Car Detailing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

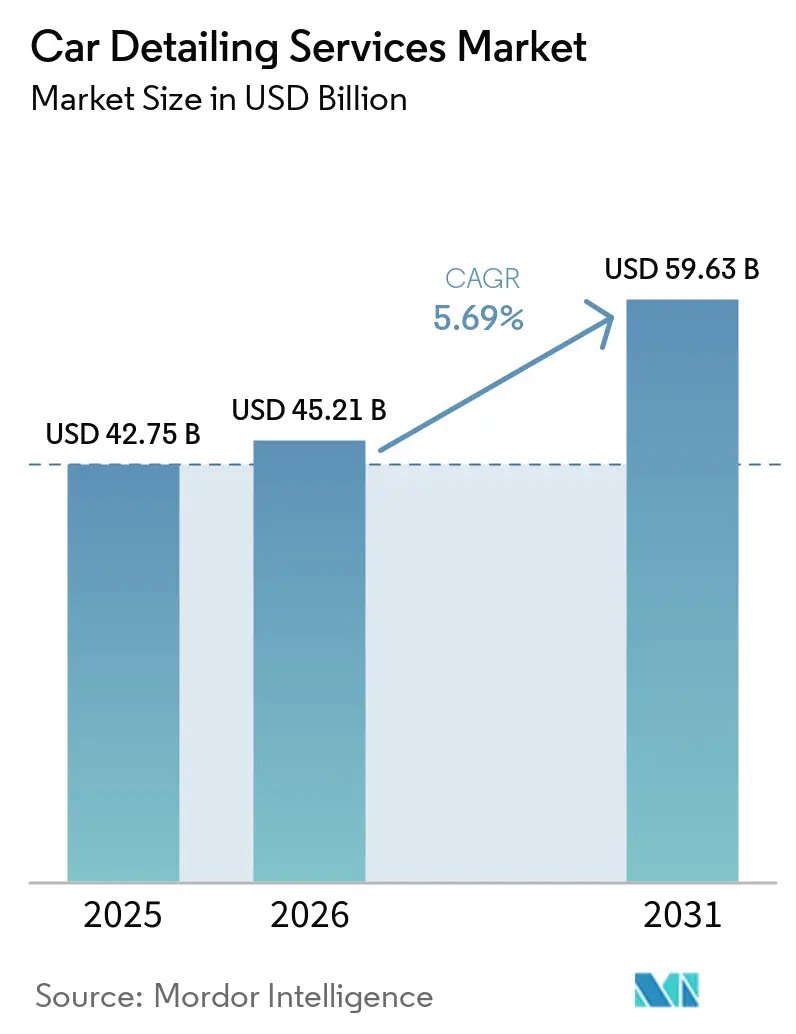

| Market Size (2026) | USD 45.21 Billion |

| Market Size (2031) | USD 59.63 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Detailing Services Market Analysis by Mordor Intelligence

The car detailing services market size is projected to be USD 42.75 billion in 2025, USD 45.21 billion in 2026, and reach USD 59.63 billion by 2031, growing at a CAGR of 5.69% from 2026 to 2031. Subscription-based membership programs now dominate revenue streams, insulating operators from weather volatility and lifting cash-flow predictability. Consolidators backed by private equity are racing to build geographic density, yet mounting regulatory scrutiny of PFAS and VOCs is elevating compliance costs. Labor shortages are encouraging chains to deploy AI-enabled inspection and robotic applicators, while water scarcity rules in California, the Middle East, and Australia accelerate the adoption of waterless chemistries. These cross-currents are widening the performance gap between capital-rich super-chains and smaller independents that rely on manual processes.

Key Report Takeaways

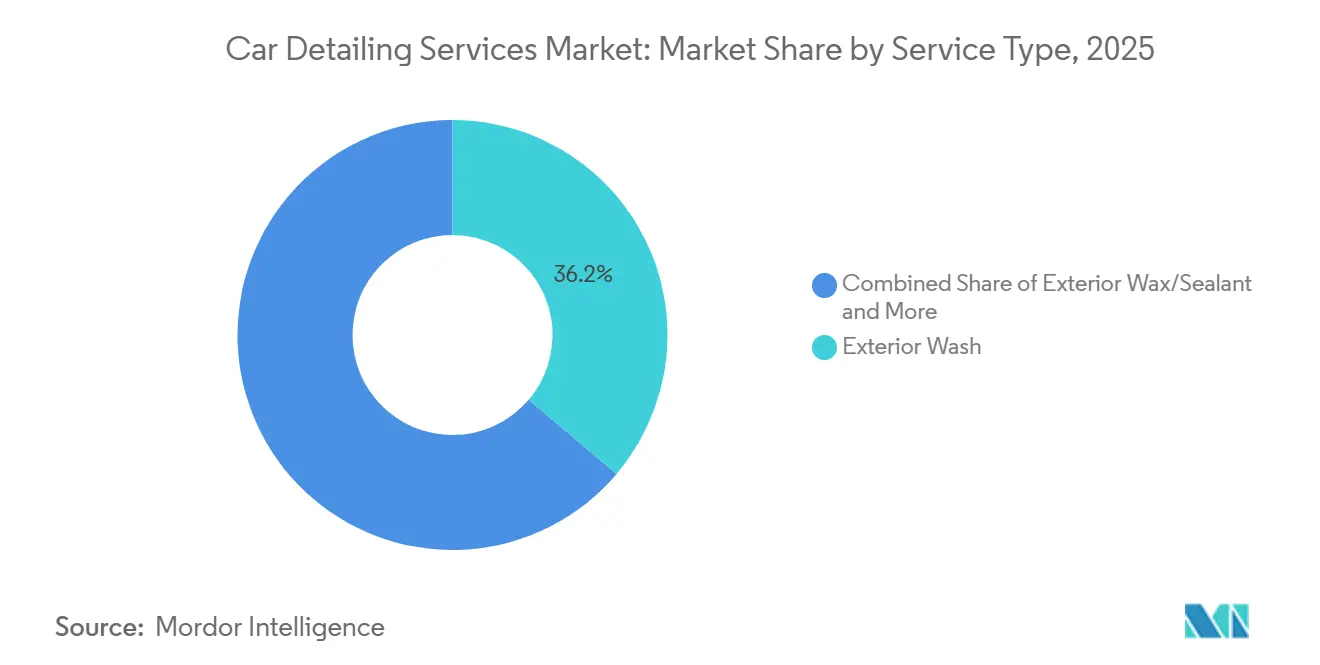

- By service type, exterior wash services led with 36.15% of the car detailing services market share in 2025, while paint correction and ceramic coating are advancing at a 12.39% CAGR to 2031.

- By provider model, conventional service stations held 73.01% of the car detailing services market size in 2025, whereas mobile and on-demand formats are projected to grow at 16.45% between 2026 and 2031.

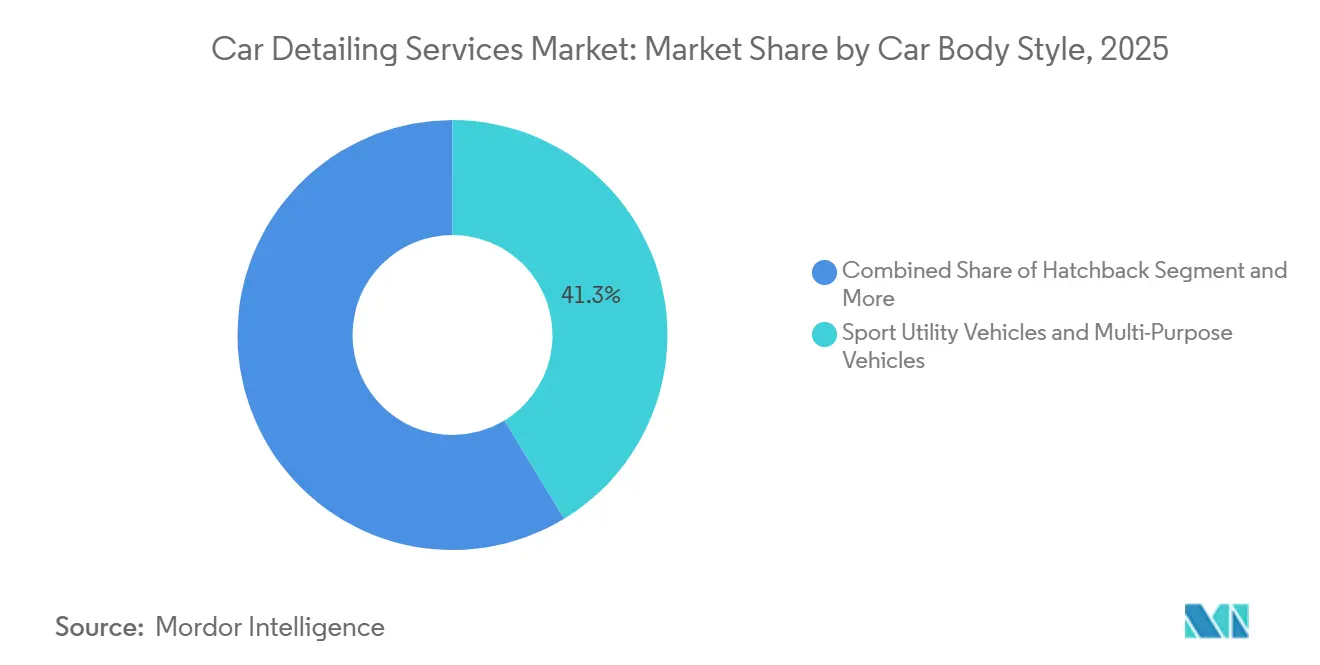

- By car body style, sport utility and multi-purpose vehicles accounted for 41.26% share of the car detailing services market size in 2025 and are moving at an 11.26% CAGR through 2031.

- By booking channel, walk-in and offline modes retained 86.33% share in 2025, while online and app-based platforms are forecast to post a 21.17% CAGR to 2031.

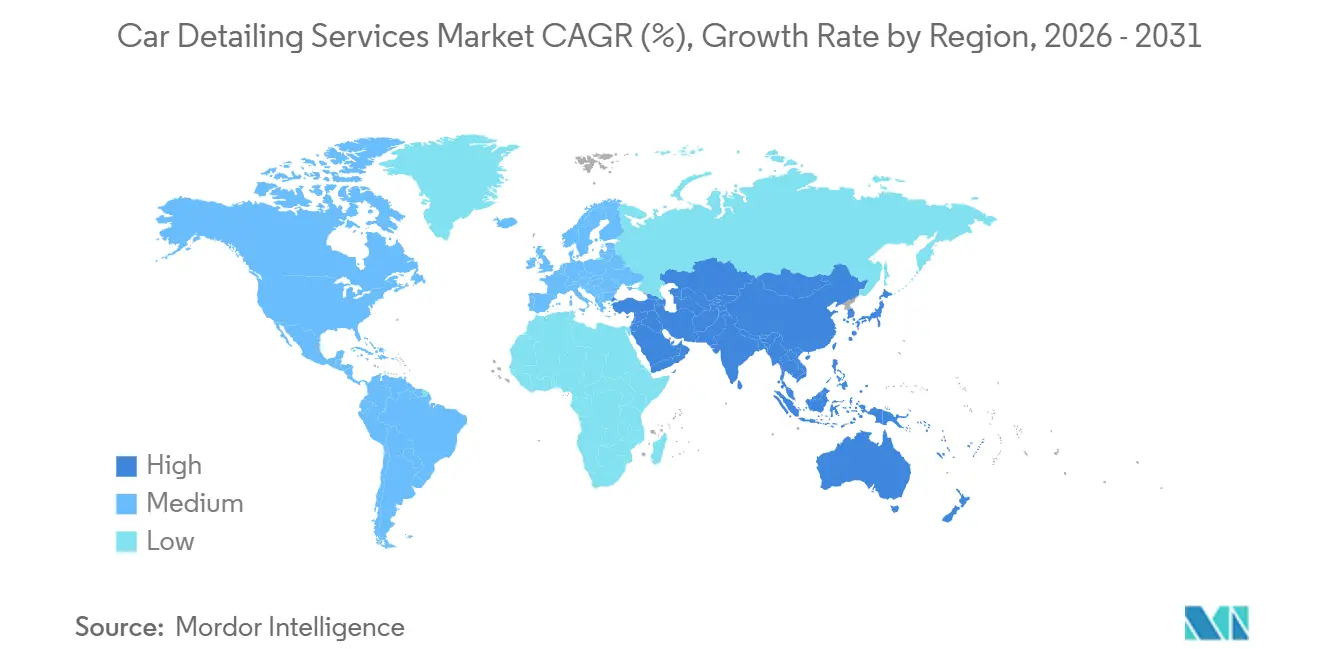

- By geography, North America commanded 39.12% of 2025 revenue, yet Asia-Pacific is expected to deliver the fastest regional CAGR of 8.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Car Detailing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury and EV Penetration | +1.5% | Global, concentrated in North America, Europe, China, Middle East | Medium term (2-4 years) |

| Subscription-Based Wash Memberships | +1.2% | Global, highest in North America, early uptake in urban Asia-Pacific | Medium term (2-4 years) |

| AI-Powered Visual-Inspection | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Paint-Protection-As-A-Service | +0.8% | North America, Europe, China | Long term (≥ 4 years) |

| Private-Equity Roll-Ups | +0.7% | North America, spillover to Europe and South America | Long term (≥ 4 years) |

| Water Scarcity Drives Waterless Innovation | +0.6% | California, Middle East, Australia, parts of India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Luxury and EV Penetration Demanding Specialty Detailing

As battery-electric vehicle prices rise, owners are turning to multi-year coatings to safeguard their resale values. In recent years, Glossgenic reported EV ticket prices soaring above standard packages. Astonishing Detail, based in the Pacific Northwest, highlighted that Tesla and Rivian owners are increasingly investing in two-step correction-plus-coating services. Meanwhile, NVN Motorworks, boasting what it claims to be the world’s largest luxury detailing facility, operates in both Dubai and Riyadh, emphasizing the segment's global footprint. This dynamic landscape compels operators to strike a balance between high-volume express tunnels and boutique studios that command premium margins.

Soaring Subscription-Based Express-Wash Memberships

Unlimited-wash memberships now anchor revenue for leading chains, shielding operators from seasonal swings. Mister Car Wash grew its Unlimited Wash Club to nearly 2.3 million members in 2025, with membership contributing 79% of wash revenue [1]“2025 Annual Report,” Mister Car Wash Investor Relations, Mistercarwash.com. In India, ROXO Hub offers similar service bundles, while ALPHASHINE in the Gulf combines interior and tire services. This strategy boosts their average revenue per user. The consistent cash inflows not only shorten working-capital cycles but also bolster leverage for expanding networks. Established brand chains can afford to underprice smaller independents, leading to a swift shift in market share. As a result, private-equity sponsors are keen on platforms that can leverage memberships across their widespread locations.

AI-Powered Visual-Inspection Upselling Platforms

Computer-vision systems now capture images of vehicles, identify defects, and seamlessly integrate real-time price quotes into booking applications. FocalX's pilot programs have demonstrated significant improvements in conversions. Similarly, CamCom and Onyx AutoPad offer tools that integrate with customer-relationship platforms, streamlining follow-up marketing efforts. This technology not only lessens the dependence on skilled sales personnel but also accelerates the quote-to-close process. This is particularly beneficial given that technician vacancy rates in U.S. metropolitan areas have been a persistent challenge in recent years. However, capital expenditure poses a challenge for smaller operators, further solidifying the competitive edge for larger chains.

OEM “Paint-Protection-As-A-Service” Partnerships

Automakers are embedding ceramic coatings and paint-protection film into vehicle financing, converting one-time accessory sales into annuity streams. Ceramic Pro and Lucid Motors jointly offer factory-installed coatings bundled into lease payments [2]“Lucid Partnership Launch,” Ceramic Pro Press Center, Ceramicpro.com. XPEL has similar pre-delivery tie-ins with Rivian. Shifting the point of sale upstream erodes aftermarket volume available to independent shops while aligning with OEM strategies to monetize installed bases through services instead of unit sales. The arrangement secures captive demand and standardizes quality, yet it raises the competitive bar for traditional detailers that depend on post-purchase up-selling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation and Technician Shortage | -0.9% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| PFAS / VOC Chemical Bans | -0.5% | North America, Europe, select U.S. states | Medium term (2-4 years) |

| Do-It-Yourself Kits | -0.4% | Global, higher impact in developed markets | Medium term (2-4 years) |

| Nanocoatings on AV Fleets | -0.3% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Cost Inflation and Technician Shortage

In 2025, median hourly wages for detailers in U.S. metros experienced significant growth. Concurrently, many shops grappled with hiring challenges. The industry faces high turnover rates, inflating training costs and limiting expansion into secondary cities. While automation offers a potential relief, the upfront costs of robotic polishers and AI inspection lines remain a hurdle for many independent operators. In contrast, chains boasting robust balance sheets leverage their position, providing career pathways and benefits, thus amplifying the existing capability gap.

PFAS / VOC Chemical Bans

The U.S. EPA and the European Chemicals Agency have initiated phase-outs of several fluoropolymer compounds used in ceramic coatings [3]“PFAS Strategic Roadmap,” U.S. EPA, Epa.gov. Washington State banned intentional PFAS in car care products under WAC 173-337. Reformulations inflate input costs and require operator training, squeezing margins for shops that lack the scale to negotiate alternative chemistries. Compliance timelines are tight, giving larger suppliers with in-house R&D a structural advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Ceramic Coatings Outpace Volume Washes

Exterior wash services generated 36.15% of revenue in 2025, confirming their role as the volume backbone of the car detailing services market. Paint correction and ceramic coating are forecast to grow at 12.39% a year to 2031 as EV owners invest in multi-year surface protection. Ticket prices for this specialty cluster soar significantly above those of express washes, boosting gross margins for studios adept at multi-layer applications. As regulatory limits tighten on VOCs, suppliers are pivoting to low-solvent formulations. This shift not only nudges prices upward but also strengthens the value proposition centered on environmental compliance. Operators who can't invest in new chemistry lines face the risk of losing premium clients to studios that offer certified low-VOC products.

By 2025, the market for ceramic-coating packages in car detailing services had already gained significant traction, with further growth projected by 2031. Partnerships like Ceramic Pro with Lucid underscore the growing legitimacy of coatings as near-standard features. While express tunnels dominate by processing a high volume of vehicles daily, subscription discounts are squeezing per-car revenue. Consequently, high-margin specialty suites are sprouting within larger operations, enabling operators to harness both scale and premium spending.

By Provider Model: Mobile Formats Capture Time-Pressed Consumers

Conventional service stations retained 73.01% share in 2025 on the strength of embedded tunnel infrastructure. However, mobile and on-demand operators are projected to compound at 16.45% through 2031. Clean Mobile Detailing in California charges significant premiums over fixed-site prices yet still enjoys repeat bookings from urban professionals who value convenience. Fleet managers view on-site service as a way to avoid routing vehicles off-shift, supporting enterprise packages that guarantee recurring volume.

Subscription clubs bridge both models. Mister Car Wash reported that membership sales contributed 79% of wash turnover in 2025. The car detailing services market share of mobile providers is expected to climb by 2031 as app-based platforms extend geographic reach without real estate drag. Conventional stations continue to dominate rural areas where land is cheap, and tunnel throughput outweighs travel cost, but the urban pendulum has swung toward mobile.

By Car Body Style: SUVs Drive Ticket Inflation

Sport utility and multi-purpose vehicles accounted for 41.26% of service revenue in 2025 and will expand at an 11.26% CAGR to 2031. Operators charge significantly more for full-service SUV packages, capitalizing on the vehicles' greater surface area and interior volume. This trend is further amplified with electric SUVs, as owners increasingly opt for long-duration coatings to safeguard resale values. Consequently, this segment boasts a disproportionately high contribution margin across both express and boutique service formats.

While sedans and hatchbacks continue to hold sway in densely populated Asian metros—where parking constraints favor smaller vehicles—their pricing power remains limited. Projections indicate that the car detailing services market, particularly for the SUV segment, will experience notable growth by 2031. This underscores the rationale behind chains adjusting tunnel widths and lift sizes to accommodate taller vehicles. While hatchbacks and compact sedans will continue to drive volume, the strategic spotlight has undeniably shifted towards utility vehicles.

By Booking Channel: Digital Platforms Accelerate Upselling

Offline and walk-in bookings captured 86.33% of transactions in 2025, a figure expected to decline as smartphone penetration climbs. Online and app-based channels are set to grow at 21.17% annually, the swiftest across all segment lenses. FocalX has seamlessly integrated inspection imagery into the booking flow, significantly enhancing average ticket value for operators like The Detailing Gang in Delhi. Additionally, dynamic pricing has been employed to further enhance yields by adjusting rates in response to demand spikes.

By 2031, digital channels are expected to play a prominent role in the car detailing services market. Operators leveraging proprietary apps are not only capturing transaction data but also using it to inform retention campaigns and cross-selling strategies, thereby strengthening their membership ecosystems. While walk-in traffic will continue to cater to impulse washes, the real monetization potential now lies within the digital funnel.

Geography Analysis

North America generated 39.12% of global revenue in 2025, underpinned by mature subscription penetration and dense express-tunnel networks. In February 2026, Mister Car Wash crossed USD 1 billion in revenue across 548 sites, and Quick Quack exceeded 300 locations following KKR funding. PFAS and VOC legislation in California and Washington is forcing chemistry shifts that reward operators with R&D depth. Canada contributes incremental growth, helped by high vehicle ownership, while Mexico lags owing to lower disposable income, but offers white space for value-priced chains.

Asia-Pacific is the fastest riser, poised for an 8.15% CAGR through 2031. In India, urban detailing studios like The Car Laundry and The Detailing Gang are catering to middle-income professionals, offering a wide range of packages. With China's substantial EV penetration in 2025, there's a growing demand for specialty coatings, particularly those addressing battery-specific thermal constraints. Meanwhile, water scarcity issues in Australia and Malaysia are driving a swift adoption of waterless chemicals, a trend that's also gaining momentum in the Gulf.

Europe, South America, the Middle East, and Africa contribute to the remaining turnover. Brazil's detailing sector has experienced remarkable growth over the past few years, fueled by an expanding vehicle parc. The Middle East stands out with the highest per-visit spending; for instance, NVN Motorworks in Dubai offers premium packages. In Europe, the push for PFAS substitution, driven by REACH regulations, presents challenges. However, smaller shops are navigating this by marketing low-impact chemistries to environmentally conscious owners. While these regions offer opportunities for portfolio diversification, they also necessitate tailored service menus to align with local climatic and regulatory landscapes.

Competitive Landscape

In the fragmented car detailing services market, the top ten operators capture a significant share of North American revenue, but their global share remains much lower. Divergent strategic theses are evident as Leonard Green & Partners takes Mister Car Wash private, while Driven Brands divests to Whistle Express. Sponsor-backed platforms emphasize subscription density, leveraging brand advertising and data systems across their networks. In contrast, mid-market buyers are on the lookout for bolt-ons in secondary metros, where valuations are still reasonable.

Technology plays a pivotal role. In recent years, WashTec AG has generated substantial revenue and EBIT by selling tunnel equipment and robotic polishers, enhancing throughput. FocalX and CamCom introduce AI inspection layers, integrating upsell logic into mobile applications. Collaborations with Ceramic Pro, XPEL, and SealPro allow OEMs to push coatings upstream. This move curtails aftermarket volume but also lends legitimacy to the category. While independents offer tailored craftsmanship for exotic cars, they face margin pressures from wage demands and chemical compliance, especially without premium pricing.

Market watchers anticipate more asset sales driven by bankruptcies, similar to Zips Car Wash, as rising interest rates challenge over-leveraged platforms. Chains boasting net-cash balance sheets and sophisticated tech infrastructures stand poised to acquire these distressed entities, furthering the trend of consolidation.

Car Detailing Services Industry Leaders

Mister Car Wash Holdings, Inc.

Delta Sonic Carwash Systems Inc.

3M Company (3M Car Care)

Splash Car Wash

Autobell Car Wash, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Splash Car Wash acquired Five Star Car Wash & Detail Center in East Northport, New York, lifting its state footprint to 47 sites.

- February 2026: Quick Quack Car Wash purchased Lightning Express Car Wash in Lawndale, California, with reopening slated for spring 2026, using upgraded vacuums and membership plans.

- January 2026: Quick Quack Car Wash opened its sixth San Antonio site after refurbishing Pirate’s Cove Car Wash at 18054 Bulverde Road.

- November 2025: Kia India launched its first Shine Zone car-detailing studio in Jaipur, India, offering ceramic coatings, interior treatments, and underbody protection.

Global Car Detailing Services Market Report Scope

The scope includes segmentation by service type (exterior wash, exterior wax/sealant, interior vacuuming, interior surface cleaning, glass and windshield cleaning, tire and wheel dressing, paint correction/ceramic coating, and others), provider model (conventional service station, mobile/on-demand, and subscription club/membership), car body style (hatchback, sedan, and sport utility vehicles and multi-purpose vehicles), and booking channel (online/app-based and walk-in/offline). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Exterior Wash |

| Exterior Wax / Sealant |

| Interior Vacuuming |

| Interior Surface Cleaning |

| Glass and Windshield Cleaning |

| Tire and Wheel Dressing |

| Paint Correction / Ceramic Coating |

| Others (Odor Removal, Engine Bay, Headlight Restoration) |

| Conventional Service Station |

| Mobile / On-Demand |

| Subscription Club / Membership |

| Hatchback |

| Sedan |

| Sport Utility Vehicles and Multi-Purpose Vehicles |

| Online / App-Based |

| Walk-in / Offline |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Exterior Wash | |

| Exterior Wax / Sealant | ||

| Interior Vacuuming | ||

| Interior Surface Cleaning | ||

| Glass and Windshield Cleaning | ||

| Tire and Wheel Dressing | ||

| Paint Correction / Ceramic Coating | ||

| Others (Odor Removal, Engine Bay, Headlight Restoration) | ||

| By Provider Model | Conventional Service Station | |

| Mobile / On-Demand | ||

| Subscription Club / Membership | ||

| By Car Body Style | Hatchback | |

| Sedan | ||

| Sport Utility Vehicles and Multi-Purpose Vehicles | ||

| By Booking Channel | Online / App-Based | |

| Walk-in / Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the car detailing services market by 2031?

The car detailing services market is forecast to reach USD 59.63 billion by 2031.

Which region is expected to grow the fastest in professional detailing?

Asia-Pacific is projected to record an 8.15% CAGR between 2026 and 2031, the highest among all regions.

Why are ceramic coatings gaining popularity among EV owners?

Higher EV acquisition costs drive owners to invest in multi-year ceramic coatings that protect paint and preserve resale value.

How quickly are mobile detailing services expanding?

Mobile and on-demand formats are projected to grow at 16.45% a year from 2026 to 2031, outpacing fixed-site growth across most regions.

Page last updated on: