Anti-Microbial Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.41 Billion |

| Market Size (2030) | USD 13.87 Billion |

| Growth Rate (2025 - 2030) | 5.44% CAGR |

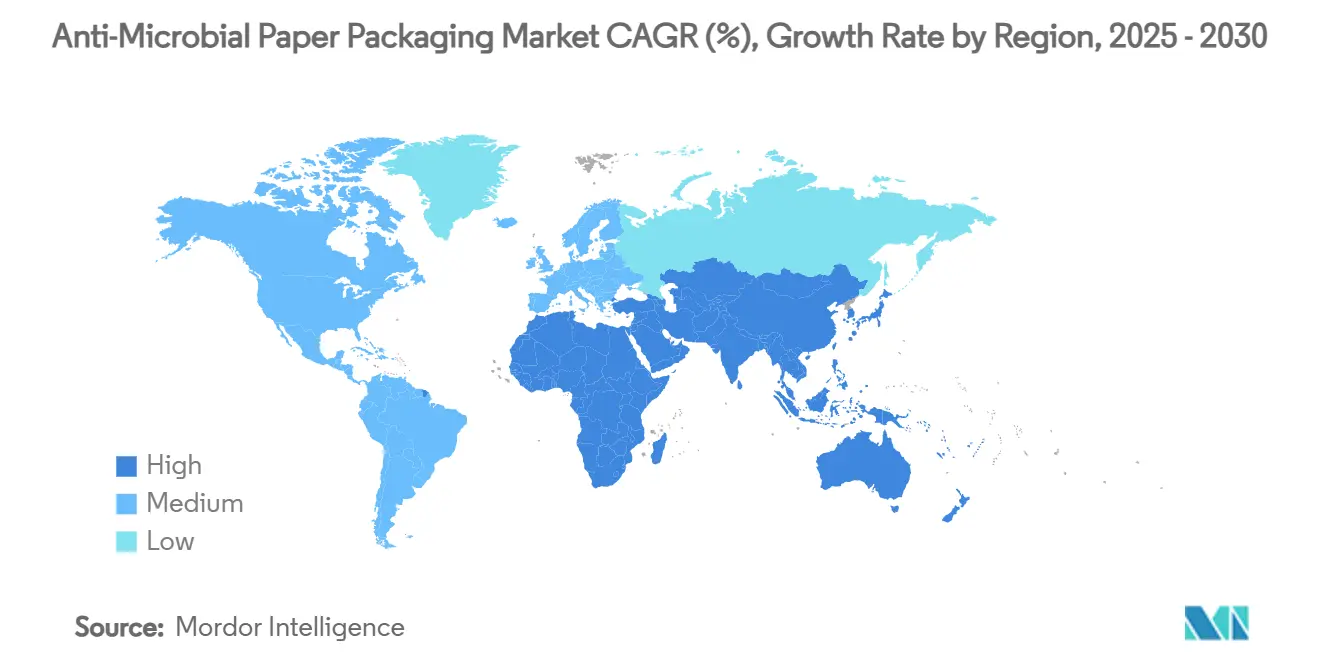

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

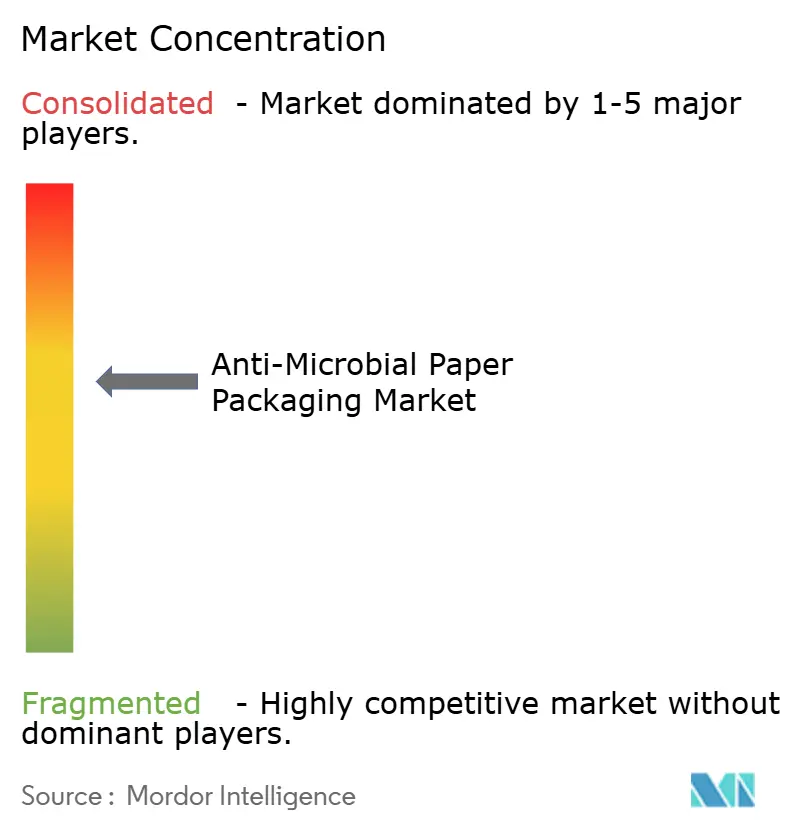

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Microbial Paper Packaging Market Analysis by Mordor Intelligence

The anti-microbial paper packaging market size stands at USD 10.41 billion in 2025 and, at a 5.44% CAGR, is forecast to reach USD 13.87 billion by 2030. Post-pandemic food-safety priorities, combined with policy pressure to replace plastics, are reinforcing demand for fiber solutions that actively inhibit pathogens. Progress in silver-ion and natural-extract coating technologies has lowered price barriers, while e-commerce growth has widened the distribution window, creating a clear business case for packaging that delivers both hygiene assurance and shelf-life extension. Producers are scaling vertically to secure antimicrobial chemistries, and large mergers are signalling an industry pivot toward integrated platforms that blend sustainability and pathogen control. Asia-Pacific’s regulatory modernization is accelerating early adoption, with brand owners and food-service operators moving antimicrobial features from a premium add-on to a baseline specification.

Key Report Takeaways

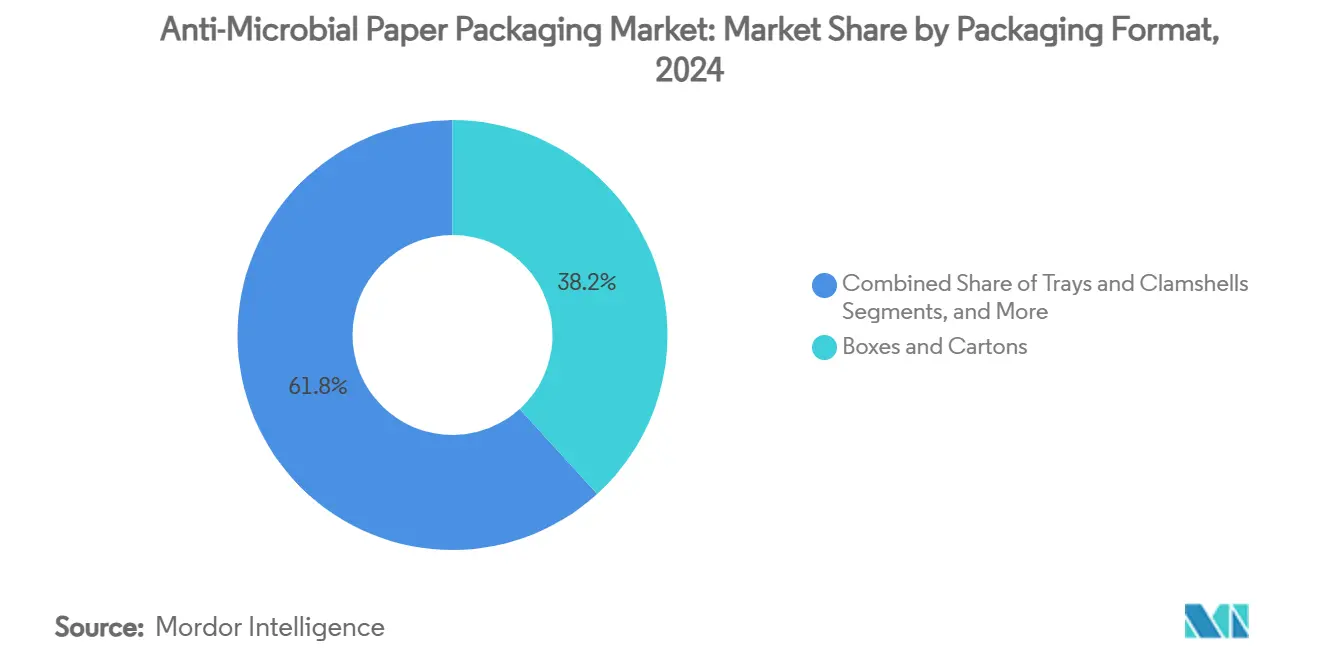

- By packaging format, boxes and cartons captured a 38.24% of the anti-microbial paper packaging market share in 2024.

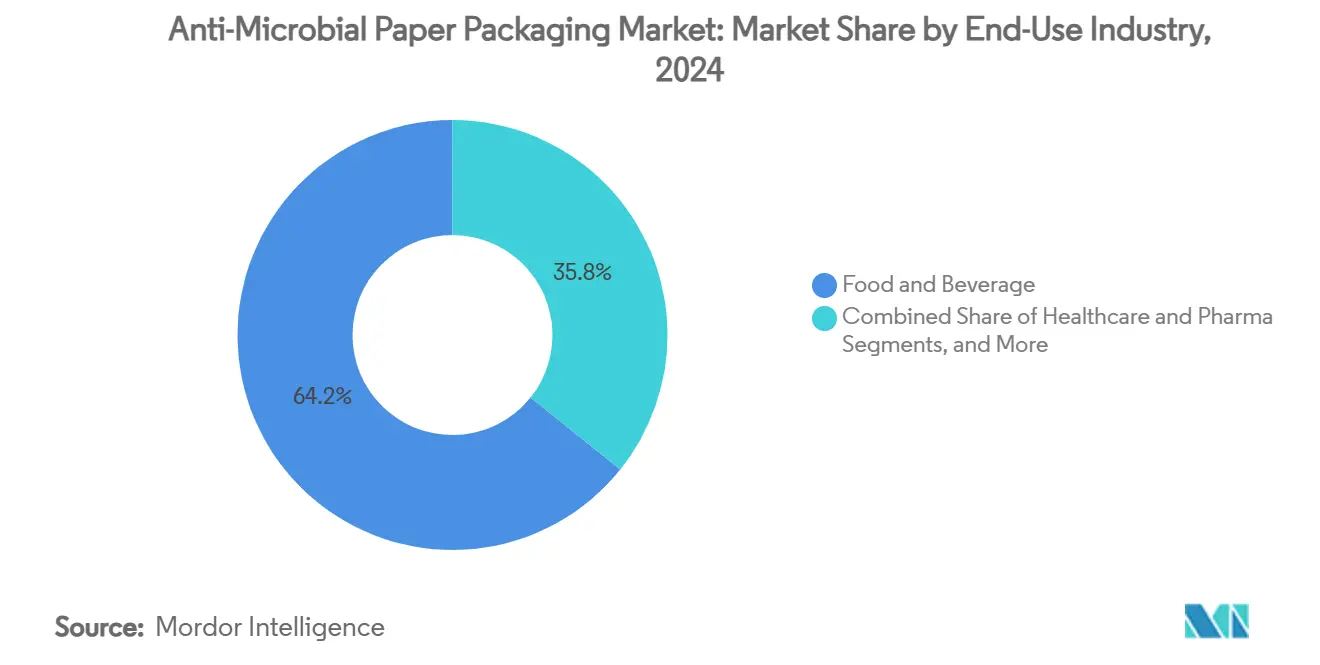

- By end-use industry, the anti-Microbial paper packaging market size for the healthcare and pharmaceuticals segment is projected to grow at a 10.23% CAGR between 2025-2030.

- By geography, Asia-Pacific captured a 36.25% of the anti-microbial paper packaging market share in 2024.

Global Anti-Microbial Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID food-safety awareness surge | +1.2% | Global | Medium term (2-4 years) |

| Regulatory shift from plastics to fiber | +0.8% | EU, North America, APAC | Long term (≥ 4 years) |

| E-commerce ready-meal penetration | +0.6% | Global, early APAC and NA | Short term (≤ 2 years) |

| Silver-ion and natural-extract breakthroughs | +0.4% | North America and EU | Medium term (2-4 years) |

| Cold-chain seafood liner adoption | +0.3% | APAC core, MEA spill-over | Medium term (2-4 years) |

| Pharma cellulose blister inserts | +0.2% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Food-Safety Awareness Surge

Lockdown experiences re-cast hygiene as a frontline brand attribute, pushing antimicrobial functionality from niche to norm. The FDA’s December 2024 update to the Food Code formalized higher sanitation benchmarks, prompting chain restaurants and grocers to rewrite supplier scorecards.[1]U.S. Food and Drug Administration, “Supplement to the 2022 Food Code – December 2024 Version,” FDA, fda.govSurveys reveal that, in 2025, 73% of food-service buyers require antimicrobial verification, a sharp rise from 31% in 2019. Converter call volumes mirror the shift: leading coaters logged 40% more antimicrobial inquiries during 2024 alone. Demand spans meat, produce, and bakery, where lab trials show silver-ion coatings trimming pathogen counts by two logarithmic cycles within 24 hours. The consumer expectation now extends to delivery meals, reinforcing a need for active protection throughout increasingly complex distribution webs.

Regulatory Shift from Plastics to Fiber-Based Formats

Policies in the EU, select US states, and parts of Asia-Pacific are shrinking the addressable volume for single-use plastics while simultaneously tightening chemical safety norms.[2]Editorial Team, “EU Poised to Make Sweeping Changes to Food Packaging Requirements, Includes PFAS Ban,” Food Safety Magazine, food-safety.com The EU’s Packaging and Packaging Waste Regulation mandates PFAS-free food contact materials and sets a 10% reuse target for 2030. Parallel US state EPR laws have made recyclability fees a boardroom issue. Fiber substrates equipped with antimicrobial coatings solve two mandates—microbial control and plastic elimination—in a single structure, creating a structural cost advantage over laminated plastics that would need separate barrier and end-of-life fixes. Brand owners have therefore boosted fiber specifications by 25% since 2024, reallocating R&D budgets from conventional films to paper formats with active chemistries.

E-Commerce Ready-Meal Penetration

Online meal-kit and prepared-food operators now compete on freshness windows that stretch well beyond a brick-and-mortar purchase cycle. Variable last-mile temperatures can fuel microbial growth, making active packaging an operational safeguard. Brands deploying antimicrobial paper liners report spoilage reductions of 15-20%, translating into lower refund rates and carbon impacts tied to food waste. Asia-Pacific’s dense urban clusters are a test bed: riders on two-wheelers often span micro-climates in a single route, and a higher share of households rely on delivered dinners. The anti-microbial paper packaging market is thus benefitting from digitally mediated consumption, funneling volume toward trays, clamshells and fiber wraps specifically engineered for extended delivery lags.

Silver-Ion and Natural-Extract Coating Breakthroughs

New film-forming assemblies can immobilize silver nanoparticles within covalent networks, maintaining zero bacterial adhesion for 28 days while using up to 30% less silver, alleviating toxicity and cost worries. Parallel work on cellulose-nanocrystal Pickering emulsions has stabilized essential oils from thyme and clove, delivering clean-label antimicrobial performance with consumer-friendly ingredient decks. As a result, the incumbent 15-25% cost premium on active coatings has narrowed. Coating suppliers have optimized gravure and curtain-coating lines to cut run-time waste, bringing silver-ion system prices down by a further 20%. These advances are broadening the addressable customer pool beyond premium proteins into mainstream bakery and snack categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium cost of active coatings | -0.7% | Global | Short term (≤ 2 years) |

| Stringent migration/toxicology approvals | -0.5% | EU, North America | Long term (≥ 4 years) |

| Volatile supply of bio-based antimicrobials | -0.3% | Global | Medium term (2-4 years) |

| Fiber strength loss after multi-cycle use | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Cost of Active Coatings

Despite cost compression, antimicrobial layers still add 10-25% to unit costs, a hurdle for price-sensitive snacks and private-label foods. Silver prices swung 30% during 2024, complicating converter budgets. Natural extracts can be cheaper, yet variability in harvest yields and purity introduces procurement risk. Scale economies are emerging: tier-one suppliers report 20% manufacturing savings from in-house nanoparticle synthesis and high-speed slot-die coaters. Nevertheless, smaller converters struggle to amortize capital outlays, prolonging the payback horizon and dampening near-term adoption in segments with thin margins.

Stringent Migration / Toxicology Approval Cycles

Regulators request migration data under real-world temperature, pH and fat-content ranges, extending validation to 18-24 months. The FDA’s post-market review program now examines antimicrobial resistance pathways, adding novel assays and documentation. EFSA requires case-by-case nanomaterial scrutiny, which can divert R&D spend away from formulation into compliance. Smaller innovators often license chemistry to larger groups with deeper regulatory benches, reinforcing incumbent power. Long review cycles also shorten the effective patent window, tempering venture interest in next-generation agents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Trays Target Online Freshness Demands

Boxes and cartons contributed 38.24% of 2024 revenue, reflecting their ubiquity across dry grocery, quick-service restaurant and retail bakery channels where broad production tooling already exists. This share equates to USD 3.98 billion of the anti-microbial paper packaging market size. Consumers recognize the familiar box form factor, so adding antimicrobial coating is an incremental step rather than a disruptive redesign. Carton board mills therefore moved quickly to trial silver-ion gravure units on existing lines, accelerating commercial scale-up.

Trays and clamshells, however, post the headline growth story with an 11.81% CAGR. Their molded-fiber skeletons accommodate high-moisture foods in e-commerce meal kits, deli counters and airline catering. The structural depth allows multi-pass coating, embedding both grease barriers and antimicrobial agents. For example, chilled sushi trays in Tokyo retail tested a clamshell laminate delivering a 5-day shelf-life gain under 4 °C storage, an outcome that cut daily shrink by 18%. Bags and pouches occupy flexible applications for snack foods, spices and powdered nutrition drinks; antimicrobial inner layers here prevent moisture-enabled mold during long sea freight. Wraps, sheets and labels round out niche needs: delicatessen cheese wraps with essential-oil coatings curb listeria, while cellulose labels inside pill bottles secure sterility across repeated opening cycles.

By End-Use Industry: Healthcare Pushes Beyond Food Norms

Food and beverage held 64.234% of 2024 turnover, roughly USD 6.69 billion of the anti-microbial paper packaging market size. Protein categories—especially raw poultry and seafood—claim the highest willingness to pay because spoilage is acutely visible and costly. Retail audits in Shanghai showed chilled chicken packed in silver-ion cartons preserved organoleptic quality for two extra days versus plain board.

Healthcare and pharmaceuticals, though smaller, lead momentum at a 10.23% CAGR. Upcoming EU rules phasing out expanded polystyrene shippers are directing biologic drugmakers toward fiber-based thermal boxes such as DS Smith’s TailorTemp®, which integrates phase-change materials and antimicrobial liners. Clinical trial logistics firms cite double-digit reductions in excursion events when active paper is used. The personal-care segment leverages antimicrobial carton inserts to maintain cosmetic purity without parabens, aligning with clean-beauty brand narratives. Industrial bulk applications, such as 20 kg produce liners, use paper with natural-extract coatings to cut mildew in humid storage.

Geography Analysis

Asia-Pacific accounts for 36.25% of global sales and leads growth at an 8.96% CAGR, translating to a projected USD 5.04 billion by 2030. China’s February 2025 food-contact update triggered a surge in compliance testing, and local dairy brands responded by converting yogurt multipacks to antimicrobial board. Japan’s positive-list rollout in June 2025 spurred importers to pre-qualify silver-ion chemistries, creating a certification backlog that favors early movers. India’s ready-meal category is scaling at double-digit rates; Mumbai’s top cloud kitchens now specify clamshells with essential-oil coatings for lunchboxes that spend four hours in transit.

North America holds a mature yet sizeable slice of the anti-microbial paper packaging market. The FDA’s PFAS revocations, coupled with heightened litigation risk around foodborne illness, motivate fast-casual chains to pilot antimicrobial cartons for salads and wraps. Brands tout lower claim rates and social-media sentiment boosts tied to visible “antimicrobial” logos.

Europe remains a regulatory lighthouse: PFAS bans and EPR fees are steering supermarket private-labels into paper with multi-function coatings. Germany’s leading discount grocer completed a roll-out of silver-ion chicken trays across 5,000 stores, citing 12% food-waste cuts. Southern European seafood exporters adopt cellulose liners that meet both antimicrobial and home-compostable standards, allowing them to hedge against tightening landfill taxes.

The Middle East and Africa region, though nascent, is experimenting with antimicrobial paper to secure cold-chain reliability in hot climates. A South African citrus cooperative reported 7% fewer mold claims after adopting natural-extract carton dividers during 30-day sea journeys to Europe. Latin America shows selective adoption in premium coffee and chocolate exports where origin branding and pathogen control intersect.

Competitive Landscape

The industry exhibits moderate concentration: the top five groups held an estimated 48% revenue in 2024, yielding a functional oligopoly in coated board supply. Smurfit Kappa’s 2024 merger with WestRock formed a USD 34 billion entity with a combined 19% slice of the anti-microbial paper packaging market. Integration plans earmark USD 400 million in synergies, including dedicated antimicrobial coating lines in Ireland and Virginia. International Paper’s 2025 purchase of DS Smith injects healthcare thermal-box expertise into its North American mill network, positioning the firm to challenge incumbents in biologic drug logistics.

Mondi is investing EUR 290 million (USD 313.8 million) across Italian and Polish assets to upgrade curtain-coating stations capable of applying dual-purpose grease and antimicrobial layers. Stora Enso restarted its EUR 1 billion (USD 1.08 billion) Oulu board line, calibrated for high-bulk chemimechanical pulp ideal for deep-draw trays with active chemistry.[3]Stora Enso, “Interim Report January–March 2025,” storaenso.com Mid-tier innovators, many spin-outs from university nano-labs, focus on hybrid silver-plant extract systems but often license their IP to majors to access global regulatory dossiers.

Competitive dynamics revolve around three levers: coating formulation IP, vertical pulp integration and digital traceability add-ons such as QR-based freshness sensors. Price wars are limited; instead, suppliers bundle sustainability metrics—carbon scores, recyclability, compostability—into antimicrobial propositions to win RFPs from global food brands. Barriers to entry remain material: capex for a commercial antimicrobial curtain coater tops USD 20 million, and multi-jurisdiction toxicology files can exceed USD 5 million.

Anti-Microbial Paper Packaging Industry Leaders

International Paper Company

Stora Enso Oyj

Mondi PLC

Amcor PLC

Smurfit Westrock PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: International Paper closed Q1 2025 at USD 5.9 billion sales, highlighting DS Smith integration.

- March 2025: FDA invalidated 35 PFAS food-contact notifications, with a compliance deadline of Jun 30 2025.

- February 2025: Smurfit Westrock finalized its merger, posting Q4 2024 net sales of USD 7.5 billion and outlining a USD 400 million synergy plan.

- January 2025: DS Smith introduced TailorTemp, a fiber-based thermal shipper offering 36-hour cool retention and 40% CO₂ cuts versus EPS.

Global Anti-Microbial Paper Packaging Market Report Scope

| Boxes and Cartons |

| Bags and Pouches |

| Wraps and Sheets |

| Trays and Clamshells |

| Labels and Linings |

| Food and Beverage | Meat, Poultry and Seafood |

| Bakery and Confectionery | |

| Fresh Produce | |

| Healthcare and Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Industrial and Institutional |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Format | Boxes and Cartons | ||

| Bags and Pouches | |||

| Wraps and Sheets | |||

| Trays and Clamshells | |||

| Labels and Linings | |||

| By End-Use Industry | Food and Beverage | Meat, Poultry and Seafood | |

| Bakery and Confectionery | |||

| Fresh Produce | |||

| Healthcare and Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Industrial and Institutional | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the anti-microbial paper packaging market in 2030?

The anti-microbial paper packaging market is projected to reach USD 13.87 billion by 2030, rising at a 5.44% CAGR.

Which region is growing fastest in anti-microbial paper packaging?

Asia-Pacific is the fastest-growing region, anticipated to post an 8.96% CAGR through 2030 due to updated food-contact regulations and e-commerce meal expansion.

Why are trays and clamshells expanding quicker than boxes and cartons?

Trays and clamshells align with ready-meal and online grocery formats, where longer distribution cycles make antimicrobial protection and rigid structure critical, driving an 11.81% CAGR.

How are regulations influencing adoption?

Policies banning PFAS and pushing fiber-based, recyclable designs create a dual need for sustainability and pathogen control, accelerating the switch from plastic to antimicrobial paper solutions.

What challenges limit broader uptake of antimicrobial paper packaging?

Premium coating costs and lengthy safety approvals add complexity and expense, especially for smaller converters and cost-sensitive food segments.

Page last updated on: