Aircraft Line Maintenance Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

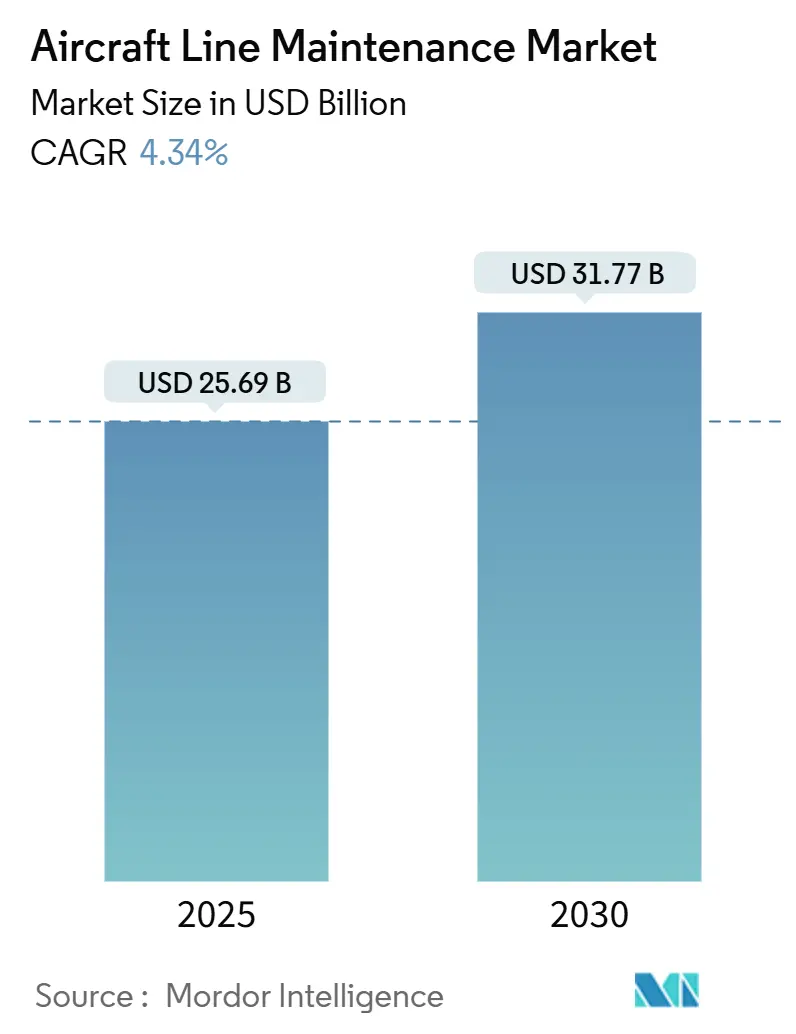

| Market Size (2025) | USD 25.69 Billion |

| Market Size (2030) | USD 31.77 Billion |

| Growth Rate (2025 - 2030) | 4.34% CAGR |

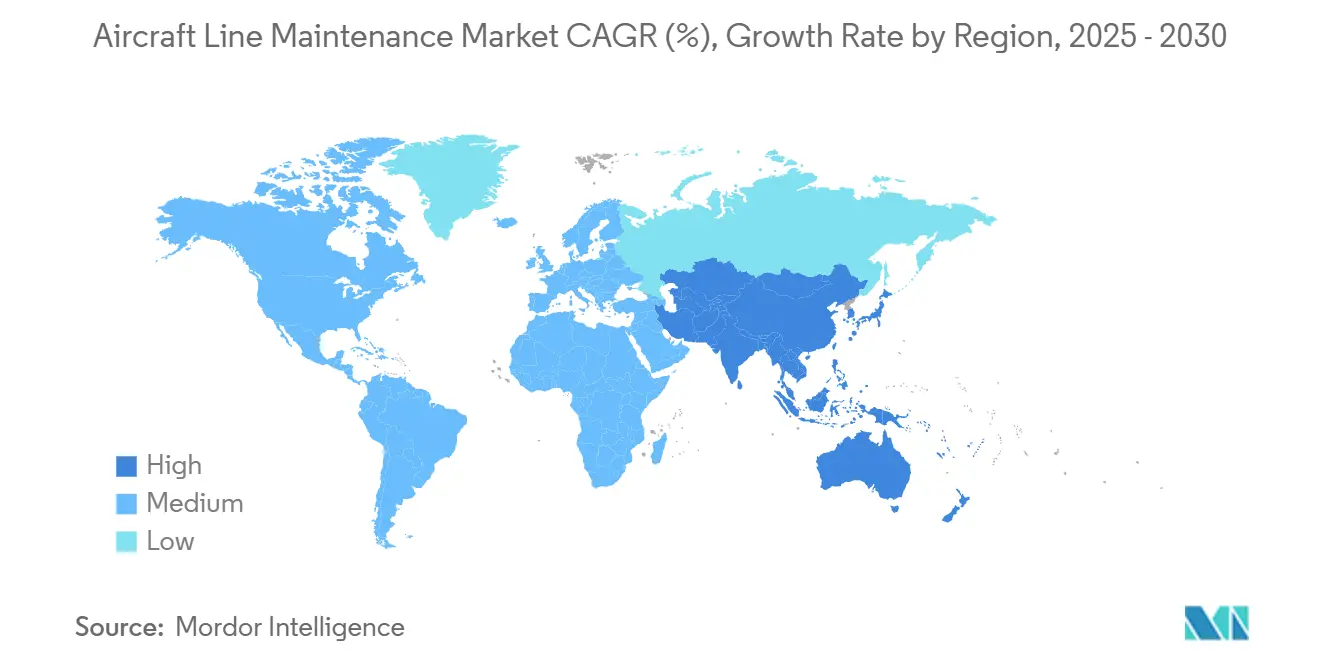

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Line Maintenance Market Analysis by Mordor Intelligence

The aircraft line maintenance market size reached USD 25.69 billion in 2025 and is projected to climb to USD 31.77 billion by 2030, reflecting a 4.34% CAGR. Fleet expansion in emerging economies, increased utilization of single-aisle jets, and rising airline outsourcing of transit checks are driving the momentum in the aircraft line maintenance market. Tighter turn-time expectations and persistent supply-chain stress heighten the strategic value of AOG response capabilities. Capital spending from power-plant OEMs, led by GE Aerospace’s USD 1 billion five-year MRO upgrade program, illustrates how incumbents are racing to close capacity gaps. Digital workcards, AI-driven fault prediction, and mobile service units at secondary airports enhance on-wing productivity while mitigating the risk of ramp congestion. Labor headwinds persist as retirements accelerate; Boeing predicts the global sector will need 716,000 new technicians by 2043.

Key Report Takeaways

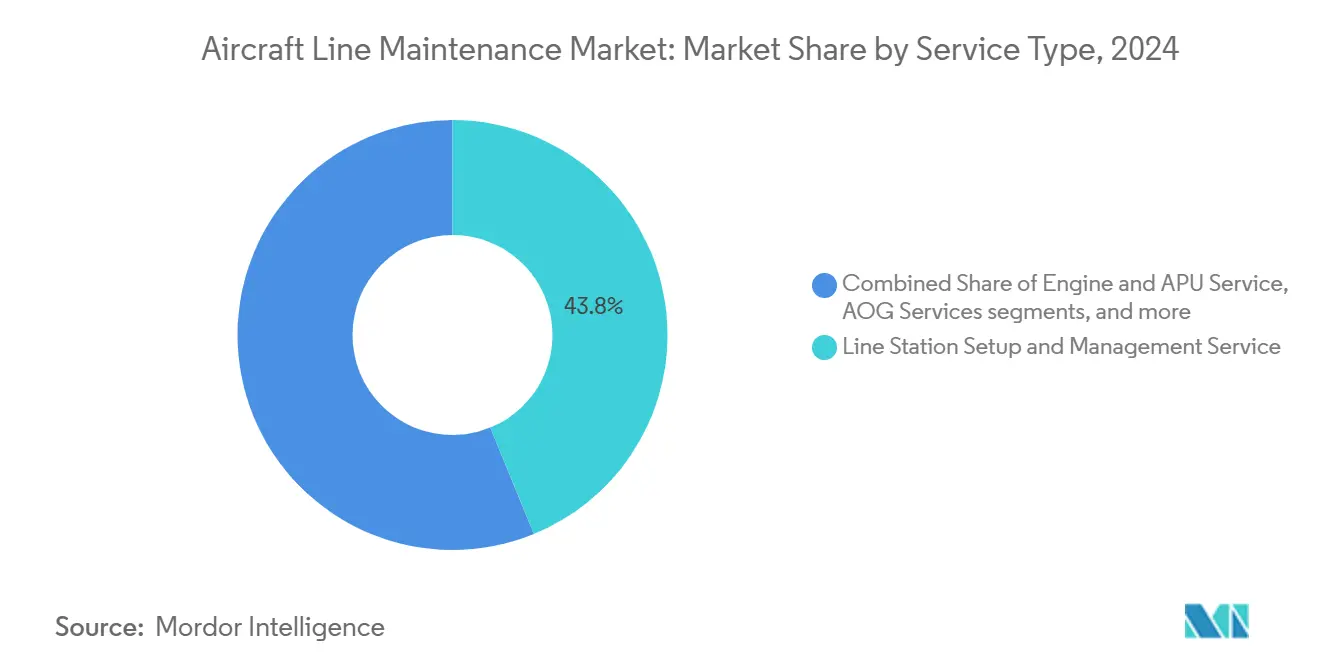

- By service type, line-station setup and management led with 43.82% revenue share of the aircraft line maintenance market in 2024, whereas AOG services are poised to advance at a 5.68% CAGR through 2030.

- By aircraft type, narrowbody jets dominated the aircraft line maintenance market share with 47.42% in 2024; freighter maintenance is projected to expand at a 6.29% CAGR through 2030.

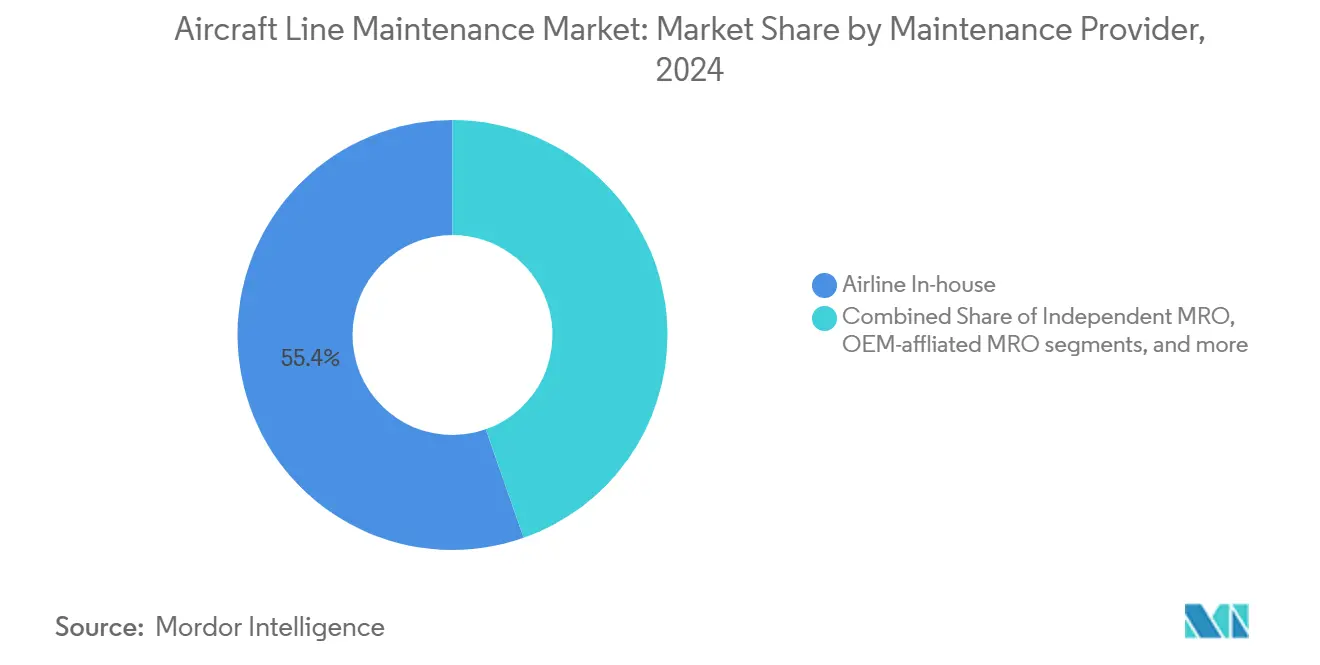

- By maintenance provider, airline in-house operations captured 55.38% of the aircraft line maintenance market in 2024, while independent MROs registered the fastest outlook, with a 7.73% CAGR to 2030.

- By schedule type, routine checks accounted for 63.47% of the aircraft line maintenance market size in 2024; transit checks are projected to expand at a 5.21% CAGR to 2030.

- By geography, North America held a 37.65% share in 2024; however, the Asia-Pacific region is expected to grow at a 6.04% CAGR through 2030.

Global Aircraft Line Maintenance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating fleet expansion in emerging markets | +1.20% | Asia-Pacific, Africa, Latin America | Medium term (2-4 years) |

| Rise in narrowbody utilization rates | +0.80% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Airline outsourcing of line maintenance to specialist MROs | +0.60% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Deployment of digital line-maintenance platforms | +0.40% | North America, Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| On-wing predictive analytics using real-time sensor data | +0.30% | Global, led by network carriers in developed markets | Long term (≥ 4 years) |

| Adoption of mobile maintenance stations at secondary airports | +0.20% | Regional airports worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Fleet Expansion in Emerging Markets

Chinese, Indian, and African operators are ordering record aircraft volumes, with China’s fleet forecast to more than double by 2043 and Africa adding 830 single-aisle jets in the same horizon. Each new aircraft requires continuous transit checks, spare part provisioning, and certified manpower, which strain existing domestic capacity. Shortfalls invite global MROs to form joint ventures for know-how transfer and workforce development. Airlines also utilize mobile service units until permanent hangars become operational. These structural shifts inject steady demand into the aircraft line maintenance market.

Rise in Narrowbody Utilization Rates

Single-aisle jets are expected to account for 76% of all deliveries through 2043, and carriers are flying longer daily to offset delivery lags.[1]Boeing Communications, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” Boeing, boeing.mediaroom.com Intensified cycles compress ground slots, creating more frequent but shorter maintenance interventions. MRO providers report parts backorders that push operators to schedule repairs years in advance. High-utilization profiles thus accelerate uptake of predictive diagnostics, ensuring defects get flagged before departure and reducing gate-hold penalties.

Airline Outsourcing of Line Maintenance to Specialist MROs

Cost discipline and access to skills prompt airlines to hand over nightly checks and AOG coverage to third-party experts. Independent shops are growing revenue at 7.73% CAGR, far outpacing internal airline maintenance budgets.[2]Oliver Wyman Insights, “Global Fleet and MRO Market Forecast 2025-2035,” Oliver Wyman, oliverwyman.com Strategic pacts, such as Air France-KLM’s MoU with Saudia, extend geographic reach and ramp manpower utilization. Outsourcing enables carriers to redeploy scarce mechanics to base-maintenance lines while specialists manage overnight transit tasks.

Deployment of Digital Line-Maintenance Platforms

Paperless task cards and AI-guided workflow tools are gaining traction, as 64% of surveyed MROs report tangible ROI from digital programs. AAR’s Trax deployment for Delta TechOps integrates work package planning, inventory visibility, and e-signatures on a single mobile dashboard. Digital platforms reduce error rates, expedite return-to-service decisions, and enable analytics that inform next-generation predictive models.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of licensed A&P technicians | -1.10% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Escalating regulatory compliance costs (Part-145) | -0.70% | Global, regional variations | Medium term (2-4 years) |

| Ramp-congestion limiting maintenance windows | -0.50% | North America, Europe, major Asia-Pacific hubs | Short term (≤ 2 years) |

| Volatile lead-times for critical LRUs | -0.40% | Global, supply chains centered in US and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Licensed A&P Technicians

Retirements outpace graduations, with 30% of mechanics set to exit within the next decade, and US training pipelines covering only half of the required seats. Oliver Wyman predicts a 27% shortfall by 2027, equal to 48,000 heads. Wage inflation averages 7.3% annually, eroding cost advantages created by digital productivity. Airlines launch tuition-payment programs and military-to-civilian bridges, yet new entrants need years to gain line-release authority, keeping capacity tight in the near term.

Escalating Regulatory Compliance Costs (Part-145)

EASA and FAA mandate rigorous quality manuals, calibrated tooling, and recurrent training, pushing initial certification costs above USD 500,000 for smaller entrants. Dual approvals compound documentation workloads, adding recurring audit expenses. While standardized oversight improves safety, it raises fixed costs and narrows margins for emerging independent MROs attempting to scale the aircraft line maintenance industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Line-Station Management Sustains Dominance While AOG Services Accelerate

Line-station management accounted for 43.82% of the aircraft line maintenance market size in 2024, underscoring carriers’ reliance on robust overnight infrastructure at hub and focus airports. Airlines integrate component swaps, minor structural repairs, and logbook rectifications into a single, coordinated work scope that must be completed before the first wave of departures. Digital job cards and inventory pre-pulls shorten elapsed time, preserving OTP commitments. Growth continues as new city pairs open in Asia and Africa, requiring fresh line stations supported by local partners.

While representing a smaller share, AOG services are expected to post a 5.68% CAGR through 2030 as fleets age and route maps expand. Boeing Distribution and Honeywell offer 24/7 crisis desks, and Textron’s mobile units promise four-hour dispatch to remote fields.[3]Textron Aviation Support, “AOG Support,” Textron Aviation, txtav.com Airlines willingly pay premium fees, knowing that every unscheduled ground hour can result in USD 10,000 in passenger and slot penalties. Consequently, the aircraft line maintenance market witnesses heightened investment in strategically located spare-parts depots and technician hotshot teams.

By Aircraft Type: Narrowbody Checks Dominate Yet Freighter Work Rises Fast

Narrowbody jets accounted for 47.42% of the aircraft line maintenance market share in 2024, as carriers increased single-aisle utilization to record levels. The transit-check frequency increases because each flight counts as one cycle that triggers OEM limits on lubrication and critical safety-item inspections. Intensive duty patterns have driven demand for service-bulletin compliance kits, which shops keep on consignment to speed release.

Freighter aircraft maintenance, although currently smaller, is forecasted to grow at a 6.29% CAGR as express and e-commerce volumes expand globally. Operators often extend the airframes' lifespan well beyond their design life, necessitating more frequent corrosion prevention and fatigue-critical checks. Specialized providers, such as HAECO and Evergreen Aviation, have established long-term agreements that ensure slot availability for converted widebody freighters. These dynamics reinforce a bifurcated aircraft line maintenance market, in which growth stems from high-cycle single-aisle operations and life-extension projects for cargo jets.

By Maintenance Provider: Airline In-House Units Retain Lead as Independents Gain Ground

Airline technical divisions held 55.38% of the aircraft line maintenance market in 2024 because legacy carriers value direct control over dispatch reliability. Wide networks allow them to rotate mechanics among bases, meeting Part-145 recurrent training requirements. Yet, cost containment and technology gaps drive the increased outsourcing of specialist tasks, especially composites and engine borescope inspections to independent MROs.

Independents are scaling fastest at 7.73% CAGR, aided by joint ventures that deliver local certificates and hangar access. AAR’s Asia-Pacific alliance with Air France Industries exemplifies geographic arbitrage where Western know-how pairs with lower-cost labor. OEM-affiliated MROs also stake claims via long-term engine contracts that bundle spare-parts discounts with on-site line support. Certification barriers favor scale, keeping entry hurdles high and sustaining pricing power across the aircraft line maintenance market.

By Schedule Type: Routine Checks Prevail but Transit-Check Demand Quickens

Routine overnight checks delivered 63.47% of revenue in 2024 as airlines adhere to OEM inspection ladders that safeguard airworthiness. Predictive health-monitoring systems now pre-load expected fault codes into work orders, enabling mechanics to stage tools and parts before arrival, thereby reducing turnaround time.

Transit checks are projected to post a 5.21% CAGR thanks to denser schedules and rapid gate returns. Low-cost carriers (LCCs) that average 25-minute turns seek ultra-efficient task sequences and wireless e-sign-offs. Providers deploy tablet-based apps, allowing certifying staff to fulfill regulatory sign-offs from the tarmac and eliminate paper delays. The dynamic underscores how evolving operating models continue to reshape service-mix allocations inside the aircraft line maintenance market.

Geography Analysis

North America generated 37.65% of 2024 revenue, reflecting the world's largest in-service fleet and mature MRO infrastructure. GE Aerospace's USD 1 billion facility upgrades and Lufthansa Technik's Calgary engine repair shop collectively create more than 700 jobs while easing CFM LEAP maintenance bottlenecks.[4]GE Aerospace Newsroom, “GE Aerospace Investing USD 1 Billion to Expand and Upgrade MRO Facilities Worldwide,” GE Aerospace, geaerospace.com Despite scale advantages, the region confronts a 19% mechanic deficit by 2028, pushing airlines to sponsor A&P school expansions and sign-on bonuses.

The Asia-Pacific is the fastest-growing aircraft line maintenance market, with a 6.04% CAGR, driven by a fleet that is expected to double by 2043.[5]Airbus Press Team, “Asia-Pacific’s Aircraft Services Market to Double Over Next 20 Years,” Airbus, aircraft.airbus.com India's MRO spend is forecasted to reach USD 4 billion by 2031, accelerating demand for line stations at newly privatized airports. Partnerships, such as GMR Aero Technic's deals with Lufthansa Technik, provide international certifications and tooling standards, positioning the region to absorb surging transit-check workloads.

Europe retains a robust share through legacy flag carriers and strong regulatory frameworks. Nevertheless, many EU hubs fight ramp congestion that compresses overnight work time. Middle Eastern fleets are growing at a rate of 5.1% annually, driving investments in Doha and Dubai's line-maintenance facilities. Latin America benefits from USD 13 billion in airport upgrades, enabling LCCs to achieve high cycle utilization, which fuels steady demand for mobile line-support units. Collectively, geographic shifts reinforce long-term diversification of services across the aircraft line maintenance market.

Competitive Landscape

The aircraft line maintenance industry is moderately concentrated, with airline tech ops, OEM-linked networks, and independents holding a meaningful share. Lufthansa Technik’s billion-euro expansion across Portugal, Hamburg, and Canada elevates its slot capacity and positions it as a top-tier integrator of AI tools and paperless workflows. AAR deepens its market reach through long-term materials agreements with FTAI Aviation and a modernized Trax platform that enhances Delta’s 450-engine yearly overhaul line.

OEMs are increasingly bundling spare parts pools with line support agreements, blurring the boundaries of the aftermarket. Pratt & Whitney’s EngineWise partners with Cebu Pacific and Delta to expand its global GTF MRO network, enhancing on-wing support depth. Safran invests over EUR 1 billion (USD 1.16 billion) to widen LEAP service coverage across four continents, cementing its role as an indispensable service partner. Rising digital adoption becomes a key differentiator; carriers favor suppliers that can prove faster turn times and data-verified reliability gains. Meanwhile, mobile specialists exploit white space at secondary airports, chipping away at incremental share from legacy giants.

Aircraft Line Maintenance Industry Leaders

AAR CORP.

Aircraft Maintenance & Engineering Corporation (Ameco)

Lufthansa Technik AG

Delta Air Lines, Inc.

Hong Kong Aircraft Engineering Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Magnetic Line, a division of Magnetic Group, signed a line maintenance agreement with Oman Air, extending their existing business relationship. The contract assigns Magnetic Line to provide comprehensive technical handling services for Oman Air's B787-9 Dreamliner fleet, powered by GEnx engines, at Amsterdam Airport Schiphol (AMS).

- June 2025: AAR subsidiary Trax selected to modernize Delta TechOps’ maintenance and engineering systems, enabling data-driven workflow optimization.

- January 2025: HAECO extended its line maintenance contract with EVA Air through 2026. The agreement includes non-technical services and cabin cleaning at Hong Kong International Airport.

- July 2024: HAECO signed a line maintenance contract with Chinese carrier Loong Air. This agreement demonstrates Loong Air's trust in HAECO's line maintenance capabilities for its global fleet operations.

Global Aircraft Line Maintenance Market Report Scope

| Component Replacement and Rigging Service |

| Engine and APU Service |

| Line Station Setup and Management Service |

| Defect Rectification Service |

| Aircraft on Ground (AOG) Service |

| Narrowbody |

| Widebody |

| Regional Jets |

| Turboprops |

| Freighter Aircraft |

| Business Jets |

| Airline In-house |

| Independent MRO |

| OEM-affiliated MRO |

| Airport-based Line Stations |

| Routine Checks |

| Transit Checks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Service Type | Component Replacement and Rigging Service | ||

| Engine and APU Service | |||

| Line Station Setup and Management Service | |||

| Defect Rectification Service | |||

| Aircraft on Ground (AOG) Service | |||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| Turboprops | |||

| Freighter Aircraft | |||

| Business Jets | |||

| By Maintenance Provider | Airline In-house | ||

| Independent MRO | |||

| OEM-affiliated MRO | |||

| Airport-based Line Stations | |||

| By Schedule Type | Routine Checks | ||

| Transit Checks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the aircraft line maintenance market in 2025?

The aircraft line maintenance market size reached USD 25.69 billion in 2025 and is forecasted to hit USD 31.77 billion by 2030, reflecting a 4.34% CAGR.

Which segment is the fastest-growing within line maintenance services?

Aircraft on Ground (AOG) response services lead growth, registering a 5.68% CAGR through 2030 as airlines prioritize rapid return-to-service.

Why is Asia-Pacific attracting so much new line-maintenance capacity?

Fleets in China and India are expanding quickly, prompting projections that Asia-Pacific maintenance revenues will more than double to USD 109 billion by 2043, outpacing every other region.

What is the main challenge hampering MRO growth?

A global shortage of licensed A&P technicians, forecasted at a 27% deficit by 2027, pressures labor availability and inflates wage costs.

How are digital platforms changing daily line checks?

AI-driven work-cards and predictive analytics reduce documentation errors, preload spare-parts needs, and shorten aircraft ground time, boosting operational reliability.

Why are AOG services emerging as a strategic priority for airlines?

Each unscheduled ground hour can cost carriers as much as USD 10,000 in passenger disruption and slot penalties, so airlines are prioritizing 24/7 AOG coverage and mobile response units to protect on-time performance and revenue.

Page last updated on: