Vehicle Recycling Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

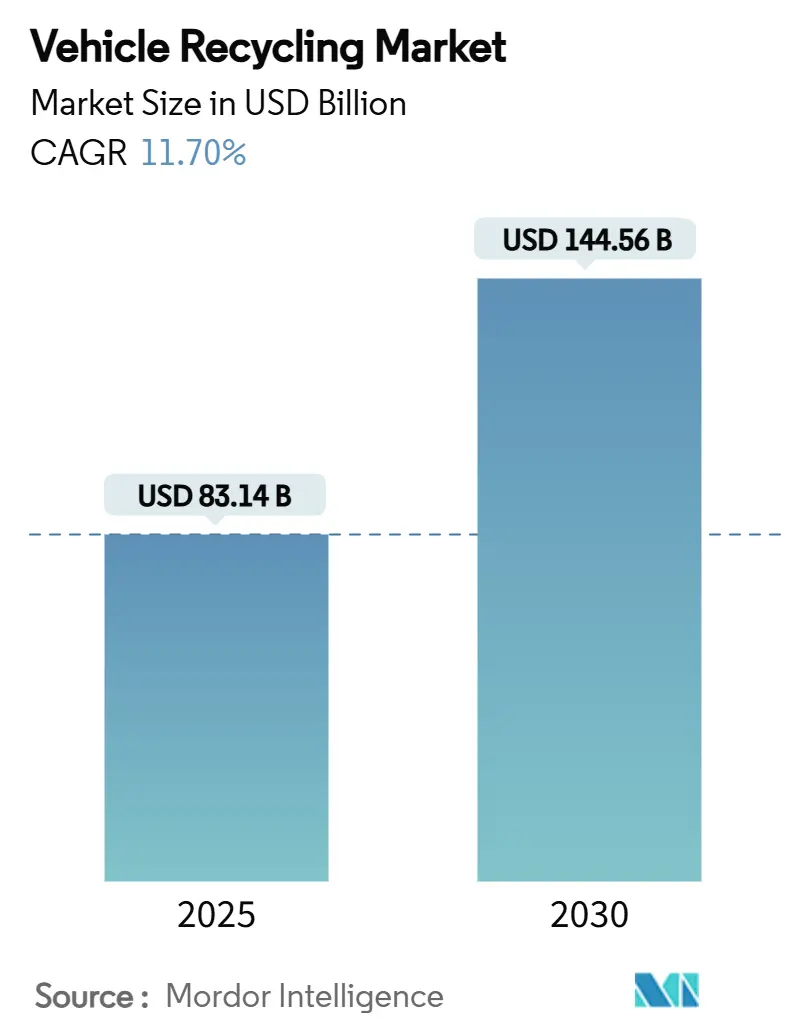

| Market Size (2025) | USD 83.14 Billion |

| Market Size (2030) | USD 144.56 Billion |

| Growth Rate (2025 - 2030) | 11.70% CAGR |

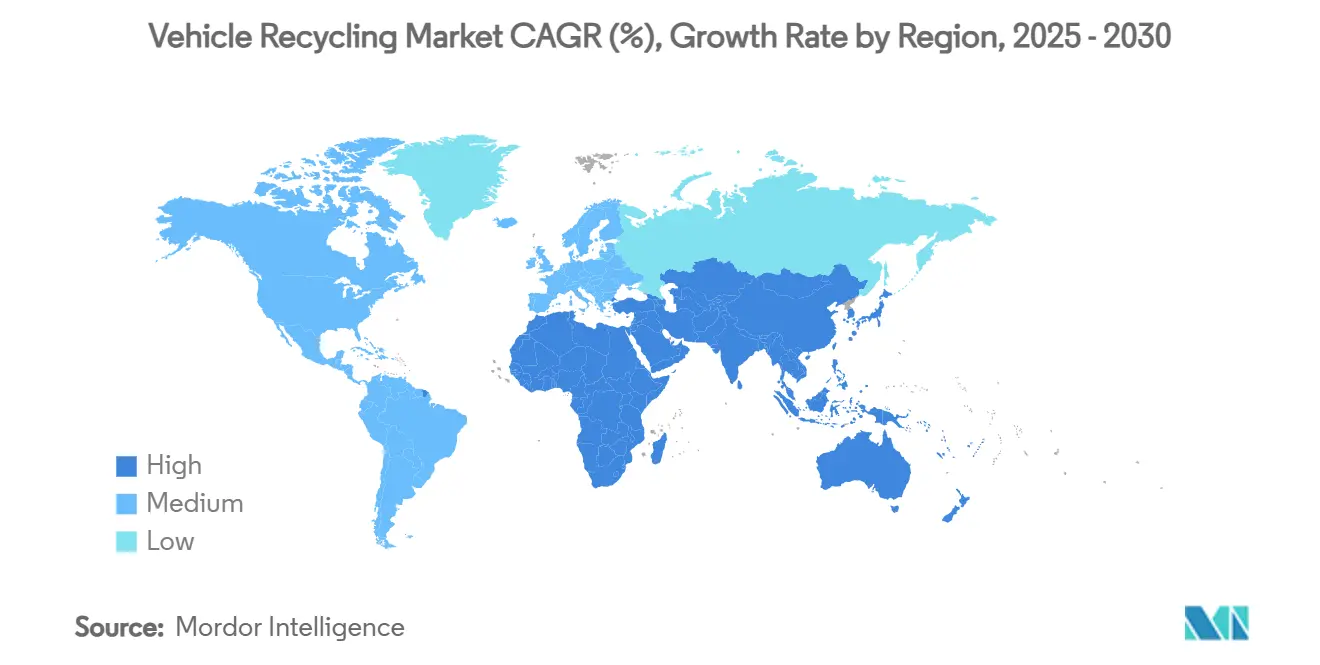

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

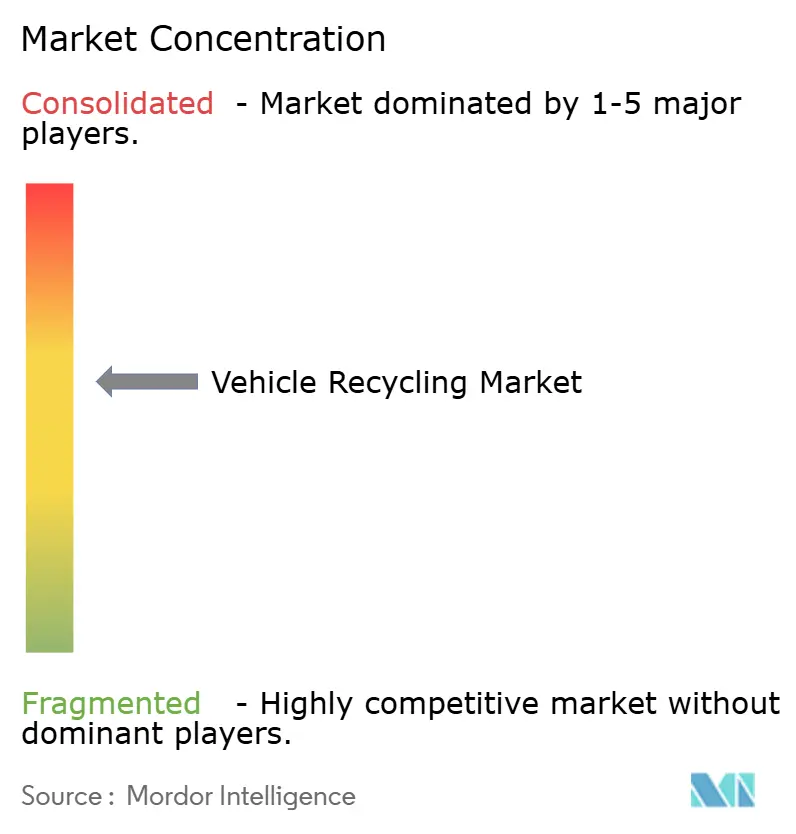

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Recycling Market Analysis by Mordor Intelligence

The vehicle recycling market size stands at USD 83.14 billion in 2025 and is forecast to reach USD 144.56 billion by 2030, reflecting an 11.70% CAGR during the period. Sustained demand for secondary metals, stricter end-of-life directives, and the rapid spread of electric vehicles are together transforming the vehicle recycling market from basic scrap collection to sophisticated material-recovery ecosystems. Automakers now treat recycled steel and aluminum as strategic inputs that hedge commodity volatility, while digital salvage auctions compress the time between vehicle retirement and parts recirculation. Capital is pouring into robotic dismantling and optical-sorting lines that lift recovery yields, yet the vehicle recycling market still contends with high investment thresholds and evolving battery-safety rules. Regional performance diverges: North America commands scale and technology leadership, Europe tightens regulatory screws, and Asia-Pacific supplies the fastest expansion track on the back of China’s and India’s EV booms.

Key Report Takeaways

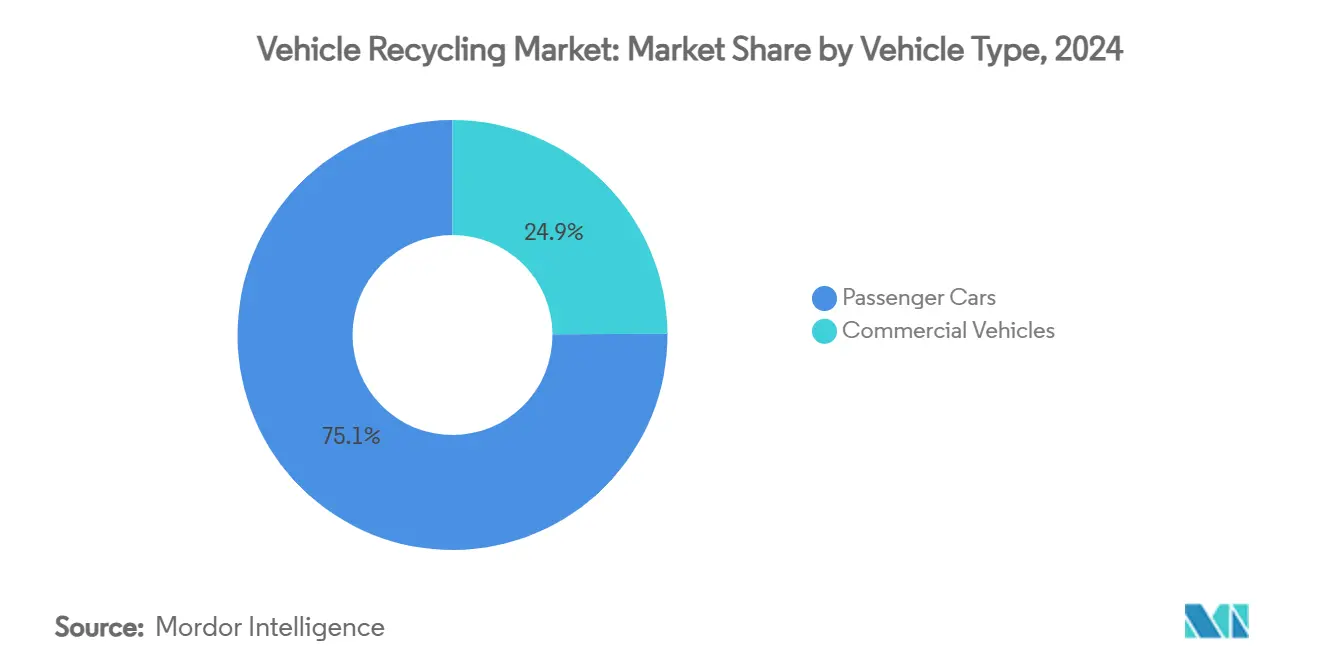

- By vehicle type, passenger cars led with 75.12% of vehicle recycling market share in 2024, whereas commercial vehicles are projected to post a 12.45% CAGR through 2030.

- By material, iron and steel commanded 59.33% share of the vehicle recycling market size in 2024, while aluminum is advancing at a 13.15% CAGR to 2030.

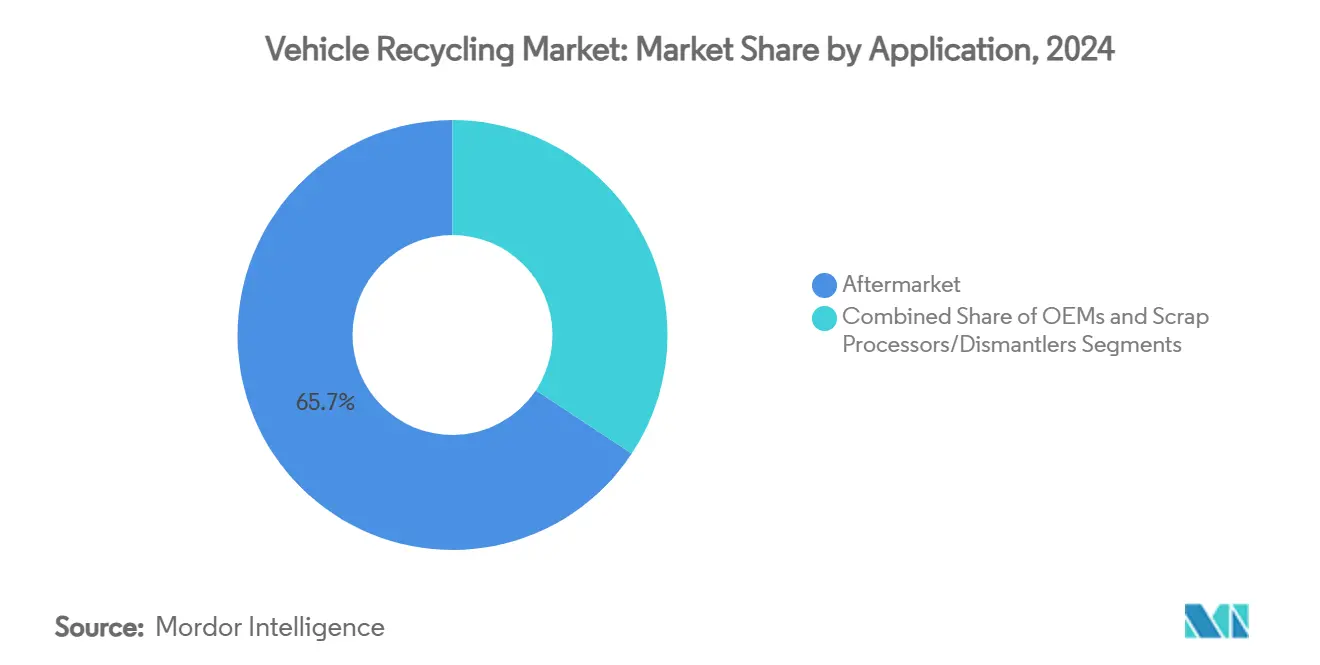

- By application, the aftermarket accounted for 65.72% of the vehicle recycling market size in 2024 and scrap processors/dismantlers are expanding at a 14.16% CAGR through 2030.

- By recycling process, manual dismantling and depollution retained 57.91% of 2024 revenue, yet adavnced lithium-ion battery recycling is climbing at 15.01% CAGR to 2030.

- By geography, North America captured 42.36% of 2024 revenue; Asia-Pacific is forecast to grow at a 13.67% CAGR through 2030.

Global Vehicle Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ELV Directives | +2.1% | EU, China, India with spillover to ASEAN | Medium term (2-4 years) |

| Volatile Virgin-Metal Prices | +1.8% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Recycled Metals for Lightweight EV Frames | +1.5% | North America, EU | Long term (≥ 4 years) |

| OEM Closed-Loop Traceability Pilots | +1.2% | North America, EU, Japan | Medium term (2-4 years) |

| AI-enabled Robotic Dismantling | +0.9% | Developed markets, gradual APAC adoption | Long term (≥ 4 years) |

| Digital Salvage Auctions | +0.7% | Global, fastest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent ELV Directives Drive Regulatory Compliance Investments

Revisions to the European End-of-Life Vehicle Directive now require 25% recycled plastic content in each new automobile by 2030, compelling global manufacturers to embed recyclability at the design stage [1]“Directive (EU) 2024/2730 on End-of-Life Vehicles,” European Commission Directorate-General Environment, Europa, europa.eu. China’s 2024 ELV framework sets a 95% material-recovery target and enforces OEM take-back responsibility, while India’s October 2025 rules introduce extended user responsibility and discharge standards. Harmonization removes competitive disparities, so compliance spending shifts from municipal budgets to corporate balance sheets. Manufacturers respond with modular battery packs and easily detachable components, speeding post-life dismantling and raising recovery economics. Collectively, these mandates add clear volume visibility to the vehicle recycling market, strengthening capital-allocation confidence for new processing facilities.

Metal Price Volatility Accelerates Secondary Material Adoption

Aluminum and copper generate a cost wedge, making recycled inputs irresistible for automakers. OEMs achieve 15-25% savings by opting for recycled aluminum in battery housings. This move is significant, especially considering that battery packs constitute 30-40% of the total bill of materials for electric vehicles (EVs). Steel fluctuated between USD 600-800/metric ton, encouraging distributed sourcing through regional recyclers that smooth supply swings. Analysts expect commodity turbulence to persist as global mining fails to keep pace with burgeoning EV material demand, reinforcing structural pull for the vehicle recycling market. As a result, procurement contracts increasingly embed indexed premiums for certified recycled feedstock.

EV Lightweighting Demands Reshape Material-Recovery Priorities

Tesla’s Model Y uses panels that contain 50% recycled aluminum, while BMW’s iVision Circular concept targets fully recyclable content, demonstrating OEM urgency to shed weight without sacrificing structural integrity. Recycled aluminum preserves 95% of its original mechanical strength and consumes 95% less energy than primary smelting, making it the lightest path to range extension for mass-market EVs. Parallel advances in recycled ultra-high-strength steel allow automakers to meet crash standards while trimming curb weight. The mixed-material turn raises recovery complexity but elevates value capture because aluminum and copper command higher margins than ferrous scrap. Consequently, the vehicle recycling market is scaling mixed-metal sorters and data-driven process controls to secure purity that meets stringent OEM input specifications.

OEM Closed-Loop Programs Establish Direct Material Channels

Toyota Tsusho’s USD 907 million purchase of Radius Recycling in 2024 secured end-to-end traceability for critical metals used across Toyota’s global production network. BMW linked with Redwood Materials to internalize lithium, nickel, and cobalt flows, trimming geopolitical risk and satisfying sustainability pledges. Closed-loop agreements collapse the distance between dismantler and factory, collapsing logistic costs and speeding certification cycles. These programs also generate failure-mode data that engineers channel back into design revisions, closing the feedback loop between materials science and product development. The vehicle recycling market evolves from a cost-center disposition function to a profit-oriented supply-chain node anchored by OEM demand visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Advanced Shredding Lines | -1.4% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Fragmented ELV Collection Channels | -0.8% | Asia-Pacific, South America, Africa | Long term (≥ 4 years) |

| Safety Risks of High-Voltage Battery Packs | -0.6% | Global, concentrated in EV-dominant markets | Short term (≤ 2 years) |

| Uncertain Economics of Composite Recycling | -0.4% | North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital Intensity Limits Advanced-Technology Adoption

Investing in a cutting-edge shredder with comprehensive depollution and sensor-driven sorting features is expensive. Additionally, specialized battery dismantling and hydrometallurgical processes require an extra investment[2] “ADuro Shredders for ELV Processing,” ANDRITZ AG Product Brochure, ANDRITZ, andritz.com. Smaller recyclers often lack collateral and face volatile scrap margins that discourage large loans, pushing them toward low-tech manual operations. The widening tech divide risks excluding SMEs from premium copper and aluminum streams that require tight purity controls. Moreover, many developing regions face currency risk that inflates debt-service costs, further delaying upgrades. Until financing models or public-private partnerships emerge, high initial outlays will temper the overall CAGR of the vehicle recycling market.

Collection Infrastructure Gaps Constrain Material Flows

In many emerging economies, informal dismantlers dominate because of low entry barriers and lucrative parts resale. India illustrates the challenge: scattered yards cherry-pick high-value components and abandon lower-value plastics or fluids, degrading aggregate recovery yields. Rural logistics shortcomings elevate transport cost and shrink catchment radii, so legitimate operators struggle to secure feedstock density that justifies automated plants. Weak enforcement lets illicit disposal undercut compliant processors, eroding profit incentives for the formal sector. Without digital traceability or reliable take-back points, the vehicle recycling market forfeits material that could finance technology upgrades and compliance training.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Growth Despite Passenger Car Dominance

Passenger cars delivered 75.12% of vehicle recycling market size in 2024, due to their overwhelming presence on global roads and the mature dismantling ecosystems built around standard sedans and compact SUVs. Collection logistics, parts databases, and pricing models for car components are well-established, producing predictable throughput and margins. However, commercial vehicles are forecast to post a 12.45% CAGR as parcel-delivery fleets electrify and regulators extend low-emission zones to trucks. A single electric delivery van can house a 100-200 kWh pack and thicker gauge wiring, lifting per-unit recycling revenue relative to a passenger EV.

Traditional car recyclers now retrofit lines for larger drivetrains, heavier frames, and more complex hydraulic assemblies present in trucks and buses. Specialized depollution rigs extract fluids at scale, and battery hoists comply with stricter safety protocols for high-voltage packs. The anticipated surge in commercial EV retirements positions this segment as an earnings catalyst within the broader vehicle recycling market.

By Material: Aluminum Acceleration Challenges Steel Supremacy

Iron and steel contributed 59.33% of the vehicle recycling market share in 2024 because magnetic separation remains inexpensive and downstream foundries accept recycled billets without alloy-purity penalties. Demand from construction and heavy machinery guarantees a liquid outlet for shredded and baled ferrous scrap. Nonetheless, aluminum is advancing at a 13.15% CAGR through 2030 as automakers chase mass reduction to extend EV range. With its high resale value, aluminum bolsters plant cash flows, validating investments in eddy-current separators and AI vision systems that greatly enhance purity[3]“Sustainable Steel for Mobility,” Nucor Corporation Investor Presentation, Nucor, nucor.com.

Copper and precious metal recovery from wiring looms and electronics also lifts blended margins, though their absolute tonnage remains modest. Plastic and composite fractions still pose technical hurdles, but progress in chemical recycling now captures resins suitable for battery casings. Ongoing innovation underlines how material diversity elevates both complexity and revenue opportunity for the vehicle recycling market.

By Application: Scrap Processors Gain Ground on Aftermarket Dominance

The aftermarket generated 65.72% of vehicle recycling market size in 2024 as cost-conscious consumers bought reclaimed engines, transmissions, and body panels instead of factory-new parts. Online marketplaces accelerate parts matching, compressing inventory days and lowering overhead. Yet scrap processors and dismantlers are poised for 14.16% CAGR because vertical integration lets them monetize every fraction- from catalytic-converter platinum to lithium salts, inside one facility.

OEMs increasingly specify certified recycled metals, so processors with lab-grade spectrometry win contracts that lock in metal premiums. With scale comes bargaining power over logistics and energy tariffs, reinforcing margin resilience even when commodity prices soften. Consequently, multi-stream processors are emerging as anchor tenants of the modern vehicle recycling market ecosystem.

By Recycling Process: Battery Technology Disrupts Manual Methods

Manual dismantling and depollution kept 57.91% revenue share in 2024, reflecting its flexibility for diverse models and critical roles in safe airbag and refrigerant recovery. Labor-intensive depollution also captures reusable part value that shredders would destroy. However, lithium-ion battery recycling is charting a 15.01% CAGR, propelled by skyrocketing EV adoption and looming battery-waste regulations. Hydrometallurgical lines reclaim up to 90% of lithium, nickel, and cobalt using low-temperature leach processes developed for automotive chemistries.

Advanced shredders now integrate battery module pre-treatment, inert-atmosphere size-reduction, and black-mass extraction before metal separation, reducing hazards while raising yield. Complementary robotic arms execute repetitive screw removal at speeds human staff cannot match, freeing technicians for high-skill diagnoses. This hybrid workflow balances safety, speed, and material integrity, making it the blueprint for the next phase of the vehicle recycling market.

Geography Analysis

North America delivered 42.36% of the vehicle recycling market size in 2024, supported by long-standing scrap networks, federal incentives for battery recycling, and clusters of steel mini-mills hungry for feedstock. The United States hosts several mega-shredders capable of 250 vehicles per hour, while Canada leverages proximity to Midwest OEM plants to secure offtake contracts. Investments such as Gerdau’s USD 60 million Tennessee upgrade underscore continual capacity modernization.

Asia-Pacific is the growth engine, projected at a 13.67% CAGR to 2030. China’s 95% ELV recovery mandate and manufacturer take-back schemes inject formal volumes into licensed facilities; new plants in Guangdong and Jiangsu target battery volumes specifically. India’s October 2025 ELV rules extend user responsibility, spurring joint ventures between domestic steelmakers and global dismantling specialists. Japan and South Korea export process technology across ASEAN, reinforcing the region’s competitive edge in high-purity aluminum and copper recovery.

Europe sustains a leading regulatory posture. The revised directive on end-of-life vehicles enforces recycled-plastic quotas and stricter depollution standards. Multinational programs such as Renault-Suez’s EUR 140 million circular-economy plan expand high-efficiency plants in France and Spain, ensuring stable demand for certified recyclate. Although the Middle East, Africa and South America presently trail in infrastructure, rising vehicle ownership, import regulations on salvaged vehicles and international climate commitments are expected to guide incremental capacity build-out, integrating these regions more tightly into the vehicle recycling market.

Competitive Landscape

The vehicle recycling market retains medium fragmentation but is trending toward consolidation as technology costs soar. In North America and Europe, the top five firms control roughly 55-60% of licensed throughput, while Asia-Pacific still counts thousands of micro-yards dealing mainly in hand-pulled parts. Capital-heavy upgrades give scale players structural cost advantages and bargaining power with OEM buyers of recycled metals.

Strategic activity is dominated by vertical integration. Toyota Tsusho’s acquisition of Radius Recycling gave the automaker an owned channel for steel and non-ferrous feedstock, while LG Energy Solution’s 2025 joint venture with Toyota targets 95% recovery of lithium, nickel, and cobalt from retired packs. Such deals shorten material travel distances, expedite certification, and embed traceability into corporate ESG narratives.

Technology partnerships are equally intense. Li-Cycle and Redwood Materials license hydrometallurgical know-how to global battery assemblers, securing offtake agreements for black-mass concentrates. Meanwhile, plant-equipment suppliers like ANDRITZ roll out sensor-fusion sorting and inert-gas shredding lines tailored for EV architectures. Competition thus revolves on who can most rapidly align process capability with OEM design shifts, reinforcing demand visibility and propelling the vehicle recycling market.

Vehicle Recycling Industry Leaders

LKQ Corporation

Sims Metal Management Ltd.

Copart Inc.

European Metal Recycling (EMR)

Schnitzer Steel Industries (Radius Recycling)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: In a move underscoring the growing emphasis on sustainability, LG Energy Solution and Toyota Tsusho Corporation have unveiled their joint venture, Green Metals Battery Innovations, LLC, dedicated to battery recycling. The agreement, inked by LG Energy Solution Michigan and Toyota Tsusho America, paves the way for the duo to set up and manage a pre-processing facility in Winston-Salem, North Carolina.

- October 2024: Alongside Renault Group, which commands an 80% stake, Suez secures a 20% stake in "The Future Is NEUTRAL," an entity focused on the automotive circular economy. This partnership aims to strengthen efforts in promoting sustainable practices within the automotive industry by leveraging both companies' expertise in recycling and resource management.

- September 2024: Gerdau Ameristeel, a North American subsidiary of Brazilian steel giant Gerdau, has inked a USD 60 million deal to acquire assets from the American Dales Recycling Partnership, as reported by NoticiasDe. Dales Recycling specializes in processing ferrous scrap. The acquisition encompasses land, inventory, and fixed assets tied to Dales' operations in Tennessee, Kentucky, and Missouri. This strategic move aims to bolster Gerdau's scrap processing capabilities, ensuring a steady supply of competitively priced raw materials for its operations.

- September 2024: In a significant move towards sustainability, BMW of North America has teamed up with Redwood Materials to recycle lithium-ion batteries. This initiative encompasses batteries from all electric, plug-in hybrid, and mild hybrid vehicles, including those from BMW, MINI, Rolls-Royce, and BMW Motorrad, across the U.S. This collaboration marks a pivotal step in establishing a closed-loop circular value chain for lithium-ion batteries in the country.

Global Vehicle Recycling Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Iron and Steel |

| Aluminum |

| Rubber |

| Copper |

| Glass |

| Plastic |

| Others |

| OEMs |

| Aftermarket |

| Scrap Processors/Dismantlers |

| Manual Dismantling and Depollution |

| Shredding and Magnetic/Eddy Sorting |

| Advanced Li-ion Battery Recycling |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Material | Iron and Steel | |

| Aluminum | ||

| Rubber | ||

| Copper | ||

| Glass | ||

| Plastic | ||

| Others | ||

| By Application | OEMs | |

| Aftermarket | ||

| Scrap Processors/Dismantlers | ||

| By Recycling Process | Manual Dismantling and Depollution | |

| Shredding and Magnetic/Eddy Sorting | ||

| Advanced Li-ion Battery Recycling | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the vehicle recycling market?

The vehicle recycling market size is USD 83.14 billion in 2025 and is projected to reach USD 144.56 billion by 2030.

Which region leads the vehicle recycling market today?

North America holds the lead with 42.36% revenue share in 2024 owing to mature infrastructure and strong regulatory compliance.

Why is aluminum recycling growing faster than steel recycling?

Automakers need lightweight metals for electric-vehicle range, and recycled aluminum offers 95% energy savings over primary smelting while retaining strength.

How fast is lithium-ion battery recycling expanding?

Battery-focused recycling lines are expected to grow at 15.01% CAGR to 2030 , due to the surge in electric-vehicle retirements and strict disposal rules.

Page last updated on: