Electric Vehicle Battery Recycling Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.88 Billion |

| Market Size (2030) | USD 15.58 Billion |

| Growth Rate (2025 - 2030) | 32.05% CAGR |

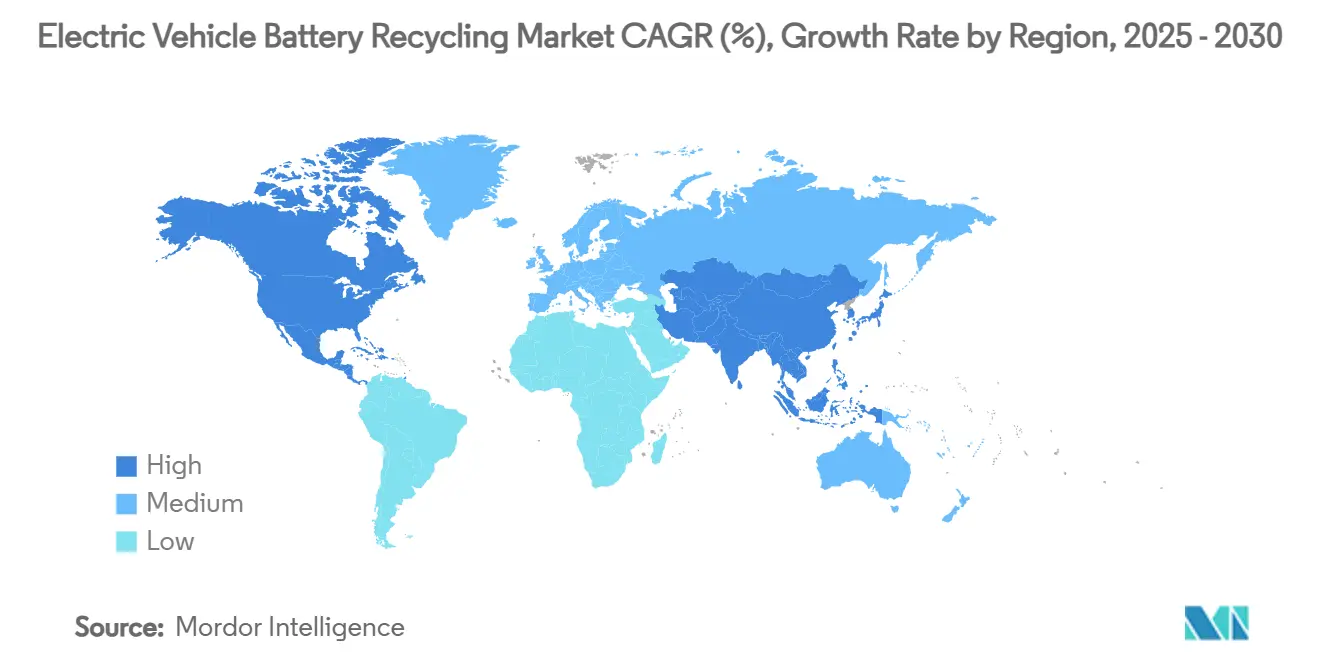

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

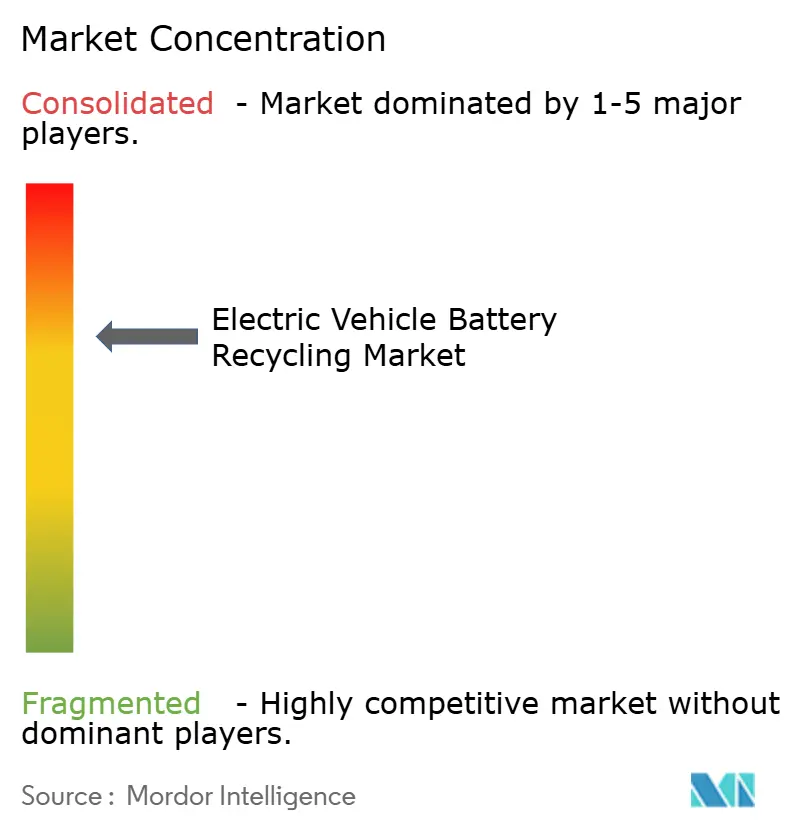

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Battery Recycling Market Analysis by Mordor Intelligence

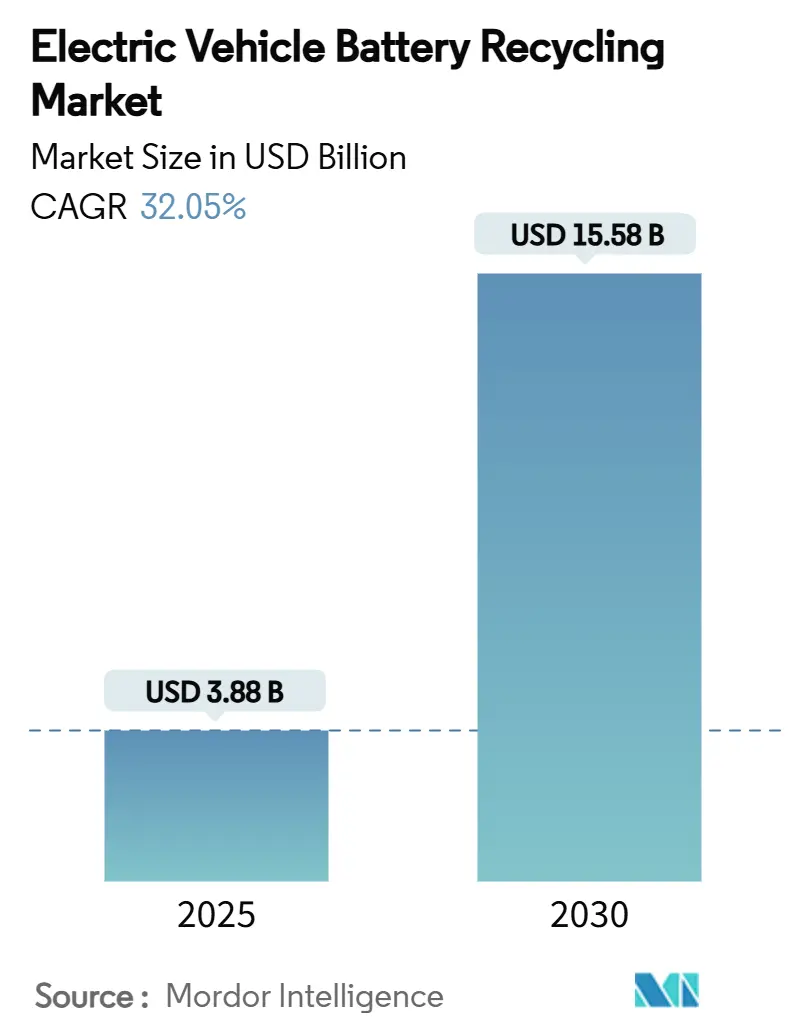

The Electric Vehicle Battery Recycling Market size is estimated at USD 3.88 billion in 2025, and is expected to reach USD 15.58 billion by 2030, at a CAGR of 32.05% during the forecast period (2025-2030). Rising regulatory pressure, a ballooning stream of end-of-life (EoL) packs, and volatile raw-material prices steer capital toward recycling plants, while fast-maturing hydrometallurgical and direct-recycling technologies unlock higher metal yields and lower energy needs. Strategic feedstock alliances between automakers and recyclers shorten supply chains, cut freight emissions, and secure critical minerals. Intensifying competition from mining conglomerates entering the space signals the start of consolidation, yet abundant white-space remains in underserved geographies and chemistries such as lithium iron phosphate (LFP). Finally, rapid two-wheeler electrification in Asia reshapes volume flows and prompts process innovations that handle smaller, more fragmented battery formats.

Key Report Takeaways

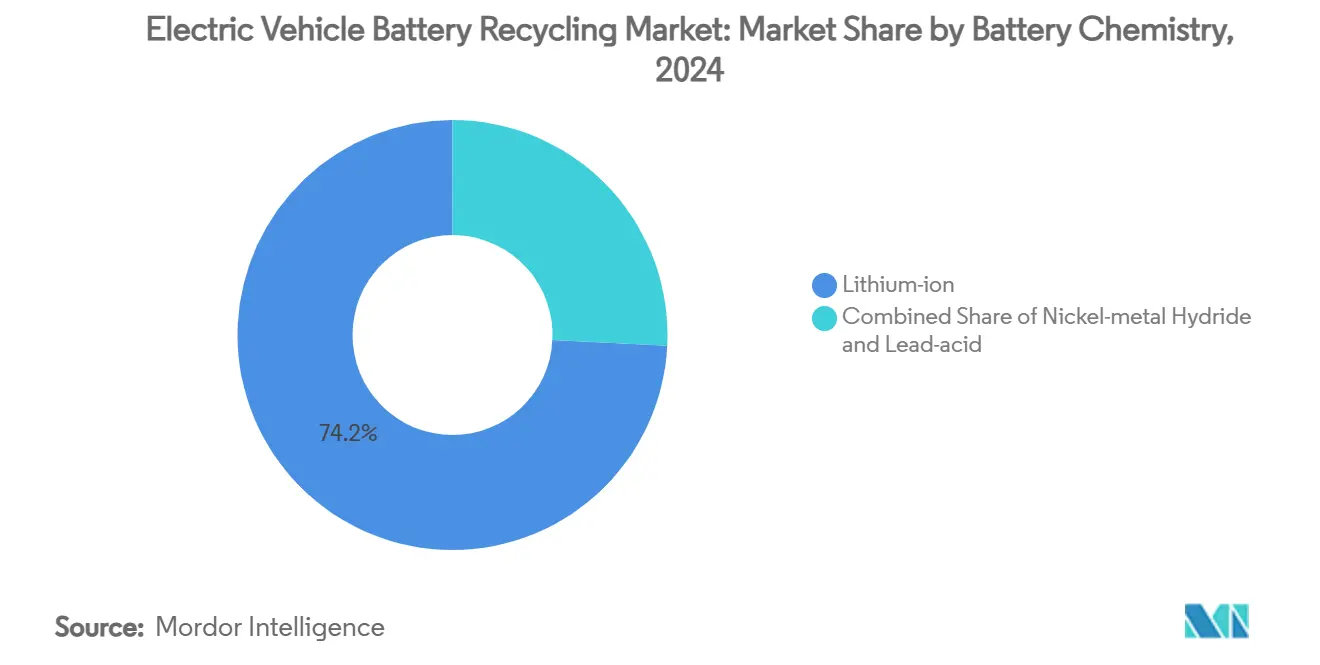

- By battery chemistry, lithium-ion batteries led with 74.17% EV battery recycling market share in 2024, also grows at a robust CAGR OF 32.17% through 2030.

- By source, production scrap commanded 54.37% of the EV battery recycling market in 2024; end-of-life batteries are projected to widen at a 34.15% CAGR through 2030.

- By recycling process, Hydrometallurgical processes accounted for 64.11% of the Electric Vehicle Battery Recycling Market size in 2024, while direct/mechanical recycling is advancing at a 32.82% CAGR to 2030.

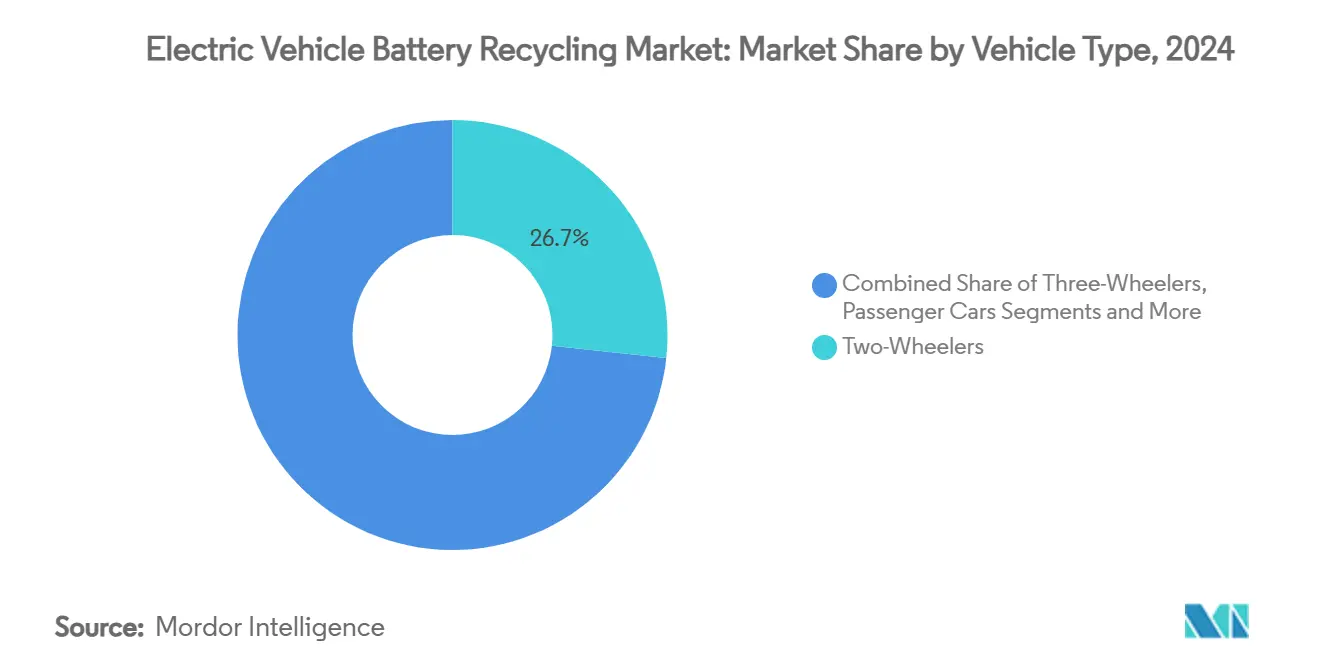

- By vehicle type, two-wheelers led with a 26.73% share of the EV battery recycling market size in 2024 and are projected to advance at a 35.47% CAGR through 2030.

- By recovered material, lithium accounted for 36.58% of the Electric Vehicle Battery Recycling Market size in 2024 and is poised to grow at a 33.71% CAGR to 2030.

- By geography, Asia-Pacific captured 78.52% of the EV battery recycling market share in 2024, and forecast to record the fastest 35.12% CAGR in 2030.

Global Electric Vehicle Battery Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV sales | +9.1% | Global, concentrated in China, Europe, North America | Long term (≥ 4 years) |

| Stringent extended-producer-responsibility | +7.2% | Global, with early gains in EU, China, emerging in US | Medium term (2-4 years) |

| Escalating critical-mineral prices | +6.3% | Global, particularly impacting import-dependent regions | Short term (≤ 2 years) |

| OEM drive for low-carbon | +4.3% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| LFP-specific lithium-recovery economics | +3.2% | APAC core, spill-over to global markets adopting LFP | Medium term (2-4 years) |

| AI-enabled automated pack disassembly | +2.1% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging EV Sales Creating End-of-Life Battery Tsunami

First-wave EV packs sold between 2015 and 2020 are nearing retirement, pushing global EoL volumes toward 315 GWh by 2030, equal to packs for 3.9 million long-range EVs.[1]“Global EV Outlook 2024,” International Energy Agency, iea.org China alone processed nearly six lakh tons in 2024. Because EoL batteries carry higher metal concentrations than production scrap, margins improve by 25-35%. Regions with early EV adoption—Norway and California—face acute waves by 2026, allowing recyclers to lock in supply contracts before feedstock tightens.

Stringent Extended-Producer-Responsibility Mandates

Mandatory recycling quotas transform the EV battery recycling market from a speculative venture to a regulated utility. The EU Battery Regulation 2023/1542 requires 16% minimum for cobalt, 6% for lithium, and 6% for nickel recycled content in new batteries by 2031. China’s producer-responsibility framework obliges makers to hand batteries to certified recyclers, while New Jersey’s 2024 law established the first US statewide collection fees. These policies guarantee feedstock volumes, underpin plant utilisation, and impose penalties that raise switching costs for OEMs. As a result, recyclers gain predictable revenue streams and easier access to project finance.

Escalating Critical-Mineral Prices Boosting Recycled-Material ROI

Even after three-fifths of retreat since 2022 peaks, lithium prices remain triple 2020 levels, and cobalt’s drastic drop still leaves healthy spreads between recycling costs and primary mining.[2]“Battery Metals Prices,” London Metal Exchange, lme.com Recycled lithium carbonate uses more than four-fifths less energy than hard-rock extraction, and at power prices above USD 80/MWh, cost advantages widen toward 40%. Geopolitical disruptions in Congo or Chile amplify the premium for domestically sourced recycled metals, particularly in North America, where OEMs gain Inflation Reduction Act credits for local content.

OEM Drive for Low-Carbon, Localised Supply Chains

Automakers are structuring closed-loop deals to cut Scope 3 emissions and de-risk raw-material exposure. BMW’s agreement with Redwood Materials in South Carolina trims logistics lead times from 60-day ocean transit to 3-day truck hauls, slashing inventory costs. Toyota’s joint venture with LG Energy Solution hinges on recycled inputs to hit 2030 carbon neutrality pathways. Such partnerships cement off-take for recyclers, reward early capacity builders, and spur rapid scaling of direct-recycling lines tuned to each automaker’s cell chemistry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & long payback | -4.7% | Global, particularly impacting new market entrants | Medium term (2-4 years) |

| Volatile black-mass spot prices | -3.8% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Safety & logistics risks | -2.3% | Global, with stricter enforcement in developed markets | Short term (≤ 2 years) |

| Patent thicket around direct-recycling IP | -2.2% | Global, with strongest impact in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Long Payback for Hydromet Plants

A greenfield hydrometallurgical line costs a lot and can take up to 10 years to break even. Umicore’s more than a lakh of tons plant in Belgium carries a million euro price tag. Utilisation rates hover at 30-50% while EoL feedstock is still building, stretching payback horizons and favouring incumbents with strong balance sheets. Consequently, capital-light direct-recycling startups pursue tolling or joint-venture models instead of fully owned hydromet complexes.

Safety & Logistics Risks in HV-Battery Collection

Damaged high-voltage packs fall under Class 9 hazardous-goods rules, necessitating fire-resistant containers and certified drivers. Collection outlays run 40-60% above conventional auto-scrap expenses, and accidents—such as the 2024 fire at Ascend Elements’ Covington hub—inflate insurance premiums. Compliance complexity squeezes small recyclers and raises barriers in rural areas where the pick-up radius exceeds economic limits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-ion Dominance Drives Market Evolution

Lithium-ion packs held 74.17% of the EV battery recycling market in 2024 and are forecast to post a 32.17% CAGR to 2030. NMC variants command premium values due to cobalt worth USD 30,000-50,000 per tonne, whereas LFP value is lower yet improving via 99.6% lithium recovery demonstrated by CATL. Nickel-metal hydride remains niche, primarily from hybrids, and 12 V lead-acid streams provide a steady baseline throughput. The Electric Vehicle Battery Recycling Market size for lithium-ion feedstock is anticipated to widen as first-generation EVs enter the waste stream, raising the share of high-value cathodes and tightening margins for recyclers dependent on production scrap.

Europe’s high-cobalt cell mix contrasts China’s pivot toward LFP, creating geographic price spreads that agile recyclers exploit. Chinese processors benefit from scale and lower labour costs, while European recyclers push process-efficiency gains to manage lower LFP margins. As OEMs commit to chemistries with lower or no cobalt, recyclers invest in flexible lines capable of quickly switching leach recipes, sustaining profitability despite metal-value shifts.

By Source: Production Scrap Yields to End-of-Life Transition

In 2024, production scrap contributed 54.37% of the EV battery recycling market, echoing gigafactory ramp-up rejects. Yet EoL batteries will overtake scrap by 2028 as EoL flows climb 34.15% CAGR. Scrap carries 60-70% useful metal content versus up to 90% in spent packs, raising unit margins. Therefore, the EV battery recycling market size linked to EoL sources will accelerate faster than the overall market and attract new entrants specialised in collection logistics.

Regional variation is marked: Tesla’s Nevada plant yields 15,000 t of scrap yearly, but China is approaching the inflection point where retiring packs exceed manufacturing rejects. Recyclers like Redwood Materials have locked in Panasonic's long-term scrap supply, ensuring baseload throughput while building EoL collection networks that will take over volume leadership later in the decade.

By Recycling Process: Hydrometallurgical Leadership Faces Direct-Recycling Challenge

Hydrometallurgical methodologies represented 64.11% of the EV battery recycling market in 2024, leveraging nickel, cobalt, and copper recovery. However, direct/mechanical routes sprint ahead at a 32.82% CAGR, offering 40% lower costs and 90% less energy use. That performance edge pushes the EV battery recycling industry to pilot hybrid flows such as Ascend Elements’ Hydro-to-Cathode process, which combines dissolution with direct cathode regeneration.

Pyrometallurgical smelting, though energy-intensive, remains vital for preprocessing mixed chemistries and fire-damaged packs. Over the forecast period, the EV battery recycling market size tied to hydrometallurgy will grow. Still, its share will erode as OEMs and regulators recognise the carbon gains from direct recycling. As exemplified by Thoth’s DisMantleBot, AI-powered robotics slashes manual disassembly costs by 60% and boosts line safety, allowing recyclers to service smaller, lower-margin pack formats profitably.

By Vehicle Type: Two-Wheelers Lead Volume and Growth

Two-wheelers captured 26.73% of the EV battery recycling market in 2024 and exhibit the fastest 35.47% CAGR to 2030. Their 2-5 kWh packs cycle out within five years, creating steady, fast-turnover feedstock. Passenger cars will soon dominate absolute tonnage as early Tesla Model S packs age out, but two-wheelers provide predictable volume peaks that smooth plant utilisation. Therefore, this segment's EV battery recycling market share will remain pivotal for Asian recyclers, where delivery fleets and personal mobility converge.

Commercial vehicles, especially buses, present attractive economics due to large pack sizes and fleet management that streamlines collection logistics. Light commercial fleets in North America have begun securing recycling contracts ahead of scheduled replacements, a trend likely to spill into Europe, where municipal bus fleets seek recycling partners that can also deliver carbon-footprint certificates.

By Recovered Material: Lithium Economics Drive Segment Growth

Lithium made up 36.58% of revenue in 2024 and is projected to grow at 33.71% CAGR as supply deficits linger despite mine expansions. Cobalt and nickel yield high margins but face volume dilution as chemistries shift to lower-cobalt designs. Graphite, comprising up to 25% of cell mass, is an under-exploited stream; Chinese firms have already purified and recovered graphite to battery-grade, showing the revenue potential once Western recyclers overcome technology hurdles. Integrated players that extract multiple metals in one flow reach USD 2,500 per tonne processed, doubling single-metal specialists’ returns.

Carbon-adjusted pricing in Europe adds 30% premiums to domestically recycled metals versus imports. This differential is expected to stay as OEMs pursue Scope 3 cuts, ensuring that the EV battery recycling market continues tilting toward integrated, low-carbon operators capable of certifying product pedigree through digital battery passports.

Geography Analysis

Asia-Pacific accounts for the highest EV battery recycling market share of 78.52% in 2024, and records the swiftest 35.12% CAGR, due to China’s nearly six lakh tons of retired battery haul in 2024 and vertically integrated giants like CATL delivering 99.6% lithium recovery. Japan and South Korea specialise in high-purity NMC metal loops, while India’s two-wheeler surge fuels concentrated streams of smaller packs. APAC's EV battery recycling market size will eclipse other regions before 2030, underpinned by policy mandates and domestic demand for battery-grade salts.

Europe EV battery recycling market in 2024, propelled by Regulation 2023/1542, which embeds recycling quotas into product law. Local recyclers could feed metals for 2 million EVs annually by 2030 as Umicore’s more than a lakh tons project and Hydrovolt capacity come online. The region’s growth quickens as compliance deadlines loom and OEMs seek in-region closed loops to earn green-deal incentives.

North America is scaling fast despite a smaller current base. DOE grants and Inflation Reduction Act credits drive rapid capacity additions, such as Redwood Materials’ Nevada hub, which will be capable of serving more than a million EVs annually by 2028.[3]"Advanced Battery Manufacturing Grants", U.S. Department of Energy, energy.gov New Jersey’s 2024 statute offers a template for wider state adoption of stewardship schemes, boosting collection infrastructure. North America's EV battery recycling market is projected to post a 31% CAGR through 2030 as feedstock agreements between recyclers and automakers like Ford and GM secure inbound volumes.

Competitive Landscape

The Electric Vehicle Battery Recycling Market is moderately fragmented, with the top five players controlling significant global capacity. Mining majors like Glencore are buying stakes in Li-Cycle, and Norsk Hydro is acquiring Hydrovolt, highlighting an emerging consolidation wave. Simultaneously, technology disruptors such as Redwood Materials and Ascend Elements scale integrated hydro-to-cathode flows that deliver 99.99% lithium yields.

Competitive intensity is shaped by several factors: proprietary direct-recycling IP that cuts OPEX by 40%, AI-enabled robotics reducing labour by 60%, and first-mover feedstock contracts that lock in long-term supply. White-space niches remain: LFP-specific processes, Indian two-wheeler pack recycling, and value-added services like digital battery passports. Universities spin off solvent-free extraction startups, while software firms provide immutable traceability ledgers demanded under EU regulation.

Partnerships between cell manufacturers and recyclers are rising; for example, LG Energy Solution’s tie-up with Toyota channels cathode scrap into Kentucky recycling lines. Firms integrating upstream scrap aggregation with downstream chemical refining are best placed to weather commodity swings and regulatory tightening.

Electric Vehicle Battery Recycling Industry Leaders

-

Li-Cycle Corp.

-

Umicore SA

-

Redwood Materials

-

Ascend Elements

-

Guangdong Brunp Recycling Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Bosch Ventures invests in two battery-recycling startups, signalling rising corporate venture capital interest in the field.

- April 2024: Ascend Elements and Elemental Strategic Metals launch the AE Elemental joint venture in Poland to expand Eastern European processing capacity.

- February 2024: Ascend Elements secures an additional USD 162 million to scale sustainable lithium-ion battery-material production in the United States.

Global Electric Vehicle Battery Recycling Market Report Scope

| Lithium-ion (NMC, NCA, LFP, LMO, LCO) |

| Nickel-metal Hydride |

| Lead-acid |

| EV-production scrap |

| End-of-life EV batteries |

| Hydrometallurgical |

| Pyrometallurgical |

| Direct / Mechanical & Other Emerging |

| Two-Wheelers |

| Three-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses & Coaches |

| Lithium |

| Cobalt |

| Nickel |

| Manganese |

| Graphite & Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Norway | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (NMC, NCA, LFP, LMO, LCO) | |

| Nickel-metal Hydride | ||

| Lead-acid | ||

| By Source | EV-production scrap | |

| End-of-life EV batteries | ||

| By Recycling Process | Hydrometallurgical | |

| Pyrometallurgical | ||

| Direct / Mechanical & Other Emerging | ||

| By Vehicle Type | Two-Wheelers | |

| Three-Wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses & Coaches | ||

| By Recovered Material | Lithium | |

| Cobalt | ||

| Nickel | ||

| Manganese | ||

| Graphite & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Norway | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the EV battery recycling market?

The market size reached USD 3.88 billion in 2025 and is projected to reach USD 15.58 billion by 2030.

Which recycling process dominates the EV battery recycling market?

Hydrometallurgy leads with a 64.11% share, though direct/mechanical recycling is the fastest-growing segment, with a 32.82% CAGR.

Why are two-wheelers significant for battery recycling volumes?

Asian two-wheelers and three-wheelers retire batteries every 3-5 years, giving them 38.73% market share and a 35.47% CAGR for recycling volumes.

How does the EU Battery Regulation impact recyclers?

It mandates recycled content thresholds—65% cobalt and 6% lithium by 2031—guaranteeing demand and raising penalties for non-compliance.

Which region is growing fastest in the EV battery recycling market?

Asia-Pacific, expanding at a 35.12% CAGR, driven by China’s surging end-of-life volumes and large-scale processing capacity.

What factors restrain investment in recycling plants?

High CAPEX of USD 200-400 million per hydromet plant, lengthy 7-10-year paybacks, and safety and logistics challenges in battery collection.

Page last updated on: