Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

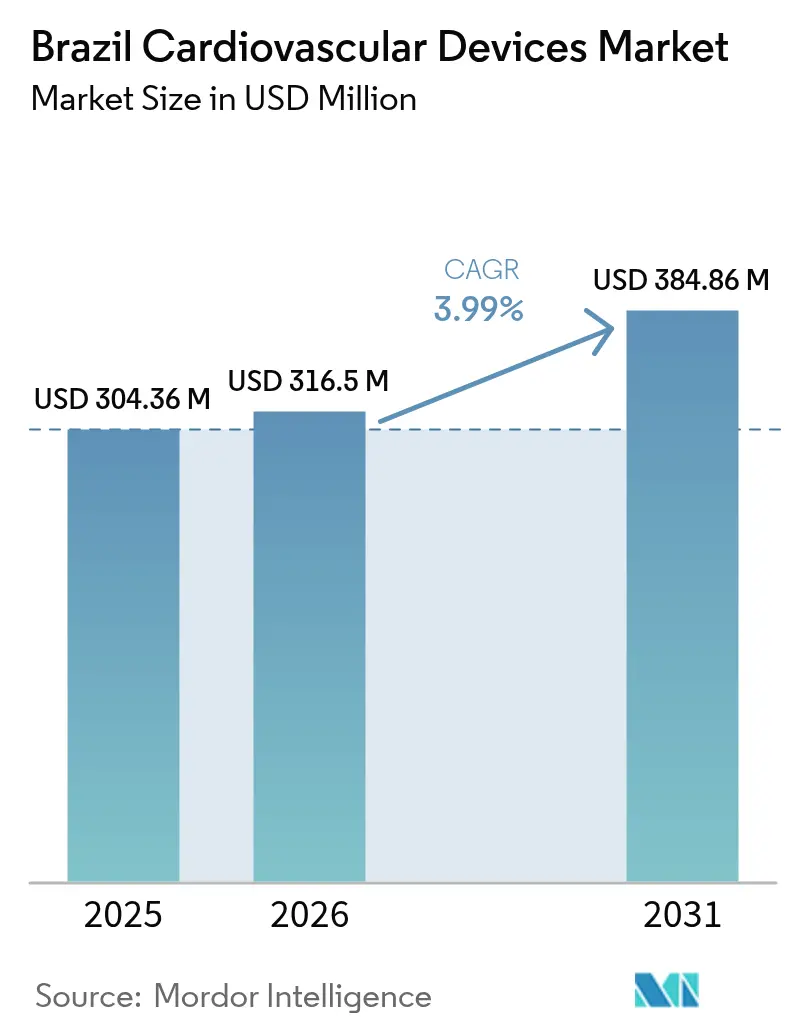

| Base Year Market Size (2025) | USD 304.36 Million |

| Market Size (2026) | USD 316.5 Million |

| Market Size (2031) | USD 384.86 Million |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Cardiovascular Devices Market Analysis by Mordor Intelligence

The Brazil Cardiovascular Devices Market size was valued at USD 304.36 million in 2025 and estimated to grow from USD 316.5 million in 2026 to reach USD 384.86 million by 2031, at a CAGR of 3.99% during the forecast period (2026-2031).

Demand is fueled by rising coronary disease prevalence in large cities, rapid uptake of transcatheter therapies in the Southeast, and continued expansion of supplementary health plans that make advanced treatments more affordable. Multinational leaders are investing aggressively even as long ANVISA timelines delay local launches and skilled-staff shortages hamper high-complexity device adoption . Digital health rules now require broader use of remote cardiac monitoring, positioning connected diagnostics to capture incremental procedure volumes across public and private systems.

Key Report Takeaways

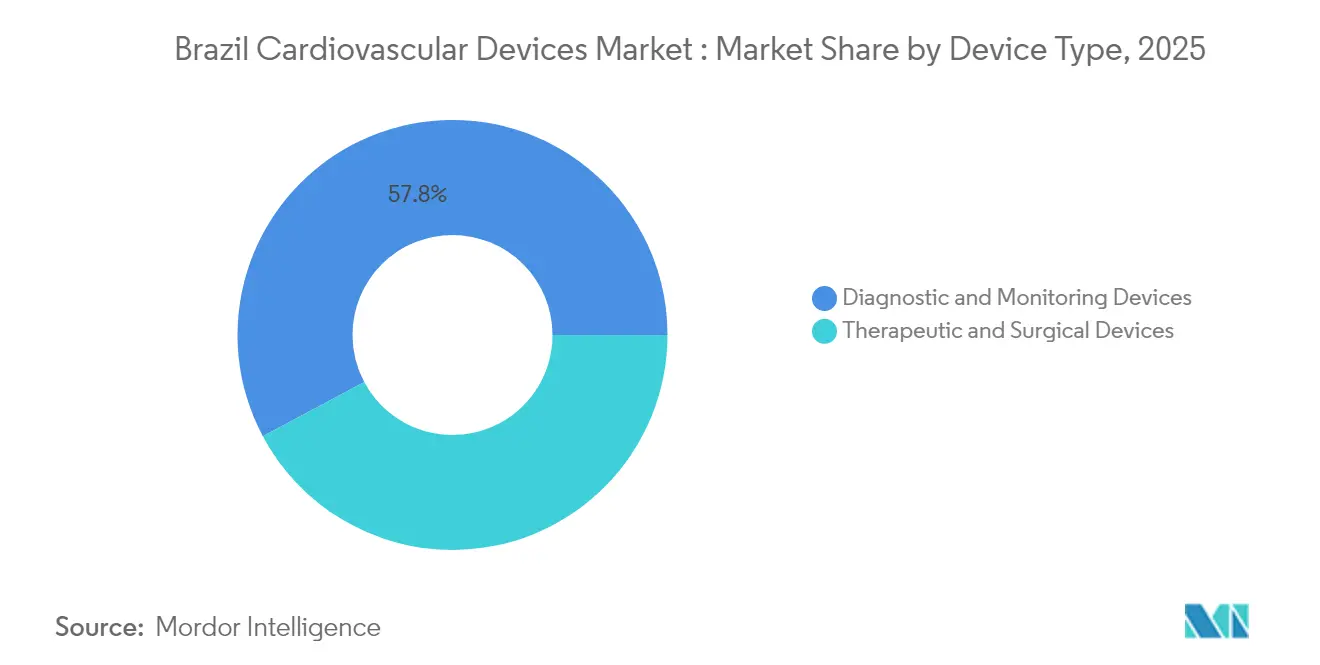

- By device type, diagnostic and monitoring products led with 57.80% of cardiovascular devices market share in 2025 while expanding at a 6.05% CAGR to 2031 .

- By application, coronary artery disease accounted for 55.00% share of the cardiovascular devices market size in 2025; structural heart disease is projected to rise at a 6.46% CAGR through 2031 .

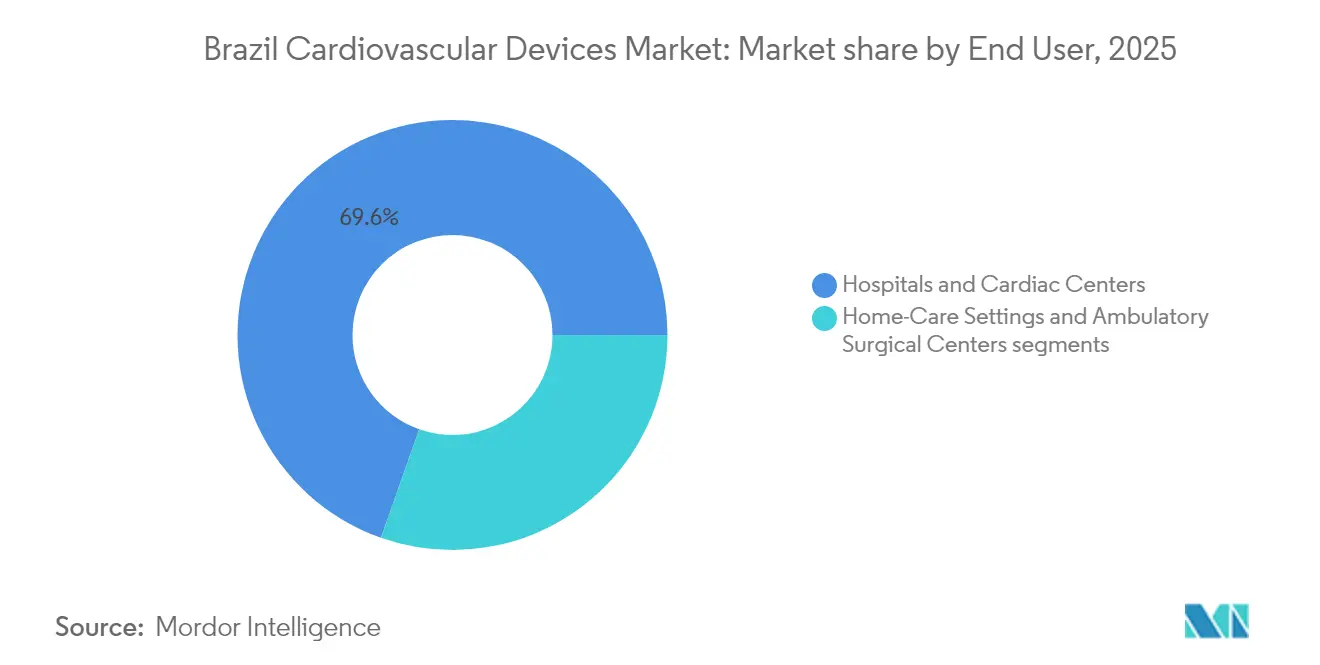

- By end-user, hospitals and cardiac centers held 69.60% revenue share in 2025, whereas ambulatory surgery centers are advancing at a 6.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of coronary artery disease in Brazil’s urban centers | 1.80% | Nationwide; highest in Southeast & South | Medium term (2-4 years) |

| Privatization-fueled growth of supplementary health insurance plans boosting device affordability | 1.20% | Major urban centers | Medium term (2-4 years) |

| Rapid adoption of transcatheter therapies in Southeast Brazil | 1.50% | Southeast with spillover to South & Northeast | Short term (≤2 years) |

| Digital health integration mandates accelerating remote cardiac monitoring uptake | 0.90% | Nationwide; early gains in Southeast & South | Medium term (2-4 years) |

| Expansion of SUS-funded high-complexity cardiac procedure reimbursement codes | 0.80% | Nationwide public-hospital network | Short term (≤2 years) |

| Localization incentives under PDPs driving multinational manufacturing investments | 0.70% | Industrial hubs in Southeast & South | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Coronary Artery Disease in Brazil's Urban Centers

Cardiovascular morbidity is climbing sharply in São Paulo, Rio de Janeiro and other metropolises as the share of residents aged ≥65 heads to 13.6% by 2030. Uneven primary-care performance—worst in the Southeast—pushes more patients toward interventional solutions rather than prevention [1]Agência Nacional de Vigilância Sanitária, “Obter autorização de importação de substância medicamento,” gov.br . Diagnostic cardiac imaging guidelines released in 2024 emphasize CT and MRI as first-line tools, spurring equipment upgrades across referral hospitals [2]. Private health insurers cover over half of specialty consultations, supporting broader access to stents, valves and rhythm devices. Collectively, these factors elevate procedure volumes and reinforce the cardiovascular devices market growth outlook.

Privatization-Fueled Growth of Supplementary Health Insurance Plans Boosting Device Affordability

Brazil’s private payer base keeps expanding, helped by hospital consolidation such as the proposed Dasa–Amil merger that would create a 4,500-bed network with USD 2 billion in annual sales. Larger systems negotiate bulk discounts yet also demand newer technology, raising throughput for transcatheter valves and intracardiac monitors. Reimbursement studies show intensive-care tariffs increase in line with provider market share, allowing investors to recoup capital expenditures on high-end devices sooner. Supplementary plans now cover a broader list of cardiovascular interventions approved by ANS in October 2024, widening eligibility for minimally invasive procedures [1]. Greater disposable income among insured urban dwellers accelerates elective uptake, supporting the cardiovascular devices market trajectory through 2030.

Rapid Adoption of Transcatheter Therapies in Southeast Brazil

Southeast cardiac centers rapidly embraced TAVR once mid-2024 data confirmed clinical parity with surgical valve replacement. Medtronic’s Evolut FX+ system began full launch after CE Mark, benefitting from established distributor footprints in Brazil medtronic. Competitive pressure intensified as Abbott and Boston Scientific readied rival platforms, putting Edwards’ leadership at risk. Global majors collectively invested more than USD 16.7 billion in cardiac assist and USD 13.1 billion in coronary intervention technology during 2024, earmarking emerging markets for near-term rollouts. Robust capital flows speed field training programs and inventory stocking, positioning transcatheter solutions to outpace the wider cardiovascular devices market over the next two years.

Digital Health Integration Mandates Accelerating Remote Cardiac Monitoring Uptake

Regulatory guidelines now push clinics to activate remote follow-up functions on implanted cardiac devices, driving a near doubling in monitoring connections from 2018 to 2021 in comparable settings revista. Paid digital practice-management systems operate in 59% of Brazilian clinics, laying infrastructure for telemetric uploads and AI-enabled rhythm analytics doctoralia. Teleconsultations already triage 58.1% of isolated-region patients with suspected cardiac symptoms, demonstrating the scalability of virtual pathways abccardiol. AI-driven adaptive devices contribute 5.2% annual sector growth as of January 2025, signalling sustained demand for software-rich implants medtechintelligence. These trends collectively lift diagnostics and rhythm segments above the base cardiovascular devices market rate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy ANVISA approval timelines for novel cardiovascular technologies | -1.30% | Nationwide | Short term (≤2 years) |

| Skilled electrophysiologist shortage constricting advanced CRM implant volumes | -0.80% | Stronger impact in North & Northeast | Long term (≥4 years) |

| Currency volatility elevating import costs of high-end devices | -1.00% | Nationwide; most acute for private importers | Short term (≤2 years) |

| Limited cath-lab density in Northern & Northeastern regions | -0.60% | North & Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy ANVISA Approval Timelines for Novel Cardiovascular Technologies

Device makers navigate multi-step submissions that include Brazilian Good Manufacturing Practice audits, technical dossiers, and in-country representation, adding 30 days just for import authorization on top of dossier review. Even after the recent IN 289/2024 aimed at streamlining certain products, approval lags still contrast with the United States’ 101-day clearance for complex valves. The delay slows first-to-market advantage and can shorten patent-protected sales windows. Hospitals may postpone capital budgets while waiting for registrations, hindering quicker penetration of leadless CRM systems or next-generation ablation catheters. Consequently, the regulatory hurdle subtracts an estimated 1.3 percentage points from the cardiovascular devices market CAGR until reforms gain traction.

Skilled Electrophysiologist Shortage Constricting Advanced CRM Implant Volumes

Only a limited pool of clinicians is certified to implant high-complexity rhythm systems, especially outside tier-one metros. Training audits in 2024 found ICU nurses underprepared to manage real-time device data, reflecting broader skills gaps bmcnursing. Professional societies are rolling out virtual mentoring and sustainability programs yet scaling remains slow. Regional inequality is stark: the Southeast already struggles with basic primary care metrics, implying even tighter capacity for sophisticated electrophysiology. The shortage restricts implant throughput for leadless CRT-pacers that entered clinical routine after promising 2024 trial results. As staffing pipelines mature slowly, the constraint weighs on the cardiovascular devices market expansion into the next decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostics Dominate as Monitoring Goes Remote

In 2025 diagnostic and monitoring products captured 57.80% of the cardiovascular devices market size and are advancing at a 6.05% CAGR to 2031, reflecting guideline-driven adoption of cardiac CT and MRI in major centers. Uptake also rides on the rollout of cloud-based ECG platforms that feed AI algorithms for arrhythmia detection. Therapeutic segments grow more slowly yet remain strategic. Cardiac rhythm management benefits from Boston Scientific’s modular leadless system that posted high implant success at ESC 2024, prompting Brazilian electrophysiologists to prepare for broader deployment once ANVISA approves. Transcatheter heart valves represent the fastest unit growth as Medtronic and Abbott channel inventory into urban hubs soon after CE-level clearances medtronic. Investments totaling USD 25.01 billion in rhythm devices worldwide indicate a pipeline of miniaturized implants and ablation tools that will expand the cardiovascular devices industry footprint in Brazil over the medium term.

By Application: Coronary Disease Holds Sway while Structural Heart Surges

Coronary artery disease procedures represented 55.00% of 2025 revenue, underscoring the heavy demand for stents, atherectomy tools and diagnostic angiography in aging urban populations. Premium drug-eluting platforms enter formularies as insurers broaden coverage, sustaining solid volumes across private networks. Structural heart interventions, including TAVR and transcatheter mitral repair, show the highest 6.46% CAGR thanks to device miniaturization and better outcome data . Arrhythmia therapy demand rises with pulsed-field ablation systems that shorten procedure time and reduce complications, aligning with workload constraints in electrophysiology units. Hypertension devices, particularly renal denervation catheters, gain traction ahead of 2025 commercialization milestones and may push the cardiovascular devices market share of this niche higher once local payers issue coverage policies.

By End-User: Hospitals Retain Primacy yet ASCs Accelerate

Hospitals and cardiac centers delivered 69.60% of cardiovascular devices market revenue in 2025 because they control hybrid ORs, catheterization labs and intensive-care capacity. Consolidation among leading chains strengthens purchasing leverage and speeds technology standardization. Ambulatory surgery centers show the most rapid 6.89% CAGR as payers encourage shifts to lower-cost sites for PCI and rhythm generator replacement beckers. Surveys of ASC executives reveal optimism that cardiology will be a top growth specialty during 2025-2030, assuming site-neutral reimbursement laws advance. Consulting analyses predict 6%-8% annual revenue expansion for Brazilian ASCs, which aligns with forecasts for the cardiovascular devices market and signals growing competition for hospital cath-lab volumes.

Geography Analysis

The Southeastern corridor of São Paulo, Rio de Janeiro and Minas Gerais accounts for the largest slice of the cardiovascular devices market size owing to dense tertiary hospitals, high insurer penetration and the country’s highest procedural throughput. Specialist referral centers such as Hospital Israelita Albert Einstein commissioned hybrid rooms for structural heart interventions in August 2024, cementing the region’s technological leadership. Diagnostic imaging standards issued by national cardiology bodies target metropolitan populations first, reinforcing regional concentration.

The Southern region ranks second in spending, helped by above-average healthcare outlays per capita and efficient public-private partnerships. Elective TAVR and left-atrial appendage closure volumes are rising as state-level systems integrate private insurers under supplementary plans. Meanwhile, the Northeast posts the fastest cardiovascular devices market growth as primary-care performance scores surpass those in wealthier areas, unlocking new demand for ultrasound, ECG and first-time stenting procedures.

North and Central-West territories remain smaller but exhibit strong latent demand. Teleconsultation programs connect isolated clinics to metropolitan cardiologists, with 58.1% of referrals addressing cardiovascular symptoms. ANVISA initiatives to speed digital-health certifications, plus federal funding of R$150 million for remote diagnostics equipment in July 2024, support a decentralized care model. These policies promise steady uptake of wearable monitors and cloud ECG hubs in regions previously underserved by the cardiovascular devices market.

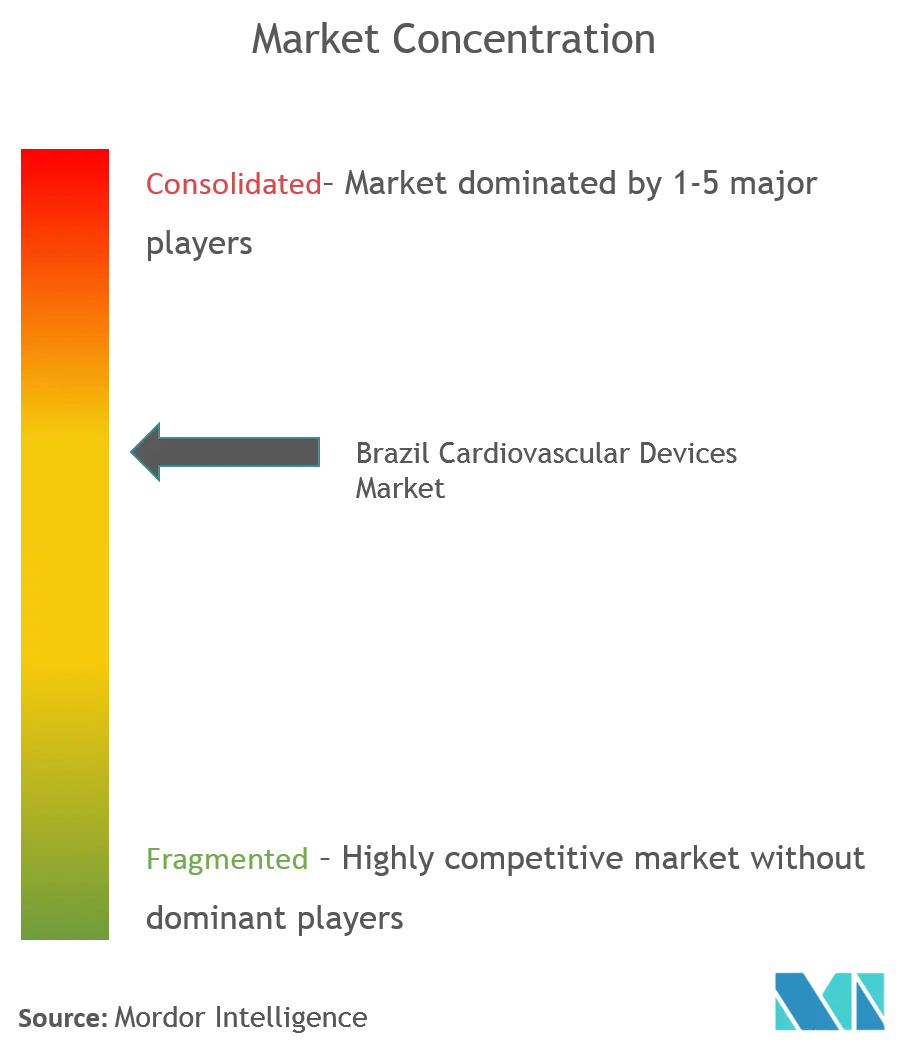

Competitive Landscape

Multinational suppliers dominate Brazilian revenue streams. Medtronic’s cardiovascular division reported higher global sales in its latest quarter and is channeling additional resources toward local valve rollouts. Abbott retains a strong worldwide share and is extending its Libre-style connectivity for rhythm‐device telemetry at Brazilian sites. Boston Scientific, buoyed by robust growth from its pulsed-field ablation technology, is expanding its sales presence around São Paulo to strengthen its position ahead of domestic challengers.

Structural heart remains the most contested battleground. Edwards faces head-to-head evaluations as Brazilian surgeons test Abbott’s Navitor and Boston Scientific’s Acurate platforms, intensifying price and outcomes comparisons medtechdive. Simultaneously, Medtronic plans to challenge Boston Scientific for leadership in implantable cardioverter-defibrillators by bundling cloud follow-up and heart failure diagnostics, citing favorable pilot data released in September 2024.

Rising digital-health adoption creates white-space opportunities for regional firms offering telemetry platforms compatible with imported hardware. Public-sector upgrades under PAEMP add volume for ultrasound probes and bedside monitors, allowing local assemblers to secure niche contracts saude. Foreign companies mitigate ANVISA delays by co-developing clinical trial sites inside academic hospitals, shortening data-collection cycles and fostering brand loyalty among key opinion leaders. Collectively, these strategic moves underscore a moderately concentrated cardiovascular devices market where innovation and distribution breadth decide future share.

Brazil Cardiovascular Devices Industry Leaders

Medtronic, Inc (Covidien Plc)

Boston Scientific Corporation

Abbott Laboratories

Cardinal Health Inc

Edwards Lifesciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Brazilian Society of Cardiology and Brazilian College of Radiology issued 2024 CT/MRI guidelines for cardiovascular diagnosis, setting new national standards.

- January 2025: The Brazilian Society of Cardiology and Brazilian College of Radiology issued 2024 CT/MRI guidelines for cardiovascular diagnosis, setting new national standards.

- September 2024: SBCCV launched a national training initiative to mitigate electrophysiologist shortages through tele-mentoring.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

The Brazil cardiovascular devices market, as framed by Mordor Intelligence, captures the yearly sales value of diagnostic, monitoring, therapeutic, and surgical heart-care equipment that reach hospitals, catheterization labs, ambulatory centers, and approved home-care channels across the country. Products span ECG systems, remote cardiac monitors, coronary stents, cardiac rhythm implants, heart valves, and ventricular assist devices. Mordor models the market at USD 304.36 million in 2025, advancing toward USD 370.94 million by 2030 at a 4.04 % CAGR, a pace closely aligned with procedure growth rather than price inflation.

Scope exclusion: Single-use disposables and contrast agents bundled within wider procedure kits fall outside the sizing.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Structural Heart Disease

- Hypertension

- Others

- By End-User

- Hospitals & Cardiac Centers

- Home-Care Settings

- Ambulatory Surgical Centers

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed interventional cardiologists, cath-lab managers, and distribution partners in São Paulo, Recife, Porto Alegre, and Manaus to validate penetration rates, replacement cycles, and ASP shifts. A short survey of supply-chain managers benchmarked inventory turns and lead-time volatility.

Desk Research

We began with tier-one public data such as ANVISA import license logs, SUS inpatient surgery records, IBGE health-spend dashboards, and Pan American Health Organization mortality tables, which ground prevalence, procedure mix, and device flow. Industry journals, investor presentations, and procurement gazettes then supplied price corridors and adoption timelines.

Paid resources, notably D&B Hoovers and Dow Jones Factiva, sharpened company revenue splits, while Questel patent searches on ablation catheters signaled technology diffusion. The sources cited are illustrative; numerous additional repositories informed the desk research stage.

Market-Sizing & Forecasting

A top-down rebuild aligns import value, domestic assembly output, and refurb flow, then cross-checks totals with sampled ASP × installed-base roll-ups at leading centers. Key inputs include angioplasty volumes, CRM implants per 100,000 inhabitants, private insurance enrollment, real effective exchange rate movements, and ANVISA approval lag. Multivariate regression combined with scenario analysis extends trends to 2030; exponential smoothing tests confirmed that an 8 % currency slide in 2022 does not distort long-term demand. Weighted averages bridge gaps in bottom-up rolls.

Data Validation & Update Cycle

We triangulate interim outputs against quarterly trade statistics and hospital billing trackers. Variances over 50 bps in CAGR prompt reruns reviewed by a second analyst. Reports refresh yearly, with interim updates triggered by material regulatory or reimbursement events.

Why Mordor's Brazil Cardiovascular Devices Baseline Commands Reliability

Published estimates often diverge because firms apply different scopes, price points, and refresh cadences. Some broaden totals with consumables or service contracts, while others straight-line past CAGRs without testing regulatory realities.

Key gap drivers include inclusion of disposables, use of global ASP multipliers without local currency adjustment, and forecasts that overlook ANVISA approval bottlenecks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 304.36 M (2025) | Mordor Intelligence | |

| USD 1.50 B (2024) | Regional Consultancy A | bundles consumables and cath-lab service fees |

| USD 2.03 B (2024) | Trade Journal B | treats retail mark-ups as market value and uses fixed FX rate |

| USD 1.43 B (2023) | Global Consultancy C | extrapolates Latin America averages lacking Brazil-specific approvals |

The comparison shows that Mordor's tighter device list, Brazil-specific pricing, and annual refresh deliver a balanced, transparent baseline traceable to public variables and repeatable steps.

Key Questions Answered in the Report

What is the size of Brazil’s cardiovascular devices market?

The Brazil cardiovascular devices market size is USD 316.50 Million in 2026.

Which device segment currently holds the largest share of Brazil’s cardiovascular devices market?

Diagnostic and monitoring products lead the market thanks to guideline-driven uptake of cardiac CT, MRI and connected ECG platforms.

Why are ambulatory surgery centers gaining traction for cardiovascular procedures in Brazil?

Payers favor the lower costs of outpatient sites, while policy momentum toward site-neutral reimbursement is shifting elective PCI and rhythm-device replacements to ASC settings.

How do ANVISA approval timelines affect cardiovascular device availability in Brazil?

Multi-step reviews and import authorizations can add months to market entry, delaying patient access to the newest valves, pacemakers and ablation catheters.

What role does digital health play in accelerating cardiovascular device adoption?

Mandates for remote follow-up and the spread of practice-management software have doubled monitoring activations, supporting broader use of connected implants and diagnostics.

How concentrated is the competitive landscape for cardiovascular devices in Brazil?

A handful of multinationals account for slightly more than 60% of sales, creating a moderately concentrated market where scale, distribution and innovation shape share.

Page last updated on: