Peripheral Vascular Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.5 Billion |

| Market Size (2031) | USD 17.80 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

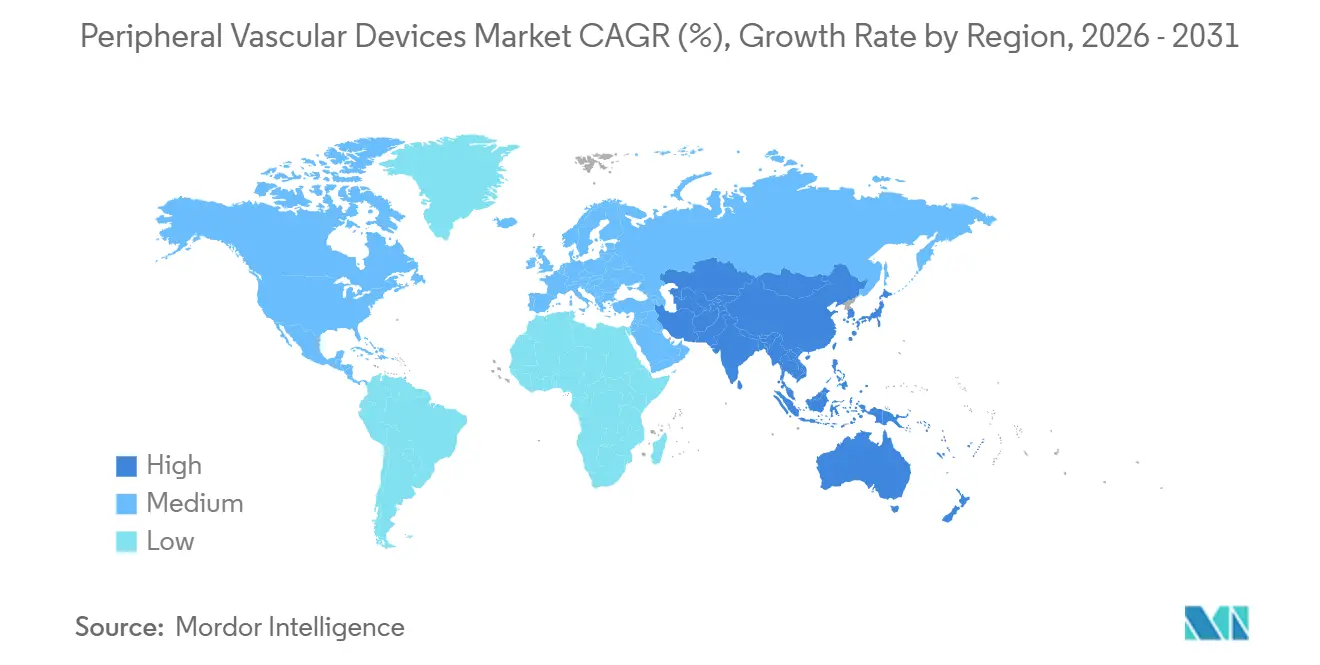

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

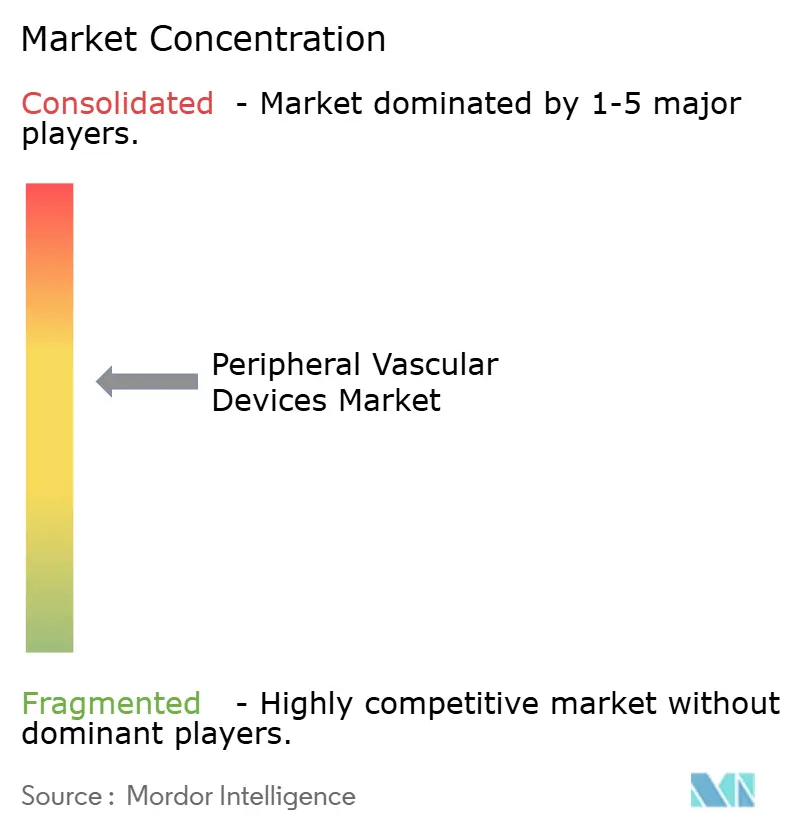

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Vascular Devices Market Analysis by Mordor Intelligence

The Peripheral Vascular Devices Market size is expected to increase from USD 13.92 billion in 2025 to USD 14.5 billion in 2026 and reach USD 17.80 billion by 2031, growing at a CAGR of 4.18% over 2026-2031.

Procedure volumes continue to climb, yet average device spend per case is leveling off as interventionalists migrate low-complexity work from inpatient suites to ambulatory surgical centers (ASCs) and office-based labs (OBLs). Angioplasty balloons retained the largest revenue slice in 2025, but atherectomy systems are closing the gap on the back of calcified-lesion prevalence and supportive reimbursement in Japan and Australia. Hospitals still dominate device procurement in value terms, though their share is slipping because CMS bundled-payment rules compel tighter formulary management and lower price ceilings. Geographic growth tilts to Asia-Pacific, where China’s Healthy China 2030 cardiovascular roadmap and India’s catheter-lab build-out are generating first-time demand for advanced balloons, stents, and thrombectomy platforms.

Key Report Takeaways

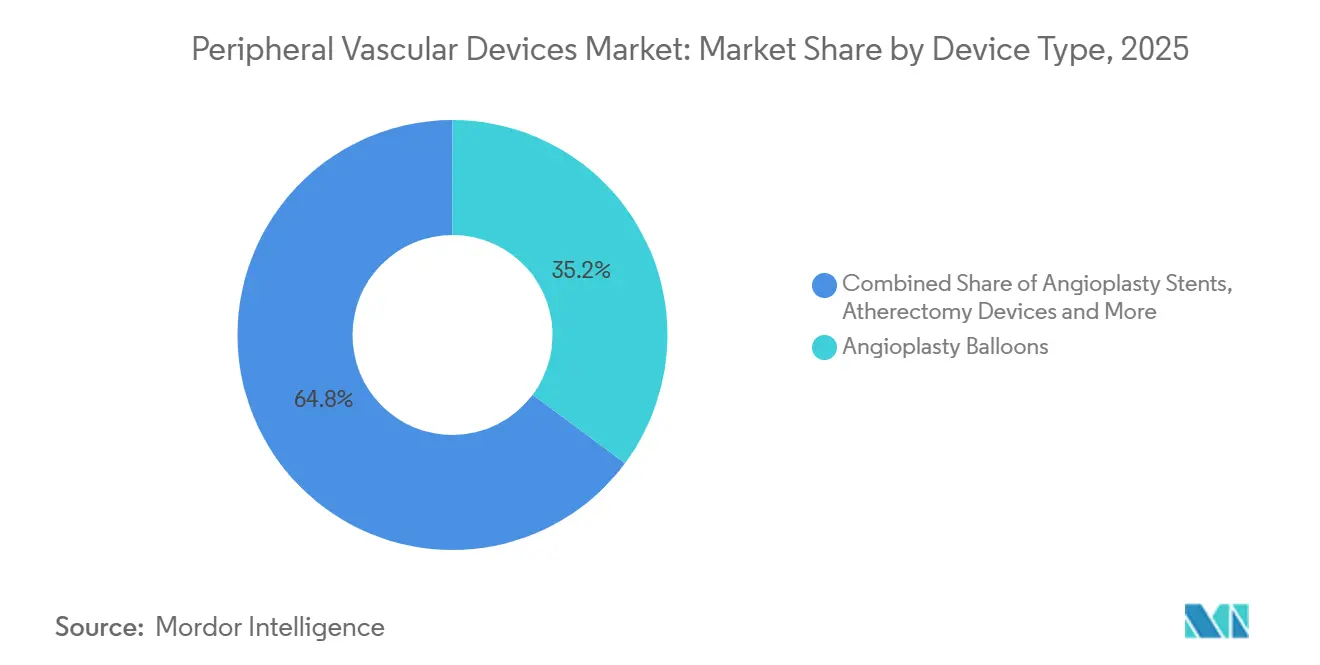

- By device type, angioplasty balloons led with 35.18% revenue in 2025, while atherectomy is forecast to advance at an 8.22% CAGR to 2031.

- By clinical application, peripheral arterial disease represented 45.21% of 2025 sales; deep-vein thrombosis procedures are projected to grow at a 5.65% CAGR through 2031.

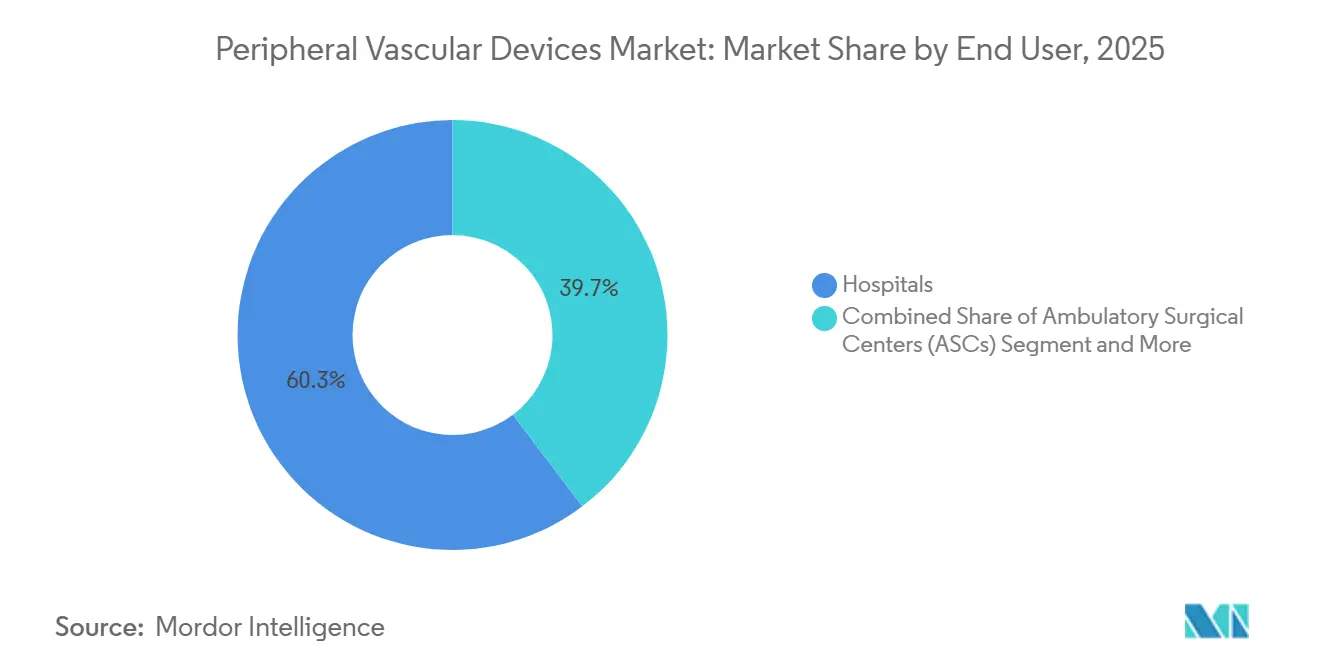

- By end user, hospitals accounted for 60.32% of turnover in 2025, yet ASCs record the fastest expansion at a 7.12% CAGR over 2026-2031.

- By geography, North America held 42.25% of 2025 revenue; Asia-Pacific is expected to post a 7.68% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peripheral Vascular Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in peripheral artery & venous disease prevalence | +1.2% | Global, with highest burden in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Shift toward minimally-invasive, catheter-based revascularization | +0.9% | North America & Europe lead; APAC adoption accelerating | Short term (≤ 2 years) |

| Rapid adoption of drug-coated balloon technology | +0.7% | North America & Western Europe; emerging in Latin America | Short term (≤ 2 years) |

| Growth of office-based labs (OBLs) in OECD nations | +0.5% | United States, Germany, Australia; limited in Japan due to regulatory barriers | Medium term (2-4 years) |

| Hospital-to-ASC site-of-care migration for PAD procedures | +0.4% | United States (CMS-driven); gradual adoption in Canada and select EU markets | Short term (≤ 2 years) |

| National screening programmes for critical-limb ischemia (CLI) | +0.3% | China (Healthy China 2030), India (PMSSSY), United Kingdom (NHS vascular checks) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Peripheral Artery & Venous Disease Prevalence

Medicare claims showed a 19% jump in lower-extremity revascularizations between 2019 and 2024, even while average length of stay fell 23%, underscoring the push for faster, device-intensive therapy. Deep-vein thrombosis incidence across OECD members increased 8% annually over 2020-2025, fueled by post-COVID sequelae and obesity. The American Heart Association positioned DVT as the third largest acute cardiovascular syndrome in its 2025 update, elevating it from a niche condition to a mainstream interventional focus.

Shift Toward Minimally-Invasive, Catheter-Based Revascularization

Open bypass volumes in the United States dropped 31% between 2015 and 2024, while percutaneous interventions rose 47%. Drug-eluting stents now deliver 78% 5-year patency in femoropopliteal disease, neutralizing the historic durability edge of surgery. Japan’s 2024 reimbursement decision on atherectomy prompted a 40% spike in procedure counts the next quarter.

Rapid Adoption of Drug-Coated Balloon Technology

Drug-coated balloons (DCBs) captured 29% of global angioplasty-balloon income in 2025. The COMPARE trial reported 83% 12-month patency with paclitaxel balloons versus 68% for uncoated options. Safety dialog continues: the FDA ordered 5-year surveillance studies and expanded mortality warnings in 2024, tempering U.S. growth but accelerating European interest in sirolimus-based alternatives.

Growth of Office-Based Labs in OECD Nations

OBLs handled 22% of U.S. peripheral interventions in 2025, translating to USD 2.1 billion in device sales at 35% lower facility cost relative to hospital outpatient departments. Germany and Australia widened OBL-eligible code lists in 2024-2025, propelling volume out of inpatient settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device reimbursement cuts in the US & select EU markets | -0.6% | United States (CMS bundled payments), Germany (DRG revisions), United Kingdom (NICE restrictions) | Short term (≤ 2 years) |

| Safety concerns over paclitaxel-eluting peripherals | -0.4% | Global, with heightened scrutiny in United States (FDA), European Union (EMA), and Japan (PMDA) | Medium term (2-4 years) |

| Supply-chain fragility for specialty polymers & nitinol | -0.3% | Global, with acute shortages in North America and Europe during 2024-2025 | Short term (≤ 2 years) |

| Short product life-cycles driving inventory obsolescence | -0.2% | Primarily affects North America and Western Europe; less pronounced in price-sensitive APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device Reimbursement Cuts in the US & Select EU Markets

The 2026 CMS bundled-payment ceiling of USD 18,500 per 90-day PAD episode forces hospitals to secure 15-25% device discounts. Germany trimmed lower-extremity DRG weights 8% in 2025; United Kingdom guidance now limits first-line DCB use to in-stent restenosis, curbing premium-technology uptake.

Safety Concerns Over Paclitaxel-Eluting Peripherals

FDA-mandated labeling revisions in 2024 follow a meta-analysis showing a 1.4% absolute mortality rise at five years. Japan’s PMDA paused new paclitaxel clearances pending local registry data, while EU regulators require annual imaging but have stopped short of withdrawal[1]FDA, “Update on Treatment of Peripheral Arterial Disease With Paclitaxel-Coated Balloons and Paclitaxel-Eluting Stents,” fda.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Atherectomy Drives Premium Shift

Atherectomy revenue is expected to post an 8.22% CAGR between 2026-2031, the highest among device classes. The peripheral vascular devices market share for angioplasty balloons was 35.18% in 2025, but aggressive price competition from Asian generics cut average selling prices 12% compared with 2022. The peripheral vascular devices market size for atherectomy systems is projected to reach a significant revenue by 2031, alongside the calcium-heavy lesion mix and supportive coding in Japan and Australia. Directional atherectomy plus DCB achieved 81% 18-month patency in calcified vessels per the DEFINITIVE LE data set. Hospitals, however, cap usage to imaging-confirmed severe calcification because a single catheter still costs USD 2,500-3,500.

Second-tier products illustrate polarization. Thrombectomy adoption surged after FDA clearance of aspiration systems for iliofemoral DVT in 2024. Self-expanding stents edge toward commoditization, with vendors pivoting to fracture-resistant alloys and thinner strut profiles. IVC filters have declined after updated ACCP guidelines against prophylactic use, whereas guidewires and sheaths anchor low-margin but indispensable recurring revenue streams.

By Clinical Application: DVT Gains as PAD Matures

Peripheral arterial disease retained 45.21% revenue in 2025; nonetheless, deep-vein thrombosis procedures are forecast to grow 5.65% annually through 2031. The peripheral vascular devices market size for DVT interventions is set to expand as catheter-directed thrombectomy earns a Class IIa recommendation in the 2024 CHEST guideline[2]CHEST, “Antithrombotic Therapy for VTE Disease Guideline 2024,” chestnet.org . Hospitals devote roughly 2.8 times more device spend treating Rutherford 5-6 critical-limb ischemia than claudication cases because multilevel lesions often require adjunct atherectomy and provisional stenting. Pelvic-venous-disorder work gains from dedicated stent launches, whereas acute limb ischemia volumes inch down under better systemic anticoagulation.

Cost-effectiveness remains under scrutiny. A 2025 JAMA Network Open analysis pegged catheter-directed thrombolysis at USD 12,000 per quality-adjusted life year above oral therapy, near payer thresholds. Vendors bankroll real-world registries to prove savings from avoided post-thrombotic syndrome, aiming to entrench the procedure.

By End User: ASCs Reshape Purchasing Dynamics

Hospitals controlled 60.32% of 2025 turnover, yet ambulatory surgical centers clock a 7.12% CAGR for 2026-2031—the fastest across settings. The peripheral vascular devices market share of hospitals will dip by 2031 as CMS and private payers enlarge ASC-covered code lists. Group-purchasing leverage lets ASCs pay 23% less than hospitals for comparable devices. Vendors answer with ASC-labeled SKUs that strip accessory kits and adopt consignment or per-case pricing. OBLs, a clinic subset, already capture 22% of U.S. peripheral procedures but face possible slowdowns where state boards propose tighter oversight.

Hospitals maintain dominance in complex, high-acuity cases requiring hybrid open and endovascular techniques as well as immediate surgical backup. That bifurcation steers routine femoropopliteal angioplasty to ASCs yet keeps multilevel critical-limb work inside tertiary centers.

Geography Analysis

North America provided 42.25% of 2025 revenue. The United States braces for tempered growth as payment caps and site-of-care migration drive negotiations that pull average device spend per case down to USD 1,800 in ASCs versus USD 2,400 in hospitals. Canada invested in cath-lab capacity, yet provincial wait times of 12 weeks restrain volume. Mexico’s private-hospital tier moves ahead with lithotripsy and limus balloons, contrasting with resource-limited public institutions.

Asia-Pacific is on track for a 7.68% CAGR. China’s peripheral vascular devices market benefits from domestic champions capturing significant market share through aggressive pricing. India’s Pradhan Mantri Swasthya Suraksha Yojana accelerates cath-lab installations beyond tier-1 metros, narrowing care disparities. Japan’s aging diabetogenic population fuels PAD prevalence, though device spend per case averages USD 1,600 amid shorter hospital stays. Australia’s 2025 OBL item numbers position it as a proving ground for next-wave sirolimus balloons.

Europe contributes sizeable absolute dollars, yet heterogenous reimbursement rules split adoption curves. Germany reimburses DCBs as first-line therapy, while the United Kingdom caps DCBs for restenosis. France green-lit orbital atherectomy in 2024. Eastern Europe, reliant on earlier-generation balloons, receives EU structural funds earmarked for cath-lab upgrades that will underpin gradual technology catch-up.

Competitive Landscape

Moderate consolidation characterizes the space: Medtronic, Boston Scientific, Abbott, BD (Bard), and Cook Medical together control a significant share of global sales. Integrated portfolios enable these players to lock multi-year supply agreements as hospitals pursue bundled discounts. Technology arms races persist—Medtronic’s IN.PACT Admiral holds U.S. DCB leadership through 5-year data, while Abbott’s Supera stent wins in flexion-heavy segments owing to kink resistance. Boston Scientific leveraged liquidity from its 2024 Axonics sale to launch Ranger DCB across Europe in 2025.

Mid-sized disruptors fill niches. Shockwave Medical rode intravascular lithotripsy to a USD 600 million segment inside four years, pressuring legacy atherectomy vendors. Chinese and Indian entrants—including MicroPort and Meril—pick off price-sensitive territories in Eastern Europe and Latin America with CE-marked generics running 40-50% beneath Western tags. Patent cliffs loom: core IN.PACT paclitaxel coat patents expire 2027-2028, inviting biosimilar influx unless incumbents transition clinics to limus formulations. International Medical Device Regulators Forum harmonization lowers filing barriers, further opening doors for lean, region-focused competitors.

Peripheral Vascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Becton, Dickinson and Company

Medtronic

Cook Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Johnson & Johnson launched the Shockwave Javelin Peripheral IVL Catheter across Europe.

- August 2025: Abbott secured CE Mark for the Esprit BTK bioresorbable scaffold system targeting below-the-knee disease in PAD patients.

Global Peripheral Vascular Devices Market Report Scope

As per the scope of the report, peripheral vascular devices are medical devices designed to diagnose, treat, or manage conditions related to the blood vessels outside the heart and brain (peripheral arteries and veins). These devices include tools such as catheters, stents, balloons, and other instruments used in procedures like angioplasty, stenting, or vascular access to improve blood flow or diagnose vascular conditions.

The segmentation of the peripheral vascular devices market is categorized by device type, clinical application, end user, and geography. By device type, the market includes angioplasty balloons, angioplasty stents, atherectomy devices, thrombectomy devices, embolic protection devices, inferior vena cava (IVC) filters, peripheral guidewires, and others. By clinical application, it is segmented into peripheral arterial disease (PAD), critical limb ischemia (CLI), deep vein thrombosis (DVT), and other clinical applications. By end user, the market is divided into hospitals, ambulatory surgical centers (ASCs), office-based labs (OBLs), and specialty vascular and cardiology clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Angioplasty Balloons |

| Angioplasty Stents |

| Atherectomy Devices |

| Thrombectomy Devices |

| Embolic Protection Devices |

| Inferior Vena Cava (IVC) Filters |

| Peripheral Guidewires |

| Others |

| Peripheral Arterial Disease (PAD) |

| Critical Limb Ischaemia (CLI) |

| Deep Vein Thrombosis (DVT) |

| Other Clinical Applications |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Office-Based Labs (OBLs) |

| Specialty Vascular & Cardiology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Angioplasty Balloons | |

| Angioplasty Stents | ||

| Atherectomy Devices | ||

| Thrombectomy Devices | ||

| Embolic Protection Devices | ||

| Inferior Vena Cava (IVC) Filters | ||

| Peripheral Guidewires | ||

| Others | ||

| By Clinical Application | Peripheral Arterial Disease (PAD) | |

| Critical Limb Ischaemia (CLI) | ||

| Deep Vein Thrombosis (DVT) | ||

| Other Clinical Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Office-Based Labs (OBLs) | ||

| Specialty Vascular & Cardiology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will peripheral revascularization spending become by 2031?

The peripheral vascular devices market is projected to reach USD 17.80 billion by 2031, expanding at a 4.18% CAGR from 2026.

Which device class is growing the fastest?

Atherectomy systems are forecast to post an 8.22% CAGR between 2026-2031 thanks to their value in calcium-heavy lesions.

Why are ambulatory surgical centers important to suppliers?

ASCs record 7.12% forecast CAGR and secure average device prices 23% below hospital levels, altering vendor pricing models.

How big is Asia-Pacific's contribution to global sales?

Asia-Pacific is set for a 7.68% CAGR and will account for an increasing share as China and India scale screening and cath-lab access.

What is driving the shift away from open surgical bypass?

Five-year patency evidence for drug-eluting stents and payer pressure to cut USD 35,000 bypass costs favor catheter-based alternatives.

Page last updated on: