UV Curing System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.93 Billion |

| Market Size (2031) | USD 17.48 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

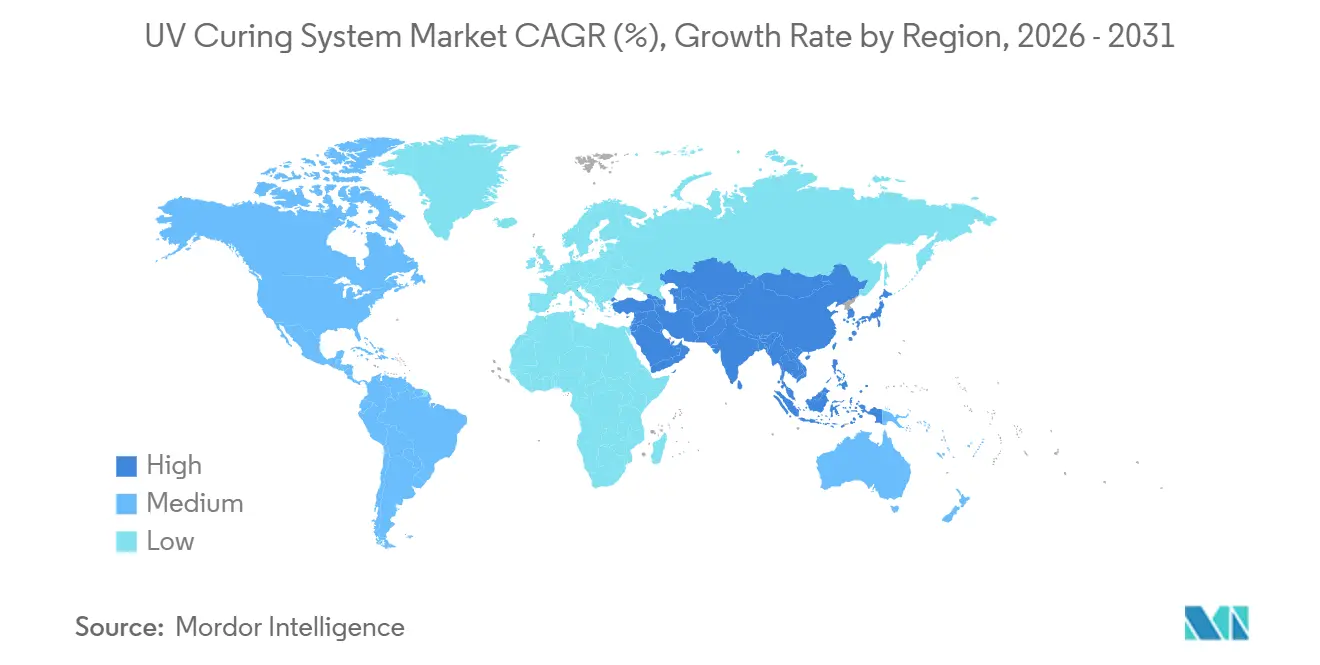

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

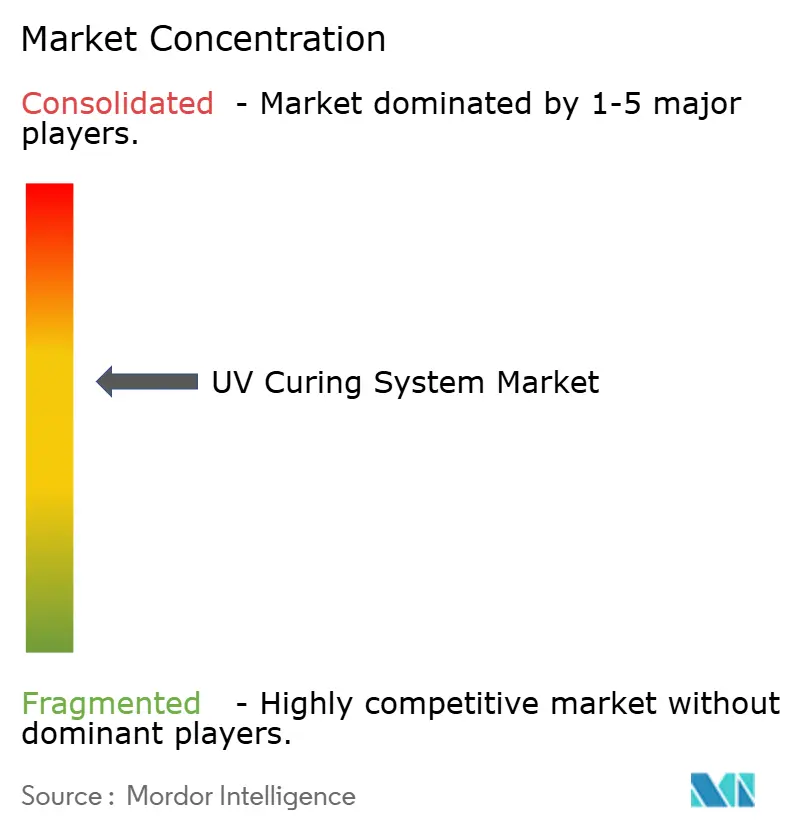

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV Curing System Market Analysis by Mordor Intelligence

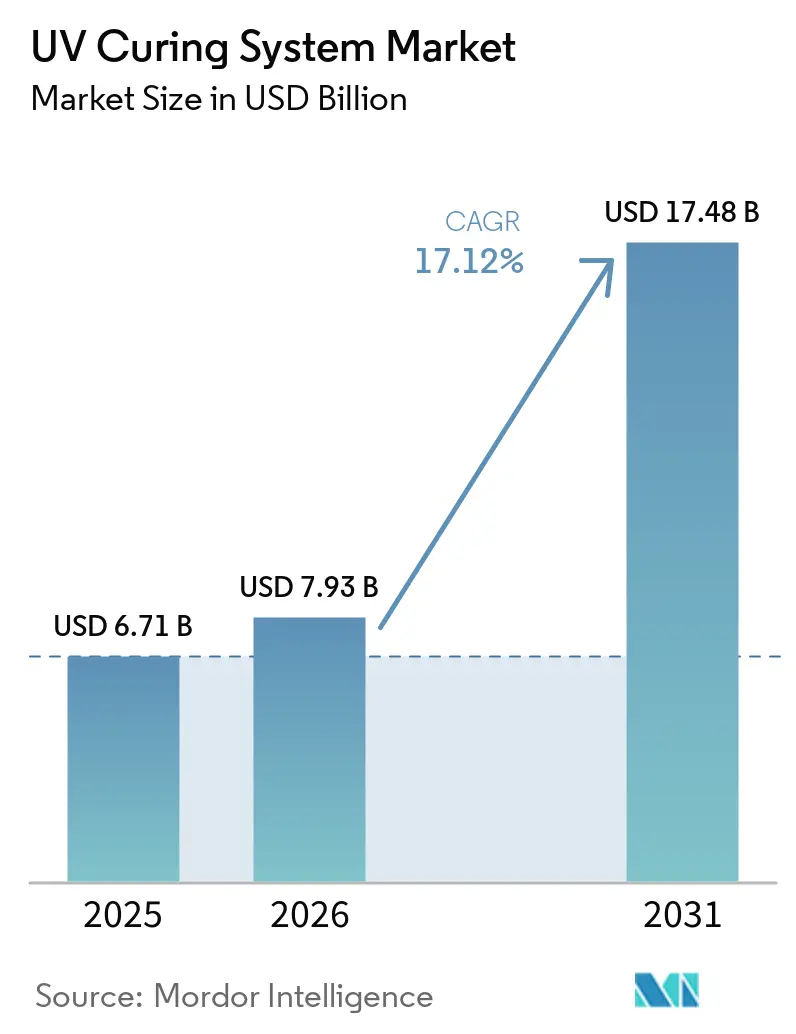

The UV curing system market size was valued at USD 6.71 billion in 2025 and is estimated to grow from USD 7.93 billion in 2026 to reach USD 17.48 billion by 2031, at a CAGR of 17.12% during the forecast period (2026-2031). Strong regulatory pressure on volatile organic compound emissions, a fast pivot to mercury-free LED architectures, and surging demand for in-line curing across high-speed printing and electronics assembly lines are reshaping capital-spending decisions. Energy savings of 60-85% achieved by UV-LED modules, the steep fall in photoinitiator loading made possible by UVC-dominant lamp spectra, and warranty extensions to 10 years are shortening payback periods for converters. Adoption is especially pronounced in the Asia-Pacific region, where electronics manufacturers seek rapid throughput, while the Middle East records the highest regional growth as packaging converters invest in digital-flexographic hybrids. Competitive intensity is rising as established lamp vendors expand solid-state portfolios and LED specialists bundle predictive-maintenance software, tilting revenue models toward data services and long-life hardware.

Key Report Takeaways

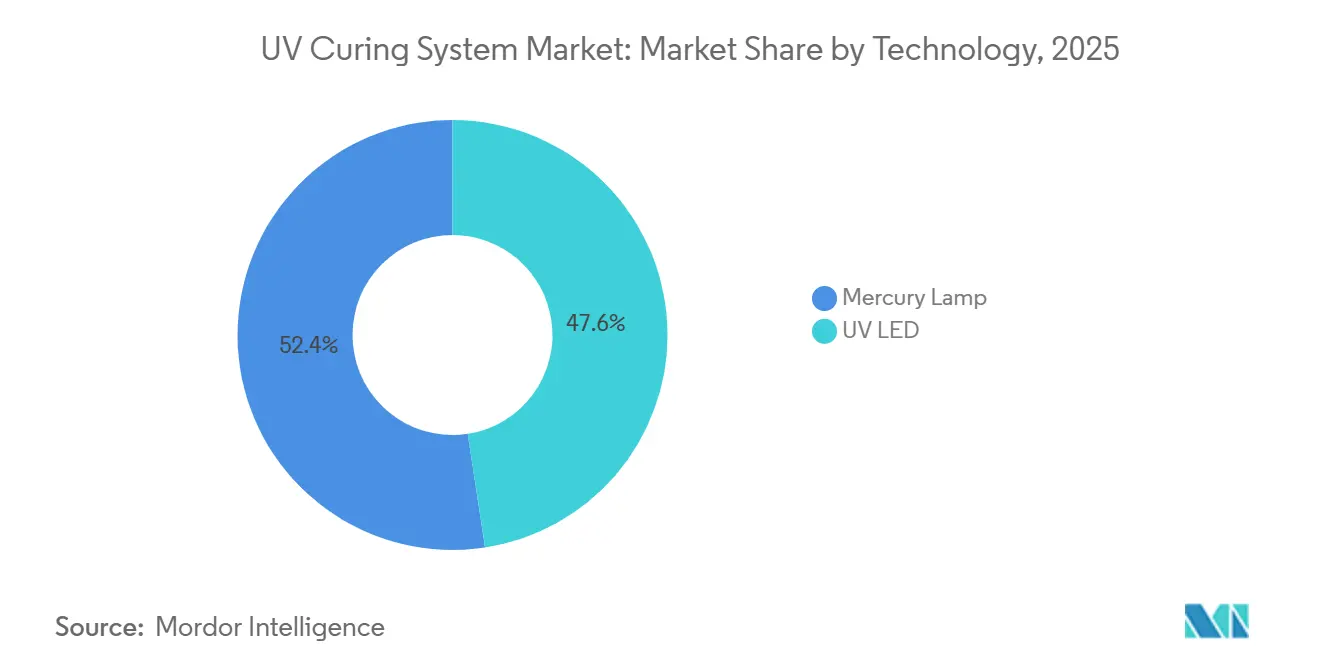

- By technology, mercury lamp systems held 52.42% of 2025 revenue in the UV curing system market, whereas UV-LED solutions are forecast to advance at a 17.94% CAGR through 2031.

- By type, conveyor cure systems accounted for 38.72% of demand in 2025, while hand-held and portable units are projected to grow at an 18.51% CAGR to 2031.

- By pressure type, medium-pressure units led with 42.03% share in 2025; low-pressure installations are set to expand at an 18.52% CAGR through 2031.

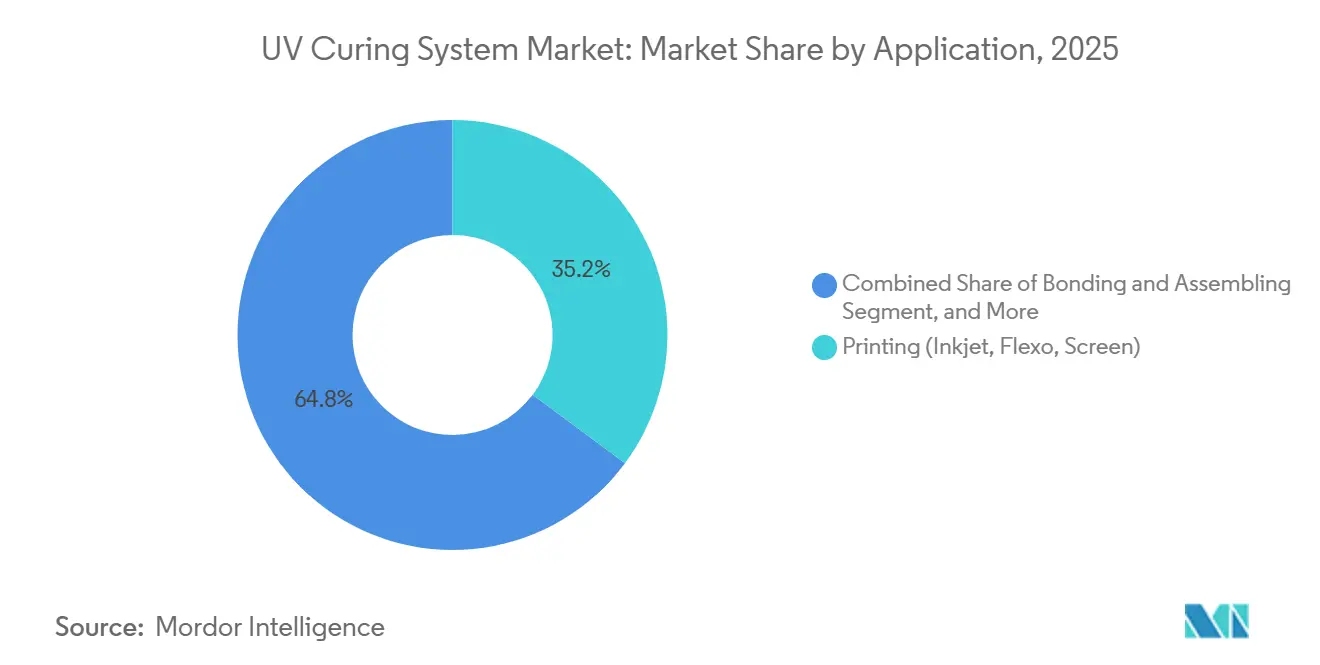

- By application, printing captured 35.25% of 2025 revenue, and 3D printing and additive manufacturing is poised to grow at an 18.26% CAGR to 2031.

- By end-use industry, electronics and semiconductors commanded 29.43% revenue share in 2025, while medical devices and healthcare is projected to log an 18.38% CAGR during 2026-2031.

- By geography, Asia-Pacific dominated with 41.88% of 2025 value, and the Middle East is forecast to register an 18.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UV Curing System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC-emission Regulations Accelerating Shift to UV Curing | +3.2% | Global, with enforcement concentration in North America and European Union | Medium term (2-4 years) |

| Rapid Uptake of UV-LEDs for Energy-Efficient Operations | +2.8% | Global, with adoption leadership in Asia-Pacific electronics hubs and North America packaging | Short term (≤ 2 years) |

| Expanding Electronics Manufacturing Demand for Conformal-Coating and Bonding | +2.5% | Asia-Pacific core, spill-over to Mexico and Central Europe automotive clusters | Medium term (2-4 years) |

| Growth in High-Speed Digital and Flexographic Printing Lines | +1.8% | Global, with concentration in North America and European Union label and packaging converters | Short term (≤ 2 years) |

| Integration of UV Curing in EV-Battery Module Assembly | +1.5% | Asia-Pacific and North America electric-vehicle manufacturing corridors | Long term (≥ 4 years) |

| AI-Enabled In-Line Process Control Improving Curing Uniformity | +0.9% | Global, with early adoption in Germany, United States, and Japan industrial automation leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC-Emission Regulations Accelerating Shift to UV Curing

Governments tightened limits in 2025-2026, capping solvent content in aerosol coatings and structural adhesives. Manufacturers avoid costly air-permit modifications by switching to nearly zero-VOC UV formulations that polymerize photochemically rather than through evaporation. New directives also flag several legacy photoinitiators as substances of very high concern, motivating chemists to adopt low-extractable initiator families. Vendors responded with UVC-dominant lamp systems that cut photoinitiator loading by up to 75%, delivering high web speeds and a 1.5-2.5-year payback through reduced waste handling and raw-material cost.

Rapid Uptake of UV-LEDs for Energy-Efficient Operations

Solid-state modules convert electricity directly into narrow-band UV, trimming power draw by as much as 85% and virtually eliminating infrared waste heat. Recent product launches deliver up to 79 W cm-¹ irradiance and 48% wall-plug efficiency while offering lifetimes of 35,000 hours, dwarfing the 1,000-2,000 hour threshold of mercury lamps. The total cost of ownership now favors LEDs in regions where industrial power exceeds USD 0.15 kWh-¹, and predictive-maintenance platforms embedded in new systems further cut unplanned downtime by 30%.

Expanding Electronics Manufacturing Demand for Conformal-Coating and Bonding

Printed-circuit producers in China, Japan, and South Korea are scaling UV lines that coat more than 1,200 boards per hour, complying with automotive and consumer-device moisture-resistance standards. Electric-vehicle battery packs rely on UV-curable adhesives that fixture in 3-5 seconds, eliminating half-hour oven cycles and aligning output with gigafactory throughput goals. Suppliers of dielectric coatings have validated biocompatible formulas that pair with 395 nm LEDs, enabling rapid processing without thermal damage to sensitive components.

Growth in High-Speed Digital and Flexographic Printing Lines

Hybrid presses harness digital inkjet for variable data and UV-flexo stations for dense colors, hitting 450 m min-¹ with in-line LED arrays that deactivate segments outside the active web. Air-cooled modules remove the need for chilled-water loops, shaving USD 15,000-25,000 from installation budgets and slashing energy use by up to 50% on short-run jobs. The technology supports migration-compliant inks, enabling converters to meet stringent food-contact regulations while achieving same-day delivery schedules.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of UV-LED Systems Versus Legacy Lamps | -2.1% | Global, with adoption barriers concentrated in South America, Africa, and Southeast Asia small and medium enterprises | Short term (≤ 2 years) |

| Limited Penetration Depth for Thick-Film Applications | -1.3% | Global industrial manufacturing and automotive refinish segments | Medium term (2-4 years) |

| Supply-Chain Volatility of Specialty Photoinitiators | -1.1% | Global, with concentration risk in European Union and Asia sourcing | Medium term (2-4 years) |

| Transitional Uncertainty from Mercury-Lamp Disposal Regulations | -0.7% | European Union and signatory nations to Minamata Convention | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of UV-LED Systems Versus Legacy Lamps

LED modules priced at USD 25,000-150,000 command a 150-300% premium over mercury alternatives, extending payback to 3-5 years in low-tariff regions. SMEs face additional hurdles in technician training and formulation re-qualification, each adding USD 5,000-15,000 per product line. Leasing and performance-based contracts ease capital strain but penetration remains below 10% of installed units.

Limited Penetration Depth for Thick-Film Applications

Single-pass curing is restricted to approximately 200 µm due to the limitations imposed by Beer-Lambert attenuation. Although dual-cure hybrids and UVC-focused lamp systems can increase the curing depth to 300 µm, these advancements come with significantly higher costs and greater process complexity. Consequently, critical industries such as wind-turbine blade manufacturing and automotive clear coat applications continue to rely on thermal ovens for curing processes. This reliance on thermal ovens limits the near-term adoption and displacement potential of UV curing solutions in these segments, despite the technological advancements in UV curing systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: LED Architectures Reshape Economics

UV-LED platforms contributed a rising share of the ultraviolet curing system market in 2025 and are projected to outpace the overall growth trajectory with a 17.94% CAGR until 2031. Hardware now approaches 48% electrical efficiency, and warranty coverage stretches to 35,000 hours, narrowing the total-cost gap with mercury lamps to roughly 20% over a decade. Mercury systems still dominate thick, pigment-rich coatings because their broad spectra activate multiple photoinitiators, sustaining 52.42% of 2025 revenue. Nevertheless, the ultraviolet curing system market share for LEDs is climbing each year as regulatory deadlines accelerate lamp retirements and energy-savings imperatives intensify.

Integrators now embed advanced cloud analytics systems that monitor key parameters such as irradiance, temperature, and run-time. These systems enable predictive maintenance by scheduling services only when required, resulting in a significant 30% improvement in line availability. Furthermore, even the legacy mercury segment has undergone notable advancements, introducing innovations like UVC-dominant FREEcure lamps. These lamps are designed to allow a lower photoinitiator content, highlighting that sustained research and development efforts across both traditional and emerging technologies will continue to coexist and drive progress throughout the forecast period.

By Type: Portable Systems Gain Field-Service Traction

Conveyor installations formed 38.72% of 2025 demand, anchoring high-throughput print and coating lines that clock 10-450 m min-¹. They remain essential for continuous webs and panels that require uniform dose. Yet the hand-held and portable sub-segment is the fastest mover, forecast at an 18.51% CAGR through 2031 as battery-powered units weighing under 1.2 kg deliver 20 W cm-² spot intensity on construction sites and in auto-glass repair bays. The UV curing system market for portable tools is small today, but gains from on-site bonding and repair applications are attracting new entrants offering modular LED heads compatible with multiple chemistries.

Spot-cure devices equipped with closed-loop irradiance feedback maintain ±3% dose uniformity over 20,000 hours, a reliability level that reduces scrap in electronics assembly. Flood-cure cabinets still serve semiconductor wafers and 3D-printed batches, with 100×100 mm to 600×600 mm footprints, processing up to 200 units per hour. Collectively, the breadth of choice widens the addressable UV curing system market, easing entry for users of all scales.

By Pressure Type: Low-Pressure UV Gains in Disinfection

Medium-pressure lamps led in 2025 with 42.03% revenue share because they balance 80-240 W cm-¹ intensity and manageable heat load, making them the workhorse for industrial coatings and flexographic presses. Low-pressure equipment, however, will log the fastest 18.52% CAGR to 2031, driven by 254 nm germicidal projects in water treatment and pharmaceutical sanitation. Although germicidal modules serve a different photochemistry than UV-A curing, manufacturers often source from the same vendors, contributing incremental volume to the broader UV curing system market.

High-pressure systems, crucial for optical-fiber coating at 1,000-3,000 m min-¹, claim a niche presence, where sub-second cure offsets their shorter 500-800-hour lamp life and USD 3,000-8,000 replacement price. The push for mercury-free operation is now steering municipal utilities toward UV-C LEDs despite 4% wall-plug efficiency, signaling potential crossover into curing applications once diode costs decline further.

By Application: Additive Manufacturing Accelerates Resin Demand

Printing still commanded 35.25% of 2025 sales due to widespread flexographic adoption, yet additive manufacturing is poised for an 18.26% CAGR, as engineering-grade photopolymers enable functional jigs and end-use parts that harden within seconds. The UV curing system market for 3D printers is growing due to dental and medical clearances for biocompatible resins.

Instant fixture boosts plant throughput by 40-60% over traditional oven-cured epoxies, with coating and bonding workflows leading the charge. In the packaging realm, converters adopt migration-compliant inks to comply with food-contact regulations, solidifying their hold on the UV curing system market, which was previously established in flexible films and labels. The growing demand for sustainable and efficient solutions further drives the adoption of UV curing systems across various applications.

By End-Use Industry: Medical Devices Lead Growth Trajectory

Electronics and semiconductors delivered 29.43% of the 2025 value as board shops rely on 10-second conformal-coat cycles. Looking ahead, medical devices and healthcare will be the fastest-growing sector, with a 18.38% CAGR, as ISO 10993-vetted UV adhesives dominate catheter and syringe assembly lines. This shift adds resilience to the UV curing system industry by diversifying beyond cyclical consumer electronics.

Automotive players are integrating LED curing for battery module adhesives, freeing up real estate formerly occupied by 30-60 minute thermal ovens. Aerospace contractors test UV conformal coats that meet MIL-I-46058C, yet full-fuselage and rotor-blade composites still await higher-glass-transition-resin chemistries. Cosmetics applications continue, but stricter safety testing encourages equipment suppliers to incorporate motion sensors and timers, ensuring controlled 365 nm exposure.

Geography Analysis

Asia-Pacific retained 41.88% of 2025 revenue, propelled by electronics clusters in China, Japan, and South Korea that demand fast-cycle conformal coating on printed-circuit boards. Government VOC limits adopted in 2024 nudged furniture plants to UV-acrylate lacquers, replacing 50-200 kW drying ovens with LED tunnels and shrinking energy intensity by two-thirds. Semiconductor equipment manufacturers integrate 365-405 nm arrays to reduce wafer-bonding temperatures below 80 °C, preserving yield on gallium-nitride power devices.[1]China Ministry of Ecology and Environment, “Volatile Organic Compound Limits for Industrial Coatings,” mee.gov.cn

The Middle East, led by the United Arab Emirates and Saudi Arabia, is the fastest-expanding region at an 18.29% CAGR. Packaging converters there are installing digital-flexographic hybrids that rely on segmented LED bars for rapid changeovers demanded by multinational consumer brands. Government loan incentives covering as much as 70% of equipment cost lower adoption hurdles, while local medical-device assemblers in Israel validate UV adhesives under stringent ISO 13485 regimes.[2]Saudi Arabia Vision 2030, “Industrial Diversification Program,” vision2030.gov.sa

North America and Europe post steady but slower gains as many converters have already replaced mercury lamps and now focus on AI-aided dose optimization. U.S. aerosol-coating rules finalized in January 2025 and the pending European RoHS phase-out of mercury lamps in February 2027 continue to backstop demand, yet small and medium enterprises in South America and Africa struggle with 150-300% LED price premiums and sub-USD 0.08 kWh-¹ power tariffs that stretch payback periods to five years.

Competitive Landscape

The top five suppliers accounted for roughly 45% of 2025 revenue, indicating moderate concentration in the UV curing systems market. Excelitas built scale through the 2023 twin acquisitions of Phoseon Technology and the Heraeus Noblelight UV business, enabling vertical integration from LED emitters to cloud analytics. IST Metz counters with LEDcure NX, a 48% wall-plug platform backed by a 10-year warranty and SMARTcure predictive-maintenance software that trims scrap by up to 30%.

GEW underscores low-cost ownership by offering air-cooled bars that remove USD 15,000-25,000 in chilled-water hardware. Regional differentiation matters: Baldwin Technology added U.S. capacity in 2025, reducing shipment times to 6-10 weeks and pairing UV-LED arrays with infrared pre-dryers for hybrid ink systems. Chinese diode makers now supply 365-405 nm chips at half the Western price, tempting cost-conscious converters, but concerns over uniformity and after-sales support are slowing Western uptake.[3]Baldwin Technology Company Inc., “United States Manufacturing Expansion,” baldwintech.com

Strategic thrusts pivot on service economics rather than pure irradiance. Vendors market pay-per-linear-meter contracts that shift capex to opex, resonating with converters wary of large upfront outlays, particularly in South America and Africa. Dual-wavelength R&D aims to overcome thick-film limits, while germicidal UV-C LED progress hints at future overlap with curing lines as diode efficiency climbs.

UV Curing System Industry Leaders

Heraeus Noblelight GmbH

IST Metz GmbH and Co. KG

GEW (EC) Limited

Nordson Corporation

Dymax Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UAVOS deployed a UV-based composite oven for unmanned-aerial-vehicle fuselages, trimming cycle time from eight hours to 45 minutes and cutting energy draw by 85%.

- January 2026: Dymax launched 9773 conformal coating that reaches tack-free in five seconds and meets MIL-I-46058C thermal-shock requirements.

- January 2026: Dymax unveiled BlueWave QX4 V3.0, a 20 W cm-² hand tool storing exposure recipes on a USB interface for ISO 13485 assembly lines.

- November 2025: Lawrence Livermore National Laboratory demonstrated simultaneous 365 nm and 405 nm exposure curing 500 µm methacrylate layers, cutting delamination in large-format additive builds.

Global UV Curing System Market Report Scope

The UV curing system market comprises equipment, materials, and solutions that utilize ultraviolet (UV) radiation to efficiently cure inks, coatings, adhesives, and resins. Through photochemical reactions, UV curing systems enable rapid curing, offering significant advantages over traditional thermal methods, including greater speed, improved energy efficiency, precise process control, and enhanced environmental sustainability.

The UV Curing System Market Report is Segmented by Technology (Mercury Lamp, and UV LED), Type (Spot Cure, Flood Cure, Conveyor Cure, and Hand-Held/Portable), Pressure Type (Low-Pressure, Medium-Pressure, and High-Pressure), Application (Bonding and Assembling, Printing, Coating and Finishing, Disinfection/Purification, and 3D Printing/Additive Manufacturing), End-Use Industry (Electronics and Semiconductors, Automotive and Transportation, Medical Devices and Healthcare, Industrial Manufacturing, Aerospace and Defense, Packaging, and Cosmetics and Personal Care), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Mercury Lamp |

| UV LED |

| Spot Cure Systems |

| Flood Cure Systems |

| Conveyor Cure Systems |

| Hand-Held/Portable Systems |

| Low-Pressure UV Systems |

| Medium-Pressure UV Systems |

| High-Pressure UV Systems |

| Bonding and Assembling |

| Printing (Inkjet, Flexo, Screen) |

| Coating and Finishing |

| Disinfection/Purification |

| 3D Printing/Additive Manufacturing |

| Electronics and Semiconductors |

| Automotive and Transportation |

| Medical Devices and Healthcare |

| Industrial Manufacturing |

| Aerospace and Defense |

| Packaging |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Mercury Lamp | |

| UV LED | ||

| By Type | Spot Cure Systems | |

| Flood Cure Systems | ||

| Conveyor Cure Systems | ||

| Hand-Held/Portable Systems | ||

| By Pressure Type | Low-Pressure UV Systems | |

| Medium-Pressure UV Systems | ||

| High-Pressure UV Systems | ||

| By Application | Bonding and Assembling | |

| Printing (Inkjet, Flexo, Screen) | ||

| Coating and Finishing | ||

| Disinfection/Purification | ||

| 3D Printing/Additive Manufacturing | ||

| By End-Use Industry | Electronics and Semiconductors | |

| Automotive and Transportation | ||

| Medical Devices and Healthcare | ||

| Industrial Manufacturing | ||

| Aerospace and Defense | ||

| Packaging | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the UV curing system market by 2031?

The market is forecast to reach USD 17.48 billion by 2031.

Which segment will record the fastest growth through 2031?

Medical devices and healthcare is expected to expand at an 18.38% CAGR.

Why are UV-LED systems gaining momentum over mercury lamps?

LEDs cut energy use by up to 85%, offer 35,000-hour lifetimes, and help companies meet upcoming mercury-phase-out rules.

Which region is poised for the highest growth rate?

The Middle East is projected to log an 18.29% CAGR between 2026 and 2031.

What are the main barriers to LED adoption in emerging economies?

High upfront costs, limited access to financing, and lower electricity tariffs extend payback periods to as long as five years.

Page last updated on: