Non-invasive Ventilators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

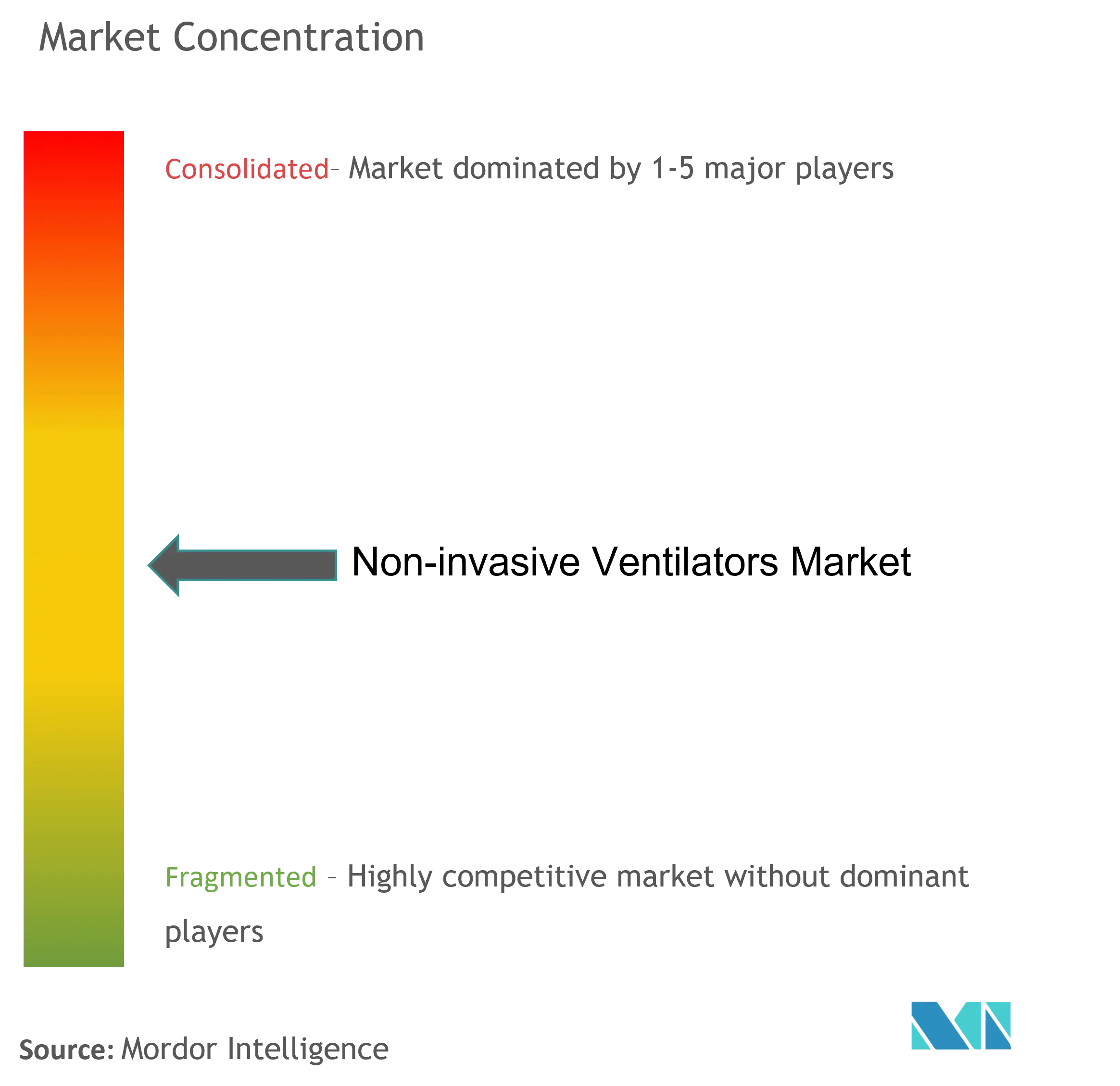

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-invasive Ventilators Market Analysis by Mordor Intelligence

The non-invasive ventilator market size is expected to grow from USD 3.18 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 4.47 billion by 2031 at 5.85% CAGR over 2026-2031. Demand is shifting from pandemic-driven surges to secular growth anchored in chronic respiratory disease management, geriatric care requirements and rising home-based therapy adoption. Artificial-intelligence algorithms that fine-tune pressure delivery, together with simplified negative-pressure concepts for resource-limited settings, are broadening the clinical footprint of the non-invasive ventilator market. Device makers focus on comfort-oriented interfaces, noise reduction and cloud connectivity to keep patients on therapy, while payers in the United States and selected European Union countries expand reimbursement to ease budget constraints. Asia-Pacific healthcare build-outs, semiconductor supply-chain stabilization and FDA fast-track clearances for portable platforms support a resilient outlook for the non-invasive ventilator market beyond traditional hospital walls.

Key Report Takeaways

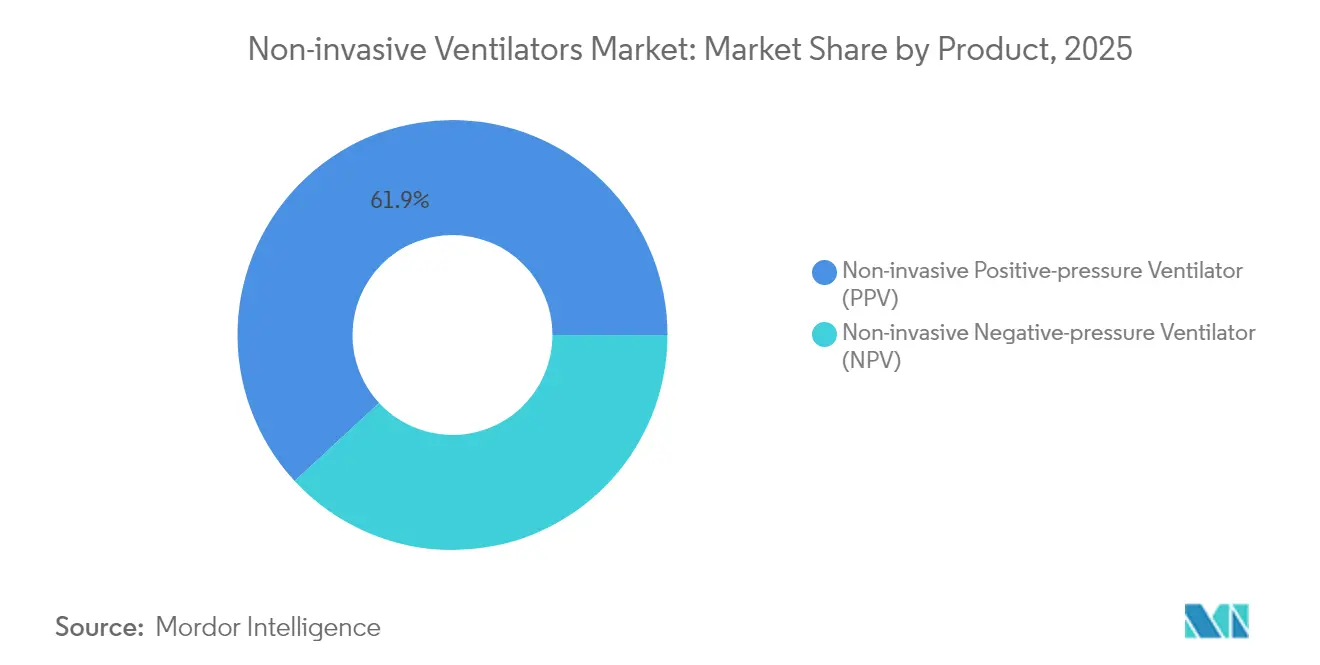

- By product category, non-invasive positive-pressure ventilators led with 61.88% revenue share in 2025; non-invasive negative-pressure ventilators are projected to grow at a 6.92% CAGR to 2031.

- By application, COPD & asthma captured 58.05% of non-invasive ventilator market share in 2025, while respiratory distress syndrome is poised for the fastest 7.05% CAGR through 2031.

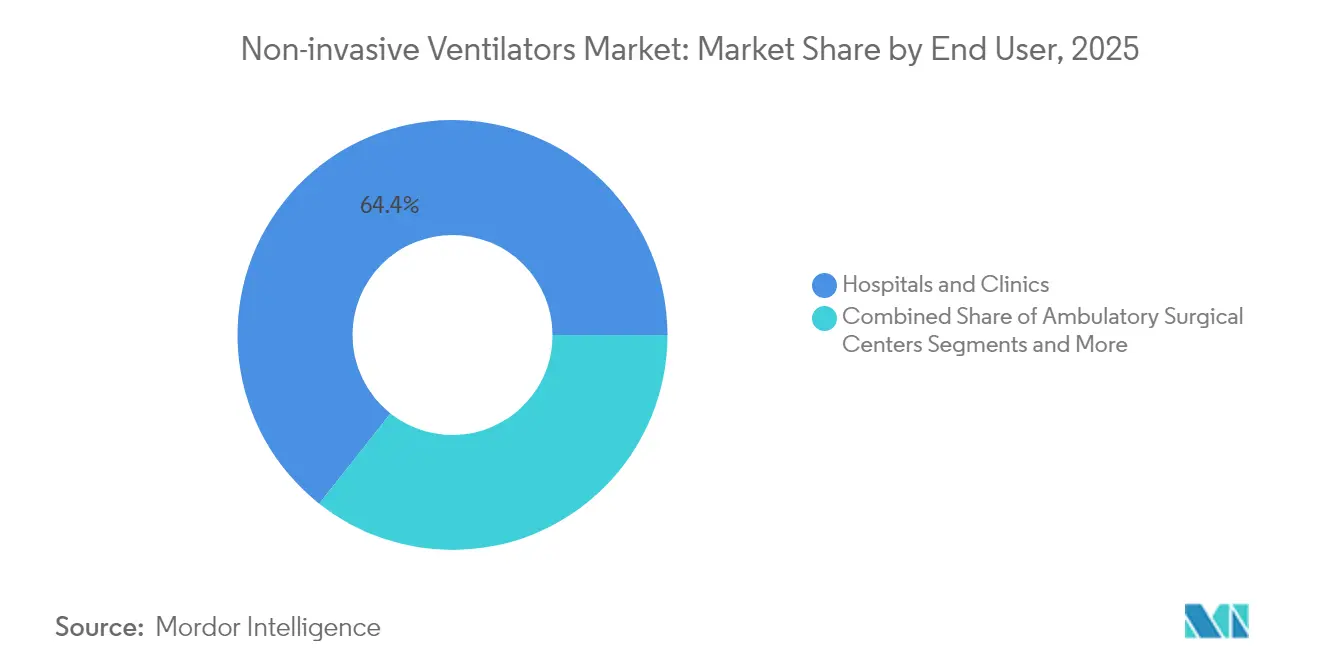

- By end user, hospitals & clinics accounted for 64.35% of the non-invasive ventilator market size in 2025, yet homecare settings are set to expand at a 7.45% CAGR between 2026-2031.

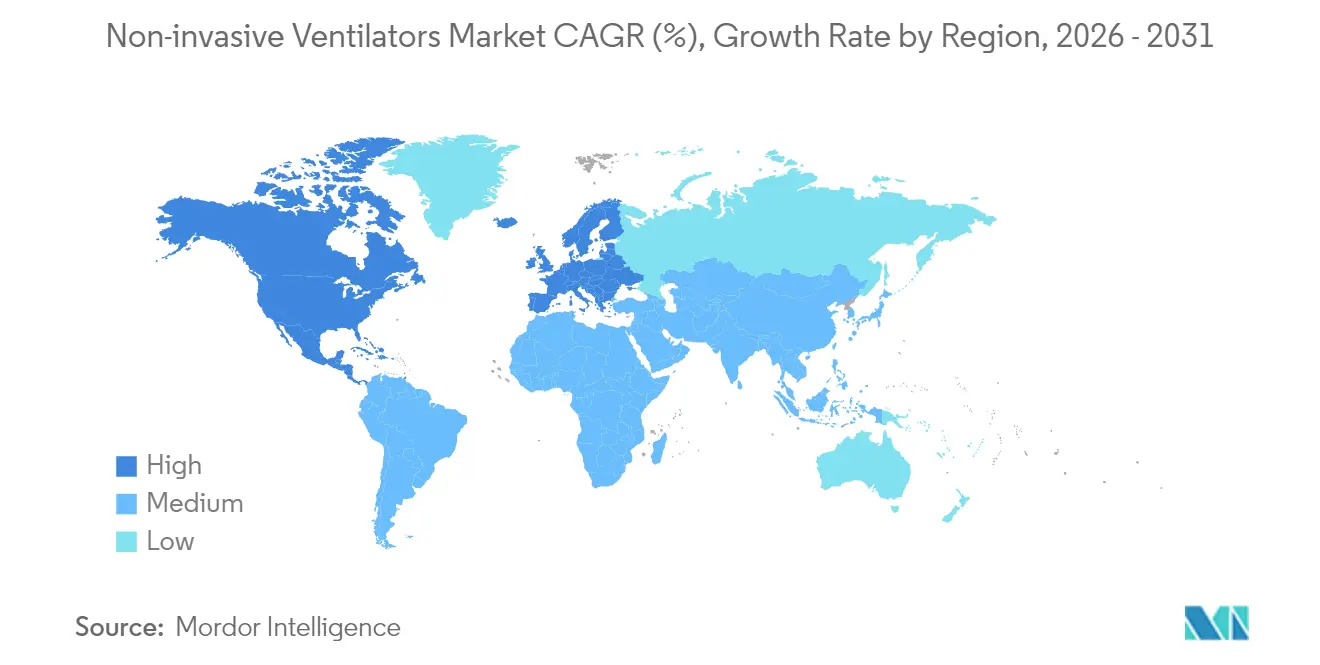

- By geography, North America commanded 42.80% of revenue in 2025, whereas Asia-Pacific is expected to post the highest 7.68% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-invasive Ventilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Prevalence Of COPD & Asthma Cases | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Increasing ICU Admissions Among Geriatrics | +1.2% | Global, particularly APAC and North America | Medium term (2-4 years) |

| Shift Toward Home-Based NIV Therapy | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Reimbursement Expansion For Home NIV | +0.9% | North America, selective EU markets | Short term (≤ 2 years) |

| AI-Driven Closed-Loop NIV Modes Gain Traction | +0.6% | Global, led by developed markets | Long term (≥ 4 years) |

| Rise Of Low-Cost Negative-Pressure NIV Devices For LMICs | +0.4% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of COPD & Asthma Cases

More than 390 million people live with COPD and 262 million with asthma worldwide, generating steady demand for advanced ventilation support. Meta-analyses show that long-term non-invasive ventilation reduces mortality in obstructive sleep apnea and hypercapnic COPD cohorts. The 2025 GOLD report adds cardiovascular risk control and climate-related exacerbation management to treatment pathways, favoring intelligent ventilation that adapts to fluctuating physiology. Average Volume Assured Pressure Support paired with transcutaneous CO₂ monitoring lowers 48-hour reintubation risk and shortens stays for acute-on-chronic COPD cases. Real-time analytics platforms further personalize therapy and cut unplanned admissions by predicting decompensation events.

Increasing ICU Admissions Among Geriatrics

Adults over 65 account for a growing portion of intensive-care occupancy, often presenting with respiratory failure and multiple comorbidities. Non-invasive ventilation reduces inspiratory effort and improves tidal volumes in elderly patients compared with high-flow nasal oxygen. Device protocols now incorporate lower trigger thresholds and synchrony features to match diminished muscle strength, lowering extubation failure odds. Health systems expand ICU beds yet prefer NIV to avoid invasive airway complications and to shorten length of stay, protecting budgets while raising quality scores.

Shift Toward Home-Based NIV Therapy

Portable platforms weighing under 2 kg, battery runtimes exceeding 10 hours and Bluetooth telemetry create viable substitutes for overnight hospital monitoring. CMS opened a national coverage analysis for home non-invasive ventilation in COPD, generating momentum for outpatient care models [1]U.S. Centers for Medicare & Medicaid Services, “National Coverage Analysis for Home Mechanical Ventilation,” cms.gov . Randomized trials confirm that home NIV significantly elevates quality-of-life metrics and slashes readmissions in severe stable COPD. Internet-of-Things dashboards transmit adherence, leak and pressure data to clinicians, enabling same-day setting tweaks that keep patients in therapeutic ranges. Cost savings accrue from avoided inpatient days and reduced transport needs.

Reimbursement Expansion for Home NIV

New HCPCS code E0468 for dual-function respiratory devices took effect in April 2024, reflecting policymaker acceptance of hybrid ventilation technologies. Proposed 2025 fee-schedule updates refine relative value units for respiratory services, potentially lifting physician participation in home NIV programs. Commercial insurers mirror Medicare moves, citing studies that document 25% lower 30-day readmission rates in patients managed with remote-monitored NIV. Streamlined 510(k) clearances for portable units reduce time-to-market for innovators while maintaining post-market surveillance rigor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ventilator-Associated Pneumonia (VAP) Risk | -0.8% | Global, higher impact in developing markets | Medium term (2-4 years) |

| High Device & Maintenance Cost | -0.7% | APAC, MEA, Latin America | Short term (≤ 2 years) |

| Skill Gap In Handling Advanced NIV Modes | -0.5% | Global, particularly LMICs | Long term (≥ 4 years) |

| Supply-Chain Fragility For Critical Components | -0.4% | Global, concentrated in semiconductor-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ventilator-Associated Pneumonia Risk

VAP incidence ranges from 9.2% to 30% in mechanically ventilated cohorts, adding roughly USD 544,467 per case to hospital bills versus non-VAP patients. Diagnostic variability complicates prevention, prompting global infection societies to standardize bundles that combine head-of-bed elevation, circuit hygiene and early mobilization. While NIV avoids intubation, mask leaks and secretion buildup can still seed infection, requiring design tweaks such as automatic secretion drainage and antimicrobial surfaces. Education campaigns in low- and middle-income countries show that bundle adherence cuts VAP rates by up to 35%, protecting fragile budgets.

High Device & Maintenance Cost

Advanced ventilators entail upfront capital outlays that strain emerging-market providers, while annual upkeep can equal 3-5% of hospital revenue dedicated to supply-chain services. Component complexity demands periodic calibration and skilled biomedical engineers. Simplified negative-pressure units fabricated from locally sourced materials at roughly USD 262 per device ease cost pressures without compromising safety when used under strict protocols. Leasing programs that bundle hardware, consumables and tele-support spread expenses over multi-year horizons, granting smaller hospitals access to premium therapy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Positive Pressure Dominance Sustains Innovation

The non-invasive ventilator market size for positive-pressure devices stood at USD 1.97 billion in 2025, corresponding to a 61.88% revenue share that reflects their entrenched role in acute and chronic care settings. Continuous Positive Airway Pressure and Bilevel PAP remain gold standards for obstructive sleep apnea and COPD exacerbations, benefiting from auto-adjusting algorithms that calibrate pressure in five-millisecond cycles. Manufacturers add humidification controls and noise-attenuation chambers to lift adherence above 80% during the first 90 days of therapy. Cloud-native dashboards push ventilatory parameters to clinicians, allowing remote titration that reduces follow-up visits. Patient-facing mobile apps gamify nightly use and flag mask-fit issues in real time.

Negative-pressure ventilators are experiencing a technical renaissance, recording the fastest 6.92% CAGR through 2031. Modern shells use lightweight composites and compact vacuum pumps, enabling patients to sit upright, converse and ingest food without therapy interruption. Clinical studies in acute respiratory distress syndrome report 15% higher PaO₂/FiO₂ ratios compared with positive-pressure modes, suggesting lung-protective advantages. Philanthropic consortia fund open-source designs aimed at district hospitals in low-resource geographies, and regulatory agencies have published fast-track guidelines to validate essential safety features.

By Application: COPD Leadership Amid Diversification

COPD & asthma accounted for 58.05% of non-invasive ventilator market share in 2025, supported by GOLD guideline endorsements for chronic hypercapnic management. Long-term NIV reduces mortality and mitigates cardiovascular comorbidity risks, prompting integrated disease management programs that pair ventilation with tele-coaching. Advanced Average Volume Assured Pressure Support linked to transcutaneous CO₂ sensors lowers 48-hour re-intubation from 18% to 10% in severe AECOPD cases. Algorithmic weaning tracks dyspnea scores and accelerates hospital discharge by 1.5 days on average.

Respiratory distress syndrome shows a 7.05% CAGR outlook as emergency departments adopt NIV for preoxygenation during intubation, cutting hypoxemia incidence to 9.1% versus 18.5% with standard mask approaches . Trials such as RENOVATE confirm NIV’s efficacy across mixed-etiology acute respiratory failure, broadening clinical confidence. Pediatric and postoperative indications join the pipeline, with size-adaptive masks and leak-compensation modes extending applicability.

By End User: Hospital Dominance Meets Home Expansion

Hospitals & clinics retained 64.35% of the non-invasive ventilator market size in 2025, leveraging multidisciplinary teams that manage complex comorbidities. Intensive-care protocols now pair NIV with closed-loop oxygen titration, minimizing desaturation episodes. Infection-control bundles that coordinate suction, oral hygiene and positioning have cut VAP rates by 25% inside large academic centers. Capital-planning committees prioritize hybrid devices capable of both invasive and non-invasive modes to hedge against future pandemic shocks.

Homecare settings post a market-leading 7.45% CAGR thanks to lightweight turbines, 4G connectivity and reimbursement liberalization. Ventilation-as-a-service models bundle hardware, disposables and 24-hour helplines, giving payers predictable cost lanes while boosting patient satisfaction scores above 90%. Remote-physiology dashboards feed machine-learning engines that identify leak spikes or apnea clusters, triggering automated alerts to nurses. Early data from North American insurers reveal 22% fewer readmissions in home-managed COPD compared with center-based pathways.

Geography Analysis

North America commanded 42.80% of non-invasive ventilator market revenue in 2025 on the back of high disease prevalence, sophisticated reimbursement and rapid device approvals. The FDA granted 510(k) clearance to the Servo-air portable ventilator in June 2024, adding choice for outpatient programs. CMS’s national coverage analysis for home NIV therapy is expected to widen beneficiary access in late 2025, stimulating supplier investment in cloud ecosystems. Data-integration mandates encourage interoperability between ventilators, electronic health records and payer portals, creating a virtuous cycle of evidence generation and reimbursement reinforcement.

Asia-Pacific records the fastest 7.68% CAGR through 2031. Healthcare expenditure in China surpassed CNY 8.5 trillion in 2022 and is projected to hit CNY 20.5 trillion by 2030, enabling tertiary-care network upgrades . Governments introduce pilot schemes for negative-pressure ventilation kits in rural clinics to address acute pneumonia outbreaks without relying on scarce intensive-care beds. Local assembly lines shorten lead times and insulate procurement from currency volatility. Regional academic partnerships generate data on NIV efficacy in tuberculosis-coexistent COPD, guiding tailored protocols.

Europe stabilizes growth at mid-single digits, supported by universal health systems and stringent safety standards. The European Respiratory Society’s latest guideline endorses early application of NIV in postoperative respiratory failure, feeding procurement pipelines for high-flow capable machines. ESG initiatives push suppliers to design recyclable circuits and to measure carbon footprints across the ventilator life cycle.

Middle East & Africa and South America contribute modest base-effect expansion. Oil-exporting economies channel surplus revenue into critical-care capacity, while public-private partnerships in Brazil fund tele-ventilation projects that connect secondary hospitals with urban pulmonology hubs. Development banks back equipment-leasing pools to sidestep high import tariffs, further democratizing access.

Competitive Landscape

Market structure remains moderately consolidated. ResMed recorded 11% fiscal-2024 revenue growth as cloud-connected AirView and myAir ecosystems drove patient engagement. Medtronic exited its Puritan Bennett ventilator line in February 2024 to redeploy capital toward robotic surgery, opening share opportunities for mid-tier entrants. ZOLL acquired select Vyaire platforms for USD 37 million, adding bellavista and LTV models that bolster its acute-care franchise.

Competitive advantage hinges on proprietary algorithms, seamless data flows and flexible financing. Philips continues remediation under an FDA consent decree that caps new Respironics shipments until quality-management milestones are met. Fisher & Paykel focuses on humidification patents that lower mucosal dryness, while Hamilton Medical markets turbine-driven units that cut oxygen consumption by 25% in high-altitude regions. Start-ups develop open-source negative-pressure shells priced under USD 300 for humanitarian missions, a niche that established players monitor for reverse-innovation cues.

Strategic partnerships proliferate. Device makers sign APIs with electronic medical record vendors to embed ventilation dashboards within clinician workflows. Telecom operators co-develop low-latency 5G gateways that transmit waveform data to cloud AI engines, enabling instant leak detection.

Non-invasive Ventilators Industry Leaders

ResMed Inc.

Teleflex Incorporated

Hamilton Bonaduz AG

Koninklijke Philips N.V.

heyer medical AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Airon Corporation introduced the pNeuton mini ventilator for neonates, compatible with MRI environments and suitable for patients from 400 g to 25 kg.

- July 2022: Nihon Kohden OrangeMed received FDA 510(k) clearance for the NKV-330 ventilator, covering invasive, non-invasive and high-flow oxygen modalities.

- April 2022: Philips Respironics launched the V60 plus ventilator, offering assist modes for invasive and non-invasive support with circuits powered up to 35 V.

Global Non-invasive Ventilators Market Report Scope

As per the scope of the report, non-invasive ventilation (NIV) refers to the delivery of ventilatory assistance through the patient's upper airway by utilizing a mask or other similar device. This method differs from those that are invasive since they use a tracheal tube, laryngeal mask, or tracheostomy to bypass the upper airway. The Intravascular Catheter Market is expected to register a CAGR of 9.0% during the forecast period. The Non-invasive Ventilators Market is Segmented by Product (Non-invasive Positive Pressure Ventilators (PPV) (Bi-level Positive Airway Pressure Ventilator (BiPAP), Constant Positive Airway Pressure Ventilator (CPAP), Autotitrating (Adjustable) Positive Airway Pressure Ventilator (APAP)), and Non-invasive Negative Pressure Ventilators (NPV)), Application (COPD and Asthma, Respiratory Distress Syndrome, and Others), End Users (Hospitals and Clinics, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Non-invasive Positive-pressure Ventilator (PPV) | Bi-level Positive Airway Pressure (BiPAP) |

| Constant Positive Airway Pressure (CPAP) | |

| Autotitrating Positive Airway Pressure (APAP) | |

| Non-invasive Negative-pressure Ventilator (NPV) |

| COPD & Asthma |

| Respiratory Distress Syndrome |

| Others |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Non-invasive Positive-pressure Ventilator (PPV) | Bi-level Positive Airway Pressure (BiPAP) |

| Constant Positive Airway Pressure (CPAP) | ||

| Autotitrating Positive Airway Pressure (APAP) | ||

| Non-invasive Negative-pressure Ventilator (NPV) | ||

| By Application | COPD & Asthma | |

| Respiratory Distress Syndrome | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Homecare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Non-invasive Ventilators Market size?

The non-invasive ventilator market size reached USD 3.37 billion in 2026 and is projected at USD 4.47 billion by 2031.

Who are the key players in Non-invasive Ventilators Market?

ResMed Inc., Teleflex Incorporated, Hamilton Bonaduz AG, Koninklijke Philips N.V. and heyer medical AG are the major companies operating in the Non-invasive Ventilators Market.

Which product type dominates sales?

Non-invasive positive-pressure ventilators led with 61.88% revenue share in 2025.

How fast is homecare adoption expanding?

Homecare settings are expected to grow at a 7.45% CAGR between 2026-2031, outpacing hospital growth.

Page last updated on: