Neonatal Ventilators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

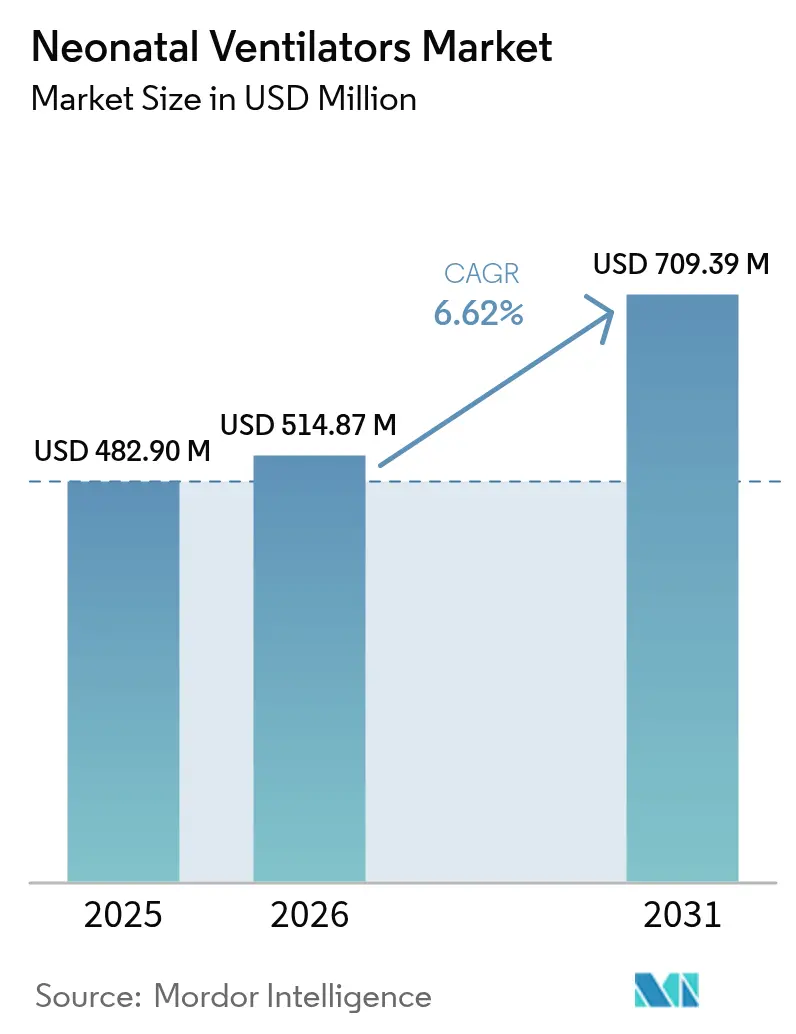

| Market Size (2026) | USD 514.87 Million |

| Market Size (2031) | USD 709.39 Million |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

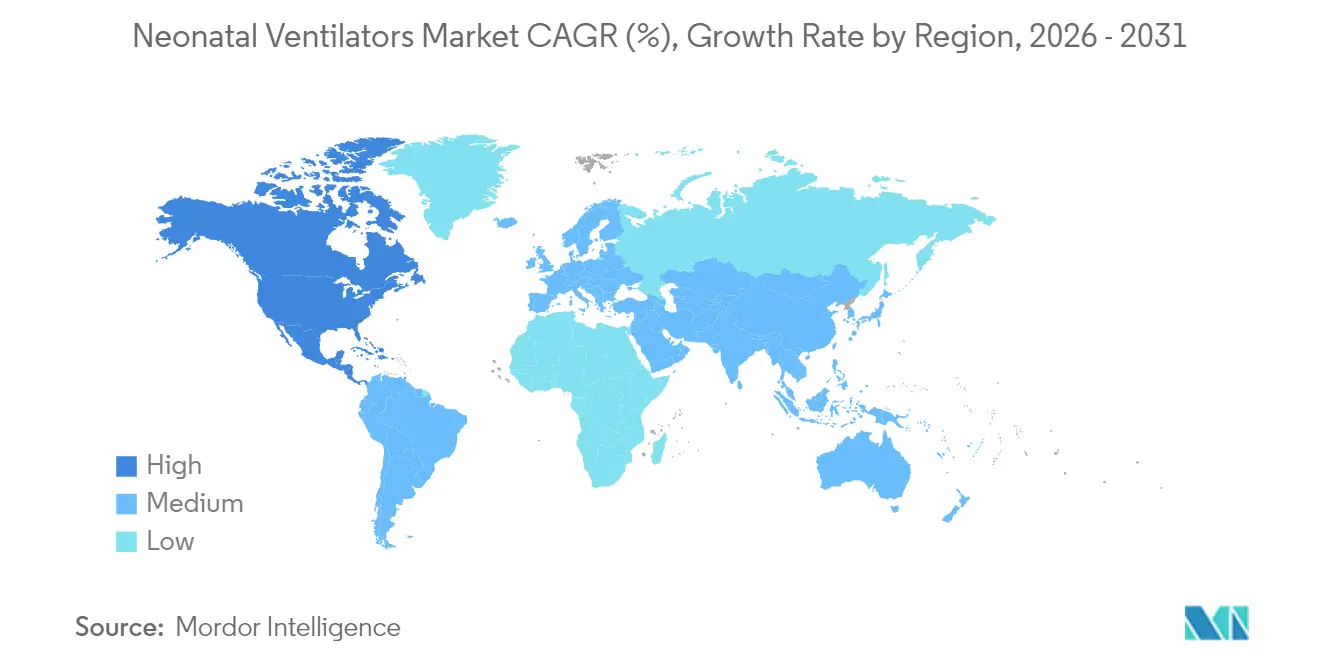

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neonatal Ventilators Market Analysis by Mordor Intelligence

The neonatal ventilators market size was valued at USD 482.90 million in 2025 and estimated to grow from USD 514.87 million in 2026 to reach USD 709.39 million by 2031, at a CAGR of 6.62% during the forecast period (2026-2031). Demand rises as prematurity rates climb, non-invasive ventilation technologies gain clinical endorsement, and public as well as private investments expand neonatal-intensive-care-unit (NICU) capacity across emerging economies. Clinical studies show early respiratory support lowers long-term complications, with non-invasive approaches cutting bronchopulmonary dysplasia incidence by up to 55% versus traditional invasive methods. Geographic momentum shifts toward Asia-Pacific, where government and donor-funded NICU upgrades accelerate infrastructure growth. Competitive dynamics favor companies integrating artificial-intelligence (AI)-driven closed-loop algorithms that adjust ventilation in real time, helping hospitals cope with shortages of specialized respiratory therapists. Meanwhile, persistent headwinds—high capital costs, complex reimbursement, and fragile component supply chains—continue to slow adoption in low-income setting.

Key Report Takeaways

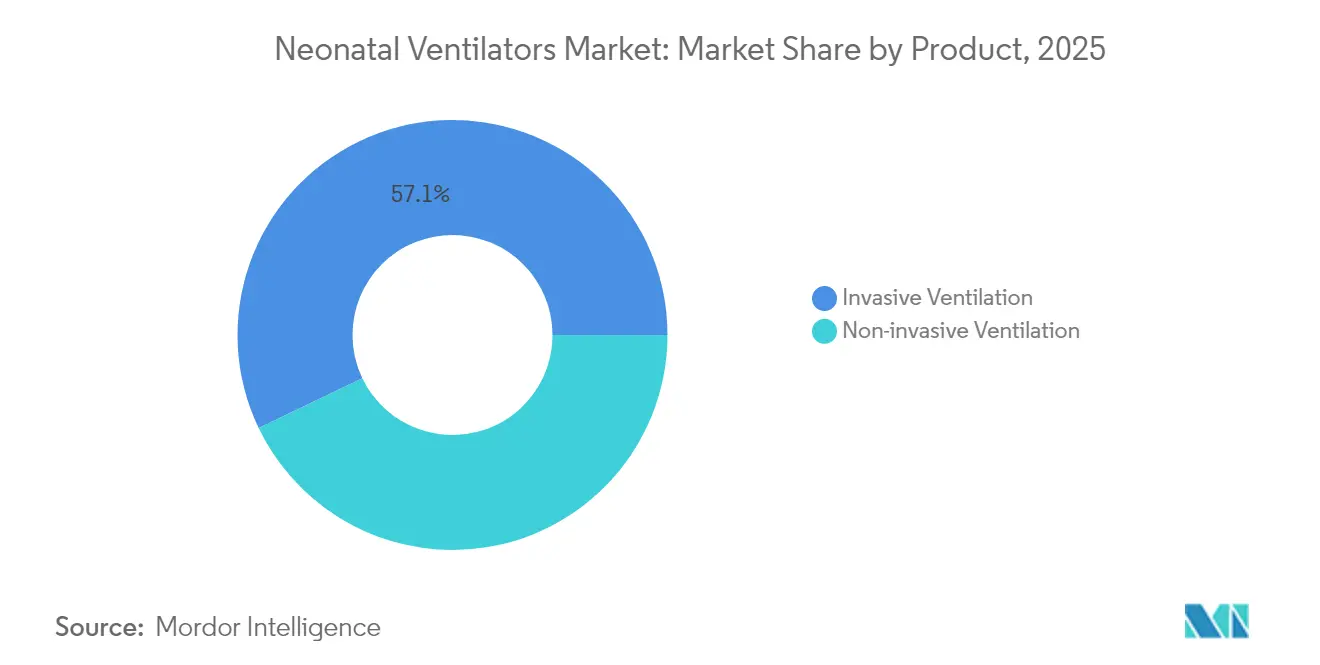

- By product, invasive ventilation led with 57.12% revenue share in 2025; non-invasive ventilation is forecast to expand at a 7.02% CAGR to 2031.

- By mobility, intensive-care ventilators held 60.98% of the neonatal ventilators market share in 2025, while portable/transport systems record the highest projected CAGR at 7.11% through 2031.

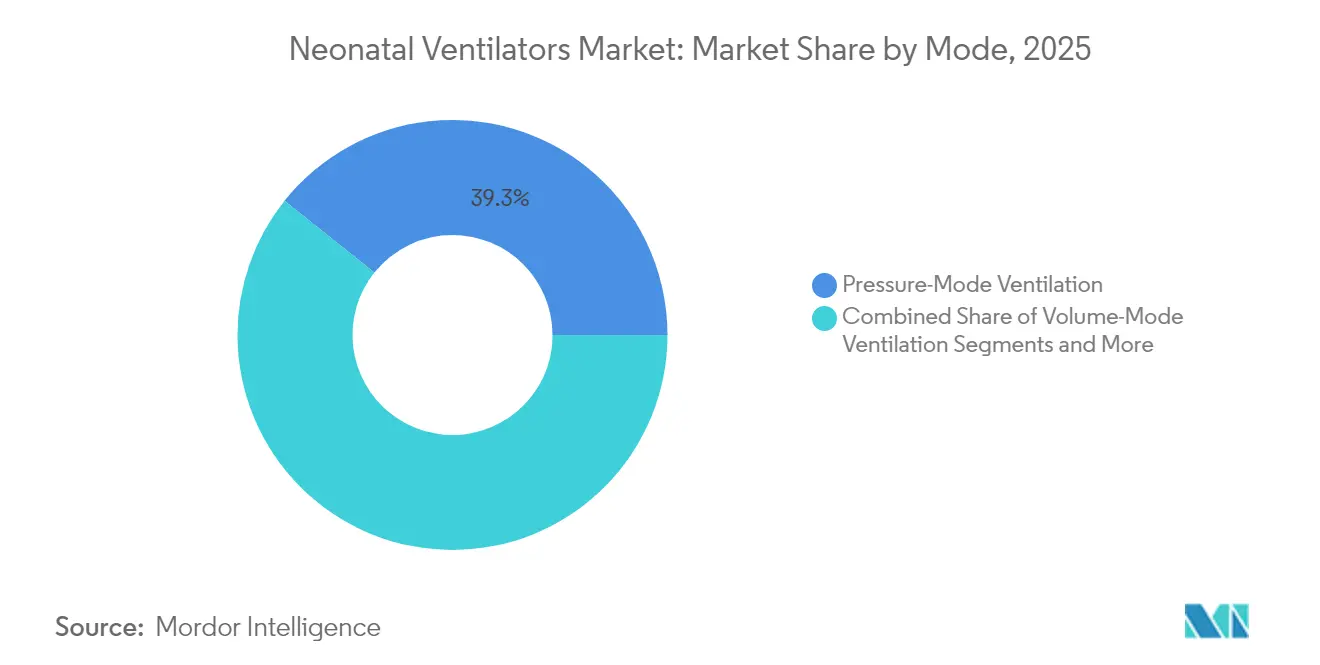

- By mode, pressure-mode ventilation accounted for a 39.27% share of the neonatal ventilators market size in 2025 and is advancing at a 4.69% CAGR; combined-mode solutions are rising at a 7.32% CAGR through 2031.

- By end user, hospitals captured 70.62% revenue share in 2025; ambulatory surgical centers represent the fastest growth trajectory at 7.06% CAGR to 2031.

- By geography, North America led with 41.02% share in 2025; Asia-Pacific is set to post an 7.72% CAGR and outpace all other regions by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neonatal Ventilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence Of Respiratory Distress Syndrome In Pre-Term Infants | +1.8% | Global, with highest impact in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Rising Pre-Term Birth Rate Globally | +1.5% | Global, concentrated in low-middle income countries | Long term (≥ 4 years) |

| Technological Shift Toward Non-Invasive & Hybrid Ventilators | +1.2% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Hospital Upgrades In NICUs Across Emerging Economies | +1.0% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| AI-Driven Closed-Loop Ventilation Algorithms Gaining Clinical Validation | +0.8% | North America & EU early adoption, global expansion | Short term (≤ 2 years) |

| Donor-Funded NICU Expansion In Sub-Saharan Africa | +0.5% | Sub-Saharan Africa, select low-income regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence Of Respiratory Distress Syndrome In Pre-Term Infants

RDS affects more than 80% of extremely pre-term neonates, maintaining structural demand for devices capable of delivering tidal volumes down to 2 ml while safeguarding fragile lung tissue. Mortality stands at 6.0% in RDS cases compared with 2.3% among non-RDS infants, pushing clinicians toward advanced modalities such as volume-guarantee ventilation and neurally adjusted ventilatory assist that synchronize support with native breathing. Evidence links early non-invasive strategies to lower disease progression, directing procurement budgets toward hybrid ventilators able to toggle seamlessly between invasive and non-invasive modes. This emphasis is keenly felt in units treating extremely-low-gestational-age neonates, a cohort whose survival has improved while RDS incidence persists. As a result, hospitals in both developed and emerging regions prioritize solutions that combine precise pressure control with algorithms mitigating ventilator-induced lung injury.

Rising Pre-Term Birth Rate Globally

Roughly 15 million pre-term births occur each year, expanding the candidate pool for respiratory support systems [1]World Health Organization, “COINN and NEST360 Partnership,” pmnch.who.int . Sub-Saharan Africa records 27 neonatal deaths per 1,000 live births, with pre-term complications dominating mortality profiles, while developed markets confront later maternal age as a risk multiplier. China’s CARE-Preterm cohort, spanning 60 NICUs and more than 10,000 infants, identified a 10.74% mortality rate accompanied by elevated bronchopulmonary dysplasia among survivors.

Technological Shift Toward Non-Invasive & Hybrid Ventilators

Clinical guidelines increasingly recommend early application of nasal continuous positive airway pressure (CPAP) and high-flow nasal cannula therapy to minimize lung injury. Devices such as Hamilton Medical’s C1 neo merge invasive, CPAP, and high-flow functions within a single chassis, cutting device inventory and easing staff training requirements. Vyaire Medical’s fabian Therapy evolution introduces Predictive Intelligent Control of Oxygenation, an AI module that automatically adjusts FiO2, shrinking clinician workload and stabilizing saturation ranges. Such convergence dovetails with workforce shortages, since AI support allows general-care staff to deliver sophisticated ventilation when specialists are not available.

AI-Driven Closed-Loop Ventilation Algorithms Gaining Clinical Validation

Closed-loop systems like SOLVe demonstrate more than 75% time within target oxygenation levels while autonomously titrating PEEP. Randomized trials confirm that automated oxygen controllers out-perform manual titration, reducing hyperoxemia episodes and enabling tighter saturation control[2]Anesthesia & Analgesia, “Applying Computer Models to Realize Closed-Loop Neonatal Oxygen Therapy,” journals.lww.com . Regulatory momentum helps: the FDA’s De Novo pathway accepted 374 AI-enabled device requests by August 2023, streamlining approvals. Hospitals deploy these platforms to offset therapist shortages, standardize ventilatory care, and gather high-resolution data sets for future predictive analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Cost Of Neonatal Ventilators | -1.5% | Global, most severe in low-middle income countries | Long term (≥ 4 years) |

| Reimbursement Gaps For NICU Respiratory Care In Low-Income Markets | -1.2% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Shortage Of Trained Neonatal-Intensive Respiratory Therapists | -0.8% | Global, acute in rural and emerging markets | Medium term (2-4 years) |

| Fragile Supply Chain For Critical Sensors & Valves | -0.6% | Global, concentrated impact during disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost Of Neonatal Ventilators

Top-tier neonatal ventilators exceed USD 50,000 per unit; annual service contracts can equal 15-20% of list price, straining facilities that operate on limited capital budgets. Medicare’s rental-payment model aggregates maintenance into monthly reimbursements, but complex documentation requirements heighten administrative burden. Emerging-market purchasers face steeper financing hurdles because donor grants often prioritize consumables or training over equipment procurement. Supply chain shocks compound cost risks: medical-device manufacturers report that logistics expenses reached 20% of revenue in 2024 amid geopolitical disruptions.

Shortage Of Trained Neonatal-Intensive Respiratory Therapists

The World Health Organization warns of a 1.3 million-person shortfall in maternal and newborn caregivers by 2030, with neonatal respiratory expertise ranking among the scarcest competencies. Workforce imbalances skew toward urban centers: 65% of Saudi Arabia’s therapists are clustered in two provinces, leaving rural NICUs under-resourced. In the United States, projected respiratory-therapist job growth of 13% over the 2022-2032 period illustrates demand outstripping training pipelines. Programlen gestation periods of 18-24 months prolong the supply gap, making automation and standardized clinical protocols critical stop-gaps in both developed and emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Non-Invasive Solutions Drive Innovation

The neonatal ventilators market size attributed to invasive ventilation remained dominant at USD 275.83 million in 2025, equal to 57.12% share. Yet the non-invasive category is accelerating at 7.02% CAGR, reflecting clinician emphasis on lung-protective strategies and heightened awareness of ventilation-induced lung injury. Integrated platforms blending invasive and non-invasive modes allow rapid modality shifts without exchanging equipment, enhancing workflow efficiency. Evidence supporting early CPAP shows that intubation can be avoided in 40% of pre-term infants presenting with mild RDS, extending the addressable pool for hybrid devices.

Growth prospects favor systems capable of advanced modalities such as high-frequency oscillatory ventilation (HFOV) for severe respiratory pathology. Vyaire Medical’s 3100A/B series demonstrates shorter oxygen-therapy duration and lower chronic lung-disease rates, reinforcing invasive ventilation’s clinical necessity. Non-invasive leaders invest in precision flow control, soft-seal patient interfaces, and AI algorithms that pre-empt desaturation events. As payer policies evolve toward value-based care, the neonatal ventilators market will see reimbursement linkage to outcomes, incentivizing hospitals to shift case mixes toward non-invasive care where clinically appropriate.

By Mobility: Transport Ventilators Capture Growth

Hospital-stationary intensive-care ventilators commanded USD 294.47 million in 2025, equating to 60.98% share of the neonatal ventilators market. These systems integrate servo-control loops, broad mode libraries, and multi-parameter monitoring suited to complex NICU cases. Portable and transport ventilators, valued at USD 121.3 million in 2025, are advancing at 7.11% CAGR thanks to regionalized perinatal networks that require safe, high-acuity transfers. Design priorities include weight reduction, longer battery life, and compliance with ISO 80601-2-87 performance standards for high-frequency devices.

Product roadmaps emphasize shared user interfaces across stationary and transport models to streamline training. The neonatal ventilators market also contains a small “others” mobility segment comprising specialized tabletop or cart-mounted systems targeting narrow use cases, such as intra-operative support during neonatal surgery. While volume remains modest, this niche offers premium pricing potential for manufacturers able to address unique clinical challenges without sacrificing portability.

By Mode: Combined-Mode Innovation Accelerates

Pressure-controlled ventilation retained 39.27% share in 2025 based on clinician familiarity and efficacy in broad NICU populations. Combined-mode systems that dynamically switch between pressure and volume targets are the fastest-growing at 7.32% CAGR, reflecting demand for devices that adjust to evolving compliance and resistance during treatment. Neurally adjusted ventilatory assist (NAVA) epitomizes this flexibility, synchronizing delivered pressure to the infant’s diaphragmatic electrical activity and reducing asynchrony episodes.

Volume-mode ventilation retains strategic importance for neonates with heterogeneous lung injury where low tidal volumes must be tightly controlled. The neonatal ventilators market share for other modes—high-frequency jet ventilation, liquid ventilation—remains single-digit but climbs steadily as evidence accrues and device reliability improves. Manufacturers increasingly embed cross-mode decision-support algorithms, allowing clinicians to tailor therapies without restarting ventilators, minimizing interruption risks.

By End User: ASCs Emerge as Growth Driver

Hospitals possessed 70.62% of neonatal ventilators market share in 2025, buoyed by their role as central hubs for high-acuity deliveries and complex neonatal surgery. Procurement cycles favor multi-functional platforms that interoperate with existing patient-monitoring systems. Ambulatory surgical centers (ASCs), although smaller in absolute volume, climb at 7.06% CAGR through 2031 as outpatient procedures expand and reimbursement models reward lower-cost settings.

Technological advances in compact ventilator design and integrated safety features encourage ASC adoption. Meanwhile, long-term and home-care segments remain nascent but promising, underpinned by miniaturization trends and payer initiatives aiming to reduce hospital readmissions. The neonatal ventilators industry thus distributes revenue across a progressively diversified provider landscape, balancing hospital dominance with emerging outpatient and home-based applications.

Geography Analysis

North America held 41.02% of global revenue in 2025, supported by sophisticated NICU networks, robust reimbursement, and an active regulatory environment that sustains clinician confidence. Despite a 227% rise in neonatologists and a 48% expansion in NICU beds over three decades, mortality reductions have plateaued, focusing market attention on care quality improvements rather than bed count growth. Software-related ventilator recalls—and associated downtime—underscore supply-chain and post-market-surveillance importance.

Asia-Pacific is the fastest-growing region, expected to post an 7.72% CAGR through 2031 as governments expand neonatal programs, multinational companies localize manufacturing, and donor initiatives fund equipment purchases. China spearheads regional demand with multicenter programs that have improved pre-term survival metrics, while India attracts foreign investment targeting hospital-technology market share gains.

Europe presents a stable, innovation-oriented market. Universal coverage eases device adoption, and regulatory changes demand rigorous clinical evidence, promoting high-quality competition. Patent filings highlight intense R&D focus: Philips submitted 594 medical-technology applications in 2024 and invested EUR 1.7 billion in research, much directed to AI-powered neonatal care solutions.

Middle East & Africa and South America represent emerging frontiers. Projects like NEST360 channel USD 65 million into neonatal care across Sub-Saharan Africa, promising to lift equipment demand as clinical capacity builds. Regulatory harmonization and workforce development remain prerequisites for sustained uptake, but donor backing and government focus on infant-mortality reduction underpin a solid long-range outlook.

Competitive Landscape

The neonatal ventilators market shows moderate fragmentation, with global conglomerates contending alongside respiratory-care specialists and AI startups. Barriers include high R&D expense, multi-year regulatory approval cycles, and compulsory clinical evidence to meet stringent safety benchmarks. Top-tier firms leverage scale advantages to secure long-term supply contracts, integrate service offerings, and maintain global distribution.

Product differentiation centers on closed-loop control, miniaturization, and interoperability with hospital information systems. Philips’ EUR 1.7 billion annual R&D outlay underscores the innovation intensity necessary for competitive leadership. M&A activity reshapes segment boundaries; ZOLL Medical’s acquisition of select Vyaire Medical ventilator lines expands its neonatal footprint while enabling asset divestiture for Vyaire amid Chapter 11 proceedings.

Competitive strategies increasingly emphasize emerging-market penetration through localized manufacturing and pay-per-use financing models that mitigate capital constraints. AI-first disruptors target predictive analytics and real-time decision support, carving niches in hospitals seeking to offset therapist shortages. Manufacturers with robust after-sales service networks and remote monitoring capabilities hold structural advantage as hospitals prioritize uptime and outcome-linked procurement.

Neonatal Ventilators Industry Leaders

Medtronic

Drägerwerk AG & Co. KGaA

Hamilton Medical

ICU Medical

Vyaire

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Getinge extended its Servo-c ventilator with a neonatal option, creating a universal platform spanning premature newborns through adults.

- October 2024: Dräger India introduced the BabyRoo TN 300 open warmer featuring AutoBreath, which automatically maintains preset ventilation parameters, supporting emergency neonatal resuscitation.

- November 2023: Inspiration Healthcare Group launched the SLE1500 compact ventilator, providing non-invasive modes tailored for extremely small infants.

Global Neonatal Ventilators Market Report Scope

As per the scope, neonatal ventilators are artificial ventilation-supporting devices developed for their use on neonates. These ventilators are designed to offer artificial gas support to neonates in the form of gas delivery and gas extraction of oxygen and carbon dioxide, respectively. The Neonatal Ventilators Market is Segmented by Product (Invasive Ventilation and Non-invasive Ventilation), Mobility (Intensive Care Ventilators, Portable/Transportable Ventilators, and Others), Mode (Pressure Mode Ventilation, Combined Mode Ventilation, Volume Mode Ventilation, and Other Modes), End User (Hospitals, Ambulatory Surgery Centers, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Invasive Ventilation |

| Non-invasive Ventilation |

| Intensive-Care Ventilators |

| Portable / Transport Ventilators |

| Others |

| Pressure-Mode Ventilation |

| Volume-Mode Ventilation |

| Combined-Mode Ventilation |

| Other Modes |

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Invasive Ventilation | |

| Non-invasive Ventilation | ||

| By Mobility | Intensive-Care Ventilators | |

| Portable / Transport Ventilators | ||

| Others | ||

| By Mode | Pressure-Mode Ventilation | |

| Volume-Mode Ventilation | ||

| Combined-Mode Ventilation | ||

| Other Modes | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Neonatal Ventilators Market?

The Neonatal Ventilators Market size is expected to reach USD 514.87 million in 2026 and grow at a CAGR of 6.62% to reach USD 709.39 million by 2031.

Which product category is expanding the fastest?

Non-invasive ventilation is registering a 7.02% CAGR because of its ability to reduce bronchopulmonary dysplasia and minimize lung injury.

Who are the key players in Neonatal Ventilators Market?

Medtronic, Drägerwerk AG & Co. KGaA, Hamilton Medical, ICU Medical and Vyaire are the major companies operating in the Neonatal Ventilators Market.

Why is Asia-Pacific attracting the most attention from manufacturers?

The region shows the highest projected CAGR at 7.72% due to rapid NICU infrastructure expansion, supportive government funding, and large pre-term birth volumes.

Which region has the biggest share in Neonatal Ventilators Market?

In 2025, the North America accounts for the largest market share in Neonatal Ventilators Market.

Page last updated on: