Portable Ventilators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

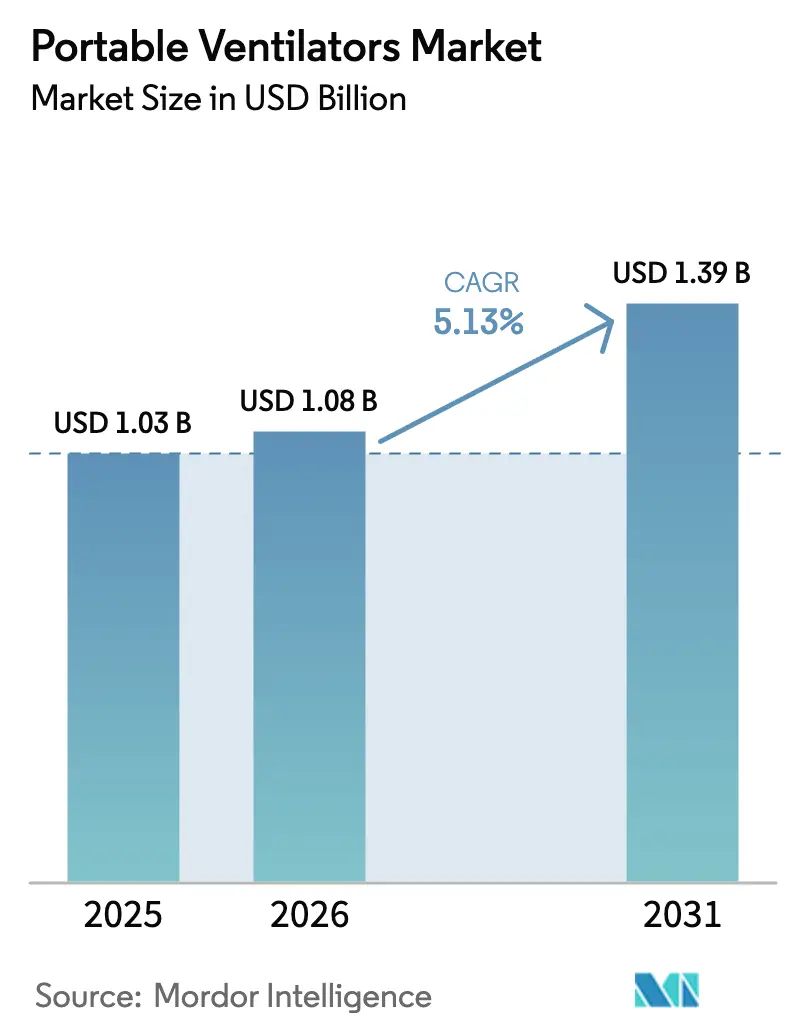

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

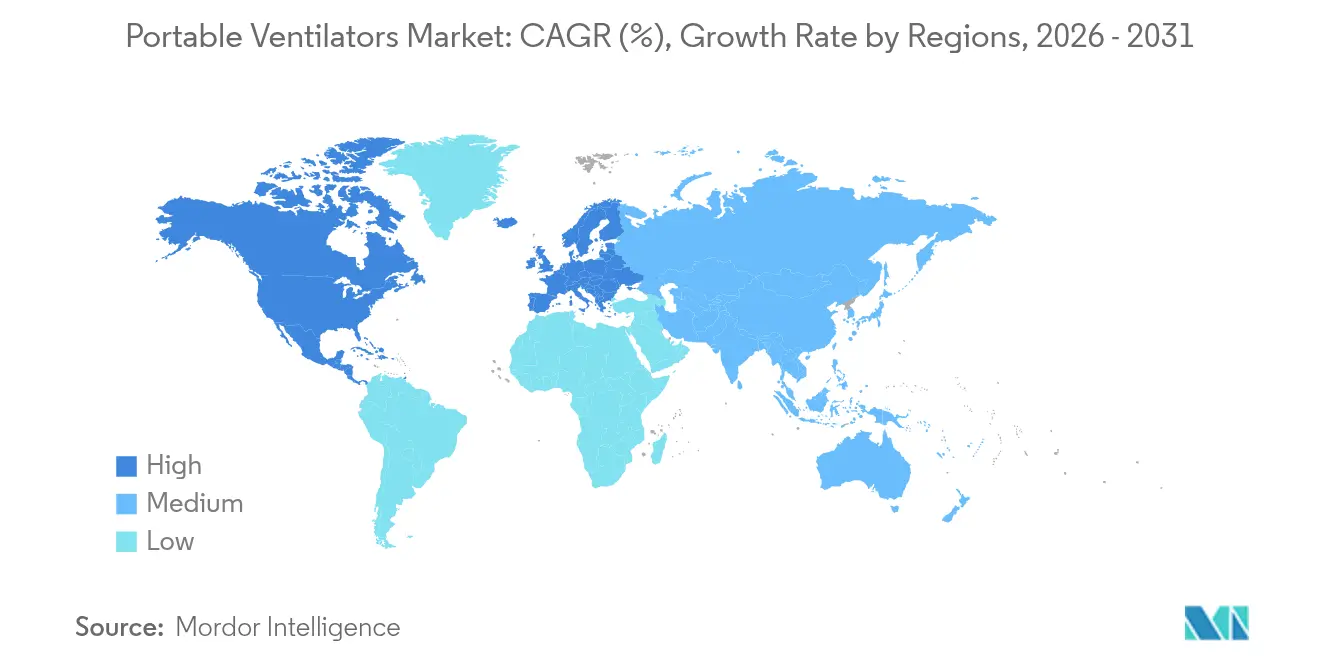

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

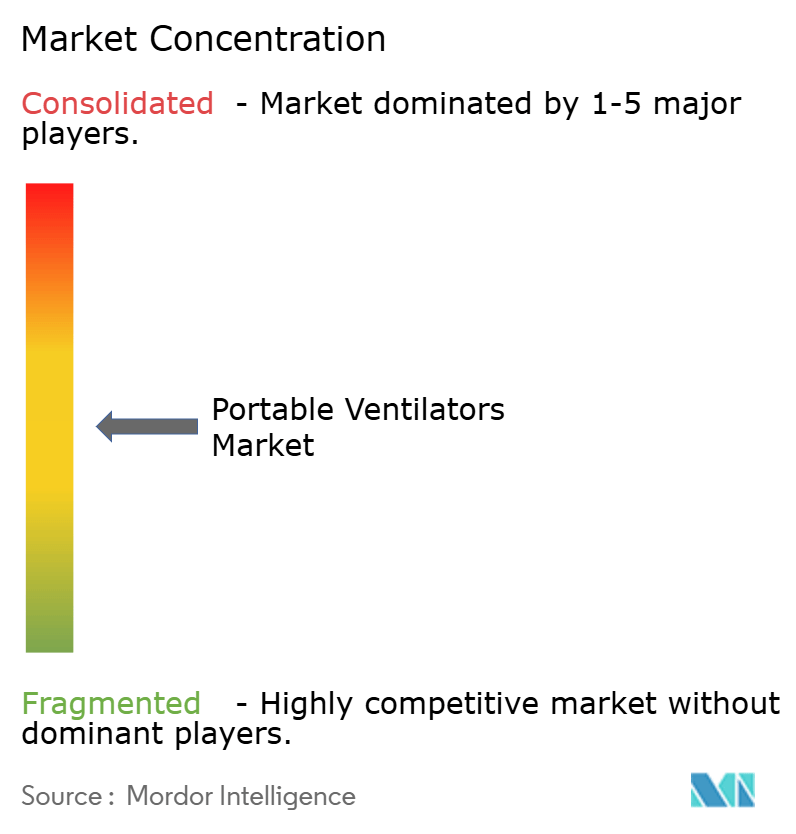

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Ventilators Market Analysis by Mordor Intelligence

The Portable Ventilators market size is expected to grow from USD 1.03 billion in 2025 to USD 1.08 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at 5.13% CAGR over 2026-2031.

The post-pandemic shift from surge procurement to structured investment in home-based and rural emergency care keeps the portable ventilator market on a steady expansion path. Demand remains resilient as chronic respiratory disease management, aging demographics, and uninterrupted emergency readiness reinforce procurement budgets across both developed and emerging health systems. At the same time, battery-efficient turbine platforms, artificial-intelligence-enabled monitoring, and simplified user interfaces lower ownership hurdles for providers. Manufacturers respond by pairing design portability with cloud-connected analytics that help clinicians optimize ventilation parameters and reduce readmissions.

Key Report Takeaways

- By patient type, adult devices held 62.54% of portable ventilator market share in 2025, while neonatal devices are projected to grow the fastest at a 5.63% CAGR through 2031.

- By interface, non-invasive ventilation accounted for 57.74% revenue share of the portable ventilator market in 2025; invasive ventilation is expected to post the highest 5.98% CAGR to 2031.

- By technology, turbine platforms captured 47.96% of portable ventilator market share in 2025 and are forecast to expand at a 5.78% CAGR.

- By end user, hospitals and clinics represented 49.86% of the portable ventilator market in 2025, whereas home-care settings are set to record a 6.05% CAGR up to 2031.

- By geography, North America led with 43.32% share in 2025, yet Asia-Pacific is positioned for the fastest 6.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Portable Ventilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic respiratory disorders | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Increasing geriatric population & COPD incidence | +0.9% | Global, particularly APAC and North America | Long term (≥ 4 years) |

| Legacy COVID-19 preparedness spending | +0.8% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Expansion of home-based respiratory care | +1.1% | Global, with early gains in US, Canada, Germany | Medium term (2-4 years) |

| Rural EMS build-outs in low-income regions | +0.6% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Mini-turbine & battery innovations lowering downtime | +0.7% | Global, with technology leadership in EU & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Respiratory Disorders

Chronic lung ailments such as asthma, COPD, and post-infectious sequelae continue to raise the baseline need for portable ventilatory support. A May 2025 World Health Assembly resolution calls for integrated national lung-health strategies that broaden access to affordable respiratory technologies, giving public purchasers a policy mandate to finance portable systems [1]World Health Organization, “Seventy-eighth World Health Assembly: Resolution on Integrated Lung Health,” who.int. Government programs increasingly bundle preventive screening, air-quality interventions, and mechanical ventilation access into single funding envelopes. Clinical teams value portable units because the devices shorten hospital stays and let stable patients continue therapy at home. Artificial-intelligence prediction tools embedded in modern ventilators personaliz e airflow settings by learning user-specific respiratory patterns, which improves adherence and minimizes exacerbations. Together, these factors keep the portable ventilator market on a supportive demand trajectory.

Increasing Geriatric Population & COPD Incidence

Population aging raises COPD prevalence and heightens the share of patients who require assisted breathing outside hospital walls. ResMed reported high revenue in Q3 2025, attributing gains to higher demand for digitally linked breathing devices, including portable ventilators that synchronize with adherence apps. Medicare is considering broader reimbursement for non-invasive ventilation in chronic COPD, a move that would dilute cost barriers for seniors. Rural hospitals, where mortality among ventilated patients averages 37%, are looking to portable units that ferry patients to tertiary centers while keeping lungs supported. Health planners therefore treat portable ventilators as core enablers of equitable care for older adults with chronic respiratory impairments.

Legacy COVID-19 Preparedness Spending

Governments continue to replenish strategic reserves with portable ventilators that can switch from routine use to field deployment in disasters. The U.S. Strategic National Stockpile keeps models from GE, Hamilton, and Philips on readiness lists and funds clinician training modules for rapid activation [2]U.S. Department of Health and Human Services, “Strategic National Stockpile Overview,” hhs.gov. Supply-chain reviews under the HHS All-Hazards Plan recommend diversified sourcing and local assembly to avert future shortages. Portable units earn procurement preference because they travel easily, can run on battery power, and offer dual functionality for daily care and crisis surge. Such preparedness budgets smooth revenue visibility for manufacturers even as acute pandemic demand ebbs.

Expansion of Home-Based Respiratory Care

Care is shifting out of hospitals to reduce costs and match patient preferences. VieMed Healthcare generated 35% revenue growth in 2023, with 58% stemming from ventilator services delivered in residences. Home Health Prospective Payment updates for 2025 include clearer coding for durable ventilator equipment, enabling providers to secure reimbursement for home initiation without extended hospital stays. Portable devices now pair with telehealth dashboards that allow therapists to adjust settings remotely, which minimizes unplanned readmissions. Manufacturers such as Vapotherm are introducing home-specific ventilators that weigh under 5 kg and run silently, making continuous therapy feasible in living rooms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & service costs | -0.7% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Stringent regulatory & quality compliance burden | -0.5% | Global, with concentration in EU & US | Medium term (2-4 years) |

| Semiconductor supply volatility for core chips | -0.4% | Global, with critical impact on North America & APAC | Short term (≤ 2 years) |

| Skill-gap & training deficiencies among caregivers | -0.3% | Global, particularly rural areas and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Service Costs

The purchase price of portable ventilators and the mandatory multi-year service contracts stretch hospital budgets, especially where reimbursements lag. Medtronic withdrew its Puritan Bennett line in February 2024, explaining that servicing commitments outweighed margins in a price-sensitive market. For providers, Medicare’s “frequent and substantial servicing” category obliges a maintenance regimen that inflates total cost of ownership. Semiconductor supply disruptions continue to elevate component prices, pushing some projects beyond target budgets. Emerging-market facilities, often running on limited capital, may defer upgrades or opt for refurbished units.

Stringent Regulatory & Quality Compliance Burden

Regulators are tightening quality standards to prevent device malfunctions. The FDA updated its Quality System Regulation in 2024 to align with ISO 13485, obliging extra documentation and audits for manufacturers. Breas Medical recalled 8,186 Vivo 45 LS ventilators in June 2025 over formaldehyde concerns, underscoring the high stakes of compliance lapses. China’s GB 9706.212-2020 introduces parallel design-verification layers that lengthen development cycles for international firms seeking access. For smaller entrants, the cost and complexity of meeting diverse regional mandates can be prohibitive, limiting product pipelines and slowing innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Patient Type: Specialized Neonatal Growth within a Large Adult Base

Adult devices continue to anchor demand, holding 62.54% portable ventilator market share in 2025 as hospitals, transport services, and long-term care facilities rely on versatile systems that transition across settings. Integration of reinforcement-learning algorithms such as VentAI helps clinicians fine-tune oxygenation and decrease ventilation time, elevating interest among intensive-care teams. The neonatal sub-segment, forecast to climb at a 5.63% CAGR, benefits from miniaturized blowers and non-contact monitors that prevent skin injury. Studies in extremely low gestational age infants reveal high-frequency percussive ventilation can cut respiratory severity scores by nearly 50%, driving adoption in tertiary neonatal units. Pediatric volumes sit between the two extremes, supported by expanded FDA pathways for child-specific high-risk devices that historically faced approval delays.

High-acuity transport services illustrate cross-age functionality; Hamilton’s HAMILTON-T1 suits both neonates and adults by auto-adjusting tidal volumes while retaining turbine autonomy. Such flexibility reinforces the portable ventilator market trajectory by letting health networks standardize fleet inventories instead of purchasing separate age-tailored models, balancing cost control with clinical precision.

By Interface: Fast-Growing Invasive Demand alongside Non-Invasive Dominance

Non-invasive units captured 57.74% revenue in 2025 because they manage stable COPD and sleep-disordered breathing without intubation. Medicare’s pending coverage expansion for chronic COPD is expected to lift long-term home prescriptions and widen the portable ventilator industry addressable pool. Invasive devices, favored in trauma and inter-facility ambulance transfers, should log a 5.98% CAGR as emergency services upgrade equipment that ensures definitive airway control. Vapotherm’s high-velocity therapy device exemplifies non-invasive innovation that safeguards delicate neonatal lungs while reducing noise, making it attractive for step-down units.

Clinicians frequently migrate patients from invasive to non-invasive support during weaning, demonstrating complementary rather than competing use cases. Updated critical-care guidelines from the Korean Society of Critical Care Medicine formalize such phased approaches, which can shorten ICU stays and reserve high-acuity beds for new admissions. This continuum reinforces steady demand across both interfaces and protects the portable ventilator market from technological obsolescence risk.

By Technology: Turbine Leadership Secures Operational Efficiency

Turbine platforms control 47.96% of 2025 sales and are expected to grow 5.78% annually through 2031, a pace supported by lightweight designs and batteries lasting up to eight hours. The MEDUVENT Standard weighs 2.1 kg, remains gas-tank independent, and therefore suits air-ambulance missions where cylinder logistics prove challenging. Hamilton’s T1 now commands 71% share among European intensive-care helicopters because its turbines auto-compensate altitude changes, protecting oxygen saturation during rapid climbs. Compressor-powered units still appeal in outpatient clinics that already stock compressed air, while gas-driven designs maintain niche roles in military deployments where power generation may be unreliable.

Blower suppliers such as ASPINA keep shrinking footprint and noise, extending the portable ventilator market size for turbine devices into sleep-apnea adjuncts and pediatric home care. As predictive maintenance algorithms join with battery health indicators, providers gain confidence in turbine longevity and schedule service preemptively, further lowering lifecycle costs.

By End User: Home Care Rises within Hospital-Centric Revenues

Hospitals and clinics delivered 49.86% of 2025 value, confirming their role as primary ventilation purchasers. They increasingly opt for multi-mode systems that shift from invasive to non-invasive, preserving capital budgets while addressing variable acuity. Home-care adoption, projected at a 6.05% CAGR, accelerates as payers promote early discharge protocols. Movair’s 8-pound Luisa ventilator, with an 18-hour battery and FDA authorization for chronic COPD, illustrates design attributes that make domiciliary therapy feasible. Remote-monitoring dashboards send adherence and alarm data to respiratory therapists, letting them intervene before health declines.

Ambulatory surgery centers benefit as well, since portable units enable safe same-day procedures by offering contingency ventilation without full critical-care infrastructure. Rural outreach programs leverage broadband-enabled monitoring to supervise ventilated patients living far from urban hospitals, bridging geographic gaps and enlarging the portable ventilator market base.

Geography Analysis

North America led with 43.32% market share in 2025 as federal agencies prioritized emergency readiness and continuity-of-care initiatives. The Department of Health and Human Services includes portable ventilators on its All-Hazards Plan equipment lists, ensuring budget allocations for periodic replenishment. Medicare reimbursement updates encourage clinicians to issue portable devices at discharge when medically justified, preventing unnecessary readmissions. Canada’s provincially funded Community Paramedicine programs equip ambulances with turbine ventilators that maintain oxygenation during long transports across remote territories. Mexico aligns device-registration protocols with North American standards, simplifying cross-border supply and service.

Asia-Pacific records the fastest 6.29% CAGR through 2031, buoyed by India’s climb toward a USD 50 billion medical-device sector and China’s stricter GB standards that favor high-quality imports . State procurement in India subsidizes portable ventilators for district hospitals that previously lacked mechanical support, while private insurers expand coverage for home ventilation. China’s tiered hospital system sets higher reimbursement for AI-enabled devices, motivating local makers to license turbine components from global suppliers. Japan remains selective, yet expedited pathways added in 2024 shorten approval timelines for critical-care innovations, thereby attracting foreign entrants with proven safety records.

Europe features mature demand rooted in universal healthcare and stringent safety rules. Germany’s DRG-based payments cover turbine portable units if patients meet oxygen-dependence thresholds, sustaining hospital orders. France completed a 2024 stockpile audit and replaced cylinder-driven transport ventilators with battery models that meet EN 794-3 standards. The Middle East channels oil revenues into trauma-care upgrades, with Gulf Cooperation Council members adopting unified procurement frameworks that require ISO 80601 compliance. Africa and South America remain volume-constrained today, yet WHO’s 2024 Compendium spotlights low-resource portable ventilators suitable for clinics lacking stable electricity, foreshadowing donor-funded rollouts. Regional diversification therefore cushions the portable ventilator market against local downturns and regulatory shocks.

Competitive Landscape

Industry consolidation is moderate as established firms prune portfolios while EMS-focused acquirers expand. ZOLL paid USD 37 million for Vyaire’s bellavista, fabian, LTV, and 3100 HFOV lines in October 2024, adding critical-care depth to its defibrillator-led hospital offering. The transaction strengthens ZOLL’s presence in transport and neonatal domains where complementary sales channels already exist. Medtronic’s exit removed a legacy brand yet opened white space for mid-size innovators targeting specialized sub-segments such as neonatal care with firmware-driven lung-protective modes.

Technology competition centers on software intelligence and battery autonomy. ResMed integrates its portable ventilators into the AirView cloud, letting clinicians track adherence and modify settings from any browser. Hamilton Medical embeds adaptive triggering algorithms that tailor breaths in real time and publishes peer-reviewed evidence of outcome gains, bolstering clinician confidence. Philips positions Trilogy Evo as an all-age platform capable of invasive, non-invasive, and hybrid modes, which appeals to providers seeking inventory rationalization.

New entrants pursue niche value propositions rather than head-to-head scale. Vapotherm focuses on late-stage hypercapnic COPD and markets a pressured-flow interface that reduces mask intolerance. Movair targets home transition with integrated oxygen concentrators, while Weinmann emphasizes field durability and extended battery life for search-and-rescue teams. As procurement increasingly requires digital service packages and outcome-based warranties, companies that align hardware with analytics and remote-support ecosystems enjoy differentiation beyond price.

Portable Ventilators Industry Leaders

Drägerwerk AG & co.

Getinge AB

Koninklijke Philips NV

Medtronic PLC

Fosun Pharmaceutical (Breas Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: WEINMANN Emergency expanded MEDUVENT Standard capabilities to support advanced ventilation modes for emergency medical service teams.

- March 2024: Vapotherm launched Access365, a home ventilator designed to improve quality of life for patients with late-stage hypercapnic COPD.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the portable ventilators market as the value generated by new, compact, battery-powered transport or home-use ventilators capable of invasive or non-invasive respiratory support, sold through hospitals, EMS fleets, ambulatory centers, and home-care channels worldwide. The definition embraces turbine, compressor, or gas-driven models that operate independently of wall gas and are supplied with accessories such as breathing circuits and humidifiers.

Scope exclusion: Stationary ICU-grade ventilators permanently fixed to critical-care beds are outside this study.

Segmentation Overview

- By Patient Type

- Adult Ventilators

- Pediatric Ventilators

- Neonatal Ventilators

- By Interface

- Invasive Ventilation

- Non-invasive Ventilation

- By Technology

- Turbine-Powered Ventilators

- Compressor-Powered Ventilators

- Gas-Driven Ventilators

- By End User

- Hospitals & Clinics

- Ambulatory Care Centers

- Home Care Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed clinicians in tertiary hospitals, emergency medical technicians, and procurement managers across North America, Europe, Asia-Pacific, and GCC states. These conversations clarified average selling prices, battery-life preferences, and post-pandemic home-care adoption rates, allowing us to cross-check desk findings and adjust gray-area assumptions.

Desk Research

Analysts first gathered usage statistics and price references from public datasets such as the WHO Global Health Observatory, OECD health expenditure tables, the United States FDA 510(k) database, and trade flow records available through UN Comtrade. Respiratory equipment shipment tallies from industry associations, including the American Association for Respiratory Care and Europe's MedTech Europe, offered baseline unit movements. Financial disclosures pulled via D&B Hoovers and recent device approvals traced in Dow Jones Factiva filled revenue and pipeline gaps. Questel patent analytics revealed innovation pacing in turbine modules and battery management. This list remains illustrative; numerous additional open and paid sources informed validation and clarification.

Market-Sizing & Forecasting

A top-down model converts country-level acute-care admissions, COPD prevalence, EMS fleet counts, and home ventilation reimbursement enrollments into ventilator demand pools, which are then matched with observed penetration rates. Select bottom-up checks, supplier roll-ups in high-volume nations and sampled ASP × volume calculations, reconcile totals. Key variables steering forecasts include: 1) annual COPD incidence, 2) EMS vehicle additions, 3) median portable vent price erosion, 4) lithium-ion battery cost trends, and 5) regulatory fast-track clearances. Multivariate regression, aligned with expert consensus on these drivers, projects values through 2030; scenario analysis flags supply chain or pandemic shocks.

Data Validation & Update Cycle

Outputs pass anomaly screening against import statistics, capital equipment order backlogs, and price outliers, followed by senior analyst peer review. Reports refresh yearly, with mid-cycle updates triggered by material recalls, landmark approvals, or macro shocks, ensuring clients receive our latest view before delivery.

Why Mordor's Portable Ventilators Baseline Commands Reliability

Published estimates often diverge because firms pick different device mixes, price benchmarks, and refresh cadences.

Key gap drivers include narrower 'home-only' scopes, unverified ASP assumptions, currency conversion dates, and less frequent updates, all of which inflate or compress totals relative to Mordor's balanced blend of care settings and validated prices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.03 B (2025) | Mordor Intelligence | |

| USD 0.98 B (2024) | Global Consultancy A | Excludes EMS purchases; uses 2023 average prices |

| USD 0.79 B (2024) | Industry Publication B | Home-care devices only; omits Asia-Pacific shipments |

| USD 0.33 B (2025) | Trade Journal C | Focuses solely on transport ventilators for ambulances |

Figures rounded to two decimals. The comparison shows that once scope and price inputs are harmonized, discrepancies narrow sharply, underscoring how Mordor's disciplined variable selection and annual refresh deliver a dependable, decision-ready baseline.

Key Questions Answered in the Report

How big is the Portable Ventilators Market?

The Portable Ventilators Market size is expected to reach USD 1.08 billion in 2026 and grow at a CAGR of 5.13% to reach USD 1.39 billion by 2031.

Which region contributes the most revenue?

North America dominates with 43.32% of 2025 revenue, supported by federal preparedness funding and favorable reimbursement.

Who are the key players in Portable Ventilators Market?

Drägerwerk AG & co., Getinge AB, Koninklijke Philips NV, Medtronic PLC and Fosun Pharmaceutical (Breas Medical) are the major companies operating in the Portable Ventilators Market.

Which is the fastest growing region in Portable Ventilators Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Page last updated on: