Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Cardiovascular Devices Market Analysis by Mordor Intelligence

The Spain cardiovascular devices market size was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 2.09 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031). This growth reflects the government’s effort to modernize public hospital equipment while maintaining overall budget discipline. Therapeutic and surgical devices command the largest Spain cardiovascular devices market share, whereas diagnostic and monitoring technologies are advancing faster as hospitals look to detect disease earlier and shorten inpatient stays. Manufacturers that bundle interventional hardware with digital monitoring services already benefit from broader recurring revenue streams. Meanwhile, accelerated investment by private cardiology networks lifts total demand and raises expectations for premium functionality, forcing suppliers to balance standardized offerings for public institutions with high-end solutions for private centers.

Key Report Takeaways

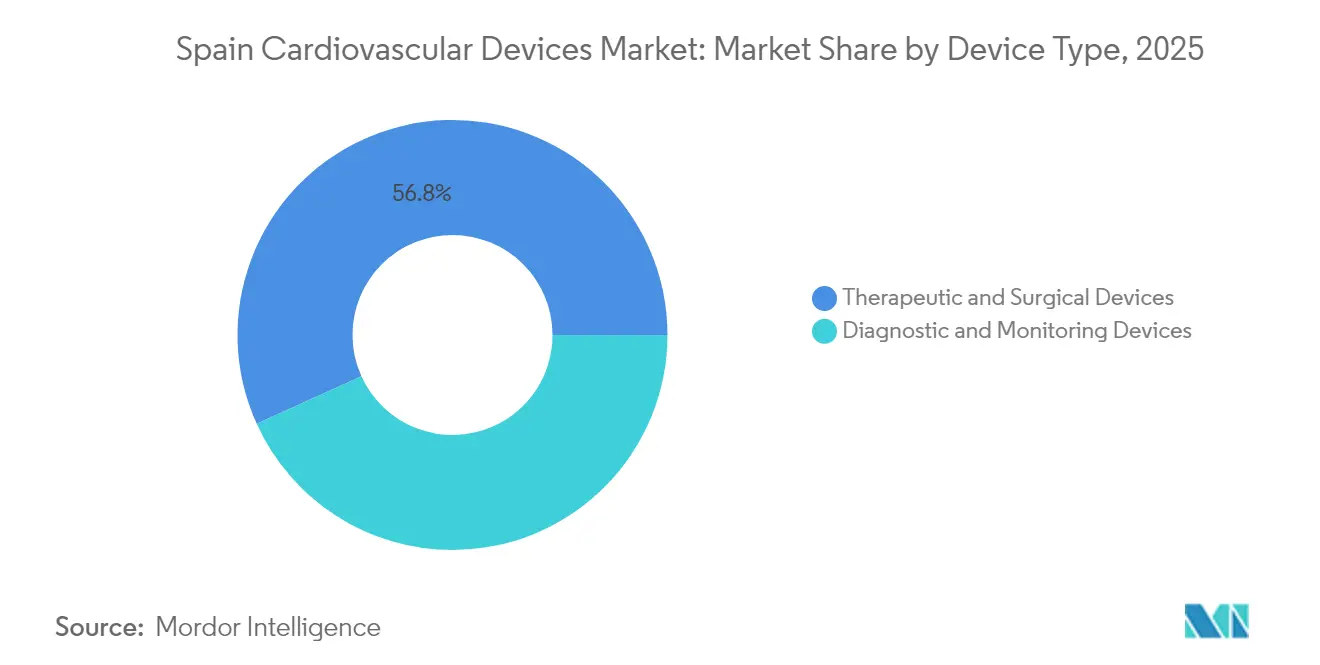

By device type, therapeutic and surgical products led with 57.20% of Spain cardiovascular devices market share in 2024; diagnostic and monitoring equipment is forecast to expand at a 6.03% CAGR to 2030.

By indication, coronary artery disease accounted for 55.21% of the Spain cardiovascular devices market size in 2024, while valvular heart disease is set to grow at a 6.84% CAGR through 2030.

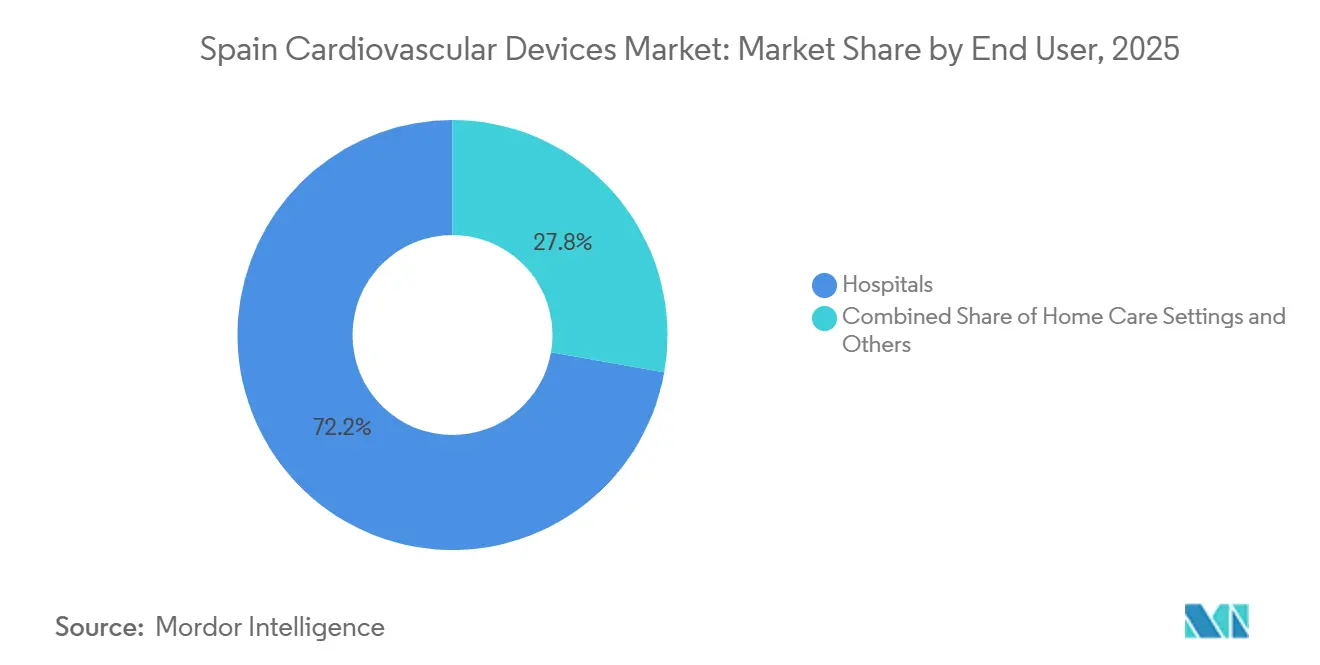

By end user, hospitals controlled 68.20% of revenue in 2024; home-care settings are projected to post the fastest growth at a 7.11% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cardiovascular Health Plan 2022-2029 | +1.8% | Nationwide, early lift in underserved regions | Medium term (2-4 years) |

| Rapidly ageing population | +1.5% | All regions, peak use along Mediterranean coast and northern provinces | Long term (≥4 years) |

| Reimbursement expansion for TAVR & TMVR | +1.2% | Madrid, Barcelona, Valencia first | Short term (≤2 years) |

| Private cardiology network growth | +0.9% | Large urban centers | Medium term (2-4 years) |

| Digital tele-monitoring funding | +0.8% | Catalonia, Basque Country first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Cardiovascular Health Plan 2022-2029 Catalyzing Public Procurement

The plan allocates EUR 215 million for cardiovascular equipment modernization, accelerating replacement of aging imaging systems and catheterization labs. Standardized multi-year service contracts shorten bid cycles and guarantee training, which spurs volume-led growth for basic diagnostic platforms and value-driven demand for advanced technologies. Hospitals in underserved regions gain faster access to updated cardiac ultrasound, while flagship centers adopt fully integrated cath-lab suites. Suppliers with tiered portfolios capture share by meeting both ends of the performance spectrum.

Rapidly Ageing Population Expanding Device Demand

Citizens older than 65 generate a disproportionate share of cardiac procedures, and their clustering along the Mediterranean coastline creates utilization hotspots. Octogenarians are now the fastest-growing group for transcatheter valve replacement, prompting hospitals to revise scheduling and after-care protocols. Manufacturers have answered with smaller implants and longer battery life, which reduce rehospitalization risk. Hospitals that embrace geriatric-friendly technology often see utilization efficiencies that exceed regional averages.

Reimbursement of TAVR & TMVR Accelerating Structural Heart Uptake

Expanded criteria in 2024 doubled the number of eligible intermediate-risk patients for transcatheter aortic valve replacement and broadened mitral repair reimbursement. Procedure volumes jumped 47% year-on-year, enabling hospitals to negotiate price concessions nearing 12%. Although unit prices fell, revenue rose on higher throughput. Vendors that bundle training and analytics within the device price protect margins despite headline discounts.

Expansion of Private Cardiology Networks Driving Premium Equipment

Private cardiology groups have grown by 23% since 2024 and update equipment about 40% faster than public institutions. These centers focus on electrophysiology and 4D imaging, demanding advanced mapping systems, hybrid operating rooms, and AI-enhanced scanners. Outcome-based insurer contracts compel vendors to document clinical benefit, allowing emerging technologies to establish footholds in the private sector before migrating into public procurement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regional tender price caps | –1.2% | Most acute in Andalusia, Valencia, Galicia | Short term (≤2 years) |

| MDR recertification backlog | –0.9% | Nationwide | Short term (≤2 years) |

| Shortage of interventional cardiologists | –0.8% | Outside Madrid and Catalonia | Medium term (2-4 years) |

| 120-day hospital payment cycles | –0.4% | Andalusia and Extremadura | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Regional Tender Price Caps Compress Selling Prices

Autonomous communities such as Andalusia and Valencia enforce reference pricing 15-20% below direct-negotiation levels. The model prioritizes total cost of ownership, encouraging bids that bundle disposables, maintenance, and training. Mid-tier suppliers leave low-margin categories, consolidating share among firms that leverage scale. Hospitals could face fewer options in commodity segments if the current rules persist.

MDR Recertification Backlog Delaying Product Launches

Class III cardiovascular devices confront average recertification delays of 14 months under the European Medical Device Regulation, limiting the arrival of next-generation products. Larger companies with robust regulatory teams maintain an advantage, while smaller innovators postpone market entry. Hospitals extend service contracts on legacy systems, raising maintenance costs and creating pent-up demand that will surface once the backlog eases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Momentum Beside Therapeutic Scale

Therapeutic and surgical devices held 56.78% of Spain cardiovascular devices market share in 2025, buoyed by coronary stents and cardiac rhythm-management implants. Concurrently, the Spain cardiovascular devices market size for diagnostic and monitoring equipment is expected to grow at 5.86% CAGR through 2031 thanks to AI-guided imaging and national funding for early detection. Advanced transcatheter tools also shorten the life cycle of older surgical devices, shifting procurement toward minimally invasive systems that shorten hospital stays. Vendors that can package modular software licenses with core hardware capture incremental revenue without proportionally higher production costs.

Diagnostic adoption is no longer confined to academic centers. Fractional flow-reserve platforms and 3D echocardiography are penetrating regional hospitals, encouraged by standardized procurement guidelines under the National Cardiovascular Health Plan. At the same time, the therapeutic segment is intensifying its focus on structural heart interventions as payers recognize the cost benefits of shorter recovery times. Hospitals that achieve lower length-of-stay metrics through device innovation often qualify for performance-based financing, bolstering demand for the latest implants.

By Indication: Coronary Dominance With Valvular Acceleration

The Spain cardiovascular devices market size allocated to coronary artery disease reached 54.83% in 2025, reflecting mature infrastructure and clinician expertise. Drug-eluting stent iterations and imaging-guided angioplasty deliver steady incremental value. Suppliers mitigate price pressure by bundling low-margin consumables with proprietary analytics. Valvular heart disease, while smaller, is positioned for a 6.63% CAGR during 2026-2031 following expanded TAVR and TMVR reimbursement. Hospitals that field dedicated heart teams already capture rising referral volumes, indicating that procedural capacity can determine future share more than device availability.

Heart-failure management and electrophysiology are gaining visibility. Implantable hemodynamic monitors furnish real-time data that prevent decompensation events, trimming readmissions. Catheter ablation volumes grew 18% in 2024, demonstrating that arrhythmia therapy is spreading beyond tertiary centers. Vendors integrating mapping systems with ablation hardware provide single-source solutions that many hospitals view as operationally advantageous.

By End User: Hospitals Lead while Outpatient Surge

Hospitals accounted for an estimated 72.23% of cardiovascular device sales in 2025. Large tertiary and university hospitals are leading the way, handling the bulk of interventional cardiology and electrophysiology procedures. These institutions serve as pivotal regional hubs, managing complex procedures such as PCI and structural heart interventions, and evaluating next-gen devices. Revenue prospects have brightened, thanks to the stabilization of GRD (Diagnosis-Related Group) tariffs by the National Health System (SNS). Additionally, capital infusions from the INVEAT public investment initiative are modernizing cath labs, imaging tools, and hybrid operating rooms. This shift promotes timely equipment upgrades over sporadic replacements.

The "Other" segment is witnessing the fastest growth, with a ~6.1% CAGR. This surge is largely attributed to a shift towards outpatient, digitally driven cardiac care. Ambulatory surgical centers are stepping up to conduct low-risk diagnostic and interventional procedures. Meanwhile, regional telecardiology initiatives are facilitating remote ECG monitoring and post-PCI follow-ups at home. While Spain may lag behind some European counterparts in officially reimbursing digital therapeutics, there's a notable rise in the adoption of remote patient monitoring. This trend, supported by autonomous community health budgets, is broadening the use of cardiovascular devices beyond just hospitals and bolstering the popularity of wearables and connected devices.

Geography Analysis

Madrid and Catalonia accounted for close to one-third of Spain cardiovascular devices market size in 2025, supported by dense networks of tertiary hospitals and vibrant clinical research programs. Capital budgets in these regions favor AI-enabled imaging and advanced electrophysiology, cementing their status as early adopters. Valencia and Andalusia, constrained by stringent price caps, often defer premium purchases or rely on multi-year leasing to introduce new technologies.

Northern provinces such as Galicia and Asturias demonstrate rising need for cardiac rhythm-management implants as their ageing populations exceed the national mean. Grants from the National Cardiovascular Health Plan financed the first catheterization labs in several of these areas, cutting patient travel times and boosting local procedure volumes. Vendors that situate service hubs near these new centers can lock in early loyalty.

Along the Mediterranean coast, seasonal tourism spikes stretch interventional capacity. Hospitals in Murcia and Alicante deploy modular cath-lab layouts and portable imaging to manage fluctuating demand. Evening TAVR sessions free daytime capacity for emergent cases, pointing to ongoing demand for consumables even during periods traditionally considered low-utilization. Suppliers capable of rapid restocking gain an advantage in these time-sensitive settings.

Competitive Landscape

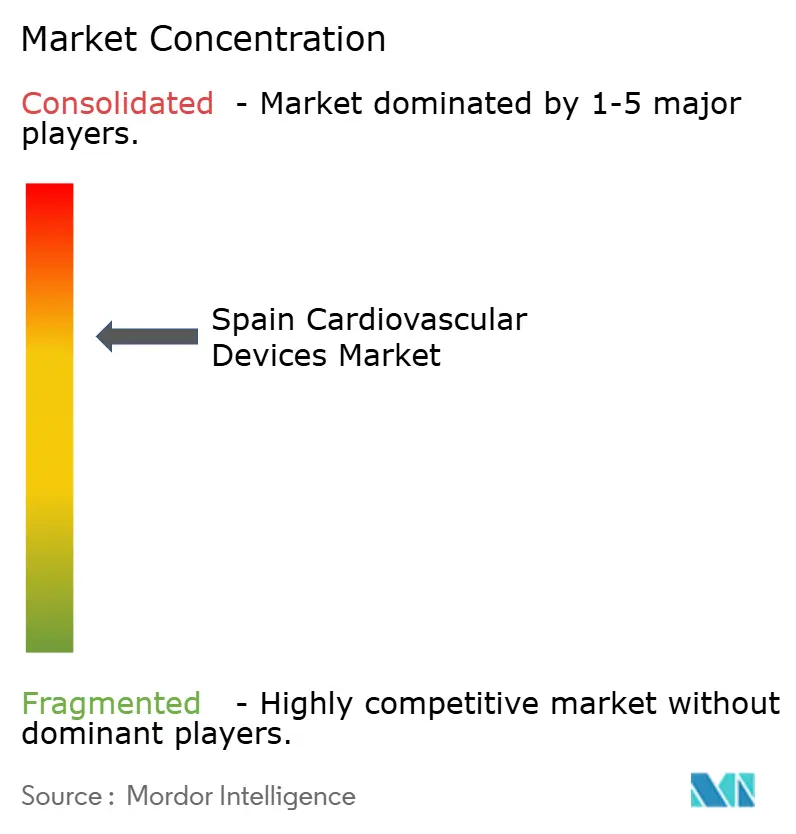

The five largest manufacturers secured more than 50% of the Spain cardiovascular devices market share in 2024, resulting in moderate market concentration. Broad-line suppliers leverage integrated portfolios to win system-wide contracts that bundle implants, imaging, analytics, and maintenance. Niche innovators succeed by excelling in specialized segments, such as drug-coated balloons or implantable loop recorders, often collaborating with academic hospitals to generate evidence of superior outcomes.

Strategic alliances with leading cardiac centers accelerate device refinement. Early access trials allow hospitals to shape iterative design, while vendors collect real-world performance data for regulatory filings. These collaborations underscore that future share battles may hinge more on clinical proof than on headline pricing alone.

Digital integration represents the new competitive frontier. Manufacturers that combine hardware with cloud-based decision support embed themselves deeply within hospital IT architecture. Patent activity in predictive analytics surged during 2024, indicating a race to control the data layer of cardiovascular care. Platforms offering open APIs could outpace closed ecosystems as health networks increasingly prioritize interoperability.

Spain Cardiovascular Devices Industry Leaders

Boston Scientific Corporation

Cardinal Health

Siemens Healthineers

Medtronic

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spanish cardiology societies issued gender-specific cardiovascular guidelines, prompting hospitals to adjust imaging protocols for women

- March 2025: Philips rolled out its ePatch wearable ECG and AI analytics to 14 Spanish hospitals, enabling 14-day continuous monitoring

Spain Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular devices are used to diagnose, monitor, and treat heart disease and related health problems. A cardiac device keeps the heart beating with a normal rhythm.

The Spain Cardiovascular Devices Market is segmented by Device Type (Diagnostic & Monitoring Devices (Electrocardiogram (ECG), Remote Cardiac Monitoring, and Other Diagnostic and Monitoring Devices) and Therapeutic & Surgical devices (Cardiac Assist Devices, Cardiac Rhythm Management Devices, Catheter, Stents and Grafts, Heart Valves, and Other Therapeutic and Surgical Devices)). The report offers value (in USD million) for the above segments.

By Device

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Indication

| Coronary Artery Disease |

| Arrhythmia |

| Heart Failure |

| Valvular Heart Disease |

By End User

| Hospitals |

| Home Care Settings |

| Others |

| By Device | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Indication | Coronary Artery Disease | ||

| Arrhythmia | |||

| Heart Failure | |||

| Valvular Heart Disease | |||

| By End User | Hospitals | ||

| Home Care Settings | |||

| Others | |||

Key Questions Answered in the Report

What is the current Spain cardiovascular devices market size?

The market is valued at USD 1.63 billion in 2026 and is projected to reach USD 2.09 billion by 2031.

Which segment holds the largest Spain cardiovascular devices market share?

Therapeutic and surgical devices lead with 56.78 % of 2025 revenue, driven by coronary stents and cardiac-rhythm implants.

How fast is the home-care end-user segment growing?

Home-care cardiovascular devices are forecast to expand at a 6.98 % CAGR between 2026-2031, the fastest among all end-user settings.

Why are structural-heart devices gaining momentum in Spain?

Expanded 2024 reimbursement for TAVR and TMVR doubled the eligible patient pool and boosted procedure volumes by 47 %, accelerating demand for transcatheter valve technologies.

Page last updated on: