Vascular Plugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

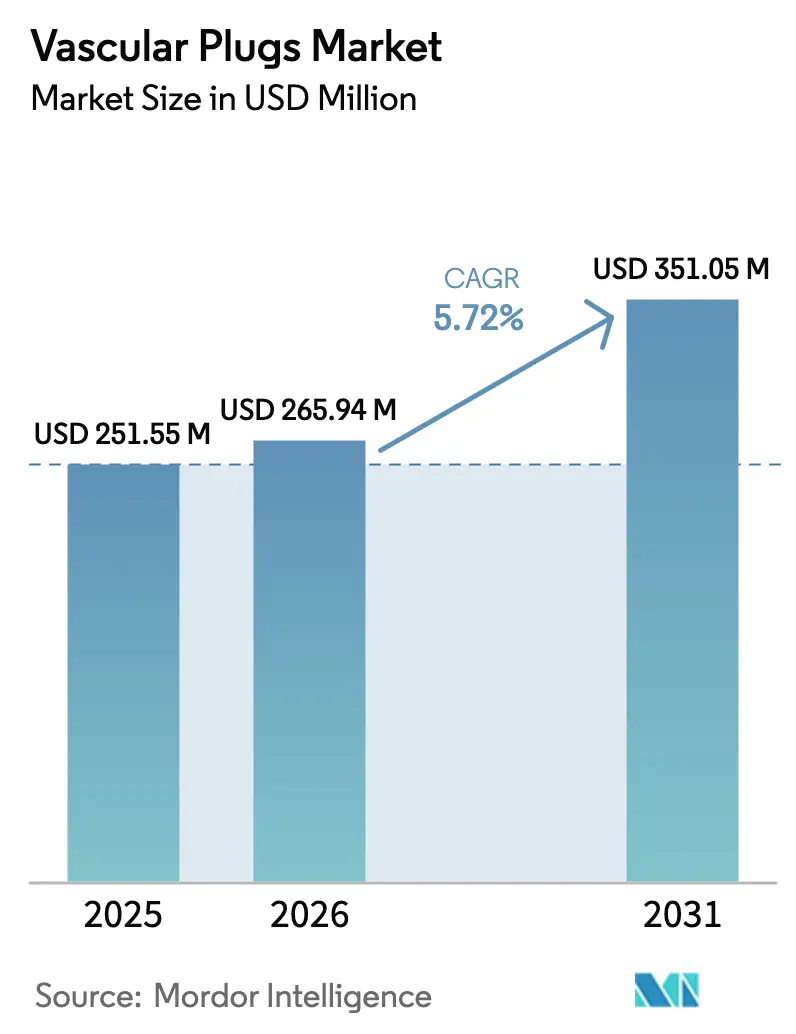

| Market Size (2026) | USD 265.94 Million |

| Market Size (2031) | USD 351.05 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Plugs Market Analysis by Mordor Intelligence

The vascular plugs market size was valued at USD 251.55 million in 2025 and estimated to grow from USD 265.94 million in 2026 to reach USD 351.05 million by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Expansion is propelled by the growing clinical burden of peripheral vascular diseases, rapid preference for minimally-invasive embolization, and continuous product design upgrades such as micro-plugs and PTFE-covered variants. Same-day discharge protocols in interventional radiology units, broadened off-label neurovascular uses, and faster humanitarian-device exemptions in emerging economies further raise procedure volumes. Larger device manufacturers continue to invest in nitinol processing technologies to shorten deployment times and reduce fluoroscopy exposure for both clinicians and patients. These advances, together with material innovations that extend device compatibility with 3 Fr micro-catheters, sustain demand even in cost-sensitive outpatient settings, reinforcing the positive outlook for the vascular plugs market.

Key Report Takeaways

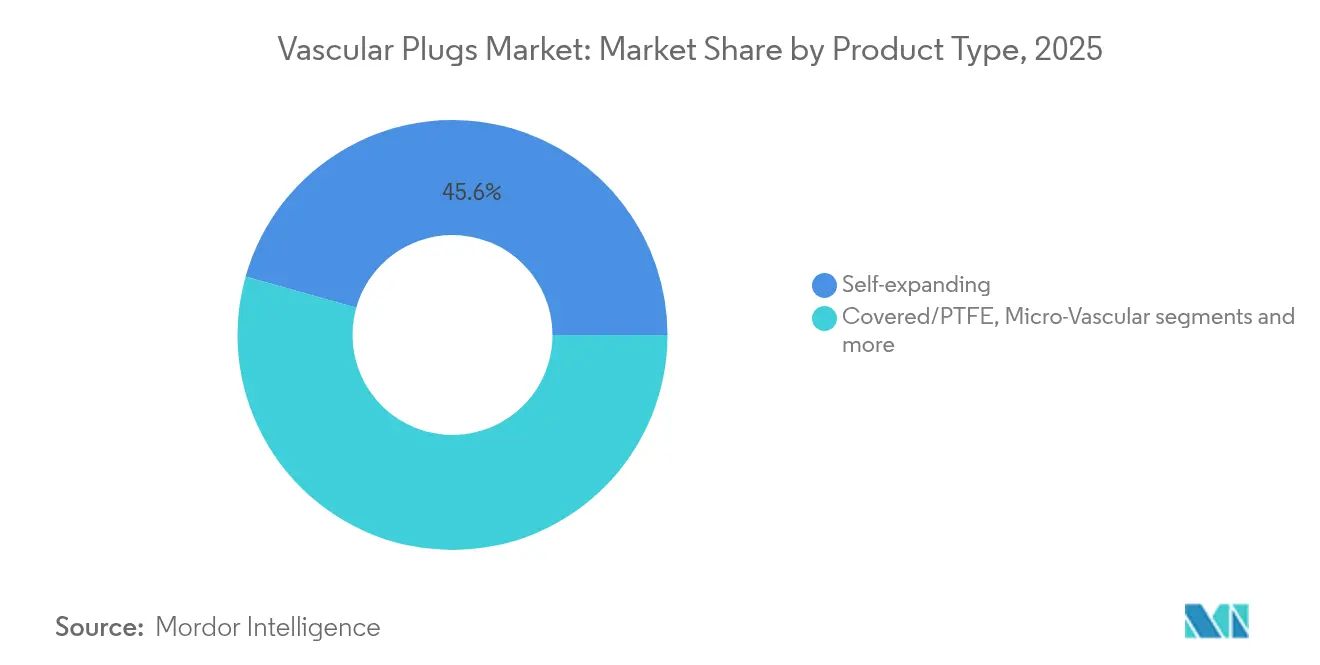

- By product type, self-expanding nitinol plugs held 45.62% of the vascular plugs market share in 2025, while shaped-memory polymer plugs are forecast to grow at a 6.21% CAGR through 2031.

- By application, peripheral vascular disease accounted for 37.68% of the vascular plugs market size in 2025; neurovascular disorders are projected to advance at a 6.78% CAGR to 2031.

- By delivery catheter, ≥ 6 Fr standard catheters led with a 55.05% revenue share in 2025, whereas ≤ 3 Fr micro-catheters are set to expand at a 6.55% CAGR over 2026-2031.

- By material, nitinol mesh devices captured 69.02% share of the vascular plugs market size in 2025; hybrid nitinol-polymer designs are likely to register a 6.86% CAGR.

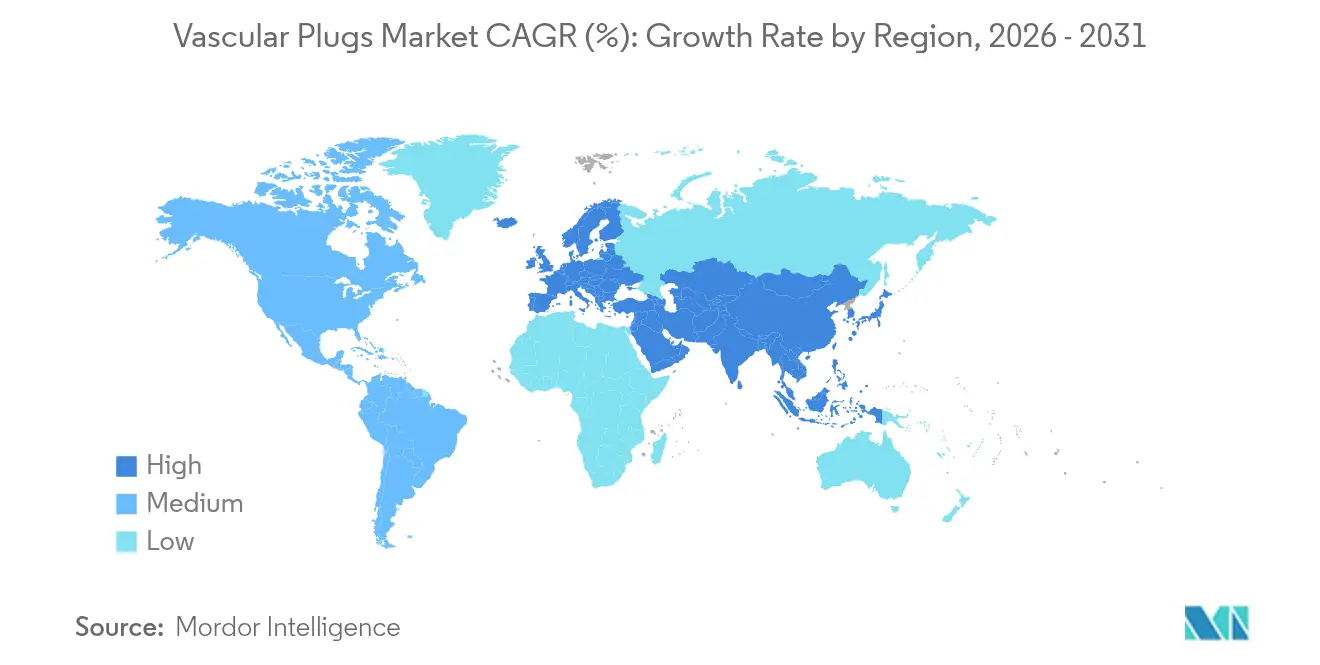

- By geography, North America dominated the vascular plugs market with 39.92% revenue share in 2025, while Asia-Pacific is anticipated to post the fastest 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vascular Plugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of peripheral vascular diseases | +1.2% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Adoption of minimally invasive embolization | +1.5% | Global; led by North America, expanding in Asia-Pacific | Medium term (2-4 years) |

| Continuous design advances | +0.8% | North America & EU innovation hubs; global adoption | Medium term (2-4 years) |

| Expanding off-label neurovascular use | +0.6% | North America & Europe | Long term (≥ 4 years) |

| Same-day discharge protocols | +0.4% | North America & Western Europe | Short term (≤ 2 years) |

| Humanitarian-device exemptions | +0.3% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of peripheral vascular diseases (PVD)

Rising obesity, diabetes, and aging populations collectively elevate PVD incidence, boosting embolization demand in limb-saving procedures. Hospitals now standardize vascular plug closure to maintain hemostasis during complex angioplasties, which cuts procedural steps and streamlines room turnover. Public health datasets show more than 200 PVD cases per 100,000 adults in high-income economies, a statistic that directly increases embolic device consumption. Favorable reimbursement that bundles plug costs into episode-of-care payments bolsters adoption and keeps the vascular plugs market on a healthy expansion path [1]Source: Centers for Disease Control and Prevention, “Peripheral Arterial Disease: Data and Statistics,” cdc.gov .

Surging adoption of minimally-invasive embolization over surgery

Endovascular occlusion with plugs avoids general anesthesia, shortens recovery, and lowers wound-care complications. Providers record up to a 20% decline in total treatment costs when embolization replaces open ligation, aligning with payer mandates for value-based care. As hospital administrators quantify reduced bed-day usage, they prioritize stocking plug inventories, a decision that lifts procedure counts and strengthens the vascular plugs market.

Continuous design advances (micro-plugs, PTFE covers)

Third-generation micro-plugs glide through tiny 0.021-inch catheters, reaching distal vasculature that coils cannot. PTFE coverings arrest flow instantly, which can eliminate multiple-coil use and shrink per-case consumables by 40% in high-volume centers. Radiopaque marker improvements slash fluoroscopy exposure 48%, easing operator concerns over cumulative radiation

Growing off-label neurovascular applications (stroke, AVFs)

Interventional neuroradiologists increasingly rely on plugs to protect distal territories during mechanical thrombectomy and to seal high-flow arteriovenous fistulas. Early studies report technical success rates above 95%, encouraging broader adoption. Compassionate-use approvals allow immediate use in life-threatening bleeds, expanding clinical familiarity and indirectly boosting the vascular plugs market

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulatory requirements | -0.7% | Global; most restrictive in EU & Japan | Long term (≥ 4 years) |

| High plug cost versus coils | -0.5% | Asia-Pacific & Latin America | Medium term (2-4 years) |

| Nitinol supply-chain volatility | -0.3% | Global; production concentrated in China/Taiwan | Short term (≤ 2 years) |

| Operator skill gaps in low-volume labs | -0.4% | Emerging markets & rural systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent global regulatory & clinical-trial requirements

Longer development timelines under the U.S. FDA and EU MDR inflate premarket costs. Multi-center trials now track vessel patency for 12 months or longer, delaying break-even points for small innovators. Venture investors react by demanding later-stage data before funding, slowing the influx of novel platforms into the vascular plugs market.

High plug cost versus coil alternatives

Even though a single plug may replace several coils, the perception of higher upfront pricing persists in cost-sensitive regions. Exchange-rate volatility magnifies price differences, prompting procurement teams to favor legacy detachment coils bundled with balloons. Budget constraints therefore temper short-term uptake in parts of Latin America and South-East Asia, restraining the vascular plugs market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Self-Expanding Platforms Hold the Lion’s Share

Self-expanding nitinol plugs delivered 45.62% of the vascular plugs market share in 2025, underpinned by broad diameter ranges and excellent conformability to vessel walls. Familiar detachment mechanisms, the ability to resheath for repositioning, and radiopacity boost operator confidence. Over 2026-2031, the segment maintains a mid-single-digit CAGR as refinements in braid density improve sealing in large proximal arteries. Shaped-memory polymer plugs will record a 6.21% CAGR, driven by rising deployment in small-caliber branches where hydrophilic coatings limit friction and endothelium trauma. Covered/PTFE plugs provide immediate hemostasis in pseudoaneurysms, while micro-vascular plugs become indispensable in neuro-interventions needing ≤ 3 Fr access. Bio-resorbable prototypes remain pre-commercial but draw interest for pediatric anomalies. Altogether, diversification sustains competition and feeds overall expansion of the vascular plugs market.

Second-generation self-expanding models integrate proximal marker bands that enhance fluoroscopic visibility, aligning with operator feedback from high-volume trauma centers. Simultaneously, shape-memory units incorporate radiolucent backbones to maximize MRI compatibility in follow-up imaging. Such incremental refinements differentiate product lines, helping vendors negotiate higher annual volume commitments with group purchasing organizations. These dynamics underpin revenue growth prospects for the vascular plugs industry across hospital tiers.

By Application: PVD Leads While Neurovascular Grows Fastest

Peripheral vascular disease interventions generated 37.68% of the vascular plugs market size in 2025 as critical-limb ischemia admissions rose across urban centers. U.S. outpatient cath labs and German angiography suites increasingly favor plug closure to limit procedure time and enable same-day discharge. Future growth moderates in markets where screening saturation slows incremental PVD diagnoses. Neurovascular disorders, however, will post the fastest 6.78% CAGR as plug-protected flow-diversion strategies expand beyond early-adopter hospitals. Plug-assisted embolization also finds a niche in giant aneurysms where coils alone are inadequate.

Oncology TACE cases continue to demand micro-vascular plugs that fit tortuous hepatic branches, ensuring predictable particulate trapping. The cardiovascular disorder segment leverages plugs for coronary‐artery fistulas and post-operative shunts, representing a smaller but technically demanding niche. In OB-Gyn, uterine artery embolization for fibroids benefits from plug devices that reduce post-procedural pain, enhancing patient satisfaction. Collectively, these indications diversify revenue sources and reinforce resilience within the vascular plugs market.

By Delivery Catheter: Shift Toward Low-Profile Access

Standard ≥ 6 Fr delivery maintained 55.05% share of the vascular plugs market in 2025 because it handles a broad diameter range and leverages existing lab stock. Micro-catheter systems ≤ 3 Fr, however, advance at 6.55% CAGR as distal therapies accelerate. The vascular plugs market size attached to micro-catheters is set to double during the forecast window, boosted by outpatient same-day interventions.

Third-generation plug deployment through 0.021-inch micro-catheters mitigates the torque and kicking issues that once limited distal reach. Supportive diagnostic catheters in the 4–5 Fr band fill a middle niche for tortuous but mid-caliber anatomies.

By Material: Nitinol Dominance Faces Polymer Challenge

Nitinol mesh devices captured 69.02% of the vascular plugs market size in 2025 on account of proven super-elasticity and biocompatibility. Tight tolerance control in nitinol processing centers in the United States and Ireland ensures consistent transformation temperatures for reliable deployment. Vendors are improving electropolishing methods to reduce nickel ion release, further enhancing safety. Hybrid nitinol-polymer plugs will grow at a 6.86% CAGR as their dual-layer structure promises faster endothelialization, a feature valued in high-flow arteriovenous malformations.

Geography Analysis

orth America generated 39.92% of 2025 revenue in the vascular plugs market. The region boasts high procedural volumes, early adopters in tertiary centers, and reimbursement that rewards minimally invasive approaches. Leading facilities such as Mayo Clinic and Cleveland Clinic provide formal plug training that spills into community hospitals, amplifying reach. Moreover, a robust clinical-trial ecosystem accelerates first-to-market timing for novel designs.

Asia-Pacific charts the steepest growth path at a 7.18% CAGR through 2031. Japan and South Korea already mirror Western procedure complexity, while China and India contribute raw volume. Government insurance pilots now reimburse plug embolization in diabetic foot ischemia, tipping the economic balance toward adoption. Local contract-manufacturing under value-engineering programs is cutting per-device cost, aligning technology with price-conscious systems.

Europe remains steady, underpinned by universal coverage and clinician preference for evidence-rich devices. The European Association of Percutaneous Cardiovascular Interventions recently updated guidelines to endorse plug use in traumatic pseudo-aneurysms, resulting in a gradual uptake. Latin America and MEA trail but benefit from humanitarian device exemptions that shorten approval cycles. Mobile training labs and tele-proctoring are addressing operator-skill gaps, positioning these regions for above-average catch-up growth

Regulatory Landscape

In the United States, vascular plugs typically align with the FDA Class II pathway for vascular and neurovascular embolization devices. Market access is supported by 510(k) clearances under the vascular embolization device category, with special controls guidance shaping testing and labeling. Recent U.S. clearances show how product iteration continues to drive compliance work, including Merit Medical Systems' Siege Vascular Plug family (FDA 510(k) clearance in May 2024) and Embolization, Inc.'s Nitinol Enhanced Device (FDA 510(k) clearance in May 2025). Across these examples, bench, biocompatibility, and performance evidence remain central to clearance.

In Europe, market access is governed by EU MDR 2017/745, with higher-risk implantable and Class III/IIb devices requiring robust clinical evaluation, and where applicable interaction with expert panels and scientific advice pathways supported by EMA guidance for high-risk medical devices. Commission Delegated Regulation (EU) 2026/1451 (adopted March 20, 2026) updated the list of implantable and Class III devices exempted from the obligation to perform clinical investigations, explicitly listing endovascular embolisation coils and particles. Manufacturers continue aligning device-drug combination and implant biological evaluation work to updated international standards, including ISO 12417-1:2024 and ISO 10993-6:2026.

Competitive Landscape

The vascular plugs market shows moderate fragmentation: no single vendor controls more than half of global revenue. Market leaders focus on proprietary radiopaque frameworks, finer delivery profiles, and faster-thrombus polymers to edge out competition. Terumo and Abbott maintain flagship nitinol franchises, while Shape Memory Medical drives polymer disruption with high-expansion foam plugs.

R&D pipelines emphasize indication-specific innovation. Neurovascular-branded platforms command premium margins because of heightened clinical risk and require micro-catheter compatibility plus short deployment time. Oncology lines are differentiated by chemotherapeutic retention properties. Mid-sized rivals unable to meet stringent MDR evidence thresholds are forging distribution alliances or becoming acquisition targets for majors seeking quick label expansion.

Hospitals with procedure volumes above 1,000 embolizations annually act as opinion leaders. Successful vendor penetration hinges on pre-clinical support, in-room proctoring, and radiation-dose audits showing measurable reductions. Vendors respond with integrated analytics dashboards that pull from angiography suites to document exposure gains, strengthening long-term purchasing contracts.

Vascular Plugs Industry Leaders

Lifetech Scientific Corporation

Infiniti Medical, LLC

Abbott

Medtronic

Lepu Medical Technology(Beijing)Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is concentrated in low-profile, microcatheter-compatible plug systems that extend embolization into smaller, more distal anatomy while fitting outpatient workflows and same-day discharge protocols in interventional radiology units. The product and procedure trends described in the market point to micro-plugs and covered/PTFE variants. Recent commercialization activity, including Merit Medical's microcatheter-compatible Siege Vascular Plug introduction (reported in February 2025 in professional clinical media), also points to vendor emphasis on faster occlusion and recapture capability in cost- and time-sensitive cath lab settings.

Material innovation remains another opportunity area, as development and clinical use move beyond traditional nitinol mesh toward shape memory polymers and bioresorbable foam-style designs intended for space-filling occlusion with a reduced permanent metallic footprint and potentially fewer imaging artifacts. Published research and technical development themes also track progress in precision deployment concepts (including electrolytic detachment) and next-generation polymer engineering, including multi-transitioning shape memory polymer concepts discussed in 2026 journal literature. This aligns with the report's broader themes around shorter deployment times, lower fluoroscopy exposure, and expanded neurovascular and oncology embolization use cases that require predictable distal navigation.

Recent Industry Developments

- March 2026: Lifetech Scientific Corporation announced its audited consolidated results for the year ended December 31, 2025, highlighting continued progress in its peripheral vascular disease business. The disclosure signals continued commercialization focus in peripheral interventions, supporting ongoing investment capacity for embolization-related portfolios and downstream clinical evidence generation.

- March 2025: Creative Science announced the acquisition of Infiniti Medical LLC, a company known for vascular occlusion devices in veterinary interventional applications. The transaction reflects ongoing consolidation in occlusion-device niches and can broaden product development and distribution reach for specialty embolization platforms adjacent to human vascular plug technology.

- June 2024: Lifetech Scientific (Shenzhen) Co., Ltd. initiated a post-market clinical follow-up study for the Cera Vascular Plug System (ClinicalTrials.gov: NCT06099015) to support EU MDR requirements. This formal clinical evidence pathway supports EU market access positioning and adds longer-term real-world performance data that can influence purchasing decisions and competitive differentiation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers vascular plug devices used by clinicians to intentionally block or close a blood vessel or abnormal vascular communication during minimally invasive procedures, and it is measured as device revenue at the point of sale.

Scope exclusions: Excludes embolization coils, liquid embolic agents, vascular closure devices for access-site sealing, and non-vascular occlusion products.

Segmentation Overview

- By Device Type

- By Product Type

- Self-Expanding

- Covered/PTFE

- Micro-Vascular

- Shaped-Memory

- Bio-Resorbable

- Application

- Peripheral-Vascular

- Oncology-Tace

- Neurovascular-Disorders

- Cardiovascular Disorders

- OB-Gyn

- By Delivery Catheter

- ≥ 6 Fr-Standard

- 4-5 Fr Diagnostic

- ≤ 3 Fr micro-Micro

- By Material

- Nitinol Mesh

- Hybrid Nitinol-Polymer

- Polymer-Only nitol only

- By Product Type

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model with repeatable, public signals around procedure volumes and disease burden that typically drive plug usage. We reviewed sources such as the US FDA device databases (including safety notices), the US Centers for Medicare and Medicaid Services procedure coding references, and CDC burden statistics to understand how embolization and related interventions move over time.

To avoid sizing based only on product talk, we also used clinical literature and guideline discussions published in peer-reviewed journals, plus association resources from interventional radiology and cardiology bodies to verify where plugs are commonly preferred over adjacent occlusion tools. This was supplemented with company annual reports, investor presentations, and trusted press coverage to check commercial launches, regional expansion, and broad pricing commentary. Where helpful, we used a paid subscription for company financials and a patent database to cross-check timelines and product focus areas. The desk sources listed here are illustrative, and many additional public documents were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were conducted across manufacturers, distributors, and clinical users (such as interventional radiologists, cardiologists, and cath lab teams) to validate adoption patterns and realistic pricing bands. We also used these conversations to test assumptions on where plugs are used most often, including arterial versus venous closure situations and congenital-related use cases, and how purchasing differs across hospitals and ambulatory surgical centers across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 38% |

| Mid tier: 47% | Functional/Unit leaders: 43% | EMEA: 37% |

| Smaller Players: 16% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where procedure demand is reconstructed by linking embolization and related intervention volumes to likely plug utilization rates, and then translating the resulting unit pool into value using realistic average selling prices by region. We keep the math grounded by tying assumptions to observable drivers, such as peripheral vascular disease burden, congenital heart intervention activity, catheter-based procedure mix, and the share of cases shifting to minimally invasive embolization.

Once the first-pass value is obtained, we use selective bottom-up approximations to corroborate totals, mainly through supplier and channel checks, sampled ASP-by-volume logic, and a review of disclosed product revenue signals where they exist. When direct unit visibility is limited, gaps are handled by using conservative ranges agreed in interviews, then narrowing them through consistency checks across end users, regions, and the expected split by plug type and material.

For forecasting, we rely on scenario analysis supported by a multivariate view of the key drivers that clinicians and commercial teams consistently cite. Those drivers are then stress-tested for slower or faster adoption. In practice, outlooks were most sensitive to procedure growth, usage rate shifts between plugs and adjacent occlusion tools, and pricing progression as newer deliverability profiles become more common.

Data Validation & Update Cycle

Validation is done through several checks so the final totals do not depend on one dataset or one interview stream. We compare outputs against independent signals like procedure growth expectations, regional healthcare capacity changes, and the implied spending per intervention, and then we investigate any sharp jumps that do not match what experts see in daily practice.

Before sign-off, the work is reviewed in steps, with model logic, assumptions, and arithmetic re-checked by another analyst and then aligned with the narrative conclusions. When variances remain high for a specific region or end user, respondents are re-contacted to confirm whether the issue is scope, pricing, or adoption timing. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Vascular Plugs Market Size Compared Against Other Published Estimates

Published market sizes for vascular plugs can look far apart because the device boundary is not always applied the same way, and because procedure-to-device conversion rates are handled differently across studies. In this topic, the biggest spreads usually come from whether adjacent occlusion tools are blended in, how congenital use cases are counted, and what pricing path is assumed over the forecast window.

By tracking procedure-linked demand signals and refreshing price and utilization assumptions with interviews, Mordor Intelligence keeps the count limited to vascular plug devices used for vessel closure and embolization, instead of mixing in coils or liquid embolics that are often purchased in the same departments. Currency timing, the split of use across hospitals versus ambulatory surgical centers, and how quickly newer deliverability features scale in Asia-Pacific are also common drivers that can push numbers up or down if they are not checked carefully.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 265.94 M (2026) | |

| Trade Publisher A | USD 680.00 M (2024) | Uses a broader interpretation that appears to bundle vascular plugs with wider embolization device spending, and it is not clear how coils, liquid embolics, or congenital-only plug use are separated. |

| Industry Portal B | USD 1800.00 M (2025) | Treats vascular embolization plugs as a wide device bucket, which likely includes multiple occlusion categories and inflates value by applying generalized ASP growth without tight linkage to plug-specific procedure use. |

Taken together, the spread is mostly explained by category boundaries and how demand is translated from procedure activity into units and then into revenue. When the scope is kept to plug devices and assumptions are cross-checked against procedure mix, end-user purchasing, and realistic price ranges, the resulting market size is easier to trace and replicate year after year.

Key Questions Answered in the Report

What is the current size of the vascular plugs market?

The vascular plugs market size stands at USD 265.94 million in 2026, with projections pointing to USD 351.05 million by 2031 at a 5.72% CAGR.

Which segment holds the largest vascular plugs market share?

Self-expanding nitinol plugs lead with 45.62% share, reflecting broad physician familiarity and versatile clinical use.

Why are micro-catheters gaining traction in the vascular plugs industry?

≤ 3 Fr micro-catheters support distal embolization, enable outpatient workflows, and post a robust 6.55% CAGR as precision interventions rise.

Which region is growing fastest?

Asia-Pacific records the highest CAGR at 7.18% through 2031, driven by expanding healthcare access and rising cardiovascular disease incidence.

How do cost savings compare between plugs and coils?

How do cost savings compare between plugs and coils?

Page last updated on: