Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.36 Billion |

| Market Size (2031) | USD 22.59 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

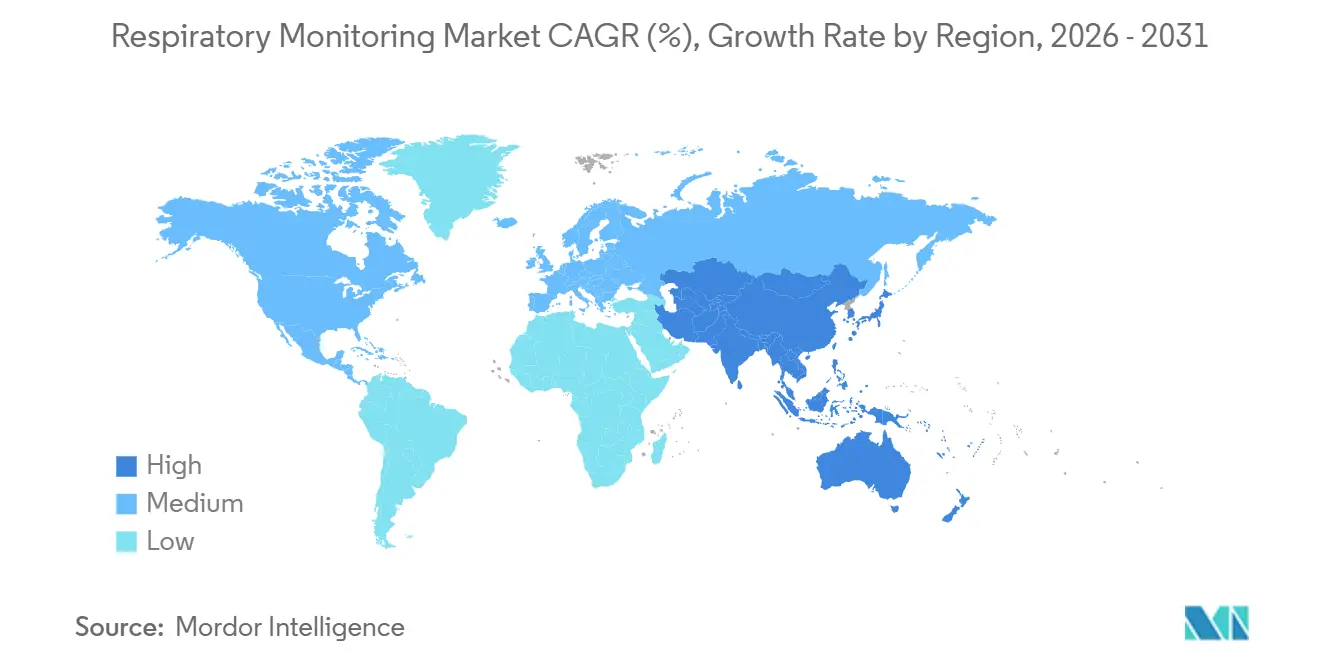

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Monitoring Market Analysis by Mordor Intelligence

The respiratory monitoring market size is expected to grow from USD 12.03 billion in 2025 to USD 13.36 billion in 2026 and is forecast to reach USD 22.59 billion by 2031 at 11.08% CAGR over 2026-2031. Momentum stems from the rapid fusion of AI, IoT, and miniaturized sensors that enable continuous, contextual respiratory data collection across care settings. Hospital demand remains strong, yet a fundamental shift toward home-based monitoring is underway, spurred by pandemic-era telehealth adoption and payer emphasis on cost containment. Wearable platforms are eroding the dominance of tabletop and handheld systems by providing real-time insight into chronic disease trajectories. Meanwhile, stringent post-recall regulatory scrutiny is lengthening approval timelines, nudging manufacturers toward earlier engagement with regulators and investment in rigorous safety validation.

Key Report Takeaways

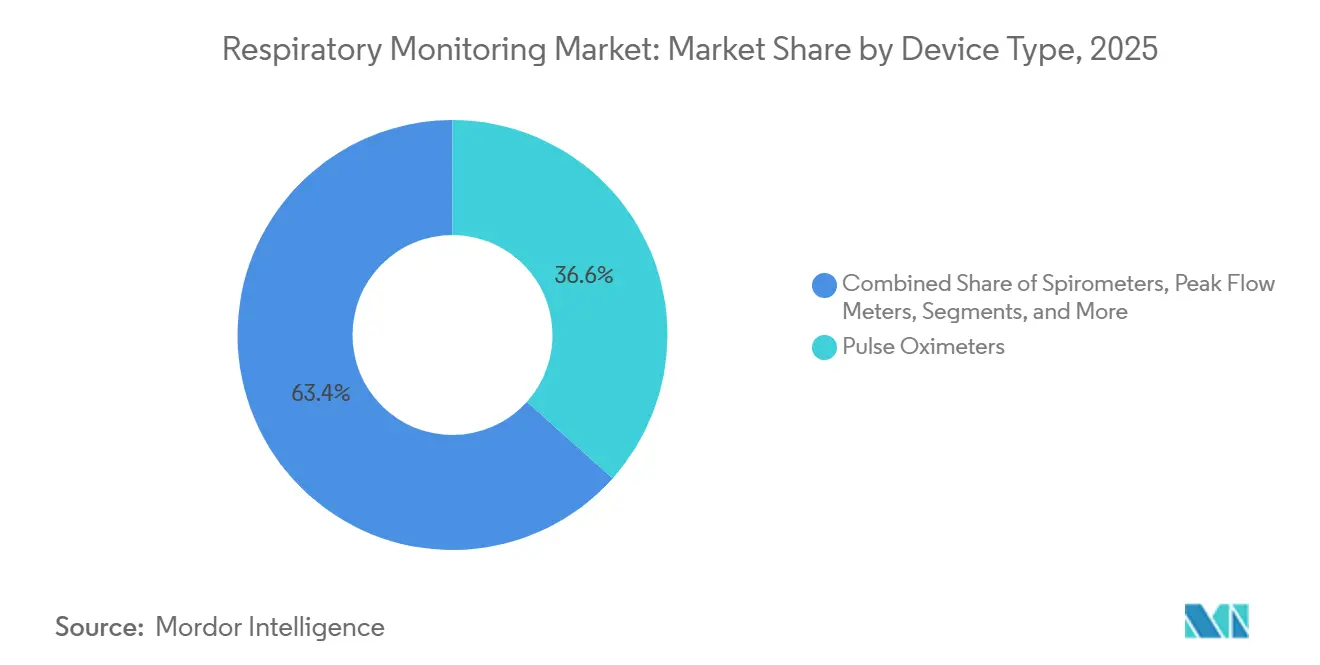

- By device type, pulse oximeters commanded 36.62% of the respiratory monitoring market share in 2025, while capnographs are set to expand at an 8.54% CAGR through 2031.

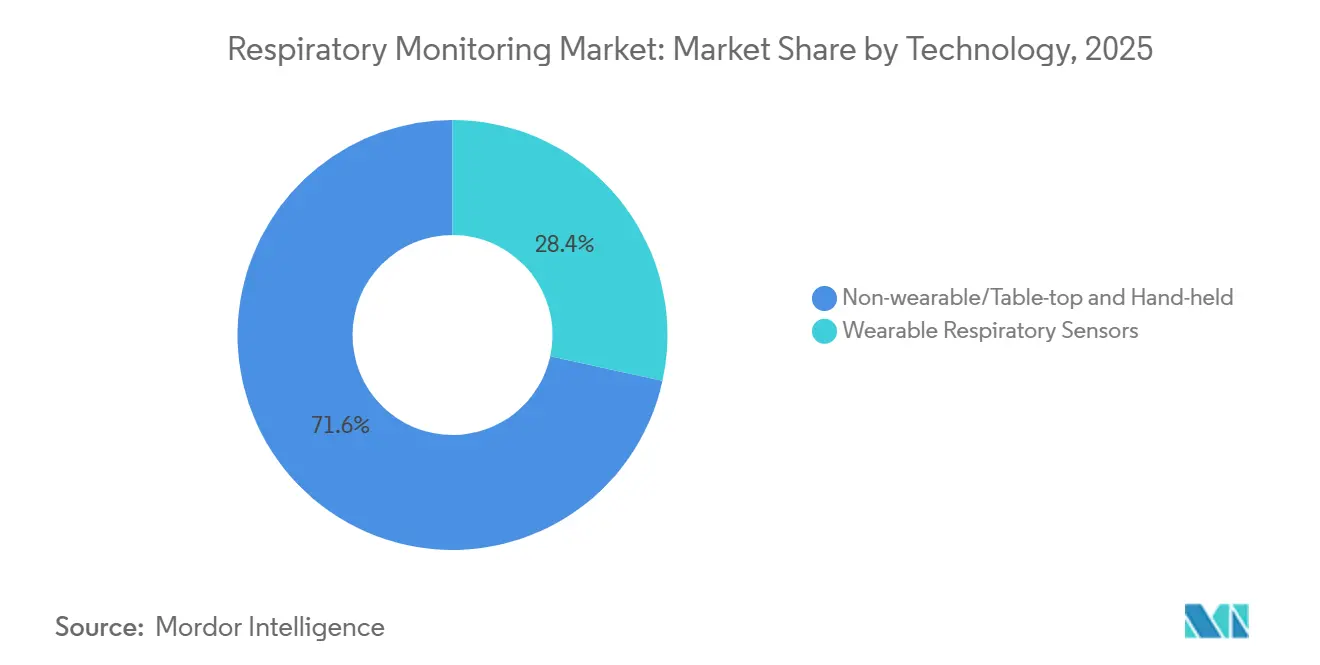

- By technology, wearable sensors captured 19.85% of the respiratory monitoring market size growth trajectory between 2026-2031, outpacing non-wearable platforms.

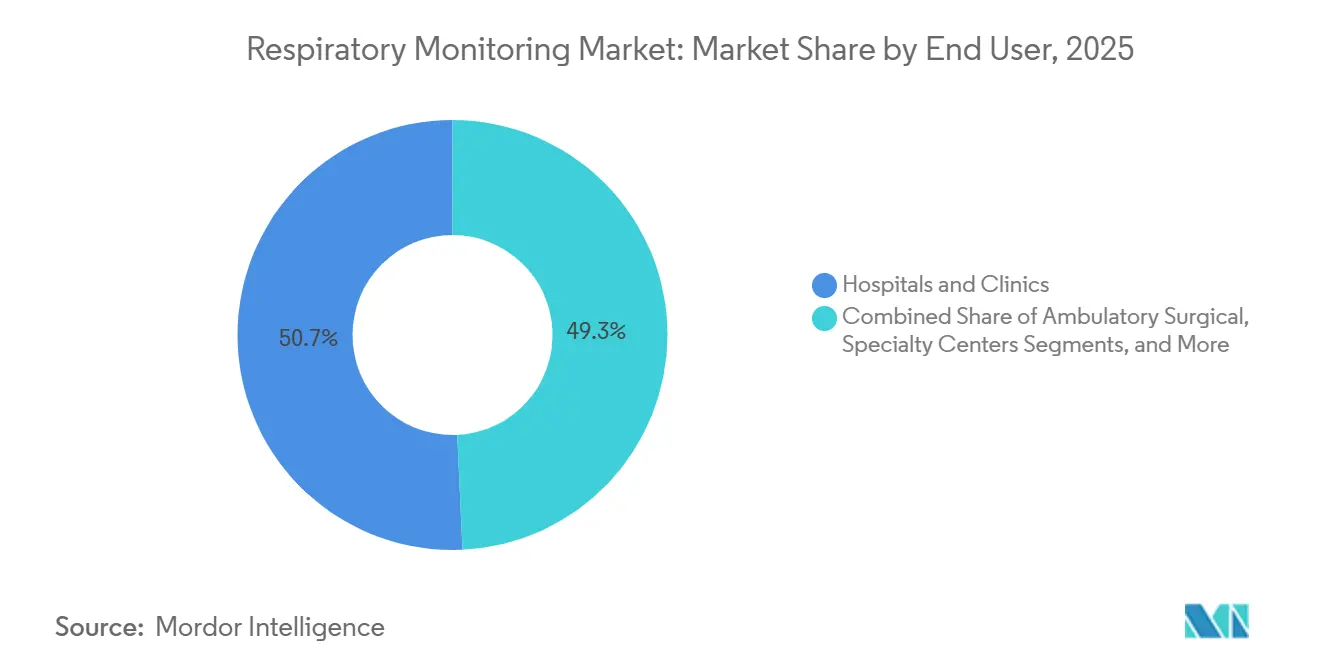

- By end-user, hospitals and clinics held 50.74% revenue share in 2025; the home-care segment is forecast to accelerate at an 8.24% CAGR to 2031.

- By geography, North America dominated with 41.62% market share in 2025, while Asia Pacific is the fastest-growing region, tracking a 14.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Respiratory Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI-powered remote respiratory telemonitoring adoption | +2.1% | Global | Medium term (3-4 yrs) |

| Rise in the number of respiratory diseases | +1.9% | Global | Long term (≥ 5 yrs) |

| Rise of smartphone-based spirometry apps and advanced technologies | +1.3% | Emerging markets & Global | Medium term (3-4 yrs) |

| High prevalence of tobacco smoking | +0.8% | APAC core, spill-over to Eastern Europe | Long term (≥ 5 yrs) |

| Government-funded neonatal respiratory screening programs across Nordic nations | +0.5% | Nordic nations | Short term (≤ 2 yrs) |

| Stringent workplace safety mandates accelerating continuous respiratory monitoring in industrial settings | +0.7% | North America & EU industrial hubs | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Surge in AI-Powered Remote Respiratory Telemonitoring Adoption

The respiratory monitoring market is transforming as AI analytics migrate from research labs into commercial platforms that process breath sounds, flow rates, and oxygen saturation in real time. An Annals of Family Medicine study showed AI-enabled home stethoscopes identifying pediatric asthma flare-ups with 93.2% accuracy.[1]Emeryk A., “Home Stethoscope Accuracy in Asthma Exacerbation Detection,” Annals of Family Medicine, annfammed.org Algorithms trained on longitudinal data sets now detect subtle pattern deviations that precede COPD exacerbation, prompting earlier therapy adjustments and reducing emergency department utilization. Hospitals are integrating these predictive dashboards into electronic health records so that care teams receive automated alerts flagged by clinical severity scores. Vendors are likewise embedding federated-learning techniques that anonymize data at the edge, addressing privacy mandates without sacrificing insight quality. For pediatric and geriatric cohorts who struggle with active self-reporting, passive AI listening systems offer a less burdensome alternative to conventional spirometry.

Rise in the Number of Respiratory Diseases

Global COPD and asthma prevalence are climbing, with chronic respiratory disorders ranking among the top five causes of disability-adjusted life years in 2025. Payers are linking reimbursement bonuses to documented reductions in hospital readmissions, pushing providers to adopt continuous monitoring pathways. The respiratory monitoring market is answering with multi-parameter devices that combine oximetry, airflow, and acoustic analytics to catch inflammatory events sooner than symptom-based escalation models. Caltech’s EBCare mask, which detects nitrite in exhaled breath condensate, exemplifies how biomarker sensing is moving from bench to bedside.[2]Yadollahi A., “Smart Mask for Breath Biomarker Monitoring,” California Institute of Technology, caltech.edu Pulmonologists now embed wearable data into risk-stratification algorithms that dynamically adjust inhaled corticosteroid dosage, demonstrating measurable declines in acute care visits. Governments in high-burden countries are launching public procurement schemes to subsidize remote monitoring kits for COPD patients, ensuring earlier intervention and easing tertiary-care loads.

Rise of Smartphone-Based Spirometry Apps Driving Early COPD Detection

Do-it-yourself spirometry apps reposition everyday smartphones as pulmonary diagnostics tools, extending reach into primary-care clinics and rural communities. Microphone-based flow estimation and AI correction for sub-optimal technique yield FEV1 accuracy within ±6% of clinical spirometers, closing the reliability gap. In the respiratory monitoring market, such apps enable community health workers to triage symptomatic smokers and refer only high-risk individuals for specialist evaluation. Developers now integrate cloud-based dashboards that compare user trends against anonymized cohorts to flag abnormal decline rates. Partnerships with national lung foundations are accelerating distribution through public-health campaigns targeting early COPD detection, especially across Southeast Asia where physician density is low. Scalability and sub-USD 10 per test cost profiles differentiate smartphone spirometry from traditional equipment, amplifying its appeal for budget-constrained systems.

High Prevalence of Tobacco Smoking

Roughly 1.2 billion people worldwide continue to smoke, sustaining the pipeline of COPD and malignancy cases despite aggressive cessation drives. Recognizing this persistent exposure, payers are underwriting annual screening programs anchored by home oximetry and breath-analysis kits. The respiratory monitoring market is witnessing specialized algorithms that parse subtle nocturnal desaturation episodes often an early sign of smoking-induced airway remodeling. Employers operating wellness programs are bulk-purchasing connected oximeters to monitor high-risk staff, linking compliance incentives to longitudinal trend improvements. Device makers are adding behavioral nudges such as real-time carbon monoxide equivalents on companion apps to reinforce cessation goals. This blend of physiology tracking and behavioral science aims to curtail downstream severity and associated system costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval processes | -1.4% | United States & Europe | Medium term (3-4 yrs) |

| High price of advanced monitoring devices | -1.1% | Emerging markets | Short term (≤ 2 yrs) |

| Supply-chain bottlenecks for micro-optical sensors driving device backlogs | -0.6% | Global | Short term (≤ 2 yrs) |

| High calibration-frequency requirement limiting wearable gas analyzer acceptance in pediatric care | -0.5% | North America & EU pediatric centers | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval

Post-recall turbulence has intensified FDA scrutiny, elevating respiratory monitoring devices to the forefront of safety oversight. Class II devices must now submit expanded bench testing and post-market surveillance protocols under updated 510(k) guidance.[3]U.S. Food and Drug Administration, “Consent Decree of Permanent Injunction Against Philips Respironics,” fda.gov The 2024 consent decree against Philips Respironics underscores the financial and reputational stakes of non-compliance. Consequently, small innovators face protracted validation cycles that strain capital reserves and delay revenue realization. To mitigate risk, venture investors are channeling funds toward start-ups that embed quality-by-design documentation from the prototype phase onward. Some manufacturers are pursuing Breakthrough Device designation to accelerate review, though the evidence burden remains significant. In Europe, alignment with the Medical Device Regulation has likewise raised documentary thresholds, adding translation and notified-body costs that pinch margins.

High Price of the Monitoring Devices

AI-enabled wearables often exceed USD 400 per unit at launch, limiting adoption in middle-income regions. Component shortages have inflated sensor prices, and proprietary analytics engines attract premium licensing fees. Health ministries in South Asia cite device cost as the primary barrier to nationwide remote-monitoring rollouts. Vendors are experimenting with stripped-down feature sets tailored to single-parameter measurement, bringing unit costs below USD 150 to meet tender thresholds. Tiered subscription models that bundle hardware leasing with cloud analytics spread capital outlays over multi-year periods, improving affordability for cash-strapped providers. Nevertheless, inconsistent reimbursement frameworks mean return-on-investment remains uncertain in several jurisdictions, tempering uptake in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Pulse Oximeters Sustain Leadership While Capnographs Accelerate

Pulse oximeters contributed 36.62% to the respiratory monitoring market share in 2025 and are projected to maintain the largest revenue pool through 2031 due to their essential status across surgical, critical-care, and ambulatory settings. Their universal applicability, non-invasive design, and established reimbursement paths underpin durable demand. The segment’s innovation pipeline centers on multispectral sensors that capture perfusion index and respiratory rate, alongside SpO2, adding clinical value without disrupting workflow. Vendors are also rolling out Bluetooth-enabled fingertip models that auto-transmit data to hospital EMRs, improving continuous ward surveillance.

Capnographs, although representing a smaller share, exhibit the highest forecast CAGR at 8.54%, driven by broader application beyond operating rooms. Emergency departments now deploy compact mainstream sensors for rapid airway assessment during resuscitation, while procedural sedation suites rely on capnography to flag hypoventilation earlier than pulse oximetry. Portable sidestream units sized for ambulances are extending monitoring into pre-hospital environments, a capability increasingly mandated in advanced life-support protocols. The respiratory monitoring market is consequently witnessing bundled sales packages that combine oximetry and capnography modules, offering a holistic respiratory profile in trauma settings.

By Technology: Wearables Redefine Monitoring Paradigms

Non-wearable platforms retained 71.58% value share in 2025, owing to front-line placement within high-acuity wards and operating theaters. However, wearable sensors are forecast to grow at a 19.85% CAGR, which dwarfs legacy formats. Adoption hinges on comfort-optimized form factors such as adhesive patches, smart clothing, and acoustic resonance stickers that collect minute-by-minute data without hindering mobility. The Sylvee device exemplifies how acoustic resonance analyzes trapped air, granting COPD patients an early warning signal of impending exacerbation.

Second-generation wearables integrate inertial measurement units with bioimpedance coils to estimate tidal volume, overcoming the limitations of accelerometer-only designs. Cloud algorithms refine artifact rejection, ensuring reliable trend lines even during physical activity. Researchers are integrating environmental telemetry, pollen counts, and particulate matter to contextualize symptom fluctuations, enabling clinicians to isolate trigger patterns. These advances reinforce wearables as the cornerstone of future remote-first respiratory monitoring models.

By End-User: Home-Care Settings Gain Momentum

Hospitals and clinics gained a 50.74% market share in 2025, driven by the critical-care dependence on continuous ventilation surveillance. Yet, policy momentum toward value-based care injects urgency into de-hospitalizing chronic disease management. Home-care settings are expected to capture a rising proportion of the respiratory monitoring market, recording an 8.24% CAGR through 2031, driven by payer coverage expansions for remote physiologic monitoring codes. Devices now ship with guided setup apps and auto-calibration routines, reducing the need for technical support visits and easing the caregiver burden.

Telehealth platforms integrate live clinician dashboards that triage alerts based on AI-scored severity, minimizing alarm fatigue. The FDA’s “Home as a Health Care Hub” initiative validates this decentralization by outlining interoperability standards for home devices, bolstering provider confidence in data integrity. Insurers are bundling respiratory monitoring with virtual pulmonary-rehabilitation sessions, demonstrating improved adherence and fewer acute events in pilot programs. Over time, the convergence of reimbursement, patient preference, and technological maturity is expected to tilt unit volumes decisively toward the home environment.

Geography Analysis

North America accounted for 41.62% of global revenue in 2025, reflecting robust payer reimbursement, entrenched telemedicine infrastructure, and a COPD prevalence nearing 6.3% of adults. The respiratory monitoring market in the United States benefits from the FDA Breakthrough Device Program, which accelerates AI-driven solutions such as predictive capnography algorithms for sepsis-screened ICU patients. Academic-industry collaborations, like the 2025 Philips–Mass General Brigham partnership, channel large real-world data pools into refined clinical-decision rules that elevate device utility. Canada, incentivizing home oxygen therapy cost offsets, is piloting nationwide oximetry tracking networks that feed provincial analytics hubs.

In Europe, National Health Service procurement frameworks favor devices with proven cost-avoidance outcomes, encouraging vendors to supply structured health-economic dossiers. Germany’s DIGA pathway, allowing prescription of digital health applications, has added four respiratory apps since 2024, boosting physician confidence in smartphone spirometry. The European respiratory monitoring market is also shaped by the Medical Device Regulation’s post-market surveillance demands, prompting manufacturers to pre-package long-term warranty upgrades that align with mandatory vigilance reporting.

Asia Pacific exhibits the fastest expansion, logging a 14.01% CAGR as urbanization, air-quality deterioration, and smoking prevalence converge to swell respiratory caseloads. China and India collectively imported over 3 million handheld oximeters in 2024, yet domestic production capacity is scaling rapidly with government incentives for med-tech self-reliance. Local start-ups leverage cost-efficient printed electronics to create sub-USD 50 sensors, democratizing access across tier-2 cities. In Japan, a rapidly aging population is driving the adoption of AI-augmented cough monitors integrated into smart speakers, offering unobtrusive elder-care oversight. Australia’s remote Indigenous communities benefit from satellite-enabled wearables that transmit lung function metrics to metropolitan pulmonology teams, bridging the tyranny of distance.

Competitive Landscape

The respiratory monitoring market features moderate concentration as legacy conglomerates and venture-fueled disruptors vie for share. Philips, Medtronic, and ResMed collectively hold a majority of share, deploying expansive service networks that hard-wire customers into multi-year maintenance cycles. Their strategies increasingly emphasize holistic ecosystems—combining bedside hardware, analytics dashboards, and cloud-based population-health modules—to boost recurring software revenue.

Mid-tier entrants exploit white spaces by targeting disease-specific niches such as transplant candidates or pediatric asthma sufferers. Seed-funded firms are integrating organic electrochemical transistors into textiles, delivering breathing-rate garments that withstand industrial wash cycles. Several have secured distribution alliances with durable medical equipment suppliers to bypass capital-heavy direct-sales models, accelerating market penetration.

Data security and interoperability emerge as competitive differentiators. Players obtaining ISO/IEC 27001 certification signal rigorous information-security governance, reassuring hospital CIOs amid rising cyber-attack frequencies. Platforms conforming to HL7 FHIR unlock seamless EMR integration, shortening deployment cycles. Strategic acquisitions are intensifying: Medtronic’s 2024 purchase of a cloud analytics start-up added AI anomaly-detection tools that now underpin its ventilator fleet management portal. Such consolidation is expected to continue as incumbents reinforce technology portfolios and defend share.

Respiratory Monitoring Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

GE Healthcare

Masimo Corporation

Vyaire Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Philips and Mass General Brigham launched a collaboration to unify ventilator and monitor telemetry within an AI-enabled analytics layer aimed at improving patient-safety curves and throughput efficiency.

- September 2024: Philips installed energy-efficient monitoring fleets at Jackson Health System, cutting monitor-related carbon emissions by 47 % and eliminating roughly 420 000 disposable batteries.

- June 2024: Respira Labs introduced Sylvee, a wearable acoustic-resonance sensor that transmits lung-air-entrapment data to smartphones, facilitating proactive COPD management.

- February 2024: ResMed rolled out the AirCurve 11 bilevel positive-airway-pressure line, integrating cellular telemetry for cloud compliance reporting.

- May 2024: Researchers published results for a 3-D-printed magnetic air-pressure sensor designed for continuous breathing rehabilitation, demonstrating additive manufacturing’s readiness for clinical-grade components.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the respiratory monitoring market as the total value of devices that continuously or periodically assess pulmonary function, such as spirometers, capnographs, pulse oximeters, peak-flow meters, sleep test systems, and allied wearable sensors, across hospital, ambulatory, and home settings worldwide. According to Mordor Intelligence, figures are presented in USD and reflect manufacturer sales plus standard distributor margins realized in seventeen major nations.

Scope exclusion: Therapeutic ventilators, oxygen concentrators, drug-delivery inhalers, and purely diagnostic imaging systems fall outside this sizing.

Segmentation Overview

- By Device Type

- Spirometers

- Peak Flow Meters

- Sleep Test Devices (Polysomnographs)

- Gas Analyzers

- Pulse Oximeters

- Capnographs

- Other Monitoring Devices

- By Technology

- Wearable Respiratory Sensors

- Non-wearable/Table-top & Hand-held Devices

- By End-user

- Hospitals & Clinics

- Home-care Settings

- Ambulatory Surgical & Specialty Centers

- Emergency Medical Services & Field Use

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed respiratory therapists, biomedical engineers, procurement officers, and telehealth executives across North America, Europe, and Asia Pacific. Their input refined penetration rates for home-use oximeters, validated replacement cycles for table-top spirometers, and confirmed emerging interest in cloud-linked wearable patches.

Desk Research

Our analysts began with public datasets from authorities such as the World Health Organization, the Global Burden of Disease database, and the OECD health statistics that track COPD and asthma prevalence, since these conditions dictate device demand. Trade bodies, including the Medical Device Manufacturers Association and the European Respiratory Society, offered shipment, ASP, and installed-base updates. Company 10-Ks, FDA 510(k) filings, and recent peer-reviewed articles on capnography accuracy supplied price corridors and technology adoption curves. Paid intelligence from D&B Hoovers and Dow Jones Factiva supplemented supplier revenue splits and news on product launches. The secondary source list is illustrative, not exhaustive, and many additional references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down construct starts with national production and import-export data to rebuild the global demand pool, which is then cross-checked through selective bottom-up roll-ups of leading suppliers and channel audits. Key variables, including COPD prevalence shifts, average selling price movements of handheld spirometers, hospital bed additions, sleep-apnea screening guidelines, and home-care insurance coverage, drive annual value calculations. Multivariate regression links those drivers to recent sales and projects market value through 2030, while scenario analysis tests high-pollution and reimbursement-tightening cases. Gaps from limited country data are bridged by region-specific proxy indicators, after which outputs are nudged to align with insights gathered from specialist interviews and distributor surveys.

Data Validation & Update Cycle

Every model run passes variance checks against historical sales, import manifests, and patented-device counts before senior review. Our reports refresh once a year, with interim updates when recalls, reimbursement shifts, or large tenders materially alter the outlook. A final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Respiratory Monitoring Baseline Commands Reliability

Published estimates often diverge because firms choose wider or narrower device baskets, mix sell-in with sell-out pricing, or apply stale epidemiology. Our disciplined scoping, yearly refresh cadence, and driver-level cross-checks keep the baseline firmly anchored.

Key Gap Drivers include whether ancillary therapeutic hardware is bundled, how home-care wearables are treated, and the rigor applied to adjusting ASP inflation. Some publishers extend scope to ventilators, inflating totals, whereas others confine sizing to laboratory equipment and undercount fast-growing consumer segments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.03 B | Mordor Intelligence | - |

| USD 23.6 B | Global Consultancy A | Bundles therapeutic and diagnostic devices; limited device-level price validation; biennial refresh |

| USD 1.81 B | Industry Data Firm B | Focuses on hospital units only; omits wearable and home-care sensors; restricted geography |

The comparison shows that over-broad or ultra-narrow scopes swing values drastically. By selecting a clinically relevant device set, grounding variables in verifiable datasets, and revisiting assumptions each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the respiratory monitoring market?

The respiratory monitoring market stands at USD 13.36 billion in 2026 and is on course to hit USD 22.59 billion by 2031.

Which device segment holds the largest share of the respiratory monitoring market?

Pulse oximeters lead with 36.62% share in 2025 due to their universal role in oxygen saturation tracking.

Why are wearable sensors growing so quickly?

Wearables deliver continuous, unobtrusive data outside clinical settings and are forecast to grow at 19.85% CAGR to 2031.

How does regulatory scrutiny impact market growth?

Tougher FDA and EU regulations lengthen approval times and add compliance costs, trimming the overall CAGR by about 1.4%.

Which region is expanding fastest?

Asia Pacific posts a 14.01% CAGR, driven by rising chronic respiratory disease incidence and improving healthcare infrastructure.

Page last updated on: