Stolen Vehicle Recovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.63 Billion |

| Market Size (2031) | USD 13.83 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

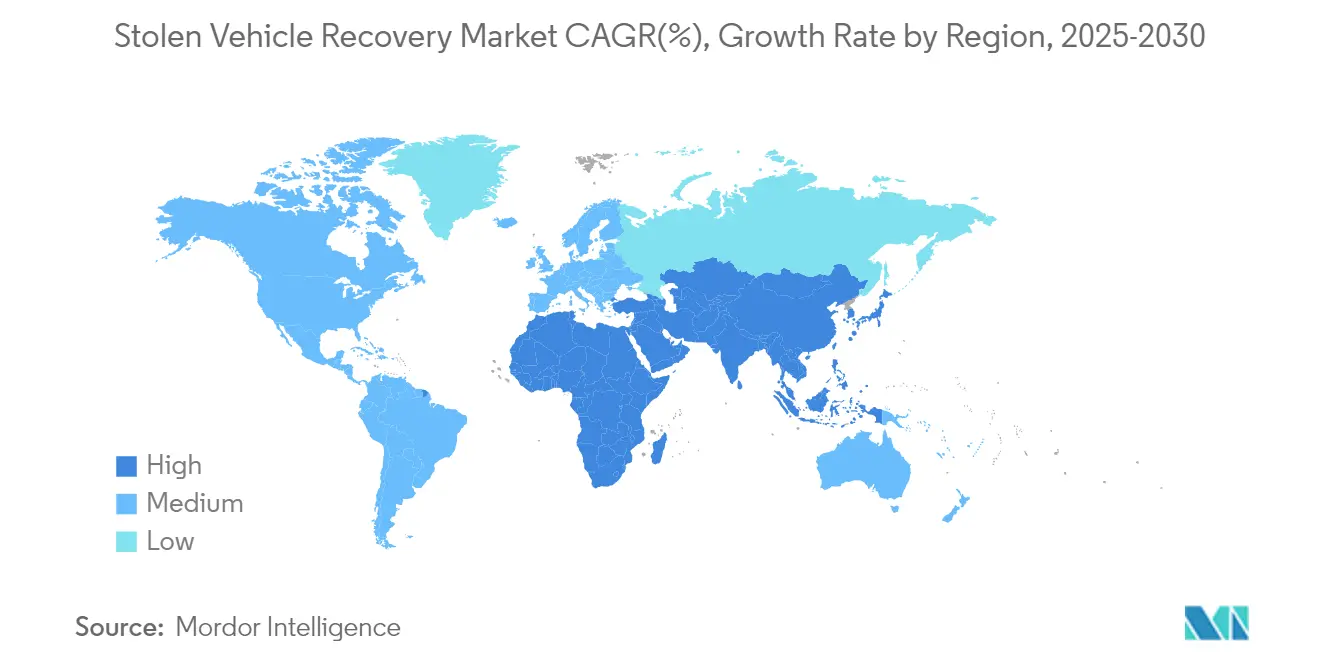

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

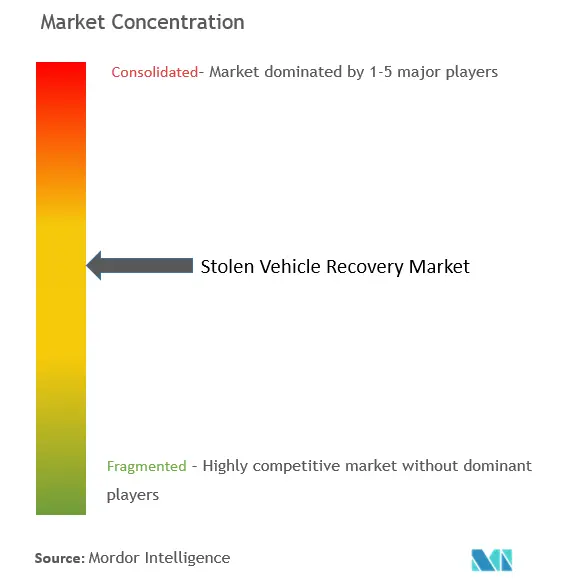

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stolen Vehicle Recovery Market Analysis by Mordor Intelligence

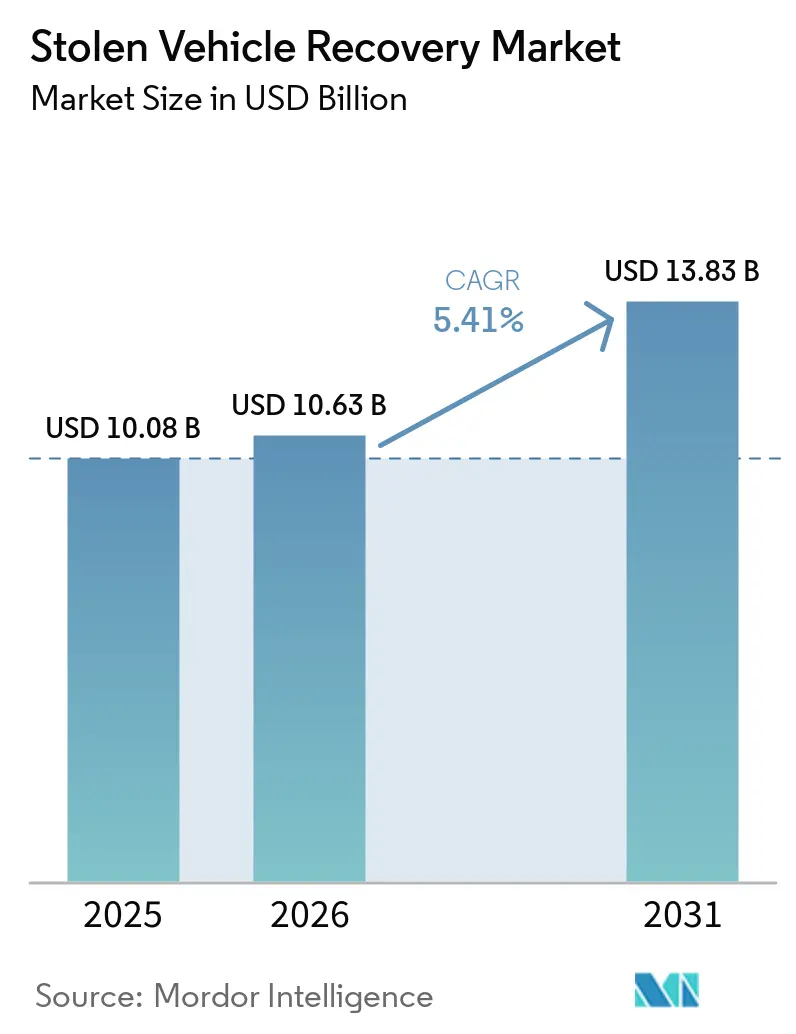

The Stolen Vehicle Recovery Market size is expected to grow from USD 10.08 billion in 2025 to USD 10.63 billion in 2026 and is forecast to reach USD 13.83 billion by 2031 at 5.41% CAGR over 2026-2031. Rapid theft-response programs, stricter safety mandates, and the pivot toward data-driven mobility services are redefining competitive priorities. Collaborations among automakers, law-enforcement agencies, and telematics vendors have already cut reported thefts in the United States by 17% yearly, confirming the market’s sensitivity to coordinated countermeasures. Europe’s General Safety Regulation II, effective July 2024, embeds telematics hardware in every new vehicle, unlocking a broad installed base for security applications. Low-power wide-area technologies compress device costs, spurring aftermarket demand in price-sensitive geographies. Meanwhile, privacy rulings that define Vehicle Identification Numbers as personal data compel providers to redesign data-handling practices to retain customer trust. Platform consolidation intensifies as financially stressed incumbents merge with cash-rich cybersecurity specialists in pursuit of scale efficiencies and cross-selling.

Key Report Takeaways

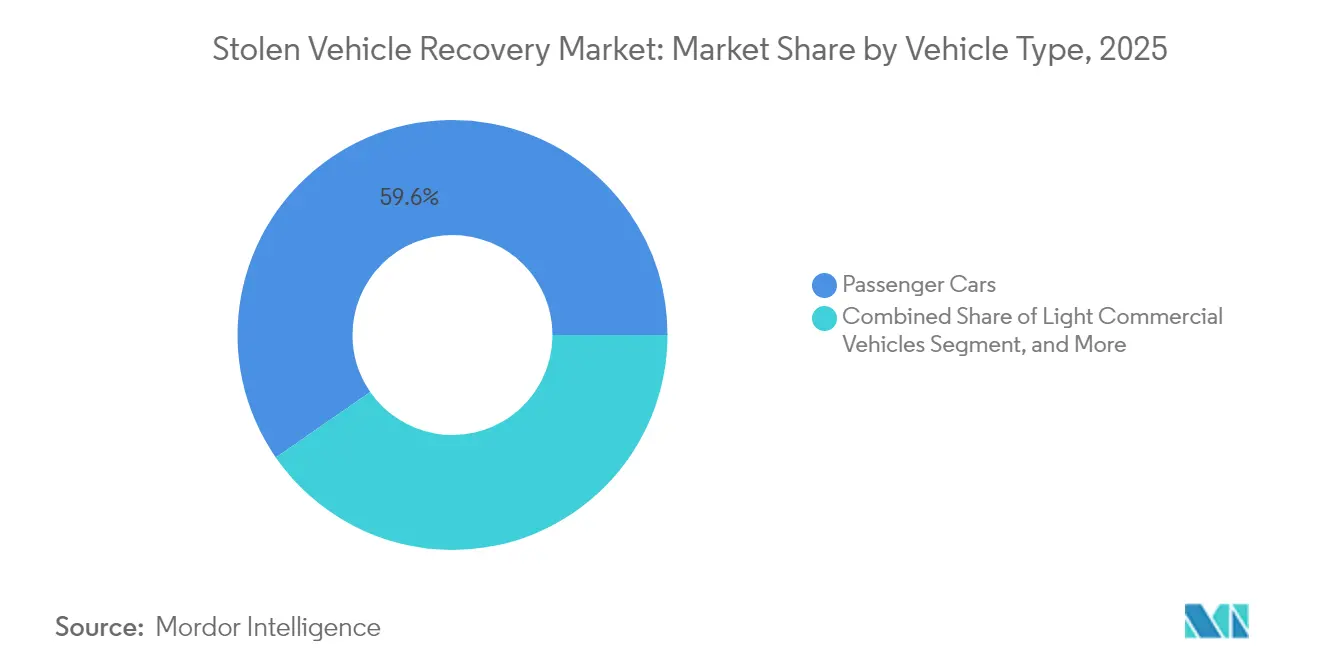

- By vehicle type, passenger cars led with 59.64% of the vehicle security and recovery market share in 2025, while two-wheelers and powersports are projected to grow at a 7.71% CAGR through 2031.

- By technology, GPS/GNSS held 62.12% revenue share in 2025, whereas LoRa/NB-IoT is forecast to expand at a 9.38% CAGR to 2031.

- By security solution, tracking and recovery devices commanded a 47.36% share of the vehicle security and recovery market size in 2025, and immobilizers are advancing at an 8.34% CAGR.

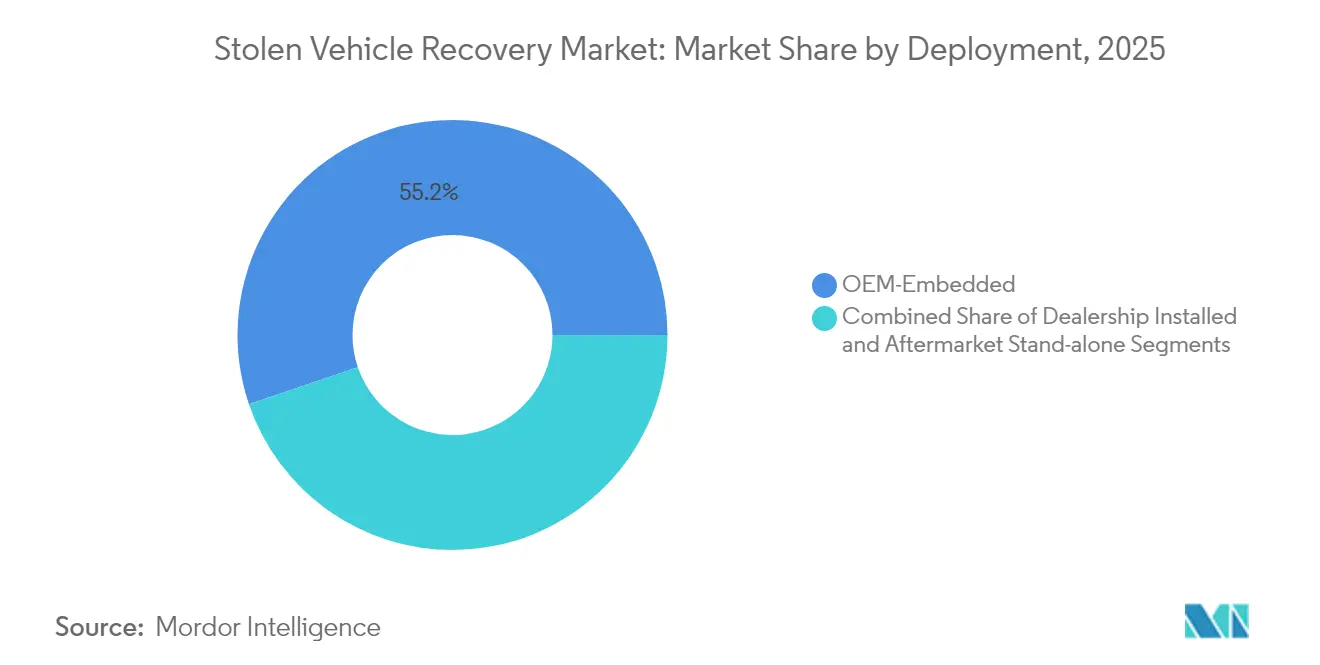

- By deployment, OEM-embedded systems led with a 55.21% share in 2025, while dealer-installed solutions are rising fastest at an 8.19% CAGR.

- By end-user, personal vehicle owners accounted for 44.87% of the vehicle security and recovery market size in 2025, and rental & leasing firms show the highest projected CAGR at 7.29%.

- By geography, North America held 36.22% of the vehicle security and recovery market share in 2025; Asia-Pacific is set to progress at a 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stolen Vehicle Recovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic theft spike | +1.2% | North America & Europe | Short term (≤2 years) |

| Mandatory OEM telematics/eCall | +0.9% | Europe; spreading to Asia-Pacific and the Middle East and Africa | Medium term (2-4 years) |

| Insurance-telematics incentives | +0.7% | North America and Europe; Asia-Pacific emerging | Medium term (2-4 years) |

| Key-fob hacking vulnerabilities | +0.6% | Developed markets worldwide | Short term (≤2 years) |

| Fleet sharing demands real-time recovery | +0.4% | Global urban hubs; Asia-Pacific leading | Long term (≥4 years) |

| Low-cost LoRa/NB-IoT aftermarket trackers | +0.5% | Asia-Pacific core; Middle East and Africa, South America spill-over | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Vehicle-Theft Incidence Post-Pandemic

Theft volumes surpassed 1 million units in the United States during 2023, the highest tally since 2008, before dropping to 850,708 in 2024 after targeted enforcement campaigns and manufacturer software fixes[1]“Vehicle Theft Trend Analysis 2024,”, National Insurance Crime Bureau, nicb.org. Push-button ignition exploits, amplified on social media, highlighted vulnerabilities in certain Hyundai and Kia models and spurred multi-layer security retrofits. Similar spikes were recorded in Victoria, Australia, where electronic re-programming devices allowed criminals to mimic key signals, prompting a 20-year theft high. Technology suppliers responded by integrating real-time immobilization with GPS beacons, producing measurable deterrence, particularly in urban corridors. Therefore, the cyclical nature of theft keeps baseline demand solid for both aftermarket kits and factory-installed recovery modules.

Stringent OEM Telematics/eCall Mandates

Europe’s General Safety Regulation II standardizes intelligent speed assistance, emergency braking, and event recorders on every new light vehicle, establishing built-in connectivity that security vendors can repurpose for theft recovery[2]“Regulation (EU) 2019/2144: General Safety Regulation II,”, European Commission, ec.europa.eu. Russia’s ERA-GLONASS and Brazil’s SIMRAV provide similar regulatory footholds, while the United States is reviewing V2V communication rules at the Federal Communications Commission. Tier 1 suppliers such as Continental have packaged security features—remote immobilization, stolen-vehicle tracking, and cyber-hardening—as compliance enablers for automakers integrating GSR II functions[3]“GSR II Compliance Portfolio,”, Continental AG, continental.com. These rules create predictable installation volumes and favor long-term OEM alliances over discretionary aftermarket sales.

Insurance-Linked Discounts & Partnerships

Insurers increasingly reward security-equipped vehicles with lower premiums, turning telematics units into revenue-sharing devices. Munich Re reports that 54% of large and 37% of small fleets in North America now transmit driving data for dynamic risk pricing[4].“Telematics Adoption in Commercial Motor Insurance,”, Munich Re, munichre.com European carriers, supported by the 2025 EU Data Act, can access OEM data feeds with customer consent, broadening telematics adoption beyond high-end vehicles. Chinese insurer Ping An P&C launched “Intelligent Driving Protection” with FAW Hongqi, embedding theft-prevention analytics into usage-based products. These partnerships transform one-time hardware margins into recurring subscription income for security vendors.

Key-Fob Hacking Surge

According to peer-reviewed testing, relay and rollback attacks compromise passive-entry systems in roughly 40% of sampled vehicle models. Automakers have begun integrating ultra-wideband chips for centimeter-level key authentication, yet researchers still demonstrate spoofing via “accurate deafening” techniques. Multi-factor methods such as PIN-to-drive—pioneered by Tesla—cut unauthorized start rates by as much as 90%. Demand is shifting toward combined RF shields, encrypted key exchanges, and cloud-verified immobilizers that thwart digital and mechanical intrusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & subscription costs | -0.8% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Signal jamming / device tampering risk | -0.4% | Global, concentrated in high-crime urban areas | Short term (≤ 2 years) |

| Data-privacy regulations curbing continuous tracking | -0.6% | Europe primary, expanding globally | Long term (≥ 4 years) |

| OEM-embedded trackers saturating premium segment | -0.3% | North America and Europe core, Asia-Pacific emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Subscription Costs

Price remains the decisive hurdle among lower-income users. LoRa/NB-IoT tags offer multi-year battery life at materially lower costs and spread quickly through Semtech-powered trackers. Verizon Connect has eased entry barriers by introducing month-to-month contracts, helping dealers bundle security without long lock-ins[5]“Verizon Connect Product Update Jan 2025,”, Verizon Communications, verizon.com. Even so, many emerging-market buyers weigh security outlays against basic mobility expenditures, tempering overall uptake.

Data-Privacy Regulations Curbing Continuous Tracking

The Court of Justice of the European Union has ruled Vehicle Identification Numbers to be personal data whenever linked to individuals, obliging automakers to anonymize or encrypt any shared records. The EU Data Act further broadens user control over connected-vehicle datasets, potentially limiting always-on tracking unless explicit consent is obtained. A 2024 Federal Trade Commission settlement in the United States prohibits OnStar from forwarding granular driving data to third parties without customer approval. Providers now hard-wire privacy-by-design frameworks—zero-knowledge encryption, owner-only decryption keys, and data-minimization policies—to stay compliant while still delivering effective theft-response performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Drive Growth Acceleration

Passenger cars retained a 59.64% share in the stolen vehicle recovery market in 2025 revenue, but the motorcycle and power sports segment is growing at a 7.71% CAGR through 2031. Asia-Pacific’s dense cities depend on scooters for last-mile transport, elevating theft risk and pushing system fit-outs. Bosch has migrated its eBike battery-lock technology to small-engine vehicles, using Bluetooth authentication to deactivate powertrains when unauthorized movement is detected bosch.com.

Two-wheelers typically lack embedded telematics, so aftermarket GPS beacons and motion sensors fill the gap, often bundled with pay-as-you-go app subscriptions. Declining component prices have reduced total ownership costs, expanding reach into mid-tier models. Fleet delivery services favor tamper-proof immobilizers that reduce downtime, reinforcing the segment’s out-performance relative to heavier vehicle classes.

By Technology: LoRa/NB-IoT Disrupts GPS Dominance

GPS/GNSS solutions represented 62.12% of the stolen vehicle recovery market size in 2025. Yet low-power LoRa and NB-IoT trackers are capturing share at a 9.38% CAGR as they operate on a coin-cell battery for multiple years and transmit indoors where GNSS signals fade. Hybrid devices pair GNSS for localization with LoRa backhaul to trim SIM fees, making them attractive for bikes, trailers, and construction equipment.

Satellite links remain vital for remote mining fleets and maritime cross-border shipments, evidenced by Iridium’s 8% commercial IoT subscriber growth to 2.46 million in 2024, iridium.com. Cellular 4G/5G modules support high-bandwidth video and over-the-air firmware updates for premium passenger cars. Suppliers increasingly ship combo boards that automatically switch among LPWAN, cellular, and satellite channels, maximizing coverage while optimizing data-plan economics.

By Security Solution: Immobilizers Gain Traction

Tracking and recovery devices held a 47.36% share in the stolen vehicle recovery market in 2025 revenue, but immobilizers are accelerating at an 8.34% CAGR. Insurers argue that preventing a theft event delivers greater loss reduction than post-incident search, prompting OEMs to tie engine-unlock authorization to encrypted cloud tokens. Current regulations in the United States call for impaired-driver detection by 2026; the same architecture allows remote disablement during theft incidents, effectively merging safety and security mandates.

Alarm systems and smart keys are evolving into biometric recognition modules- facial ID or fingerprint readers- that act as second-factor checks. Battery-backed sirens and interior motion sensors supplement the immobilizer, providing audio deterrents and real-time intrusion alerts. Suppliers bundle these parts on a single telematics board as they converge, yielding installation efficiencies for dealership technicians.

By Deployment: Dealer-Installed Solutions Accelerate

Factory-fitted systems captured a 55.21% share in the stolen vehicle recovery market in 2025 revenue. Still, dealer-installed packages are rising fastest at an 8.19% CAGR as manufacturers co-develop white-label suites with security specialists. Dealers favor plug-and-play hardware flashed with OEM credentials, preserving warranty coverage while letting retailers upsell service contracts. Bosch’s Roadside Protect acquisition grants access to 12,000 towing partners, enabling dealers to bundle rapid recovery assistance alongside installation.

Flexible billing- month-to-month plans, mid-contract upgrades, remote diagnostics- helps dealers retain customers well beyond the initial vehicle sale, a key revenue hedge as electrification lengthens maintenance intervals. Stand-alone aftermarket channels still prosper in older-vehicle retrofits, particularly in South America, where gray-import units often lack inbuilt connectivity.

By End-User: Rental & Leasing Drives Adoption

Personal owners held a 44.87% share in the stolen vehicle recovery market in 2025, but rental and leasing companies are forecast to expand at a 7.29% CAGR. Asset pools spanning thousands of cars across multiple cities require unified dashboards that flag unauthorized movement, mileage overruns, and tamper attempts. Merchants Fleet’s partnership with Ridecell automates lifecycle commands- unlock, fuel level, immobilize- directly from a cloud console.

Insurers and finance houses increasingly insist on certified trackers before underwriting high-value fleets, locking in demand. Government agencies remain niche buyers of covert beacons for evidence collection, influencing ruggedization and encryption standards that later migrate to civilian models.

Geography Analysis

North America contributed a 36.22% share in the stolen vehicle recovery market in 2025 revenue, anchored by embedded telematics penetration and insurer discounts. U.S. thefts fell to 850,708 in 2024 after topping 1 million the prior year, demonstrating the elasticity of theft patterns to coordinated crackdowns and software patches. Over-the-air firmware fixes issued by OEMs such as Hyundai highlight how cloud connectivity can blunt large-scale exploit campaigns without physical recalls. Canada’s collaboration with INTERPOL, which repatriated more than 2,000 stolen SUVs and pickups, underscores cross-border trafficking risks and the need for international roaming connectivity.

Europe benefits from the regulatory certainty of General Safety Regulation II. Automakers must now integrate event data recorders and lane-keeping assistance, giving security vendors instant access to power, antennas, and CAN bus data. The European privacy framework, however, elevates compliance overhead. Security providers that adopted zero-knowledge encryption early enjoy a marketing edge in countries such as Germany and the Netherlands, where consumer associations scrutinize data-sharing clauses. Allianz’s consumer survey confirms that most drivers will trade data for premium discounts, provided transparency is clear.

Asia-Pacific is growing at 8.92% CAGR through 2031. Chinese OEMs equip electric vehicles with always-connected telemetry as standard, enabling remote diagnoses that double as theft-mitigation channels. India’s two-wheeler population exceeds 220 million units, and localized GPS devices priced below USD 30 are rapidly penetrating major metros. Japanese suppliers pioneer ultra-wideband keyless entry chipsets that resist relay attacks, seeding global design templates. South Korean carriers market bundled 5G data plans for car infotainment, adding theft-alert tiers to raise ARPU. INTERPOL’s 2024 operation across West Africa found scores of vehicles stolen from APAC ports, reinforcing the necessity of global satellite backup for cross-continental asset recovery.

Competitive Landscape

Competition is moderate, with platform scale and cybersecurity depth emerging as the key differentiators. Powerfleet’s USD 200 million purchase of Fleet Complete created a 2.6 million-subscriber base, unlocking cross-selling of AI video analytics and generating expected revenues above USD 400 million. Platform Science agreed to acquire Trimble’s telematics assets, combining navigation, compliance, and security on a single stack—an attractive proposition for over-the-road fleets juggling multiple vendors.

Financial stress is forcing smaller GPS box makers out of the field. CalAmp exited Chapter 11 by transferring equity to its senior lenders while continuing day-to-day operations. The restructuring signals that pure-play hardware margins are insufficient without subscription heft. Cyber-specialists such as Upstream Security raised nine-figure funding rounds to monitor anomalies across millions of connected vehicles, positioning themselves as must-have adjuncts to traditional SVR features.

Bosch sold its security and communications division for roughly USD 735 million but simultaneously bought Roadside Protect to strengthen service reach, highlighting renewed focus on mobility-centric offerings. Verizon Connect widened its product suite with near-360° dash cameras and streamlined Driver Vehicle Inspection Reports, cementing stickiness among North American fleets. As insurers, automakers, and telecom operators converge, vendors that present bundled safety, compliance, and theft-response capabilities stand to outpace niche equipment suppliers.

Stolen Vehicle Recovery Industry Leaders

CalAmp (LoJack)

Vodafone Automotive

Robert Bosch GmbH

Verizon Communications

Altron Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ping An P&C and FAW Hongqi launched Hongqi Intelligent Driving Protection Services for connected EVs.

- February 2025: Bosch acquired Roadside Protect, adding 12,000 towing partners across the United States and Canada to accelerate AI-enabled breakdown response.

- September 2024: Semtech and Traxmate partnered to deliver AI-enabled hybrid LoRa asset trackers.

Global Stolen Vehicle Recovery Market Report Scope

A stolen car recovery system is a technological solution to track and locate a stolen vehicle. This system typically utilizes GPS technology to provide real-time location information, aiding law enforcement in recovering the stolen vehicle.

The stolen vehicle recovery market is segmented by vehicle type, technology, solution, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By technology, the market is segmented into GPS tracking, ultrasonic, RFID chips, and other technologies. By solution, the market is segmented into ultrasonic intrusion protection, battery backed alarms, central lock systems, and other solutions. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. The report offers the market size in value terms in USD for all the abovementioned segments.

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium & Heavy Commercial Vehicles (MHCV) |

| Two-Wheelers & Powersports |

| GPS / GNSS |

| Cellular (LTE/5G) |

| RF (VHF/UHF) |

| LoRa / NB-IoT |

| Bluetooth / BLE |

| RFID Tags |

| Ultrasonic |

| Satellite-based |

| Tracking & Recovery Devices |

| Immobilizers |

| Alarm Systems |

| Central Locking and Smart Key |

| Intrusion Sensors |

| Battery-Backed Sirens |

| OEM-Embedded |

| Dealer-Installed |

| Aftermarket Stand-alone |

| Personal Vehicle Owners |

| Fleet Operators and Logistics |

| Rental and Leasing Firms |

| Insurance & Finance Providers |

| Law-Enforcement / Government |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium & Heavy Commercial Vehicles (MHCV) | ||

| Two-Wheelers & Powersports | ||

| By Technology | GPS / GNSS | |

| Cellular (LTE/5G) | ||

| RF (VHF/UHF) | ||

| LoRa / NB-IoT | ||

| Bluetooth / BLE | ||

| RFID Tags | ||

| Ultrasonic | ||

| Satellite-based | ||

| By Security Solution | Tracking & Recovery Devices | |

| Immobilizers | ||

| Alarm Systems | ||

| Central Locking and Smart Key | ||

| Intrusion Sensors | ||

| Battery-Backed Sirens | ||

| By Deployment | OEM-Embedded | |

| Dealer-Installed | ||

| Aftermarket Stand-alone | ||

| By End-User | Personal Vehicle Owners | |

| Fleet Operators and Logistics | ||

| Rental and Leasing Firms | ||

| Insurance & Finance Providers | ||

| Law-Enforcement / Government | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the vehicle security and recovery market by 2031?

By 2031, the Stolen Vehicle Recovery Market is projected to generate revenues of USD 13.83 billion, marking a growth rate of 5.41% CAGR.

Which vehicle segment is expanding the fastest?

Urban adoption and heightened exposure to theft are propelling two-wheelers and powersports units to a robust 7.71% CAGR.

Why are LoRa and NB-IoT technologies gaining traction?

Their cost-effective, low-power design ensures multi-year battery life, making them ideal for reliably tracking price-sensitive or hard-to-reach assets.

What role do insurance partnerships play in market growth?

Insurers provide premium discounts for connected vehicles, transform telematics devices into subscription platforms, and boost the expected CAGR by 0.7% by 2031.

Which region offers the highest growth potential?

Asia-Pacific leads with a 8.92% CAGR, propelled by rapid urbanization, expanding vehicle ownership, and rising awareness of theft risks.

Page last updated on: