Breathing Circuits Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

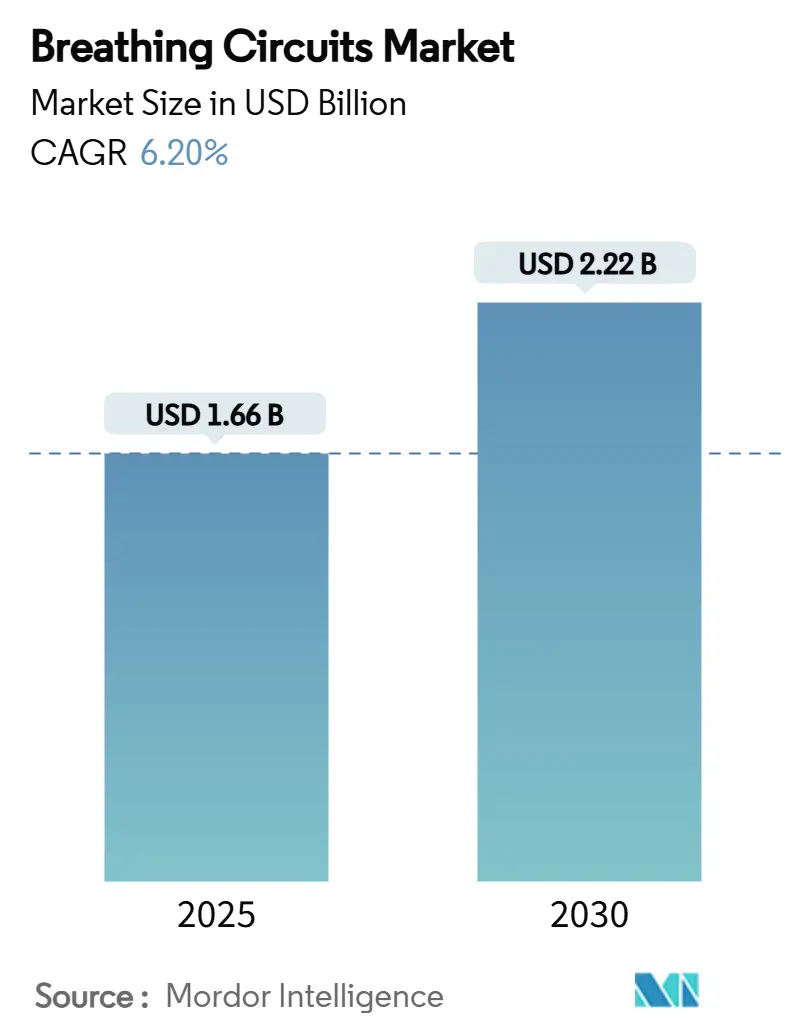

| Market Size (2025) | USD 1.66 Billion |

| Market Size (2030) | USD 2.22 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

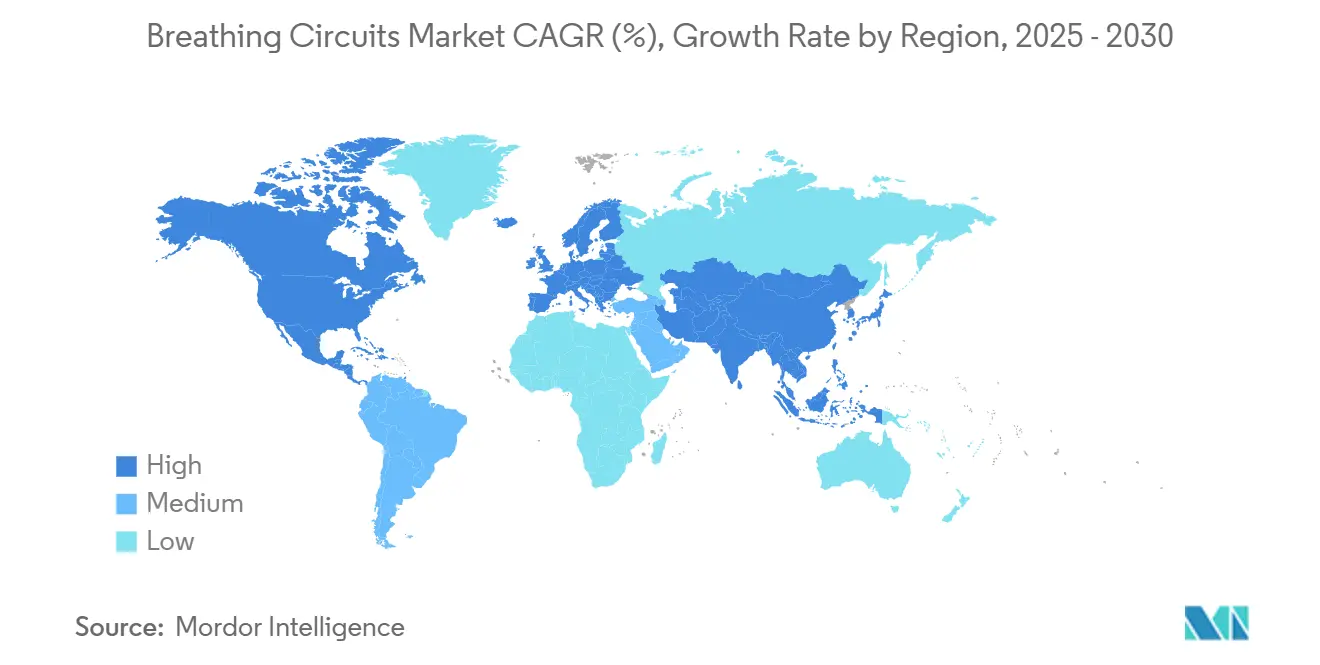

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breathing Circuits Market Analysis by Mordor Intelligence

The breathing circuits market size stood at USD 1.66 billion in 2025 and is projected to reach USD 2.22 billion by 2030, reflecting a 6.20% CAGR over the forecast period. Rising post-pandemic surgical volumes, ICU capacity build-outs in Asia Pacific and the Gulf, and steady technological upgrades in circuit design together reinforce the growth trajectory of the breathing circuits market. Hospitals continued to account for most unit volumes, but portable devices for home use are expanding rapidly, while sustainability mandates are pulling buyers toward closed, low-flow systems. Manufacturers face margin pressure from volatile silicone and PVC prices, yet supply-chain risk is also fueling regionalized production and strategic sourcing programs. Competitive differentiation increasingly centers on heated-wire technology, sensor-enabled “smart” circuits, and low-carbon materials that satisfy tightening regulatory expectations in Europe and North America.

Key Report Takeaways

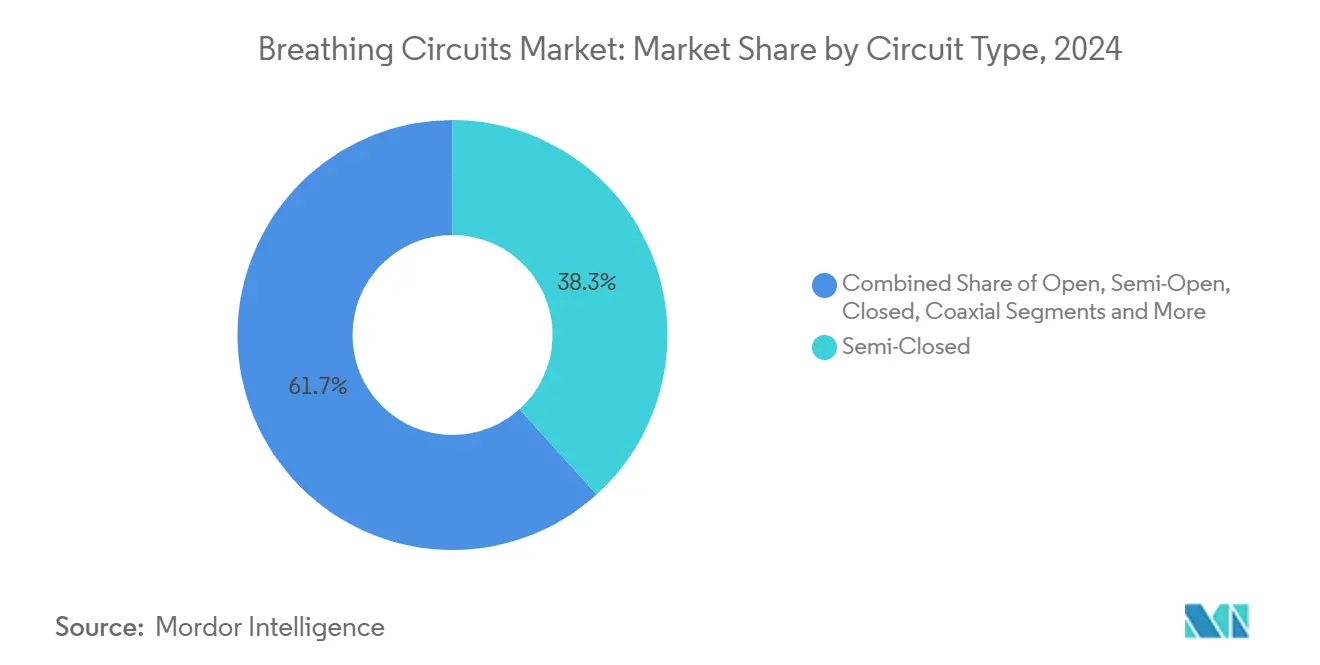

- By circuit type, semi-closed circuits led with 38.3% of breathing circuits market share in 2024; closed circuits are projected to expand at a 7.8% CAGR through 2030.

- By usability, disposable systems accounted for 64.2% share of the breathing circuits market size in 2024, while reusable systems are advancing at a 6.4% CAGR through 2030.

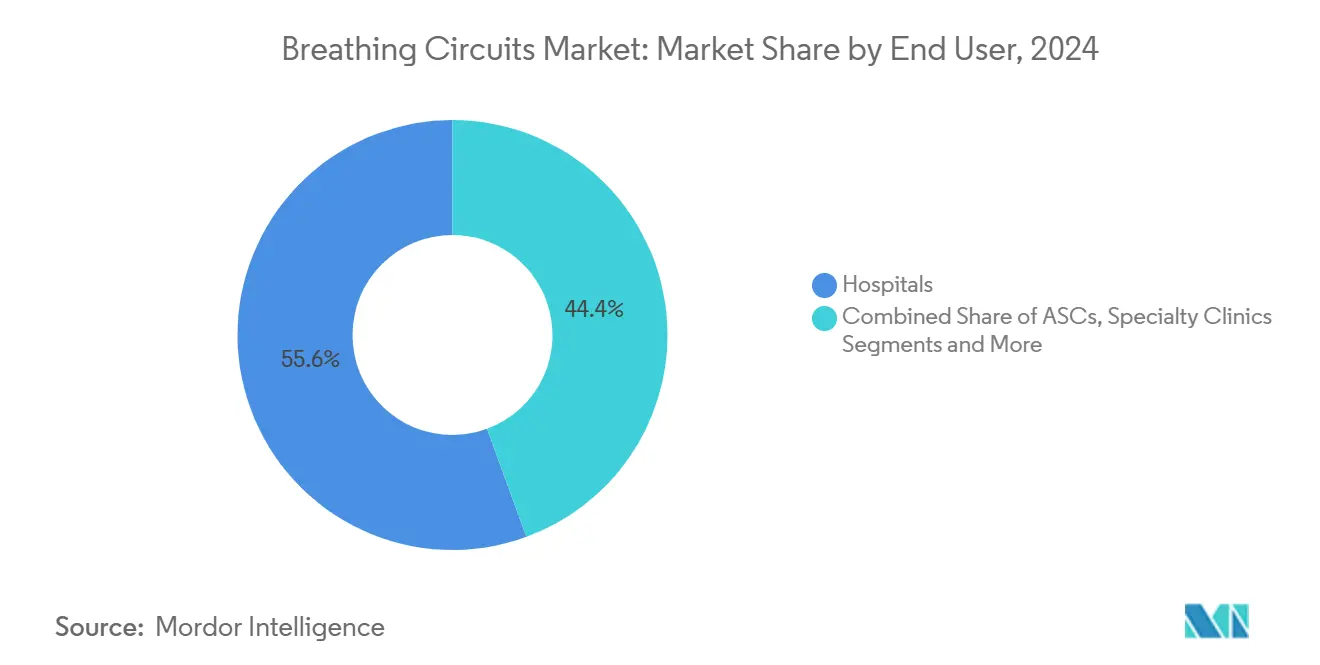

- By end user, hospitals held 55.6% of volumes in 2024; homecare settings are forecast to register an 8.3% CAGR to 2030.

- By geography, North America led with 34% of market share in 2024, while Asia Pacific is forecast to register a 7.3% CAGR between 2025 and 2030.

Global Breathing Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Elective-Surgery Backlog Post-COVID-19 Boosts Demand For Breathing Circuits | +1.20% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Accelerating ICU Bed Expansions In Asia & GCC Private Hospitals | +0.90% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Adoption Of Heated-Wire Circuits To Curb Ventilator-Associated Pneumonia (VAP) | +0.80% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Sustainability Mandates Driving Shift To Low-Flow, Closed-Loop Circuits | +0.60% | Europe & North America leading, expanding globally | Long term (≥ 4 years) |

| AI-Enabled "Smart Circuits" Integrating Flow-Sensor Telemetry | +0.40% | North America & Europe, gradual APAC adoption | Long term (≥ 4 years) |

| Space-Flight-Proven Mini-Circuits Entering Neonatal Transport Market | +0.20% | Global, specialized applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Elective-Surgery Backlog Post-COVID-19 Boosts Demand for Breathing Circuits

Elective procedures postponed during the pandemic exceeded 28 million cases worldwide, and the clearing of this backlog keeps operating rooms at sustained high utilization.[1]Priya Venkatesan, “The UK COVID-19 Inquiry and Critical Care,” Lancet Respiratory Medicine, thelancet.com Health systems expanded critical-care beds in 2020 and have retained much of that added capacity, so the breathing circuits market benefits from elevated baseline demand. Anesthesia teams standardize semi-closed circuits to conserve fresh gas flow during heavy caseloads, thereby reducing per-case cost while ensuring safety. Manufacturers offering bundled kits with integrated filters, manifolds, and connectors help hospitals streamline setup times. As surgical volumes normalize, procurement managers are negotiating multi-year framework agreements, locking in hybrid disposable-reusable mixes that balance infection-control and sustainability goals.

Accelerating ICU Bed Expansions in Asia & GCC Private Hospitals

China and India are adding ventilator capacity as part of broader critical-care upgrades, while well-capitalized private hospitals in the Gulf Cooperative Council (GCC) region respond to universal insurance coverage by scaling ICU footprints.[2]Ayesha T. Jalal et al., “Health Workforce Capacity of Intensive Care Units in the Eastern Mediterranean Region,” PLoS ONE, journals.plos.org Ventilator-ready beds require a steady flow of disposable circuits, yet multi-patient reusable sets are gaining share as sterile-processing capabilities mature. Premium demand concentrates in urban quaternary centers that specify heated-wire circuits for humidity control. Global suppliers are partnering with regional distributors to navigate diverse device-registration pathways and to localize inventory buffers that mitigate shipping delays.

Adoption of Heated-Wire Circuits to Curb Ventilator-Associated Pneumonia (VAP)

VAP incidence runs from 1.4 to 7.0 episodes per 1,000 ventilator days in high-income countries and even higher in low-resource settings.[3]Rangelova Vanya et al., “Ventilator-Associated Pneumonia in the Neonatal Intensive Care Unit—Incidence and Strategies for Prevention,” Diagnostics, mdpi.com Heated-wire technology maintains inhaled gas at near-physiological humidity (≈ 90%) and temperature (≈ 36 °C), markedly reducing condensate that can seed pathogens. Pediatric and neonatal ICUs have been early adopters, and adult ICUs are following bundled infection-prevention protocols, linking device choice to quality metrics. Although list prices for heated-wire sets are higher, outcome studies showing shorter ventilation days help justify procurement. Vendors integrate temperature sensors and closed-loop controllers that alert clinicians to moisture imbalance, supporting premium positioning in the breathing circuits market.

Sustainability Mandates Driving Shift to Low-Flow, Closed-Loop Circuits

Healthcare contributes roughly 4-5% of global greenhouse-gas emissions, and anesthetic gases such as sevoflurane possess high global warming potential. European hospitals now track scope-3 emissions within purchasing criteria, elevating closed systems that can cut volatile agent use by up to 90%. Modern computer-controlled loops stabilize end-tidal concentrations with minimal fresh gas flow, so operating-room managers cite both cost savings and sustainability benefits. Environmental product declarations (EPDs) are becoming mandatory in tender documents, advantaging suppliers that provide cradle-to-grave carbon data. Similar policies are emerging in Canada and several U.S. states, signaling global diffusion of low-flow practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Silicone & PVC Raw-Material Prices Compress Margins | -0.70% | Global, particularly affecting cost-sensitive markets | Short term (≤ 2 years) |

| Stringent Single-Use Plastic Bans In EU Operating Rooms | -0.40% | Europe leading, expanding to other developed markets | Medium term (2-4 years) |

| Sterile-Processing Bottlenecks Limiting Reusable-Circuit Uptake | -0.30% | Global, more pronounced in resource-constrained facilities | Medium term (2-4 years) |

| Supply-Chain Fragility For Medical-Grade CO₂ Absorbers | -0.20% | Global, with acute impact in specialized applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone & PVC Raw-Material Prices Compress Margins

Average silicone prices swung more than 20% between 2023 and 2024, driven by energy-cost spikes and geopolitical disruptions that curtailed resin production. Circuit makers now earmark up to one-fifth of revenue for supply-chain overhead, eroding price competitiveness. Contract manufacturers are expanding direct-purchase agreements and dual-sourcing molds to lower exposure. Small firms lacking scale face disproportionate cost shocks, nudging them toward mergers or OEM alliances, thus gradually increasing concentration within the breathing circuits market.

Stringent Single-Use Plastic Bans in EU Operating Rooms

Directive (EU) 2019/904 compels hospitals to reduce disposable plastics, funneling purchasing committees toward reusable or recyclable alternatives. The Packaging & Packaging Waste Regulation demands fully recyclable packaging by 2030, though healthcare exemptions remain under review. Transitioning to reusables requires capital outlays for washers, tracking software, and staff retraining, which slows adoption. Nevertheless, early-compliant suppliers gain access preference, while laggards incur redesign costs or risk being delisted in EU tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Circuit Type: Closed Systems Drive Sustainability Gains

Closed systems, while still smaller in volume, logged the fastest growth at 7.8% CAGR and captured 90% less volatile anesthetics per case than open setups. Semi-closed systems held 38.3% of the breathing circuits market share in 2024 on familiarity and safety buffers. Enhanced microprocessor controls now allow closed loops to auto-adjust fresh-gas flow and end-tidal concentration, reducing clinician workload and unlocking further adoption. Coaxial and open circuits remain staples for emergency airway management where simplicity outweighs efficiency, yet incremental refinements such as kink-resistant tubing extend their life cycle. Manufacturers highlight carbon-footprint data and anesthetic-agent savings during value analysis committee reviews, anchoring closed circuits firmly on hospital decarbonization road maps.

Broader market dynamics suggest continued dual-track demand. Cost-sensitive centers standardize semi-closed sets for routine cases, whereas tertiary hospitals pivot toward closed systems to meet net-zero targets. Training modules embedded in anesthesia-information software demystify loop management, shrinking the learning curve. Together, these factors preserve diversity within the breathing circuits market, even as environmental considerations steer growth toward closed systems.

By Usability: Reusables Gain Ground Despite Disposable Dominance

Disposable sets retained 64.2% of the breathing circuits market size in 2024, thanks to turnkey infection-control workflows. Yet reusable sets are climbing at 6.4% CAGR, driven by lifecycle-cost models that assign financial value to reduced plastic waste. Durable silicone formulations now withstand over 80 autoclave cycles without loss of compliance, lowering the cost per use. Hospitals employ RFID tagging to track cycle counts and verify decontamination, addressing historical safety concerns. Hybrid single-patient-use kits, combining disposable limbs with reusable connectors, offer a stepping-stone strategy for centers lacking full reprocessing infrastructure.

Purchasing committees factor in regulatory pushback on single-use plastics and negotiate bundled pricing that amortizes sterilization equipment over long-term contracts. Heated-wire functionality commands premium pricing in both disposable and reusable lines, reflecting its association with VAP reduction. As sustainability reporting becomes mandatory, reusable penetration is likely to accelerate, albeit from a lower base.

By End User: Homecare Emergence Reshapes Market Dynamics

Hospitals accounted for 55.6% of the breathing circuits market size in 2024, underpinned by high surgical throughput and established ICU infrastructure. Ambulatory surgery centers (ASCs) are gaining relevance because payer incentives favor outpatient procedures, and their volumes are set to expand 21% by 2034. The fastest growth, however, lies in home respiratory support. Tele-enabled portable ventilators and oxygen concentrators require lightweight, kink-proof circuits tailored for unsupervised handling. Device makers integrate ergonomic connectors and disposable bacterial filters to simplify patient use. Insurers reimburse remote-monitoring add-ons that flag circuit occlusion or leak, enhancing adherence.

Specialty clinics for sleep apnea and chronic obstructive pulmonary disease represent a further niche, often preferring single-patient-use sets to minimize cross-contamination. Manufacturers that design user-friendly, color-coded packaging and provide instructional videos gain loyalty in the consumer channel, carving new terrain within the breathing circuits market.

Geography Analysis

North America remains the most significant regional block for the breathing circuits market, buoyed by robust procedural volumes and early adoption of sensor-enabled devices. The region’s supply-chain resilience initiatives encourage local contract-manufacturing clusters, cushioning raw-material shocks. U.S. hospital consolidations translate into multi-state group purchasing agreements, providing large, predictable tenders for top vendors. Federal alignment with ISO 13485 from 2026 will streamline new-device approvals and foster incremental innovation.

Sustainability mandates and harmonized medical-device regulations shape Europe’s breathing circuits market. Procurement frameworks increasingly award eco-credits for closed-loop systems with validated low-flow performance. Hospitals in Germany, France, and the Nordics have piloted volatile-gas capture systems that feed anesthetic recycling programs, creating complementary demand for compatible circuits. Brexit-related dual-registration rules raise administrative burden, but pan-European distributors buffer inventory to maintain smooth supply.

Asia Pacific registers the swiftest CAGR as demographic shifts, urbanization, and medical-tourism corridors spur critical-care expansion. China quadrupled ICU beds between 2019 and 2024, and India’s government incentives for domestic ventilator assembly stimulate aligned consumption of disposable circuits. Japanese hospitals emphasize smart-sensor integration, dovetailing with the country’s digital-health blueprint. In the GCC, high private-sector capital expenditure scales ventilator fleets in large tertiary centers, feeding premium heated-wire uptake. Varied regulatory pathways—from Australia’s TGA to India’s CDSCO—require vendors to adopt staggered rollout plans, but the sheer patient volume anchors Asia Pacific as a primary growth engine for the breathing circuits market.

Competitive Landscape

The breathing circuits market exhibits moderate concentration: the top five brands collectively command slightly above 40% of global revenue. Medtronic, Drägerwerk, and Fisher & Paykel Healthcare leverage integrated product portfolios that bundle circuits with anesthesia workstations and humidifiers. Patents around humidification chambers and temperature-control algorithms reinforce differentiation. Heated-wire circuits remain the most defensible niche, where proprietary micro-heating elements and embedded sensors create high switching costs.

Mid-tier manufacturers often anchor growth on regional strengths, such as strong distributor networks in Latin America or specialized neonatal lines in Europe. Strategic partnerships—illustrated by recent OEM deals to co-develop reusable kits—align smaller firms with the sustainability agenda while expanding scale. Supply-chain turbulence propels vertical integration: Several players now mold tubing in-house to secure resin supplies and lock in margins.

M&A activity maintains tempo. A headline 2024 deal saw a respiratory-care leader divest its ventilation unit to focus on high-growth consumables, while a 2025 acquisition in interventional cardiology signaled broader diversification among large medtech groups. Across all tiers, investment in AI-ready telemetry and cloud connectivity stands out as the unifying theme, positioning vendors to ride the long-term digitalization wave sweeping the breathing circuits market.

Breathing Circuits Industry Leaders

Drägerwerk AG & Co. KGaA

Medtronic plc

Fisher & Paykel Healthcare

Philips Healthcare

Hamilton Medical AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex Incorporated announced the acquisition of BIOTRONIK's Vascular Intervention business for approximately EUR 760 million (USD 820 million), enhancing its interventional portfolio and expanding capabilities in the estimated USD 10 billion interventional cardiology market, demonstrating strategic focus on high-growth medical device segments.

- October 2024: Vyaire Medical completed the sale of its Ventilation Business Unit to ZOLL Medical Corporation, transferring key product lines including bellavista, fabian, and LTV ventilators along with associated consumables and service offerings. This represents significant market consolidation in respiratory care equipment.

- September 2024: Medtronic launched the VitalFlow ECMO system, designed to enhance critically ill patient management requiring respiratory support, built on a proven Nautilus ECMO oxygenator design with a user-friendly interface, addressing clinicians' needs for simplicity and performance in extracorporeal membrane oxygenation.

- July 2024: Beyond Air received CE Mark approval for the LungFit PH system, the first device to generate nitric oxide (NO) for treating hypoxic respiratory failure and pulmonary hypertension. The system uses patented Ionizer technology to produce NO from ambient air and deliver it through ventilator circuits.

Global Breathing Circuits Market Report Scope

| Open Circuits |

| Semi-Open Circuits |

| Semi-Closed Circuits |

| Closed Circuits |

| Coaxial Circuits |

| Disposable Circuits |

| Reusable Circuits |

| Single-Patient-Use Kits |

| Heated-Wire Circuits |

| Humidified Circuits |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Circuit Type | Open Circuits | |

| Semi-Open Circuits | ||

| Semi-Closed Circuits | ||

| Closed Circuits | ||

| Coaxial Circuits | ||

| By Usability | Disposable Circuits | |

| Reusable Circuits | ||

| Single-Patient-Use Kits | ||

| Heated-Wire Circuits | ||

| Humidified Circuits | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected global value of breathing circuits by 2030?

Spending is forecast to reach USD 2.22 billion, reflecting a 6.20% CAGR through 2025-2030.

Which region is expected to post the highest growth over the next five years?

Asia Pacific is set to advance at roughly 7.3% CAGR on the back of ICU build-outs and medical-tourism demand.

Why are closed breathing circuits gaining traction among anesthesiologists?

Sustainability mandates and low-flow techniques cut volatile agent use by up to 90%, helping the segment log a 7.8% CAGR.

How fast is home-based use of respiratory circuits expanding?

Homecare volumes are rising at an 8.3% CAGR as portable ventilators and remote monitoring penetrate chronic-care pathways.

What makes heated-wire designs important for infection control?

They hold inhaled gas near 36 °C and 90% humidity, lowering ventilator-associated pneumonia risk and justifying premium prices.

How do EU single-use plastic rules influence hospital purchasing?

Directive 2019/904 steers buyers toward reusable or recyclable, low-flow sets, favoring vendors with verified eco-credentials.

Page last updated on: