Mechanical Ventilators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.1 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

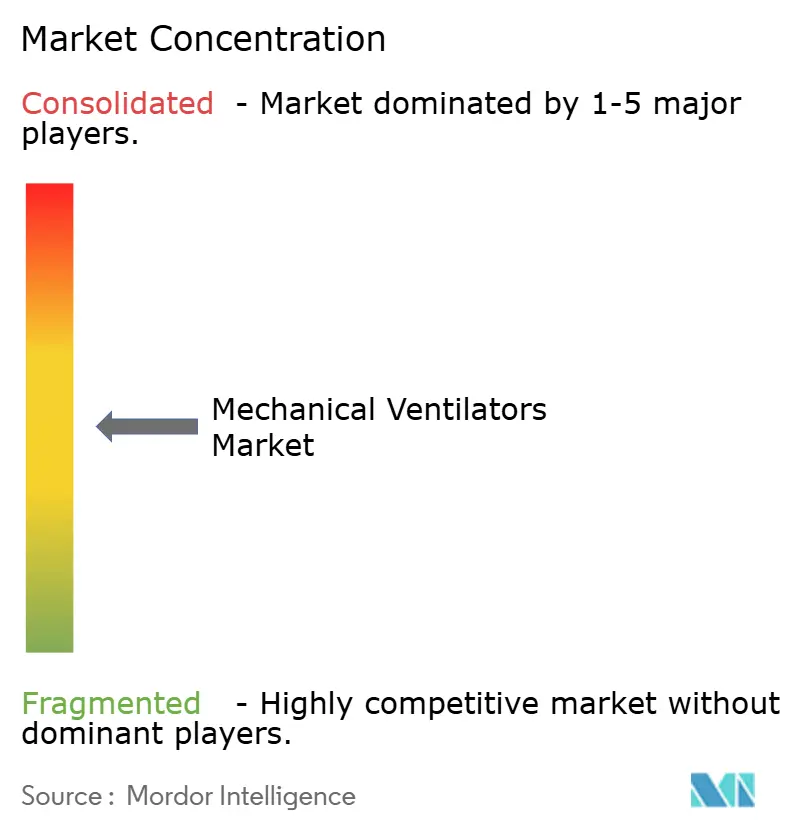

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mechanical Ventilators Market Analysis by Mordor Intelligence

The mechanical ventilator market size is expected to grow from USD 5.33 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 7.1 billion by 2031 at 4.9% CAGR over 2026-2031. Growth is shifting from pandemic-driven surges to steady expansion supported by aging populations that demand longer ICU stays and by rising chronic respiratory conditions such as COPD. Artificial-intelligence features now automate closed-loop ventilation, cut clinician workload, and reduce complications, encouraging hospitals to refresh fleets despite tighter capital budgets. Home care is emerging as a parallel growth engine because updated Medicare rules cover non-invasive ventilation for chronic respiratory failure, enabling patients to avoid repeat admissions. Regional imbalances in critical-care infrastructure, especially in Asia-Pacific, create white-space opportunities for cost-effective devices that meet lower-acuity needs.

Key Report Takeaways

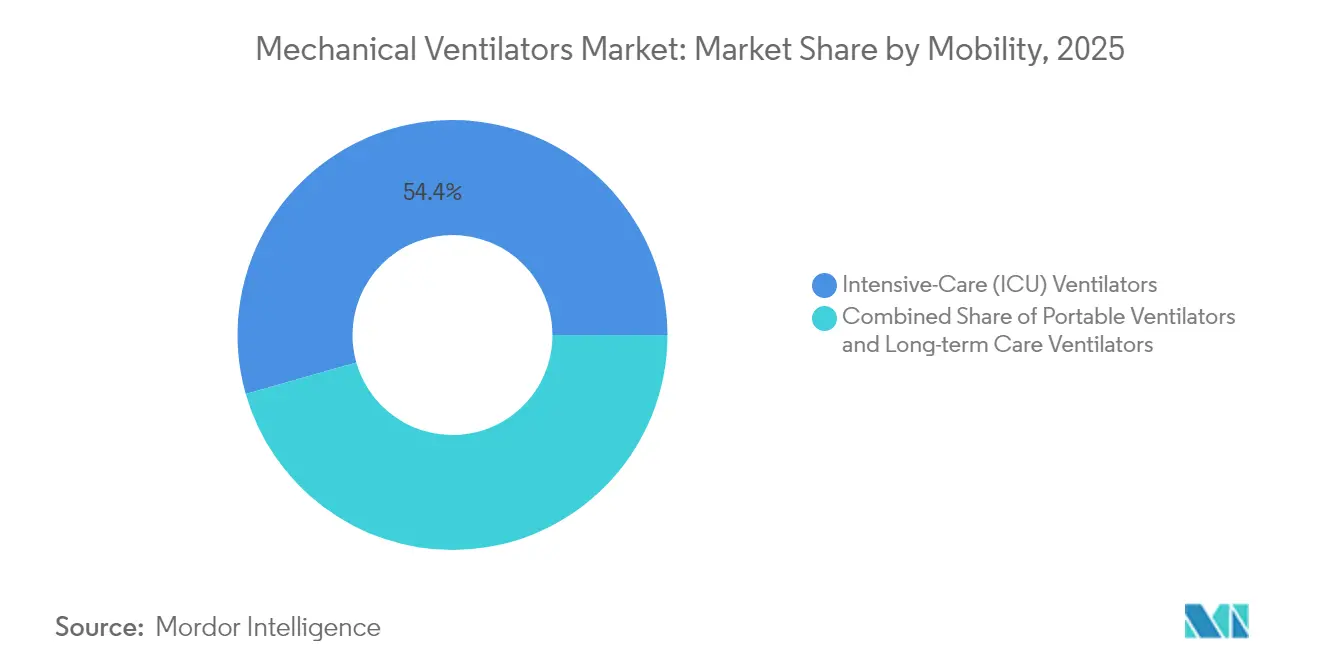

- By mobility, intensive care ventilators led with 54.42% of mechanical ventilator market share in 2025, while transport and portable units post the fastest 5.26% CAGR to 2031.

- By interface, invasive systems held 63.72% of the mechanical ventilator market size in 2025; non-invasive ventilation is projected to expand at 5.58% CAGR through 2031.

- By patient age, adults commanded 70.63% share of the mechanical ventilator market size in 2025; neonatal devices record the highest 5.74% CAGR to 2031.

- By end-user, hospitals controlled 74.05% of mechanical ventilator market share in 2025, whereas home healthcare is growing fastest at 5.96% CAGR to 2031.

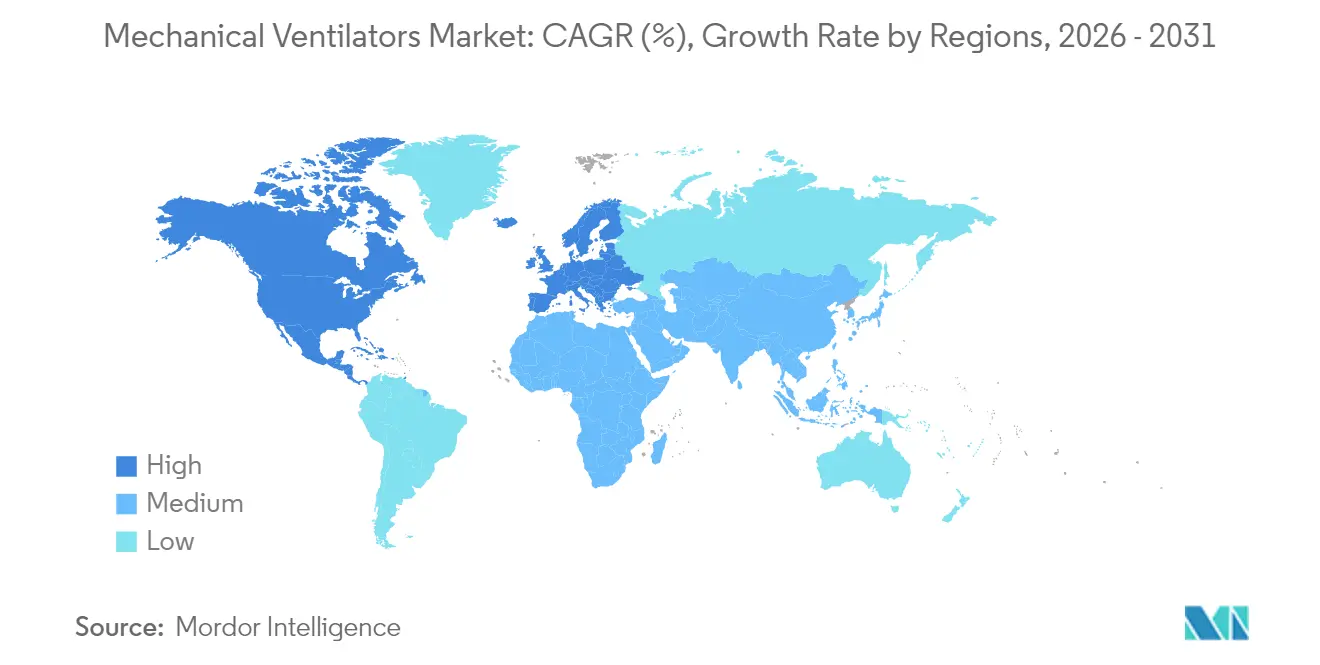

- By geography, North America accounted for 42.44% of mechanical ventilator market share in 2025; Asia-Pacific advances at the highest 6.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mechanical Ventilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising COPD prevalence | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Aging population & ICU capacity expansion | +1.5% | Global, strongest in developed economies | Long term (≥ 4 years) |

| Government pandemic-preparedness stockpiles | +0.8% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| AI-driven closed-loop ventilation adoption | +1.0% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| Home NIV growth for obesity hypoventilation | +0.7% | North America, Europe | Medium term (2-4 years) |

| Micro-turbine & battery efficiency advances | +0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising COPD prevalence

Global COPD cases continue climbing, reinforcing baseline demand across invasive and non-invasive devices. The Centers for Medicare & Medicaid Services broadened 2025 coverage for home ventilation when PaCO₂ remains at or above 52 mmHg, which expands the treated COPD population.[1]Centers for Medicare & Medicaid Services, “Final Rule for Home Ventilation Coverage,” cms.govOverlap with obesity hypoventilation syndrome and obstructive sleep apnea has produced a 1.560% prevalence pool that often requires domiciliary ventilatory support. Home therapy lowers readmissions and improves blood-gas exchange, even though daytime dyspnea persists. These outcomes underpin payer acceptance and spur manufacturers to tailor compact, low-maintenance non-invasive models. As the disease burden skews older, demand also converges with the broader demographic shift toward chronic comorbidity management.

Aging population and ICU capacity expansion

Older adults already make up 22% of Australia’s population and similar trajectories exist across Europe and North America. Hospital associations project 170 million inpatient days in the United States by 2030 as chronic conditions rise. Longer ventilation courses drive equipment turnover, while persistent intensivist shortages prompt hospitals to invest in smarter modes that reduce hands-on adjustments. In France, two-thirds of ICUs now report at least one physician vacancy, magnifying the value of automation. Nations such as China plan large expenditure increases that could lift per-capita health spending more than 10-fold by mid-century, signaling sustained capacity buildouts. The COVID-19 pandemic exposed geographic imbalances that technology suppliers can help correct through modular, rapidly deployable units.

Government pandemic-preparedness stockpiles

Ventilator reserving has become a policy anchor since 2021. The U.S. Strategic National Stockpile can absorb as many as 56,300 additional units at peak demand, contingent on trained staff and accessories. Federal agencies now prefer decentralized storage that aligns with outbreak clusters and logistical realities. Decision-support software helps health departments model allocation scenarios during respiratory crises, ensuring the mechanical ventilator market remains linked to wider emergency infrastructure needs. Brazil’s collaborative repair network restored 62.17% of idle ventilators in 2024, underscoring maintenance as a pillar of preparedness. Suppliers that bundle service programs with hardware gain traction as budgets tilt toward lifecycle value over one-off purchases.

AI-driven closed-loop ventilation adoption

Machine learning now detects asynchrony events that affect one-quarter of ventilated patients, improving outcomes and shortening stays. Systems such as INTELLiVENT-ASV automatically modify tidal volume and respiratory rate in real time, cutting clinician adjustments by double-digit margins. High-frequency jet ventilation algorithms further personalize settings and lower lung injury risk. The FDA’s upcoming Quality Management System Regulation aligns national standards with ISO 13485:2016, raising compliance costs yet simplifying global approvals. Vendors that absorb these costs early strengthen competitive positions as hospitals prioritize cyber-secure, upgradeable platforms.

Home NIV growth for obesity hypoventilation

Medicare coding changes and remote-monitoring tools have repositioned home NIV as a mainstream therapy for obesity-related respiratory failure. Manufacturers now integrate cloud dashboards so clinicians can track adherence, which boosts reimbursement compliance and patient satisfaction. Qualitative studies show that users shift from initial resistance to full dependence once symptom relief stabilizes daily activities. Portable turbines with 8-hour batteries and noise levels below 35 dB help adoption alongside mask designs that reduce pressure points. These user-centric improvements underpin the 6.15% CAGR expected in home healthcare spending.

Micro-turbine and battery efficiency advances

Lithium-ion power-management chips can extend ventilator battery life 30% without weight penalties, critical for transport and military applications. Rapid-charge technology makes swap-out logistics easier during regional disasters. Turbine innovations also allow non-pressurized oxygen sources, easing deployment in remote clinics. Such upgrades land quickly in procurement cycles, influencing near-term sales while larger AI overhauls take longer to standardize.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & maintenance costs | -0.9% | Global, strongest impact in emerging markets | Long term (≥ 4 years) |

| Ventilator-associated pneumonia (VAP) | -0.6% | Global | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.7% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Reimbursement cuts for long-term home use | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High device and maintenance costs

Total supply-chain expenses absorb up to 20% of device revenue as geopolitical shocks raise component prices. Ventilators fall under Medicare’s Frequent and Substantial Servicing category, obligating regular upkeep that inflates ownership costs. Compliance with the FDA’s 2026 quality rule will further increase documentation and validation spending, particularly for AI software updates. Emerging hospitals with below-average ICU bed density struggle to finance premium models, steering them toward refurbished or locally assembled units. Suppliers respond with modular designs that share parts across acuity tiers to curb logistics overhead.

Ventilator-associated pneumonia

VAP incidence ranges from 1.4 to 7 episodes per 1,000 ventilator days in developed settings and up to 89 in resource-constrained hospitals. The infection lengthens stays and can double mortality risk, discouraging aggressive ventilation strategies. Silver-coated tubes cut bacterial colonization by 99.9%, yet high cost and patchy evidence slow uptake. Antimicrobial peptide coatings now under trial promise broad-spectrum protection without fostering resistance. Training-driven care bundles improve results but require consistent nurse staffing, which remains elusive in many ICUs. As AI matures, early detection alarms may limit secretion pooling and micro-aspiration.

Semiconductor supply-chain volatility

Chip shortages tied to regional conflicts and trade restrictions delayed up to 6 months of ventilator shipments in 2024, raising prices and feeding hospital frustrations. Manufacturers accelerate near-shoring and dual-sourcing yet still face logistics headwinds, especially for high-end micro-controllers used in turbine speed regulation. Continuous-flow turbines benefit from less complex circuitry and thus maintain steadier lead times, aiding lower-end market resilience.

Reimbursement cuts for long-term home use

Periodic payment reviews in Europe have trimmed tariffs for home ventilation bundles, pressuring provider margins and potentially delaying device renewals. Companies diversify into remote-monitoring subscriptions to defend revenue. Policy risk therefore limits forecast upside despite robust clinical demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mobility: ICU platforms anchor innovation in portable formats

Intensive care units dominate with 54.42% mechanical ventilator market share in 2025. Their purchasing decisions steer supplier R&D, producing adaptive closed-loop modes and low-noise turbines that then migrate into transport variants. The mechanical ventilator market size for ICU models is projected to continue outpacing overall revenue because hospitals refresh fleets faster than lower-acuity sites when software advances push measurable quality gains. Portable devices, though starting from a smaller base, accelerate on 5.26% CAGR through 2031 as emergency services and disaster-response teams prioritize battery runtime and rugged housings. The HAMILTON-C6 illustrates cross-segment technology transfer by packaging ICU-grade algorithms in a moveable chassis that weighs under 10 kg. Transport adoption also rises when reimbursement codes permit billing during inter-facility transfers, particularly in North America.

A hybrid product class for sub-acute wards has emerged, blending weaning tools with moderate flow capabilities to avoid full-price ICU hardware. Fleet managers appreciate common consumables across chassis families, which lowers inventory. Suppliers that design shared user interfaces across mobility classes simplify training and cut user error. These value propositions help defend premium pricing even as public tenders emphasize lowest cost compliant bids.

By Interface: Invasive leadership meets rapid non-invasive gains

Invasive ventilation accounts for 63.72% of revenue in 2025 because severe ARDS and surgical procedures still require endotracheal access. The mechanical ventilator market size linked to invasive systems will expand modestly, while non-invasive lines post 5.58% CAGR through 2031 thanks to domiciliary uptake and early intervention protocols. Leakage-compensation software such as IntelliTrig enhances patient synchrony, reducing escalation to intubation. Hospitals increasingly deploy dual-mode devices so clinicians can switch without swapping hardware, which lowers capital intensity.

Non-invasive gains also stem from growing pediatric and neonatal applications. Interfaces tailored to small airways and facial structures reduce skin injuries while enabling prolonged therapy. Helmets and mouthpiece ventilation deliver alternatives where masks trigger claustrophobia. Regulatory approvals for high-flow nasal cannula add competitors to conventional NIV by covering mild hypoxemia cases. Manufacturers balance portfolio breadth with inventory complexity through modular manifold connectors and sensor arrays.

By Patient Age: Adults dominate volume, neonates lead percentage growth

Adults remain the primary driver with 70.63% share in 2025 because chronic disease prevalence skews older and surgery volumes are highest in this cohort. The mechanical ventilator market size tied to adult care captures the biggest absolute revenue increments each year. Neonatal systems, though smaller in dollars, grow at 5.74% through 2031 as survival of very-low-birth-weight infants improves and more NICUs adopt gentle ventilation strategies. New trials report decision-support software lifting spontaneous breathing trial success to 55%, shaving a day off median ventilation time in pediatrics. These gains translate into shorter bed occupancy, freeing capacity.

Hardware miniaturization features sensors sensitive enough to track tidal volumes under 10 mL, critical for preventing volutrauma in neonates. Servo-controlled humidifiers stabilize airway conditions, while algorithms automatically transition between pressure and volume control when patient effort rises. In adult wards, diaphragm-protective modes adjust expiratory pauses to mitigate atrophy during long ventilation runs, a growing need in geriatric populations.

By End-User: Hospital outlay meets disruptive home-care economics

Hospitals hold 74.05% mechanical ventilator market share in 2025, yet home healthcare’s 5.96% CAGR through 2031 draws investor attention as value-based care shifts services outward. Hospitals justify premium ICU models through bundled reimbursement that rewards reduced length of stay. They remain the earliest adopters of AI features because they possess IT teams able to validate cybersecurity requirements from regulators such as the Defense Health Agency. Home providers prioritize low noise, portability, and remote telemetry to keep nurse visit frequency low.

VieMed’s revenue jump in 2024 highlights profitability when device financing aligns with chronic-care billing cycles, especially under new Medicare coverage for persistent hypercapnia. Firms offering service contracts and replacement consumables shield revenue from tariff fluctuations. Ambulatory surgical centers purchase mid-range units that support quick weaning; this raises after-sale parts demand but keeps capital budgets manageable.

Geography Analysis

North America, with 42.44% mechanical ventilator market share in 2025, benefits from extensive ICU infrastructure, federal stockpiles, and supportive reimbursement frameworks . Public procurement policy now blends centralized reserve purchases with hospital fleet refresh subsidies, smoothing order patterns after the 2020-2022 demand spike. Adherence to FDA cybersecurity guidance also favors domestic suppliers with validated software lifecycles.

Europe follows as a mature yet innovative buyer. The region enforces strict eco-design and data-protection rules that push vendors toward energy-efficient turbines and encrypted cloud connectors. Several countries roll out national AI roadmaps for critical care, making funding available for pilot deployments. Market volume remains steady; revenue growth arises from higher average selling prices and software subscriptions.

Asia-Pacific records the fastest 6.45% CAGR through 2031, powered by health infrastructure initiatives that aim to lift critical-care bed density above 5 per 100,000 population in middle-income nations . Variance within the region is high. High-income economies such as Japan sustain upgrade cycles every five years, whereas low-income countries rely on grant financing. Suppliers succeed by offering scalable platforms that accept both wall and compressor oxygen sources.

China’s recognition of intensive care as a specialty in 2009 ignited a network of professional societies that standardize protocols and accelerate equipment tendering. Local firms co-licensed western turbine technology to bypass import tariffs, putting price pressure on multinationals. India and Indonesia prioritize Make-in-Country schemes that favor domestic value addition above 30%.

Latin America saw emergency manufacturing booms during COVID-19. Governments now convert some pop-up facilities into permanent critical-care wards, sustaining baseline demand for mid-tier ventilators. Currency volatility nevertheless complicates capital imports, so lease models gain popularity.

The Middle East and Africa trail in penetration yet hold long run potential. Oil-rich Gulf states fund high-spec ICUs, demanding premium devices with integrated nitric oxide delivery. Resource-poorer nations depend on donor funding and require rugged units capable of dusty environments and variable power supply. Suppliers partner with NGOs to bundle training, easing adoption.

The United States dominates the North American mechanical ventilators market, accounting for approximately 44.62% of the regional ventilator market share in 2025. The country's market leadership is supported by its extensive healthcare network comprising over 5,000 hospitals with advanced intensive care facilities. The presence of leading manufacturers, robust healthcare infrastructure, and high healthcare expenditure further strengthen its market position. The US market is characterized by strong demand for both intensive care ventilators and portable ventilation solutions, driven by the rising incidence of chronic respiratory diseases and an aging population requiring long-term ventilation support.

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 6.78% during 2026-2031. The country's market growth is driven by increasing healthcare expenditure, growing adoption of home healthcare solutions, and rising awareness about respiratory care management. Canadian healthcare facilities are increasingly investing in advanced ventilation technologies to improve patient outcomes. The government's supportive healthcare policies and focus on enhancing critical care infrastructure contribute to market expansion. The country also shows strong demand for portable ventilators, particularly in remote healthcare settings and home care applications.

The European mechanical ventilators market demonstrates significant strength, supported by well-established healthcare systems across Germany, the United Kingdom, France, Italy, and Spain. The region's market is characterized by high adoption rates of advanced medical technologies and a strong presence of major ventilator manufacturers. European countries maintain strict regulatory standards for medical devices while continuously investing in healthcare infrastructure improvement. The market benefits from an increasing focus on home healthcare solutions and rising demand for portable ventilation devices.

Germany leads the European mechanical ventilators market, holding approximately 19.74% of the regional ventilator market share in 2025. The country's market leadership is attributed to its robust healthcare system, substantial healthcare spending, and strong domestic manufacturing capabilities. German hospitals maintain high standards of intensive care facilities and demonstrate consistent demand for advanced ventilation solutions. The presence of major manufacturers and research institutions contributes to continuous innovation in ventilation technologies, while the country's aging population drives sustained market growth.

The United Kingdom represents a significant market in Europe, with a projected growth rate of approximately 6.82% during 2026-2031. The UK's healthcare system continues to invest in modernizing its critical care infrastructure and expanding access to advanced respiratory care solutions. The country shows increasing adoption of portable and home ventilation solutions, driven by a growing emphasis on home healthcare services. British healthcare facilities are actively incorporating new ventilation technologies to improve patient care outcomes and operational efficiency.

The Asia-Pacific mechanical ventilators market demonstrates robust growth potential, encompassing diverse healthcare markets across China, Japan, India, South Korea, and Australia. The region experiences increasing healthcare infrastructure development, rising healthcare expenditure, and growing awareness about respiratory care. Rapid urbanization, increasing pollution levels, and rising incidence of respiratory diseases drive market expansion across these countries. The region also benefits from growing domestic manufacturing capabilities and increasing adoption of advanced medical technologies.

China maintains its position as the largest market for mechanical ventilators in the Asia-Pacific region. The country's extensive healthcare system modernization, large patient population, and growing domestic manufacturing capabilities drive market growth. Chinese healthcare facilities continue to expand their critical care capabilities, while increasing focus on home healthcare solutions creates new market opportunities. The country's investment in healthcare infrastructure and emphasis on medical device manufacturing self-sufficiency strengthens its market position.

South Korea emerges as the fastest-growing market in the Asia-Pacific region. The country's advanced healthcare system, strong technological capabilities, and increasing focus on healthcare innovation drive market expansion. Korean healthcare facilities demonstrate high adoption rates of advanced ventilation technologies, while the country's aging population creates sustained demand. The market benefits from strong domestic manufacturing capabilities and continuous investment in healthcare infrastructure development.

The Middle East & Africa mechanical ventilators market shows promising growth potential, with significant variations across different regions. The GCC countries lead the regional market, benefiting from substantial healthcare investments and modern medical facilities. South Africa represents another key market, with growing healthcare infrastructure development and increasing adoption of advanced medical technologies. The region demonstrates an increasing focus on improving critical care facilities and expanding access to advanced respiratory care solutions, with the GCC emerging as both the largest and fastest-growing market in the region.

The South American mechanical ventilators market continues to evolve, with Brazil and Argentina representing key markets in the region. The market benefits from ongoing healthcare infrastructure development, increasing healthcare expenditure, and rising awareness about respiratory care. Brazil maintains its position as the largest market in the region, while Argentina shows the fastest growth potential. The region demonstrates increasing adoption of both intensive care and portable ventilation solutions, supported by growing healthcare investments and expanding access to advanced medical technologies.

Competitive Landscape

Top Companies in Mechanical Ventilators Market

The mechanical ventilator market straddles moderate consolidation. Top brands leverage patented algorithms, validated cybersecurity, and regulatory expertise to defend share. Medtronic’s 2024 exit signaled a pivot away from capital-heavy respiratory portfolios, freeing niche players to capture legacy installed bases. Hamilton Medical leads with more than 605 patent families covering INTELLiVENT-ASV and real-time waveform analysis, creating a defensible moat.

Getinge secured U.S. Defense Health Agency clearance for its Servo line, differentiating on cybersecurity and fleet-management dashboards. Zoll expanded by acquiring Vyaire assets, broadening consumables to lock in recurring revenue. GE HealthCare collaborates with AWS on generative-AI applications that combine imaging and respiratory data, positioning its ventilators within a wider digital ecosystem.

Supply-chain resilience remains a strategic focal point. Firms pursue dual manufacturing footprints and vertically integrate PCB assembly to buffer chip shortages. Some clients negotiate vendor-managed inventory to guarantee 30-day supply of critical parts. Software subscription models shift income toward predictable streams while opening cross-selling of analytics.

Emerging-market entrants use frugal engineering to compete on price yet incorporate essential safety alarms to meet IEC 60601 norms. Partnerships with local distributors accelerate regulatory filings and training roll-outs. As AI features mature, intellectual-property control becomes the main barrier, preserving premium pricing among established incumbents.

Mechanical Ventilators Industry Leaders

Getinge AB

Smiths Medical

ResMed Inc.

Medtronic PLC

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Nihon Kohden America broadened access to the NKV-440 ventilator system, targeting providers facing staff shortages and budget limits.

- October 2024: Zoll finalized the acquisition of select assets from Vyaire Medical’s ventilator division, ensuring continued availability of acquired product lines.

- January 2023: Getinge launched the Servo-c ventilator with pediatric and adult lung-protective modes and modular components for fleet efficiency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the mechanical ventilators market as the worldwide sales of electrically or pneumatically powered devices that deliver controlled volumes or pressures of gas through invasive or non-invasive interfaces to support or replace spontaneous respiration across acute, transport, and home-care settings.

Scope exclusion: non-mechanical high-flow oxygen therapy systems and standalone CPAP/BiPAP sleep-apnea units are not counted.

Segmentation Overview

- By Mobility

- Intensive-Care (ICU) Ventilators

- Transport / Portable Ventilators

- Sub-acute & Long-term Care Ventilators

- By Interface

- Invasive Ventilation

- Non-Invasive Ventilation (NIV)

- By Patient Age

- Adult

- Pediatric

- Neonatal

- By End-User

- Hospitals

- Home Healthcare

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview critical-care physicians, biomedical engineers, hospital procurement heads, and respiratory therapists across North America, Europe, Asia, and LATAM. These conversations validate installed-base estimates, discount levels, replacement cycles, and emerging preferences for hybrid invasive/non-invasive modes, allowing us to tighten assumptions surfaced from desk work.

Desk Research

We start with public anchors, regulatory device clearances (FDA 510(k), EU MDR), trade statistics from UN Comtrade, and ventilator-specific procedure volumes published by bodies such as OECD Health and WHO. Clinical guidelines from societies (ERS, ATS) and ICU bed build-out plans released by ministries of health help us size demand pools. Company 10-Ks, investor decks, and quarterly shipments supplement pricing and mix trends, while paid databases like D&B Hoovers and Dow Jones Factiva provide revenue splits that sharpen vendor roll-ups. This list illustrates our desk inputs; many additional open and subscription sources underpin the database we keep up-to-date.

Market-Sizing & Forecasting

We reconstruct global demand top-down by linking ICU bed counts, ventilator penetration ratios, and replacement cadence. We then cross-check with sampled average selling price multiplied by unit shipments from leading manufacturers. Key variables include COPD prevalence, elective surgery volumes, neonatal ICU admission rates, export-import flows of HS 9019 devices, and average device lifespan. A multivariate regression model, stress-tested with three macro scenarios, projects each driver to 2030; outputs are benchmarked against selective bottom-up supplier roll-ups and adjusted where variance exceeds five percent.

Data Validation & Update Cycle

Analysts run variance, outlier, and currency-conversion checks before senior review. The model refreshes every twelve months, with interim revisions triggered by material recalls, pandemic surges, or reimbursement changes. A final validation pass occurs just prior to report release so clients receive the freshest view.

Why Mordor's Mechanical Ventilators Baseline Commands Reliability

Published estimates rarely align because firms pick different product mixes, base years, and inflation adjustments.

We recognize these gaps at the outset.

Key gap drivers in rival studies include lumping high-flow oxygen devices with true ventilators, using pandemic-year peaks as baselines, or applying static ASPs despite post-COVID price normalization.

Mordor's scope, currency harmonization, and annual refresh cadence minimize such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.33 B (2025) | Mordor Intelligence | - |

| USD 3.71 B (2024) | Global Consultancy A | Excludes home-care ventilators; relies on 2023 ASPs without post-pandemic resets |

| USD 3.40 B (2024) | Trade Journal B | Omits neonatal units and uses limited hospital procurement surveys from two regions |

| USD 3.17 B (2024) | Regional Consultancy C | Combines mechanical and non-mechanical high-flow systems, narrowing true ventilator share |

These comparisons show that when scope breadth, currency parity, and driver trends are consistently applied, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Mechanical Ventilators Market?

The Mechanical Ventilators Market size is expected to reach USD 5.59 billion in 2026 and grow at a CAGR of 4.9% to reach USD 7.1 billion by 2031.

Which segment holds the largest mechanical ventilator market share?

Intensive care ventilators lead with 54.42% share as of 2025, supported by hospitals expanding ICU capacity.

Who are the key players in Mechanical Ventilators Market?

Getinge AB, Smiths Medical, ResMed Inc., Medtronic PLC and Koninklijke Philips NV are the major companies operating in the Mechanical Ventilators Market.

Which is the fastest growing region in Mechanical Ventilators Market?

Asia-Pacific posts the highest 6.45% CAGR because governments are investing in critical-care infrastructure.

Which region has the biggest share in Mechanical Ventilators Market?

In 2025, the North America accounts for the largest market share in Mechanical Ventilators Market.

Page last updated on: