Ventilators Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

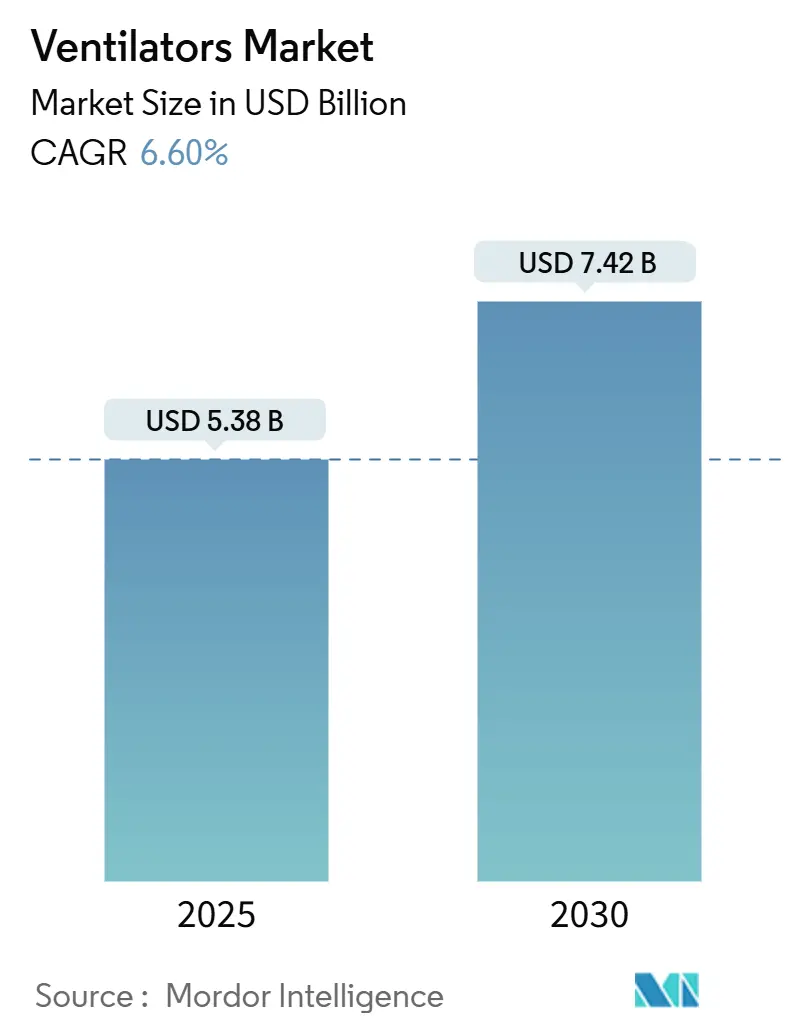

| Market Size (2025) | USD 5.38 Billion |

| Market Size (2030) | USD 7.42 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ventilators Market Analysis by Mordor Intelligence

The Ventilators Market size is estimated at USD 5.38 billion in 2025, and is expected to reach USD 7.42 billion by 2030, at a CAGR of 6.60% during the forecast period (2025-2030).

Momentum has shifted from the pandemic-driven spike toward structural growth rooted in population aging, the high prevalence of chronic respiratory disorders, and rapid product innovation that embeds decision-support software and connectivity into critical-care workflows. Hospitals are replacing legacy systems with intelligent platforms that lower alarm fatigue, self-calibrate for lung-protective strategies, and interface seamlessly with electronic health records. Subscription-based ventilation-as-a-service models that bundle hardware, analytics, and maintenance are gaining traction among budget-constrained providers because they convert large capital outlays to predictable operating expenses. Manufacturers are also responding to sustainability mandates by lowering power consumption and offering upgrade kits that extend asset life cycles, an approach that helps hospitals meet decarbonization targets without major fleet overhauls.

Key Report Takeaways

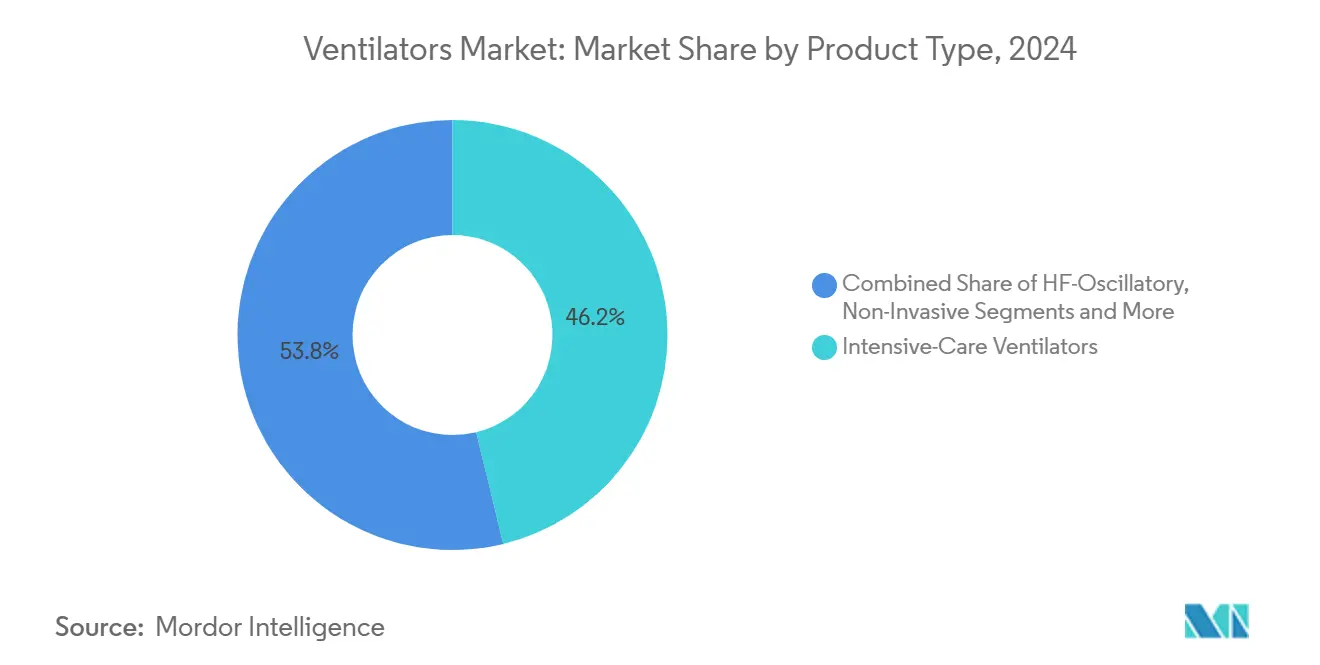

- By product type, intensive-care ventilators led with 46.2% of ventilators market share in 2024; portable ventilators are forecast to expand at an 8.7% CAGR through 2030.

- By interface, invasive ventilation held 55.7% of the market in 2024, while non-invasive ventilation is advancing at a 9.3% CAGR to 2030.

- By end user, hospitals and clinics captured 63.8% of the 2024 market; home-care settings are projected to grow at an 8.9% CAGR, reflecting payer support for out-of-hospital respiratory therapy.

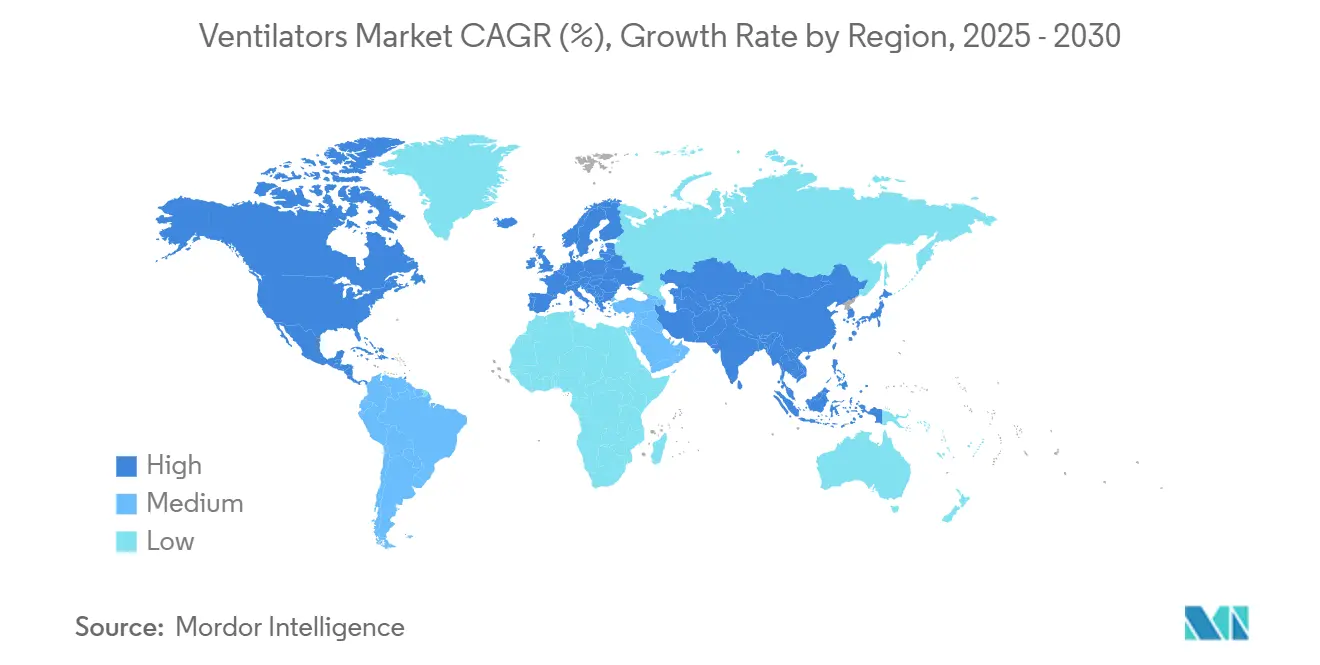

- By geography, North America accounted for 34.6% of the ventilators market revenue in 2024; Asia-Pacific is set to record the fastest 15.9% CAGR through 2030.

Global Ventilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing ICU bed capacity in emerging economies | +1.20% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Rapid adoption of non-invasive ventilation | +0.90% | North America, Europe | Short term (≤ 2 years) |

| Portable ventilators for EMS fleets | +0.70% | North America, Europe, developed APAC | Short term (≤ 2 years) |

| AI-enabled closed-loop algorithms | +0.80% | Global, early uptake in North America & Europe | Long term (≥ 4 years) |

| Hospital decarbonization upgrades | +0.40% | Europe, North America, Australia | Medium term (2-4 years) |

| Subscription-based ventilation services | +0.60% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing ICU Bed Capacity in Emerging Economies

Infrastructure expansion programs across China, India, Indonesia, and Gulf Cooperation Council states are lifting base demand for high-acuity ventilators, thereby driving growth in the ventilators market.. China’s plan to reach 15 intensive-care beds per 100,000 people by 2025 equates to an incremental requirement of more than 200,000 machines over the next two years.[1]National Health Commission of the People’s Republic of China, “China Moves to Improve Critical Care Medical Services,” nhc.gov.cnIndian private hospital chains have earmarked INR 11,500 crore (USD 1.38 billion) for 4,000 new beds in FY 2025-26, with critical-care equipment procurement built into every project budget. Indonesia’s medical device roadmap, which applies local-content rules and tax incentives, further stimulates purchasing from regional assembly partners. These multi-country initiatives align with aging populations and pollution-linked lung disease, ensuring that incremental bed capacity translates directly into ventilator installations rather than remaining idle.

Rapid Adoption of Non-Invasive Ventilation in Chronic-Care Settings

Remote-monitored home NIV cut COPD-related hospital readmissions by 45% within 12 months in a recent cohort study, while lowering bed-day burden and improving survival.[2]Charlotte Levey, “Impact of Remote-Monitored Home Non-Invasive Ventilation on Patient Outcomes,” medrxiv.org High-intensity NIV protocols reduced annual exacerbation frequency from 1.5 to 0.5 per patient, a clinically meaningful shift that convinces payers to reimburse device rental and tele-monitoring services. further supporting growth in the ventilator market. Hospitals save USD 449,101 over a 90-day episode of care when NIV replaces more invasive respiratory assist devices, strengthening the financial case for early community deployment. Feasibility pilots that link provider companies with hospital respiratory teams achieved 74% enrolment and high patient-reported satisfaction while trimming clinician workload through automated data dashboards.

Surging Demand for Portable Ventilators from EMS Fleets

First-responder agencies are overhauling fleets after pandemic usage peaks, switching to lighter turbine-driven models that remove compressed-air dependency without compromising performance. Devices such as Hamilton’s HAMILTON-T1 meet military ruggedization standards and deliver up to nine hours of battery life, a specification increasingly written into municipal EMS tenders. Recalls of older transport units accelerated replacement cycles and raised awareness of connectivity and cybersecurity features that ensure data integrity during hand-offs to hospital teams. Disaster-preparedness funding streams in the United States, Japan, and Australia further underpin demand for transport ventilators that can be stockpiled without specialized gas infrastructure.

AI-Enabled Closed-Loop Ventilation Algorithms

Artificial-intelligence-driven modes automatically titrate pressure, volume, and oxygen fractions to minimize ventilator-induced lung injury marking a transformative shift in the ventilators market.. Clinical trials show IntelliVent-ASV lowered manual setting interventions by 42% compared with conventional protocols while improving end-tidal CO₂ control and reducing traumatic brain injury mortality to 8% from 24%. Reinforcement-learning engines that train on anonymized ICU data have demonstrated 91.7% accuracy in proportional-assist mode selection, paving the way for adaptive support solutions that learn across patient populations. Regulators now require algorithm change-control plans and post-market surveillance, prompting vendors to build real-time performance dashboards into their platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent semiconductor shortages | -0.80% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Reimbursement caps on home ventilation | -0.60% | North America, Europe, developed APAC | Medium term (2-4 years) |

| OEM liability exposure post emergency use | -0.50% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Cybersecurity vulnerabilities in connected ICU devices | -0.30% | Global, higher impact in digitally advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Shortages Elongating Lead Times

Up to 50% of ventilator sub-assemblies rely on microcontrollers that share fabrication lines with consumer electronics. A Deloitte poll found 75% of device manufacturers reported allocation cuts that delayed shipments by an average of eight weeks, forcing some providers to ration equipment.[3]Kevin Zhai, “The Changing Landscape of Semiconductor Manufacturing: Why the Health Sector Should Care,” frontiersin.org Medical buyers account for only 11% of total industrial chip demand, limiting their leverage during industry-wide crunches. Strategies now include dual-sourcing, board redesigns that accept pin-compatible parts, and long-term supply agreements extending to ten years.

Cybersecurity Vulnerabilities in Connected ICU Ventilators

FDA and CISA advisories revealed hard-coded credentials and unsecured channels in popular patient monitors that integrate with ventilators, prompting urgent patch cycles and, in extreme cases, device recalls. A Class I recall of 4,100 Life2000 units underscored how even therapy devices with limited network features can compromise patient safety if exploited. New U.S. legislation now requires cybersecurity risk assessments as part of every 510(k) submission, increasing pre-market costs but ultimately strengthening ecosystem resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Critical-Care Leadership with Portable Acceleration

Intensive-care ventilators held 46.2% of the ventilators market in 2024, cementing their status as the backbone of high-acuity respiratory support. Procurement momentum is tied to hospital capacity expansion as emerging countries add ICU beds. Portable units, though smaller in revenue, are forecast to grow at an 8.7% CAGR, lifted by EMS modernization, military procurement, and home-transition protocols that require seamless intra-facility transport options. Devices such as the HAMILTON-T1 provide turbine-based ventilation that maintains tidal-volume accuracy in altitude and vibration conditions typical of rotor-wing evacuation. Neonatal-pediatric sub-segments benefit from policy drives to reduce infant mortality, prompting tertiary centers to install specialized modes like High-Frequency Oscillation for surfactant deficiency cases.

The ventilator market for portable models is projected to reach USD 1.42 billion by 2030 as compact designs incorporate closed-loop controls and multi-parameter monitoring, narrowing functional gaps with full ICU stations. Service-oriented revenue streams that bundle disposables and predictive-maintenance analytics help vendors secure recurring margins. Competitive intensity is rising as new entrants focus on rugged, low-maintenance designs to win defense and disaster-response tenders, further shaping the ventilators market landscape.

By Interface: Invasive Dominance Faces Non-Invasive Momentum

Invasive modes generated a 55.7% share of the ventilators market. They remain indispensable for acute respiratory distress syndrome, post-operative care, and traumatic injury. Non-invasive ventilation, however, is outpacing at a 9.3% CAGR, propelled by payer preference for lower-cost home management of COPD and obesity hypoventilation. Dedicated NIV platforms reduce asynchrony and improve patient comfort, while dual-capability systems like Philips V680 allow seamless switch-over when clinical status changes. High-flow nasal cannula adoption adds incrementa l volumes by delaying intubation in acute hypoxemic respiratory failure.

By 2030, non-invasive models are on track to command 41% of segment revenue as evidence builds for reduced readmissions and higher patient satisfaction. The ventilators market size for NIV devices is expected to record a 10.1% CAGR in Europe, where stringent infection-control rules encourage minimal airway invasion. Vendors differentiate with adaptive trigger sensitivities, advanced humidification systems, and tele-monitoring dashboards that alert clinicians to adherence issues.

By Mode: Volume-Control Stability Meets Adaptive Support Innovation

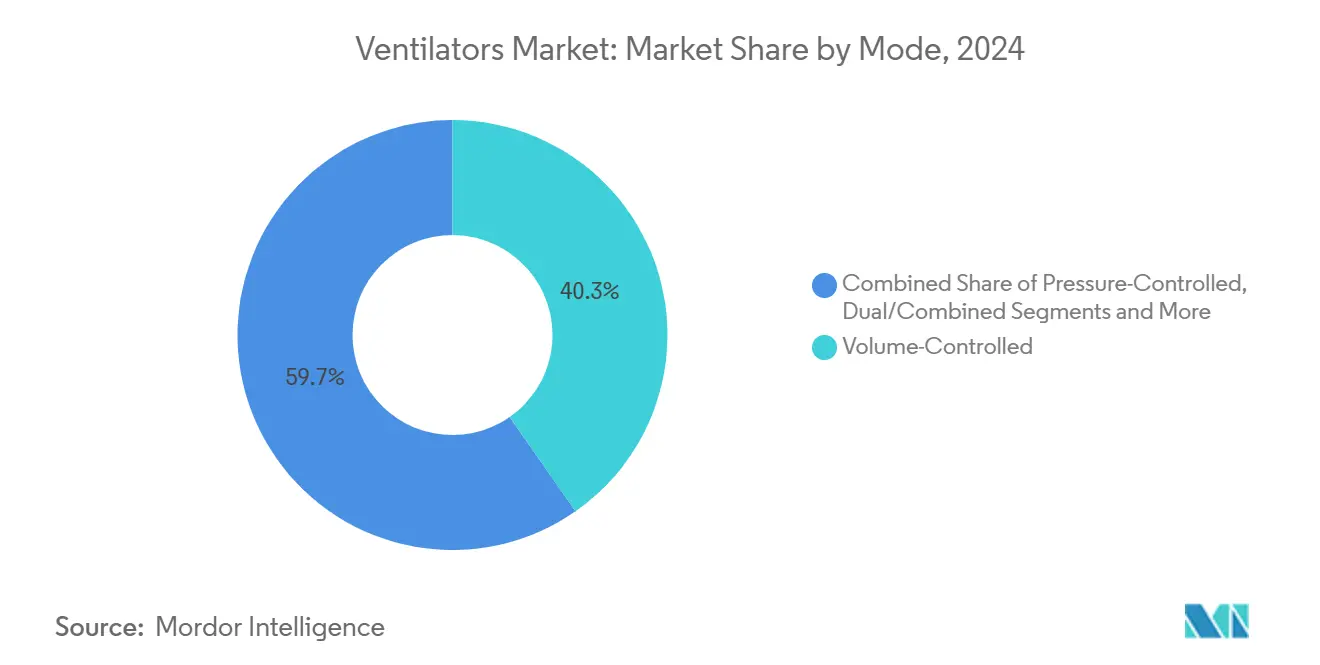

Volume-controlled ventilation held a 40.3% of the ventilators market share and remained the clinical default in 2024 because tidal-volume predictability simplifies protocols and facilitates comparative research. Pressure-controlled and dual modes supply flexibility for patients with variable compliance, while synchronized intermittent mandatory ventilation assists in systematic weaning. Proportional assist and other adaptive modes are slated for a 10.4% CAGR as artificial-intelligence layers allow algorithms to respond instantly to patient-specific effort, minimizing over-assist and diaphragmatic atrophy. Hamilton’s IntelliVent-ASV and Getinge’s Neural Pressure Support exemplify the move toward physiology-tuned assistance.

Clinical adoption accelerates when studies confirm shorter ventilation days and reduced staff workload, a benefit that aligns with persistent ICU nurse shortages. The ventilators market share for adaptive modes is projected to surpass 15% by 2030 as algorithm transparency and cybersecurity safeguards become mainstream selling points.

By End User: Hospital Core with Home-Care Upswing

Hospitals and clinics absorbed 63.8% of total shipments in 2024, reflecting large-scale procurement programs and new ICU wing openings in Asia and the Middle East. Yet, home-care environments are forecast for an 8.9% CAGR because value-based payment models prefer out-of-hospital management when clinically appropriate, adding momentum to the ventilator market. Long-term acute-care facilities fill the intermediate need for patients not yet ready for full discharge but no longer requiring full ICU oversight.

Ventilators industry participants now tailor education, supply-chain, and support services for non-professional caregivers. Subscription models such as Vent360+ combine rental, disposables, and clinician dashboards, lowering entry barriers for mid-sized home-medical-equipment providers. Veterans Affairs Canada’s reimbursement framework illustrates how national health systems can stimulate adoption by covering device and service costs for eligible patients.

Geography Analysis

North America generated 34.6% of the ventilators market share in 2024, with growth supported by resilient capital budgets, comprehensive reimbursement, and first-mover adoption of AI-enabled platforms. Federal regulatory updates on remanufacturing and cybersecurity shape purchasing criteria, pushing hospitals toward systems with secure firmware-over-the-air capabilities. Consolidation trends are evident as ZOLL absorbs Vyaire assets and Medtronic exits, opening whitespace for mid-tier innovators.

Asia-Pacific is projected for a 15.9% CAGR through 2030, underpinned by large-scale government investment. China’s bed-expansion mandate fuels multi-year tender pipelines stretching to county-level hospitals. India’s private network, with 4,000 planned beds and INR 11,500 crore capex, seeks versatile ventilators capable of invasive, non-invasive, and high-flow oxygen therapy modes to optimize return on capital. Getinge’s localized Servo-c launch illustrates vendor adaptation to price-sensitive, high-volume markets.

Europe remains a steady but less volatile market, with growth centered on energy-efficient upgrades that help facilities comply with Green Deal objectives. Dual-capability ventilators that minimize circuit breakage support infection-control protocols and now dominate replacement cycles. Middle East & Africa and South America post mid-single-digit growth, though fiscal constraints and currency volatility cause uneven tender schedules.

Competitive Landscape

Strategic realignment has increased concentration, yet multiple technology niches remain contested. ZOLL Medical’s USD 37 million acquisition of Vyaire ventilator lines delivered immediate scale in the portable and high-frequency oscillation categories. Conversely, Medtronic chose to divest its ventilator division, citing lower margin potential compared with monitoring and imaging assets, thereby reallocating R&D spend toward connected-care platforms.

Technology differentiation is now anchored in software rather than pure hardware. Hamilton Medical’s C6 integrates IntelliSync+ algorithms that track patient effort every five milliseconds, reducing asynchrony without clinician input. Getinge’s Neural Pressure Support synchronizes ventilation to diaphragmatic EMG signals, protecting lung tissue while preserving muscle strength. Fisher & Paykel leverages its humidification expertise to bundle NIV and high-flow therapy into home-care packages, improving adherence and comfort.

Service innovation rounds out competitive positioning. Subscription models lower customer capex hurdles and lock in multiyear consumables revenue. Vendors that backstop fleets with remote diagnostics and preventive maintenance win favor among overstretched biomedical engineering departments. Compliance with ISO 80601-2-12:2020 and forthcoming EU Artificial Intelligence Act provisions is emerging as a gate-to-market that advantages firms with robust regulatory teams.

Ventilators Industry Leaders

Medtronic plc

Koninklijke Philips N.V.

GE HealthCare

Drägerwerk

Hamilton Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The FDA issued a Class I recall for certain Medtronic ventilators after a reported patient death, intensifying competitive pressure just a year after the company announced plans to leave the segment.

- May 2025: Viemed Healthcare broadened its home-respiratory footprint by purchasing Lehan’s Medical Equipment for USD 26 million, adding new geographic coverage and a larger patient base for its ventilation services.

- February 2025: Movair secured FDA emergency-use authorization for Luisa, an 8-pound home ventilator that delivers hospital-grade performance in an ultra-portable form factor, expanding patient mobility options.

Global Ventilators Market Report Scope

| Intensive-Care Ventilators |

| Transport / Portable Ventilators |

| Neonatal / Pediatric Ventilators |

| High-Frequency Oscillatory Ventilators |

| Non-Invasive Ventilators |

| Invasive Ventilation |

| Non-Invasive Ventilation |

| Continuous Positive Airway Pressure (CPAP) |

| Bi-level Positive Airway Pressure (BiPAP) |

| High-Flow Nasal Cannula (HFNC) |

| Volume-Controlled Ventilation |

| Pressure-Controlled Ventilation |

| Dual / Combined Modes |

| Synchronized Intermittent Mandatory Ventilation (SIMV) |

| Proportional Assist / Adaptive Support Ventilation |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Emergency Medical Services (EMS) |

| Home-Care Settings |

| Long-Term Acute Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Intensive-Care Ventilators | |

| Transport / Portable Ventilators | ||

| Neonatal / Pediatric Ventilators | ||

| High-Frequency Oscillatory Ventilators | ||

| Non-Invasive Ventilators | ||

| By Interface | Invasive Ventilation | |

| Non-Invasive Ventilation | ||

| Continuous Positive Airway Pressure (CPAP) | ||

| Bi-level Positive Airway Pressure (BiPAP) | ||

| High-Flow Nasal Cannula (HFNC) | ||

| By Mode | Volume-Controlled Ventilation | |

| Pressure-Controlled Ventilation | ||

| Dual / Combined Modes | ||

| Synchronized Intermittent Mandatory Ventilation (SIMV) | ||

| Proportional Assist / Adaptive Support Ventilation | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Emergency Medical Services (EMS) | ||

| Home-Care Settings | ||

| Long-Term Acute Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the ventilators market by 2030?

The market is expected to reach USD 7.42 billion by 2030.

Which product category is growing fastest?

Portable ventilators are advancing at an 8.7% CAGR through 2030 as EMS fleets and home-care programs expand.

Why is non-invasive ventilation gaining popularity?

NIV lowers hospital readmissions, improves patient comfort, and aligns with payer incentives for home-based care.

How are semiconductor shortages affecting supply?

Lead times have lengthened by up to eight weeks, prompting manufacturers to adopt dual-sourcing and redesign strategies.

What role does artificial intelligence play in new ventilators?

AI-enabled closed-loop modes automatically adjust settings, reduce manual interventions, and support lung-protective strategies.

Which region offers the highest growth potential?

Asia-Pacific is forecast for a 15.9% CAGR thanks to large-scale ICU bed expansion and demographic shifts.

Page last updated on: