Peripheral Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

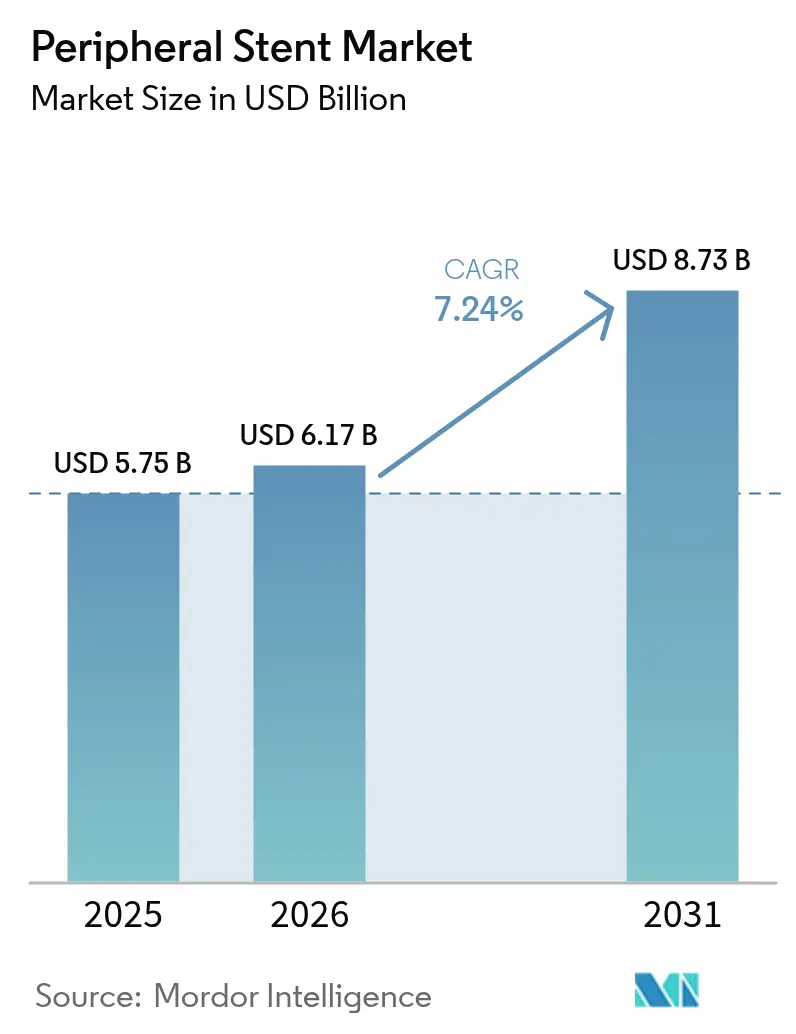

| Market Size (2026) | USD 6.17 Billion |

| Market Size (2031) | USD 8.73 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

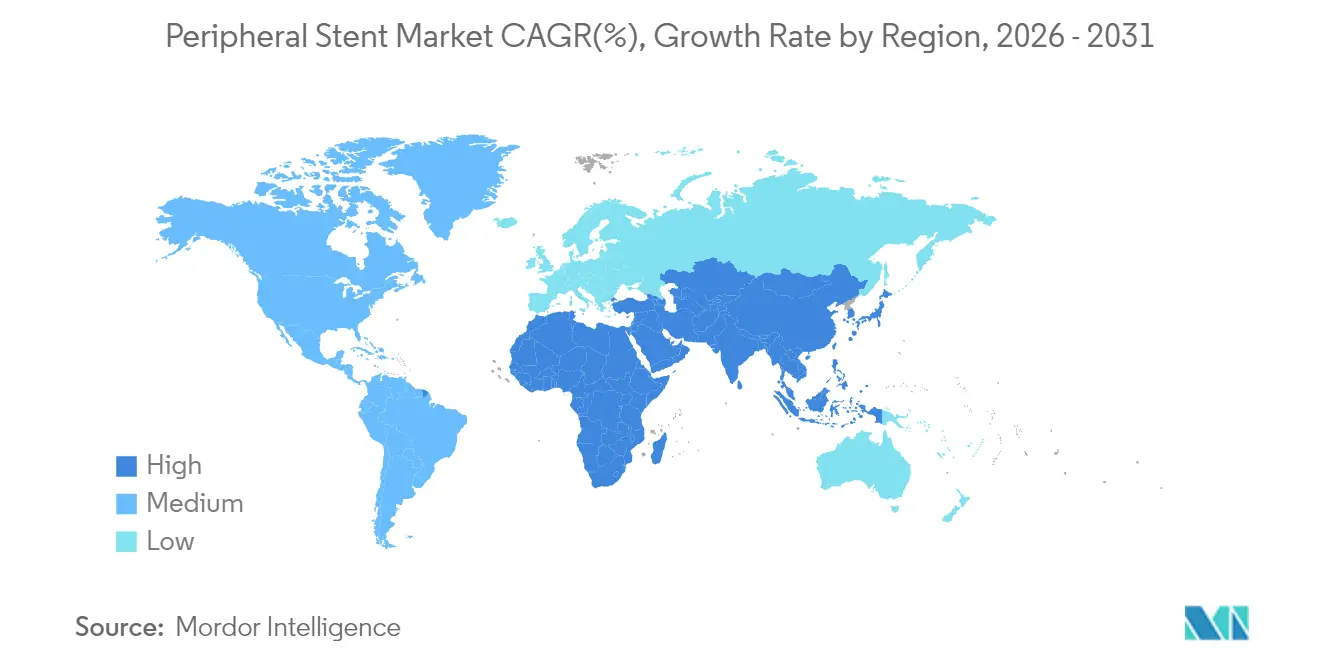

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Stent Market Analysis by Mordor Intelligence

The peripheral stents market size was valued at USD 5.75 billion in 2025 and estimated to grow from USD 6.17 billion in 2026 to reach USD 8.73 billion by 2031, at a CAGR of 7.24% during the forecast period (2026-2031). The upward curve stems from rising peripheral artery disease (PAD) prevalence, rapid product innovation, and greater reliance on minimally invasive treatments that shorten recovery times. Growing life expectancy, steady procedure volume growth, and the expanding footprint of ambulatory surgical centers (ASCs) keep demand steady. The peripheral stents market is also benefiting from breakthrough approvals of drug-eluting and bio-resorbable scaffolds, which broaden therapeutic options and improve long-term patency.[1]Abbott, “Abbott's Breakthrough Dissolving Stent Receives FDA Approval for Arteries Below the Knee,” Abbott Newsroom, abbott.mediaroom.com Consolidation among leading device makers adds competitive energy as companies scale portfolios and enter new clinical niches.

Key Report Takeaways

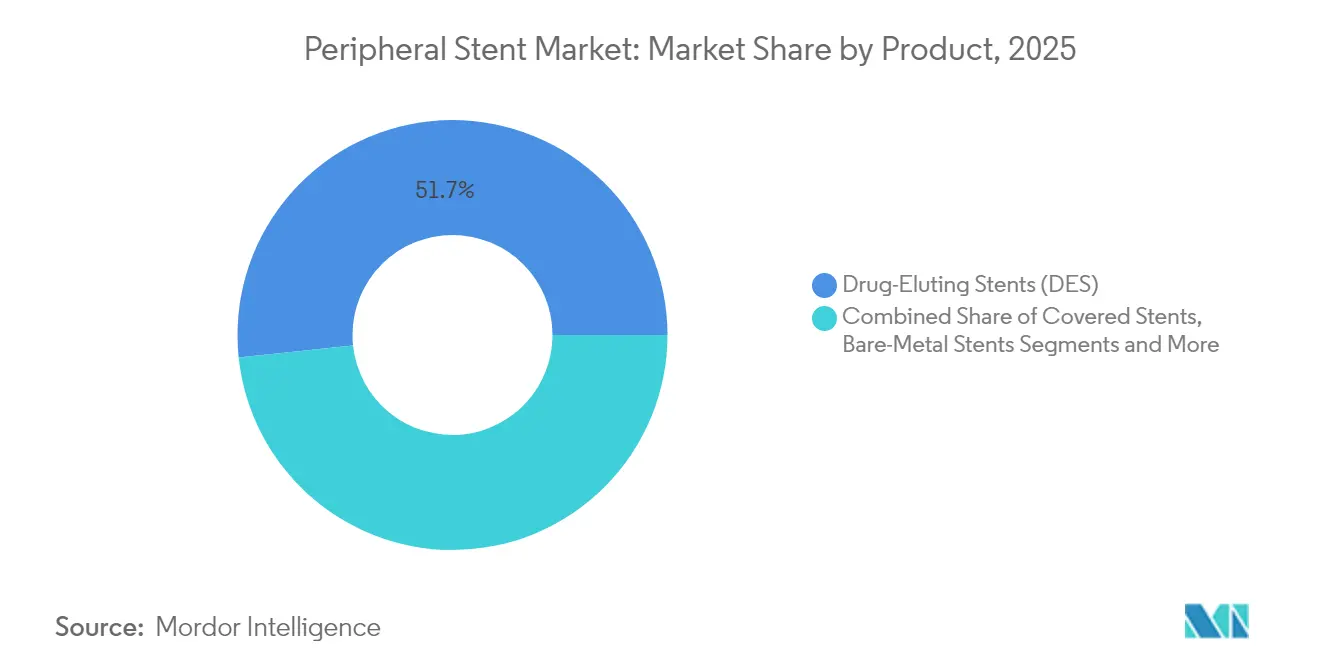

- By product, drug-eluting stents led with 51.66% revenue in 2025, while bio-resorbable scaffolds are projected to grow at 10.05% CAGR through 2031.

- By artery type, femoral-popliteal devices held 35.88% of the peripheral stents market share in 2025; infrapopliteal solutions are poised for a 9.32% CAGR to 2031.

- By material, nitinol accounted for 64.02% of segment revenue in 2025, whereas polymer/composite variants will expand at 8.12% CAGR.

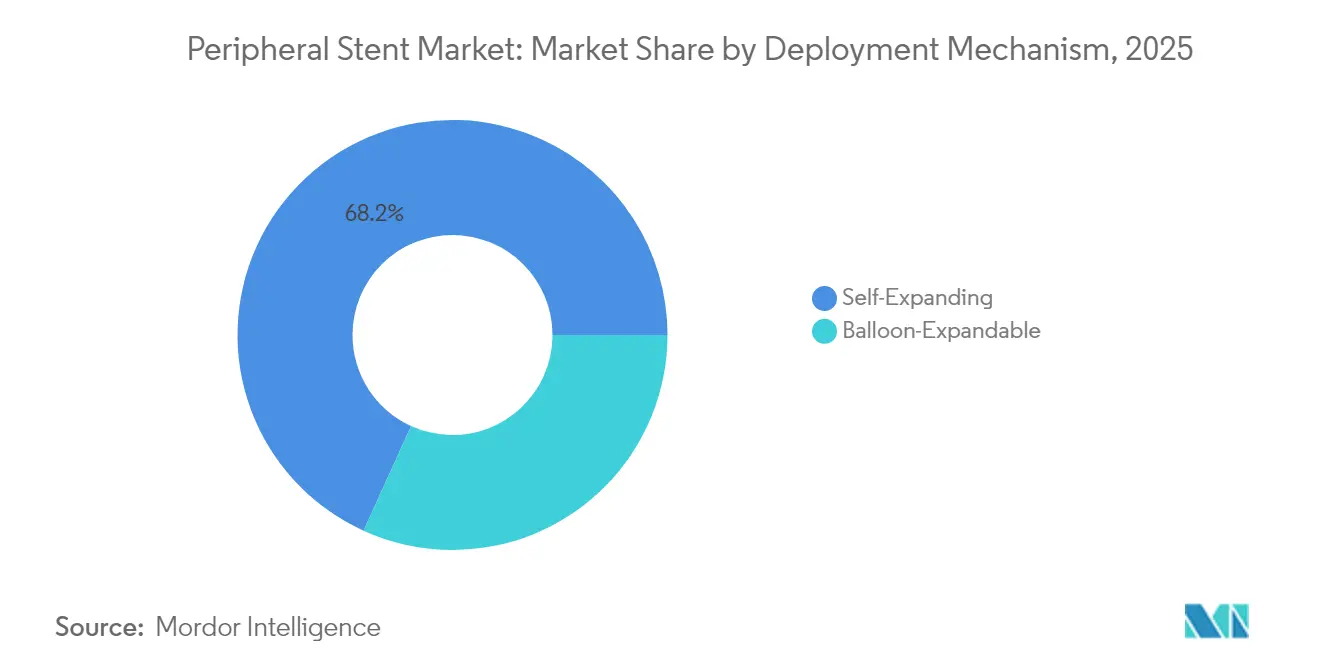

- By deployment, self-expanding systems commanded 68.21% of the peripheral stents market size for deployment mechanisms in 2025; balloon-expandable designs are rising at 7.86% CAGR.

- By end user, hospitals controlled 64.85% of the peripheral stents market size in 2025, but ASCs are expected to register 8.54% CAGR as case mix shifts outpatient.

- Regionally, North America retained 38.55% of 2025 revenue, while Asia-Pacific is forecast to outpace all regions at 8.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peripheral Stent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of PAD and aging population | +1.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Rapid adoption of drug-eluting and bio-resorbable platforms | +1.5% | Global, led by North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift to minimally invasive day-care procedures | +1.2% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| AI-guided image-based sizing and placement | +0.9% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Development of specialty stents and tech advances | +1.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Hospital value-based purchasing accelerates upgrades | +0.8% | Primarily North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of PAD and Aging Population

PAD procedure volumes climbed from 933 in 2023 to 1,422 in 2024 across major systems, underscoring a widening patient pool. Prevalence touches 20% among people over 70, creating a durable base for intervention. Smoking and hypertension remain core risk factors, together accounting for nearly 70% of disease burden. Developed regions show the highest prevalence, but emerging markets such as South Korea recorded incidence growth from 2.68 to 3.09 per 1,000 persons between 2023 and 2024 as diagnostic reach improves. These demographic realities assure sustained demand for interventions and keep the peripheral stents market moving upward.

Rapid Adoption of Drug-Eluting & Bio-Resorbable Platforms

Drug-eluting devices already hold majority share, while bio-resorbable scaffolds log double-digit growth as new evidence accumulates. FDA clearance of Abbott’s Esprit BTK system in 2024 delivered the first below-the-knee dissolving stent in the United States and reduced restenosis 25.8% versus balloon angioplasty. Registry data for magnesium scaffolds showed 4.3% target lesion failure at 12 months, fuelling clinical confidence. The shift supports the broader “leave nothing behind” strategy, pushing the peripheral stents market toward next-generation solutions.[2]EuroIntervention, “Safety and performance of a resorbable magnesium scaffold under real-world conditions: 12-month outcomes of the first 400 patients enrolled in the BIOSOLVE-IV registry,” eurointervention.pcronline.com

Shift to Minimally-Invasive Day-Care Procedures

ASC revenues are projected to reach USD 59 billion by 2028 as vascular cases exit inpatient settings. Same-day discharge and lower infection risk appeal to patients, while payers reward cost efficiency. Radial-to-peripheral access kits and streamlined stent delivery systems enable shorter case times, aligning with value-based purchasing. These efficiencies incentivize providers to select platforms that quicken turnover, adding momentum to the peripheral stents market.

AI-Guided Image-Based Sizing & Placement Optimisation

AI tools now deliver vessel measurements that mirror ultrasound accuracy while trimming procedure time. Trials such as FLAVOUR II confirmed comparable safety with fewer catheter exchanges, and deep-learning plaque analytics accelerate pre-procedure planning. Predictive sizing increases patency and limits reintervention, improving long-term economics of stent therapy. As hospitals adopt these systems, device makers offering AI-ready stents gain a competitive edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy regulatory pathways for novel materials | -0.7% | Global, most restrictive in North America and Europe | Long term (≥ 4 years) |

| Price erosion from group purchasing organisations | -0.9% | Primarily North America | Medium term (2-4 years) |

| Long-term data gaps on bio-absorbable scaffold safety | -0.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Reimbursement disparities across emerging markets | -0.6% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Regulatory Pathways for Novel Materials

The FDA’s Quality Management System Regulation overhaul effective February 2026 adds process layers for magnesium and polymer platforms, prolonging time-to-market. De Novo submissions face demanding evidence rules that favor incumbents familiar with compliance. These hurdles can slow innovation diffusion and dampen growth in the peripheral stents market FDA.[3]Center for Devices and Radiological Health, “Quality Management System Regulation: Final Rule Amending the Quality System Regulation – Frequently Asked Questions,” FDA, fda.gov

Price Erosion From Group Purchasing Organisations

GPOs steer more than USD 300 billion in annual purchasing, pressing device prices while collecting supplier fees. Novel stents struggle to secure premium reimbursement, and cost-focused tenders pressure margins despite clinical advantages. Developers must balance R&D spending with aggressive price points, a dynamic that can hinder adoption rates in the peripheral stents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bio-Resorbable Platforms Drive Innovation Despite DES Dominance

Drug-eluting stents retained 51.66% of 2025 revenue and are forecast to advance steadily as clinical familiarity persists. The peripheral stents market size for drug-eluting platforms is projected to rise in line with the overall 7.24% CAGR, supported by ongoing design refinements that boost patency. Bio-resorbable scaffolds, while only a fraction of sales today, are tracking 10.05% CAGR, the fastest within the product mix, thanks to FDA endorsements that validate safety and efficacy. Covered and bare-metal devices meet niche needs but face share migration toward higher-performing alternatives.

Physicians cite the Eluvia system’s one-year patency record and the Esprit BTK scaffold’s dissolving profile as evidence that new chemistry and coatings can outperform legacy metal frames. Growing clinical confidence, combined with reimbursement alignment for innovative therapies, fuels capital budgets aimed at next-generation products. As data matures, the peripheral stents market is likely to rebalance toward platforms that combine proven drug delivery with resorption to minimize long-term complications.

By Artery Type: Infrapopliteal Segment Gains Momentum as BTK Treatments Advance

Femoral-popliteal interventions generated 35.88% of 2025 revenue, underscoring their central role in PAD management. That dominance rests on a large installed base of equipment and clinical protocols perfected over decades. Yet infrapopliteal procedures are tipped for 9.32% CAGR, eclipsing all other artery categories. The introduction of purpose-built below-the-knee scaffolds, improved imaging, and rising chronic limb-threatening ischemia awareness underpin that growth. Iliac, renal, and carotid segments maintain steady demand, but incremental gains remain modest relative to infrapopliteal momentum.

Infrapopliteal devices benefit from unmet clinical need, as earlier interventions extend limb salvage and improve quality of life. Successful early outcomes from dissolving platforms are expected to widen physician adoption. That shift will expand the peripheral stents market share devoted to distal limb revascularization, especially as clinical guidelines endorse earlier BTK treatment.

By Material: Polymer Innovation Challenges Nitinol Supremacy

Nitinol accounted for 64.02% of 2025 revenue, reflecting its unmatched shape-memory properties that support self-expanding behavior. Supply chain strain and fabrication costs, however, are prompting exploration of alternative materials. Polymer and composite scaffolds are growing 8.12% annually, and cobalt-chromium maintains a foothold in balloon-expandable use cases. Stainless steel remains relevant largely in cost-sensitive markets or specific clinical scenarios.

Bio-resorbable polymers such as PLLA and magnesium composites demonstrate high degradation predictability and respectable radial strength. Registries indicate near-complete absorption by two years, a feature valued by clinicians looking to avoid late-stage complications. The peripheral stents market size allocated to polymer solutions is expected to increase as safety data and volume manufacturing lower per-unit costs.

By Deployment Mechanism: Self-Expanding Systems Leverage Nitinol Advantages

Self-expanding devices held 68.21% of revenue in 2025, leveraging nitinol’s elasticity to accommodate vessel motion and chronic outward force. These attributes limit restenosis and fracture risk in tapered or mobile arteries, translating into lower retreatment rates. Balloon-expandable systems, growing at 7.86% CAGR, gain share in calcified or ostial lesions requiring precise placement and immediate high radial force.

Recent delivery-system improvements streamline balloon-expandable deployment, making them more competitive in complex anatomies. Continual refinements in catheter profiles and fluoroscopic markers will sustain unit growth. Still, long-term dominance of self-expanding platforms appears secure, anchoring a large portion of the peripheral stents market.

By End User: ASC Growth Reshapes Procedural Economics

Hospitals retained 64.85% of global revenue in 2025 as tertiary centers handled the highest-acuity cases and maintained extensive imaging suites. Nonetheless, ASCs, projected for 8.54% CAGR, are gradually absorbing routine and mid-complexity procedures. Same-day discharge, lower overhead, and favorable patient satisfaction scores bolster the ASC value proposition.

Device developers now design packaging and inventory models tailored to outpatient environments. Integrated kits reduce setup time, and single-use delivery systems minimize reprocessing steps. As reimbursement incentives align with site-neutral payment agendas, ASCs are likely to account for a bigger slice of the peripheral stents market.

Geography Analysis

North America generated 38.55% of 2025 revenue, with the United States representing the largest single market due to well-funded health systems, routine screening, and broad reimbursement for endovascular care. Canada and Mexico contribute incrementally as access widens, though reimbursement and regulatory nuances shape product mix. Successful large-scale adoption of drug-eluting and bio-resorbable solutions solidifies regional leadership.

Europe follows closely, propelled by harmonized clinical guidelines and a single-market regulatory environment that speeds cross-border adoption. The European Society for Vascular Surgery emphasizes individualized care and endorses drug-eluting systems, supporting the peripheral stents market across member states. Western European countries benefit from established value-based care frameworks, and Central & Eastern Europe show emerging growth as infrastructure modernizes.

Asia-Pacific is the fastest climber, advancing at a 8.90% CAGR through 2031. China’s target-lesion failure dropped from 6.8% to 4.3% between 2023 and 2024 as advanced stents penetrated tier-one cities. India, aided by updated Medical Device Rules, recorded peripheral interventions rising from 2,850 in 2023 to 3,420 in 2024. South Korea and Japan remain technology-forward, quickly incorporating AI imaging and next-generation materials. Improved payor coverage and government focus on cardiovascular disease drive capacity expansion, lifting the peripheral stents market.

Latin America and the Middle East & Africa present untapped opportunity. Reimbursement variability and budget constraints slow uptake, but epidemiological transition and public-health campaigns create long-term upside. Pilot projects with cost-sharing models may establish proof-points that unlock broader adoption. As training partnerships and mobile cath-labs proliferate, regional stakeholders anticipate gradual but steady contribution to global volumes.

Competitive Landscape

The market shows moderate concentration. Abbott, Boston Scientific, and Medtronic anchor the top tier with extensive portfolios and global distribution. Abbott differentiates through interwoven nitinol architecture that yields zero fracture rates in studies, whereas Boston Scientific leverages polymer-coated drug delivery for class-leading patency.

Acquisition activity intensifies rivalry. Teleflex moved to acquire BIOTRONIK’s vascular unit for €760 million in February 2025, broadening its reach in drug-coated balloons and expanding into the peripheral intervention market. Stryker closed its Inari Medical purchase to add venous thromboembolism solutions. These moves stack R&D resources and consolidate hospital relationships, accelerating product launches and cross-selling.

Technology serves as a key battleground. Platforms integrating AI-guided workflow or dissolving scaffolds secure premium positioning. Companies with proven regulatory expertise advance fastest through updated quality standards, raising entry barriers for small challengers. Cost competition remains sharp in commodity segments, yet clinical evidence and outcome-based contracting often tilt purchasing toward brands that reduce reintervention risk.

Peripheral Stent Industry Leaders

Medtronic

Abbott Laboratories

Terumo Medical

Becton Dickinson and Company

Boston Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced plans to acquire BIOTRONIK’s vascular intervention business for approximately €760 million, gaining drug-coated balloon and stent assets with 25% of revenue tied to peripheral interventions.

- January 2025: Medtronic entered an exclusive US distribution agreement with Contego Medical for the FDA-cleared Neuroguard IEP System, a three-in-one carotid stenting platform.

- April 2024: Abbott secured FDA approval for the Esprit BTK Everolimus-Eluting Resorbable Scaffold, the first dissolving stent for below-the-knee disease.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the peripheral stent market as the total sales revenue generated from new, minimally invasive metal, polymer, or hybrid scaffolds deployed to reopen narrowed or blocked peripheral arteries in the iliac, femoropopliteal, infra-popliteal, renal, and carotid beds. Devices covered include bare metal, covered, drug eluting, and bio-resorbable formats supplied through balloon expandable or self-expanding delivery systems. Clinical settings span hospitals, outpatient catheter labs, and ambulatory surgical centers.

Scope exclusion: venous stents, cerebral stent systems, and aortic stent grafts are intentionally left outside this assessment.

Segmentation Overview

- By Product

- Bare-Metal Stents (BMS)

- Covered Stents

- Drug-Eluting Stents (DES)

- Bio-resorbable Vascular Scaffolds (BVS)

- By Artery Type

- Iliac Artery Stents

- Femoral-Popliteal Stents

- Renal & Related Artery Stents

- Carotid Artery Stents

- Infrapopliteal (Below-knee) Stents

- By Material

- Nitinol

- Cobalt-Chromium

- Stainless Steel

- Polymer / Composite

- By Deployment Mechanism

- Balloon-Expandable

- Self-Expanding

- By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with interventional radiologists, vascular surgeons, catheter lab managers, and material scientists across North America, Europe, and key Asia-Pacific hubs helped validate adoption rates of drug eluting and bio-resorbable platforms, typical length of stay, and emerging day care reimbursement models. Insights also refined average selling prices and flagged regional stock keeping nuances.

Desk Research

We started with disease burden data from sources such as the World Health Organization, CDC's National Health Interview Survey, and Eurostat to size the population at risk. Reimbursement schedules from the US Centers for Medicare and Medicaid Services and Japan's MHLW clarified weighted average procedure prices, while import export filings on Volza and customs dashboards indicated cross-border volume flows. Academic journals, notably the Journal of Endovascular Therapy, offered restenosis benchmarks that informed effectiveness driven replacement cycles. Company 10-K filings and device recall notices rounded out the landscape. This list is illustrative; several other open and subscription sources supported data collection and fact checking.

Market-Sizing & Forecasting

A top down prevalence to treated patient pool build drew on PAD incidence, intervention rates, and multi lesion frequencies, then cross checked through selective bottom up supplier roll ups of sampled ASP × volume. Key variables feeding the model include PAD prevalence growth, procedure to diagnosis conversion, average stent per procedure, ASP deflation tied to group purchasing contracts, regulatory approval cadence for next gen scaffolds, and the hospital to ASC migration rate. Forecasts employ multivariate regression layered with scenario analysis; parameters were stress tested with our primary experts to capture upside from bio-resorbable launches and downside from reimbursement cuts. Data gaps in bottom up counts were bridged using trade data proxies and regional sampling factors.

Data Validation & Update Cycle

Outputs pass three rounds of analyst review, variance checks against independent procedure trackers, and anomaly flags generated by our automated dashboards. Reports refresh each year, with interim updates triggered by material recalls, landmark trial read outs, or major regulatory approvals.

Why Our Peripheral Stent Baseline Commands Reliability

Published estimates often diverge because firms choose different arterial scopes, bundle accessories, or shift base years.

Key gap drivers include: some publishers pool venous and aortic graft revenues, a few inflate volumes by applying coronary ASPs, and others project growth from unapproved scaffold pipelines that our analysts classify as speculative. Mordor's disciplined refresh cadence and strict exclusion of out of scope devices keep our 2025 baseline of USD 5.75 billion on solid ground.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 5.75 B USD (2025) | Mordor Intelligence | - |

| 1.80 B USD (2023) | Global Consultancy A | excludes drug eluting premiums and applies narrower product mix |

| 3.90 B USD (2023) | Trade Journal B | folds venous stents and accessories into topline, older ASP benchmark |

These comparisons show that when scope, variables, and refresh cadence are harmonized, Mordor's figures offer the balanced, transparent baseline decision makers can rely on.

Key Questions Answered in the Report

What is the current value of the peripheral stents market?

The peripheral stents market stands at USD 6.17 billion in 2026 and is projected to grow to USD 8.73 billion by 2031.

Which product type holds the largest peripheral stents market share?

Drug-eluting stents lead with 51.66% revenue in 2025, driven by strong clinical evidence of long-term patency.

Which region is expanding fastest in the peripheral stents market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Peripheral Stent Market?

Asia-Pacific is forecast to post a 8.90% CAGR through 2031 on the back of improving healthcare infrastructure and higher PAD detection rates.

Why are bio-resorbable scaffolds gaining attention?

They dissolve after restoring blood flow, lower late-stage complication risk, and deliver drug therapy, leading to a segment CAGR of 10.05% through 2031.

How is the shift to ambulatory surgical centers affecting demand?

ASCs enable same-day discharge and lower procedure costs, encouraging physicians to adopt minimally invasive stents, thus supporting an 8.54% CAGR for this end-user segment.

What challenges could slow the peripheral stents market?

Lengthy regulatory reviews for new materials, price pressure from group purchasing organisations, and incomplete long-term safety data for bio-absorbable scaffolds may temper growth.

Page last updated on: