Electric Vehicle Repair Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

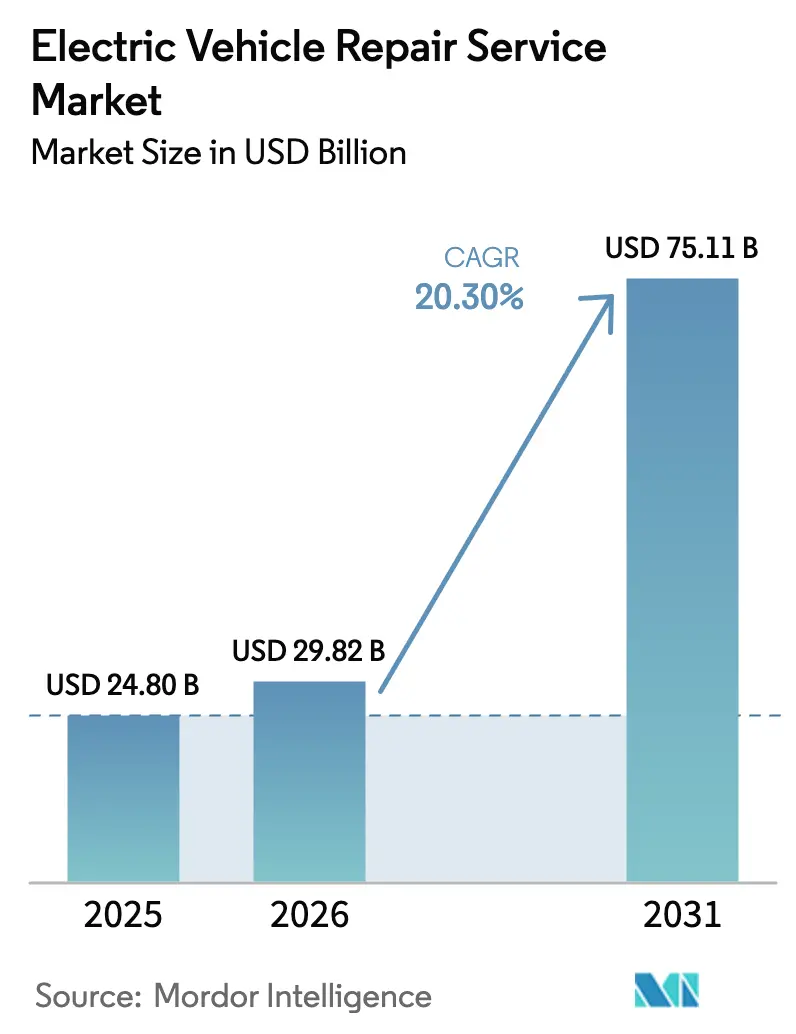

| Market Size (2026) | USD 29.82 Billion |

| Market Size (2031) | USD 75.11 Billion |

| Growth Rate (2026 - 2031) | 20.30% CAGR |

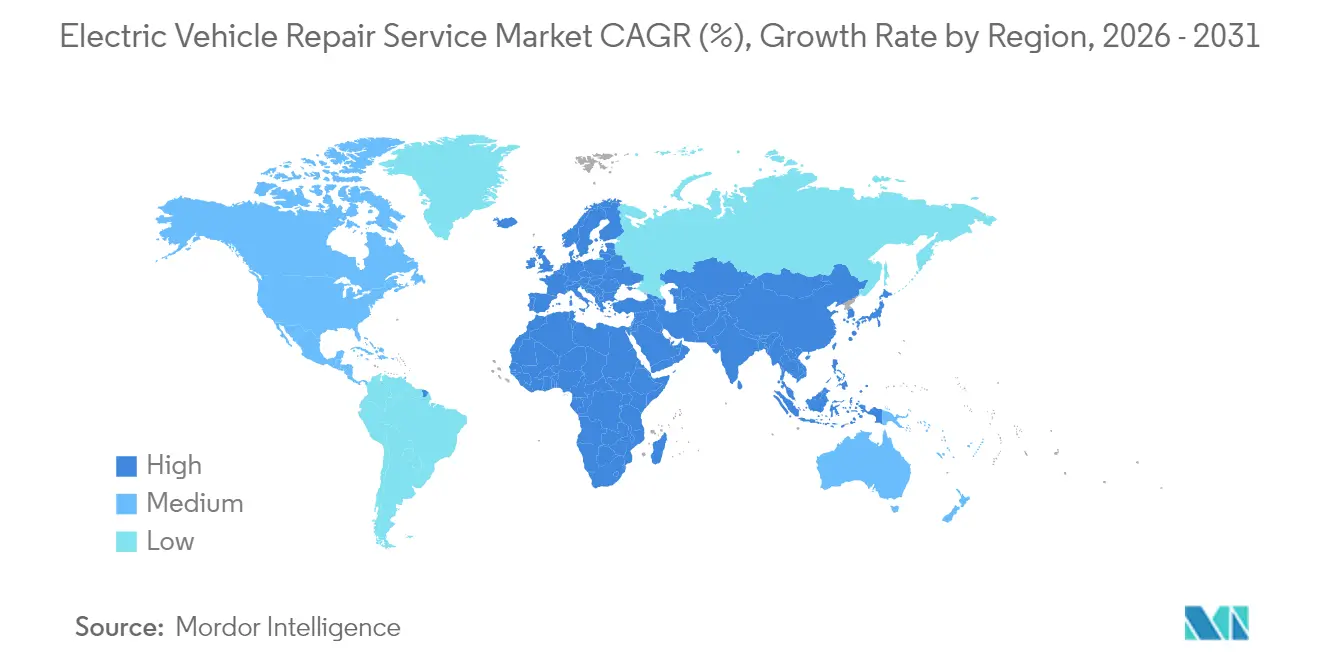

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

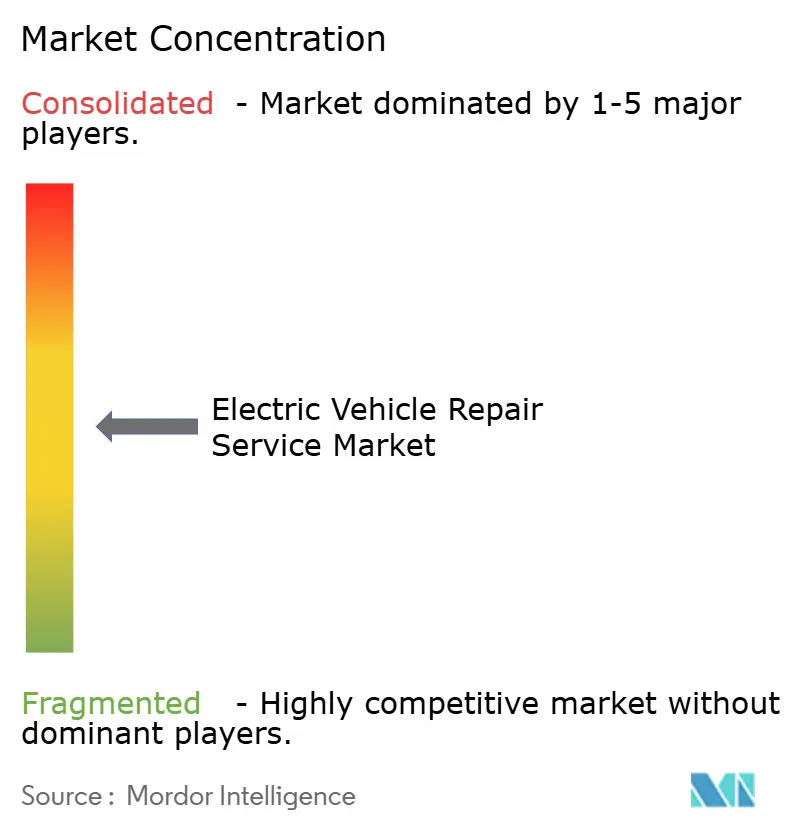

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Repair Service Market Analysis by Mordor Intelligence

The electric vehicle repair service market size is expected to grow from USD 24.80 billion in 2025 to USD 29.82 billion in 2026 and is forecast to reach USD 75.11 billion by 2031 at 20.3% CAGR over 2026-2031. Surging post-warranty vehicle counts, tightening zero-emission mandates, and wider public fast-charging infrastructure are displacing traditional mechanical repairs with high-voltage diagnostics, battery analytics, and software-driven preventative maintenance. OEM warranty expirations now overlap with the first large global EV cohort sold between 2020-2022, pulling a growing share of work away from franchised service bays toward certified independents. Meanwhile, right-to-repair debates and telematics data-sharing rules could reshape competitive dynamics once secure interfaces mature. Regulatory fleet-conversion timetables, particularly for medium and heavy commercial vehicles, further amplify demand for specialized uptime-critical services across regional corridors.

Key Report Takeaways

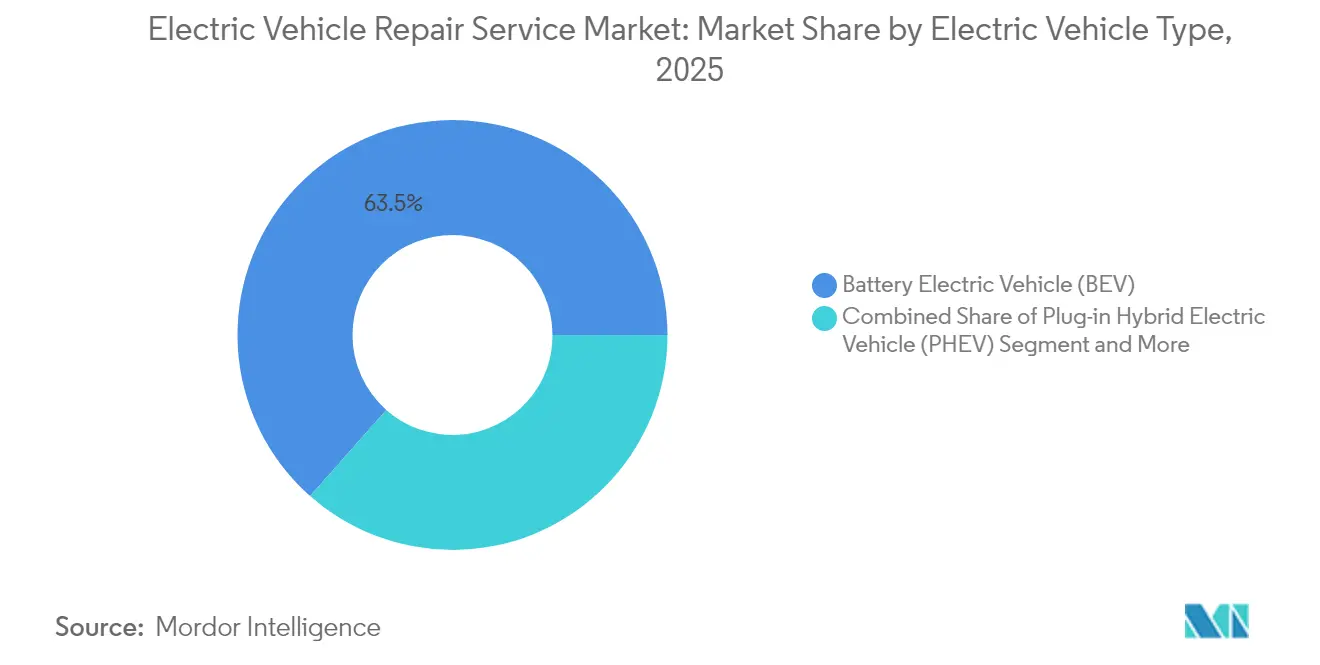

- By electric vehicle type, battery electric vehicles held 63.48% of the electric vehicle repair service market share in 2025, while fuel-cell electric vehicles are projected to register a 23.95% CAGR through 2031.

- By service type, preventive maintenance generated 32.10% of the electric vehicle repair service market share in 2025, whereas battery diagnostics and remanufacturing are tracking the fastest 22.12% CAGR outlook.

- By component type, high-voltage battery and BMS services commanded 29.02% of the electric vehicle repair service market share in 2025 and are advancing at a 21.10% CAGR through 2031.

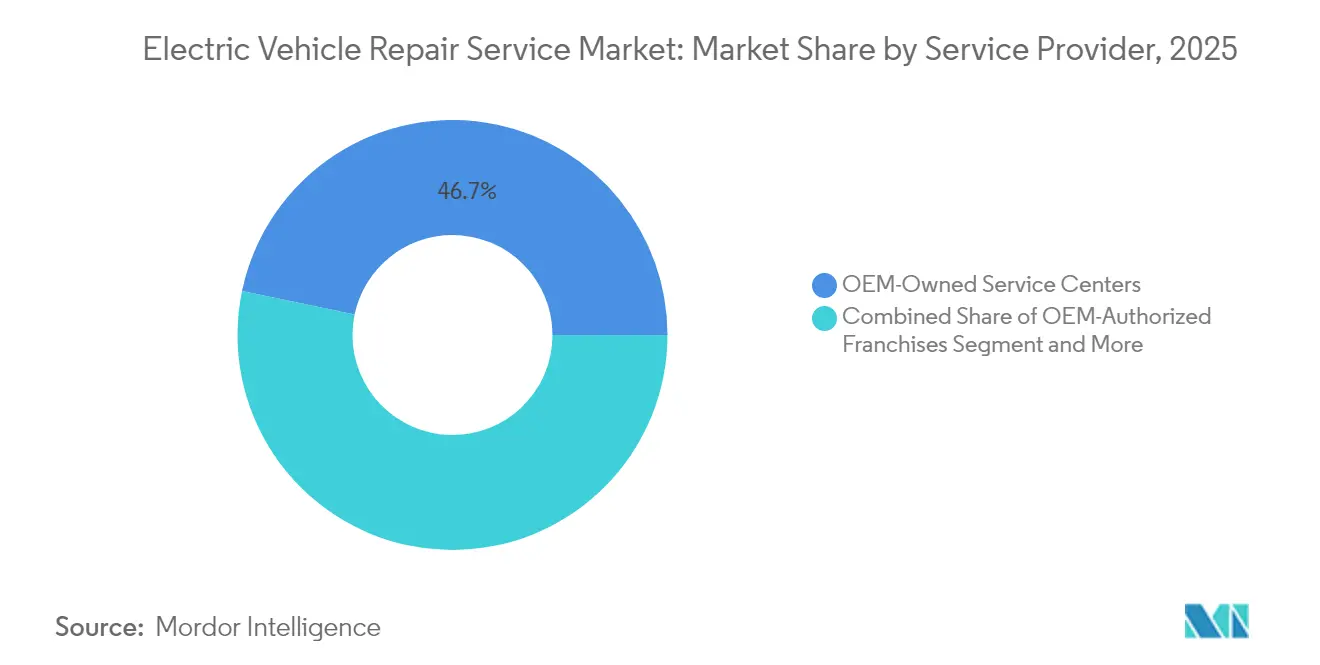

- By service provider, OEM-owned centers accounted for 46.72% of the electric vehicle repair service market share in 2025; mobile repair networks are anticipated to expand at a 21.98% CAGR to 2031.

- By vehicle type, passenger cars delivered 68.42% of the electric vehicle repair service market share in 2025, but medium and heavy commercial units are forecast to post a 22.55% CAGR to 2031.

- By geography, Asia-Pacific generated 44.80% of the electric vehicle repair service market share in 2025, whereas the Middle East and Africa will track the fastest 21.58% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Repair Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global EV Parc and Aging | +4.2% | Global (China, Europe, North America) | Medium term (2-4 years) |

| Government ZEV Mandates and Incentives | +3.8% | North America, Europe, select APAC | Short term (≤2 years) |

| Rapid DC-Fast Charging Network Build-Out | +2.9% | Global (led by China, Europe) | Medium term (2-4 years) |

| OEM Certification for Independents | +2.1% | North America, Europe | Medium term (2-4 years) |

| Right-To-Repair and Telematics Access | +1.8% | North America, Europe | Long term (≥4 years) |

| Emergence of Battery-Second-Life Ecosystems | +1.6% | Global (early gains in China, Europe) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global EV Parc and Post-Warranty Vehicle Aging

Vehicle cohorts sold between 2020-2022 have begun to exit warranty, exposing owners to full repair costs and creating a surge in independent shop volumes. China illustrates scale effects as heavy-duty electric trucks reached 22% penetration in the first half of 2025, far ahead of other regions, concentrating service activity along logistics corridors. Unscheduled downtime now costs commercial fleets USD 500-1,000 per day, pushing preventive maintenance contracts and battery refurbishment adoption. South Korea’s Poen grew significantly from 2020-2023 by remanufacturing battery packs at one-third the new-unit price. The maturing parc therefore underpins long-run revenue visibility for operators with energy-storage competencies.

Government ZEV Mandates and Purchase Incentives

Policies such as California’s Advanced Clean Trucks rule compel escalating zero-emission fleet percentages, guaranteeing a predictable volume of in-service vehicles that require certified maintenance capacity. Brazil’s EV sales surged 90% to 177,360 units in 2024, 71% plug-ins after infrastructure subsidies widened, demonstrating how incentives translate into aftermarket demand. Domestic-production credits also push OEMs to seed regional service footprints to secure compliance support. However, uncertainty over post-2025 federal incentives could inject procurement volatility, especially in commercial adoption, where operating-cost parity remains marginal.

Rapid Build-Out of Public DC-Fast Charging Networks

Global DC-fast points multiplied, with Brazil alone recording 2,430 units by February 2025, each costing about BRL 300,000 (USD 150,000) [1]“Brazil Fast-Charger Census,” Valor Econômico, valor.com.br. Higher utilization accelerates wear on charging ports, thermal loops, and contactors, lifting service frequency. Energy majors like Vibra and Raízen bundle maintenance contracts for their charger rollouts, opening novel revenue lines for mobile technicians stationed along transit corridors. Competing platform standards such as Tesla V4 Superchargers and BYD megawatt chargers will require multi-protocol diagnostic equipment and technician cross-training.

Mainstream OEM Certification Programs for Independent Shops

Programs from GM, Tesla, and others grant tool access and parts pricing to independents that meet safety and training criteria. Bosch earmarked EUR 2.5 billion (~USD 1.17 billion) through 2027 for AI-enabled diagnostics to support these certified channels [2] “Bosch invests heavily in AI as a growth driver,” Robert Bosch GmbH, bosch-presse.de. While the framework widens geographic coverage, cost barriers favor well-capitalized chains capable of acquiring insulated lifts, battery lifts, and high-voltage PPE. Hydrogen-equipped models like Honda’s CR-V e: FCEV layer additional certification hurdles around fuel-cell stack service and leak detection.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled EV Technician Shortage | -2.8% | Global (North America, Europe most severe) | Short term (≤2 years) |

| High Battery Replacement Costs | -2.3% | Global (higher in emerging markets) | Medium term (2-4 years) |

| OEM Software Limits Access | -1.9% | Global (independent shops affected) | Medium term (2-4 years) |

| Declining EV Parts Revenue | -1.4% | Global | Long ter |

| Source: Mordor Intelligence | |||

Acute Shortage of High-Voltage-Licensed Technicians

Certification pipelines currently produce too few specialists to meet fleet electrification timelines. High-voltage coursework can run 6-12 months, and demand is worst for commercial truck platforms that integrate complex BMS and telematics overlays. Premium wages inflate repair pricing and limit the expansion of regional service density. Firms investing early in technician up-skilling, like Bosch, gain durable labor advantages while smaller garages stall on capital and talent.

High Cost and Logistics Risk of Lithium-ion Battery Replacement

The high cost of passenger-vehicle and commercial packs exceeds the residual values of aging units. Hazmat shipping, insurance, and inventory financing compound cost exposures. Supply bottlenecks prolong vehicle downtime, and insurers lack granular failure-rate data, complicating actuarial pricing. Refurbishment specialists such as Poen mitigate by offering certified packs at one-third the new-unit cost, yet warranty confidence remains a buyer hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Electric Vehicle Type: BEVs Anchor Current Demand While FCEVs Accelerate

Battery Electric Vehicles represented 63.48% of the electric vehicle repair service market share in 2025, underscoring their entrenched dominance within the electric vehicle repair service market. The segment’s mechanical simplicity translates into recurring needs for battery diagnostics, inverter calibration, and thermal-loop flushing rather than drivetrain overhauls. As the electric vehicle repair service market expands, BEVs' high installed base guarantees steady workshop throughput. Though only a minimal share today, Fuel-Cell Electric Vehicles headline growth at 23.95% CAGR as refueling networks emerge around freight corridors. Hydrogen stack servicing demands additional cleanroom protocols and gas-leak detection, which few facilities possess, creating a premium niche.

Fleets still running Plug-in Hybrids and conventional Hybrids generate hybrid dual-powertrain work, obligating shops to maintain ICE tooling alongside high-voltage gear. Specialized garages use this cross-skill to cross-sell full BEV conversions to operators seeking maintenance simplification. With BEVs pushing into heavier classes and FCEVs scaling in long-haul trucking, providers that stratify training across energy architectures will capture multi-segment wallet share.

By Service Type: Preventive Maintenance Dominates Revenue Mix

Preventive schedules delivered 32.10% of the electric vehicle repair service market share in 2025 through software updates, coolant replacement, and high-voltage insulation checks. Over-the-air diagnostics now flag thermal-pack deviations weeks before failure, enabling just-in-time part ordering that lifts first-time fix rates. AI-assisted triage, pioneered by Tesla in 2025, mines sentiment data from service requests to prioritize cases and reduce communication lags. Battery diagnostics and remanufacturing, growing at 22.12% CAGR, anchor the future revenue arc as aging packs swell refurbishment pipelines.

Corrective mechanical repairs retreat in share but remain necessary after collisions or suspension stress from battery weight. Bodywork centers now install insulated isolation zones and EV-only bays to mitigate arc flash risk. Mobile and remote repair visits—covering firmware flashes, tire rotations, and 12-V battery swaps—accelerate as fleets prize uptime and urban charging queues provide predictable technician staging points.

By Component Type: Battery and BMS Lead Both Volume and Growth

High-voltage battery work captured 29.02% of the electric vehicle repair service market share in 2025 and is also growing fastest at 21.10% CAGR. This rare dual leadership underscores the centrality of energy storage expertise. Degradation analytics leveraging impedance spectroscopy and cell-level data loggers underpin early warning interventions. Inverters and traction motors add a steady workload, though their solid-state nature means fewer catastrophic failures than internal combustion equivalents. Heat-pump HVACs and liquid-cooled charging ports introduce new service lines around refrigerant loop balancing and dielectric-fluid exchanges.

Advanced driver-assistance sensor recalibration climbs alongside Level-2+ autonomy packages, demanding millimeter-level camera alignment and software handshakes post-repair. Meanwhile, chassis and suspension items wear faster on heavier battery vehicles, pushing alignment centers to upgrade to higher-capacity lifts and recalibrated torque tools.

By Service Provider: OEM Control Persists as Mobile Networks Surge

OEM-owned outlets held a 46.72% of the electric vehicle repair service market share in 2025 due to exclusive diagnostic rights during warranty. Franchise fleets extend reach but follow OEM protocols. As the electric vehicle repair service market advances, mobile repair networks log a 21.98% CAGR, bolstered by Ford Pro’s 700-unit mobile fleet that cuts visit times to around 70 minutes per van . Certified independents leverage Bosch’s AI diagnostics to close complexity gaps, though capital requirements deter many small shops.

Software gatekeeping remains the chief moat, yet right-to-repair momentum could erode this advantage later in the decade. Operators are able to bundle mobile convenience with certified tooling to arbitrage both OEM parts pricing and fleet downtime economics.

By Vehicle Type: Commercial Fleets Become Growth Engine

Passenger cars supplied 68.42% of the electric vehicle repair service market share in 2025, reflecting mass-market adoption and a broad service footprint. Medium and heavy commercial vehicles, however, project a 22.55% CAGR through 2031 as fleet mandates bite. China already shows significant penetration in electric heavy trucks, compressing learning curves and lifting battery-swap adoption.

Light commercial last-mile vans keep steady volume as e-commerce surges, demanding route-optimized charging and predictive fleet maintenance platforms. Battery-swap stations have almost reached 3,000 in NIO’s network by the end of 2024, promise rapid turnaround, but service providers must master pack lock-out and thermal-cache equalization routines before swaps return to circulation.

Geography Analysis

Asia-Pacific held 44.80% of the electric vehicle repair service market share in 2025, anchored by China’s battery manufacturing scale and aggressive fleet conversion quotas. Dense urban clusters yield high workshop utilization, while vertically integrated incumbents like CATL supply both packs and service toolkits, reinforcing regional dominance. NIO’s swap network trialing fifth-generation stations by Christmas 2025 further deepens localized service sophistication. Japan and South Korea contribute niche leadership in hydrogen systems and battery refurbishment. Poen’s notable CAGR battery remanufacture exemplifies capability depth. India’s market shows promise yet wrestles with technician shortages and uneven charging rollouts.

North America combines established dealership networks with legislative pressure for data access. California’s ZEV mandates and extensive Tesla Supercharger grids deliver the densest repair volumes, though technician scarcity inflates labor rates. Federal right-to-repair bills could unlock independent shop participation once secure APIs arrive. Canada follows closely with incentives mirrored in the United States structures.

Europe benefits from stringent CO₂ standards and robust corporate fleet commitments. Germany and the Nordic nations lead workshop upgrades, while the EU battery directive accelerates recycling capacity buildouts like SK tes’s Rotterdam plant. However, skilled-labor constraints echo North American challenges. Southern Europe and emerging Eastern European clusters adopt retrofit business models, converting light commercial ICE vans to BEV drivetrains to comply with urban low-emission zones.

Middle East & Africa shows the fastest 21.58% CAGR, catalyzed by GCC sovereign funds funneling capital into charging corridors and assembly plants. Harsh desert climates stress thermal management, raising service intervals on cooling plates and coolant pumps. Turkey’s customs-union link to Europe positions it as a regional parts and service hub, while South Africa leverages mining ties to anchor battery material flows. Brazil anchors South America, its significant EV-sales surge in 2024 validating infrastructure-driven adoption; public chargers rose to 2,430 DC units by February 2025, expanding aftermarket footprints.

Competitive Landscape

Competition remains fragmented but tilts toward consolidation around intellectual property and software platforms. OEM-controlled centers leverage gated diagnostics, warranty coverage, and over-the-air update streamlining to lock in early-life vehicles. Tesla’s 2025 AI service module triages customer tickets with sentiment filters, reducing escalation time and cementing brand retention. Bosch’s EUR 2.5 billion (~USD 1.17 billion) AI spend democratizes sophisticated scanning through certified independents, potentially redistributing volume away from OEM exclusivity.

Independent EV-specialist chains chase differentiation via convenience and cost transparency. Mobile fleets, free from brick-and-mortar overhead, undercut traditional rates and meet fleet downtime KPIs. Battery-focused refurbishers like Poen exploit high pack prices to offer economical alternatives, gaining traction among ride-hailing and light-commercial operators.

Strategic alliances proliferate: charger network operators contract maintenance bundles; insurers partner with certified centers to cap claim exposure; parts suppliers embed telematics in replacement components to monitor in-field performance. The market rewards depth over breadth—operators mastering high-voltage safety, cybersecurity compliance, and predictive analytics carve defensible niches even without national footprints.

Electric Vehicle Repair Service Industry Leaders

Tesla Inc.

Robert Bosch GmbH

LKQ Corporation

Hyundai Motor Co.

BYD Auto Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Contemporary Amperex Technology launched a cell-to-pack battery repair service via its Ning Service aftermarket arm, cutting EV owner costs and challenging traditional replace-only norms.

- August 2025: Admiral and The Vella Group opened a co-branded Manchester repair center equipped with dedicated EV bays, chargers, and high-voltage-trained technicians.

- June 2025: Maruti Suzuki announced a network upgrade plan covering 1,500 workshops for its debut e-Vitara SUV launch, aiming for 8,000 service touchpoints by April 2031.

- July 2024: Steer Automotive Group debuted Steer Electric, a 14,000-sq-ft EV repair hub in Eastleigh with full aluminum structural capability and battery oversight instrumentation.

Global Electric Vehicle Repair Service Market Report Scope

Electric vehicles, mechanical and electrical inspections, and repair are all offered in automotive services. The service sector includes routine and non-routine services like rustproofing and exterior painting. Routine services include tire repair, air conditioning, and oil changes.

The electric vehicle repair service market has been segmented by electric vehicle type, component, service provider, vehicle type, and geography. By electric vehicle type, the market is segmented into battery electric vehicles, plug-in electric vehicles, and fuel-cell electric vehicles. The target market is segmented by component type into mechanical, exterior, structural, and other components. The market is divided into franchise general repairs, OEM-authorized service centers, and other service providers. The market is divided into passenger cars and commercial vehicles based on vehicle type. The market is segmented by region into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

The market value will be provided in USD for all the mentioned segments.

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Preventive Maintenance (software updates, HV-system checks) |

| Corrective Mechanical Repair |

| Battery Diagnostics and Remanufacture |

| Body and Paint (EV-specific materials) |

| Mobile and Remote Repair Services |

| High-Voltage Battery and BMS |

| Electric Motor / Inverter |

| Thermal Management and HVAC |

| ADAS Sensors and Calibration |

| Chassis / Suspension |

| OEM-Owned Service Centers |

| OEM-Authorized Franchises |

| Independent EV-Specialist Garages |

| Mobile Repair Networks |

| Passenger Car |

| Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Service Type | Preventive Maintenance (software updates, HV-system checks) | |

| Corrective Mechanical Repair | ||

| Battery Diagnostics and Remanufacture | ||

| Body and Paint (EV-specific materials) | ||

| Mobile and Remote Repair Services | ||

| By Component Type | High-Voltage Battery and BMS | |

| Electric Motor / Inverter | ||

| Thermal Management and HVAC | ||

| ADAS Sensors and Calibration | ||

| Chassis / Suspension | ||

| By Service Provider | OEM-Owned Service Centers | |

| OEM-Authorized Franchises | ||

| Independent EV-Specialist Garages | ||

| Mobile Repair Networks | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicle | ||

| Medium and Heavy Commercial Vehicle | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global value of the electric vehicle repair service market in 2026?

The electric vehicle repair service market size stands at USD 29.82 billion in 2026.

How fast is demand for EV repair services expected to grow through 2031?

Aggregate revenue is forecast to rise at a 20.3% CAGR between 2026 and 2031.

Which service type leads current spending?

Preventive maintenance delivers 32.10% of 2025 revenue, reflecting OEM focus on software updates and battery health checks.

Which component category generates the most workshop revenue?

High-voltage battery and BMS services account for 29.02% of 2025 turnover and remain the fastest-growing line item.

Which region shows the highest growth outlook?

The Middle East & Africa region projects a 21.58% CAGR, driven by large infrastructure investments and electrification mandates.

Page last updated on: