Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

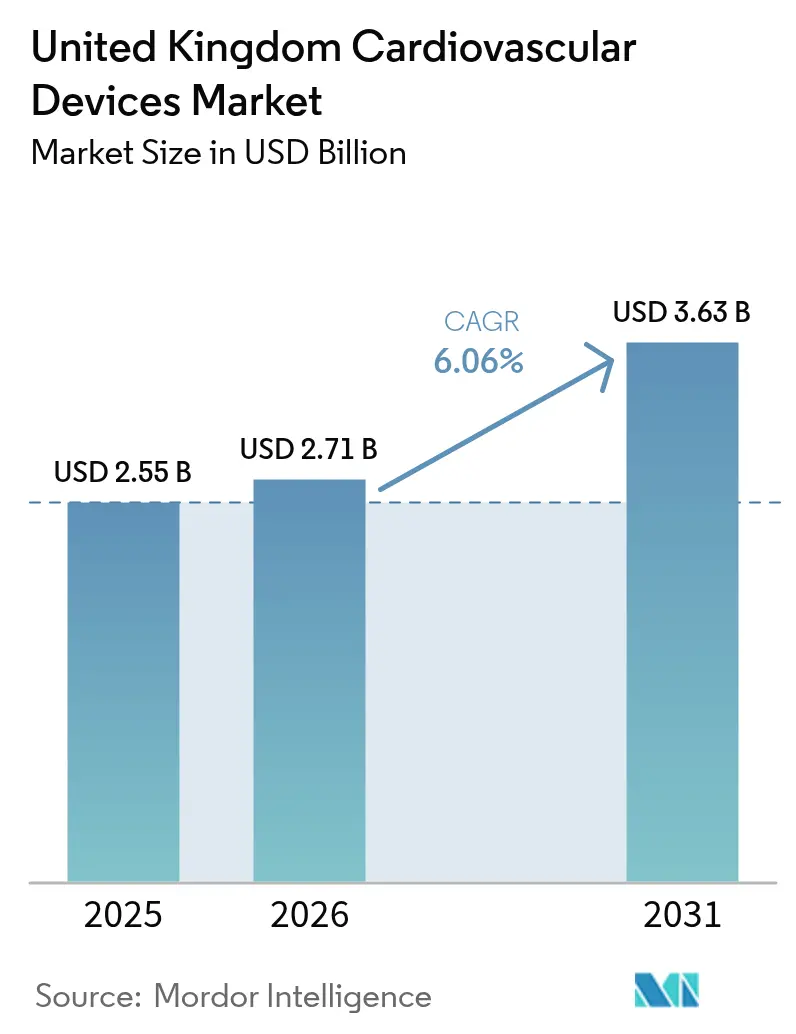

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Cardiovascular Devices Market Analysis by Mordor Intelligence

The UK cardiovascular devices market size was valued at USD 2.55 billion in 2025 and estimated to grow from USD 2.71 billion in 2026 to reach USD 3.63 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031). Robust NHS capital funding, virtual ward roll-outs and rapid uptake of AI-enabled diagnostics are sustaining momentum even as post-Brexit regulatory duplication adds cost and complexity. Demand is concentrating around minimally invasive systems that shorten hospital stays, with transcatheter valve and pulsed-field ablation platforms becoming mainstay therapies. Supply-chain pressures have encouraged domestic manufacturing initiatives, while sustainability mandates are spurring investment in recyclable single-use catheters. Competitive dynamics remain intense, with strategic acquisitions and AI-centric product launches reshaping technology leadership.

Key Report Takeaways

- By product type, therapeutic and surgical devices led with 57.62% revenue share in 2025; diagnostic and monitoring devices is forecast to expand at a 6.63% CAGR through 2031

- By application, coronary artery disease accounted for 40.03% of the UK cardiovascular devices market share in 2025; heart failure applications are advancing at a 6.72% CAGR through 2031

- By end user, hospitals and cardiac centres held 49.15% share of the UK cardiovascular devices market size in 2025; home-care and remote monitoring programs are poised to grow at a 6.41% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHS Long-Term Plan funding boost for cardiac networks accelerating device adoption | +1.2% | England and devolved administrations | Medium term (2 – 4 years) |

| Rapid uptake of remote cardiac monitoring under NHS “virtual wards” programme | +0.8% | National; early gains in Greater Manchester and Norfolk | Short term (≤ 2 years) |

| Growing backlog of elective cardiac procedures driving shift to minimally invasive devices | +0.9% | National; major cardiac centres | Medium term (2 – 4 years) |

| Increasing prevalence of atrial fibrillation in ageing UK population raising demand for rhythm-management devices | +1.1% | National; higher impact in England and Wales | Long term (≥ 4 years) |

| Government procurement frameworks favouring environmentally sustainable single-use catheters | +0.4% | National; aligned with NHS net-zero targets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NHS Long-Term Plan Funding Boost for Cardiac Networks Accelerating Device Adoption

Targeted investments channelled through the GBP 25.7 billion NHS uplift for 2024-2025 are modernising cardiac networks and enabling faster technology rotation . Allocating GBP 1.5 billion to surgical hubs and GBP 70 million to advanced radiotherapy suites gives trusts the capacity to clear procedure backlogs while integrating novel devices. The NHS 10-Year Plan ties procurement to measurable outcomes, favouring vendors with strong clinical-evidence files. Integrated care systems encourage cross-trust purchasing, increasing order volumes and shortening adoption cycles by up to two years[1]Source: Department of Health and Social Care, “Fit for the Future: Health and Social Care Secretary's statement,” GOV.UK . These funding streams thus reinforce first-mover advantages for innovators with proven value propositions.

Rapid Uptake of Remote Cardiac Monitoring under NHS “Virtual Wards” Programme

NHS England aims to deliver 50,000 virtual-ward beds by 2025, fundamentally redesigning cardiac care pathways. Early pilots such as the Northern Care Alliance’s 500-bed model cut acute admissions by 30%, validating the service design at scale. NICE guidance endorsing HeartLogic and TriageHF technologies, which reduce heart-failure hospitalisations by up to 72%, further underpins rapid diffusion[2]Source: Imperial College Healthcare NHS Trust, “Remote Monitoring of Heart Attack Patients Significantly Reduced Hospital Readmissions,” Imperial College Healthcare NHS Trust, imperial.nhs.uk . Academic studies at Imperial College Healthcare show 76% fewer readmissions when tele-monitoring complements standard therapy. Savings of GBP 1,958 per patient strengthen the business case, opening new revenue channels for device makers aligned with NHS digital architecture.

Growing Backlog of Elective Cardiac Procedures Driving Shift to Minimally Invasive Devices

Pandemic disruptions left thousands awaiting cardiac surgery, accelerating the pivot to catheter-based interventions that shorten procedure times and recovery periods. TAVR platforms such as Medtronic’s Evolut FX+ now serve broader patient groups following 2024 FDA approval. Investments in hybrid operating theatres allow complex cases to be handled as day-care procedures, easing throughput bottlenecks. Pulsed-field ablation systems like Abbott’s Volt deliver 99.1% pulmonary-vein isolation while reducing collateral damage, attracting electrophysiologists under time pressure. NHS commissioning teams therefore prioritise devices that compress length of stay and free capacity for high-acuity work.

Increasing Prevalence of Atrial Fibrillation in Ageing UK Population Raising Demand for Rhythm-Management Devices

More than 1.5 million Britons live with atrial fibrillation and lifetime risk has climbed to 30.9% for adults ≥45 years. Direct treatment costs now exceed GBP 2.5 billion annually. AI-enabled insertable monitors such as Biotronik’s BioMonitor IV cut false detections by 86%, conserving clinician time. Leadless systems like Abbott’s AVEIR dual-chamber pacemaker reduce surgical complications and infection risk, aligning with NHS targets to lower avoidable admissions. Demographic momentum guarantees sustained demand for advanced rhythm-management solutions.

Restraint Imoact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| High failure-recall rates of certain stent and pacemaker models eroding clinician confidence | –0.7% | National; major cardiac centres | Short term (≤ 2 years) |

| NHS workforce shortage constraining equipment replacement cycles | –0.5% | National; rural and underserved regions | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

High Failure-Recall Rates of Certain Stent Models Eroding Clinician Confidence

Class I recalls involving Boston Scientific’s Accolade pacemakers and Abbott’s Assurity series have shaken trust, prompting closer scrutiny of new technologies. MHRA reforms effective June 2025 demand active surveillance and faster incident reporting, raising compliance costs and delaying launches. Adverse publicity extends beyond recalled SKUs, dampening uptake across adjacent product categories. Clinicians now seek extensive post-market data before switching platforms, lengthening sales cycles and elevating barriers for SMEs.

NHS Workforce Shortage Constraining Equipment Replacement Cycles

England requires 49,162 additional full-time doctors merely to hit OECD averages, with staffing gaps most acute in cardiology theatres. Resource-strapped trusts stretch device lifecycles, deferring upgrades that demand specialised training. Government plans to double medical-school places will take seven years to influence capacity, sustaining near-term bottlenecks. Shortfalls in cardiac technicians further restrict deployment of sophisticated devices needing expert programming. Immigration curbs amplify exposure to workforce risk, prolonging the utilisation of legacy equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Devices Lead Despite Diagnostic Acceleration

Therapeutic and surgical platforms generated 57.62% of 2025 revenues, sustained by well-resourced cardiac centres performing high-value interventions. Uptake of ultrathin drug-eluting stents and TAVR systems illustrates how procedural efficiency steers purchasing decisions. Abbott’s AVEIR leadless pacemaker, now under breakthrough-device designation, shows the innovation premium vendors can command .

Diagnostic and monitoring solutions, though smaller today, are projected to grow at a 6.63% CAGR through 2031 as prevention and remote care take centre stage. AI-enabled ECG devices that rival 12-lead hospital units underscore this momentum. Virtual-ward expansion embeds remote telemetry in standard care pathways, lifting recurring revenue from cloud analytics. Consequently, the UK cardiovascular devices market size for diagnostics is on path to outstrip therapeutics in growth pace, reshaping revenue mixes over the decade.

By Application: Coronary Dominance Challenged by Heart-Failure Growth

Coronary artery disease applications controlled 40.03% of the UK cardiovascular devices market share in 2025, benefiting from decades of PCI optimisation and a broad installed base of cath-lab infrastructure . Drug-eluting stents with ultrathin struts deliver superior long-term patency, justifying premium pricing .

Heart-failure interventions are expanding fastest at 6.72% CAGR, pushed by earlier detection and an ageing population. Remote monitoring platforms approved by NICE reduce rehospitalisations, freeing resources and validating continued investment . Ventricular assist devices remain niche but pipeline recalls open white-space for emergent alternatives. Overall, the UK cardiovascular devices market size allocated to heart-failure solutions will widen markedly as community-based management scales.

By End User: Hospital Dominance Faces Home-Care Disruption

Hospitals and cardiac centres held 49.15% of 2025 spend, powered by complex procedure volumes and large capital budgets . Dedicated surgical hubs funded under the NHS uplift further bolster inpatient device use. Ambulatory surgical centres provide cost-effective outlets for same-day TAVR or ablation, gradually siphoning share from tertiary centres.

Home-care and remote monitoring programmes are rising at 6.41% CAGR, propelled by virtual-ward economics that save GBP 1,958 per patient . Wearables paired with AI-driven analytics alert clinicians to decompensation events, reducing emergency admissions. As interoperability with NHS electronic records improves, vendors offering frictionless data flows gain decisive advantage. The UK cardiovascular devices market share captured by at-home modalities is therefore set to climb steadily.

Geography Analysis

England remains the epicentre of demand, reflecting its 56 million population and concentration of advanced cardiac centres. Barts Health NHS Trust alone supports 1.5 million cardiovascular patients, anchoring large-volume procurement . Greater Manchester’s 500-bed virtual-ward success story demonstrates northern capacity for rapid innovation diffusion, cutting admissions by 30% . Scotland leverages centralised procurement via NHS National Services to drive uniform adoption, while Wales emphasises population-health dashboards to pre-empt disease progression.

Regulatory nuances under the Northern Ireland Protocol mean providers in Belfast often navigate dual UKCA and CE compliance, influencing vendor choice. Deprived coastal and rural locales show higher disease prevalence, steering public-health funding toward preventive diagnostics. Norfolk and Waveney’s GBP 1.425 million digital-population-health initiative exemplifies these targeted investments .

Brexit-induced import friction spurs interest in local manufacturing; government incentives now support domestic catheter and lead production to harden supply chains. Nationwide, the GBP 10 billion digital-transformation envelope earmarked through 2029 will standardise interoperability, lowering adoption barriers for cloud-connected devices. Academic-industry clusters around London, Oxford and Cambridge catalyse early trials, enabling innovators to refine offerings ahead of national rollout. Collectively, these geographic dynamics ensure demand remains resilient yet regionally nuanced.

Regulatory Landscape

Cardiovascular devices in Great Britain are primarily regulated under the UK Medical Devices Regulations 2002 (UK MDR 2002), as amended, with the Medicines and Healthcare products Regulatory Agency (MHRA) overseeing market access, clinical investigations, and post-market controls. For drug-device combination products relevant to cardiovascular care (for example, drug-eluting or heparin-coated devices), classification depends on the principal intended action. Where the medicinal substance is ancillary, the product is regulated as a medical device under UK MDR 2002 (with consultation on the medicinal aspects), while integral combinations where the medicine is the principal component follow the medicinal product route.

The UK reform program continues to reshape compliance planning and evidence generation. Post-market surveillance requirements strengthened via 2024 legislation took effect on 16 June 2025, raising expectations around traceability and safety reporting for implanted and high-risk cardiovascular products. In May 2026, the MHRA published draft Medical Devices (Amendment) Regulations 2026 for notification, including proposals such as international reliance pathways and updated, risk-proportionate classification concepts aligned with international frameworks. Manufacturers are monitoring these changes alongside UKCA/CE considerations, especially where Northern Ireland pathways and cross-border supply increase labeling and conformity complexity.

Value Chain Analysis

The UK cardiovascular devices value chain starts with specialized raw materials and components (for example, polymers, electronics, and alloys such as nitinol), moving into device design, prototyping, and regulated manufacturing under quality-system requirements. The chain then progresses through conformity assessment and registration with the MHRA under UK MDR 2002. For combination products and clinical evidence generation, it includes structured regulatory submissions and study operations, including the MHRA-integrated IMP+Device review route for investigations that include both an investigational medicinal product and a medical device, which can align timelines and reduce duplicative review steps.

Downstream, procurement and distribution are shaped by NHS buying power and centralized frameworks. NHS Supply Chain runs category-led procurement and framework agreements that concentrate volumes and standardize supplier requirements, including resilience measures such as contingency stock and forward tracking (for example, the Structural Heart and Ventricular Assist Devices framework launched on 20 June 2025). Distribution typically flows from UK warehousing and regional logistics networks into acute trusts and cardiac centers, while private providers often contract more directly with manufacturers or distributors. The value chain is also tightening through engineering and manufacturing capability consolidation (for example, cleanroom assembly and specialized metal processing), along with hospital-industry collaborations that pair hardware supply with digital workflow integration for remote monitoring and AI-supported care pathways.

Competitive Landscape

Market leadership alternates among Medtronic, Abbott, Boston Scientific and Edwards Lifesciences, each leveraging differentiated portfolios to secure NHS contracts. Teleflex’s EUR 760 million acquisition of Biotronik’s vascular-intervention unit adds CE-marked drug-coated balloons and metallic scaffolds, broadening competitive repertoire . Edwards’ USD 300 million buyout of Innovalve secures next-generation mitral-valve systems, reinforcing its structural-heart franchise.

AI integration is emerging as a decisive moat; Medtronic’s AccuRhythm platform cuts false alerts by 85% and frees 186 hours of clinician time per 200 patients. Meanwhile, Johnson & Johnson MedTech’s recycling scheme satisfies NHS sustainability scoring, a differentiator in tenders. Disruptors like Echopoint Medical, backed by GBP 4.2 million Series A funding, showcase UK ingenuity with optical-flow coronary assessment that could challenge incumbent FFR technologies.

Competitive intensity is further heightened by MHRA’s faster innovation pathway, which pairs stricter surveillance with clearer guidance. Vendors able to generate robust real-world evidence and meet environmental targets are positioned to capture outsized share as procurement frameworks evolve.

United Kingdom Cardiovascular Devices Industry Leaders

Abbott Laboratories

Cardinal Health

Medtronic Plc

Boston Scientific Corporation

Biotronik

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two near-term whitespace areas are taking shape around (1) evidence-backed remote monitoring ecosystems linked to NHS virtual ward pathways and (2) faster, lower-friction routes for UK market entry and clinical validation. NHS England is scaling virtual wards, with a stated aim of 50,000 virtual-ward beds by 2025. NICE-endorsed heart-failure monitoring technologies also strengthen the commissioning logic for connected sensors plus analytics, creating room for vendors that offer interoperable devices, workflow integration, and services that reduce alert burden and admissions. This opportunity extends beyond devices into recurring software, data-management, and clinical-support layers that fit with NHS digital architecture.

On the access side, MHRA actions create practical openings for innovators and global firms balancing UKCA requirements with international approvals. The MHRA introduced a fee waiver pilot in January 2026 for micro and small UK firms, and in February 2026 reported a 17% increase in approved clinical investigations in 2025 versus 2024, with average approval times of 51 days. That development supports faster iteration for novel cardiovascular platforms, including combination products routed via IMP+Device reviews. In parallel, the draft Medical Devices (Amendment) Regulations 2026 published in May 2026 signaled movement toward reliance-style pathways and updated classification concepts. This is encouraging companies with strong prior regulatory dossiers and robust post-market evidence capabilities to build UK strategies that combine accelerated study execution, real-world evidence generation, and tender readiness under NHS procurement frameworks, which increasingly score sustainability and supply resilience.

Recent Industry Developments

- June 2026: Medtronic completed its acquisition of Scientia Vascular, adding neurovascular access technologies to its portfolio. The deal strengthens Medtronic's position in catheter-based procedures that share adjacent capabilities with cardiovascular interventions, including guide and access platforms and hospital purchasing alignment. It also signals continued consolidation among large strategics as they broaden procedural toolkits and bundled offerings for NHS and private cath labs.

- May 2026: Boston Scientific announced a strategic investment in MiRus LLC, taking an equity stake and expanding access to next-generation structural heart technology, including a balloon-expandable TAVR concept. The deal deepens Boston Scientific's exposure to minimally invasive valve therapy innovation, a priority area for UK cardiac centers focused on throughput and length-of-stay reduction. It also adds competitive pressure on incumbent transcatheter valve portfolios as novel materials and designs progress.

- May 2025: NHS England began a nationwide roll-out of advanced 3D heart scans to speed diagnosis and improve pathway efficiency. Broader deployment of high-end cardiac imaging increases demand for capital equipment, service contracts, and downstream interventional planning tools, supporting diagnostic and monitoring growth alongside therapeutic procedures. It also reinforces procurement momentum for technologies that shorten time to diagnosis and help manage elective backlogs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the UK cardiovascular devices market is defined as revenue generated from diagnostic, monitoring, therapeutic, and surgical devices used to detect, manage, or treat heart and vascular conditions across the United Kingdom.

Scope exclusions: We exclude pharmaceuticals, standalone consumables not sold as part of a cardiovascular device system, and software-only health apps that are not tied to a regulated device sale.

Segmentation Overview

- By Product Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia & Conduction Disorders

- Heart Failure & Cardiomyopathy

- Structural & Congenital Heart Defects

- Peripheral Vascular Disease

- By End User

- Hospitals & Cardiac Centres

- Ambulatory Surgical Centres

- Cardiology/EP Clinics

- Home-care & Remote Monitoring Programs

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by setting the demand context for the UK, since devices are used when diagnostics and procedures occur. We reviewed public healthcare activity and funding signals, including NHS England publications, NHS Supply Chain updates, and NICE guidance and technology appraisals, to understand how care pathways are changing.

To keep assumptions realistic, we also checked national statistics and trade signals, including the Office for National Statistics for macro indicators, HMRC trade statistics for import and export direction, and peer-reviewed clinical journals for adoption patterns in stents, rhythm management, and structural heart procedures. Company filings, investor presentations, and reputed press were used to sanity-check pricing direction and product mix shifts. Paid subscriptions were used selectively for company financial intelligence, patent screening, and shipment-level trade records to fill gaps. The sources named here are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and used in the UK, and on separating one-time capital equipment from recurring device demand. We spoke with a mix of manufacturers, distributors, hospital procurement contacts, cath lab and cardiac center staff, and clinicians, and then used these inputs to align procedure-linked volumes, typical price bands, and replacement cycles across major device groups.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | |

| Mid tier: 49% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 56% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where procedure and diagnosis activity in the UK is translated into device demand pools and then value is reconstructed using device usage per case and average selling prices by major product group. Once that structure was stable, selective bottom-up approximations were used to test the totals, including supplier revenue splits, channel checks for high-volume categories, and sampled ASP multiplied by estimated unit volumes.

Key inputs that shaped the model included the number of cath lab and electrophysiology procedures, stent and balloon utilization patterns, implant volumes for pacemakers and ICDs, structural heart intervention growth (including TAVI), and the shift toward remote cardiac monitoring in follow-up care. For pricing, we tracked list-to-net discount direction, mix shifts between premium and standard devices, and currency conversion timing for imported categories. When data was patchy for smaller categories, gaps were handled by anchoring to adjacent procedure volumes and using expert-validated share splits, and then checking that the combined picture still fits overall care capacity and referral patterns.

Forecasts were produced using scenario analysis because NHS funding cycles, waiting list clearance, and adoption of minimally invasive procedures can change at different speeds. Each scenario was tied to explicit assumptions on procedure growth, replacement cycles, and price progression, and then refined using primary feedback on what procurement teams and clinical users expect over the next few years.

Data Validation & Update Cycle

Validation is done by triangulating outputs across multiple checks, so the final number is not dependent on one input series. Analysts compare results against independent signals like procedure volumes, import direction for key device families, and company-level revenue exposure to the UK, and then review anomalies such as sudden price jumps or unit growth that does not match care capacity.

Before sign-off, the model and assumptions go through multi-step analyst reviews, and re-contact is triggered when a mismatch shows up in a high-value area like rhythm management, coronary intervention devices, or valves. Reports are refreshed annually, with interim updates when material events occur such as policy changes, major reimbursement moves, or supply disruptions. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's UK Cardiovascular Devices Market Size Compared With Other Published Estimates

Published market values for UK cardiovascular devices can look far apart because authors draw the market boundary differently, and they also use different starting years. In this space, small choices like whether capital imaging platforms are bundled into cardiovascular devices, or whether remote monitoring services are priced in, can quickly change the total.

NHS procedure throughput signals and device adoption checks across stents, rhythm management implants, and structural heart interventions are used as evidence to keep Mordor Intelligence's estimate tied to procedure-linked volumes and procurement-validated price bands. Gaps usually come from scope expansion into broader medical equipment, aggressive price inflation assumptions that are not confirmed through buyer feedback, and currency conversion done using a different reference period, which can overstate USD values in certain years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.55 B (2025) | |

| Industry Publisher A | USD 3.07 B (2024) | Uses a different base year and a wider type bucket that can blend cardiovascular monitoring hardware with broader digital care categories, which lifts the starting value before forecasting. |

| Regional Consultancy B | USD 19.07 B (2022) | The value appears to reflect a much broader inclusion set, or a price and volume basis that does not reconcile with procedure-linked demand scaling and typical UK procurement price ranges for the listed device groups. |

The comparison shows that most of the spread is driven by what gets included, plus how prices and currency timing are handled for imported devices. By tying volumes to care activity and checking pricing through procurement and channel inputs, we keep the market value traceable to clear drivers that can be repeated and updated.

Key Questions Answered in the Report

What is the current size of the UK cardiovascular devices market?

The market is valued at USD 2.71 billion in 2026 and is forecast to reach USD 3.63 billion by 2031.

Which product segment leads sales in the UK cardiovascular devices market?

Therapeutic and surgical devices account for 57.62% of 2025 revenues, driven by TAVR systems and rhythm-management implants.

How fast is the diagnostic and monitoring segment growing?

The diagnostic and monitoring category is projected to advance at a 6.63% CAGR through 2031 thanks to AI-enabled ECG and remote-monitoring platforms.

Why are virtual wards important for device manufacturers?

NHS virtual wards cut hospitalisations by up to 30% and save GBP 1,958 per patient, creating recurring demand for remote-monitoring hardware and analytics services.

Page last updated on: