Continuous Positive Airway Pressure Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

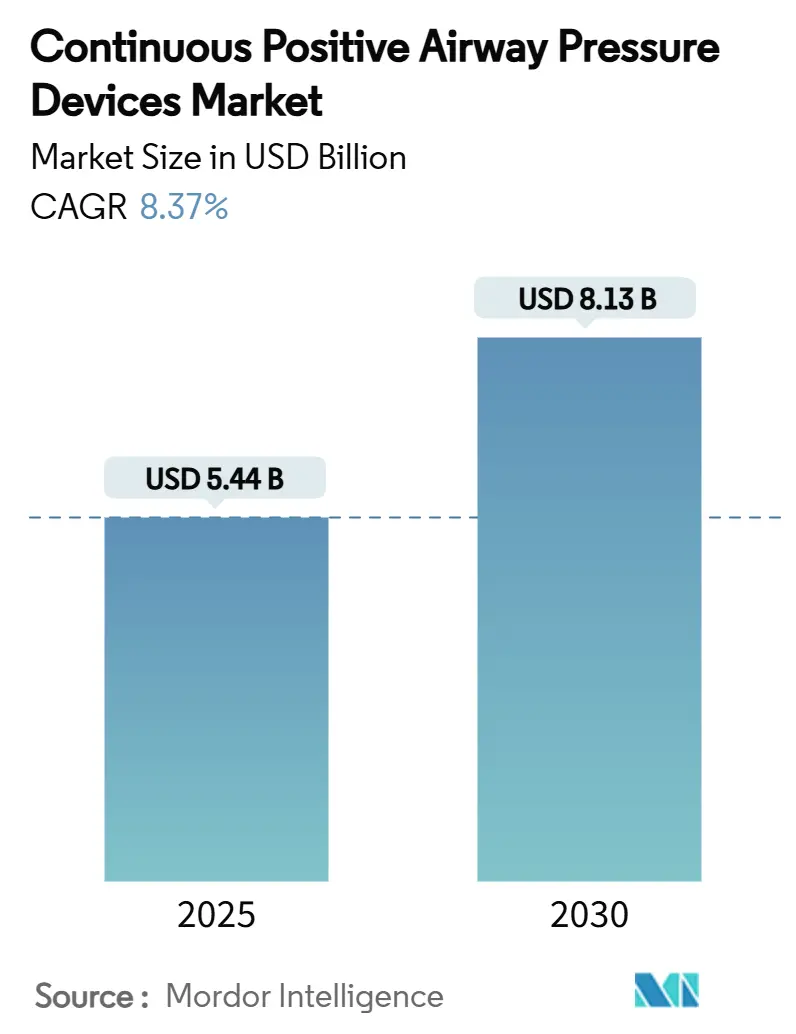

| Market Size (2025) | USD 5.44 Billion |

| Market Size (2030) | USD 8.13 Billion |

| Growth Rate (2025 - 2030) | 8.37% CAGR |

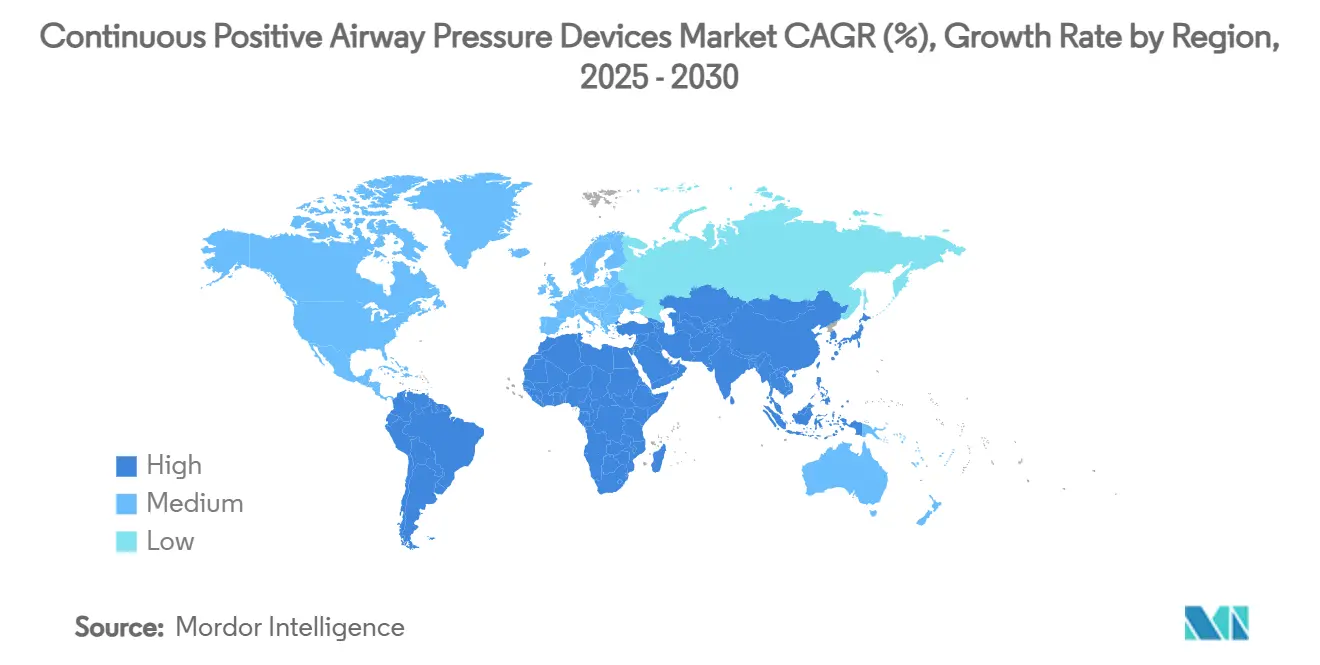

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuous Positive Airway Pressure Devices Market Analysis by Mordor Intelligence

The continuous positive airway pressure devices market size is valued at USD 5.44 billion in 2025 and is forecast to reach USD 8.13 billion by 2030, progressing at an 8.37% CAGR during the period. Robust demand stems from rising obstructive sleep apnea (OSA) prevalence, the pivot toward home-based care, and AI-enabled adherence platforms that raise nightly usage. North America retains leadership thanks to strong reimbursement and mature distribution, while rapid obesity growth and expanding middle-class populations lift Asia-Pacific demand at a double-digit pace. Comfort-oriented low-pressure algorithms, expanding employer-sponsored sleep health programs, and broader payer coverage are widening the treatment funnel. Meanwhile, persistent patient non-adherence, device recalls, and European Union Medical Device Regulation (MDR) bottlenecks temper growth momentum.

Key Report Takeaways

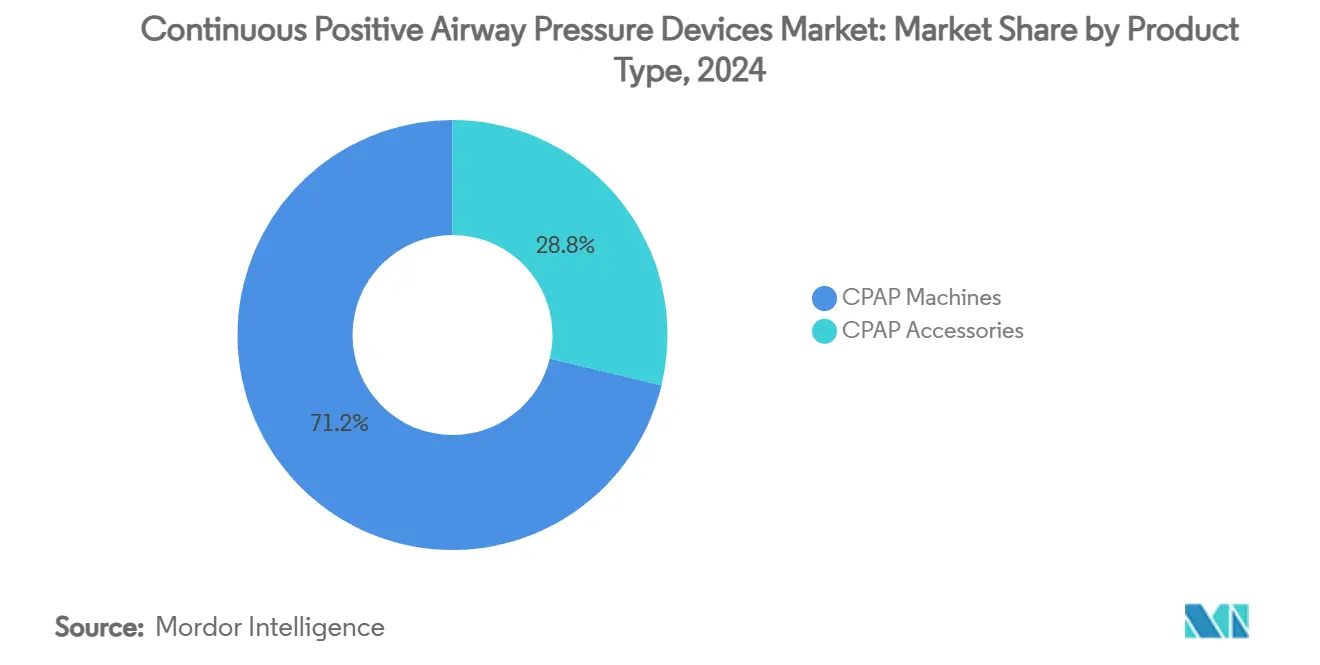

- By product type, CPAP machines led with 71.23% revenue share in 2024, while accessories are projected to advance at an 11.45% CAGR through 2030.

- By interface type, nasal masks held 41.23% of the continuous positive airway pressure devices market share in 2024, whereas nasal pillow masks are on track for a 12.37% CAGR to 2030.

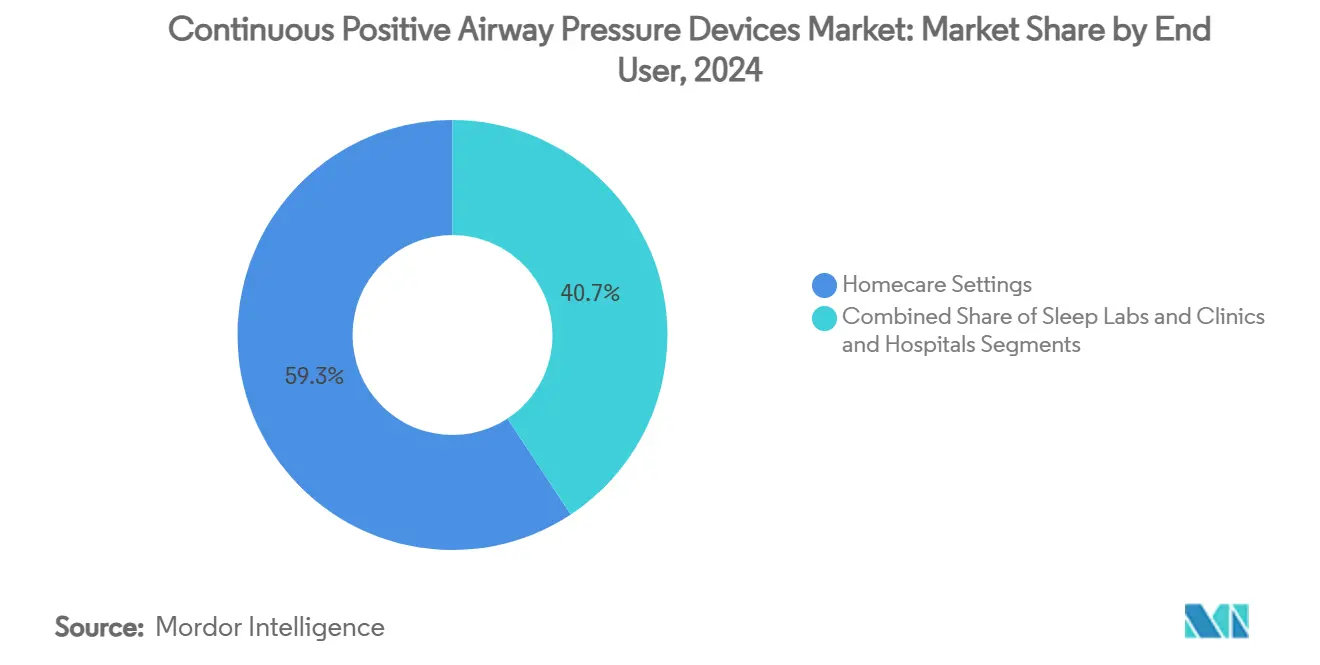

- By end user, homecare settings accounted for 59.27% share of the continuous positive airway pressure devices market size in 2024 and are expanding at an 11.74% CAGR over the forecast horizon.

- By distribution channel, medical equipment distributors commanded 61.23% revenue share in 2024, while direct-to-consumer online sales are forecast to grow at a 12.78% CAGR through 2030.

- By geography, North America dominated with 44.32% revenue share in 2024; Asia-Pacific exhibits the fastest growth at a 10.56% CAGR to 2030.

Global Continuous Positive Airway Pressure Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising OSA Prevalence & Obesity Burden | +2.1% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Growing Shift Toward Home-Based Sleep Therapy | +1.8% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Reimbursement Expansion For PAP Devices | +1.5% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| AI-Driven Adherence Platforms Boost Compliance | +1.2% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Adoption Of Low-Pressure Comfort Algorithms | +0.9% | Global, technology-driven adoption | Short term (≤ 2 years) |

| Employer-Sponsored Sleep-Health Programs | +0.7% | North America, expanding to Europe & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising OSA Prevalence and Obesity Burden

Roughly 936 million adults live with OSA worldwide, and prevalence in the United States alone is set to climb 26.7% for adults aged 30-70 by 2050. Growing visceral adiposity strengthens disease severity links, lifting long-term device demand. The untreated OSA economic toll in the country already reaches USD 150 billion annually, intensifying health-system focus on early therapy.[1]Antonino Maniaci, “The Global Burden of Obstructive Sleep Apnea,” MDPI, mdpi.com Source: American Academy of Sleep Medicine staff, “Economic Burden of Undiagnosed Sleep Apnea in US Is Nearly USD 150 Billion Per Year,” sciencedaily.com Climate change may further raise global OSA prevalence by 45% this century, potentially doubling demand for continuous positive airway pressure devices market therapies.[2]Danny J. Eckert, “Global Warming May Increase the Burden of Obstructive Sleep Apnea,” Nature Communications, nature.com These converging pressures make OSA management a public-health priority, sustaining market growth.

Growing Shift Toward Home-Based Sleep Therapy

More care is moving into the home as patients favor convenience and payers seek lower costs. Connected platforms such as ResMed’s AirView allow remote monitoring that improves nightly usage and reduces clinic visits. FDA clearance of home sleep apnea tests streamlines diagnosis, shortening time to treatment initiation. Predictive analytics now alert clinicians to lapses before non-adherence sets in, boosting engagement. This home-centric delivery reshapes the continuous positive airway pressure devices market by pairing hardware sales with digital support.

Reimbursement Expansion for PAP Devices

Medicare and large private insurers recently broadened coverage to include auto-adjusting CPAP and bilevel devices, along with oral appliances meeting defined indices. New HCPCS codes effective July 2025 simplify durable medical equipment billing. These moves lower out-of-pocket costs, expanding eligibility and accelerating prescription volumes—especially important in markets where price sensitivity restricts adoption.

AI-Driven Adherence Platforms Boost Compliance

Machine-learning tools now predict and prevent therapy dropout. Linde’s AIRGENIOUS platform identifies compliance risks and recommends personalized interventions, while startups such as NovaResp secure investment to refine algorithmic coaching. Early trials show higher nightly usage and longer retention, directly addressing the prime obstacle to sustained CPAP use and energizing the continuous positive airway pressure devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Patient Non-Adherence To CPAP | -1.4% | Global, with higher impact in developing markets | Long term (≥ 4 years) |

| Supply-Chain Recalls & Quality-Control Issues | -1.1% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Grey-Market Imports Undercut Pricing | -0.8% | Emerging markets, spillover to developed regions | Medium term (2-4 years) |

| Pending EU MDR Re-Certification Bottlenecks | -0.6% | Europe, with secondary effects on global supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Patient Non-Adherence to CPAP

Despite better masks and coaching apps, adherence ranges from 35-65%. Up to half of new users abandon therapy within a year, mainly due to discomfort and lifestyle disruption. Popular interest in GLP-1 weight-loss drugs and neurostimulation implants offers alternatives that could siphon potential users. Unless comfort advances outpace these options, non-adherence will restrain the continuous positive airway pressure devices market.

Supply-Chain Recalls and Quality-Control Issues

The Philips Respironics recall covering 15 million units disrupted global supply, intensified FDA scrutiny, and raised patient safety anxiety.[3]U.S. Food and Drug Administration staff, “CDRH Provides Update on Philips June 2021 Recall,” fda.gov Subsequent magnet-related mask recalls from multiple vendors highlight industry-wide quality gaps. Recertification delays under EU MDR further slow new product flow into Europe. Compliance investments, inventory write-offs, and brand erosion weigh on profitability and near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accessories Propel Growth Beyond Core Devices

The CPAP machines segment commanded 71.23% of the continuous positive airway pressure devices market share in 2024, reflecting its position as the primary therapy channel for newly diagnosed patients. Fixed-pressure machines remain a widely prescribed entry option, yet auto-adjusting models are gaining ground among clinicians seeking individualized pressure delivery that minimizes residual apnea events. Bi-level PAP devices retain a specialized role in complex respiratory cases, supporting a stable but comparatively small revenue base.

Accessories are reshaping value capture as patients upgrade comfort and hygiene components, driving an 11.45% CAGR through 2030. Heated humidifiers reduce nasal dryness, antimicrobial tubing limits bacterial growth, and smart filters integrate usage analytics, turning previously commoditized parts into recurring revenue streams. FDA clearance of sanitation devices such as SoClean 3+ reinforces patient focus on maintenance, while connectivity modules create upsell paths for software subscriptions and real-time coaching. The continuous positive airway pressure devices market increasingly rewards brands that offer integrated ecosystems rather than isolated hardware, positioning accessories as a strategic growth lever over the forecast horizon.

By Interface Type: Nasal Pillow Momentum Challenges Traditional Masks

Nasal masks remained the most used interface in 2024, supported by a 41.23% revenue contribution to the continuous positive airway pressure devices market. Their balanced footprint delivers reliable seal performance for a broad patient cohort, keeping them the default clinical choice for first-line fittings. Full-face masks serve mouth-breathing users and individuals with chronic congestion, whereas oral or hybrid designs fill specific anatomical niches and remain a small yet innovative category.

Nasal pillow masks are advancing at a 12.37% CAGR through 2030 on the promise of minimal contact and reduced claustrophobia, evidenced by launches such as Fisher & Paykel’s Nova Micro, the firm’s smallest and lightest model. Slimmer headgear also eliminates magnetic clips, addressing recent safety recalls linked to implant interference. Interface suppliers invest in softer silicone blends, variable-thickness cushions, and dynamic venting to curb noise and facial marks. As comfort directly correlates with nightly usage, interface evolution remains central to sustaining adherence and expanding the continuous positive airway pressure devices market.

By End User: Homecare Dominance Accelerates Through Digital Integration

Homecare settings accounted for 59.27% of revenue from the continuous positive airway pressure devices market size in 2024 and are expanding at an 11.74% CAGR to 2030. Payors prefer domiciliary therapy for its lower cost compared with institutional care, while patients value flexibility and privacy. Growth also benefits from the wider availability of telehealth prescriptions that shorten the path from diagnosis to first-night therapy.

Connected platforms such as ResMed’s AirView pair real-time data with predictive analytics, letting clinicians intervene early when usage drops and thereby curbing attrition. Sleep labs and clinics still anchor diagnostic polysomnography and titration, yet many now bundle remote monitoring services to stay relevant in a home-centric model. Hospitals focus on complex comorbid cases where continuous observation is required. This blended ecosystem underlines how digital oversight reinforces the continuous positive airway pressure devices industry by merging clinical rigor with patient-led environments.

By Distribution Channel: Online Direct Sales Reshape Traditional Supply Chains

Medical equipment distributors retained 61.23% of 2024 revenue, reflecting entrenched relationships with payors and providers that simplify reimbursement workflows. Their services include in-home setup, mask fitting, and periodic compliance reporting, roles that sustain relevance despite shifting purchase behaviors. Wholesale scale also supports inventory buffering during recall-driven shortages, keeping therapy pipelines open for large health systems.

Direct-to-consumer online channels are growing at a 12.78% CAGR, lifting the continuous positive airway pressure devices market size for e-commerce platforms that offer self-service replenishment and subscription bundles. Telehealth integration allows digital storefronts to issue prescriptions, match patients with compatible masks, and push firmware updates remotely. Transparent pricing and doorstep delivery attract technology-savvy users, while data-sharing agreements enable manufacturers to harvest real-world evidence on comfort preferences and failure points. As digital convenience redefines expectations, hybrid models that blend clinical support with online ordering will likely dominate distribution strategy over the forecast window.

Geography Analysis

North America accounted for 44.32% of 2024 revenue and continues to generate high per-patient spending under favorable insurance coverage and strong physician awareness. Device replacement demand following large recalls and steady obesity rates sustain unit volumes.

Europe represents a mature reimbursement environment but faces MDR recertification backlogs that could constrain near-term launches. Conditional CE proposals may relieve pressure, yet compliance costs prompt some producers to prioritize the United States.

Asia-Pacific is the fastest growing continuous positive airway pressure devices market, advancing at a 10.56% CAGR as rising disposable income, urban lifestyles, and higher obesity prevalence drive diagnosis and therapy adoption. Japan exhibits notable comorbidity overlap between asthma and OSA, highlighting latent demand, while China and India invest in sleep health infrastructure and local manufacturing. Government insurance expansion also lifts unit affordability.

Middle East and Africa along with South America show early-stage adoption. Growing private insurance coverage and public-health awareness campaigns improve diagnosis rates, creating long-term upside for multinational and domestic vendors.

Competitive Landscape

The market remains moderately consolidated. ResMed and Philips anchor global supply, although Philips’ recall-related headwinds open share opportunities for Fisher & Paykel, Inspire Medical Systems, and agile AI-driven entrants. Differentiation pivots from hardware to integrated digital ecosystems: ResMed commits 7% of revenue to R&D focused on cloud connectivity and predictive analytics.

Start-ups deploy machine learning to personalize therapy and supply replacement schedules, while technology giants test sleep-health features that could funnel users to PAP devices. Concurrently, alternative therapies such as hypoglossal-nerve stimulators gain traction, forcing CPAP leaders to emphasize superior comfort, lower total cost, and seamless digital support.

Strategic actions center on acquisitions that bundle diagnostics, software, and consumables; expanded manufacturing footprints to mitigate supply risk; and partnerships with payers and employers to embed sleep solutions in wellness programs. Regulatory compliance investments rise as FDA and European authorities intensify oversight.

________________________________________

Continuous Positive Airway Pressure Devices Industry Leaders

ResMed Inc.

Koninklijke Philips N.V.

Fisher & Paykel Healthcare Corp

Drive DeVilbiss Healthcare

BMC Medical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ResMed completed the USD VirtuOx acquisition to integrate home sleep testing with therapy platforms.

- November 2024: ResMed unveiled AirSense 11 at its Singapore advanced manufacturing center.

- February 2024: ResMed introduced the AirCurve 11 bilevel series built on the AirSense 11 digital backbone.

Global Continuous Positive Airway Pressure Devices Market Report Scope

| CPAP Machines | Fixed-Pressure CPAP Devices |

| Auto-Adjusting CPAP Devices (APAP) | |

| Bi-Level PAP Devices (BiPAP) | |

| CPAP Accessories | Humidifiers |

| Tubing & Filters |

| Nasal Masks |

| Nasal Pillow Masks |

| Full-Face Masks |

| Oral/Hybrid Masks |

| Homecare Settings |

| Sleep Labs & Clinics |

| Hospitals |

| Direct-to-Consumer (Online) |

| Medical Equipment Distributors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Product Type | CPAP Machines | Fixed-Pressure CPAP Devices |

| Auto-Adjusting CPAP Devices (APAP) | ||

| Bi-Level PAP Devices (BiPAP) | ||

| CPAP Accessories | Humidifiers | |

| Tubing & Filters | ||

| Interface Type | Nasal Masks | |

| Nasal Pillow Masks | ||

| Full-Face Masks | ||

| Oral/Hybrid Masks | ||

| End User | Homecare Settings | |

| Sleep Labs & Clinics | ||

| Hospitals | ||

| by Distribution Channel | Direct-to-Consumer (Online) | |

| Medical Equipment Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current continuous positive airway pressure devices market size?

The market is valued at USD 5.44 billion in 2025, with an 8.37% CAGR projected to lift revenues to USD 8.13 billion by 2030.

2. Which region leads the continuous positive airway pressure devices market?

North America holds the largest revenue share at 44.32% in 2024 due to established reimbursement and high OSA awareness.

3. Why are accessories growing faster than CPAP machines?

Innovations in humidification, filters, and smart connectivity enhance comfort and hygiene, driving an 11.45% CAGR for accessories through 2030.

4. How is AI improving CPAP adherence?

Machine-learning platforms forecast usage drop-offs and deliver personalized coaching, raising nightly usage and reducing long-term abandonment.

5. What challenges threaten market growth?

Patient non-adherence, supply-chain recalls, and European MDR certification delays collectively restrain the otherwise robust growth trajectory.

Page last updated on: