Battery Cyclers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

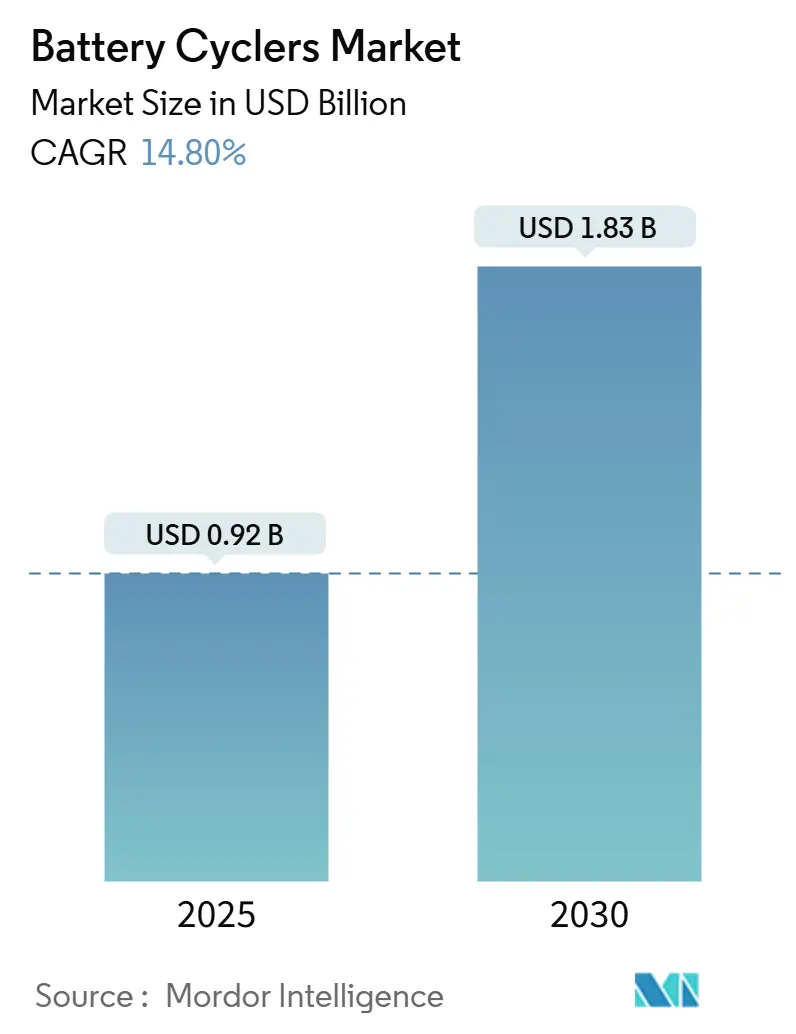

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.83 Billion |

| Growth Rate (2025 - 2030) | 14.80% CAGR |

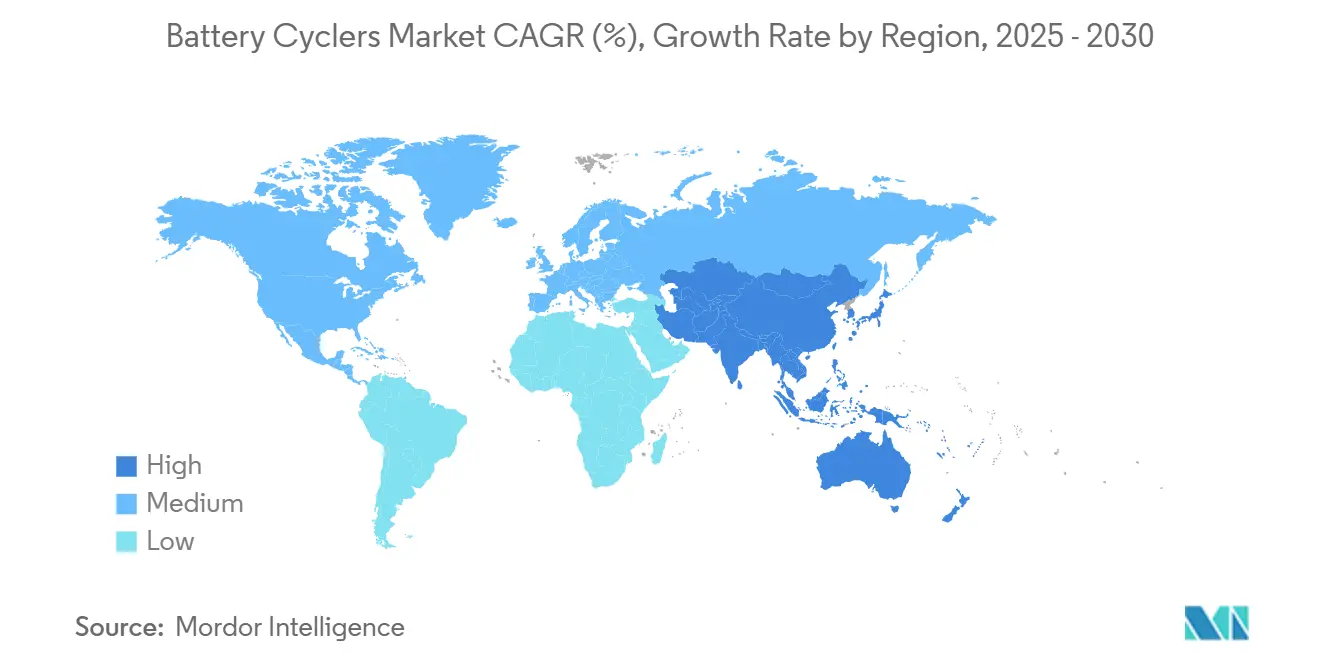

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Cyclers Market Analysis by Mordor Intelligence

The battery cyclers market size stands at USD 0.92 billion in 2025 and is forecast to reach USD 1.83 billion by 2030, registering a robust 14.8% CAGR over the period. Demand accelerates as electric-vehicle (EV) makers ramp up cell output, utilities add grid-scale storage, and research teams validate next-generation chemistries, all of which require precision formation, cycling, and lifetime testing. Multi-channel architectures, medium-power ranges, and AI-enabled software now dominate buying criteria, while regulatory mandates for stringent safety evaluations raise the technical bar for new equipment. Intensifying investment in North American and European gigafactories diversifies the customer base beyond Asia-Pacific, although China still anchors global capacity. Competitive intensity remains moderate; technology, not price, drives differentiation as vendors integrate analytics that shrink test times, cut energy use, and predict failure modes.

Key Report Takeaways

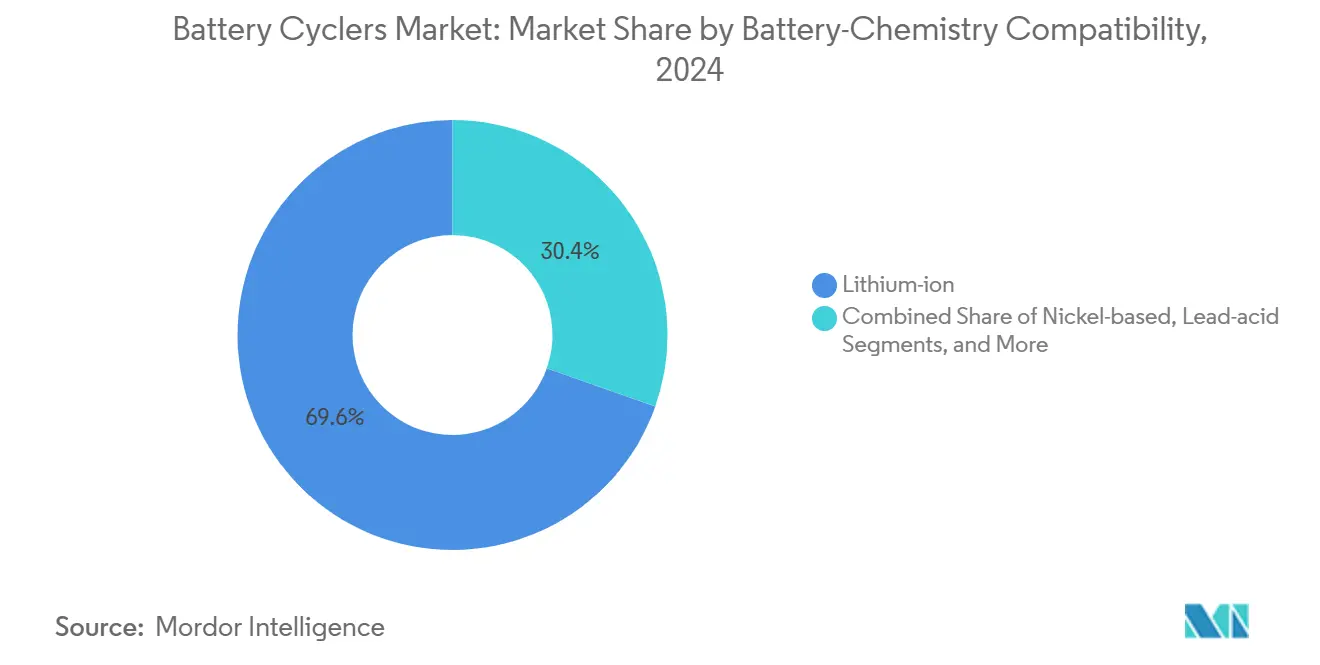

- By battery-chemistry compatibility, lithium-ion products captured 69.6% of the battery cyclers market share in 2024, while solid-state and other emerging chemistries are projected to expand at a 17.2% CAGR to 2030.

- By channel count, ≥8-channel systems led with 62.1% revenue share in 2024; configurations with ≥16 channels are forecast to rise at a 16.7% CAGR through 2030, reflecting a shift toward high-throughput validation.

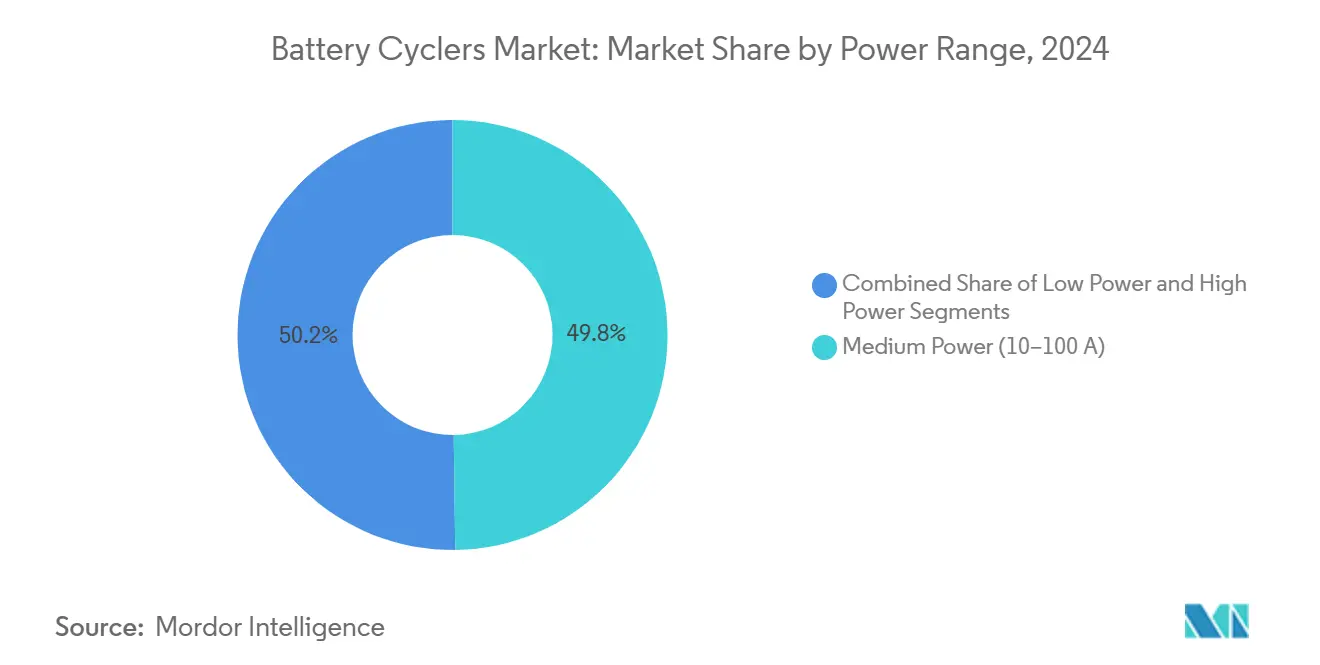

- By power range, medium-power cyclers (10-100 A) held 49.8% of the battery cyclers market size in 2024, whereas >100 A high-power models are advancing at a 16.1% CAGR through 2030.

- By end-user industry, automotive customers commanded 45.5% of 2024 revenue; the energy and power segment is expected to log the fastest 15.9% CAGR to 2030 as utilities deploy long-duration storage.

- By geography, Asia-Pacific retained 43.7% of global sales in 2024 and is set to expand at a 16.2% CAGR through 2030 on the back of China’s battery research and manufacturing concentration.

Global Battery Cyclers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV battery production capacity | +3.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Regulatory push for safety and durability | +2.8% | China, EU, North America | Short term (≤ 2 years) |

| Grid-scale storage adoption | +2.1% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Falling multi-channel cycler costs | +1.9% | Global | Long term (≥ 4 years) |

| AI/ML-enabled predictive analytics | +1.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| High-precision solid-state R&D needs | +1.5% | Japan, South Korea, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Battery Production Capacity Expansions

Gigafactory build-outs create unprecedented orders for high-throughput battery cyclers capable of handling cylindrical, prismatic, and pouch formats. LG Energy Solution’s USD 5.5 billion Arizona complex alone adds 32 GWh, each gigawatt-hour requiring proportional formation and cycling lanes.[1]Michael C. Anderson, “Battery-Industry Trends to Watch in 2025,” batterytechonline.com Formation can represent 20% of cell cost, so manufacturers invest in systems that maximize precision and yield. The migration to 800 V EV architectures elevates voltage and current demands, prompting equipment that tolerates >600 kW loads without thermal derating. Panasonic’s Kansas line reports 20% productivity gains over earlier Nevada operations through integrated high-density testers. Automakers project 4,100 GWh total cell demand by 2030, reinforcing long-run visibility for cycler suppliers.

Regulatory Push for Battery Safety and Durability Testing Standards

Safety legislation forces deeper test cycles and harsher abuse protocols. China’s GB38031-2025 standard requires 2-hour containment after thermal runaway and 5-minute early-warning systems; compliance sharply raises cycler-time per batch.[2]Kai-Philipp Kairies, “China Takes Lead on EV Battery Safety with GB38031-2025,” greencarcongress.com New EU battery regulations demand digital tracking of materials and carbon footprints, enlarging data-logging requirements during every charge-discharge event. The U.S. EPA proposes that EVs retain 80% of range for 10 years, translating into millions of additional validation cycles. IEC 62619:2022 further codifies stationary-system abuse tests, cementing demand for purpose-built stationary-storage cyclers.

Growing Adoption of Energy-Storage Cyclers for Grid-Scale Batteries

Global utility-scale storage rose 27.9% to 1.7 GW in Germany alone by 2023 and is forecast to top 24 GW by 2037, driving sales of large-format cyclers that accommodate cell stacks exceeding 300 Ah. The U.S. Department of Energy’s long-duration storage program targets 90% cost cuts by 2030, intensifying R&D on flow, sodium-ion, and zinc chemistries that need distinct testing regimes.[3]U.S. Department of Energy, “FOTW #1347: Battery Cell Production in North America Expected to Exceed 1,200 GWh per Year by 2030,” energy.gov California envisions 37 GW of storage by 2045, ensuring multi-decade demand for module-level cyclers able to replicate grid load profiles.

Integration of AI/ML in Cycler Software Enabling Predictive Analytics

Software upgrades transform cyclers into analytics hubs. SandboxAQ’s large quantitative models slash life-prediction time by 95% while improving accuracy 35-fold, letting labs cut physical cycles from thousands to hundreds. The U.S. Army harvests 2 million hours of test data to predict shelf life in days, not years, reducing logistical costs. Commercial platforms such as ACCURE’s Lifetime Manager achieve 96% forecast accuracy, underpinning warranty analytics for storage operators. Embedding machine-learning models in firmware now allows real-time protocol optimization under varying temperatures and C-rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for more than 100 A cyclers | -2.3% | Global, acute for SMEs | Short term (≤ 2 years) |

| Heat-management challenges at more than 800 V | -1.8% | North America and EU | Medium term (2-4 years) |

| Ultra-precision component supply gaps | -1.5% | Global, sharper in North America and EU | Short term (≤ 2 years) |

| Virtual BMS-in-loop simulations | -1.2% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for High-Current Cyclers

Systems exceeding 100 A per channel require expensive power-electronics stages, regenerative loads, and active cooling that raise unit prices beyond the reach of smaller laboratories. Thermal management infrastructure and safety interlocks inflate total cost of ownership, extending payback beyond three years for low-volume users. Consolidation in the test-and-measurement sector—transaction values jumped 337.6% in Q3 2024—underscores the financial hurdles for new entrants.

Virtual BMS-in-the-Loop Simulations Reducing Physical Cycling Demand

Hardware-in-loop (HIL) platforms replicate thousands of drive cycles digitally, cutting the volume of physical tests. dSPACE’s SCALEXIO performs fault injection at up to 1,500 V without real batteries, shrinking prototype timelines and slashing energy costs.[4]dSPACE, “Battery Management Systems: High-Precision Validation,” dspace.com As algorithms improve, early-stage developers increasingly validate designs virtually, curbing near-term demand for bench-top cyclers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery-Chemistry Compatibility: Lithium-Ion Dominance Drives Market Evolution

Lithium-ion units held 69.6% revenue in 2024, underscoring the chemistry’s ubiquity across EV, consumer, and stationary applications. The battery cyclers market size for solid-state and other emerging chemistries, though modest, is forecast to swell at a 17.2% CAGR as research programs target sulfide and polymer electrolytes that promise higher energy density and intrinsic safety. Japan and South Korea lead investment in production pilots slated for 2028, suggesting regional realignment once commercialization matures. Cyclers must therefore measure ultra-low leakage currents, detect dendrite inception, and accommodate elevated temperature cycles unique to solid-state prototypes. Vendors able to supply sub-microamp resolution and advanced impedance spectroscopy are best positioned for this shift.

Commercial lithium-ion cells will continue to dominate transportation, yet regulatory pressure for higher energy density accelerates silicon-carbon anode adoption, further tightening tolerance specs. Testing of 1750 mAh/g anodes requires deeper voltage windows and refined coulombic-efficiency tracking. Meanwhile, nickel-based chemistries retain aerospace niches where reliability trumps energy metrics, and legacy lead-acid formats persist in starter-lighting-ignition and stationary backup roles. Together these smaller categories still create significant volume, sustaining demand for versatile cyclers capable of automated multi-chemistry profiles.

By Channel Count: Multi-Channel Systems Enable High-Throughput Testing

Systems with ≥8 channels represented 62.1% of 2024 sales as manufacturers pursue statistical validation across large cell populations. The battery cyclers market benefits when facilities configure ≥16 channels per rack, a segment tracking a projected 16.7% CAGR to 2030. High channel density reduces floor-space cost per unit tested and aligns with gigafactory takt times. Automated switching matrices match cells to power supplies in real time, trimming idle capacity and boosting overall equipment effectiveness.

Research labs still purchase single- or 2-channel instruments for exploratory work requiring flexible waveform scripting and ultra-high accuracy. Medium-scale developers often accept 2–7-channel units for pilot lines where budget restraints outweigh need for mass parallelism. Across all groups, integration with manufacturing execution systems (MES) and data lakes is now standard to satisfy traceability rules and predictive-maintenance algorithms.

By Power Range: Medium-Power Dominance Reflects Application Diversity

Medium-power cyclers (10–100 A) accounted for 49.8% revenue in 2024 because they cover cell and module testing for both EV and stationary storage. These units provide an optimal balance of footprint, cost, and flexibility, making them staple equipment for Tier-1 suppliers. The battery cyclers market share of >100 A systems is set to climb as fast-charging R&D pushes current envelopes; their 16.1% CAGR through 2030 will outstrip overall demand. Hardware vendors respond with regenerative architectures that recapture up to 93% of energy and suppress heat output.

At the low end, <10 A precision testers remain vital for coin, pouch, and wearable-device cells where microamp leakage resolution matters more than brute force. High-power rigs, meanwhile, face mounting thermal-safety hurdles at 800 V stacks, triggering innovations in liquid cooling, insulated-gate drive, and redundant shutdown logic. Suppliers offering turnkey safety cabinets gain traction among integrators unwilling to self-engineer containment.

By End-User Industry: Automotive Leadership Faces Energy Sector Challenge

Automotive OEMs and pack integrators constituted 45.5% of 2024 revenue, reflecting the volume of formation, grading, and end-of-line quality checks in EV supply chains. Yet utility operators and independent power producers are the fastest-growing buyers as the energy and power segment registers a 15.9% CAGR to 2030. Long-duration storage, virtual-power-plant aggregation, and frequency-regulation markets extend test durations and impose deeper cycle counts per module.

Consumer electronics firms continue ordering sub-10 A cyclers tailored for mobile devices, while universities and national labs demand ultra-high-precision units for fundamental electrochemistry. Aerospace and defense programs impose extremes of vibration, vacuum, and temperature, spawning micro-gravity cycler variants that validate CubeSat batteries across low-Earth-orbit profile swings. Collectively, these niche orders foster product diversity, permitting vendors to differentiate on specialty features.

Geography Analysis

Asia-Pacific recorded 43.7% revenue in 2024, underpinned by China’s control of more than 75% of lithium-ion cell capacity and 65.4% of influential research outputs. Strong governmental support, deep value-chain integration, and an expanding domestic EV market accelerate the adoption of AI-enabled cycler platforms optimized for high-volume lines. Japan and South Korea concentrate on solid-state pilots scheduled for 2028 mass production, potentially resetting performance benchmarks and creating premium demand for nanovolt-level instrumentation.

North America is on a steep growth trajectory, backed by more than USD 60 billion in announced cell factories and mandates for localized supply chains. The region’s battery cyclers market benefits from dual-chemistry R&D—high-nickel long-range cells and low-cost LFP variants—requiring flexible equipment capable of switching protocols on the fly. Regulatory emphasis on durability (10 years/150,000 miles) and safety analytics drives extended-cycle and abuse-test purchases, often bundled with machine-learning analytics subscriptions.

Europe prioritizes stationary storage for grid stabilization amid aggressive renewable targets. Germany forecasts 24 GW of utility storage by 2037, and EU rules now stipulate digital material tracking, pushing demand for seamless MES integration. Local vendors compete on low-carbon manufacturing credentials, while established Asian suppliers partner with European contract test houses to retain share. Eastern European economies provide cost-competitive labor pools for cycler assembly lines, widening regional sourcing options without compromising regulatory compliance.

Competitive Landscape

First-tier suppliers, Arbin Instruments, Chroma ATE, Neware Technology, and Bio-Logic Science Instruments, collectively dominate the mid- to high-precision brackets. Their entrenched installed bases, global service networks, and extensive software libraries yield switching-cost advantages. Mid-tier firms such as Maccor, Gamry, and Bitrode compete through niche specializations in high-voltage packs or impedance spectroscopy. New entrants emphasize AI-driven analytics, cloud connectivity, and virtual-testing modules that couple hardware with digital twins.

Strategic alliances shape differentiation. Emerson’s stake in EecoMobility provides an embedded analytics layer across its industrial-automation portfolio, expanding addressable revenue beyond hardware. TWAICE’s partnership with Element Materials Technology gives European analytics IP a foothold in U.S. certification labs, integrating cycler data into lifetime models. Toyo Technica’s exclusive Bio-Logic distribution in China strengthens aftermarket service for GOTION and CALB, reinforcing brand stickiness in the region’s incumbent cell giants.

Technology convergence centers on predictive analytics and energy regeneration. Vendors tout up to 95% power-recapture efficiencies and embedded large-language-model code assistants that cut script-development time for new test recipes. Suppliers lacking firmware upgrade paths or cloud APIs risk obsolescence as customers seek total-cost-of-ownership savings via reduced cycle counts and compressed development timelines.

Battery Cyclers Industry Leaders

Arbin Instruments, Inc.

Chroma ATE Inc.

Neware Technology Limited

Bio-Logic Science Instruments SAS

Maccor, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: China imposed export controls on lithium-iron-phosphate process know-how, requiring licenses for outbound technology transfers.

- July 2025: Toyo Technica secured nationwide rights to distribute Bio-Logic cyclers within China, targeting top-tier manufacturers.

- June 2025: Korean and Japanese cell makers increased litigation against Chinese rivals; Tulip Innovation gained an injunction banning specific Sunwoda models in Germany.

- May 2025: Chroma ATE disclosed 4,300 semiconductor test systems installed worldwide and unveiled LLM-driven software migration tools for its battery cycler portfolio.

Global Battery Cyclers Market Report Scope

| Lithium-ion |

| Nickel-based |

| Lead-acid |

| Solid-state and emerging chemistries |

| Single-channel |

| 2-7 Channels |

| Greater than equal to 8 Channels |

| Low Power (Less than 10 A) |

| Medium Power (10 - 100 A) |

| High Power (Greater than 100 A) |

| Automotive |

| Consumer Electronics |

| Energy and Power |

| Research and Academia |

| Aerospace and Defense |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Battery-Chemistry Compatibility | Lithium-ion | ||

| Nickel-based | |||

| Lead-acid | |||

| Solid-state and emerging chemistries | |||

| By Channel Count | Single-channel | ||

| 2-7 Channels | |||

| Greater than equal to 8 Channels | |||

| By Power Range (Max Current / Channel) | Low Power (Less than 10 A) | ||

| Medium Power (10 - 100 A) | |||

| High Power (Greater than 100 A) | |||

| By End-User Industry | Automotive | ||

| Consumer Electronics | |||

| Energy and Power | |||

| Research and Academia | |||

| Aerospace and Defense | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the global battery cyclers market?

The battery cyclers market size is USD 0.92 billion in 2025.

What CAGR is forecast for the battery cyclers market between 2025 and 2030?

The market is projected to grow at a 14.8% CAGR through 2030.

Which region leads the market and how fast is it growing?

Asia-Pacific holds 43.7% of revenue and is expanding at a 16.2% CAGR.

Which end-user industry is the fastest-growing?

The energy and power sector is set to post a 15.9% CAGR, driven by grid-scale storage deployment.

Why are AI/ML features becoming important in battery cyclers?

Predictive analytics reduce test cycles by up to 95% and enhance accuracy, cutting development time and cost.

What is the biggest restraint facing high-power cycler adoption?

High capital expenditure for >100 A systems limits access for smaller manufacturers in the near term.

Page last updated on: