Therapeutic Respiratory Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

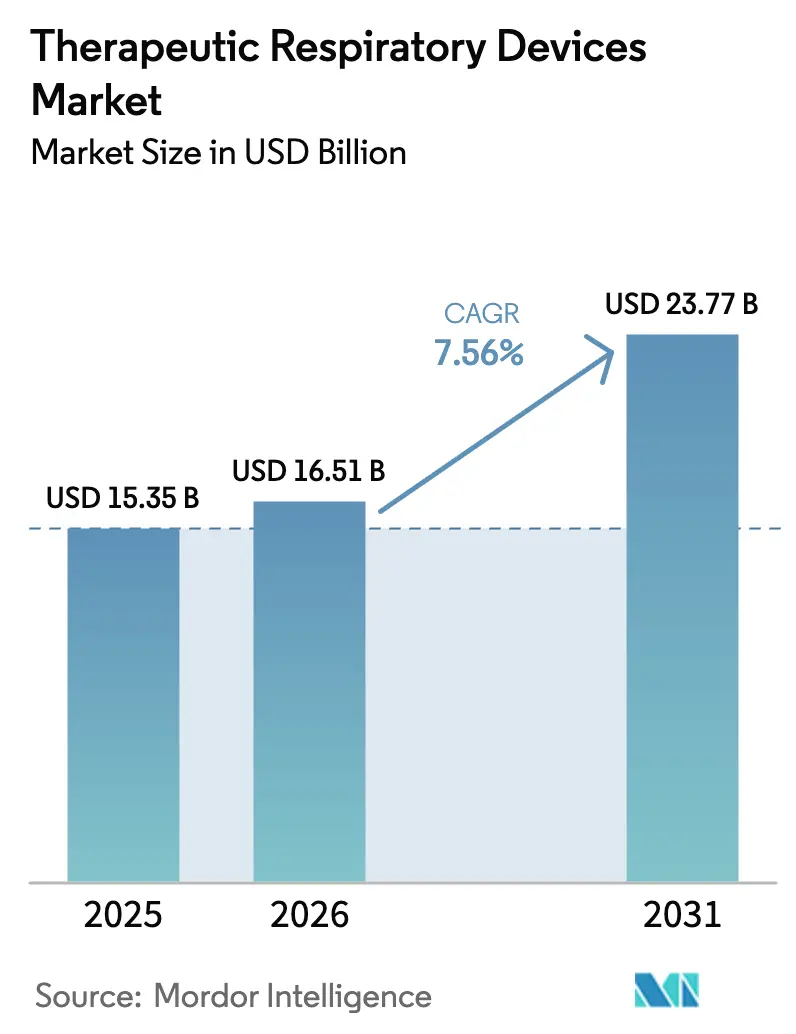

| Market Size (2026) | USD 16.51 Billion |

| Market Size (2031) | USD 23.77 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

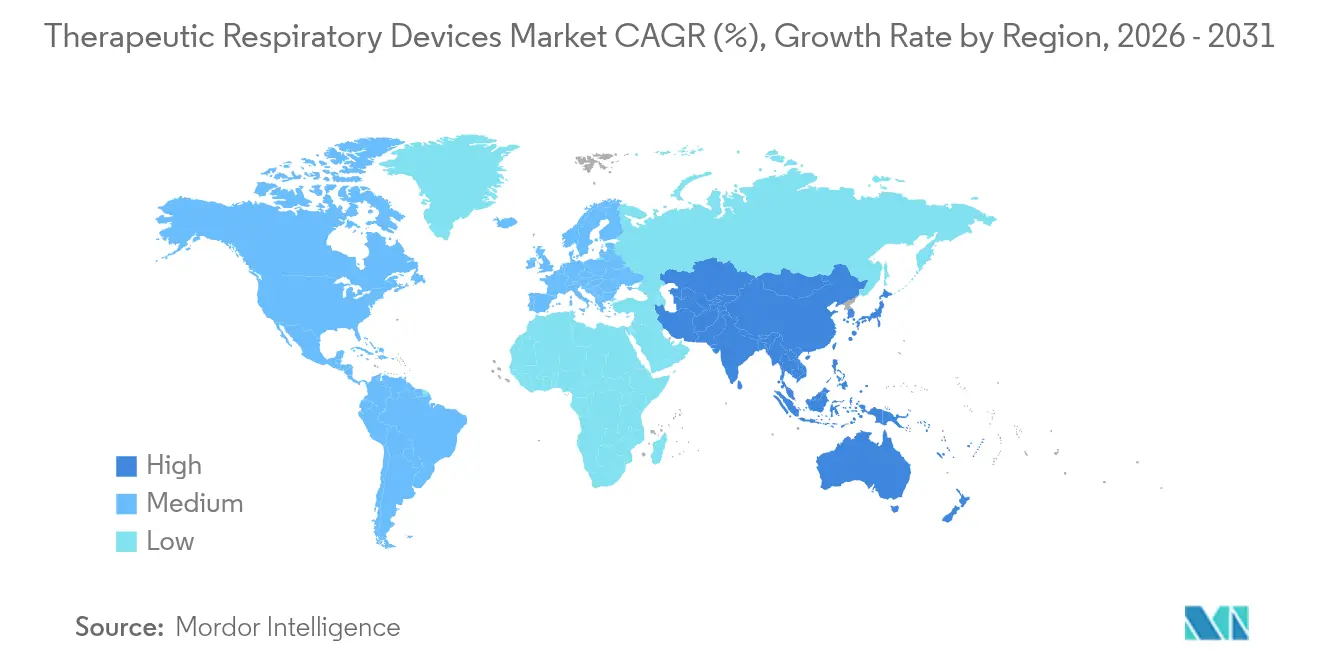

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Therapeutic Respiratory Devices Market Analysis by Mordor Intelligence

The Therapeutic Respiratory Devices Market size was valued at USD 15.35 billion in 2025 and estimated to grow from USD 16.51 billion in 2026 to reach USD 23.77 billion by 2031, at a CAGR of 7.56% during the forecast period (2026-2031). Widening adoption of home-care treatment models, rapid diffusion of digital therapeutics, and steady innovation in miniaturised oxygen systems underpin this growth trajectory. Demand also benefits from rising chronic obstructive pulmonary disease (COPD) prevalence, an ageing population that increasingly requires long-term oxygen therapy, and payer willingness to reimburse connected devices that demonstrably cut readmission costs. Competitive pressure is intensifying as manufacturers fold artificial-intelligence (AI) analytics into positive airway pressure (PAP) platforms, while supply-chain resilience has become a core differentiator after semiconductor shortages disrupted component flows. Regionally, North America continues to generate the bulk of revenue, yet Asia-Pacific is outpacing all other regions on the back of hospital infrastructure expansion and broader access to diagnostics.

Key Report Takeaways

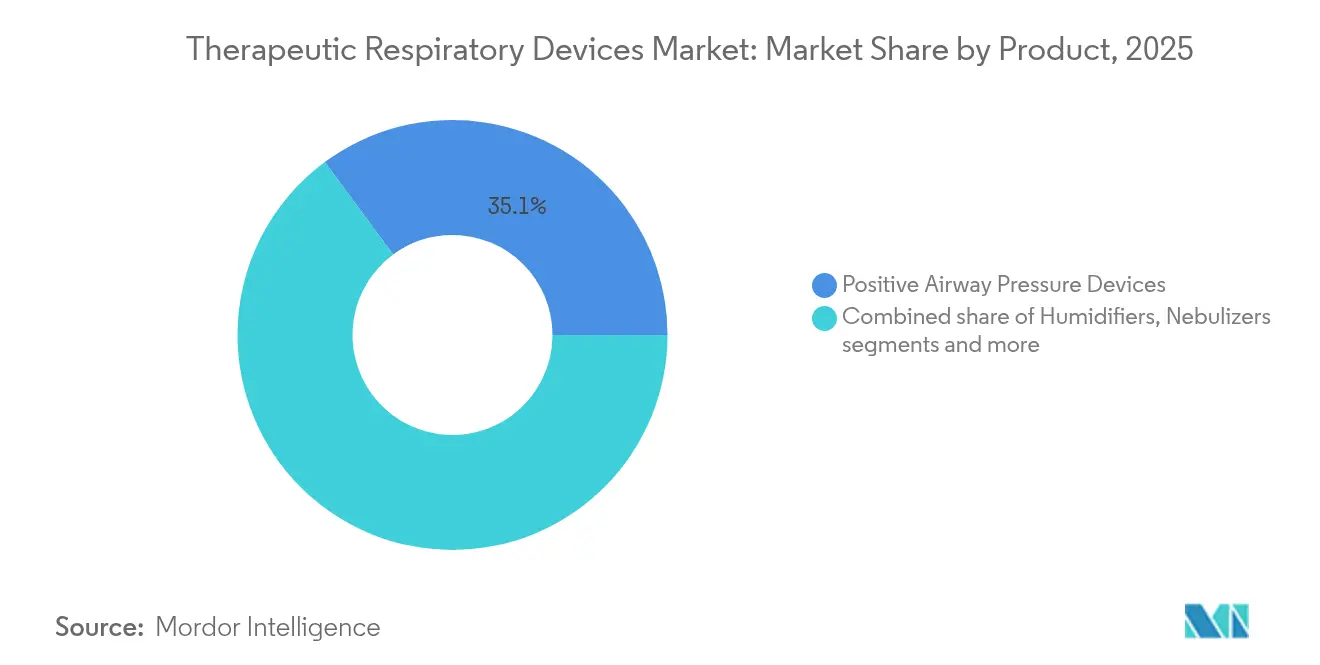

- By product type, positive airway pressure devices held 35.12% of the therapeutic respiratory devices market share in 2025, whereas connected inhalers are projected to post an 8.59% CAGR to 2031.

- By application, COPD accounted for 42.55% of the therapeutic respiratory devices market size in 2025; sleep apnea is forecast to expand at 8.49% CAGR through 2031.

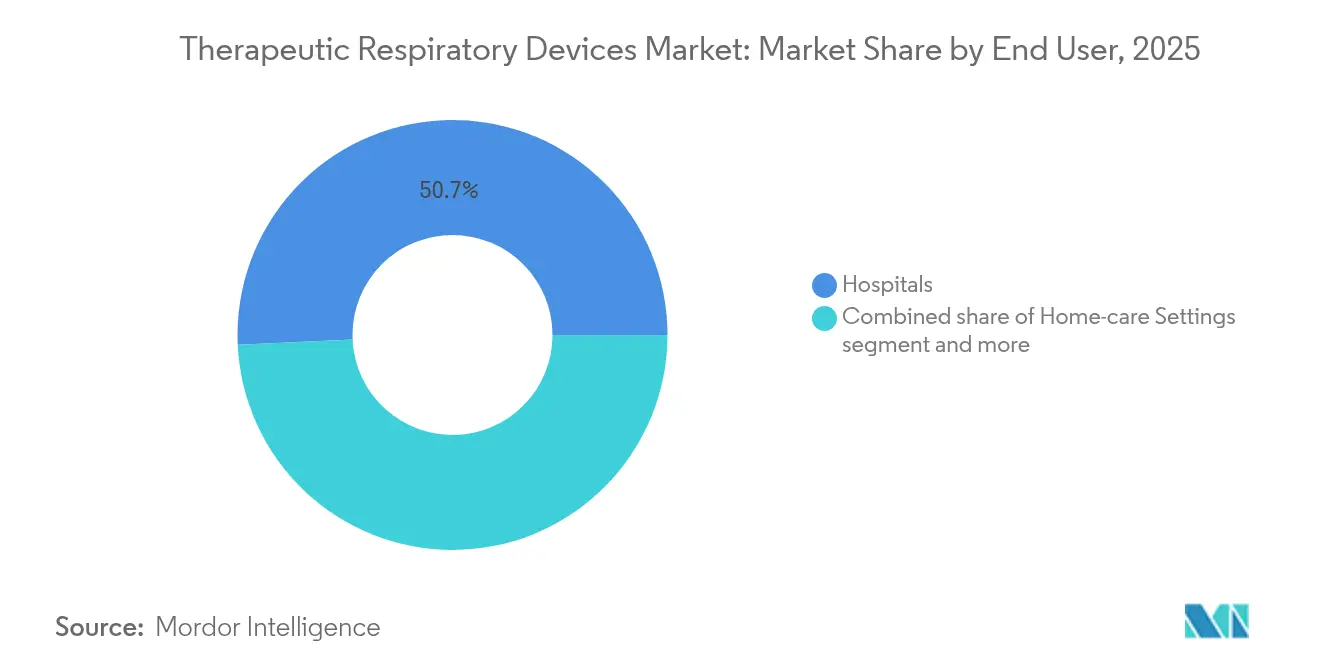

- By end user, hospitals controlled 50.72% revenue share in 2025, while the home-care segment is growing fastest at 9.05% CAGR.

- By geography, North America led with 39.21% revenue contribution in 2025, but Asia-Pacific is projected to record an 8.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Therapeutic Respiratory Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of COPD & asthma | +1.8% | Global, with highest burden in North America, Europe, and aging APAC markets | Medium term (2-4 years) |

| Surging adoption of home-care respiratory support | +1.5% | North America & EU leading, expanding to urban APAC centers | Short term (≤ 2 years) |

| Technological advances in PAP & portable O₂ concentrators | +1.2% | Global, with R&D concentrated in North America and Europe | Medium term (2-4 years) |

| Reimbursement expansion for long-term oxygen therapy | +0.9% | APAC emerging markets, Latin America, with spillover to MEA | Medium term (2-4 years) |

| Miniaturised high-flow nasal cannula systems for pediatrics | +0.6% | Global specialized pediatric centers, early adoption in North America | Medium term (2-4 years) |

| AI-enabled connected inhalers boosting adherence | +0.8% | North America & EU first-movers, expanding to tech-forward APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of COPD & Asthma

Chronic respiratory diseases now cut across age brackets and geographies. Particulate-matter pollution accounts for 41.79% of COPD among younger cohorts, dwarfing the 19.81% attributable to smoking, while occupational exposure contributes 11.73%. Global prevalence among adults aged ≥ 40 years stands at 12.64%. In the United States alone, COPD-related direct medical expenditure reached USD 24 billion in 2024, translating to USD 4,322 per patient. Mortality rates remain higher in rural regions, signalling the need for wider deployment of oxygen concentrators and PAP devices that can be remotely supported.

Surging Adoption of Home-Care Respiratory Support

COVID-19 accelerated payers’ shift toward cost-effective, patient-centric models. Medicare now reimburses portable oxygen concentrators under Part B through 36-month rental periods that cover maintenance.[1]Source: Medical News Today, “Will Medicare pay for portable oxygen concentrators?” medicalnewstoday.com FDA-cleared home spirometers such as NuvoAir enable clinicians to monitor lung function remotely. Home oxygen therapy averages USD 65 per month, well below institutional care outlays. FlexO2 patient-controlled flow selectors doubled the frequency of oxygen-dose adjustments and achieved 83% satisfaction.

Technological Advances in PAP & Portable O₂ Concentrators

Kairos positive airway pressure equals continuous PAP in therapeutic effect while improving comfort metrics. Inogen’s Rove 4 supplies 840 ml/min of oxygen, weighs under 3 lb, and operates 5 hours 45 minutes per charge.[2]Source: Inogen, “Inogen Launches Rove 4 Portable Oxygen Concentrator,” investor.inogen.com Lithium-based zeolite sieves enhance purity and cut energy use in concentrators.[3]Source: Bulletin of the National Research Centre, “Synthesis and characterization of lithium zeolite for oxygen production,” bnrc.springeropen.com ResMed’s myAir integrates smartwatch analytics for adherence coaching. The convergence of hardware miniaturization and software intelligence creates competitive advantages for manufacturers who can deliver integrated solutions that address both clinical efficacy and patient experience requirements.

AI-Enabled Connected Inhalers Boosting Adherence

Meta-analysis confirms digital inhalers deliver three-point gains on the Asthma Control Test. Sensor data from 360 users captured 53,083 inhaler events over 12 weeks, uncovering hidden short-acting beta-agonist overuse in 29% of patients. The FDA cleared Adherium’s Smartinhaler for Airsupra and Breztri devices, signalling regulator confidence in connected platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device capital cost & limited payor coverage in EMs | -0.7% | Emerging markets across APAC, Latin America, and MEA regions | Short term (≤ 2 years) |

| Supply-chain fragility for critical components | -0.5% | Global impact, with semiconductor and electronics dependencies | Short term (≤ 2 years) |

| Infection-control concerns with aerosol-generating devices | -0.4% | Global, particularly acute in hospital settings post-COVID | Short term (≤ 2 years) |

| Rare-earth dependency for high-grade O₂ sieve beds | -0.3% | Global supply chain, concentrated mining in China affecting worldwide production | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Device Capital Cost & Limited Payor Coverage in Emerging Markets

Brazil’s hospitals are modernising rapidly, yet reimbursement lags, pushing 94% of oxygen-therapy claims toward lower-cost stationary concentrators. ANVISA’s 2024-2025 priority list, which includes e-labeling and risk-based reprocessing, aims to cut market-entry friction. Manufacturers must therefore tailor stripped-down devices that maintain clinical efficacy while hitting local price points. The disparity creates market segmentation where premium features concentrate in developed markets while emerging regions require cost-optimized solutions that balance clinical efficacy with economic accessibility.

Supply-Chain Fragility for Critical Components

Semiconductor and rare-earth shortages forced 14 shortage-mitigation strategies, including delayed procedures and alternate suppliers. Medtronic responded by consolidating sites and automating production. Zeolite production for concentrators remains concentrated, prompting near-shoring and strategic-buffer initiatives across the value chain. The industry response includes nearshoring initiatives, strategic inventory management, and development of alternative material sources to reduce single-point-of-failure risks in critical component supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: PAP Devices Lead Innovation Wave

Positive airway pressure systems commanded 35.12% revenue in 2025, maintaining first position within the therapeutic respiratory devices market. ResMed’s fabric-lined AirTouch N30i mask won 92.6% preference among experienced users, underscoring how comfort upgrades can lift compliance. Inhalers, supported by AI-driven monitoring, represent the fastest-growing product category at 8.59% CAGR, signalling an imminent pivot toward drug-device hybrids that capture usage data.

Humidifiers and nebulisers are benefiting from paediatric high-flow therapies that shave 0.65 days off inpatient stays. Concentrators are evolving through Nitroxy molecular sieves that elevate purity and battery life. Ventilator portfolios are consolidating after Medtronic exited the acute-care segment to focus on integrated monitoring. Airway-clearance devices such as Simeox 200 show how oscillatory vibration can expand treatment options for bronchiectasis.

By Application: Sleep Apnea Accelerates Past COPD Growth

COPD remains the largest application with 42.55% market share in 2025, reflecting the sizeable disease burden. However, sleep apnea is growing faster at 8.49% CAGR as diagnostic tools proliferate and therapies broaden. The Inspire V hypoglossal-nerve stimulator illustrates how neurostimulation is carving a niche for moderate-to-severe obstructive cases.

Asthma management is improving through smartwatch-based predictive analytics that warn of attacks using environmental and physiological cues. Other indications, such as cluster headaches treated with home oxygen, signal diversification beyond core pulmonary diseases. Gene-delivery systems that transport mRNA therapies directly to lung tissue herald long-term growth avenues.

By End User: Home-Care Settings Reshape Delivery Models

Hospitals held 50.72% of 2025 revenue within the therapeutic respiratory devices market. Yet home-care environments are expanding at 9.05% CAGR, supported by connected devices that transmit usage and physiological data directly to clinicians. Portable concentrator rentals generate stable cash flows under multiyear Medicare contracts.

Ambulatory clinics are scaling diagnostic capacity with compact sleep-testing rigs, while long-term care facilities equip resident rooms with low-noise concentrators to meet geriatrics needs. Monthly home oxygen costs averaging USD 65 underscore the economic appeal relative to institutional care. Devices such as FlexO2 empower patients to titrate flow, reducing caregiver workload.

Geography Analysis

North America generated 39.21% of global revenue in 2025 by leveraging robust reimbursement and early uptake of digital therapeutics, yet growth in the region is moderating as penetration rates rise. The therapeutic respiratory devices market size for North America is forecast to increase steadily but below the Asia-Pacific pace. Recent CDC infection-control directives are shaping product specifications focused on aerosol-reduction and single-patient use.

Asia-Pacific is the fastest-growing territory, projected at 8.83% CAGR through 2031. Governments are investing in hospital infrastructure and local manufacturing, while India positions its device sector for global prominence by 2025. Regional demand is further buoyed by urban air-quality deterioration and the rising prevalence of sleep-disordered breathing. Local firms are forming joint ventures with multinationals to bring cost-optimised PAP systems to market, supported by e-commerce channels that bypass traditional distribution bottlenecks.

Europe maintains mid-single-digit expansion, sustained by harmonised regulatory frameworks and clinical excellence in tertiary centres. In the Middle East and Africa, market entry remains challenged by procurement cycles and funding variability, yet notable progress is evident. Saudi Arabia registered 5,462 respiratory therapy practitioners by January 2024, reinforcing clinical capacity for device deployment.

Competitive Landscape

The therapeutic respiratory devices market exhibits moderate concentration. ResMed posted USD 1.3 billion in quarterly revenue, reflecting 8% year-over-year growth, driven by cloud-connected PAP ecosystems. Philips, meanwhile, is rebuilding its U.S. franchise under a consent decree following large-scale product recalls.

Fisher & Paykel Healthcare secured patents for nasal-seal interfaces that enhance fit across diverse facial geometries. The competitive landscape increasingly rewards companies that can demonstrate measurable clinical outcomes through real-world evidence, with digital biomarkers and remote monitoring capabilities becoming essential differentiators in both clinical adoption and reimbursement negotiations.

Strategic focus is shifting from standalone hardware to outcomes-based platforms that combine device, software, and coaching services. Industry players allocate roughly 7% of revenue to R&D, prioritising AI algorithms that flag non-adherence or predict exacerbations. Strengthening supply-chain redundancy and embedding antimicrobial surfaces in new models address post-pandemic procurement criteria

Therapeutic Respiratory Devices Industry Leaders

ResMed Inc.

Koninklijke Philips N.V.

Fisher & Paykel Healthcare Ltd

Drägerwerk AG & Co. KGaA

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Honeywell has entered into a long-term supply agreement with DevPro Biopharma. Together, they aim to develop a respiratory inhaler that prioritizes patient well-being and minimizes carbon emissions typically linked to conventional inhalers.

- March 2024: Vapotherm announced plans to debut new home ventilator aimed at enhancing patient care, addressing growing demand for effective home care solutions in respiratory therapy

- April 2023: OxyGo announced the launch of OxyHome 5L Stationary Concentrator, specifically designed to provide continuous oxygen flow of up to 5 liters per minute for use at home.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the therapeutic respiratory devices market as all proprietary, non-disposable equipment that delivers or supports treatment for chronic or acute pulmonary conditions. Devices considered include positive airway pressure systems, ventilators, oxygen concentrators, nebulizers, humidifiers, smart inhalers, and adjunct analyzers used across hospitals, specialty clinics, and home-care settings.

Scope exclusion: Purely diagnostic tools such as spirometers and standalone pulse oximeters remain outside this assessment.

Segmentation Overview

- By Product

- Positive Airway Pressure Devices

- Humidifiers

- Nebulizers

- Oxygen Concentrators

- Ventilators

- Inhalers

- Other Therapeutic Devices

- By Application

- COPD

- Asthma

- Obstructive Sleep Apnea

- Other Applications

- By End User

- Hospitals

- Home-care Settings

- Ambulatory Surgical and Specialty Clinics

- Long-term Care Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with respiratory therapists, biomedical engineers, and procurement heads across North America, Europe, and Asia Pacific tested secondary findings, revealed average device replacement cycles, and clarified price dispersion between hospital and home channels. Follow-up surveys with sleep-lab directors validated prevalence-to-treatment assumptions for obstructive sleep apnea.

Desk Research

We began with granular device shipment and trade statistics from bodies such as the UN Comtrade, OECD Health Data, and the WHO Global Health Observatory, supplemented by payer utilization files released by the US CMS and Eurostat. Patent analytics from Questel and company 10-Ks added insight on pipeline breadth and installed base. Newsflows tracked on Dow Jones Factiva and prescribing trends published by the Global Initiative for Chronic Obstructive Lung Disease helped us map therapy uptake. These sources illustrate rather than exhaust the evidence pool consulted by analysts.

Market-Sizing & Forecasting

A top-down model starts with COPD and sleep-apnea patient pools, which are then layered with treatment penetration, device ownership per patient, and weighted average selling prices. Results are corroborated through selective bottom-up checks, sampled ventilator shipments, channel audits, and PAP manufacturer revenue splits to align volumes and values. Key variables include hospital ICU bed additions, home-care reimbursement limits, average device life (five to seven years), urban air-quality indices, and telehealth adoption rates. Multivariate regression, informed by expert consensus on these drivers, projects demand to 2030, while scenario analysis adjusts for regulatory or pandemic shocks. Data gaps in supplier roll-ups are bridged by price-volume proxies agreed upon during interviews.

Data Validation & Update Cycle

Outputs pass a two-step anomaly review before sign-off. We compare modeled values with independent indicators such as import duty receipts and public tender awards. Mordor analysts refresh the model annually and trigger interim updates after material events, ensuring clients always receive the latest validated view.

Why Our Therapeutic Respiratory Devices Baseline Commands Reliability

Published figures often diverge because studies vary in device mix, pricing logic, and refresh cadence. By centering on therapy-grade hardware only, using blended hospital and home ASPs, and refreshing each year, Mordor Intelligence narrows those gaps.

Key gap drivers include some publishers folding diagnostic or single-use items into totals, others applying list rather than transaction prices, and a few locking forecasts for five years without mid-course corrections when reimbursement shifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.35 B (2025) | Mordor Intelligence | - |

| USD 13.20 B (2024) | Global Consultancy A | Broader historic base yet fewer future drivers, limited home-care channel validation |

| USD 20.44 B (2024) | Trade Journal B | Includes diagnostic kits and consumables, uses list prices |

| USD 25.24 B (2025) | Industry Association C | Assumes universal device adoption and constant premium pricing |

In sum, our disciplined scope selection, live price checks, and annual refresh cadence give decision-makers a balanced, transparent baseline that traces back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the therapeutic respiratory devices market?

The market is valued at USD 16.51 billion in 2026 and is projected to reach USD 23.77 billion by 2031.

Which region is expanding fastest in the therapeutic respiratory devices market?

Asia-Pacific is forecast to grow at an 8.83% CAGR through 2031, outpacing all other regions.

Which product category leads revenue share today?

Positive airway pressure systems hold 35.12% revenue, maintaining the top spot.

Why are connected inhalers gaining traction?

AI-enabled sensors improve adherence and clinical outcomes, driving an 8.59% CAGR for inhalers.

How quickly is the home-care segment growing?

Home-care settings are advancing at 9.05% CAGR thanks to reimbursement expansion and remote-monitoring capabilities.

What supply-chain risks affect manufacturers?

Semiconductor shortages and rare-earth dependency for zeolite sieve beds remain key vulnerabilities, prompting near-shoring and diversification strategies.

Page last updated on: