Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.97 Billion |

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Gas Sensors Market Analysis by Mordor Intelligence

The United States gas sensors market size in 2026 is estimated at USD 2.09 billion, growing from 2025 value of USD 1.97 billion with 2031 projections showing USD 2.83 billion, growing at 6.23% CAGR over 2026-2031. Demand is sustained by federal safety rules that push factories and refineries to install continuous leak-detection systems, while stricter ASHRAE ventilation standards extend adoption across commercial buildings. Wireless and IoT-ready devices are rapidly gaining favour as low-power networks cut installation costs and enable remote diagnostics that improve uptime. Edge-AI analytics now run directly on the sensor node, turning raw data into real-time alerts that help prevent costly incidents. [2]EPA Staff, “Controlling Air Pollution from Oil and Natural Gas Operations,” U.S. Environmental Protection Agency, epa.gov Hydrogen infrastructure rollouts are creating a surge of orders for ultra-sensitive detectors, and MEMS-based designs are lowering size and power requirements, opening new uses in wearables and portable safety gear. Competitive intensity is moderate: diversified safety leaders still dominate critical-process niches, but semiconductor specialists are carving out share with compact, software-driven platforms. [1]OSHA Staff, “Hazard Communication Standard; Final Rule,” Occupational Safety and Health Administration, osha.gov

Key Report Takeaways

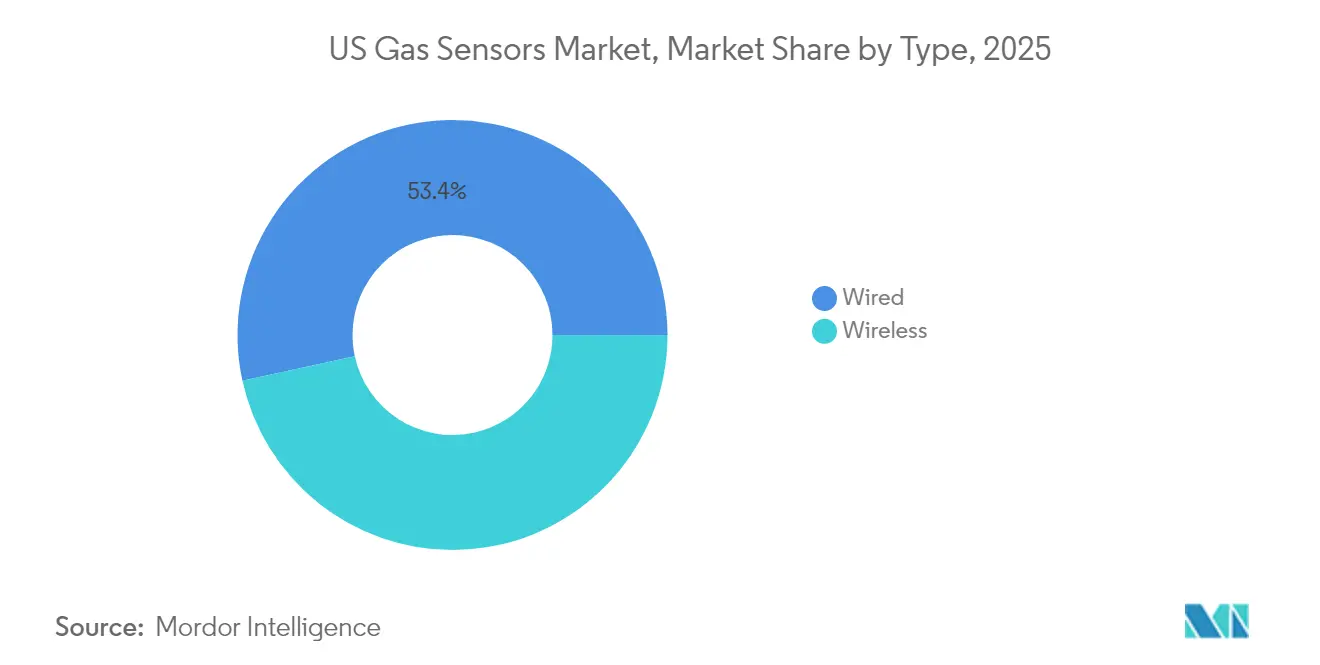

- By connectivity type, the wired segment held 53.42% of the United States gas sensors market share in 2025, while wireless devices are forecast to grow at an 11.12% CAGR through 2031.

- By gas type, carbon monoxide sensors led with 27.62% share in 2025; hydrogen sensors are projected to expand at a 14.05% CAGR to 2031.

- By technology, electrochemical sensors accounted for 31.08% of the United States gas sensors market size in 2025, whereas MEMS MOS platforms are expected to increase at a 12.74% CAGR between 2026 and 2031.

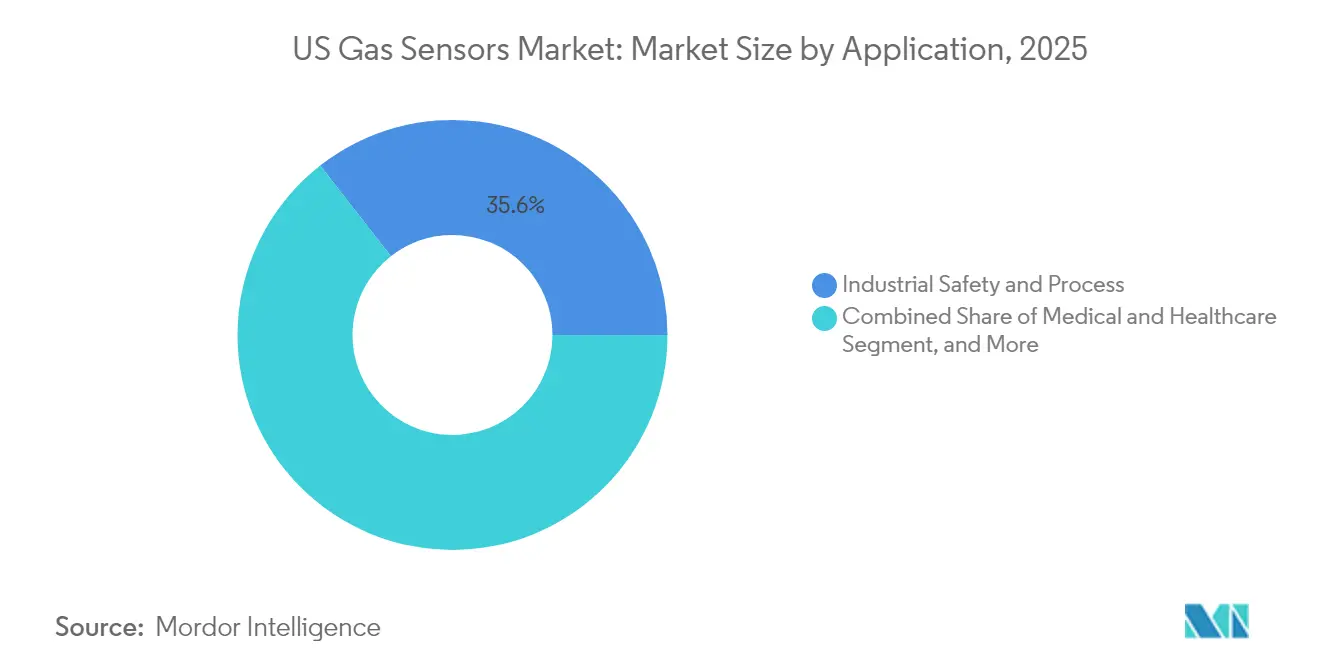

- By application, industrial safety and process systems commanded 35.55% of the United States gas sensors market in 2025; hydrogen fuelling stations are expected to post the fastest growth at a 14.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Gas Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OSHA & EPA compliance driving industrial demand | +2.1% | National, industrial hubs | Medium term (2-4 years) |

| Growing HVAC / IAQ adoption (ASHRAE 62.1) | +1.8% | National, Northeast and West | Medium term (2-4 years) |

| Automotive cabin-air quality monitoring | +1.2% | National, automotive manufacturing regions | Long term (≥ 4 years) |

| Edge-AI & IoT-enabled predictive maintenance | +1.5% | National, early adoption in industrial centers | Medium term (2-4 years) |

| Hydrogen refuelling leak-detection roll-out | +1.3% | West and Northeast, expanding nationally | Long term (≥ 4 years) |

| Methane-leak rules under IIJA pipelines program | +1.7% | National, oil and gas producing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OSHA and EPA Compliance Driving Industrial Demand

Regulatory updates on methane and toxic gas emissions require plants to verify leaks at lower thresholds and carry penalties that can reach USD 25,000 per day. Facilities therefore invest in multi-gas arrays that detect parts-per-billion concentrations, adding process-control value beyond compliance. Engineering teams are now specifying detectors that integrate with safety-instrumented systems to automate shutdowns when hazardous levels arise, a capability that shortens response time and limits liability exposure. Compliance spending is heaviest in oil, gas, and chemical clusters across Texas, Louisiana, and Pennsylvania, securing a reliable revenue stream for suppliers. Large buyers prefer product lines supported by calibration programs and cloud-based audit trails that simplify regulatory reporting.

Growing HVAC / IAQ Adoption (ASHRAE 62.1)

The 2024 update to ASHRAE 62.1 tightened accuracy targets for CO₂ meters, prompting building operators to swap older hardware for advanced optical or electrochemical devices. Office towers, hospitals, and schools now integrate occupancy-based ventilation controls that link gas readings to air-handling units, balancing energy savings with health criteria. Portfolio owners see indoor-air data as an amenity that supports tenant retention, elevating gas sensors from back-of-house equipment to a visible part of wellness branding. Strongest adoption is in the Northeast and California, where state incentives pair with sustainability mandates. System integrators bundle sensors with analytics dashboards to provide fault alerts and ventilation scorecards in a single view. [4]ASHRAE Committee, “Standards Actions,” ASHRAE, ashrae.org

Automotive Cabin-Air Quality & Emissions Monitoring

Carmakers install multi-gas modules in HVAC ducts to maintain healthy cabin environments amid congested traffic. Research shows in-cabin pollutant peaks that exceed outdoor levels by up to 10 times during commutes, spurring fitment in mid-range models. Electric vehicles present unique ventilation challenges due to sealed battery compartments, increasing demand for low-power MEMS arrays that monitor organics, CO, and particulates together. Suppliers package these arrays with software that triggers recirculation or filtration events, enhancing occupant comfort and brand differentiation. Production lines in Michigan and Ohio anchor early volume, while Asian manufacturers prepare to import sensor-equipped vehicles that match U.S. indoor-air expectations.

Edge-AI and IoT-Enabled Predictive Maintenance

Deploying analytics at the sensing node reduces bandwidth costs and turns time-series gas readings into failure forecasts. Field trials in shale production show maintenance cost cuts of 30-50% after deploying edge-enabled detectors on compressors and flare stacks. Algorithms trained on historic leak patterns flag drift in baseline readings, letting crews service equipment before a release occurs. Battery-powered devices last five years when paired with low-power wide-area networks, making them viable for remote wellheads and midstream assets. Vendors monetize value-added subscriptions that deliver predictive reports and compliance logs through secure dashboards.

Methane-Leak Rules Under IIJA Pipelines Program

Pipeline operators must now perform quarterly leak surveys and rapidly repair any exceedances, raising orders for continuous monitors capable of detecting sub-ppm methane. Projects concentrate in Texas, Oklahoma, and Pennsylvania, where aging infrastructure intersects with new gas production. Industrial Internet gateways relay readings to central control rooms, reducing truck rolls for inspection rounds. Technology suppliers' partner with aerial-survey firms to combine fixed-sensor data with drone and satellite imagery, delivering compliance documentation in a single platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High calibration & maintenance costs | −1.2% | National, higher impact where skilled labour is scarce | Medium term (2-4 years) |

| Sensor price commoditisation | −0.9% | National | Long term (≥ 4 years) |

| Domestic MEMS-fab capacity bottlenecks | −0.8% | Semiconductor manufacturing regions | Short term (≤ 2 years) |

| Cyber-security worries for cloud sensors | −0.7% | National, critical infrastructure sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Calibration & Maintenance Costs

Quarterly calibration protocols require specialty test gas, trained staff, and downtime that can push lifetime ownership costs to 40% of equipment spend. Smaller plants often delay service intervals, risking false alarms or undetected leaks that undermine safety investments. Manufacturers respond with self-calibrating cells and remote diagnostics, yet capital prices rise, forcing buyers to weigh upfront savings against recurring labour. Skill shortages in rural regions worsen the burden, prompting some operators to outsource maintenance contracts that bundle sensors, service, and compliance documentation.

Sensor Price Commoditisation

Basic carbon-monoxide and combustible-gas detectors now face price drops of 15-30% as new Asian entrants replicate mature designs. Falling margins pressure established firms to shift R&D toward multi-gas arrays and software-enhanced systems where differentiation lies in analytics and integration rather than hardware alone. Customers benefit from cheaper single-gas units but may face higher total cost of ownership if low-cost imports lack local support or long-term calibration parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wireless Connectivity Drives Remote Monitoring Revolution

The wired category maintained a 53.42% position in the United States gas sensors market during 2025, anchored by process industries that require uninterrupted power and fail-safe communication. These installations typically connect directly to distributed control systems, ensuring compliance in hazardous zones. However, wireless nodes are growing at an 11.12% CAGR, propelled by low-power wide-area technologies that stretch battery life to more than five years. Facility managers deploy mesh networks that allow temporary placement during turnarounds or in legacy buildings where cabling is cost prohibitive. Wireless flexibility supports granular sensor placement, elevating coverage in multi-story schools and hospitals that seek better ventilation insight. Integrators combine wireless gas data with occupancy and energy metrics, bundling value propositions that extend beyond safety into operational efficiency.

The rise of wireless options also reshapes service models. Vendors now offer subscription packages that wrap hardware, network connectivity, and analytics dashboards in single agreements. This shift reduces capital budgets and enables evergreen upgrades when new sensors emerge. As the United States gas sensors market size relevant to wireless installations climbs, procurement teams pivot toward total-cost evaluations that emphasize lifetime value and software functionality. While wired systems will remain standard in high-risk areas, hybrid architectures emerge, pairing permanent wired detectors in Class I Division 1 zones with wireless devices in less hazardous spaces to optimize spend.

By Technology: MEMS MOS Sensors Disrupt Traditional Platforms

Electrochemical cells held 31.08% of the United States gas sensors market share in 2025 due to their proven accuracy for CO, H₂S, and NO₂. Catalytic-bead designs persisted as the go-to choice for combustible gases in Class I environments, while NDIR optics gained popularity for CO₂ in HVAC controls. PIDs served niche roles monitoring VOCs during hazmat response and industrial hygiene campaigns.

MEMS MOS devices are on track to post 12.74% CAGR growth between 2026 and 2031 as semiconductor production reduces per-unit costs and enables multi-gas identification in coin-sized packages. Machine-learning algorithms compensate for cross-sensitivity, letting a single die discriminate among methane, hydrogen, and volatile organics with contextual accuracy. Wearables for lone-worker safety and consumer electronics integrate these chips to alert users to hazardous environments in real time. The migration to MEMS also lowers power draw, extending battery life in wireless nodes and aligning with sustainability objectives that discourage frequent battery swaps.

By Application: Industrial Safety Leads While Hydrogen Fuelling Accelerates

Industrial safety and process applications contributed 35.55% of 2025 revenue, underscoring the prime importance of gas monitoring in petrochemical, mining, and steel operations. Regulations mandate multi-layer detection, from personal monitors to fixed-point arrays that alarm both locally and in centralized control rooms. Building-automation deployments continue to rise as facility managers link gas readings to HVAC controls for energy optimization and occupant wellness. Medical settings rely on oxygen and anaesthetic-gas sensors in surgical suites and respiratory-therapy equipment. Food and beverage producers use CO₂ and ethanol detectors to manage fermentation and packaging processes, reducing spoilage and ensuring worker protection.

Hydrogen fuelling stations represent the fastest-growing domain at 14.88% CAGR. Each station requires overhead, pit, and compressor-cabinet detectors that must endure outdoor conditions, vibration, and potential water spray. Sensor packages integrate modular control panels with automated shutdown valve logic to meet code. Early deployments along California’s I-5 corridor and the Northeast’s proposed hub validate the business case for purpose-built hydrogen detection solutions. As federal funding accelerates buildouts, vendors with certified offerings anticipate multi-year backlog expansion, reinforcing hydrogen’s role as a demand catalyst for the United States gas sensors market.

By Gas Type: Hydrogen Detection Emerges as Growth Catalyst

Carbon-monoxide detectors held 27.62% share in 2025, evidencing their ubiquitous role in boilers, parking garages, and residential compliance. Toxic gases such as hydrogen sulphide and nitrogen dioxide maintain steady demand, driven by process-safety regulations across refineries and chemical plants. Carbon dioxide sensors gain traction in indoor air-quality schemes aligned with ASHRAE guidance, especially in office retrofits that aim for WELL or LEED certifications. Nitrogen-oxide sensors expand within emissions-control systems as power stations adopt selective catalytic reduction.

Hydrogen detectors, forecast to rise at a 14.05% CAGR, are transforming vendor roadmaps. Fuelling-station developers integrate multi-sensor arrays that couple fast optical detectors with slower catalytic beads to guarantee redundancy under NFPA 2 rules. The Department of Energy’s hub initiatives increase volume needs, leading manufacturers to invest in palladium-film MEMS processes that deliver ppm-level sensitivity without drift. As the United States gas sensors market aligns to hydrogen infrastructure, component suppliers offering certified intrinsically safe models secure early design wins across electrolyser halls, compression skids, and transport trailers.

Geography Analysis

The United States gas sensors market serves a nation-wide customer base spanning heavy industry, utilities, transportation, commercial real estate, and residential codes. Federal rules such as OSHA’s Hazard Communication Standard and EPA emissions limits apply uniformly across all states, creating consistent baseline demand for fixed and portable detectors. National building standards, including ASHRAE 62.1, fuel widespread CO₂ and CO monitoring in offices, schools, and healthcare facilities. Large industrial corporations often deploy standardized sensor platforms across multiple states to streamline maintenance, calibration, and regulatory reporting.

Infrastructure initiatives funded by the Infrastructure Investment and Jobs Act (IIJA) stimulate deployment of continuous methane monitors along national pipeline corridors. The Department of Energy’s hydrogen-hub program distributes grants to multiple consortia, triggering orders for hydrogen detectors in production, storage, and fueling applications across the country. Automotive assembly plants from Michigan to South Carolina integrate multi-gas modules into vehicle HVAC systems, demonstrating uniform uptake of air-quality sensors in manufacturing and transportation segments.

Uniform national demand encourages suppliers to operate centrally managed service contracts, remote diagnostics, and cloud-based calibration dashboards that support installations from Alaska to Florida. Distribution partners maintain stocking branches in key industrial metros, while e-commerce channels extend reach to small and medium-sized enterprises throughout the United States gas sensors market. This cohesive national landscape allows vendors to build scale economies in production, logistics, and customer training, supporting robust long-term growth prospects.

Competitive Landscape

Market concentration is moderate; the top five participants hold an estimated 45% share, yet no single company dominates. Honeywell, MSA Safety, and Amphenol Advanced Sensors leverage broad portfolios and global service networks to retain leadership in hazardous-location applications. Honeywell’s 2025 launch of the Sensepoint XRL Plus underscores the shift toward connected platforms that pair field devices with cloud-ready software. MSA’s USD 200 million purchase of M&C TechGroup adds process-analysis depth that complements its portable and fixed device lines.

Semiconductor suppliers enter with MEMS offerings, challenging incumbents on size, power efficiency, and integrated analytics. Partnerships between chipmakers and software firms signal a pivot toward data-centric value propositions, where recurring subscription revenue outpaces hardware margins. Niche players focus on specialty gases or ultralow detection limits, securing research contracts and regulatory pilots. The field also sees alliances between optical-sensor experts and wireless-network providers that bundle connectivity and cybersecurity features for critical infrastructure clients.

White-space segments include low-power sensors for battery-operated IoT nodes, miniaturized multi-gas arrays for wearables, and detectors tailored to emerging fuels such as ammonia and e-methanol. Intellectual-property filings concentrate on machine-learning algorithms and sensor-fusion techniques, highlighting a race to convert raw data into actionable intelligence. Successful vendors position themselves as solution partners, offering complete packages from hardware to analytics, calibration, and compliance documentation, an approach that strengthens switching costs and customer loyalty within the United States gas sensors market.

United States Gas Sensors Industry Leaders

Honeywell International Inc.

Emerson Electric Co.

MSA Safety Incorporated

Amphenol Advanced Sensors

Figaro USA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MSA Safety reported a 4% organic rise in its detection segment, citing strong demand for connected safety solutions.

- February 2025: The Environmental Protection Agency finalized stricter NESHAP rules for ethylene-oxide sterilization facilities, mandating continuous monitoring.

- January 2025: Honeywell launched the Sensepoint XRL Plus with integrated wireless connectivity and on-device edge processing.

- November 2024: PHMSA implemented new leak-detection regulations under the PIPES Act, expanding requirements for advanced methane sensors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States gas sensors market as the annual value of newly manufactured sensing elements and modules that directly quantify the presence or concentration of gases such as CO, CO₂, O₂, NOₓ, hydrocarbons, and related compounds across industrial, automotive, building automation, and healthcare settings. Measurements embedded inside complete gas analyzers or multi-parameter detection systems are included only when the sensing element is sold as a discrete bill of materials line item.

Scope exclusion: portable gas detection handsets, stack analyzers, and pure software analytics modules are outside this value chain.

Segmentation Overview

- By Type

- Wired

- Wireless

- By Gas Type

- Oxygen

- Carbon Monoxide

- Carbon Dioxide

- Nitrogen Oxide

- Hydrocarbon

- Others

- By Technology

- Electrochemical

- Photo-Ionisation Detector (PID)

- Solid-State / MOS

- Catalytic Bead

- Infra-Red (NDIR)

- Semiconductor

- By Application

- Medical and Healthcare

- Building Automation

- Industrial Safety and Process

- Food and Beverage

- Automotive

- Transportation and Logistics

- Other Applications

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interact with EHS managers at petrochemical plants, HVAC integrators, automotive Tier 1 engineers, and component distributors from California to Pennsylvania. These interviews validate adoption rates, average selling prices (ASPs), and technology shift assumptions that secondary data alone cannot reveal.

Desk Research

We first map the demand pool using open datasets from agencies such as the US Environmental Protection Agency, Occupational Safety and Health Administration, National Institute for Occupational Safety and Health, US Census Bureau Industrial Surveys, and the American Chemistry Council. Industry white papers, peer-reviewed journals like Sensors & Actuators B, and filings lodged with the Securities and Exchange Commission supply trend, pricing, and capacity cues.

Paid repositories, namely D&B Hoovers for company revenues, Dow Jones Factiva for deal flow, and Questel for patent velocity, enrich the public record and help us benchmark competitive intensity. Many other publicly available sources are also consulted to cross-check numbers and narrative coherence.

Market-Sizing & Forecasting

A calibrated top-down construct starts with domestic manufacturing shipments and import-export ledgers before applying penetration factors tied to new industrial facility starts, vehicle production, and smart building completions; selective bottom-up roll-ups of leading sensor suppliers' revenues serve as a reasonableness test. Key variables modeled include average sensor ASPs, unit shipments by gas type, semiconductor material costs, EPA rule implementation timelines, and plant capital expenditure cycles. Multivariate regression, augmented by scenario analysis for regulatory pace, extends the forecast to 2030 while smoothing short-term volatility.

Data Validation & Update Cycle

Outputs undergo variance checks against historical series, peer benchmarks, and fresh interview feedback. Our analysts revisit the model at least annually and issue interim revisions when material events, major regulation, supply shocks, or M&A alter underlying drivers.

Why Our US Gas Sensors Baseline Stands Reliable

Published figures often diverge because firms choose different scope edges, pricing ladders, and refresh cadences. We anchor our baseline in the actual traded value of sensors, align gas and technology buckets with EPA monitoring protocols, and update every twelve months, thereby minimizing vintage bias.

Key gap drivers versus other publishers include narrower product coverage, static ASP assumptions, and less frequent refreshes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.97 billion (2025) | Mordor Intelligence | - |

| USD 659 million (2024) | Global Consultancy A | Excludes MEMS MOS platforms and applies fixed ASP till 2030 |

| USD 431 million (2024) | Trade Journal B | Counts only electrochemical and catalytic devices; limited primary validation |

In sum, our disciplined scope selection, live primary inputs, and annual refresh make Mordor's numbers a dependable baseline for planners seeking transparent, repeatable market evidence.

Key Questions Answered in the Report

What is the current value of the United States gas sensors market?

The market stands at USD 2.09 billion in 2026 and is projected to reach USD 2.83 billion by 2031.

Which connectivity type is growing fastest?

Wireless gas sensors are forecast to grow at an 11.12% CAGR from 2026 to 2031 as organizations shift toward IoT-enabled remote monitoring.

Why is hydrogen detection seeing rapid adoption?

Federal funding for hydrogen hubs and strict safety codes is driving a 14.05% CAGR for hydrogen gas sensors, the fastest among all gas types.

How do edge-AI gas sensors improve maintenance?

On-device analytics transform raw readings into predictive alerts, cutting maintenance costs by up to 50% in pilot programs across oil and gas operations.

Which region shows the strongest regulatory influence on adoption?

California imposes the nation’s most stringent leak-detection requirements, accelerating sensor deployment in industrial plants and hydrogen fuelling stations.

What is the main challenge limiting wider sensor adoption in small facilities?

High calibration and maintenance costs, often representing 40% of total ownership expenses, deter smaller operators from deploying optimal sensor coverage.

Page last updated on: