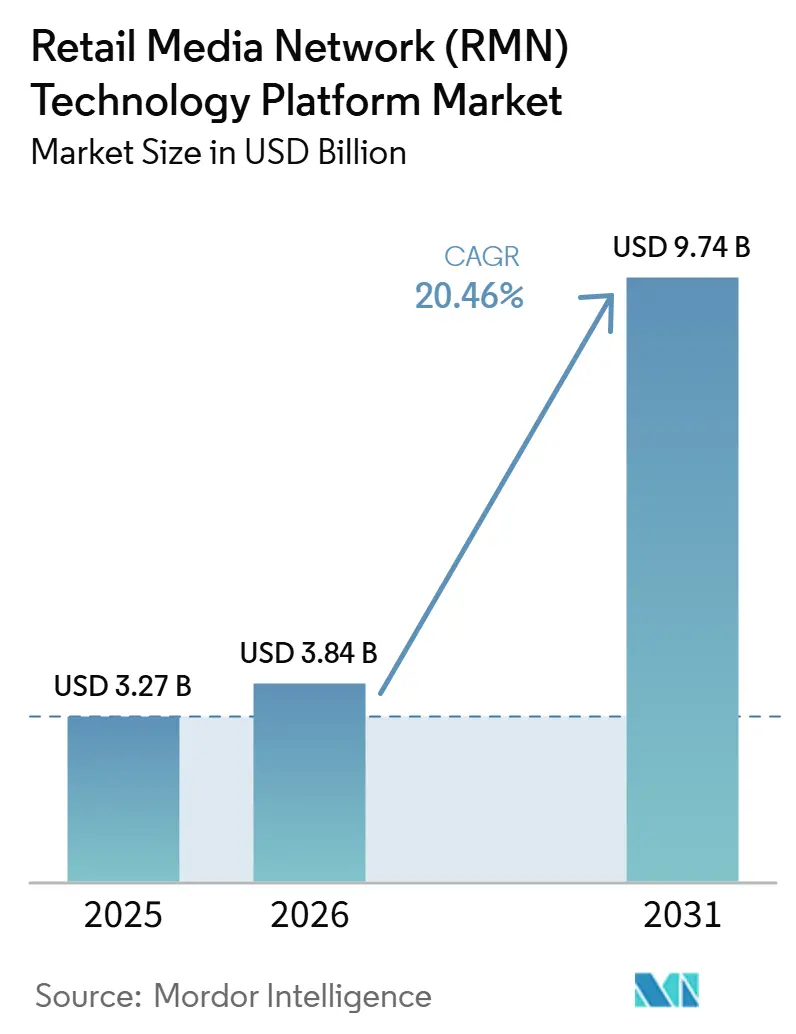

The retail media network (RMN) technology platform market size is projected to expand from USD 3.27 billion in 2025 and USD 3.84 billion in 2026 to USD 9.74 billion by 2031, registering a CAGR of 20.46% between 2026 to 2031. The retail media network (RMN) technology platform market is growing because retailers now treat commerce data as a revenue-generating asset instead of a support function for merchandising alone. Privacy rules, stricter consent requirements, and tighter restrictions on third-party access to identifiers have made retailer-owned purchase signals more important for advertisers that still need measurable targeting and closed-loop reporting. Competitive advantage is shifting toward platforms that connect ad serving, audience activation, and attribution within a single operating environment, favoring scaled retailers and specialist providers with flexible integrations. Omnichannel execution across on-site placements, off-site media, connected TV, and in-store screens is widening the addressable role of these platforms, while AI-led workflow automation is lowering the operating threshold for mid-tier retailers and smaller advertisers. The retail media network (RMN) technology platform market still faces a practical ceiling if measurement remains fragmented across networks and if rising ad loads weaken shopper experience on the retailer surfaces that make these platforms valuable in the first place.

Key Report Takeaways

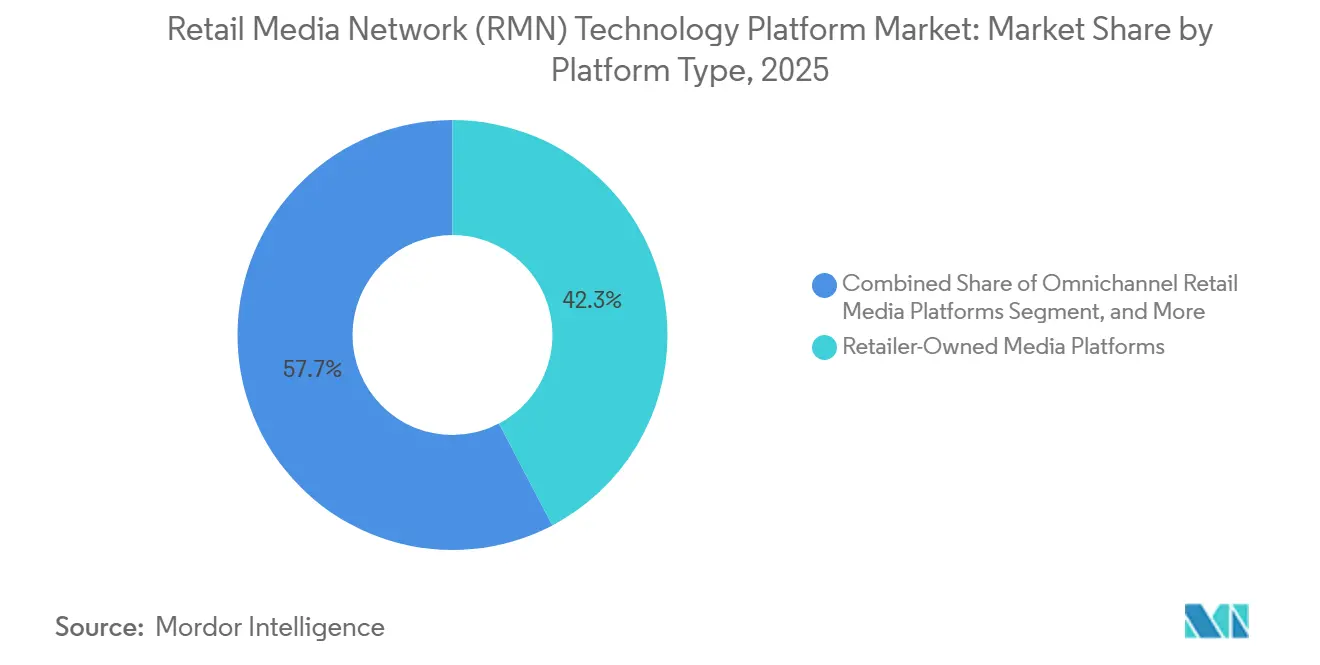

- By platform type, retailer-owned media platforms held 42.31% of the retail media network (RMN) technology platform market share in 2025, while omnichannel retail media platforms are projected to expand at a 24.83% CAGR through 2031.

- By ad format, search ads accounted for 31.24% of the retail media network (RMN) technology platform market in 2025, while video ads are projected to grow at a 26.47% CAGR through 2031.

- By deployment mode, cloud-based deployment held 74.18% share in 2025, while hybrid deployment is projected to grow at a 22.69% CAGR through 2031.

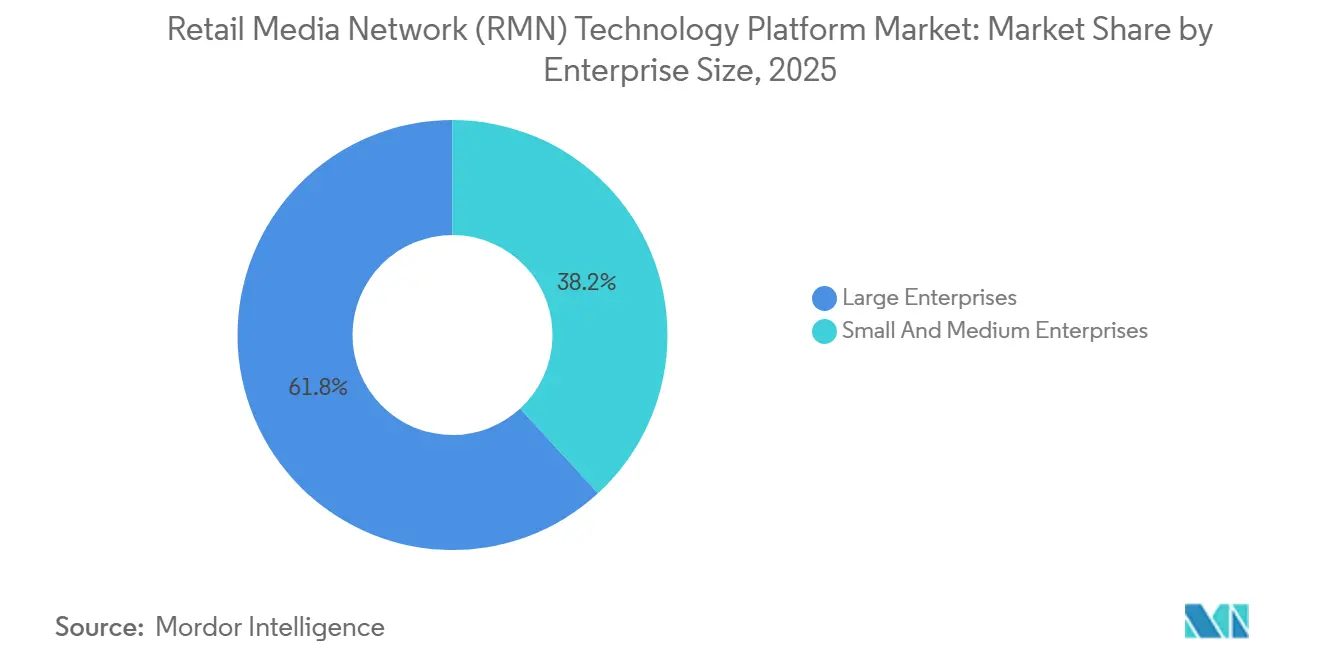

- By enterprise size, large enterprises held 61.83% share in 2025, while small and medium enterprises are projected to expand at a 23.94% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 28.76% of the market share in 2025, while automotive is projected to record the fastest growth at a 25.31% CAGR through 2031.

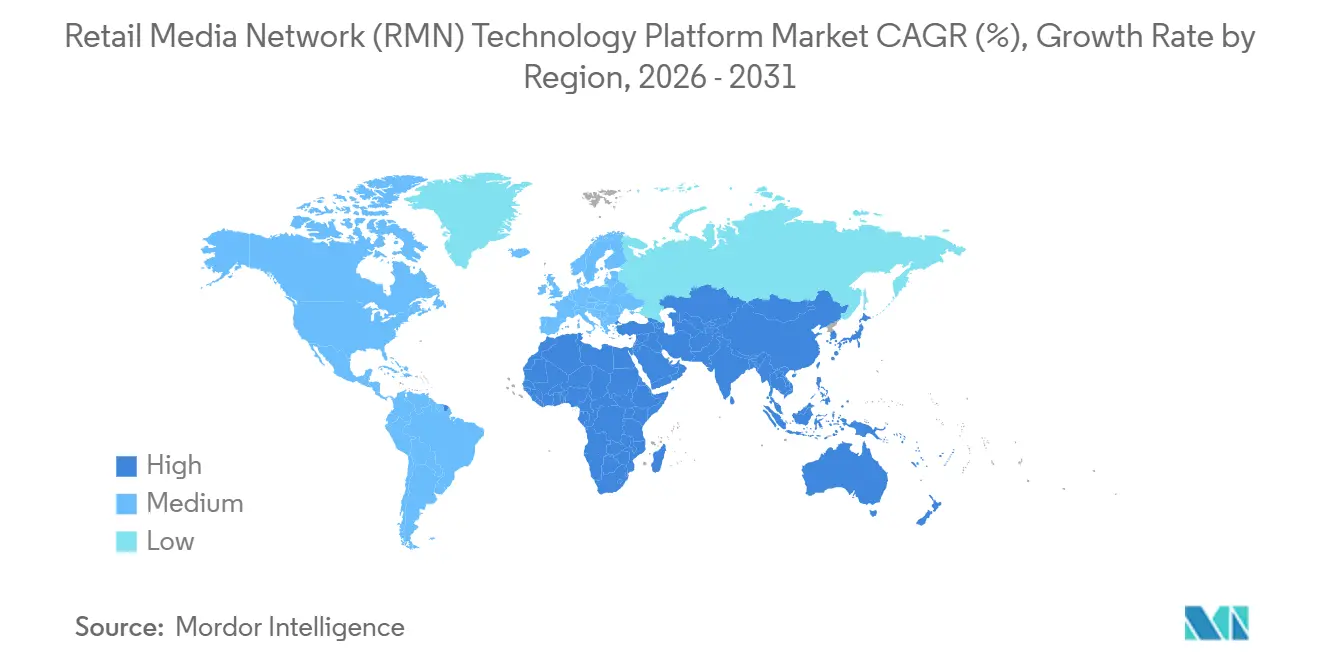

- By geography, North America held 36.42% share in 2025, while Asia-Pacific is projected to expand at a 24.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retail Media Network (RMN) Technology Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-Party Cookie Depreciation and First-Party Data Acceleration | +4.2% | Global, with early concentration in North America and Europe | Short term (≤ 2 years) |

| AI-Driven Audience Activation and Automated Campaign Operations | +3.8% | Global, led by North America and Asia-Pacific core | Medium term (2-4 years) |

| Retailer Monetization Pressure from High-Margin Media Revenue | +3.5% | North America and Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Omnichannel Orchestration Across On-Site, Off-Site, and In-Store Inventory | +3.1% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Self-Service Ad Platforms Expanding Access to Smaller Advertisers | +2.4% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Retail Media As a Commerce Content Operating System | +1.8% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Third-Party Cookie Depreciation and First-Party Data Acceleration

The retail media network (RMN) technology platform market now relies more on consented shopper data because third-party audience access is becoming less reliable and privacy obligations are becoming stricter.[1]Interactive Advertising Bureau, “Untangling the Issues in Commerce Media Networks,” IAB, iab.com Retailers that built loyalty programs, point-of-sale records, and authenticated account systems can offer targeting based on verified purchase behavior rather than rented external segments. That changes media allocation because brands can place spend inside environments where audience identity, transaction data, and conversion reporting already sit within the same commercial system. It also improves the compliance posture for advertisers because activation stays closer to opted-in customer records and away from more exposed data-sharing models. As those conditions spread across major markets, the retail media network (RMN) technology platform market is likely to favor platforms that keep audience activation close to the retailer data stack and inside clearer consent boundaries.

AI-Driven Audience Activation and Automated Campaign Operations

AI is moving from a support tool to an operating layer within the retail media network (RMN) technology platform market, as campaign setup, bidding, segmentation, and reporting all benefit from faster automation.[2]Walmart Connect, “The Next Generation of AI-Powered Retail Media with Walmart Connect,” Walmart Connect, walmartconnect.com The practical effect is that retailers do not need to rely as heavily on large manual teams to launch and maintain more sophisticated campaigns across formats. Walmart Connect strengthened that direction with Luminate Bid Intelligence, which links first-party purchase signals from its weekly shopper base to real-time targeting across display, video, and sponsored placements. Criteo and Dentsu also showed how AI interfaces are changing campaign management by enabling natural-language orchestration for retail media execution through a fully orchestrated MCP campaign launch in May 2026. As these tools become easier to deploy, the retail media network (RMN) technology platform market becomes more accessible to mid-tier retailers and smaller advertisers that previously struggled with operational complexity.[3]Pacvue, “Pacvue Launches MCP Server, Making Commerce Media Data Accessible Across Enterprise AI Tools,” Pacvue, pacvue.com

Retailer Monetization Pressure from High-Margin Media Revenue

Retailers are placing greater emphasis on media infrastructure because advertising provides a revenue stream that is less dependent on product margins and more closely tied to the value of their shopper data. That pressure is pushing the retail media network (RMN) technology platform market toward platforms that can convert supplier demand into transparent, measurable, and repeatable campaigns across owned digital inventory.[4]Skai, “The 2026 State of Retail Media Measurement and Incrementality,” Skai, skai.io It is also changing supplier relationships because spend that once sat within broader trade promotion discussions is moving into self-serve or API-connected media-buying environments, where performance is easier to monitor. Retailers that can expose campaign controls and audience tools, and demand access, in a cleaner workflow are better positioned to win those budgets at scale. The retail media network (RMN) technology platform market, therefore, rewards providers that can help merchants monetize traffic without forcing them into slow, service-heavy operating models.

Omnichannel Orchestration Across On-Site, Off-Site, and In-Store Inventory

The retail media network (RMN) technology platform market is moving beyond single-surface ad serving, as advertisers seek a single planning and execution layer across on-site listings, off-site activation, video inventory, and in-store media. That matters because many purchase journeys start in one channel and end in another, which weakens the value of isolated campaign systems. Mirakl took this direction in March 2026, when it launched MCP-native ad serving within Mirakl Ads, enabling retailers to surface sponsored products directly in on-site AI shopping agents without changing existing campaigns. Walmart Connect is also aligning purchase data with display, video, and sponsored formats to support broader cross-format execution rather than isolated placements. Providers that reduce the number of tools, interfaces, and reporting handoffs required across channels are likely to keep gaining share in the retail media network (RMN) technology platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Measurement Fragmentation and Weak Incrementality Proof | -1.9% | Global | Short term (≤ 2 years) |

| Integration Complexity Across Legacy Retail Tech Stacks | -1.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Privacy, Consent, and Data Localization Compliance Burden | -1.1% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Ad Load Versus Shopper Experience Trade-Off | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Measurement Fragmentation and Weak Incrementality Proof

Measurement remains a real constraint because each network still tends to define lift, attribution windows, and test design in its own way, making direct performance comparisons difficult. The IAB and IAB Europe released joint incrementality guidance in November 2025, but a shared definition alone does not ensure uniform execution across networks. Brands are clearly asking for stronger proof of outcome, and Skai's 2026 work on measurement and incrementality shows that this remains one of the central conditions for budget expansion. The problem for the retail media network (RMN) technology platform market is that weak comparability lowers confidence, which can cap spending even when campaign results look strong within a single network. Until measurement becomes more auditable across platforms, the retail media network (RMN) technology platform market is likely to face budget friction from advertisers that want proof they can compare across retailers on a fair basis.

Integration Complexity Across Legacy Retail Tech Stacks

The retail media network (RMN) technology platform market still has to work around retail systems that were not originally built for real-time ad decisioning, audience activation, and cross-channel reporting. That creates friction between commerce platforms, data layers, ad servers, and analytics tools, especially when retailers try to scale quickly without a unified architecture. API-first providers are gaining traction because they let retailers connect data and campaign functions in smaller steps instead of replacing the entire stack at once. Kevel's Adobe Experience Platform destination and its partnership with Skai both reflect the value retailers place on more direct audience activation and demand connectivity across systems. Even so, the retail media network (RMN) technology platform market will continue to face rollout delays and uneven execution, as merchants still depend on fragmented legacy infrastructure and limited internal technical capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Omnichannel Networks Raise The Standard For Retail Media Infrastructure

Retailer-owned media platforms held a 42.31% share in 2025, reflecting the advantage of controlling shopper identity, inventory, and attribution within a single commercial environment. In the retail media network (RMN) technology platform market, that model benefits the largest merchants by enabling them to monetize traffic directly while keeping audience and conversion data close to the transaction layer. Amazon Ads and Walmart Connect illustrate how far this structure can scale when ad demand, retail traffic, and closed-loop reporting reinforce one another. It also explains why brands often prioritize the biggest retailer-operated platforms first when they want clearer purchase-linked measurement and broad category reach. The retailer-owned segment, therefore, led not just because of media inventory, but because it packaged data depth, control, and measurement into a single operating system.

Third-party retail media platforms still play an important role because they let advertisers access multiple retailer relationships from a single buying point rather than managing each network independently. That reduces workflow strain for brands that need broader reach across mid-market merchants whose proprietary platforms are still developing. The retail media network (RMN) technology platform industry also leaves room for specialists that can aggregate demand and simplify execution where retailer scale is not yet sufficient on its own. Omnichannel platforms are projected to grow at a 24.83% CAGR through 2031, as retailers seek unified systems that connect on-site ads, off-site activations, in-store surfaces, and measurement without separate tools. Mirakl's MCP-native ad serving launch and Pacvue Prism both demonstrate how the market is moving toward broader orchestration rather than isolated point solutions.

By Ad Format: Video Expands While Search Keeps Conversion Leadership

Search ads held a 31.24% share in 2025, which confirms that sponsored products remain the core performance format for the retail media network (RMN) technology platform market. Their strength comes from intent, proximity to purchase, and the ease with which advertisers can connect bidding decisions to measurable commercial outcomes. Search placements also fit naturally into retailer websites and apps because they can be embedded in discovery flows without radically changing the shopping experience. Display and sponsored content continue to support awareness and consideration, but the budget center of gravity still sits closer to conversion-oriented placements. Native formats remain smaller, yet they matter because retailers need ad units that preserve usability as monetization intensity rises.

Video ads are projected to grow at a 26.47% CAGR through 2031, which makes them the fastest-growing format in the retail media network (RMN) technology platform market. That shift is closely tied to connected TV adoption, richer product storytelling, and the growing effort to link upper-funnel exposure with commerce outcomes. The IAB's 2026 digital video work shows that video remains a growth area, while self-serve tools are lowering entry barriers for advertisers that want to test broader media strategies. Mirakl and Walmart Connect also show how video, sponsored commerce, and audience data are moving into tighter operational alignment across surfaces. As a result, the retail media network (RMN) technology platform market is becoming less dependent on a single bottom-funnel format, even though search still anchors monetization.

By Deployment Mode: Hybrid Adoption Reflects The Push For Speed And Control

Cloud-based deployment held 74.18% share in 2025, which shows how strongly the retail media network (RMN) technology platform market favors fast integration, elastic processing, and API-led activation. Real-time bidding, audience segmentation, campaign adjustment, and reporting all work more efficiently when data services and ad decisioning can scale without long infrastructure cycles. Cloud-native providers have gained ground because they shorten time-to-launch and reduce the amount of custom engineering retailers need before campaigns can go live. That matters in a market where merchants want monetization systems that can fit into broader commerce operations without lengthy technology replacement projects. It also explains why many specialist providers present interoperability and activation speed as core product strengths rather than secondary features.

Hybrid deployment is projected to grow at a 22.69% CAGR through 2031, as retailers still need tighter control over sensitive shopper data across several jurisdictions. The appeal of hybrid architecture is that it lets merchants keep critical records in private or controlled environments while using cloud-based components for decisioning and campaign execution. That makes the hybrid less of a temporary compromise and more of an intentional operating model for retailers, balancing speed with governance. The retail media network (RMN) technology platform market is, therefore, rewarding providers that can plug modular services into existing retailer systems rather than insisting on a fully uniform stack. Privacy rules in Europe, state-level compliance obligations in the United States, and cross-border transfer limits all support this direction.

By Enterprise Size: Smaller Advertisers Gain Access Through Simpler Tools

Large enterprises held a 61.83% share in 2025, reflecting the early shape of the retail media network (RMN) technology platform market, where managed services, minimum-spend requirements, and specialized commerce teams favored larger advertisers. National brands and large agencies could absorb the operational work required to manage multiple retailer relationships, formats, and reporting systems simultaneously. They also had the staff depth to optimize bids, creative, and measurement in environments that were still maturing. This legacy advantage remains visible because enterprise budgets still anchor volume across the biggest networks. It is one reason many platform providers first built their products around agency workflows, broad brand portfolios, and high-frequency campaign management.

Small and medium enterprises are projected to grow at a 23.94% CAGR through 2031 because self-serve design, AI-assisted setup, and simpler interfaces are making participation easier. Pacvue's MCP server and its broader commerce media tooling reflect the move toward plain-language access, quicker reporting, and more scalable management for a wider advertiser base. Walmart Connect's AI bidding direction also supports a model where better automation reduces the manual burden that once kept smaller advertisers from competing effectively. The retail media network (RMN) technology platform industry is therefore opening up to a broader set of merchants, marketplace sellers, and mid-sized brands that can now access tools previously geared toward larger accounts. The pace of that shift will depend on how well platforms continue to reduce complexity without weakening control over targeting, spend, and measurement.

By End-User Industry: Automotive Broadens The Addressable Use Case

Retail and e-commerce accounted for 28.76% of the market in 2025, consistent with the origins of the retail media network (RMN) technology platform market. These operators already owned the transaction histories, product discovery surfaces, and conversion loops that make commerce media effective, so they entered with structural advantages that other sectors are still trying to build. The category also continues to attract heavy use from consumer packaged goods and fast-moving consumer goods brands that need visibility near the digital shelf. Consumer electronics, BFSI, healthcare, travel, and telecom remain meaningful because each can adapt first-party audience targeting to its own conversion cycle. The common pattern across these sectors is the effort to monetize proprietary demand signals rather than relying solely on broad external advertising channels.

Automotive is projected to grow at a 25.31% CAGR through 2031, which shows that the retail media network (RMN) technology platform market is expanding well beyond traditional retail categories. Longer purchase journeys, model-level targeting needs, and strong value per conversion make automotive a good fit for first-party data-led activation and closed-loop measurement. Video, search, and inventory-aware messaging also align well with dealer and marketplace needs because shoppers often move through research, comparison, and inquiry stages before purchase. That makes the vertical structurally similar to earlier retail media expansion in grocery, where transaction-linked data created a monetizable signal advantage. As more non-retail sectors build comparable data assets, the retail media network (RMN) technology platform market will continue to expand into new advertiser groups.

Geography Analysis

North America accounted for 36.42% of the market in 2025, making it the largest regional block in the retail media network (RMN) technology platform market. The region benefits from the presence of the biggest retailer-led advertising businesses, deep advertiser familiarity with commerce media, and broad availability of shopper data tied to large digital commerce ecosystems. Scale still matters here because large operators can offer inventory breadth, purchase-linked reporting, and more mature activation tools than most smaller networks. Walmart Connect's continued AI investment and broad multi-format activation show how North American leaders are trying to deepen advertiser value rather than rely only on traffic scale. At the same time, measurement expectations are rising, which continues to pressure platform providers to improve comparability and auditability across retail media programs.

Asia-Pacific is projected to grow at a 24.19% CAGR through 2031, which makes it the fastest-growing region in the retail media network (RMN) technology platform market. The region supports faster expansion because digital commerce is already deeply embedded in shopping behavior across several large economies, which creates dense first-party signal pools. Mobile-led engagement patterns also make commerce surfaces easier to monetize through sponsored placements, video, and integrated campaign journeys. Many retailers and marketplaces in the region already operate at a scale where audience activation and closed-loop measurement can become viable revenue engines rather than side offerings. That combination leaves Asia-Pacific well positioned to continue attracting platform investment as the retail media network (RMN) technology market becomes increasingly global.

Europe remained a core region within the retail media network (RMN) technology platform market, and GDPR-linked data-handling requirements and cross-border transfer constraints more directly shape its development path. Those conditions create a stronger demand for architectures that support consent control, data minimization, and more localized activation workflows. South America is moving from pilot activity toward more structured adoption, and provider partnerships around retail media scaling show that the region is gaining strategic attention from platform vendors. Middle East and Africa remain earlier-stage opportunities, but digital commerce investment and expanding shopper data infrastructure give the region a longer runway within the retail media network (RMN) technology platform market.

Competitive Landscape

The retail media network (RMN) technology platform market is fragmented, as a small group of scale operators continues to shape advertiser expectations for inventory depth, measurement quality, and campaign sophistication. Large retailer-led ecosystems set the performance benchmark, while specialist technology providers compete by making retail media easier to launch, manage, and extend across multiple merchant environments. This structure means market leadership does not depend on a single dimension alone, because traffic scale, first-party data quality, activation tools, and interoperability all matter simultaneously. The strongest vendors are those that can either control a powerful retailer environment directly or provide the connective layer that helps retailers and advertisers work across fragmented networks. That is why the competitive field includes both retail giants and specialist adtech firms rather than a single vendor class.

A clear theme in the retail media network (RMN) technology platform market is the move toward open, API-first, and AI-ready infrastructure. Kevel's Adobe Experience Platform destination and its strategic partnership with Skai both point to the value of linking retailer audience data more directly with activation and demand access. Criteo and Dentsu's fully orchestrated MCP campaign shows how natural-language interaction and agentic workflow design are becoming part of campaign execution rather than an experimental layer. Pacvue's MCP server extends this logic to reporting and enterprise workflow integration, helping advertisers move retail media data into broader decision systems more quickly. In practical terms, the retail media network (RMN) technology platform market rewards vendors that reduce operational friction as much as those that add new media surfaces.

Another competitive theme is the race to serve new interfaces and new decision rules before they become mainstream. Mirakl's MCP-native ad serving and Zitcha's partnership with Pentaleap both show how providers are adapting to AI shopping agents, relevance-led merchandising, and tighter links between ad outcomes and product economics. These moves matter because retailers want ad products that support category objectives and the shopper experience, rather than working against them. Measurement standards are also becoming part of competition, since stronger incrementality frameworks can influence whether large advertisers are willing to scale budgets across networks. The retail media network (RMN) technology platform market is therefore moving toward a contest over orchestration quality, data governance, and cross-network usability rather than simple ad serving alone.

Retail Media Network (RMN) Technology Platform Industry Leaders

Kevel, Inc.

Epsilon Data Management, LLC

Criteo S.A.

Pacvue, Inc.

Skai Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zitcha Pty Ltd and Pentaleap, Inc. announced a formal partnership to connect retail media auction decisions to product-level margin and relevance data. The integration combines Pentaleap's unified product ranking engine with Zitcha's Margin Manager merchant intelligence layer, enabling retailers to align sponsored product outcomes with sell-through velocity and category margin objectives simultaneously.

- May 2026: Criteo S.A. and dentsu launched the first fully orchestrated MCP campaign in retail media, enabling brands using large language model assistants to create, manage, and monitor retail media campaigns in natural language through Criteo's agentic innovation layer. The capability connects real-time commerce intelligence, including SKU-level purchase intent data and category demand signals, to campaign optimization without requiring platform switching.

- April 2026: Topsort, Inc. launched Sponsored Prompts, the market's first agentic ad format designed to monetize AI-powered chat and shopping agent interfaces. Delivered through a Topsort MCP server, Sponsored Prompts integrates with existing sponsored listing auction infrastructure and campaign structures, allowing marketplaces to extend retail media monetization into conversational commerce environments without building new systems.

- April 2026: Topsort, Inc. announced an integration with Placements.ai's agentic operating system for digital advertising, enabling streamlined ad sales, contract management, real-time optimization, and reporting within a connected system designed for enterprise retail media operators.

Global Retail Media Network (RMN) Technology Platform Market Report Scope

The retail media network (RMN) technology platform market refers to the ecosystem of software solutions that enable retailers to build, manage, and monetize their digital advertising inventory by allowing brands and advertisers to target shoppers directly on the retailer's digital properties (such as e-commerce websites and mobile apps) and in-store digital channels. These platforms leverage retailer first-party data to offer advanced audience targeting, campaign management, and closed-loop attribution for advertisers across various ad formats, including display, search, sponsored content, video, and native ads. The market includes retailer-owned, third-party, and omnichannel retail media platforms deployed via cloud, on-premise, or hybrid models. It serves both large enterprises and small and medium enterprises across industries such as CPG/FMCG, consumer electronics, BFSI, and automotive, ultimately providing retailers with a high-margin revenue stream while giving advertisers a controlled environment to reach high-intent consumers at the point of purchase.

The Retail Media Network (RMN) Technology Platform Market Report is Segmented by Platform Type (Retailer-Owned Media Platforms, Third-Party Retail Media Platforms, and Omnichannel Retail Media Platforms), Ad Format (Display Ads, Search Ads, Sponsored Content, Video Ads, and Native Ads), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small And Medium Enterprises), End-User Industry (Retail & E-Commerce, CPG/FMCG, Consumer Electronics, BFSI, Healthcare, Automotive, Travel, Telecom, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Retailer-Owned Media Platforms |

| Third-Party Retail Media Platforms |

| Omnichannel Retail Media Platforms |

| Display Ads |

| Search Ads |

| Sponsored Content |

| Video Ads |

| Native Ads |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail & E-Commerce |

| CPG/FMCG |

| Consumer Electronics |

| BFSI |

| Healthcare |

| Automotive |

| Travel |

| Telecom |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform Type | Retailer-Owned Media Platforms | ||

| Third-Party Retail Media Platforms | |||

| Omnichannel Retail Media Platforms | |||

| By Ad Format | Display Ads | ||

| Search Ads | |||

| Sponsored Content | |||

| Video Ads | |||

| Native Ads | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail & E-Commerce | ||

| CPG/FMCG | |||

| Consumer Electronics | |||

| BFSI | |||

| Healthcare | |||

| Automotive | |||

| Travel | |||

| Telecom | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the retail media network (RMN) technology platform market?

The retail media network (RMN) technology platform market was valued at USD 3.27 billion in 2025, stands at USD 3.84 billion in 2026, and is forecast to reach USD 9.74 billion by 2031 at a 20.46% CAGR.

Which platform type leads revenue generation in this space?

Retailer-owned media platforms led in 2025 with 42.31% share because they combine first-party shopper data, owned inventory, and closed-loop reporting under one operator.

Which ad format is growing the fastest across retail media technology platforms?

Video ads are projected to grow the fastest at a 26.47% CAGR through 2031, while search ads remained the largest format in 2025 with a 31.24% share.

Why are cloud and hybrid deployment models both important for retailers?

Cloud led with 74.18% share in 2025 because it supports faster activation and integration, while hybrid is projected to grow at a 22.69% CAGR because retailers still need tighter control over sensitive shopper data.

Which advertiser group is creating the next wave of demand?

Small and medium enterprises are projected to grow at a 23.94% CAGR as self-serve tools and AI-assisted workflows make campaign setup and reporting easier to manage.

Which region is expanding the fastest and which one is the largest?

North America held the largest share at 36.42% in 2025, while Asia-Pacific is projected to record the fastest regional growth at a 24.19% CAGR through 2031.

Page last updated on: